Middle East and Africa Commercial Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

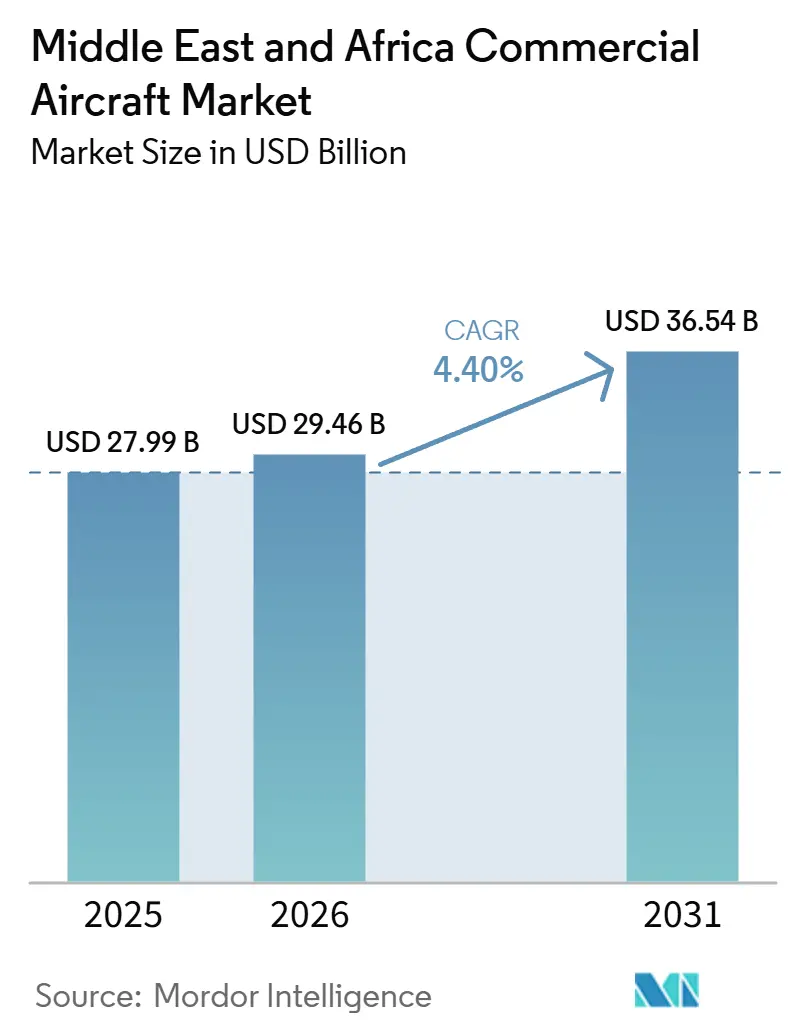

| Base Year Market Size (2025) | USD 27.99 Billion |

| Market Size (2026) | USD 29.46 Billion |

| Market Size (2031) | USD 36.54 Billion |

| Growth Rate (2026 - 2031) | 4.40% CAGR |

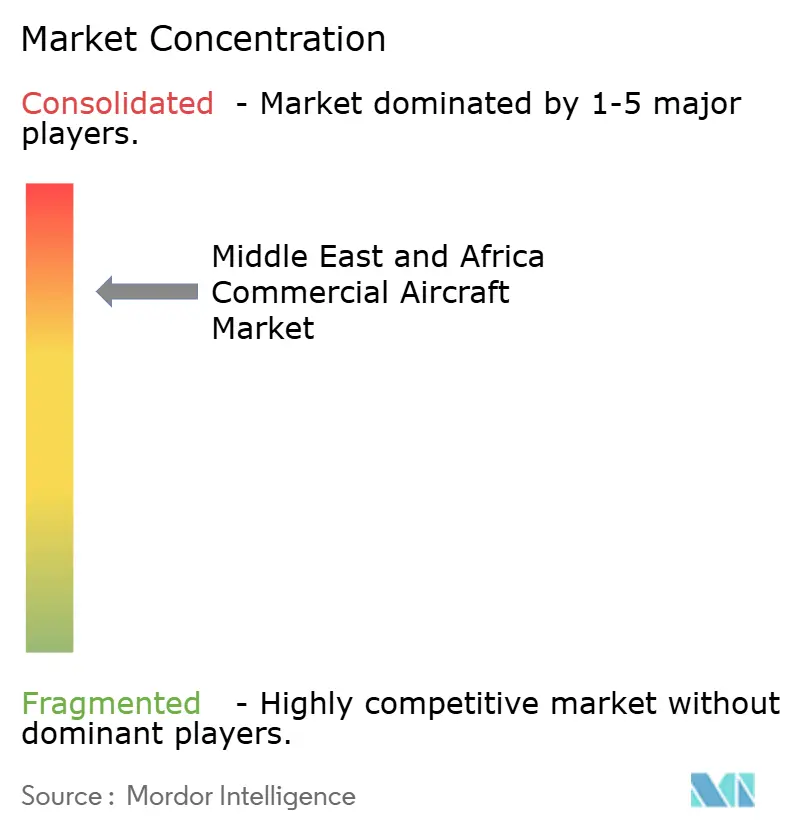

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Commercial Aircraft Market Analysis by Mordor Intelligence

The Middle East and Africa commercial aircraft market size is expected to grow from USD 27.99 billion in 2025 to USD 29.46 billion in 2026, and is forecasted to reach USD 36.54 billion by 2031 at a 4.40% CAGR over 2026-2031. The market is moving away from crisis-era fleet conservation and toward planned fleet expansion that is tied to national aviation agendas, airport build-out, and longer route development cycles. Demand remains anchored in two parallel patterns: Gulf carriers adding aircraft to large hub systems, and African airlines adding smaller, more flexible capacity to thinner domestic and regional routes. According to Boeing's Commercial Market Outlook published in 2025, Middle East airlines will require 2,950 new aircraft deliveries between 2025 and 2044, including 1,430 single-aisle jets and 1,370 widebody jets, which supports the long replacement cycle now evident across the region.[1]Boeing, “Boeing Middle East Airlines Enter New Era of Growth as Region's Fleet Will More Than Double by 2044,” Boeing Investor Relations, investors.boeing.com The Middle East and Africa commercial aircraft market is also being shaped by uneven access to financing, delivery availability, and airport readiness across sub-regions. That mix keeps opportunity high, but it also means growth is likely to remain concentrated among carriers and countries that can simultaneously secure aircraft, capital, and operating infrastructure.

Key Report Takeaways

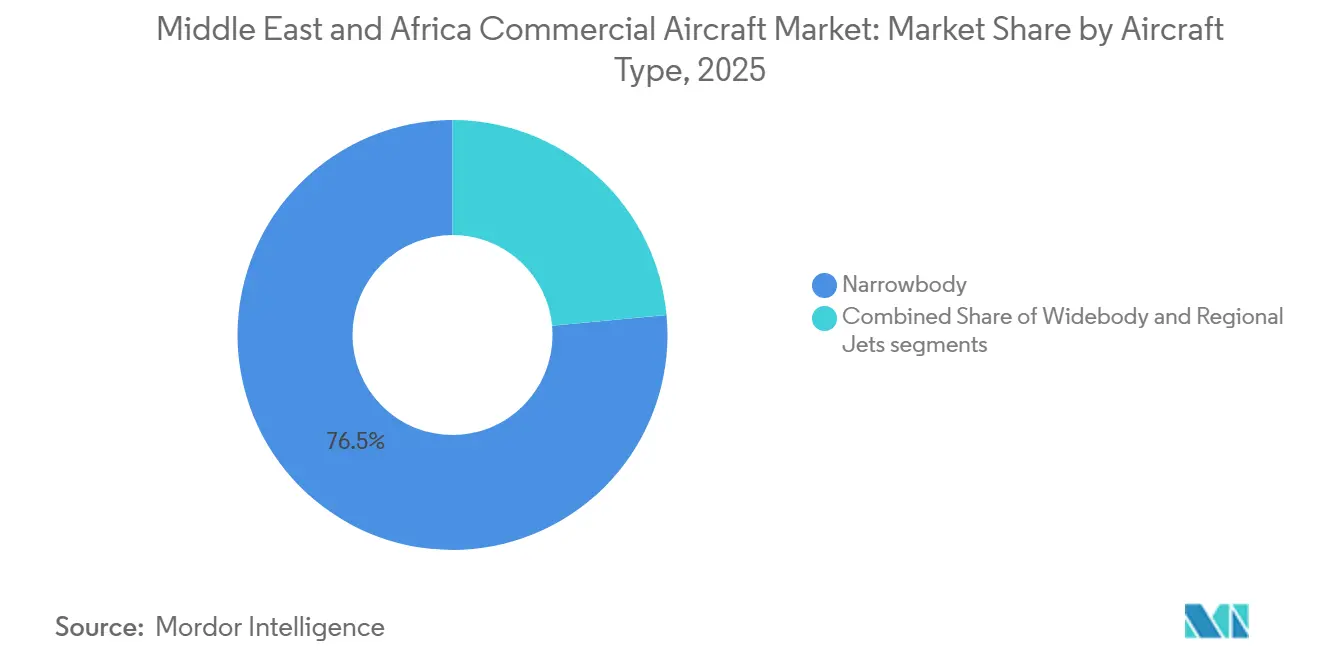

- By aircraft type, narrowbody aircraft held 76.49% of the Middle East and Africa commercial aircraft market share in 2025, and are also projected to grow at a 5.65% CAGR through 2031.

- By application, passenger aircraft accounted for 90.34% of the market in 2025, and are projected to expand at a 5.35% CAGR through 2031.

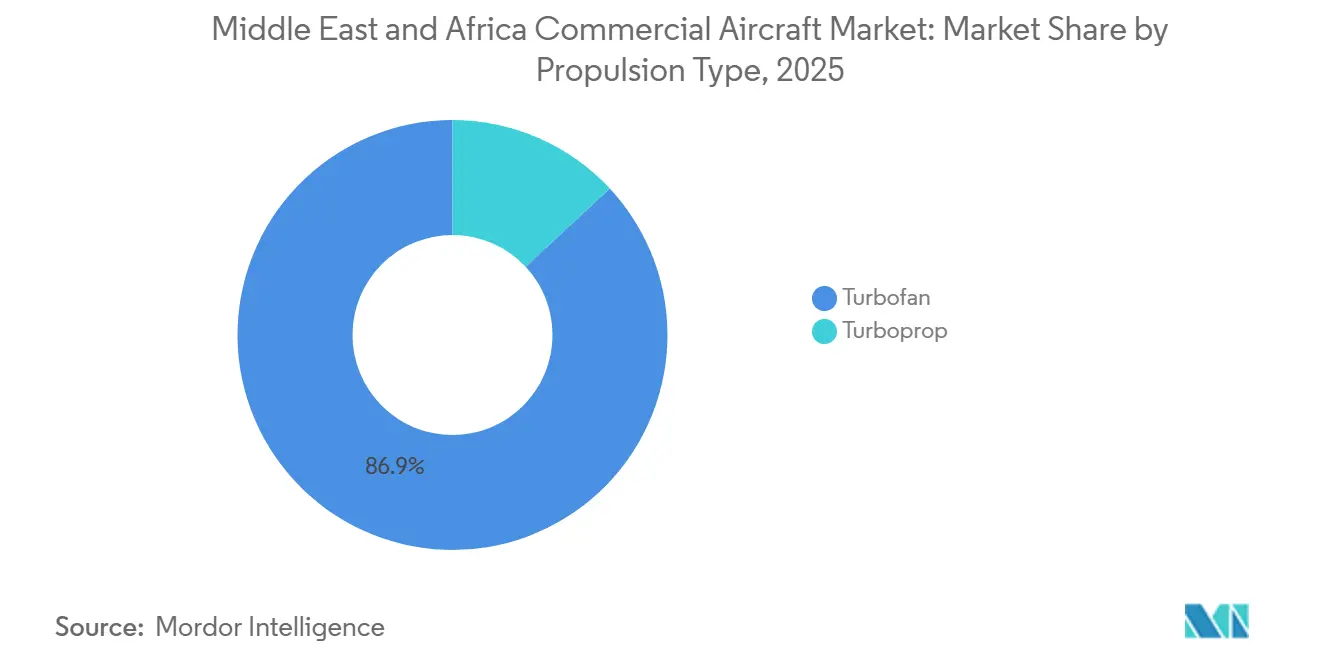

- By propulsion type, turbofan aircraft accounted for 86.94% of the market in 2025, while turboprop aircraft are forecast to grow at a 6.01% CAGR through 2031.

- By component, airframe structures held 28.08% of the market in 2025, while avionics and flight control are projected to grow at a 5.23% CAGR through 2031.

- By geography, the Middle East accounted for 52.41% of the market in 2025, while Africa is forecast to grow at a 6.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Commercial Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fleet replacement cycles across GCC carriers | +1.20% | GCC core, Saudi Arabia, UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Expansion of low-cost and narrowbody networks | +1.00% | Saudi Arabia, UAE, South Africa, East Africa | Short term (≤ 2 years) |

| Growth in sixth-freedom hub traffic through the Gulf countries | +0.80% | UAE, Qatar, with spillover to Bahrain and Oman | Medium term (2-4 years) |

| Cargo capacity addition for e-commerce and perishables | +0.50% | UAE, Qatar, Egypt, Nigeria, Ethiopia | Medium term (2-4 years) |

| CORSIA and fuel-burn pressure accelerating new aircraft uptake | +0.40% | GCC core, with compliance spillover to North and East Africa | Long term (≥ 4 years) |

| Thin-route expansion in Africa requiring right-sized aircraft | +0.30% | Sub-Saharan Africa, particularly DRC, Ethiopia, Algeria, and domestic routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Fleet Replacement Cycles Across GCC

GCC airlines entered 2025 with a stronger case for renewal than for life extension, which is lifting procurement activity across the Middle East and Africa commercial aircraft market. flydubai signed a landmark agreement for 150 A321neo aircraft in November 2025, becoming a new Airbus customer through that order. The change is important because replacement is no longer tied solely to aircraft age but also to fuel efficiency, seat economics, and the need to match competitors' fleets on cost per trip. Saudia Group also disclosed an order for 10 A330-900 aircraft for flyadeal in April 2025, indicating that renewal in the Gulf is broadening from simple narrowbody replacement to longer-haul network planning. As a result, the Middle East and Africa commercial aircraft market is seeing replacement cycles accelerate rather than waiting until the late 2020s.

Growth In Sixth-Freedom Hub Traffic

Widebody demand in the Gulf still rests on the long-standing hub model that channels passengers through a few large transfer airports, and that continues to support the Middle East and Africa commercial aircraft market. Boeing said in 2025 that Middle East airlines will need 1,370 widebody jets by 2044, which is one of the clearest signs that long-haul hub traffic still matters deeply in regional fleet planning. Saudi Arabia is also pushing a larger aviation build-out under Vision 2030, with a target of reaching 330 million annual air passengers by 2030 through airport modernization and airline development. That policy direction supports future fleet growth not only for flagship carriers but also for new capacity platforms designed to compete for intercontinental flows. The result is a market where narrowbody expansion in domestic and regional systems can sit alongside continued widebody investment for long-haul transfer traffic.

Expansion Of Low-Cost And Narrowbody Networks

Low-cost carrier (LCC) growth is changing the aircraft mix in the Middle East and Africa commercial aircraft market, especially by strengthening the case for high-frequency narrowbody operations. Boeing projected that LCC seat capacity in the Middle East would reach nearly 25% of the regional total by 2044, indicating a larger role for single-aisle fleets over time.[2]Boeing, “Boeing Africa's Rising Passenger Air Traffic Will Spur Region's Fleet to More Than Double by 2044,” Boeing Newsroom, boeing.mediaroom.com In Africa, Boeing also stated that 70% of new commercial deliveries through 2044 are expected to be single-aisle aircraft, which supports the same narrowbody-led pattern from a different starting point, as the African LCC and regional operators are not just adding direct point-to-point services; they are also creating feeder traffic that can support Gulf hub connectivity over time. That link between local route development and long-haul transfer viability keeps narrowbodies central to demand across both sub-regions.

Cargo Capacity Addition For E-Commerce And Freight

Cargo is a smaller part of fleet value than passenger activity. However, it still supports demand for commercial aircraft in the Middle East and Africa through route viability and utilization economics. IATA reported that African airlines recorded 6% year-on-year growth in air cargo demand in 2025, making Africa the fastest-growing regional cargo market that year.[3]International Air Transport Association, “Global Air Cargo Demand Achieved Record Volume in 2025,” IATA Press Release, iata.org That growth matters because freight revenue can improve the route economics of aircraft that would otherwise rely solely on passenger yields. It also supports the case for mixed passenger and cargo fleet planning, especially where long sectors or lower frequencies make full utilization harder to achieve. In practice, cargo growth strengthens the demand case for both freighter and passenger aircraft with useful belly cargo capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aircraft delivery backlogs extending fleet renewal timelines | -0.80% | Global, concentrated in GCC and African new-order carriers | Short term (≤ 2 years) |

| USD-denominated financing pressure on African operators | -0.60% | Sub-Saharan Africa, North Africa, Algeria, Tanzania, Mozambique | Medium term (2-4 years) |

| Infrastructure and runway constraints beyond major hubs | -0.40% | Sub-Saharan Africa, secondary cities across the Middle East and Africa | Medium term (2-4 years) |

| Pilot, crew, and simulator capacity shortages | -0.50% | Middle East and East Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aircraft Delivery Backlogs Extending Fleet Renewal Timelines

A major brake on the Middle East and Africa commercial aircraft market is the simple fact that aircraft are harder to obtain on schedule than airlines had expected. Large order queues at major OEMs are stretching renewal timelines, which is especially difficult for carriers trying to modernize quickly or launch new routes with a specific aircraft type. That pushes some operators toward lease extensions, used aircraft, and phased fleet plans instead of the direct transition they originally preferred. The issue matters more in this region because many airlines' strategies are tied to formal expansion programs, so any delivery slippage can also delay route launches, staffing plans, and airport utilization, keeping demand intact but slowing the rate at which that demand converts into active fleet capacity.

USD-Denominated Financing Pressure On African Carriers

Financing pressure remains a structural hurdle for many African operators in the Middle East and Africa commercial aircraft market. Airline revenues are often generated in local currencies, while aircraft leases, maintenance inputs, fuel purchases, and spare parts are largely tied to USD obligations. That mismatch weakens balance sheets, narrows financing options, and reduces room for rapid fleet renewal even when route demand is improving. It also raises leasing risk perception across the continent, which can make pricing less favorable even for operators with relatively stronger fundamentals. The result is a market where growth can be real, but fleet modernization may still arrive in uneven bursts rather than in a steady replacement cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbodies Define the Commercial Architecture

Narrowbody aircraft accounted for 76.49% of the market in 2025, making them the largest aircraft category in the Middle East and Africa commercial aircraft market. The same segment is also projected to record the fastest 5.65% CAGR through 2031, which shows that current fleet leadership is expected to continue rather than reverse. That pattern reflects the operational reality of both sub-regions, where short- and medium-haul flying still accounts for most route activity and where single-aisle economics remain the most flexible. Boeing’s 2025 outlook for the Middle East pointed to 1,430 single-aisle deliveries through 2044, reinforcing the long-term role of narrowbody fleets in regional expansion. Boeing also said that 70% of new African aircraft deliveries through 2044 will be single-aisle aircraft, which supports the same aircraft preference from the African side of the market. The Middle East and Africa commercial aircraft market is therefore being shaped by a dominant fleet logic: adding capacity with aircraft that can serve dense domestic links, regional services, and lower-risk international routes.

Within this category, the A321neo family has taken on a stronger strategic role because airlines can use it across both standard regional missions and longer thin routes. flydubai’s 2025 agreement for 150 A321neo aircraft was one of the clearest signals that narrowbody replacement has become central to fleet strategy in the Gulf. Widebody aircraft still play a necessary role at Gulf transfer hubs, but their role is more concentrated on long-haul trunk routes and intercontinental connectivity. Regional jets remain smaller in value, yet they are relevant in Africa, where some carriers need a step between turboprops and larger narrowbodies. The full picture is a bifurcated narrowbody market, with Gulf operators using aircraft for high-frequency scale and African operators using them as sub-regional connectors where larger aircraft are not economical.

By Application: Passenger Dominance With Freight As a Structural Enabler

Passenger operations accounted for 90.34% of the market in 2025, keeping them far ahead of freighter activity in the Middle East and Africa commercial aircraft market. Passenger aircraft are also projected to grow at a 5.35% CAGR through 2031, making the largest application segment the fastest-growing. That result aligns with the region’s airline structure, where network growth, connectivity goals, and airport investment are still centered mainly on carrying people rather than cargo alone. Boeing projected that Africa’s passenger traffic will grow at 6% annually through 2044, supporting a long runway for airline fleet growth across the continent. The Middle East and Africa commercial aircraft market, therefore, remains heavily passenger-led, even as freight economics become more important in route planning.

Freighter aircraft are much less valuable, but they carry strategic weight by improving network resilience and aircraft utilization. IATA’s report of 6% air cargo growth for African airlines in 2025 showed that freight demand is not a side issue, especially in corridors where cargo revenue helps support thinner schedules. That is why some carriers increasingly view passenger and freight planning together rather than as separate fleet decisions. In practical terms, the freighter sub-segment helps stabilize the broader passenger system by improving revenue quality on routes with less even demand patterns. The Middle East and Africa commercial aircraft market is still dominated by passenger aircraft. Still, cargo has become a more meaningful support layer than its share of value alone would suggest.

By Propulsion Type: Turboprops Unlock Africa's Connectivity Gap

Turbofan-powered aircraft led with an 86.94% share in 2025, which reflected the broad dominance of jet-powered narrowbody and widebody fleets across the region. Turboprops, however, are projected to grow at the fastest CAGR, at 6.01%, through 2031, making propulsion demand more mixed than the current share split suggests and signaling that African route development requires a wider set of aircraft tools. ATR stated that 40% of key African city pairs still lacked direct air links, and 60% of potential intra-African routes are best served by aircraft with 70 seats or fewer. That route profile aligns well with turboprop economics and keeps the segment relevant in the Middle East and Africa commercial aircraft market.

Turboprops also match runway and cost realities in secondary African markets better than larger jets do. ATR’s expanding regional presence supports the idea that these aircraft remain useful where demand density is still developing, and airfield constraints remain material. ICAO’s African Air Navigation planning framework also points to a longer improvement cycle in airport and navigation infrastructure, which supports gradual route unlocking rather than an immediate jump to larger aircraft everywhere. In that setting, turboprops fill a genuine connectivity gap rather than a temporary one. The Middle East and Africa commercial aircraft market is therefore still led by turbofans. Still, future connectivity gains in parts of Africa continue to create room for faster turboprop growth.

By Component: Avionics Upgrades Outpace Structural Demand

Airframe structures accounted for 28.08% of the market in 2025, making them the largest component segment in the Middle East and Africa commercial aircraft market. That leadership is consistent with the value concentration that comes from new aircraft deliveries, especially where widebody platforms and large fleet programs remain active. Aero-engines also retain a large position because propulsion contracts carry high unit value across both narrowbody and widebody programs. At the same time, cabin interior and in-flight entertainment spending is rising as airlines seek to differentiate the passenger experience and refresh aircraft for longer service lives. That combination keeps component demand broad even when aircraft deliveries themselves are uneven.

Avionics and flight control are projected to grow at the fastest CAGR, at 5.23%, through 2031, making it the most dynamic component category in the forecast period. The Middle East and Africa commercial aircraft market is seeing this shift because digital upgrades now matter for both connectivity and the longer useful life of existing fleets. SCIT Group and SKYFive Arabia signed agreements at the Dubai Airshow 2025 with partners including Nokia, Lufthansa Technik, and Kontron to build a large-scale air-to-ground in-flight connectivity network in the region. That move matters because avionics growth is no longer tied only to new deliveries, but also to retrofit cycles and digital modernization across in-service aircraft. The result is a component mix in which structural hardware remains the largest, but high-value electronics and control systems are gaining share more quickly.

Geography Analysis

The Middle East accounted for 52.41% of the Middle East and Africa commercial aircraft market share in 2025, which kept it ahead of Africa by value. That position reflects the concentration of fleet investment in Gulf carriers, the long-haul role of regional hubs, and the policy backing now visible in national aviation programs. Boeing projected in 2025 that Middle East airlines will need 2,950 new aircraft deliveries by 2044, underscoring how large the region’s fleet expansion pipeline remains. Saudi Arabia’s Vision 2030 agenda also targets 330 million annual passengers by 2030, which supports sustained demand for airport capacity, airline growth, and fleet procurement. In this environment, the Middle East benefits from greater access to capital, larger route platforms, and more predictable fleet planning than most African sub-markets.

The Gulf also remains the center of widebody relevance in the region, because intercontinental transfer traffic still depends on large long-haul fleets and major hub infrastructure. At the same time, the region’s narrowbody story has deepened as carriers expand short-haul and medium-haul operations alongside their long-haul systems. flydubai’s 150-aircraft A321neo agreement and flyadeal’s A330-900 order show that Gulf fleet growth is no longer confined to one operating model or one aircraft family. This broadens the regional demand base and brings LCC, hybrid, and long-haul expansion into a single geographic story. It also means the Middle East can sustain demand for both single- and twin-aisle aircraft simultaneously.

Africa is projected to grow at the fastest CAGR, at 6.54%, from 2026 to 2031, making it the highest-growth geography in the Middle East and Africa commercial aircraft market. Boeing projected that Africa’s commercial fleet will more than double to 1,680 aircraft by 2044, with annual passenger traffic growth of 6%, the fastest of any global region. Boeing also stated that 70% of Africa’s new deliveries are expected to be single-aisle aircraft, which supports the view that growth will be concentrated in practical, right-sized fleet additions rather than only in large flagship programs. Yet this growth remains uneven because infrastructure and financing are still weaker outside a limited group of leading aviation markets. Kenya’s Ministry of Roads and Transport said JKIA handled 8.93 million passengers in 2025, against a design capacity of 7.5 million, underscoring how quickly airport bottlenecks can constrain traffic absorption even where demand is already present.

Competitive Landscape

The Middle East and Africa commercial aircraft market is consolidated at the OEM level, but far less so at the component, systems, and upgrade levels. Airbus and Boeing dominate new aircraft demand across the region because most large fleet programs still revolve around their narrowbody and widebody platforms. Boeing’s 2025 regional outlook showed how deep that long-term need remains, especially in single-aisle and widebody categories across the Middle East. Airbus has reinforced its regional position through large orders, including flydubai’s 150 A321neo agreement and the A330-900 order disclosed for flyadeal in 2025. These moves show that competition is intense at the top, but still limited to a small number of airframe leaders.

Below the OEM layer, the competitive picture becomes more specialized and more fragmented. ATR holds a clear role in smaller African route development because turboprops remain the best fit for many underserved city pairs and lower-density corridors. Connectivity and avionics suppliers are also gaining importance as airline competition moves beyond aircraft ownership and into onboard experience, digital systems, and retrofit speed. SCIT Group’s 2025 connectivity agreements around SKYFive Arabia illustrate how the region is building its own aircraft digital infrastructure rather than relying only on imported service frameworks. That creates room for companies that may not compete in airframes, but can still shape airline purchasing priorities through equipment and upgrade programs. The Middle East and Africa commercial aircraft market, therefore, shows strong concentration in airframe supply and much wider competition in systems and support layers.

Regulation is also shaping competitive positioning, especially where fuel burn and emissions compliance influence replacement timing. ICAO’s CORSIA framework provides another reason for carriers to favor newer aircraft and efficiency-oriented upgrades, particularly in countries already engaged in the program, thereby favoring companies that can combine aircraft supply, engine performance, retrofit capability, and operating efficiency into a single commercial proposition. It also means competition is no longer only about delivery slots but about which suppliers can help airlines meet cost, network, and compliance goals. The competitive field is therefore narrow at the top and layered underneath, with scale leaders in aircraft manufacturing and a wider group of challengers in engines, avionics, cabins, and digital connectivity.

Middle East and Africa Commercial Aircraft Industry Leaders

Airbus SE

The Boeing Company

Embraer S.A.

Safran SA

Avions de Transport Régional GIE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ethiopian Airlines exercised options to purchase six additional B787-9 Dreamliners, bringing its firm B787 order to 26 aircraft, with deliveries from 2028. The carrier simultaneously progressed construction of the new Bishoftu international airport, designed to serve as a multi-runway continental hub competing with Gulf mega-airports.

- March 2026: Air Algérie announced the acquisition of 10 B737 MAX 8 aircraft as part of its fleet modernization program, adding to the 16 ATR 72-600 order placed earlier in 2025, signaling Algeria's two-tier fleet strategy of jet-based international services and turboprop-based domestic connectivity.

- January 2026: Ethiopian Airlines signed for 9 more B787-9s and had earlier placed a firm order for 11 B737 MAX commitments. At the same time, construction formally commenced on its new Bishoftu international airport hub outside Addis Ababa, a project designed to handle long-haul widebody traffic at scale.

Middle East and Africa Commercial Aircraft Market Report Scope

This report analyzes the Middle East and Africa commercial aircraft market, focusing on the design, manufacturing, assembly, delivery, and aftermarket support of fixed-wing aircraft used for passenger and cargo transportation. The study includes narrowbody, widebody, and regional aircraft, covering both jet and turboprop platforms. It evaluates market performance across original equipment manufacturing (OEM) sales, fleet replacement, and capacity expansion driven by airline demand. The analysis encompasses the entire aircraft ecosystem, including airframe and propulsion systems, avionics, cabin interiors, and integrated service offerings, for both linefit and retrofit installations.

The Middle East and Africa commercial aircraft market is segmented by aircraft type, propulsion type, application, component, and geography. By aircraft type, the market is segmented into narrowbody, widebody, and regional jets. By application, the market is segmented into passenger and freighter. By propulsion type, the market is segmented into turbofan and turboprop. By component, the market is segmented into airframe structures, aero-engines, avionics and flight control, cabin interior and IFEC, and other components. The report also covers market sizes and forecasts for the Middle East and Africa commercial aircraft market in ten countries across the region. For each segment, the market size is provided in terms of value (USD).

| Narrowbody |

| Widebody |

| Regional Jets |

| Passenger |

| Freighter |

| Turbofan |

| Turboprop |

| Airframe Structures |

| Aero-Engines |

| Avionics and Flight Control |

| Cabin Interior and IFEC |

| Other Components |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Israel | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Algeria | |

| Nigeria | |

| Rest of Africa |

| By Aircraft Type | Narrowbody | |

| Widebody | ||

| Regional Jets | ||

| By Application | Passenger | |

| Freighter | ||

| By Propulsion Type | Turbofan | |

| Turboprop | ||

| By Component | Airframe Structures | |

| Aero-Engines | ||

| Avionics and Flight Control | ||

| Cabin Interior and IFEC | ||

| Other Components | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Algeria | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the Middle East and Africa commercial aircraft market?

The Middle East and Africa commercial aircraft market size is expected to grow from USD 27.99 billion in 2025 to USD 29.46 billion in 2026, and is forecasted to reach USD 36.54 billion by 2031 at a 4.40% CAGR over 2026-2031.

Which aircraft type leads demand across the region?

Narrowbody aircraft lead with 76.49% of 2025 demand and are also projected to post the fastest 5.65% CAGR through 2031.

Why is Africa growing faster than the Middle East in commercial aircraft demand?

Africa is forecast to grow at a 6.54% CAGR because it is starting from a lower base, adding regional connectivity, and building single-aisle capacity across underserved routes.

What is supporting widebody demand in the Gulf?

Gulf demand is supported by long-haul transfer traffic and hub expansion, while Boeing expects Middle East airlines to need 1,370 widebody jets by 2044.

Which component area is growing the fastest?

Avionics and flight control is the fastest-growing component segment with a 5.23% CAGR, supported by retrofit cycles and new connectivity deployments such as the SKYFive Arabia program.

What is the biggest operational risk for airlines in this region?

Aircraft delivery delays and financing pressure are the two main risks, because they can slow fleet renewal even when passenger and cargo demand remain firm.

Page last updated on: