Middle-East And Africa Electric Vehicle (EV) Fluids Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

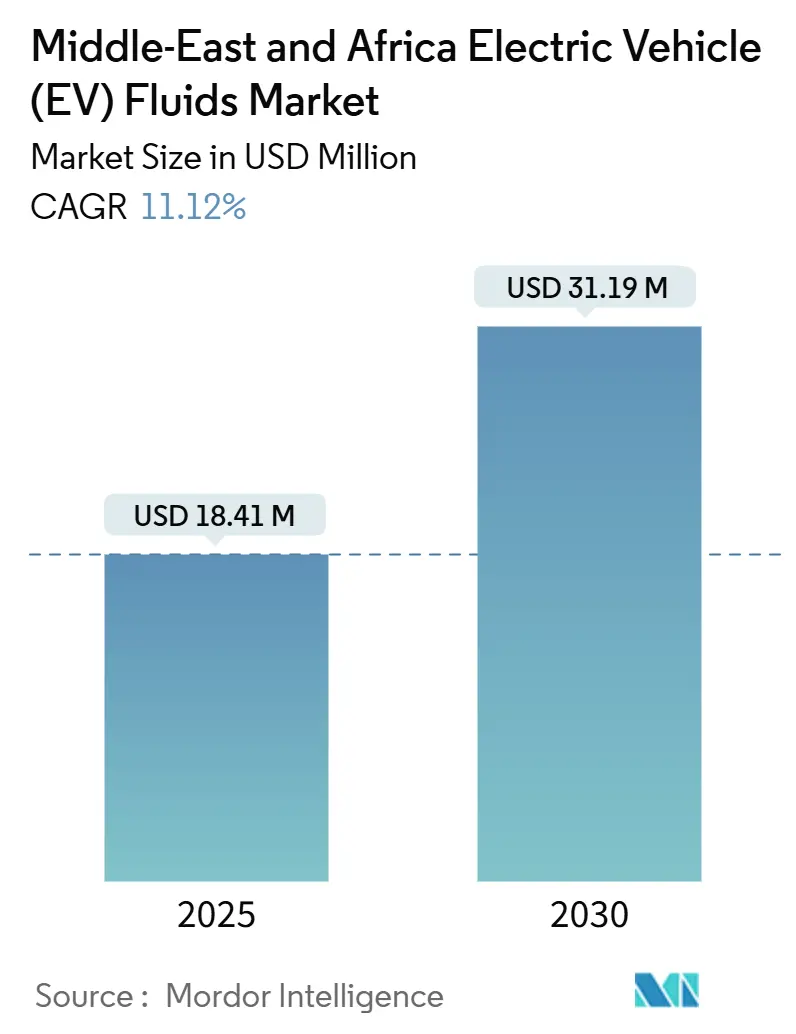

| Market Size (2025) | USD 18.41 Million |

| Market Size (2030) | USD 31.19 Million |

| Growth Rate (2025 - 2030) | 11.12% CAGR |

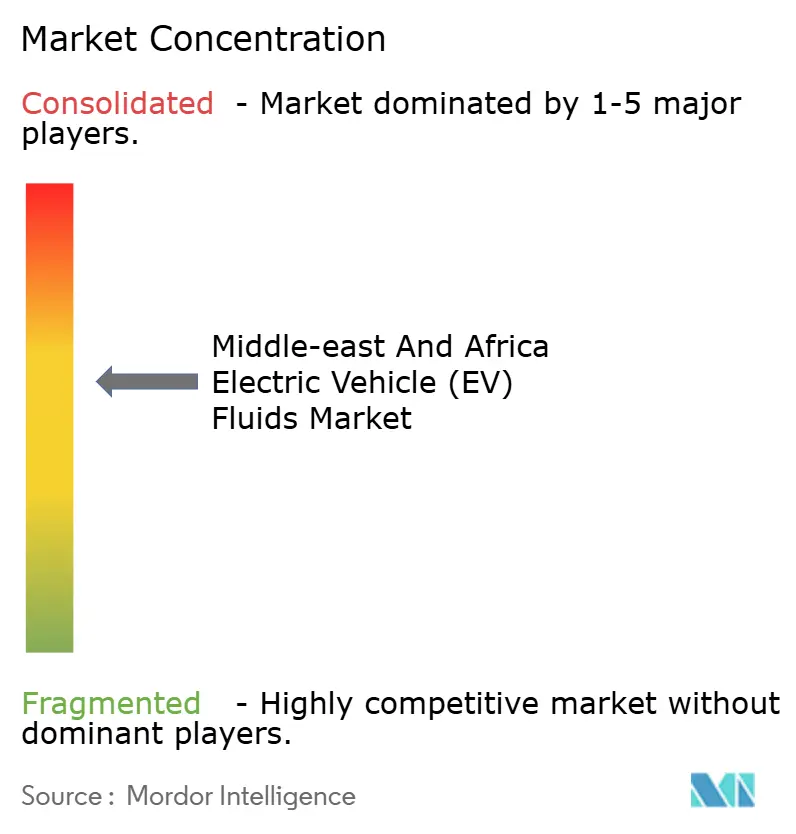

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Electric Vehicle (EV) Fluids Market Analysis by Mordor Intelligence

The Middle-East and Africa Electric Vehicle Fluids Market size is estimated at USD 18.41 million in 2025, and is expected to reach USD 31.19 million by 2030, at a CAGR of 11.12% during the forecast period (2025-2030). Rapid electrification mandates, the push for domestic battery production, and innovations in high-temperature thermal-management fluids collectively underpin this growth path. Saudi Arabia’s investment program, Morocco’s 20 GWh gigafactory, and the UAE’s 40 GWh cell plant are recasting the regional supply chain from import-dependent to increasingly localized. Parallel advances in 800-V vehicle platforms, immersion-cooling technologies, and dielectric coolant chemistries are redefining product specifications well beyond conventional glycol blends. Market opportunities favor suppliers that can co-engineer fluids with OEMs, ensure ultra-low conductivity, and navigate fragmented tariff regimes. Conversely, the absence of harmonized service-interval standards, high import duties on specialty base oils, and widespread counterfeit penetration in a few African channels continue to temper the overall market expansion.

Key Report Takeaways

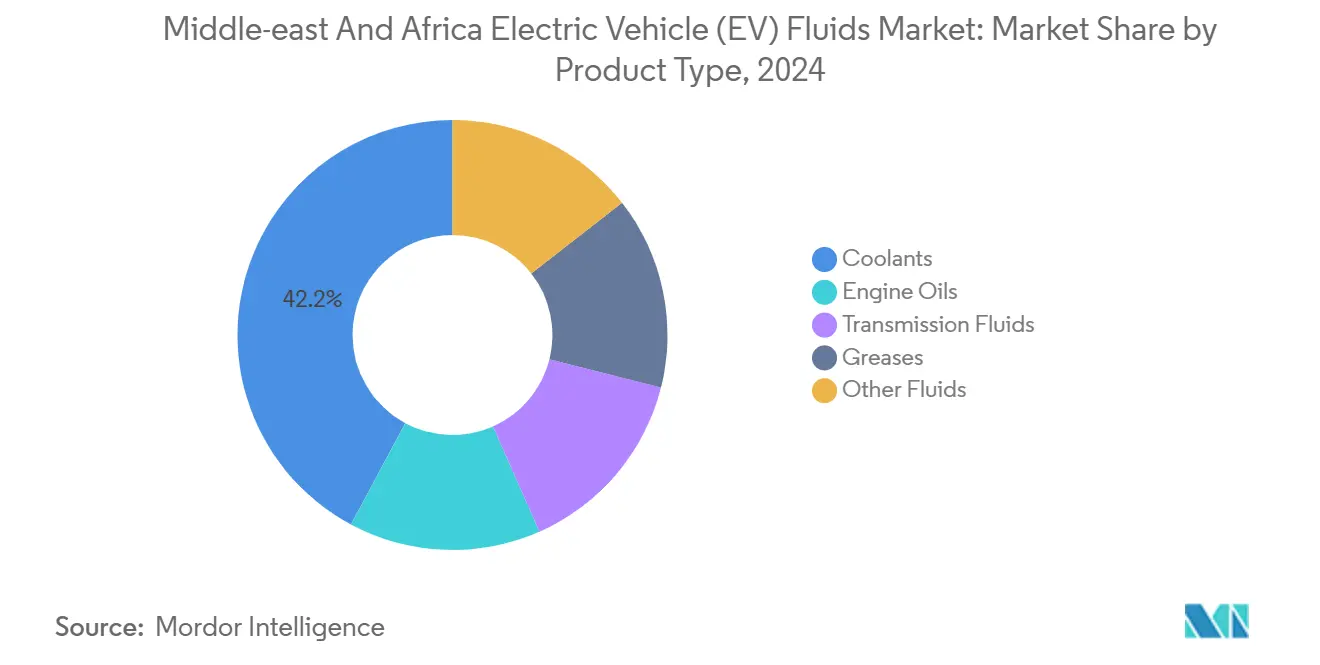

- By product type, coolants led with 42.17% of the Middle-east and Africa electric vehicle (EV) fluids market share in 2024. Transmission fluids are forecast to expand at a 12.18% CAGR through 2030.

- By propulsion type, battery electric vehicles captured 71.22% share of the Middle-east and Africa electric vehicle (EV) fluids market size in 2024. Plug-in hybrids are advancing at a 12.67% CAGR to 2030.

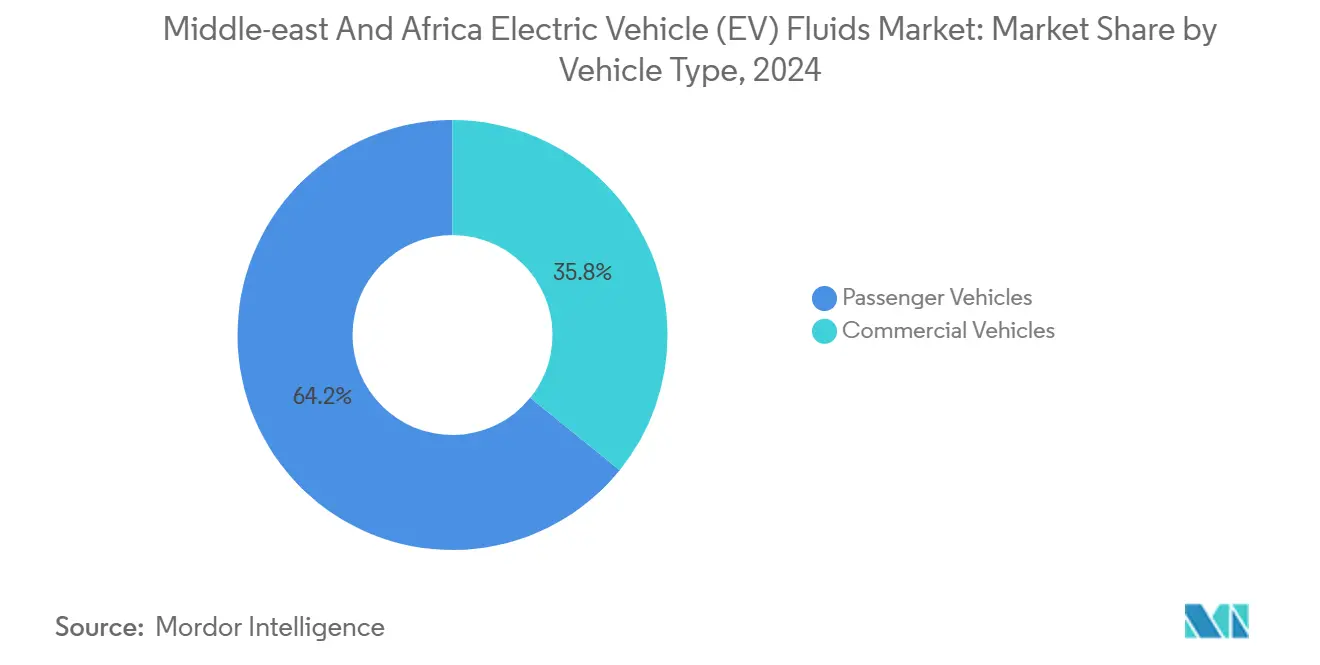

- By vehicle type, passenger vehicles accounted for a 64.18% share of the Middle-east and Africa electric vehicle (EV) fluids market size in 2024. Commercial vehicles post the strongest growth, at an 11.75% CAGR to 2030.

- By geography, the Rest of Middle-east and Africa segment held 56.18% revenue in 2024; Saudi Arabia is growing at 12.43% CAGR through 2030.

Competitive positioning in Middle east and africa includes both locally based firms and those operating across multiple regions. The market landscape in the global electric vehicle (ev) fluids industry research shows how these players are arranged internationally.

Middle-East And Africa Electric Vehicle (EV) Fluids Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring OEM demand for high-performance EV thermal-management fluids | +3.2% | Saudi Arabia, UAE, South Africa, with early concentration in Riyadh and Dubai | Medium term (2-4 years) |

| Government ZEV mandates and subsidy programmes accelerating BEV parc | +2.8% | Saudi Arabia (Vision 2030), Egypt (2040 target), South Africa (APDP incentives), UAE (Net Zero 2050) | Long term (≥ 4 years) |

| Rapid build-out of MEA gigafactories and e-bus assembly lines | +2.5% | Morocco (Gotion 20 GWh), UAE (Statevolt 40 GWh), Saudi Arabia (Ceer, Lucid), Egypt (planned capacity) | Medium term (2-4 years) |

| Shift to 800-V architectures requiring low-conductivity coolants | +1.9% | UAE and Saudi Arabia luxury segments, spill-over to South Africa premium market | Short term (≤ 2 years) |

| Rise of immersion-cooling for desert-operated commercial EV fleets | +1.5% | Saudi Arabia, UAE, with pilot deployments in logistics and public transport sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring OEM Demand for High-Performance EV Thermal-Management Fluids

Desert duty cycles subject battery packs to ambient air above 50 °C, and OEM programs in Riyadh and Dubai now require coolants with boiling points exceeding 170 °C and conductivity below 10 µS/cm[1]Lucid Motors, “Thermal Management in the Lucid Air,” lucidmotors.com. TotalEnergies introduced its EV Fluids line in September 2024 and, by March 2025, published regional electrical-conductivity benchmarks, signaling a shift toward standardized high-temperature specifications[2]TotalEnergies, “EV Fluids Technical Guide,” totalenergies.com . New-energy densities exceeding 300 Wh/kg generate higher waste heat, while Saudi Arabia’s target of 5,000 public fast chargers amplifies thermal load during rapid charging. The supplier role is migrating from commodity blending to early-stage co-engineering, a gap that smaller local brands struggle to bridge. The trend intensifies as luxury platforms integrate immersion cooling and demand on-site fluid analytics to protect warranty exposure.

Government ZEV Mandates and Subsidy Programmes Accelerating BEV Parc

Saudi Vision 2030 intends to achieve electric penetration in Riyadh by 2030, funding charging corridors and domestic manufacturing. Egypt’s roadmap also targets EV sales and layers fiscal rebates on locally assembled vehicles. The UAE’s Net Zero 2050 strategy subsidizes fleet conversions, enabling Dubai’s transport authority to field electric buses that rely on immersion-cooling fluids. Policy uptake is uneven: Morocco’s gigafactory incentives outpace consumer rebates, stalling mass adoption in rural areas. Fluid demand inflects when early incentive-driven vehicle cohorts require first coolant changes around 2027–2028, urging suppliers to synchronize inventory with staggered parc growth.

Rapid Build-Out of MEA Gigafactories and E-Bus Assembly Lines

Morocco’s Gotion High-Tech plant came online in 2024, with the UAE’s Statevolt project following, each consuming dielectric fluids for formation cycling and initial pack testing. Saudi Arabia’s Ceer facility and Lucid’s plant in King Abdullah Economic City anchor OEM-fill volumes and local-content mandates. South African, Egyptian, and UAE e-bus lines integrating BYD technology depend on proprietary coolant formulations that aftermarket blenders must license or replicate. This build-out creates a bifurcated supply chain: premium OEM-fill fluids that meet strict conductivity and materials-compatibility thresholds, and aftermarket alternatives battling counterfeit risks in some African channels.

Shift to 800-V Architectures Requiring Low-Conductivity Coolants

Hyundai’s E-GMP, Porsche Taycan, and Lucid Air platforms mandate coolant conductivity below 10 µS/cm to avoid parasitic current losses, pushing glycol-water mixtures beyond their performance envelope. Castrol’s ON and Shell’s Immersio fluids deploy synthetic ester bases to hold conductivity under 5 µS/cm over 150,000 km in 50 °C environments. Luxury EV concentration in the UAE and Saudi Arabia compels regional test labs to develop accelerated-aging protocols, while South Africa’s premium segment follows suit by 2027. Formulating to these standards limits the competitive field to multinationals with additive-chemistry depth and regional technical centers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import duties on specialty base oils and additives | -1.4% | South Africa (SACU 0-30% tariffs), Egypt (2-40% range), partial relief in GCC free zones | Medium term (2-4 years) |

| Undefined regional service-interval standards for EV driveline fluids | -0.9% | MEA-wide, with acute gaps in Saudi Arabia, Egypt, and sub-Saharan markets | Long term (≥ 4 years) |

| Chronic counterfeit-lubricant penetration in parts of Africa | -1.2% | Nigeria, Kenya, South Africa, Ghana, with estimated 10-30% market penetration in certain channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Duties on Specialty Base Oils and Additives

The Southern African Customs Union levies tariffs on synthetic esters and polyalphaolefins, raising landed costs for coolants engineered for ultra-low conductivity. Egypt’s duty bands stretch, and customs classification can add procedural delays. Although the GCC applies a unified import tariff, finished fluids still incur VAT in Saudi Arabia and the UAE, eroding margins. These duty structures encourage local blending, yet the region produces few advanced corrosion inhibitors or ion-scavenging additives, keeping supply chains exposed to international freight volatility.

Undefined Regional Service-Interval Standards for EV Driveline Fluids

OEM coolant-change guidance of 150,000 km originates from temperate-climate tests and lacks validation for continuous 50 °C cycles common in the Gulf. National bodies—SASO in Saudi Arabia, ESMA in the UAE, and SABS in South Africa—have yet to publish electric-fluid benchmarks, leaving fleet operators and aftermarket suppliers to interpret disparate OEM manuals. The absence of standards fragments SKU assortments, inflates inventory costs, and complicates liability claims if premature fluid failure damages battery packs. Harmonization efforts have begun through regional industry associations but remain unlikely to yield enforceable guidelines before 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coolants Dominate, Transmission Fluids Surge

Coolants contributed 42.17% of 2024 revenue as battery packs shed 3–5 kW of heat during rapid charging in ambient temperatures above 45 °C. The Middle-east and Africa electric vehicle (EV) fluids market size for coolants is forecast to broaden alongside immersion solutions that leverage dielectric esters to lower flash points and suppress conductivity drift. Transmission fluids, although a smaller slice today, will climb at 12.18% CAGR as multi-speed e-axles gain traction in commercial vans and buses where torque density and hill-climb efficiency justify added gearing. The Middle-east and Africa electric vehicle (EV) fluids market share for transmission fluids consequently widens as OEMs such as ZF and BorgWarner validate friction-modifier packs tailored to high-torque electric gearing. The segment landscape underscores a pivot from traditional glycol blends to bespoke chemistries that integrate ion-scavenging additives and boosted boiling ranges.

Engine oils endure in plug-in hybrids yet trend downward as full battery platforms proliferate, while greases cater to battery-pack cell tabs and e-motor bearings that demand low-outgassing performance at 150 °C operating envelopes. Niche categories—waterless coolants, dielectric immersion fluids, and low-viscosity brake fluids—gain prominence in continuous-duty e-bus fleets across Dubai and Gauteng, where operators prioritize reduced downtime and extended service intervals. PETRONAS’s partnership with Iceotope in mid-2024 highlights a growing preference for turnkey immersion-cooling ecosystems over discrete fluid sales.

By Propulsion Type: BEV Parc Leads, PHEV Growth Surprises

Battery electric vehicles constituted 71.22% of 2024 fluid demand, driven by subsidy-fueled purchases in Saudi Arabia, the UAE, and Egypt. The Middle-east and Africa electric vehicle (EV) fluids market size for BEVs concentrates on coolants, dielectric immersion liquids, and specialty greases, streamlining SKU complexity but raising quality thresholds. Plug-in hybrids, despite smaller volumes, will rate a 12.67% CAGR to 2030 as consumers in sub-Saharan Africa and rural Egypt retain combustion engines for range security. This dual-powertrain architecture doubles per-vehicle fluid consumption, spanning both advanced coolants and conventional low-ash engine oils.

Hybrid electric vehicles without plug-in capability shrink under tightening emissions policies, redirecting research and development budgets to full electric platforms. Suppliers with deep legacy lubricant portfolios—Shell, TotalEnergies, and BP’s Castrol—capitalize on PHEV demand by offering integrated coolant and engine-oil packages, while pure-play specialists such as Engineered Fluids focus on dielectric immersion niches where incumbents possess limited domain knowledge.

By Vehicle Type: Passenger Volume, Commercial Intensity

Passenger models delivered 64.18% of 2024 fluid consumption on the back of luxury EV uptake in Dubai and early adopter cohorts in Riyadh. While unit volumes lead the market, average coolant fills per vehicle remain modest. This modesty pushes suppliers to differentiate based on conductivity stability and extended service life. Commercial vehicles, including e-buses and last-mile vans, represent the value accelerator, posting an 11.75% CAGR through 2030. Each e-bus, consuming significant amounts of coolant or immersion fluid, operates continuously in extreme heat. This not only amplifies lifetime fluid throughput but also highlights the advantage for suppliers adept at on-site condition monitoring.

Regional initiatives, like Dubai's electrified bus routes and South Africa's Gautrain feeder fleet, utilize immersion-cooling systems. These systems forgo pumps and heat exchangers, prioritizing performance metrics such as flash-point resilience and sealed-life stability. Consequently, the commercial sector increasingly values holistic service offerings—encompassing fluid analytics, predictive maintenance, and thermal modeling—over mere product transactions.

Geography Analysis

Saudi Arabia is on track for a 12.43% CAGR through 2030, driven by Vision 2030's goal of achieving 30% EV penetration in Riyadh and an investment in infrastructure and production. While Ceer and Lucid plants bolster OEM-fill pull-through, VAT and import duties incentivize localized blending. Gulf Oil and potential entrants like Saudi Aramco, which debuted its AramcoDURA, AramcoPRIMA, and AramcoULTRA base-oil lines in January 2025, stand to benefit. Given the desert heat exceeding 50 °C, there's a demand for coolants with boiling points of 170 °C and conductivity under 10 µS/cm. This sets a performance benchmark that European formulations struggle to achieve without auxiliary chillers. Meanwhile, as SASO drafts EV-fluid standards, their release isn't anticipated before 2027.

South Africa, despite its smaller size, grapples with steep tariffs on synthetic base oils. Additionally, certain lubricant channels face counterfeit penetration. The Automotive Production and Development Programme promotes local assembly, yet the country recorded limited EV sales in 2024. While Shell and TotalEnergies run blending plants in Durban and Cape Town, leveraging logistic advantages, market acceptance remains stagnant, awaiting a broader rollout of charging infrastructure. High landed costs hinder the adoption of advanced coolants, making pricing a pivotal factor in purchasing decisions.

The Rest of Middle-east and Africa cluster—UAE, Egypt, Morocco, Kenya, Nigeria—combined for 56.18% 2024 revenue. This is indicative of the UAE's inclination towards luxury EVs and Morocco's burgeoning gigafactory. The UAE enjoys a customs tariff advantage and boasts a dense charging infrastructure, facilitating the early adoption of advanced 800-V platforms and immersion systems. In Egypt, a wide tariff spread coupled with ambiguous customs procedures introduces budgetary unpredictability. However, e-bus pilots in Cairo signal a strong appetite for fleets, contingent on easing fiscal hurdles. Morocco's impressive cell output positions it as a key regional export hub. Yet, with domestic EV incentives trailing, local fluid sales remain confined to OEM-fill. In frontier markets like Kenya and Nigeria, the need for validated anti-counterfeit packaging and distribution strategies focused on fleets is paramount, given the challenges of weak regulatory enforcement.

Mordor Intelligence tracks the electric vehicle (ev) fluids market across other major regions such as North America, Europe, and Asia.

Competitive Landscape

The Middle-east and Africa electric vehicle (EV) fluids market is moderately consolidated. Competitive levers pivot on sub-10 µS/cm conductivity expertise, regional blending capacity to sidestep tariffs, and OEM co-development contracts that lock in design wins for next-gen platforms. Niche innovators like Engineered Fluids concentrate on immersion chemistries for logistics depots, avoiding crowded glycol segments. Strategic partnerships span additive suppliers, thermal-system integrators, and gigafactory operators, underscoring that future advantage rests on cross-disciplinary engineering rather than volume scale alone.

Middle-East And Africa Electric Vehicle (EV) Fluids Industry Leaders

Shell plc

TotalEnergies

Exxon Mobil Corporation

Saudi Arabian Oil Co.

BP plc (Castrol)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ENOC Company rolled out Elektra, a portfolio of EV and hybrid fluids, and unveiled revamped packaging aimed at anti-counterfeit assurance.

- June 2025: BP plc (Castrol) announced plans to divest its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion asset sale program.

Middle-East And Africa Electric Vehicle (EV) Fluids Market Report Scope

EV fluids are lubricants that have been designed and developed specifically to suit the needs of electric vehicles. EV fluids keep the electric vehicle's powertrain and transmission system cool. The functions of the EV fluid include heat transfer, lubrication of EV parts, energy loss reduction, and improving the transmission system. The Middle-east and Africa electric vehicle (EV) fluids market is segmented by product type, propulsion type, vehicle type, and geography. By product type, the market is segmented into coolants, engine oils, transmission fluids, greases, and other fluids. By propulsion type, the market is segmented into battery electric vehicles (BEVs), hybrid electric vehicles (HEVs), and plug-in hybrid electric vehicles (PHEVs). By vehicle type, the market is segmented into passenger vehicles and commercial vehicles. The report also covers the market size and forecasts for the electric vehicle (EV) fluids market in 2 countries across the Middle-east and Africa region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Coolants |

| Engine Oils |

| Transmission Fluids |

| Greases |

| Other Fluids (Brake, Dielectric, Waterless) |

| Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Passenger Vehicles |

| Commercial Vehicles |

| Saudi Arabia |

| South Africa |

| Rest of Middle-East and Africa |

| By Product Type | Coolants |

| Engine Oils | |

| Transmission Fluids | |

| Greases | |

| Other Fluids (Brake, Dielectric, Waterless) | |

| By Propulsion Type | Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| By Geography | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

What is the current value of the Middle-east and Africa electric vehicle (EV) fluids market?

The Middle-east and Africa electric vehicle (EV) fluids market size is expected to reach USD 18.41 million by 2025.

What is the projected value of the Middle-east and Africa electric vehicle (EV) fluids market by 2030?

The market is forecast to reach USD 31.19 million by 2030, expanding at an 11.12% CAGR.

Which product category currently leads demand for EV fluids in MEA?

Coolants dominate, accounting for 42.17% of 2024 revenue due to the extreme thermal loads in desert duty cycles.

Why are 800-V architectures important for fluid suppliers?

They demand ultra-low-conductivity coolants below 10 µS/cm, driving innovation in synthetic ester-based dielectric fluids.

Which segment is expected to post the fastest growth through 2030?

Transmission fluids, fueled by the adoption of multi-speed e-axles in commercial vehicles, will grow at a 12.18% CAGR.

Page last updated on: