Middle East and Africa Football Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

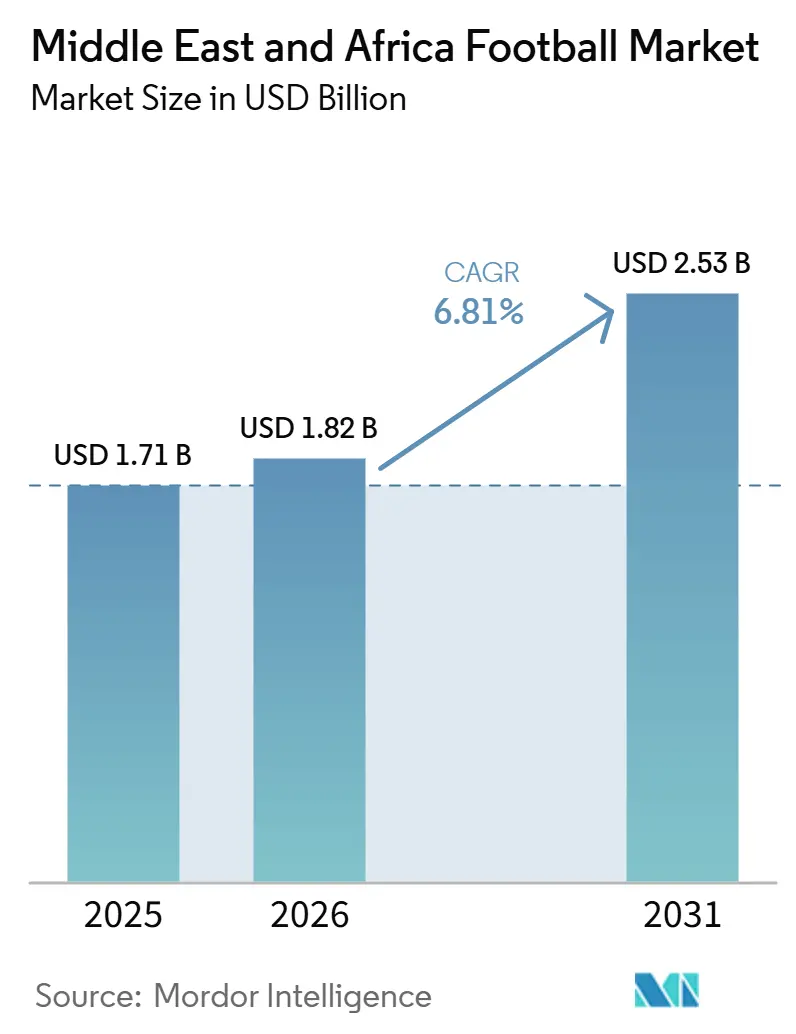

| Base Year Market Size (2025) | USD 1.71 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

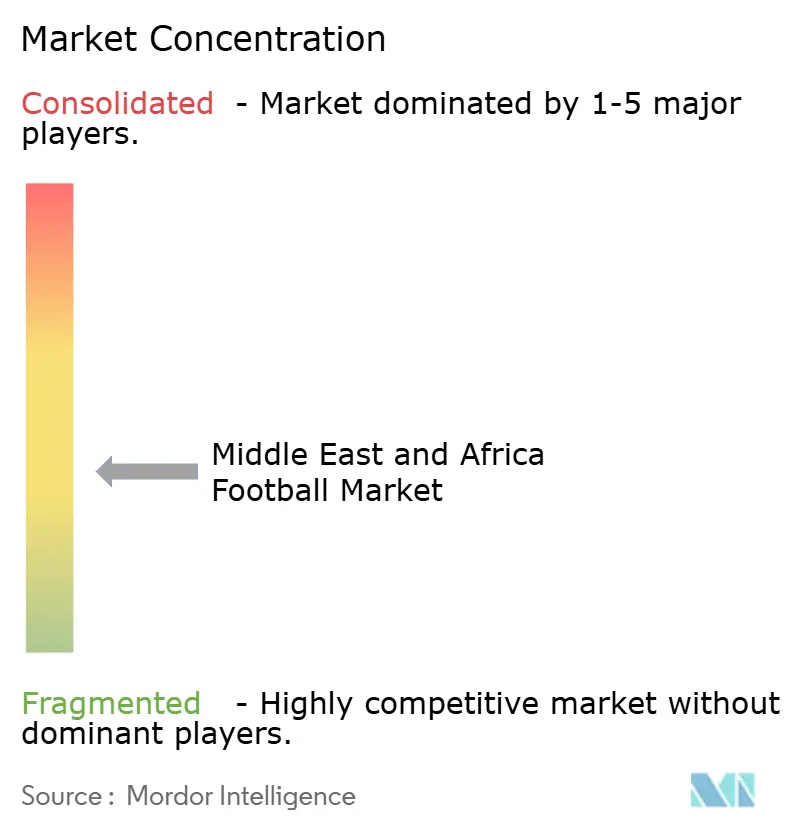

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Football Market Analysis by Mordor Intelligence

The Middle East and Africa football market size is projected to grow from USD 1.71 billion in 2025 and USD 1.82 billion in 2026 to USD 2.53 billion by 2031, registering a CAGR of 6.81% during 2026-2031. Football remains the most established participatory sport across the region, while state-backed league development and the broader formalization of women’s competitions continue to strengthen demand. The broader sports goods landscape also remains favorable, with the World Economic Forum identifying Africa and the Middle East as among the fastest-growing sports consumption zones over the next decade[1]Source: World Economic Forum Staff, “Sports for People and Planet,” World Economic Forum, weforum.org. Commercial demand in the Middle East and Africa football market is becoming more structured as privatized clubs, academies, and federations replace equipment through planned procurement cycles rather than ad hoc purchases. The market is also benefiting from stronger acceptance of premium products, rising digital retail activity, and investments in training infrastructure that support demand for higher-value equipment. However, counterfeit products, import costs, and weaker affordability in lower-income countries continue to limit formal sales. As a result, the strongest gains remain concentrated in markets with better regulation, stronger club systems, and deeper retail networks.

Key Report Takeaways

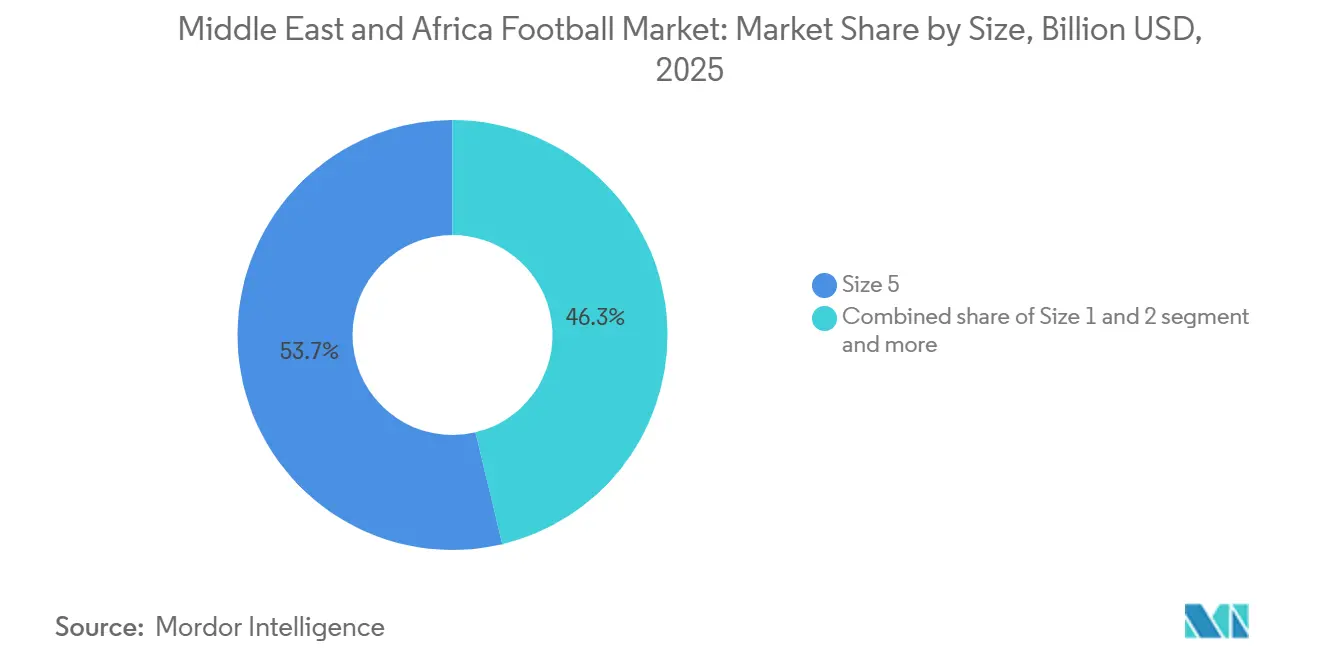

- By size, Size 5 led with a 53.71% revenue share in 2025, while Size 1 and Size 2 are projected to expand at the fastest pace with a 7.96% CAGR through 2031.

- By category, Mass footballs accounted for 71.79% of revenue in 2025, while the Premium category is forecast to grow at a 7.81% CAGR through 2031.

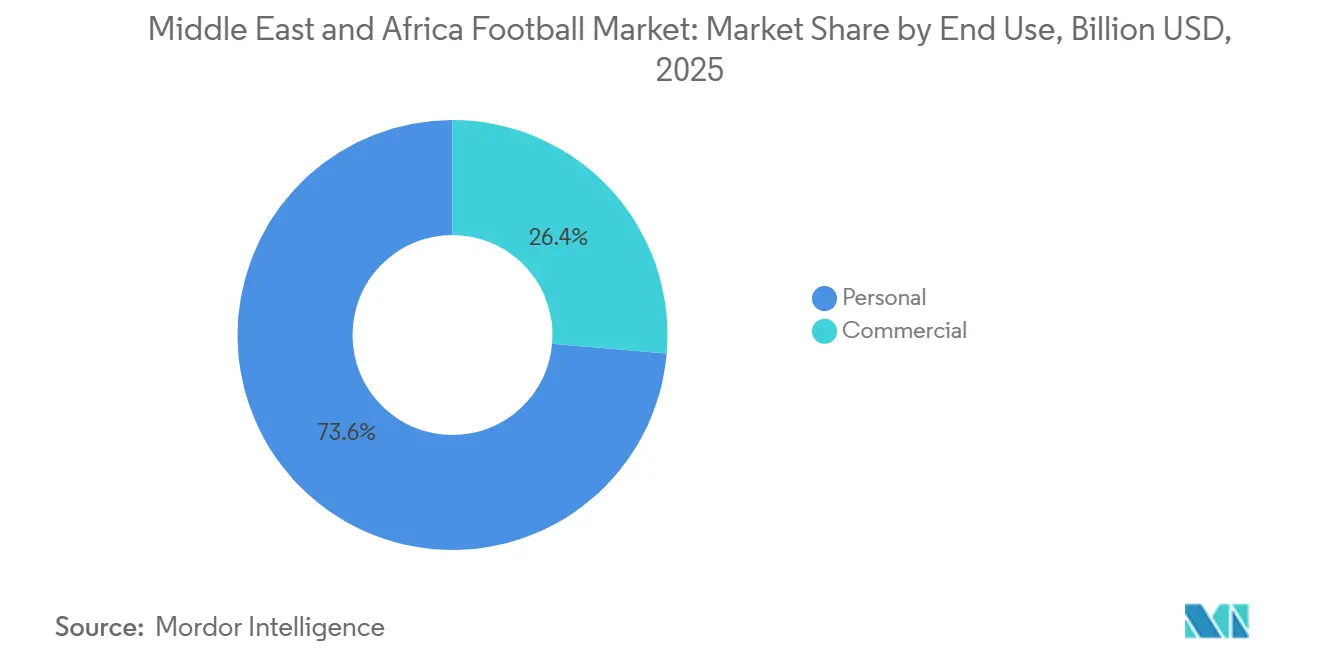

- By end use, Personal purchases represented 73.62% of revenue in 2025, while Commercial demand is expected to advance at an 8.42% CAGR through 2031.

- By distribution channel, Offline Stores captured 83.62% of revenue in 2025, while Online Stores are projected to grow fastest at an 8.93% CAGR through 2031.

- By geography, Saudi Arabia held the largest share at 29.13% in 2025, while the United Arab Emirates is forecast to record the fastest growth at an 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Football Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising organized football participation in youth and school programs | +2.1% | Global, concentrated gains in Saudi Arabia, Nigeria, Morocco, Egypt | Medium term (2–4 years) |

| Premiumization of match balls and training balls | +1.2% | GCC core, spill-over to South Africa and Egypt | Medium term (2–4 years) |

| Expansion of professional leagues, federations, and event-led spending | +1.3% | Saudi Arabia, United Arab Emirates, Qatar, and early spill-over to Kenya, Nigeria | Long term (≥4 years) |

| E-commerce and direct-to-consumer access for branded football products | +1.0% | North America and Europe equivalents; the United Arab Emirates, Saudi Arabia, leading MENA | Short term (≤2 years) |

| Women’s football commercialization and grassroots investment | +0.6% | Nigeria, Uganda, Saudi Arabia, South Africa, Morocco | Long term (≥4 years) |

| Data-enabled training demand for smart and sensor-ready balls | +0.4% | The United Arab Emirates, Qatar, Saudi Arabia, core; emerging in South Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising organized football participation in youth and school programs

CAF's African Schools Football Championship has mobilized more than 1.965 million boys and girls across 46 countries since its inception, making it the continent's most successful youth sports mobilization initiative[2]Source: CAF Staff, “African Schools Football Championship,” CAF, cafonline.com. However, the headline figure reflects a more commercially significant shift: grassroots programs now create structured demand for equipment, as affiliated leagues increasingly require participants to use certified balls instead of informal substitutes. The FIFA Quality Program, which governs FIFA Basic, FIFA Quality, and FIFA Quality Pro certifications, provides a compliance framework that local federations increasingly reference when procuring matchday equipment. This framework directly increases average selling prices and legitimizes branded product channels at the grassroots level. Morocco's historic U-20 2025 FIFA World Cup win is expected to strengthen public confidence in the continent's football ecosystem and drive measurable near-term increases in academy enrollments and equipment purchases across West and North Africa. The FIFA World Cup 2026 is also expected to feature 10 MENA nations, marking the region's highest proportional representation on record and sustaining consumer interest at an elevated level.

Expansion of professional leagues, federations, and event-led spending

Saudi Arabia's Ministry of Sport completed transactions involving 11 football clubs and plans to offer additional clubs to investors “within months,” supported by Saudi Arabia's role as host of the FIFA 2034 World Cup. The second phase of the Saudi Pro League's PACE (Player Acquisition Center of Excellence) program, scheduled for launch in May 2026, will regulate club spending based on sporting performance, television viewership, and commercial success metrics. This shift indicates that the league is increasingly prioritizing commercial viability over owner-funded spectacle alone. Each newly privatized club functions not only as a broadcasting asset but also as a procurement entity for kits, training balls, and coaching equipment under commercial governance disciplines. This structural shift is the primary reason the Commercial end-use segment is expected to record a higher forecast growth rate than the Personal segment, as clubs with institutionalized budgeting cycles replace equipment systematically rather than individually. Beyond Saudi Arabia, the Rwanda Premier League's three-year deal with Nigeria's ProStar Sports International, set to take effect in January 2026, shows how league formalization directly creates certified match-ball supply contracts across Sub-Saharan Africa.

Women’s football commercialization and grassroots investment

Nigeria's National Women's Football League secured a 10-year, NGN 20 billion partnership (~USD 12.5 million at 2025 average exchange rates) with Toptier Sports Management, marking the largest private-sector commitment to women's football in Sub-Saharan Africa[3]Source: Independent Nigeria Staff, “NWFL 10-Year Partnership Announcement,” Independent Nigeria, independent.ng. The partnership targets full club licensing compliance and 2.5 million media impressions. CAF also doubled the prize money for the WAFCON 2025 winner and increased the total prize pool by 45%, signaling a structural, rather than cyclical, commitment to enhancing the commercial value of women's competitions. This shift has a less obvious implication for equipment procurement cycles. As match counts increase, fixtures become more competitive, and broadcast time expands, clubs and federations that previously purchased one set of matchday balls per season are now replacing equipment at intervals aligned with professional men's competition standards. Saudi Arabia's Women's Premier League, launched in 2022 and already attracting national broadcast coverage by 2025, is creating parallel demand in a historically untapped consumer segment for premium football equipment. Uganda and Romania are also serving as FIFA pilot markets for structured commercialization strategies for women's football, creating a replicable model that other African federations are already benchmarking.

E-commerce and direct-to-consumer access for branded football products

The MENA e-commerce market recorded an increase of more than 30% in online orders in 2024, while the regional Average Order Value rose from USD 30 in 2023 to USD 35.6 in 2024. The UAE’s AOV increased to USD 102, and Saudi Arabia’s reached USD 52.5. Online Stores represent the fastest-growing distribution channel in the MEA football market, with an 8.93% CAGR through 2031, aligning with the projected growth in MENA’s e-commerce retail penetration. For the football market, this shift has a second-order implication: a change in channel margins. Direct-to-consumer platforms enable brands to price premium SKUs closer to their European retail equivalents, while Offline Stores in price-sensitive markets often rely on promotional pricing, which compresses brand margins. Offline Stores retain the largest share, at 83.62% in 2025, reflecting consumers’ preference to physically assess equipment before purchase. However, the online channel’s faster growth is expected to materially narrow this gap over the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity in lower-income African markets | -1.2% | Sub-Saharan Africa core, including Nigeria, Ghana, Kenya, Tanzania | Long term (≥4 years) |

| Counterfeit and unbranded product leakage in informal retail | -0.9% | Nigeria, South Africa, Kenya, Ghana, Cameroon | Long term (≥4 years) |

| Import dependence and FX volatility affecting brand pricing | -0.7% | Sub-Saharan Africa broadly; East African Community, Economic and Monetary Community of Central Africa, Nigeria | Medium term (2–4 years) |

| Heat, surface wear, and short product replacement cycles in harsh climates | -0.4% | GCC countries, Sahel belt, North Africa | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Price sensitivity in lower-income African markets

African markets face a compounding challenge, as high prices for authentic products push consumers into a large counterfeit ecosystem. Nigerian customs officials seized approximately 180,000 counterfeit jerseys valued at more than USD 4 million in the 12 months preceding the most recent FIFA World Cup qualification cycle, and seizures of this scale represent only a fraction of the total contraband entering African markets. Cameroon Customs is expected to launch a dedicated anti-counterfeiting campaign in April 2025 in partnership with FECAFOOT, with an August 2025 operation projected to seize nearly 3,500 counterfeit kits. A significant price gap remains the key structural driver, and formal-channel brands cannot easily close it. In Ghana, official replica jerseys retail at approximately GHS 1,200, while counterfeits sell for as little as GHS 100. This price differential pushes most mass-market buyers toward unbranded alternatives, regardless of quality considerations. Regulatory measures, including national customs cooperation agreements modeled on Cameroon’s FECAFOOT arrangement and the AfCFTA’s phased tariff harmonization, currently at 4% for qualifying African-origin goods, offer a compliance framework that could gradually shift purchases toward formally certified products.

Import dependence and FX volatility affecting brand pricing

Football equipment manufactured outside origin countries faces a layered duty structure that materially increases landed costs across the MEA region. South Africa applies a 40–45% customs duty on finished clothing and apparel. The EAC Common External Tariff imposes a 25% duty on finished consumer goods across Kenya, Tanzania, Uganda, and Rwanda, while Kenya adds a 2.5% Import Declaration Fee and a 2% Railway Development Levy. From January 2025, GCC nations will mandate a 12-digit Harmonized System code for sports supplies, increasing documentation and compliance costs for importers serving the Gulf market. The market response is notable, as local manufacturers are emerging as cost-effective alternatives to imports. These include Tanzania's Justfit, which is expected to supply the Tanzanian Premier League in 2025; Nigeria's Owu Sportswear, which will kit three NPFL clubs for 2025/26 continental and domestic competitions; and Nigeria's ProStar, which signed the Rwanda Premier League ball contract. The AfCFTA preferential tariff corridor could materially rebalance import economics once more comprehensively implemented. However, implementation gaps across 54 signatory states remain the key uncertainty affecting the timeline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size: Match-Grade Demand Drives Value, Youth Programmes Accelerate Volume

Size 5 balls are expected to account for 53.71% of the MEA football market in 2025, reflecting the segment’s dominance as the standard format for adult match and training applications. This concentration is proportionally higher in the MEA market than in global markets, as the region’s professional league formalization, driven by Saudi Pro League privatization and CAF competition structures, creates recurring institutional replacement cycles for full-size match balls that meet FIFA Quality Pro standards. Size 1 and Size 2 balls are projected to record the fastest CAGR of 7.96% through 2031, supported by the rapid proliferation of skill-development programs, fan merchandise positioning at tournament events, and street soccer initiatives. Nike’s “Toma” franchise, which promotes street soccer in urban environments, positions this format as both a training and lifestyle product.

PUMA’s ITRI ball, unveiled as the official match ball for AFCON 2025 in November 2025 and built on Orbita 6 technology with thermally bonded panels for precision, stability, and durability, was commercially priced at EUR 130 in African markets, establishing a visible benchmark for the premium Size 5 segment. Size 3 and Size 4 balls serve intermediate training and youth league applications and are expected to maintain stable mid-range growth as grassroots programs across Nigeria, Kenya, Egypt, and Morocco expand participation pathways. Tanzania’s Justfit became the local match-ball supplier for the Tanzanian Premier League in 2025, demonstrating that the region’s domestic manufacturing base is beginning to assert technical competitiveness at a nationally sanctioned level.

By Category: Mass Preserves Share While Premium Earns Disproportionate Revenue Growth

Mass footballs are expected to account for 71.79% of category revenue in 2025, supported by volume-driven purchases across informal and grassroots leagues in Sub-Saharan Africa and the strong price sensitivity that defines large parts of the MEA consumer base. However, the premium segment is projected to grow faster, registering a CAGR of 7.81% through 2031. GCC professional clubs, school academies, and high-income consumer groups willing to pay for certified performance features are driving this growth. New Balance’s MEAI region is expected to grow by 35% in 2025, contributing to total global revenue of USD 9.2 billion. The company has identified the Middle East as a priority region for premium growth, supported by the launch of its first Grey Store concept in Doha. This development signals the rapid maturation of upscale sports retail positioning in Gulf markets.

The premium-mass dynamic varies across the MEA geography. In the GCC, premium positioning aligns with lifestyle and performance aspirations at both club and individual levels. In Sub-Saharan Africa, mass products with FIFA Basic certification increasingly represent the aspirational tier, as certified products signal a level of quality that unbranded alternatives cannot offer. Decathlon’s Kipsta brand, which has been elevated to Major Partner of the Ligue de Football Professionnel through 2032 and supplies official match balls, represents the category’s most strategically significant mid-tier positioning. It offers performance-grade products at accessible price points, challenging both premium incumbents and unbranded competition.

By End Use: Personal Volume Dominates, Commercial Systems Purchasing Accelerates

Personal end use is projected to account for 73.62% of market revenue in 2025, driven by individual consumer and informal club purchases that form the volume backbone of the MEA football market. The commercial segment is expected to record the fastest growth, at a CAGR of 8.42% through 2031, mainly as the institutional procurement model linked to professional club management expands from the Saudi Pro League to second-tier and emerging leagues across the region. The Qatar Football Association’s multi-year partnership with Iterpro to digitize operations across Qatar Stars League clubs centralizes player data, physical performance tracking, and equipment utilization on a unified platform.

This governance model indicates a shift toward formalized equipment procurement schedules. Academic and school football, as a commercial end-use sub-category, is expanding rapidly. The UAE Ministry of Sports’ accredited AI-driven Professional Diploma in Sports Management and Analysis, developed with Precision Football and using wearable technologies such as Playermaker, highlights how educational institutions are procuring specialized training equipment alongside analytical platforms. The personal segment retains considerable structural durability in Sub-Saharan Africa, where individual and neighborhood purchasing is expected to remain the primary channel until club formalization advances further.

By Distribution Channel: Offline Stores Anchor Reach, Online Stores Define Growth Trajectory

Offline Stores are projected to retain 83.62% of distribution channel revenue in 2025, with the segment’s dominance reflecting consumers’ preference for tactile purchases in sports equipment, particularly in markets where online return logistics remain underdeveloped. Online Stores are expected to record the fastest CAGR, at 8.93%, through 2031, aligning with MENA’s structural e-commerce expansion trajectory. Decathlon’s aggressive retail footprint expansion across Africa, including plans to add its fourth Ghana store in Kumasi in March 2026, renew its Ghana Football Association partnership in March 2025, and report FY2025 global GMV of EUR 20.7 billion, is expected to blur the distinction between offline and online channels, as its omnichannel model supports online discovery and offline conversion simultaneously.

JD Sports’ 10-year franchise agreement with Gulf Marketing Group (GMG), which targets approximately 50 stores in the UAE, Saudi Arabia, Kuwait, and Egypt by 2028, represents a parallel offline channel expansion that consolidates access to premium sports brands under one roof in key GCC markets. The Online Stores channel’s long-term structural advantage lies in its ability to serve the large geographic area of MEA, a market where millions of sports consumers live more than 50 km from the nearest branded sports retailer, once logistics infrastructure matures enough to support reliable delivery and returns.

Geography Analysis

Saudi Arabia is expected to capture 29.1% of the Middle East and Africa football market share in 2025, making it the largest country market in the region. The country’s leadership rests on league privatization, a broader sports participation base, and a commercial ecosystem that continues to become more structured each year. The Saudi Pro League is now broadcast in more than 180 countries, extending club visibility well beyond the domestic market and supporting demand for merchandise and equipment. Kingdom Holding’s agreement to acquire a 70% stake in Al-Hilal Club Company at an enterprise value of SAR 1.4 billion, equivalent to USD 373 million, shows that football assets in Saudi Arabia are being valued and managed on commercial terms. Adidas is also set to begin its kit partnership with Al Qadsiah on July 1, 2026, across the men’s, women’s, and academy teams, while PUMA continues to work with Al-Hilal. These developments show that the Saudi market is attracting deeper brand participation across multiple club tiers.

The United Arab Emirates is the fastest-growing geography in the Middle East and Africa football market, with a forecast CAGR of 8.6% through 2031. Investment in training quality, sports technology, and premium performance environments is driving growth more than basic participation volume. Precision Football’s Dubai facility has trained more than 7,000 athletes, attracted private investment of more than USD 10 million, and uses performance analysis tools that support demand for higher-specification football products. The UAE also plays an important role in shaping regional standards in coaching, sports management, and retail presentation through institution-backed programs. Egypt, Morocco, and South Africa remain major football consumption centers in Africa, and each is attracting renewed attention from global brands through national team and major tournament partnerships.

Nigeria, Kenya, and the rest of MEA sustain the breadth of the Middle East and Africa football market, although their maturity levels vary widely. Nigeria remains structurally important due to its population scale and strong football culture, but affordability constraints and counterfeit pressure keep formal channel revenue below its participation potential. Kenya continues to benefit from youth participation and event-led visibility, including the East Africa Cup 2025 under UNESCO’s Fit for Life initiative, which brought together more than 600 young participants from Kenya, Tanzania, and Zanzibar. Gulf markets, such as Qatar, Kuwait, Oman, and Bahrain, benefit from investment spillover from Saudi Arabia, especially in club formation and academy systems that support institutional demand. Qatar also stands out at the elite level, where football operations are becoming more closely linked with digital performance management and formal coaching tools. Across Africa, local manufacturing and intra-regional trade initiatives could gradually improve pricing and supply responsiveness, but implementation still varies by country. This dynamic gives the Middle East and Africa football market a dual geography, with Gulf countries driving premium and commercial growth and African markets providing participation depth and long-term volume potential. The strongest regional gains will likely come from markets where organized competition, professional management, and retail access improve simultaneously.

Competitive Landscape

The Middle East and Africa football market shows moderate-to-high concentration at the top end, with Nike, Adidas, and PUMA dominating elite sponsorship visibility and much of the premium branded segment. These brands hold the strongest positions in federation kits, club partnerships, and major tournament exposure, giving them a significant advantage in brand recall and aspirational demand. PUMA has been especially active in Africa, as it will serve as the official technical partner for AFCON 2025 in Morocco and back 5 African national federations in its 2026 portfolio. This strategy is important because federation ties support apparel visibility, ball merchandising, grassroots activation, and broader retail pull. In the Middle East and Africa football market, the top global brands shape perception well beyond their direct sales footprint.

Nike continues to strengthen its football position through premium product launches and distribution upgrades linked to its broader category strategy. Its focus on products such as Tiempo, Mercurial, and AeroFit kits, along with expansion across more than 5,000 global football doors, helps reinforce premium demand and visibility in the region. Adidas is defending its regional presence through club and federation relationships, including its Al Qadsiah partnership from July 2026 and its return as South Africa’s official kit sponsor from January 2026. These moves show that the Middle East and Africa football market remains strategically important for brands seeking both Gulf purchasing power and African fan reach. PUMA’s Al-Hilal relationship provides another example of how companies use club-level partnerships to build visibility across licensed merchandise and on-pitch performance products simultaneously. Together, these strategic moves keep the top tier competitive, highly visible, and difficult for smaller international rivals to displace quickly.

However, the market remains open to challengers, as local and mid-tier suppliers gain ground in targeted contracts and price-sensitive segments. ProStar Sports International’s Rwanda Premier League ball deal, Owu Sportswear’s Nigerian club relationships, and Justfit’s role in Tanzania show that local companies can compete more effectively on delivery, pricing, and domestic relevance. Joma’s equipment deal with Saudi club Al Khalij also confirms that mid-tier European brands are finding entry points through club partnerships below the most expensive sponsorship layers. Select Sport, Miter, Uhlsport, Molten, and Derbystar continue to hold niche positions where certified match-ball quality matters more than mass retail scale. In the Middle East and Africa football market, concentration is significant at the top, but it does not extend across the full value chain. Premium branding remains concentrated, while the wider equipment supply landscape remains more open because local producers and specialist brands can still win league contracts, value segments, and selected performance categories.

Middle East and Africa Football Industry Leaders

Nike, Inc.

Adidas AG

PUMA SE

Molten Corporation

Select Sport A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Adidas commenced its official kit partnership with Al Qadsiah FC on July 1, 2026. The partnership covered the club’s men’s and women’s teams and its Elite Academy program. Al Qadsiah, one of the fastest-growing clubs in the Saudi Pro League, was led by a management team with stated ambitions to compete at the international level.

- March 2026: PUMA officially launched national team kits for 11 nations, including five African federations: Morocco, Ghana, Senegal, Côte d'Ivoire, and Egypt. The kits featured ULTRAWEAVE technology, while the replica versions used RE:FIBRE sustainable production. The launch strengthened PUMA's position as the kit brand with the strongest African portfolio for the FIFA World Cup 2026.

- March 2026: Decathlon opened its fourth store in Ghana at Kumasi City Mall on March 21, 2026. The store was its first in the Ashanti Region, extending its football retail presence into Ghana’s second-largest city and strengthening its position as Ghana’s leading sports retail provider.

Middle East and Africa Football Market Report Scope

A football is an inflated ball used to play various sports sharing the same name. The Middle East and Africa football market report is segmented by size, category, end use, distribution channel, and geography. By size, the market is segmented into size 1 and 2, size 3, size 4, and size 5. By category, the market is segmented into mass and premium. By End use, the market is segmented into personal and commercial. By distribution channel, the market is segmented into online stores and offline stores. By geography, the market is segmented into the United Arab Emirates, South Africa, Saudi Arabia, Qatar, Kuwait, Oman, Bahrain, Kenya, Nigeria, Egypt, Morocco, and the rest of the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Size 1 and 2 |

| Size 3 |

| Size 4 |

| Size 5 |

| Mass |

| Premium |

| Personal |

| Commercial |

| Online Stores |

| Offline Stores |

| United Arab Emirates |

| South Africa |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Kenya |

| Nigeria |

| Egypt |

| Morocco |

| Rest of Middle East and Africa |

| Size | Size 1 and 2 |

| Size 3 | |

| Size 4 | |

| Size 5 | |

| Category | Mass |

| Premium | |

| End Use | Personal |

| Commercial | |

| Distribution Channel | Online Stores |

| Offline Stores | |

| Geography | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Kenya | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the 2031 outlook for football sales across the Middle East and Africa?

The Middle East and Africa football market is projected to reach USD 2.53 billion by 2031 from USD 1.82 billion in 2026, growing at a 6.81% CAGR over 2026 to 2031.

Which country currently leads regional revenue?

Saudi Arabia led in 2025 with a 29.13% share, supported by club privatization, stronger sports participation, and deeper brand activity.

Which country is expanding the fastest through 2031?

The United Arab Emirates is forecast to grow fastest at a 8.56% CAGR, driven by sports performance infrastructure and premium training demand.

Which product size generates the most revenue?

Size 5 footballs led with a 53.71% share in 2025 because they are the standard for adult matches and structured training.

Page last updated on: