Middle East and Africa Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

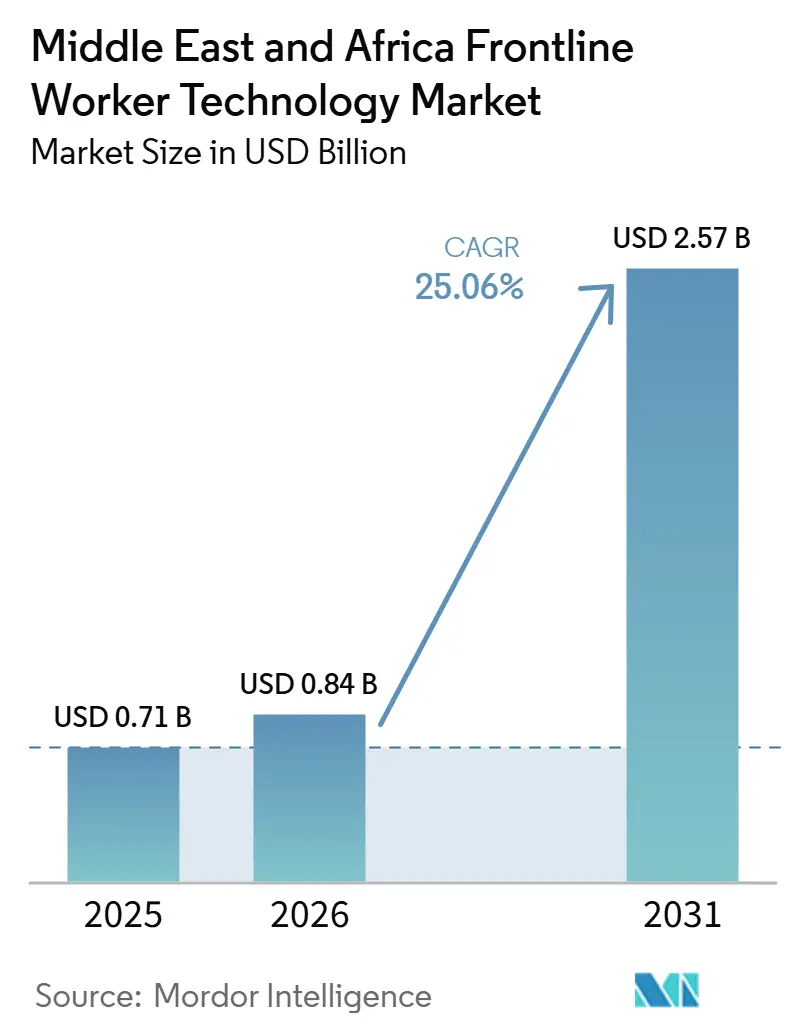

| Base Year Market Size (2025) | USD 0.71 Billion |

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 25.06% CAGR |

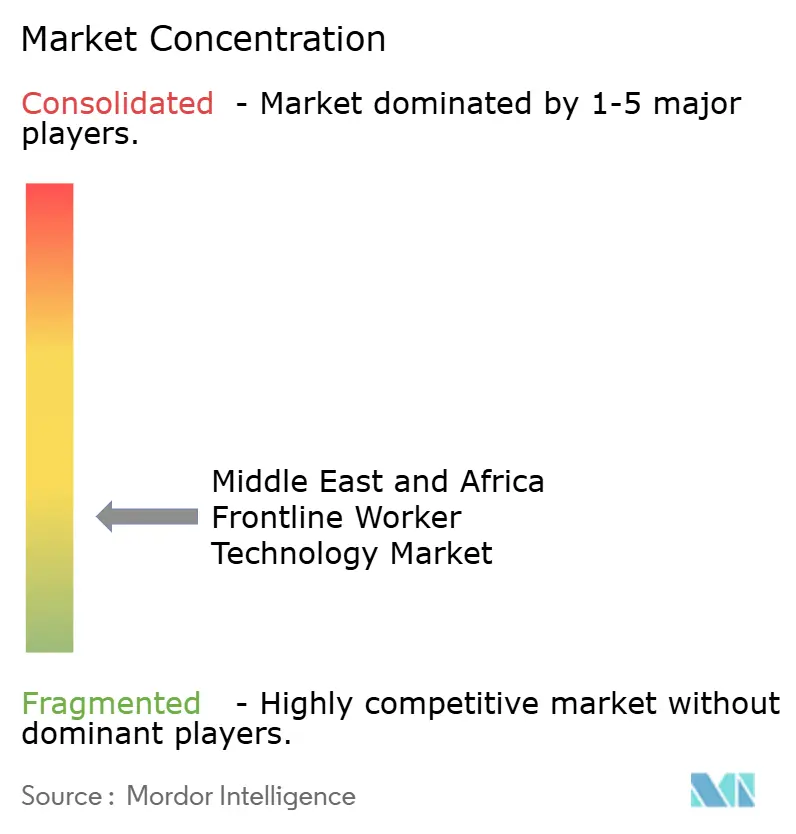

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Frontline Worker Technology Market Analysis by Mordor Intelligence

The Middle East and Africa frontline worker technology market size is projected to expand from USD 0.71 billion in 2025 and USD 0.84 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 25.06% between 2026 and 2031. The Middle East and Africa frontline worker technology market is advancing as sovereign digital programs, wage protection rules, and field-level compliance requirements are driving employers to replace paper processes with mobile systems. Large project pipelines in Saudi Arabia and the UAE are making digital attendance, workflow tracking, and safety reporting part of normal operating practice for contractors and subcontractors. The vendor field remains broad, with global platform providers competing for enterprise contracts while regional specialists focus on Arabic interfaces, blue-collar HR needs, and local compliance workflows. The Middle East and Africa frontline worker technology market is also gaining support from cloud delivery, AI-enabled task execution, and growing demand for real-time worker visibility across construction, logistics, and industrial operations. Cost barriers to rugged deployments and integration gaps with older HR, ERP, and EHS systems still slow adoption, but SME demand is expanding the addressable base as SaaS pricing and bring-your-own-device models reduce entry barriers.

Key Report Takeaways

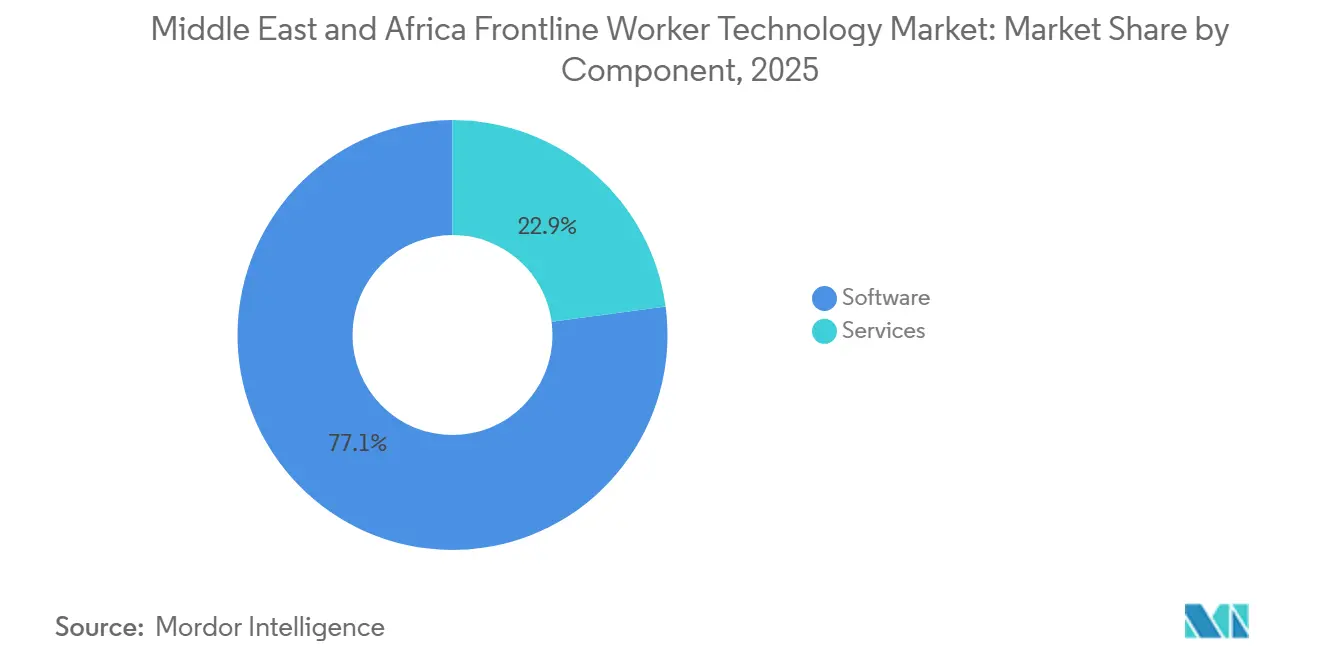

- By component, software held 77.11% of the Middle East and Africa frontline worker technology market in 2025, while services are projected to expand at a 26.11% CAGR through 2031.

- By deployment mode, cloud-based deployment held 69.66% share in 2025 and is projected to record the fastest CAGR at 27.44% through 2031.

- By organization size, large enterprises held 68.66% of the Middle East and Africa frontline worker technology market share in 2025, while SMEs are projected to grow at the highest CAGR of 28.86% through 2031.

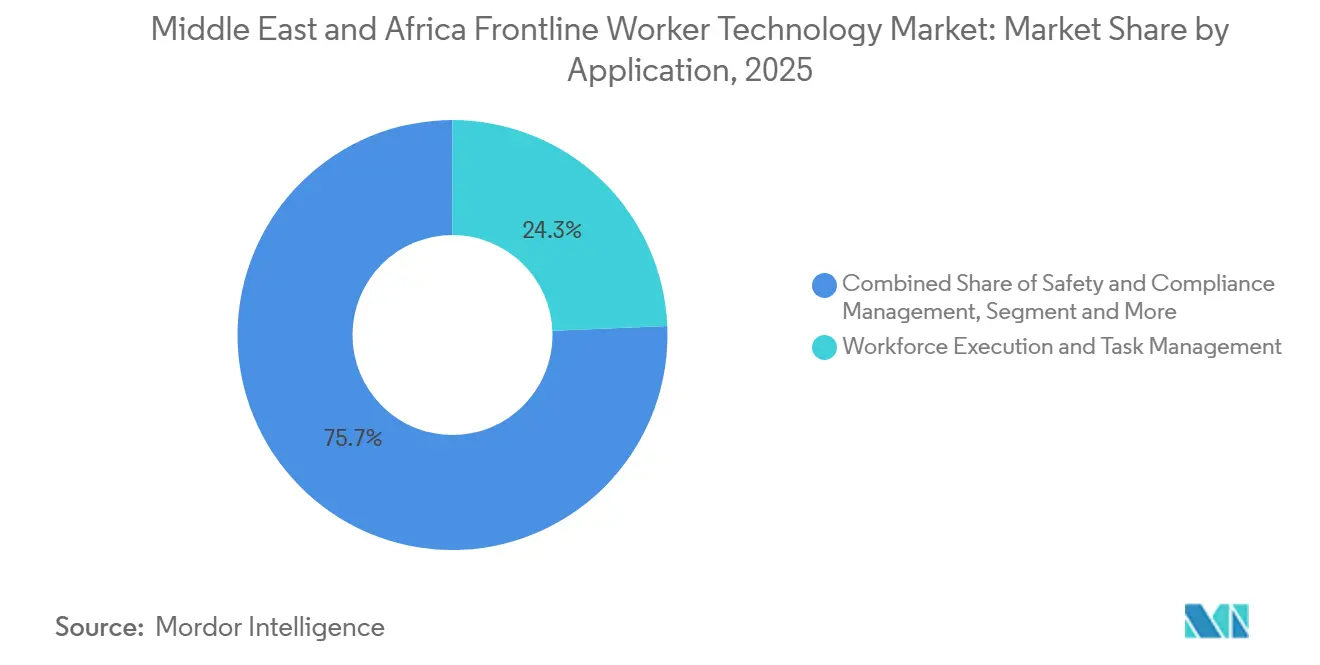

- By application, workforce execution and task management accounted for 24.33% share of the Middle East and Africa frontline worker technology market size in 2025, while safety and compliance management is projected to expand at a 29.31% CAGR through 2031.

- By end-user industry, construction led with 24.99% share in 2025, while transportation and logistics are projected to advance at a 31.19% CAGR through 2031.

- By geography, the Middle East held 65.12% share in 2025, while Africa is projected to expand at a 32.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-First Digitization Of Deskless Workflows | +7.5% | Global, concentrated gains in Middle East | Short term (≤ 2 years) |

| Rising Worker Safety Compliance In High-Risk Sites | +6.0% | Gulf states, particularly Saudi Arabia and UAE | Medium term (2-4 years) |

| Expansion Of Ruggedized Enterprise Mobility In Industrial Operations | +4.2% | Global, industrial hubs across Middle East and Africa | Medium term (2-4 years) |

| Growth Of Real-Time Workforce Visibility And Dispatching | +3.8% | Global, with accelerated uptake in Africa | Short term (≤ 2 years) |

| Demand For Offline-Capable Applications In Connectivity-Constrained Sites | +2.5% | Africa core, Middle East remote and subsurface sites | Long term (≥ 4 years) |

| Adoption Of Wearable And Voice-Enabled Hands-Free Productivity Tools | +2.0% | Global, early adoption in Gulf industrial sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-First Digitization of Deskless Workflows

The shift from paper instructions and verbal supervision to mobile workflows remains the strongest force behind demand in the Middle East and Africa frontline worker technology market. Rockwell Automation's 2026 survey showed that 98% of manufacturers in Saudi Arabia and the UAE viewed digital transformation as essential, and 40% of employees were in reskilling programs, up from 30% a year earlier.[1]Rockwell Automation, “Middle East Manufacturers Lead in Industrial AI, State of Smart Manufacturing 2026,” Rockwell Automation, rockwellautomation.com This shows that digitization is moving beyond core systems and into the daily execution layer used by frontline teams. Mashreq's 2025 rollout of SAP Fieldglass across contingent worker management, services procurement, and staffing management also showed that highly regulated employers are digitizing workforce processes that sit close to field operations. As a result, vendors that can deploy mobile tools quickly in Arabic and across many subcontractor locations are in a stronger position in the Middle East and Africa frontline worker technology market.

Rising Worker Safety Compliance in High-Risk Sites

Safety compliance has become a direct demand driver, as site operators now need auditable digital records rather than manual reporting in many high-risk environments. The UAE Ministry of Human Resources and Emiratisation introduced its Smart Safety Tracker at GITEX Global 2025, using generative AI to support occupational health and safety monitoring across work sites.[2]UAE Ministry of Human Resources and Emiratisation, “MoHRE Unveils Smart Safety Tracker at GITEX Global 2025 to Enhance Occupational Health and Safety,” UAE Ministry of Human Resources and Emiratisation, mohre.gov.ae This matters because public-sector adoption raises the compliance standard for private employers that serve regulated sectors or public projects. The same pressure is lifting interest in safety and compliance platforms across construction, industrial, and infrastructure sites where reporting speed and data quality now carry commercial consequences. In the Middle East and Africa frontline worker technology market, this has pushed safety workflows closer to core operating systems rather than keeping them as separate administrative tools.[3]Al Bayan, “Mashreq Enhances Smart Employee Management With Advanced Digital Solutions,” Al Bayan, albayan.ae

Expansion of Ruggedized Enterprise Mobility in Industrial Operations

Industrial sites across the region still need devices that can withstand dust, heat, vibration, and long operating cycles, which supports demand for rugged mobility. The broader supplier ecosystem has expanded, as TechBridge Distribution MEA was appointed in 2025 to distribute Honeywell enterprise mobility products across the region for logistics, manufacturing, healthcare, and field services users. That wider channel reach makes it easier for enterprises to pair device procurement with barcode, printing, and worker productivity workflows in one buying cycle. Rugged hardware also tends to pull software selection in the same direction, as device management, workflow orchestration, and support services work better when they sit within a shared ecosystem. This provides industrial modernization with another layer of support in the Middle East and Africa frontline worker technology market.

Growth of Real-Time Workforce Visibility and Dispatching

Real-time visibility has become increasingly important as project owners and operators want to know where workers are, what they are doing, and whether tasks are progressing on schedule. Rawasi AI has positioned its construction intelligence platform in Saudi Arabia around connected workers, contractors, assets, IoT feeds, and executive dashboards built for large project environments.[4]Rawasi AI, “Rawasi AI, Smart Construction Operations Platform for Saudi Arabia and the GCC,” Rawasi AI, rawasiai.com This kind of operating model suits a region where the same contractor base often works across multiple sites and needs a single view of labor, tasks, and exceptions. It also supports more robust dispatching in African freight and logistics networks, where fragmented operations create avoidable delays. In the Middle East and Africa frontline worker technology market, visibility tools are therefore moving from site supervision aids to broader coordination platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership For Ruggedized Deployments | -4.2% | Global, particularly acute in African markets | Medium term (2-4 years) |

| Interoperability Gaps Across Legacy HR, EHS, and Field Systems | -3.5% | Global | Medium term (2-4 years) |

| Uneven Digital Infrastructure Across Secondary Cities and Remote Sites | -2.8% | Africa primarily, Middle East remote industrial sites | Long term (≥ 4 years) |

| Data Sovereignty and Device Governance Complexity | -1.8% | Middle East government sector, global data residency pressures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Ruggedized Deployments

The cost of rugged devices, device management, data plans, accessories, and support remains a real barrier for smaller buyers. This challenge is sharper in African markets where many employers still manage field mobility with tight budgets and long replacement cycles. The issue is not only the upfront device bill, because recurring connectivity and support costs can also limit actual usage across a workforce. Vendors are responding with SaaS pricing and bring-your-own-device options, but those models do not fully solve use cases that require industrial-grade hardware. The Middle East and Africa frontline worker technology market, therefore, continues to split between better-funded enterprise buyers and price-sensitive adopters that move more slowly.

Interoperability Gaps Across Legacy HR, EHS, And Field Systems

Integration remains difficult because many large employers still run older HR, finance, payroll, and compliance systems that were not built for easy data exchange. Rockwell Automation reported in 2026 that only 41% of Middle East manufacturers were effectively using their operational data, indicating persistent silos between plant-level tools and enterprise systems. This slows rollout timelines and raises implementation costs when companies try to connect frontline workflows with payroll, EHS reporting, or planning systems. The burden can be higher in African markets where payroll practices and HR tools are often less standardized across sites. For the Middle East and Africa frontline worker technology market, these gaps favor vendors that can reduce customization work and make integration easier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Revenue While Services Build Faster

Software held 77.11% of the Middle East and Africa frontline worker technology market in 2025, confirming that subscription licensing and SaaS delivery remain the main revenue drivers. This lead reflects the practical value of applications that can be deployed onto existing devices without large hardware investment. In many field settings, buyers first choose workflow, communication, and compliance software because these tools deliver visible operational improvements in a short period. That pattern keeps software at the center of the Middle East and Africa frontline worker technology industry as employers replace manual routines with mobile execution systems.

Services are projected to record the fastest growth, with a 26.11% CAGR through 2031, as implementation and localization needs rise. More buyers now need Arabic-language setup, multi-site deployment support, integration with payroll and EHS systems, and managed adoption services. Firstup said in 2026 that a commissioned Forrester study found 398% return on investment over 3 years from its workforce communications platform, which shows why vendors are attaching analytics and managed support to the base subscription. As the Middle East and Africa frontline worker technology market matures, service depth is becoming increasingly important, as customers seek measurable adoption and stronger post-deployment performance.

By Deployment Mode: Cloud Holds The Lead As Hybrid Use Expands

Cloud-based deployment held a 69.66% share in 2025, making it the largest share of the Middle East and Africa frontline worker technology market. This reflects the need for faster rollout, lower infrastructure burden, and easier updates across distributed workforces. Cloud delivery also fits wage protection and payroll-linked workflows that depend on system connectivity rather than isolated site-level installations. The Middle East and Africa frontline worker technology market has therefore moved toward cloud as the default option for most new projects.

Cloud is also projected to post the fastest CAGR of 27.44% through 2031, indicating its lead is still widening. At the same time, hybrid models are gaining support in accounts that need local control over sensitive workforce records or specific hosting requirements. Cority launched its CorityOne EHS platform in Saudi Arabia on Google Cloud's Dammam region in 2024 to meet local data-residency requirements, demonstrating how vendors are adapting their infrastructure to regional compliance expectations. On-premises models remain in the mix for some public and tightly controlled environments, but their role is narrowing as the Middle East and Africa frontline worker technology industry moves to more flexible delivery models.

By Organization Size: Large Enterprises Dominate While SMEs Gain Momentum

Large enterprises accounted for 68.66% of the Middle East and Africa frontline worker technology market share in 2025, which reflects stronger budgets and the scale of multinational contractors, industrial groups, and major retailers. These organizations manage large labor pools, multiple sites, and layered compliance needs, making it easier for them to justify enterprise-wide platform purchases. They also have more pressure to standardize attendance, task execution, safety reporting, and contractor oversight across locations. That keeps large accounts at the center of the Middle East and Africa frontline worker technology market.

SMEs are projected to grow at a 28.86% CAGR through 2031, making them the fastest-expanding buyer group. Their adoption is improving because SaaS pricing, bring-your-own-device support, and mobile-first design reduce the cost and complexity of entry. Cairo-based Bluworks raised a USD 1 million seed round in 2025 to build blue-collar workforce tools for Egyptian and wider MENA SMEs, indicating a real commercial opportunity at the smaller-business tier. This shift matters because the Middle East and Africa frontline worker technology market is no longer dependent only on top-tier enterprise spending.

By Application: Task Management Leads Scale While Safety Compliance Accelerates

Workforce execution and task management accounted for 24.33% of the Middle East and Africa frontline worker technology market in 2025, making it the anchor application across the platform stack. Companies often start here because task tools are easier to deploy and can quickly replace paper checklists, verbal handoffs, and manual follow-up. This also creates a foundation for later modules such as communication, scheduling, analytics, and learning. The Middle East and Africa frontline worker technology market continues to use task management as the first entry point in many deployments.

Safety and compliance management is projected to advance at 29.31% CAGR through 2031, making it the fastest-growing application area. WorkJam's 2026 release integrated AI directly into frontline task workflows to enforce standard operating procedures, flag exceptions, and support issue resolution, demonstrating how task and compliance workflows are converging. Axonify launched Checkpoint in 2026 to turn paper audits, inspections, and walkthroughs into AI-powered workflows that automatically create corrective actions. As compliance pressure rises, the Middle East and Africa frontline worker technology market is pulling audit, inspection, and corrective-action workflows into the same systems that manage daily execution.

By End-User Industry: Construction Holds The Base While Logistics Advances Faster

Construction accounted for 24.99% of the Middle East and Africa frontline worker technology market in 2025, which made it the largest end-user segment. This lead comes from the scale of active project work and the strong need for attendance tracking, site safety reporting, labor coordination, and contractor management. Construction buyers also tend to need multi-site deployment and rapid worker onboarding, which supports broad platform usage. That keeps construction at the core of the Middle East and Africa frontline worker technology market.

Transportation and logistics are projected to grow at a 31.19% CAGR through 2031, making it the fastest-growing end-user industry. Real-time dispatch, scheduling, shipment visibility, and driver workflow control are becoming more important as operators try to improve service quality across fragmented networks. GIG Logistics Technologies expanded the use of its GIGGo app in 2026 to support real-time shipment tracking and scheduling across a large service center network in Nigeria. Dangote Cement also deployed AI and telematics in 2026 to strengthen transport safety and driver management, showing how logistics-focused operating tools are spreading beyond pure freight firms.

Geography Analysis

The Middle East accounted for 65.12% of the Middle East and Africa frontline worker technology market share in 2025, making it the largest regional block. Saudi Arabia and the UAE led this position because digital transformation mandates, large project pipelines, and workforce compliance needs are stronger and more formalized there. The market in this subregion benefits from a contractor ecosystem that increasingly expects digital attendance, workflow control, and site-level safety visibility as part of normal execution. That creates a pull effect in which large buyers influence smaller contractors to adopt the same operating systems. The Middle East, therefore, remains the revenue anchor of the Middle East and Africa frontline worker technology market.

Within that Middle East lead, the UAE has added a clear policy signal around digital safety oversight. The Ministry of Human Resources and Emiratisation introduced its Smart Safety Tracker in 2025, which showed direct government support for AI-enabled occupational health and safety monitoring. Employers in the UAE are therefore operating in an environment where compliance systems need to be timely, digital, and easier to audit. This strengthens demand for platforms that can combine communication, tasking, and safety records in one environment.

Africa is projected to expand at a 32.64% CAGR through 2031, giving it the fastest growth rate in the Middle East and Africa frontline worker technology market. South Africa remains the strongest base because large retail, mining, logistics, and manufacturing employers have already shown wider deployment readiness. YOOBIC rolled out its platform with Shoprite in 2025 across more than 3,600 stores, which illustrated the scale at which large African employers are standardizing frontline operations tools. Nigeria and Egypt are adding another layer of growth through logistics digitization, blue-collar workforce platforms, and health workforce tools. PATH also launched a 2025 trial in Nigeria for a voice-based hotline that connects rural health workers to generative AI support, demonstrating how offline, voice-led models can extend digitization into lower-connectivity environments. This gives Africa a wider mix of growth drivers than simple smartphone adoption alone.

Competitive Landscape

The Middle East and Africa frontline worker technology market remains fragmented, with global platforms competing for major enterprise contracts while local and regional firms address narrower operating gaps. Multilingual workforce needs, local compliance rules, and the practical demands of deskless work in construction, logistics, retail, healthcare, and industrial settings shape competition. Large vendors are expanding their footprints by combining communication, workflow, analytics, and compliance features into a single platform. Regional specialists, in contrast, gain relevance when they offer Arabic-first interfaces, lower-cost deployment, and tighter alignment with local blue-collar workflows. This keeps the Middle East and Africa frontline worker technology market open to both scale players and niche challengers.

One major strategic move came in July 2025 when LumApps and Beekeeper agreed to merge, creating an AI-powered employee hub valued at more than USD 1 billion and serving more than 7 million users across 2,000 clients. Another came when Beekeeper launched Maia in 2025, a multilingual AI assistant built for frontline teams, demonstrating that language support is becoming a competitive lever rather than a secondary product feature. WorkJam also strengthened its position in 2026 by embedding AI more deeply into frontline task workflows and highlighting its enterprise certification stack, including ISO 27001 and SOC II Type 2. These moves show that vendors are no longer competing solely on messaging or scheduling.

Another visible pattern is the push toward deeper platform capabilities in worker execution and enterprise integration. Workvivo introduced Workvivo HQ in 2026 as an AI-native digital headquarters that brings communication, knowledge, and action workflows together across frontline and office users. YOOBIC's Shoprite deployment demonstrated how large-scale retail operators in Africa are standardizing on task management, communications, and employee engagement through a single operating layer. The strongest white-space opportunities still sit below the top enterprise tier, especially in affordable contractor tools, Arabic-native safety workflows, and SME-focused blue-collar HR platforms. That is why the Middle East and Africa frontline worker technology market still leaves room for new entrants, even as larger vendors broaden their suites and pursue deeper enterprise relationships.

Middle East and Africa Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Datalogic S.p.A.

ProGlove GmbH

Sonim Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Workvivo (by Zoom) launched Workvivo HQ, an AI-native digital headquarters that unifies communication, knowledge management, and AI-powered action workflows for frontline and corporate employees. The platform serves over 10 million users across global brands including Amazon, Delta, and Heineken, reinforcing Workvivo's position in the enterprise frontline experience segment.

- June 2026: Zebra Technologies launched Zebra Nucleus, a unified software platform consolidating device fleet management, AI-powered operational analytics, and Workcloud workflow orchestration for frontline workers across logistics, retail, healthcare, and industrial operations in the MEA region and globally.

- June 2026: Firstup released findings from a Forrester Consulting-commissioned total economic impact study, reporting 398% return on investment over 3 years for organizations using its AI-powered workforce communications platform, with improvements in frontline retention, productivity, and workplace safety.

- March 2026: Firstup extended its platform with Firstup AI, a comprehensive agentic AI suite covering AI Search, AI Content Creator, and AI Insights, with AI Actions, enabling natural-language task execution across Workday, ServiceNow, and ADP, and AI Audience Builder planned for general availability later in 2026.

Middle East and Africa Frontline Worker Technology Market Report Scope

The Middle East and Africa frontline worker technology market refers to the ecosystem of software and services designed to empower non-desk employees, who primarily execute their duties away from a traditional office setting. This includes tools that facilitate communication, task management, scheduling, knowledge sharing, and performance tracking for workers in sectors such as retail, manufacturing, healthcare, and logistics across the MEA region. The market encompasses cloud-based, on-premises, and hybrid deployment models tailored to the operational, connectivity, and security needs of organizations of varying sizes, from small and medium enterprises to large corporations. Key applications include workforce scheduling and coordination, safety and compliance management, and learning enablement, all aimed at improving operational efficiency, employee engagement, and real-time decision-making at the edge of business operations.

The Middle East and Africa Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries), and Geography (Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Employee Communication and Engagement | |

| Workforce Execution and Task Management | ||

| Workforce Scheduling and Coordination | ||

| Learning and Knowledge Enablement | ||

| Workforce Analytics and Performance Management | ||

| Safety and Compliance Management | ||

| Other Applications | ||

| By End-User Industry | Retail and E-Commerce | |

| Industrial Manufacturing | ||

| Healthcare and Life Sciences | ||

| Transportation and Logistics | ||

| Hospitality | ||

| Construction | ||

| Government and Public Administration | ||

| Other Industries | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the Middle East and Africa frontline worker technology market?

The Middle East and Africa frontline worker technology market stood at USD 0.84 billion in 2026 and is forecast to reach USD 2.57 billion by 2031 at a 25.06% CAGR.

Which component leads revenue in frontline worker technology across the Middle East and Africa?

Software led with 77.11% share in 2025, showing that SaaS and subscription-based applications remain the main revenue engine.

What is driving faster adoption across this space in the Middle East and Africa?

Mobile-first workflow digitization, stronger safety compliance needs, cloud rollout, and demand for real-time workforce visibility are the main factors supporting adoption.

Which application area is growing the fastest?

Safety and compliance management is projected to post the highest CAGR at 29.31% through 2031, ahead of other application areas.

Why does the Middle East lead while Africa grows faster?

The Middle East led with 65.12% share in 2025 because of stronger compliance systems and large project activity, while Africa is projected to grow faster at 32.64% CAGR as adoption broadens across retail, logistics, and health workforce use cases.

Which end-user group offers the strongest growth opportunity?

Transportation and logistics is projected to grow the fastest at 31.19% CAGR through 2031, supported by rising demand for dispatching, scheduling, and real-time worker coordination.

Page last updated on: