Middle East and Africa Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

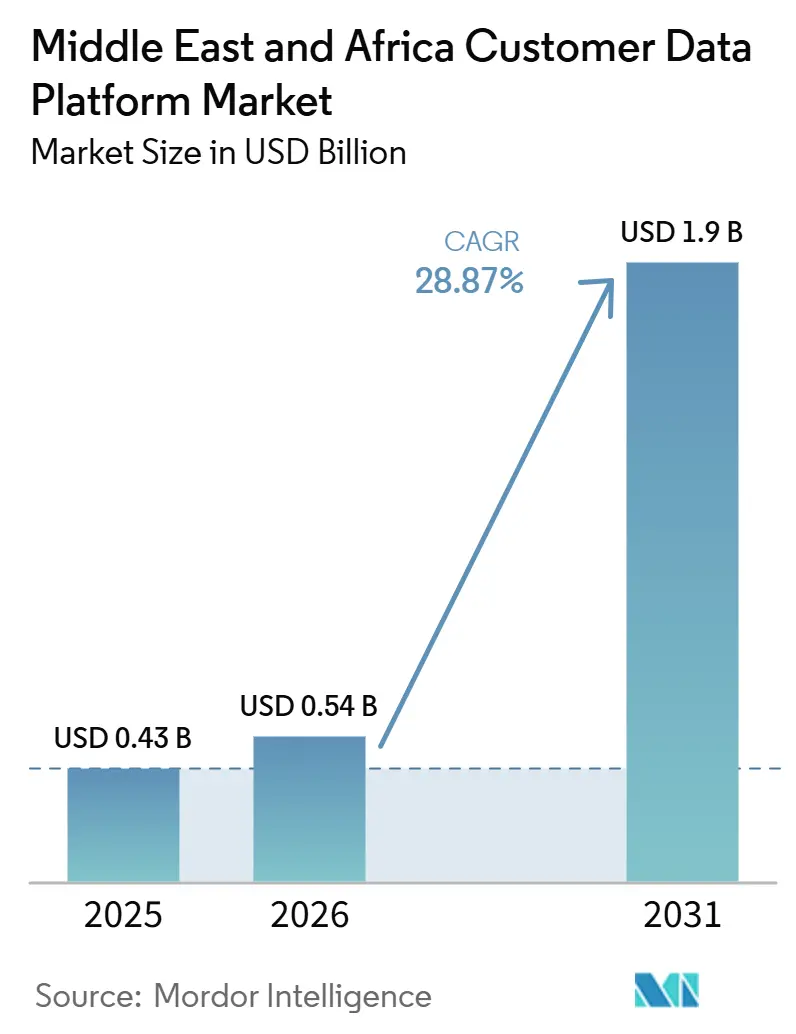

| Base Year Market Size (2025) | USD 0.43 Billion |

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 28.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Customer Data Platform Market Analysis by Mordor Intelligence

The Middle East and Africa customer data platform market size is projected to expand from USD 0.43 billion in 2025 and USD 0.54 billion in 2026 to USD 1.90 billion by 2031, registering a CAGR of 28.87% between 2026 and 2031. Growth is being sustained by telecom operators that are turning 5G subscriber data into monetization programs, pushing CDP adoption beyond marketing use cases into broader commercial operations. Cloud-first modernization across retail and banking is also accelerating demand, as enterprises move customer identity, consent, and engagement data into unified environments that can support faster decision-making. The shift toward first-party data strategies is further strengthening adoption, as enterprises now need durable customer records that can support personalization without relying on third-party tracking. Demand in this region is also coming from technology, operations, and data teams, especially in telecom and BFSI, where real-time identity resolution across multiple products has become a practical requirement. Infrastructure gaps, integration complexity, and skills shortages continue to slow deployment in parts of Africa, but national cloud and digital transformation programs across key countries are supporting the long-term expansion of the market.

Key Report Takeaways

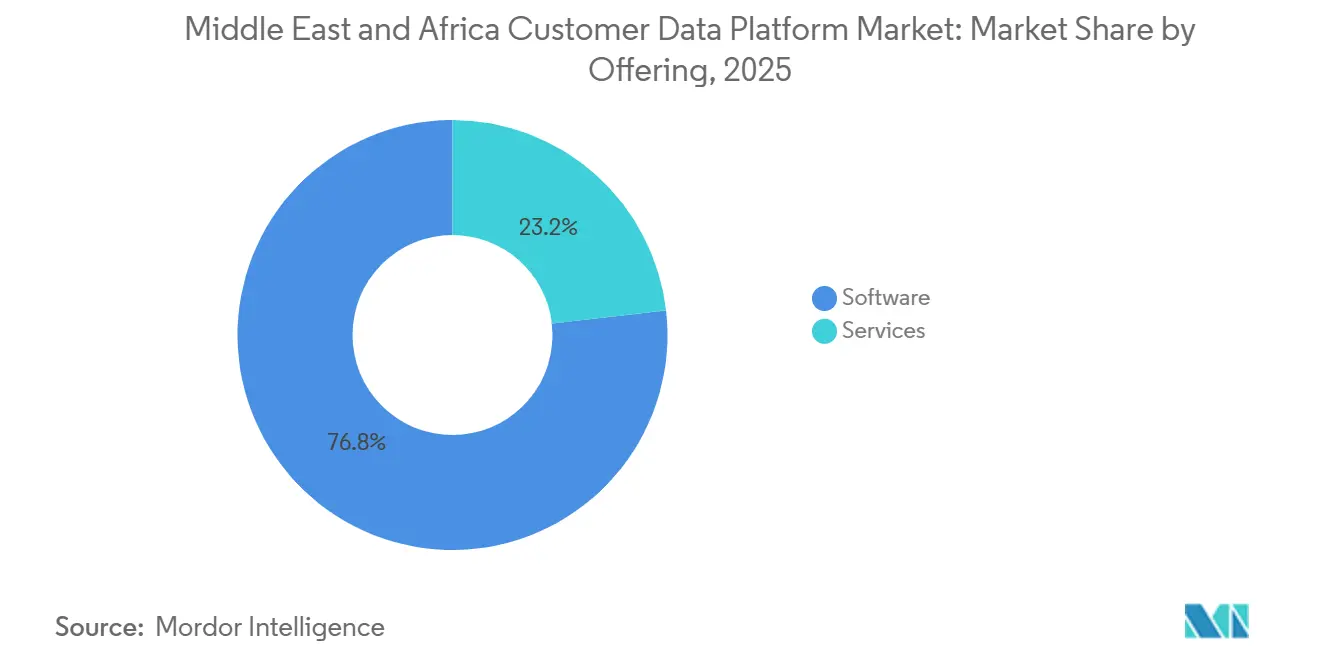

- By offering, software held 76.82% share in 2025, while services are projected to expand at a 30.96% CAGR through 2031.

- By deployment mode, cloud accounted for a 69.18% share in 2025 and is also projected to record the fastest CAGR of 31.54% through 2031.

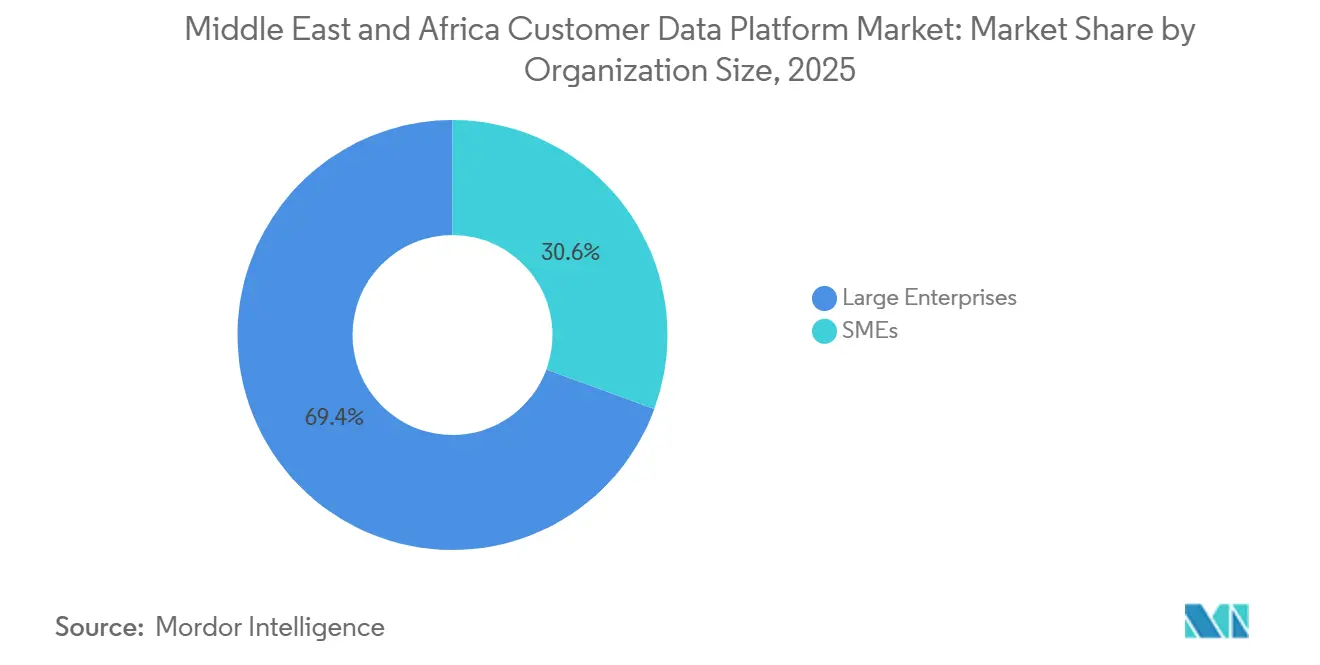

- By organization size, large enterprises led with 69.41% share in 2025, while SMEs are projected to advance at a 31.86% CAGR through 2031.

- By application, customer data collection and profile unification accounted for 28.73% of the market share in 2025, while customer analytics and insights are projected to grow at a 32.48% CAGR through 2031.

- By end-user industry, BFSI held 23.18% share in 2025, while healthcare and life sciences are projected to expand at a 33.27% CAGR through 2031.

- By geography, Saudi Arabia held 28.64% of the Middle East and Africa customer data platform market share in 2025, while the United Arab Emirates is projected to grow at a 33.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Telco 5G Monetization in the Middle East | +5.8% | UAE, Saudi Arabia, Qatar, Kuwait | Short term (≤ 2 years) |

| Cloud-First Customer Identity Consolidation Across Retail and BFSI | +4.9% | Saudi Arabia, UAE, Turkey, South Africa | Medium term (2-4 years) |

| Growth of Real-Time Personalization Across Omnichannel Journeys | +4.2% | UAE, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Warehouse-Native Activation Reducing Data Movement Costs | +3.6% | UAE, Turkey | Medium term (2-4 years) |

| AI-Assisted Audience Segmentation and Next-Best-Action Orchestration | +3.1% | UAE, Saudi Arabia, with wider regional spillover | Long term (≥ 4 years) |

| Consent-Aware First-Party Data Strategies Replacing Third-Party Dependency | +2.7% | UAE, Saudi Arabia, with emerging impact across MEA | Short term (≤ 2 years) and Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Telco 5G Monetization in the Middle East

Telecom operators across the Gulf are using customer data platforms as subscriber intelligence systems rather than as simple campaign tools. This shift matters because 5G monetization depends on a single, governed view of each customer across prepaid, postpaid, business, and digital service relationships. That need gives the Middle East and Africa customer data platform market a durable demand base in telecom, where data activation is tied to new revenue rather than to promotional efficiency alone. It also pulls buying decisions away from a marketing-only model and into network, data, and commercial teams that manage larger transformation budgets. As operators search for non-connectivity revenue, platforms that can unify identity and activate data in real time become more central to execution. The Middle East and Africa customer data platform market, therefore, benefits from a telecom use case that is operational, strategic, and difficult to defer.

Cloud-First Customer Identity Consolidation Across Retail and BFSI

Banks and retailers across the region are moving toward cloud-native customer identity consolidation because years of siloed systems have made service, marketing, and compliance workflows harder to manage. First Abu Dhabi Bank extended its collaboration with Temenos in Saudi Arabia in May 2026 to modernize core banking, payments, and data hub capabilities on cloud infrastructure, which reflects the wider push toward a unified customer view.[1]Temenos, “First Abu Dhabi Bank Extends Collaboration with Temenos to Modernize Banking in Saudi Arabia,” Temenos Press Release, temenos.com Once institutions place customer records, transaction context, and service interactions into connected cloud environments, CDP adoption becomes easier to justify on both operational and regulatory grounds. Local cloud expansion in Saudi Arabia and the United Arab Emirates has also reduced a key barrier for enterprises that were previously unwilling to move customer data workloads off older infrastructure. That change has made local hosting, low latency, and governance support basic procurement expectations rather than premium features. The Middle East and Africa customer data platform market is therefore gaining momentum from both business simplification and compliance readiness.

Growth of Real-Time Personalization Across Omnichannel Journeys

The push for real-time personalization is growing because customer journeys in the region span apps, stores, messaging channels, and service touchpoints. Enterprises need the current customer context to decide which message, offer, or service action to take next, and static campaign logic is becoming less effective in this setting. This has raised the value of CDPs that can connect identity resolution with fast activation across digital and physical channels. Adobe’s January 2026 research in the Middle East showed that enterprises were moving quickly on AI, cloud infrastructure, and customer experience, but still faced execution and measurement gaps, which supports the case for stronger customer data foundations. As companies try to close those gaps, they are shifting attention from simple data collection to data that supports timely decisions and more relevant engagement. The Middle East and Africa customer data platform market is benefiting from that change because real-time personalization needs a governed customer layer before AI tools can deliver consistent results.

Warehouse-Native Activation Reducing Data Movement Costs

Warehouse-native activation is becoming increasingly relevant as many enterprises seek to use customer data where it already resides rather than duplicate it into another proprietary system. This model reduces unnecessary data movement, which helps with governance and can lower implementation effort for organizations that have already invested in cloud data platforms. It also fits buyers who want activation capability without taking on the full operational burden of a traditional enterprise deployment. For the Middle East and Africa customer data platform market, what matters most is in countries where cost control and integration complexity can delay decisions. A warehouse-connected approach can make adoption more practical for mid-sized enterprises that need measurable business value without a long transformation cycle. This trend does not replace packaged platforms, but it expands the set of architectural choices available to buyers across the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Data Residency-Ready Cloud Infrastructure in Parts of Africa | -3.8% | Sub-Saharan Africa, Egypt, North Africa | Long term (≥ 4 years) |

| High Integration Complexity Across Legacy MarTech and CRM Stacks | -3.2% | Turkey, South Africa, Egypt, with wider relevance across MEA | Medium term (2-4 years) |

| Skills Shortage for CDP Governance, Identity Resolution, and Activation | -2.5% | MEA-wide, most acute in Egypt and sub-Saharan Africa | Long term (≥ 4 years) |

| Budget Sensitivity Among Small and Medium Enterprises in Emerging Markets | -2.1% | Egypt, sub-Saharan Africa, Turkey | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Data Residency-Ready Cloud Infrastructure in Parts of Africa

The biggest infrastructure constraint in several African markets is not software availability but the lack of cloud environments that can support local data-residency expectations at scale. That slows enterprise adoption because regulated customer data cannot be moved freely when compliance requirements are stricter than local infrastructure capacity. Nigeria’s National Cloud Policy 2025 formalized this challenge by pushing sensitive data in sectors such as finance, healthcare, and government toward domestic storage expectations.[2]National Information Technology Development Agency, “National Cloud Policy 2025,” National Information Technology Development Agency, nitda.gov.ng As a result, some enterprises can procure a platform but still struggle to deploy it in a way that satisfies internal governance and sector oversight. This keeps near-term demand more concentrated in Gulf markets and in better-served African hubs. The Middle East and Africa customer data platform market, therefore, remains uneven, with infrastructure readiness acting as a practical filter on where cloud-led adoption can scale first.

High Integration Complexity Across Legacy MarTech and CRM Stacks

Integration complexity remains a major restraint because many enterprises still operate with disconnected CRM, ERP, commerce, and service systems built over long procurement cycles. A CDP only creates value when those systems can exchange data cleanly, and that usually requires common definitions, stable connectors, and better data quality than many organizations currently have. IBM research in the Middle East and Africa found that only 27% of regional chief data officers were confident in their organization’s ability to derive business value from unstructured data, reflecting the broader readiness gap in integration work.[3]IBM Institute for Business Value, “MEA IBV CDO Study 2025,” IBM Newsroom Middle East and Africa, mea.newsroom.ibm.com When source systems define the same customer or event differently, the platform can reproduce fragmentation rather than remove it. That lengthens implementation cycles and erodes confidence in early returns. The Middle East and Africa customer data platform market still has strong momentum, but this integration burden remains one of the main reasons why procurement decisions do not always convert into rapid production scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads Platform Demand While Services Deepen Execution

Software accounted for 76.82% of the Middle East and Africa customer data platform market share in 2025, which shows the strong preference for packaged platforms over custom-built customer data layers. Large telecom operators, banks, and retail groups have generally favored software-led deployments because they provide identity resolution, audience building, and activation tools without long internal development cycles. That approach fits a region where digital transformation timelines are moving quickly and where buyers often want visible operational outcomes soon after deployment. The software segment also benefits from enterprise demand for standard governance controls, prebuilt connectors, and platform support across multiple business units. In the Middle East and Africa customer data platform market, software therefore remains the anchor of adoption because it lowers technical friction for organizations that need scale, reliability, and speed at the same time.

Services is projected to grow at a 30.96% CAGR from 2026 to 2031, which makes it the fastest-expanding offering in the regional market. This growth reflects the fact that many deployments still need local customization around language, consent workflows, sector rules, and existing enterprise architecture. Regional buyers often need implementation support that goes well beyond setup, especially when CDPs must connect to banking cores, telecom systems, or complex retail stacks. Salesforce reinforced that services-led model in February 2025 through its USD 500 million investment in Saudi Arabia and its partner ecosystem expansion, which signaled that in-country delivery depth would matter as much as product breadth.[4]Salesforce, “Salesforce Invests $500M in Saudi Arabia,” Salesforce Newsroom, salesforce.com NTT DATA also expanded Salesforce capabilities across East Africa in June 2026, which showed that systems integration capacity is becoming a direct enabler of adoption across the broader Middle East and Africa customer data platform market.[5]NTT DATA, “NTT DATA Expands Salesforce Capabilities in East Africa to Help Organisations Improve Client Engagement and Growth,” NTT DATA Newsroom, services.global.ntt

By Deployment Mode: Cloud Becomes the Standard While Hybrid Remains a Bridge

Cloud accounted for 69.18% of the Middle East and Africa customer data platform market size in 2025, and it is also projected to record the fastest CAGR of 31.54% through 2031. That mix shows that cloud is not only the dominant deployment mode, but also the one still gaining momentum fastest. National digital strategies, local hosting expansion, and the need for faster implementation have all favored cloud adoption in the region. On-premises deployments continue to matter in government, defense-adjacent, and top-tier financial environments where internal control over infrastructure remains critical. Hybrid models also retain importance because many enterprises are still moving from older on-premises estates toward cloud-native operating models in stages rather than through a single transition.

Cloud growth has been helped by the simple fact that local data center availability in Saudi Arabia and the United Arab Emirates has reduced one of the biggest objections to customer data migration. Once enterprises are confident that data can remain in-country while still benefiting from cloud scale, CDP adoption becomes easier to approve across legal, technology, and operations teams. The market has therefore shifted from debating whether cloud should be used toward deciding which hosting model best supports sovereignty, latency, and AI readiness. This is especially important in the Middle East and Africa customer data platform market because cloud choice now shapes not only cost and speed, but also the viability of regulated use cases. As a result, vendors without a clear regional hosting and governance story face a growing disadvantage against competitors that can meet local infrastructure expectations with less complexity.

By Organization Size: Large Enterprises Hold Revenue While SMEs Accelerate Faster

Large enterprises held 69.41% share of the Middle East and Africa customer data platform market in 2025, reflecting the complexity of their customer environments and the higher urgency of data unification at scale. Conglomerates in telecom, banking, and retail often manage multiple brands, channels, and jurisdictions, which makes a governed identity layer essential rather than optional. In these settings, a CDP supports not only marketing but also customer service consistency, consent management, analytics, and cross-sell execution. Larger organizations also have the budgets and internal teams needed to run longer platform programs with multiple integrations. The Middle East and Africa customer data platform market has therefore depended heavily on large-enterprise demand during the current phase of adoption.

SMEs are projected to grow at a 31.86% CAGR through 2031, which shows that the adoption base is widening beyond top-tier enterprises. Cloud-native delivery has reduced upfront infrastructure needs, and smaller organizations can now access customer data tools that once required much larger technology budgets. This change is especially visible in digital commerce and retail, where smaller brands are under pressure to improve personalization and retention as customer expectations rise. The result is a faster move from basic CRM use toward more structured identity, segmentation, and activation capabilities. In the Middle East and Africa customer data platform market, that SME acceleration matters because it broadens the addressable customer base and makes growth less dependent on a small pool of very large contracts.

By Application: Profile Unification Builds the Base While Analytics Drives the Next Stage

Customer data collection and profile unification accounted for 28.73% of the market share in 2025, making it the largest application, as many enterprises are still grappling with fragmented customer records. Years of separate CRM, service, commerce, and campaign systems created duplicate profiles and inconsistent engagement logic, so unification remains the first practical priority. Audience segmentation and personalization, journey orchestration, and consent and preference management all build on that foundation. This means application demand is moving in sequence, with data capture and identity resolution still leading before broader activation scales. In the Middle East and Africa customer data platform market, the current application mix shows that many organizations remain in the platform-building stage, even as more advanced use cases are emerging.

Customer analytics and insights are projected to grow at a 32.48% CAGR through 2031, which signals a shift from data consolidation toward data-led decisioning. As enterprises gain cleaner customer records, they can move into churn modeling, next-best-action logic, and more predictive engagement planning. That transition also raises the importance of consent and data quality, because analytics only creates value when usable data can be activated within policy limits. IBM research showed that only 25% of chief data officers in the Middle East and Africa felt confident that their data could support AI-enabled revenue streams, which explains why advanced analytics is growing fast but still requires stronger data readiness. The Middle East and Africa customer data platform market is therefore entering a stage where analytics growth depends as much on governance and trust as it does on modeling capability.

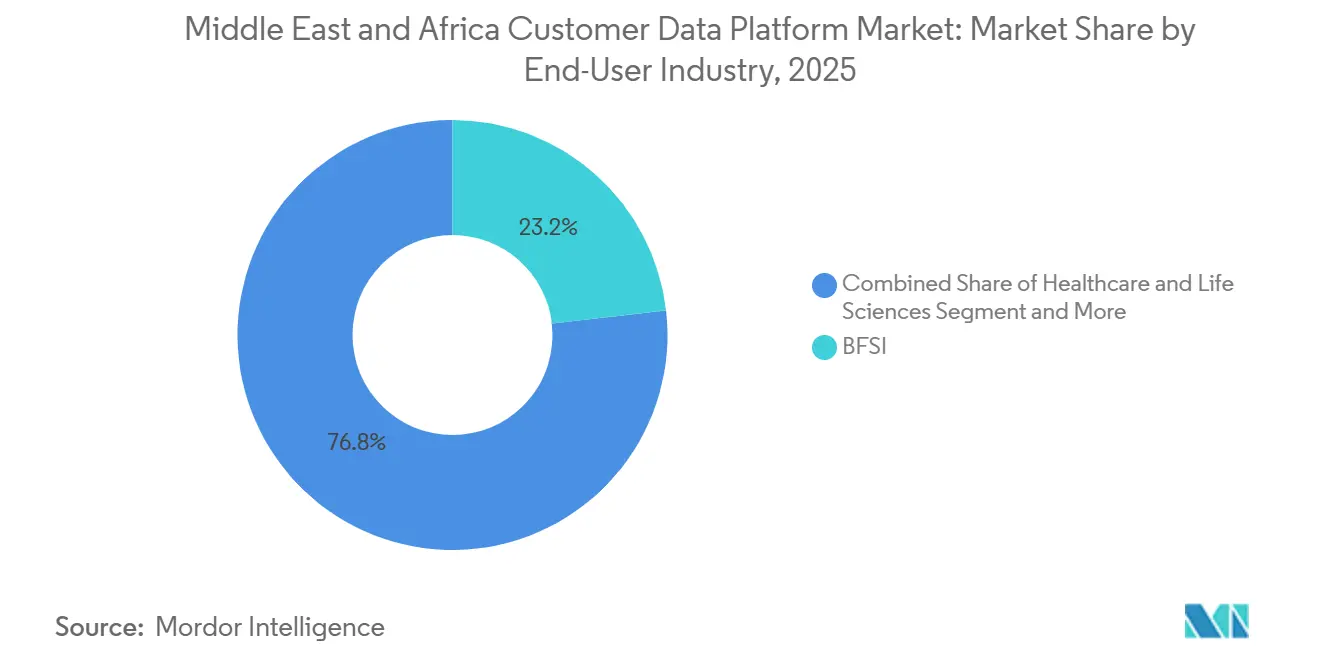

By End-User Industry: BFSI Anchors Current Demand While Healthcare and Life Sciences Rises Fast

BFSI held 23.18% share in 2025, which made it the largest end-user industry in the regional market. Financial institutions manage high-value customer relationships, multiple product lines, and strict governance demands, so they have a stronger immediate case for unified customer data than many other sectors. CDPs in this segment support churn reduction, cross-sell planning, fraud-related pattern visibility, and more consistent service interactions across channels. Open banking initiatives and stronger data protection requirements have also pushed banks to improve the way they structure and govern customer records. In the Middle East and Africa customer data platform market, BFSI has therefore become the clearest example of CDP adoption as both a growth tool and a compliance tool.

Healthcare and life sciences is projected to grow at a 33.27% CAGR through 2031, which makes it the fastest-expanding end-user vertical. Digital health programs in Saudi Arabia and the United Arab Emirates are improving the underlying data environment needed for patient-level engagement, outreach, and service continuity. Retail and e-commerce remain important contributors as well, because high competition and rising digital activity keep pressure on customer experience performance. Government and public administration is also emerging as a meaningful demand area as digital identity and citizen data programs increase the need for governed profile management. This wider end-user mix strengthens the Middle East and Africa customer data platform market because adoption is no longer tied to one or two traditional commercial sectors alone.

Geography Analysis

Saudi Arabia held a 28.64% share of the Middle East and Africa customer data platform market in 2025, making it the largest country market in the region. The country’s leadership position reflects large enterprise technology spending, national digital transformation priorities, and a stronger focus on data governance across major sectors. Salesforce announced a USD 500 million investment in Saudi Arabia in February 2025, including the deployment of Hyperforce on Amazon Web Services to support local data residency and a commitment to train 30,000 Saudi citizens in AI, which reinforced the country’s role as a leading demand center for enterprise customer data platforms. The United Arab Emirates is projected to grow at a 33.94% CAGR through 2031, which makes it the fastest-growing country market in the region. Its momentum comes from strong enterprise digitization, mature cloud readiness, and a compliance environment that is converting delayed evaluations into active procurement.

Turkey and South Africa represent the next tier of opportunity, but for different reasons. Turkey benefits from a large domestic consumer base, strong commerce activity, and cross-sector demand in retail, telecom, and financial services, which supports steady CDP adoption. South Africa remains the most established market in sub-Saharan Africa because of its stronger enterprise technology base and deeper compliance focus in financial services and digital commerce. NTT DATA’s 2025 acquisition of EXAH in South Africa, followed by its East Africa expansion in June 2026, showed that implementation capacity is scaling alongside regional demand.

Egypt and the rest of the regional market are earlier-stage, but they remain strategically important for long-term expansion. Egypt has a large consumer base, an active fintech environment, and growing digital commerce activity, though infrastructure and budget constraints lengthen adoption cycles compared with Gulf markets. Across other parts of Africa, mobile-first commerce and telco-led data models offer practical entry points for CDP use. Nigeria’s National Cloud Policy 2025 also points to a broader infrastructure buildout path that should support more compliant data hosting over time.

Competitive Landscape

The Middle East and Africa customer data platform market is moderately fragmented, with global enterprise software vendors and specialist CDP firms competing on different strengths. Salesforce, Oracle, Adobe, and SAP SE remain well-positioned in large enterprise accounts because their customer data tools connect naturally with existing CRM, ERP, commerce, and marketing estates. That installed-base advantage is especially powerful in banking, telecom, and large retail, where switching costs are higher and integration depth matters early in the buying process. At the same time, specialist vendors have been gaining attention by offering more flexible deployment models, stronger localization, and faster activation paths for specific use cases. The Middle East and Africa customer data platform market, therefore, does not exhibit winner-take-all behavior because both broad platform breadth and specialist execution remain commercially relevant.

Several strategic moves in 2025 and 2026 showed that vendors are trying to strengthen their regional positions. Salesforce operationalized its Saudi strategy in November 2025 by formally launching its regional headquarters in Riyadh, following an earlier USD 500 million investment that improved its local delivery profile and ecosystem depth. NTT DATA expanded its Salesforce capabilities across East Africa in June 2026, signaling that systems integration capacity is becoming a competitive differentiator rather than a support function. Tealium’s collaboration with Amazon Web Services on UAE-hosted infrastructure also strengthened its position with Gulf enterprises that place a premium on local hosting and alignment with compliance requirements.

The competitive field is also being shaped by architecture choices rather than by branding alone. Packaged platforms remain attractive to buyers who want broad functionality and bundled integration with existing enterprise stacks. Warehouse-connected and composable approaches appeal to organizations that have already invested heavily in cloud data platforms and want tighter control over how data moves and is activated. In the Middle East and Africa customer data platform market, this means vendors are competing on implementation fit, data governance credibility, local ecosystem strength, and AI readiness as much as on core CDP features.

Middle East and Africa Customer Data Platform Industry Leaders

Salesforce, Inc.

Oracle Corporation

Adobe Inc.

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NTT DATA expanded Salesforce capabilities across East Africa, deploying Agentforce Financial Services, Agentforce Marketing, MuleSoft, and Data 360 in Kenya's financial services and fintech market, following its 2025 acquisition of EXAH, a Salesforce Consulting Partner in South Africa. The expansion extends CDP and AI-powered data management services to East Africa, where NTT DATA joined Salesforce's Forward Deployed Engineering Partner Network to accelerate Agentforce deployment at scale.

- April 2026: Salesforce launched Headless 360 in the Middle East, enabling enterprises to access the full depth of its Data Cloud and CRM capabilities through APIs and Model Context Protocol connectors without requiring user interface navigation. The launch positions Salesforce's platform as a programmable data backbone for agentic enterprise architectures across the region, with the Testing Center and Salesforce Catalog scheduled for release in mid-2026.

- April 2026: Salesforce made Agentforce available across its full Suites in the Gulf Cooperation Council at no additional cost to small and medium enterprises, removing the technical setup barrier that had previously restricted enterprise-grade AI-powered customer data activation to large organizations, in direct response to GCC governments' accelerating efforts to build private-sector-led, SME-competitive economies.

- January 2026: Adobe held its AI Forum in Riyadh, releasing research showing that Middle East enterprises are rapidly advancing AI, cloud infrastructure, and customer experience investments, but face persistent execution, measurement, and integration gaps that limit their ability to translate digital investment into measurable business impact, insights actively shaping enterprise CDP procurement priorities in the Kingdom.

Middle East and Africa Customer Data Platform Market Report Scope

The Middle East and Africa Customer Data Platform Market is Segmented by Offering (Software and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, and More), End-User Industry (Retail and E-Commerce, BFSI, and More), and Country. The Market Forecasts are in Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| Saudi Arabia |

| UAE |

| Turkey |

| South Africa |

| Egypt |

| Rest of Middle East and Africa |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Country | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the projected size of the Middle East and Africa customer data platform market by 2031?

The Middle East and Africa customer data platform market is projected to reach USD 1.90 billion by 2031, rising from USD 0.54 billion in 2026 at a 28.87% CAGR.

Which offering leads regional demand for customer data platforms?

Software led the market in 2025 with a 76.82% share, reflecting strong demand for packaged platforms that can unify customer data and support activation without heavy in-house development.

Which deployment mode is expanding the fastest across the region?

Cloud is both the largest and fastest-growing deployment mode, with a 69.18% share in 2025 and a projected 31.54% CAGR through 2031.

Why does BFSI lead customer data platform adoption in this region?

BFSI held a 23.18% share in 2025 because banks and financial institutions need unified customer records for cross-sell, retention, fraud visibility, and compliance-led data governance.

Which countries are shaping the next phase of growth?

Saudi Arabia led with a 28.64% share in 2025, while the United Arab Emirates is projected to grow the fastest at a 33.94% CAGR through 2031.

What are the main barriers slowing adoption in parts of the region?

The main barriers are limited data residency-ready cloud infrastructure in parts of Africa, high integration complexity across older enterprise systems, skills shortages, and budget sensitivity among SMEs.

Page last updated on: