Middle East and Africa Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

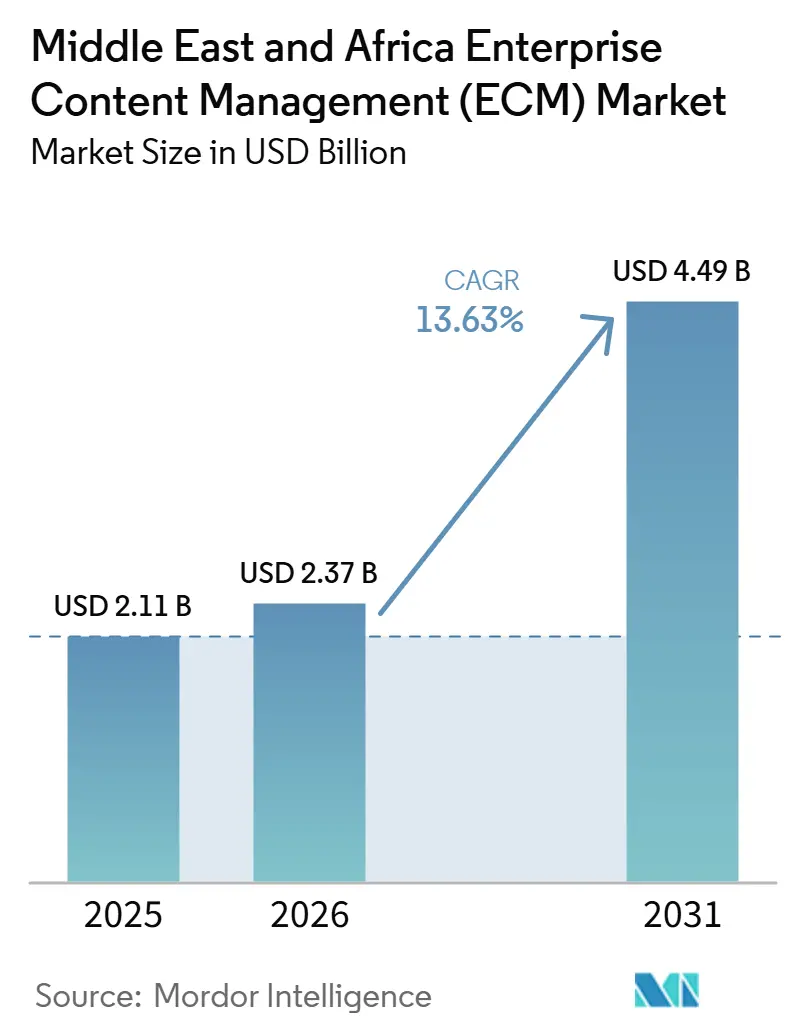

| Base Year Market Size (2025) | USD 2.11 Billion |

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 13.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

The Middle East and Africa Enterprise Content Management (ECM) Market size is projected to expand from USD 2.11 billion in 2025 and USD 2.37 billion in 2026 to USD 4.49 billion by 2031, registering a CAGR of 13.63% between 2026 and 2031. The market is moving forward as public-sector digitization programs, stronger compliance requirements, and wider acceptance of sovereign cloud environments reinforce one another across the region. Saudi Arabia and the UAE continue to shape demand because government agencies and regulated industries now need systems that support record governance, controlled access, and in-country hosting requirements. Vendor competition is also changing because buyers increasingly look for Arabic language automation, local hosting credentials, and stronger integration with legacy banking and ERP environments rather than basic document storage alone The Middle East and Africa Enterprise Content Management (ECM) Market is also benefiting from a shift toward workflow led deployments, which means customers are using these platforms to automate approvals, compliance tracking, and records handling instead of only digitizing archives. Growth will still be moderated by integration complexity, uneven infrastructure outside the Gulf, and a shortage of implementation talent, but the balance of demand remains positive through the forecast period.

Key Report Takeaways

- By geography, the Middle East held 68.42% of the Middle East and Africa Enterprise Content Management (ECM) Market share in 2025, while Africa is projected to record the highest CAGR at 16.94% through 2031.

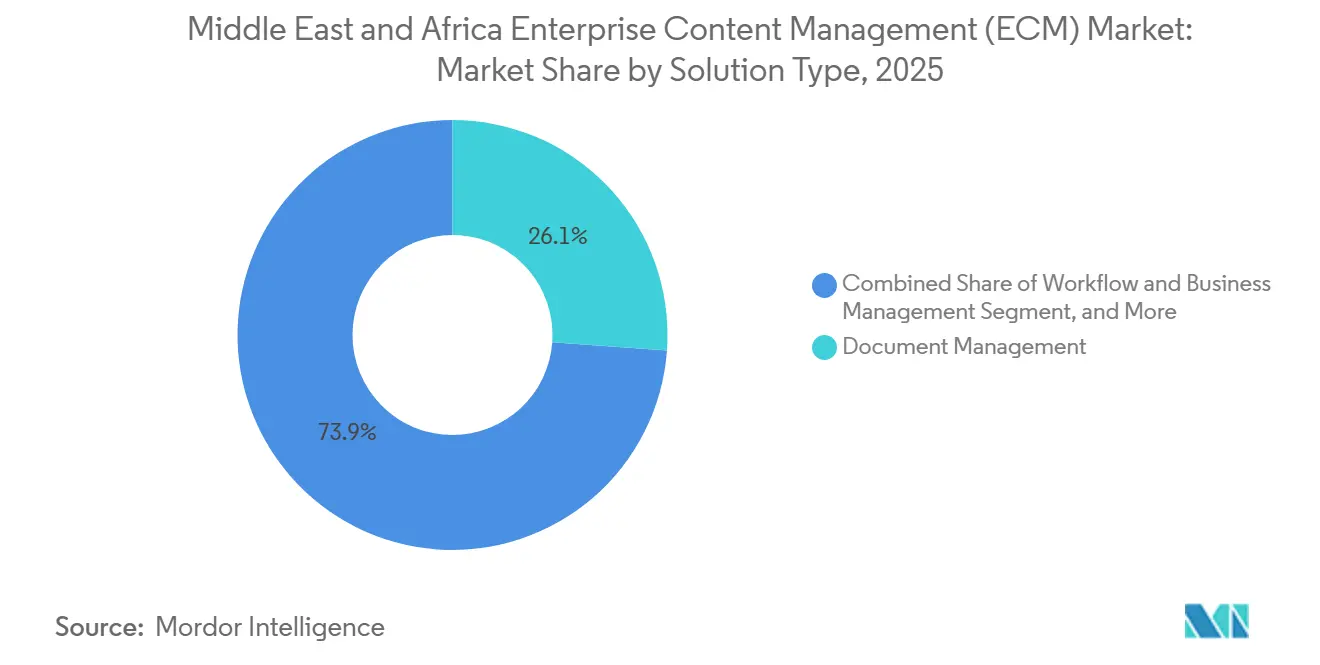

- By solution type, document management accounted for 26.14% of the Middle East and Africa Enterprise Content Management (ECM) Market size in 2025, while workflow and business process management is forecast to expand at a 15.82% CAGR through 2031.

- By deployment mode, cloud held 73.41% of the market in 2025 and also registers the fastest projected CAGR at 16.24% through 2031.

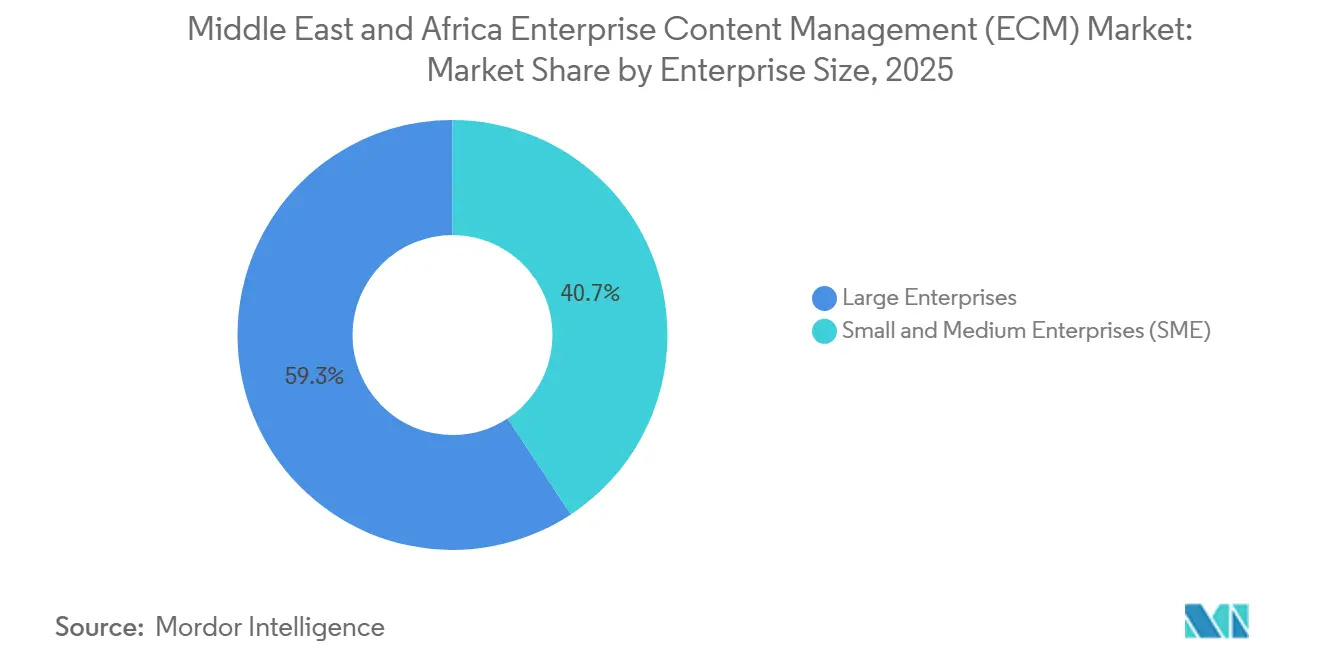

- By enterprise size, large enterprises represented 59.28% of the market in 2025, while SMEs are set to grow at the highest CAGR of 15.63% through 2031.

- By end user industry, BFSI captured 24.53% of the market in 2025, while healthcare is forecast to advance at a 16.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Cloud-First Public Sector Modernization | +3.1% | Middle East, primarily Saudi Arabia, UAE, Qatar, Turkey | Medium term (2-4 years) |

| Rising Demand for Compliance-Ready Digital Records | +2.7% | Middle East and Africa, concentrated in Saudi Arabia, UAE, South Africa, Nigeria | Short term (≤ 2 years) |

| AI-Based Document Classification and Retrieval Adoption | +2.2% | UAE and Saudi Arabia first, expanding into Egypt and South Africa | Medium term (2-4 years) |

| Sovereign Data Hosting Requirements in Regulated Industries | +1.8% | National, with early gains in Saudi Arabia, UAE, and Qatar | Short term (≤ 2 years) |

| Cross-Enterprise Workflow Orchestration Growth | +1.6% | Broad regional relevance | Medium term (2-4 years) |

| Shift From Email-Centric Sharing to Controlled Platforms | +1.2% | Broad regional relevance, strongest in BFSI and government | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Cloud-First Public Sector Modernization

Public sector demand has become one of the clearest growth channels for the Middle East and Africa Enterprise Content Management (ECM) Market because governments now treat controlled content platforms as part of national digital infrastructure rather than optional office software. This pattern is most visible in the Gulf, where ministries are moving document handling, archive management, and internal workflow processes into cloud-aligned environments that can scale across departments. Hyland expanded its regional footprint in August 2025 and deployed its Content Innovation Cloud across Saudi government-related organizations through a local partner, demonstrating how vendors are using reference projects to gain broader public-sector credibility.[1]Hyland Software, “Hyland Expands in Saudi Arabia and UAE for GCC Growth,” Hyland, hyland.com The same demand pattern is also spreading into African public agencies, where digital modernization programs are placing more emphasis on local hosting and simpler deployment economics. This means vendors now face two distinct buying environments: Gulf buyers want advanced automation and Arabic-language capability, while many African agencies focus first on sovereignty, affordability, and workflow control. The effect is a market where public procurement supports both near-term volume and longer-term platform standardization across regulated institutions.

Rising Demand for Compliance-Ready Digital Records

Compliance has moved from a supporting factor to a primary buying trigger for the Middle East and Africa Enterprise Content Management (ECM) Market. Saudi Arabia’s personal data protection regime and the UAE’s federal privacy framework are pushing organizations toward stronger retention rules, access governance, and tighter control over cross-border record movement. That shift matters because email-based sharing and unmanaged file repositories do not provide the audit trails or policy controls that regulated buyers now need. The healthcare example in Dubai shows how this requirement has become operational, as the NABIDH platform had unified more than 9.5 million patient records across over 1,300 facilities by November 2024, underscoring the importance of structured interoperability and governed content exchange. The same pressure is evident in public agencies and municipalities in South Africa, where record systems are increasingly aligned with legal compliance and service delivery requirements. As a result, buyers are not only asking whether they need a platform, but also comparing which architecture best satisfies the rules that apply to their sector and jurisdiction.[2]Dubai Health Authority, “NABIDH Initiative Reaches Major Milestone,” Dubai Health Authority, dha.gov.ae

AI-Based Document Classification and Retrieval Adoption

Artificial intelligence is changing the value proposition of the Middle East and Africa Enterprise Content Management (ECM) market, as buyers increasingly expect platforms to classify, extract, and route content rather than simply store it. This is especially important in Arabic-language environments, where global models trained primarily on Latin-script documents may not deliver the precision needed for regulated workflows. A peer-reviewed study published in June 2026 demonstrated automated compliance classification of Arabic privacy policy documents under the Saudi PDPL, supporting the case for region-specific AI deployment in governance-heavy environments.[3]PLOS One Editors, “Mumtathil, Automatic PDPL Compliance Identification System of Arabic Privacy Policies Documents,” PLOS One, plos.org The shift also changes vendor screening, because buyers in Saudi Arabia and the UAE now look more closely at model quality, language support, and metadata extraction reliability during procurement. This trend aligns with a broader move from passive digital repositories toward active document intelligence in customer onboarding, claims handling, case management, and public administration. Over time, the vendors that document strong Arabic-language accuracy and controlled automation will be better positioned for high-value government and BFSI deals.

Sovereign Data Hosting Requirements in Regulated Industries

Sovereign hosting has become a direct architecture requirement rather than a secondary preference in the Middle East and Africa Enterprise Content Management (ECM) Market. Saudi Arabia’s cybersecurity and financial supervision frameworks have raised the importance of keeping sensitive content inside national boundaries, especially for financial institutions and critical infrastructure operators.[4]SITE Cloud, “SITE Sovereign Cloud Brochure,” SITE Cloud, site.sa In the UAE, the Central Bank launched a sovereign financial cloud services infrastructure in February 2026 with Core42, reinforcing the need for jurisdiction-controlled environments across banking and insurance records workflows. The UAE Sovereign Launchpad will also become commercially available in November 2025 through e& and Amazon Web Services, providing regulated customers with a compliant path into hyperscale infrastructure. These developments matter because they reduce hesitation around cloud deployment in sectors that previously viewed external infrastructure as a compliance risk. They also narrow the vendor field, since suppliers without recognized sovereign hosting options can be screened out before product evaluation even starts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy ERP and Line-of-Business Systems | -2.0% | Broad regional relevance | Long term (≥ 4 years) |

| Uneven Data Residency Infrastructure Across the Region | -1.5% | Africa, especially South Africa, Nigeria, Egypt, and non-GCC Middle East | Medium term (2-4 years) |

| Shortage of ECM Implementation and Governance Talent | -1.0% | Broad regional relevance, strongest in Africa and smaller GCC states | Long term (≥ 4 years) |

| Budget Sensitivity Among Mid-Market Buyers | -0.7% | Africa and Turkey | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy ERP and Line-Of-Business Systems

Legacy ERP estates remain a major barrier to faster rollouts in the Middle East and Africa Enterprise Content Management (ECM) Market. Many large organizations across government, utilities, energy, and financial services still operate long-standing SAP and Oracle environments that were not designed for modern metadata structures, workflow orchestration, or AI-ready document classification. This creates practical problems during migration because old filing taxonomies, process steps, and access policies rarely map cleanly into current content models. The result is that implementation work can become large, slow, and expensive, thereby increasing service costs and delaying business value realization. The challenge is especially evident in industrial settings, where engineering files, plant maintenance records, and safety documentation reside across multiple legacy systems with different formats and controls. Even when buyers want modernization, they often move in phases because replacing document flows is harder when those flows are deeply tied to core operational systems.

Uneven Data Residency Infrastructure Across The Region

Infrastructure readiness remains uneven, limiting how quickly the Middle East and Africa Enterprise Content Management (ECM) Market can scale beyond the strongest Gulf markets. Saudi Arabia, the UAE, and Qatar already offer more mature in-country cloud options that support the compliance needs of regulated buyers and reduce deployment friction. Many African markets lack the same depth of certified local infrastructure, so organizations often need hybrid models that keep sensitive records on premises while shifting selected processing tasks to the cloud. That design can still work, but it increases operating complexity and total cost of ownership compared with a straightforward cloud rollout. South Africa stands out as a stronger environment than many neighboring markets, while Egypt, Nigeria, and other countries continue to build local capacity from a smaller base. This gap slows deal velocity in parts of Africa and keeps demand tilted toward vendors that can support both hybrid and on-premises operating models without weakening governance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Workflow Automation Outpaces Legacy Storage Architectures

Document management accounted for 26.14% of the Middle East and Africa Enterprise Content Management (ECM) Market in 2025, indicating that core archive digitization and records capture still represent a large part of regional demand. This leadership reflects the fact that many public agencies, banks, and healthcare providers are still migrating large paper-based and file-share-based repositories to structured systems with stronger access controls and retrieval logic. The OpenText Extended ECM deployment for Egypt’s Ministry of Communications and Information Technology demonstrates that document management remains central to large public-sector programs when governments seek a common repository and standardized taxonomy across departments. That use case matters because central repositories often become the first governed layer before organizations extend into process automation, case flows, and broader interoperability. Document management, therefore, remains the point where many buyers begin, even when their longer-term plan is much broader. It provides the foundation for content standardization, enforcement of retention policies, and migration away from unmanaged local storage.

Workflow and business process management is forecast to expand at a 15.82% CAGR through 2031, making it the fastest-growing solution area in the region. This change suggests that buyer priorities are shifting from static storage toward content-enabled process execution, especially in approvals, compliance routing, onboarding, and service delivery. Records management demand is also rising because privacy and governance rules now require clearer retention schedules and defensible audit trails in regulated institutions. Case management is gaining relevance in healthcare and legal workflows, while digital asset management is becoming more visible in tourism, media, and cultural content environments. Web content management also remains relevant because governments and enterprises continue to expand digital service delivery and online interaction across the region. Taken together, the solution mix shows a market that still values strong repositories, but increasingly rewards vendors that connect those repositories to live operational workflows.

By Deployment Mode: Sovereign Cloud Mandates Entrench Cloud-Led Spending

Cloud accounted for 73.41% of the Middle East and Africa Enterprise Content Management (ECM) Market share in 2025 and is also projected to post the highest CAGR of 16.24% through 2031. This combination shows that cloud is not only the leading deployment model today but is also gaining momentum faster than the rest of the market. The reason is not only scalability or lower infrastructure effort. The stronger reason is that sovereign cloud frameworks now provide regulated sectors with a compliant route to modern deployment, provided data residency and auditability requirements are met. That has been particularly important in BFSI, government, healthcare, and education, where customers want elastic infrastructure without giving up local control. Cloud also enables faster access to AI services, strengthening the business case for intelligent classification, content search, and automated workflows.

On-premises deployment still plays a role in the Middle East and Africa Enterprise Content Management (ECM) Market because some large industrial and public-sector buyers remain tied to legacy systems, internal policies, or operational technology environments. In energy, utilities, and manufacturing, local processing continues to matter where engineering files and operational documentation must remain close to established systems. Hybrid deployment is therefore becoming an important bridge model, especially in African markets where local cloud capacity remains uneven, and organizations want to combine control with selective scalability. That pattern is important because it means buyers are not simply choosing between old and new models. Instead, many are building layered architectures that place sensitive content in controlled environments while moving workflow, search, and analytics into more flexible infrastructure. Vendors that support content federation across these models will hold an advantage over those that push a single deployment path. The deployment picture, therefore, confirms that cloud leads the market, but adaptability still matters strongly across countries and end users.

By Enterprise Size: SMEs Emerge As The Next High-Volume Customer Tier

Large enterprises accounted for 59.28% of spending in 2025, reflecting the concentration of high-value projects within government bodies, banks, health systems, and other complex institutions. These buyers often need broad governance controls, multi department routing, policy based access, and deep integration with existing platforms, which naturally raises contract size and deployment scope. Newgen’s document and records management deployment for Vision Bank in the UAE demonstrates how large financial institutions are standardizing on enterprise-grade platforms that provide full lifecycle management and integration with core systems. Large organizations also tend to move first when new compliance expectations emerge, because they face heavier audit exposure and more complex internal reporting needs. In the Middle East and Africa Enterprise Content Management (ECM) Market, large enterprises remain the primary source of revenue, even as other customer groups expand. Their role remains important because they set reference standards that other buyers often follow.

SMEs are forecast to grow at a 15.63% CAGR through 2031, making them the fastest-growing enterprise size tier in the region. This growth is being supported by SaaS pricing models that lower upfront costs and make adoption more realistic for mid-sized firms that once viewed these platforms as too complex or too expensive. The opportunity is particularly visible in countries such as Turkey, Egypt, South Africa, and Nigeria, where businesses are adopting structured content tools for invoices, contracts, HR files, and service workflows. This shift also reflects a move away from email-centered document exchange toward more controlled systems that can track approvals and reduce operational friction. Vendors that package modular subscriptions, support local-language usability, and require lighter implementation are likely to compete more effectively in this tier. Budget sensitivity remains real, but the addressable base is widening as customers look for practical workflow control rather than large-scale transformation programs. Over time, SMEs may not match large enterprises in deal value, but they can become a much broader volume engine for regional growth.

By End-User Industry: BFSI Anchors Volume While Healthcare Scales Fastest

BFSI accounted for 24.53% of spending in 2025, making it the largest end-user group in the regional market. Banks, insurers, and related financial institutions face strong demands around customer documentation, anti-money laundering controls, onboarding records, approval trails, and retention rules, which keep content governance close to core operations. This group also places a premium on sovereign hosting, audit readiness, and secure workflow integration, which aligns closely with current vendor differentiation across the region. The Middle East and Africa Enterprise Content Management (ECM) Market, therefore, continues to rely on BFSI as its strongest source of current spending and reference quality projects. Financial institutions also tend to evaluate vendors more rigorously on integration and compliance depth, which raises the importance of proven regional templates. That dynamic favors suppliers that can align platform design with local supervisory and data control expectations.

Healthcare is projected to expand at a 16.41% CAGR through 2031, making it the fastest-growing end-user group. The main reason is that healthcare providers increasingly need systems that can support governed document exchange, patient record interoperability, and controlled retention across distributed facilities. Dubai’s NABIDH program illustrates the scale of this transition, with over 9.5 million patient records unified across more than 1,300 facilities by November 2024. Government and public sector demand is also growing strongly, while IT and telecommunications, manufacturing, retail, media, education, and energy each add their own use cases based on document volume and compliance exposure. Energy and utilities remain especially significant because engineering records, safety documents, and environmental files often sit in fragmented formats that are hard to govern consistently. The end-user mix, therefore, combines strong current spending in BFSI with a rapidly rising healthcare opportunity and a broader public sector and industrial pipeline across the region.

Geography Analysis

The Middle East held 68.42% of the Middle East and Africa Enterprise Content Management (ECM) Market share in 2025, which confirms that the region remains the main revenue center for current demand. This lead reflects deeper public sector technology spending, stronger sovereign cloud readiness, and a more mature compliance environment across Saudi Arabia, the UAE, and Qatar. Saudi Arabia and the UAE continue to serve as the clearest reference markets because both countries combine government modernization programs with stringent regulatory oversight of data handling and hosting. OpenText opened its regional headquarters in Riyadh in February 2026, indicating that global vendors view Saudi Arabia as a base for both government and private-sector expansion. Saudi Arabia’s Ministry of Tourism also launched the ARDOC platform in November 2025, demonstrating how public-sector use cases are expanding beyond records storage into digital asset governance and Arabic-language metadata handling.

Qatar adds to regional demand through its regulated financial ecosystem and its cloud control framework, which supports BFSI-focused deployments. Turkey has a different profile because demand there is more closely tied to private-sector modernization and mid-market needs than to sovereign digital programs. That difference matters because it broadens the vendor opportunity set inside the Middle East portion of the market. Some buyers need large, bespoke deployments for ministries and regulated institutions, while others prefer lighter SaaS-led rollouts with lower implementation effort. The Middle East portion of the Middle East and Africa Enterprise Content Management (ECM) Market, therefore, combines scale, maturity, and varied customer profiles within a relatively concentrated revenue base.

Africa is forecast to record the highest CAGR of 16.94% through 2031, indicating faster expansion from a smaller starting point. Growth is being shaped by sovereign public-sector digitization, rising compliance awareness, and the need to move away from fragmented manual record-keeping across agencies and enterprises. Egypt stands out because its government digitization program includes the OpenText Extended ECM deployment for the Ministry of Communications and Information Technology, as well as the OneTrack platform, which processes 250 million documents across 103 government bodies. South Africa remains important because POPIA-related record governance and formal public-sector requirements create a clearer compliance-led demand path than in many other African markets. Across the rest of sub-Saharan Africa, the opportunity is earlier stage, but low existing penetration and growing digital connectivity create room for leapfrog adoption through cloud-native and hybrid platforms. That makes Africa the faster growth engine in the regional outlook, even though the Middle East continues to dominate current value.

Competitive Landscape

The Middle East and Africa Enterprise Content Management (ECM) Market remains moderately fragmented, with global software vendors competing alongside regional specialists that bring stronger localization and implementation familiarity. The main global names visible in the landscape include OpenText, Hyland, Newgen Software, Laserfiche, M-Files, and DocuWare, while local and Arabic-capable providers are gaining relevance in regulated public sector and BFSI opportunities. Competition is no longer based only on repository functions. Buyers increasingly compare sovereign hosting options, Arabic-language automation, workflow depth, and integration readiness with banking cores and long-standing ERP systems. This means the best-positioned vendors are often the ones that can combine core platform breadth with country-specific delivery credibility. The Middle East and Africa Enterprise Content Management (ECM) Market, therefore, rewards a mix of product capability and regional operating fit rather than a one-size approach.

Hyland provides one clear example of how vendors are adapting to that environment. The company expanded its presence in Saudi Arabia and the UAE in August 2025, then deepened its sovereign cloud alignment in June 2026 through a partnership with Microsoft to deliver the Content Innovation Cloud on Azure. OpenText offers another example, establishing its regional headquarters in Riyadh in February 2026 and strengthening its public sector relevance through the deployment of the Egyptian government repository. Newgen is also gaining traction in financial services through its Vision Bank project and its 2026 agreement with a large UAE government organization, demonstrating how regional execution strength can translate into repeat institutional demand. These moves show that vendors are investing not just in product features but also in local presence, reference deployments, and compliance-aligned infrastructure partnerships.

Product differentiation is also shifting toward AI-enabled classification, retrieval, and workflow orchestration, especially for Arabic-language records and high-volume regulated document sets. The 2026 PLOS One study supports the technical direction of this shift by demonstrating automated PDPL classification of Arabic privacy documents. At the same time, buyers in Africa and Turkey are more price sensitive, which leaves room for vendors that can deliver practical hybrid or SaaS led deployments without the cost structure of large custom rollouts. Mid-market whitespace remains meaningful because many smaller organizations still need basic workflow control, invoice handling, contract governance, and HR records management with local support. This keeps the competitive field open, even though the larger global platforms currently anchor many of the most visible reference accounts across government and BFSI.

Middle East and Africa Enterprise Content Management (ECM) Industry Leaders

Microsoft Corporation

OpenText Corporation

IBM Corporation

Hyland Software, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Hyland announced a strategic partnership with Microsoft to deliver the Hyland Content Innovation Cloud on Microsoft Azure, enabling MEA customers to deploy Hyland ECM solutions with flexible geographic hosting, data residency options aligned with GCC sovereign cloud requirements, and access to Azure AI services for agentic content automation.

- February 2026: The Central Bank of the UAE partnered with Core42, a G42 company, to launch the world's first sovereign financial cloud services infrastructure, a dedicated, isolated cloud ecosystem for UAE financial sector content and compliance workloads that anchors deployments for UAE banks and insurance firms within UAE jurisdiction

- February 2026: OpenText opened its Middle East regional headquarters at the King Abdullah Financial District in Riyadh, Saudi Arabia, establishing a central hub for GCC government and private sector customers transitioning from AI experimentation to enterprise scale deployment of secure information management on February 3, 2026

- November 2025: The UAE Sovereign Launchpad, a joint sovereign cloud offering from e& and Amazon Web Services, became commercially available for UAE government, healthcare, financial services, and education operators, providing a hyperscale cloud environment satisfying UAE regulatory compliance requirements for content workloads

Middle East and Africa Enterprise Content Management (ECM) Market Report Scope

The Middle East and Africa enterprise content management (ECM) market refers to the ecosystem of software solutions and services designed to systematically capture, manage, store, preserve, and deliver an organization's unstructured and structured content and documents. This includes technologies such as document management, records management, workflow and business process management, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across diverse industries in the region, including BFSI, government, healthcare, manufacturing, and retail. Driven by rapid digital transformation initiatives (such as Saudi Vision 2030), economic diversification efforts, and the growing need for regulatory compliance and data security across MEA countries, ECM solutions enable businesses to streamline operations, enhance cross-departmental collaboration, mitigate operational risks, and reduce reliance on manual paper-based processes to improve overall productivity and decision-making.

The Middle East And Africa Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises (SME), and Large Enterprises), End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecommunications, Manufacturing, Retail, Media and Entertainment, Education, Energy and Utilities, and Other End-User Industries), and Geography (Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Retail |

| Media and Entertainment |

| Education |

| Energy and Utilities |

| Other End-User Industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Solution Type | Document Management | |

| Records Management | ||

| Workflow and Business Process Management | ||

| Case Management | ||

| Digital Asset Management | ||

| Web Content Management | ||

| Other Solutions | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises (SME) | |

| Large Enterprises | ||

| By End-User Industry | BFSI | |

| Government and Public Sector | ||

| Healthcare | ||

| IT and Telecommunications | ||

| Manufacturing | ||

| Retail | ||

| Media and Entertainment | ||

| Education | ||

| Energy and Utilities | ||

| Other End-User Industries | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size outlook for the Middle East and Africa Enterprise Content Management (ECM) Market?

The market is projected at USD 2.37 billion in 2026 and is expected to reach USD 4.49 billion by 2031 at a 13.63% CAGR, which points to strong regional expansion over the forecast period.

Which factor is pushing adoption the most across the region?

Public sector modernization and compliance led records governance are the main demand drivers, especially where ministries, banks, and healthcare providers need auditable and locally hosted content systems.

Why is cloud deployment leading in this space?

Cloud held 73.41% of spending in 2025 because sovereign hosting options now give regulated buyers a compliant path to scale, automation, and AI enabled workflows.

Which end user group is growing fastest?

Healthcare is the fastest growing end user segment at a 16.41% CAGR through 2031, supported by rising demand for governed document exchange and patient record interoperability.

What makes vendor selection harder in this region?

Buyers are screening more closely for Arabic language intelligence, sovereign data hosting support, and integration with legacy ERP and banking systems, which narrows the field quickly.

Which geography is shaping the next growth wave?

The Middle East still dominates current revenue with 68.42% share in 2025, but Africa is forecast to grow faster at a 16.94% CAGR as public sector digitization expands from a smaller base.

Page last updated on: