Middle East and Africa AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

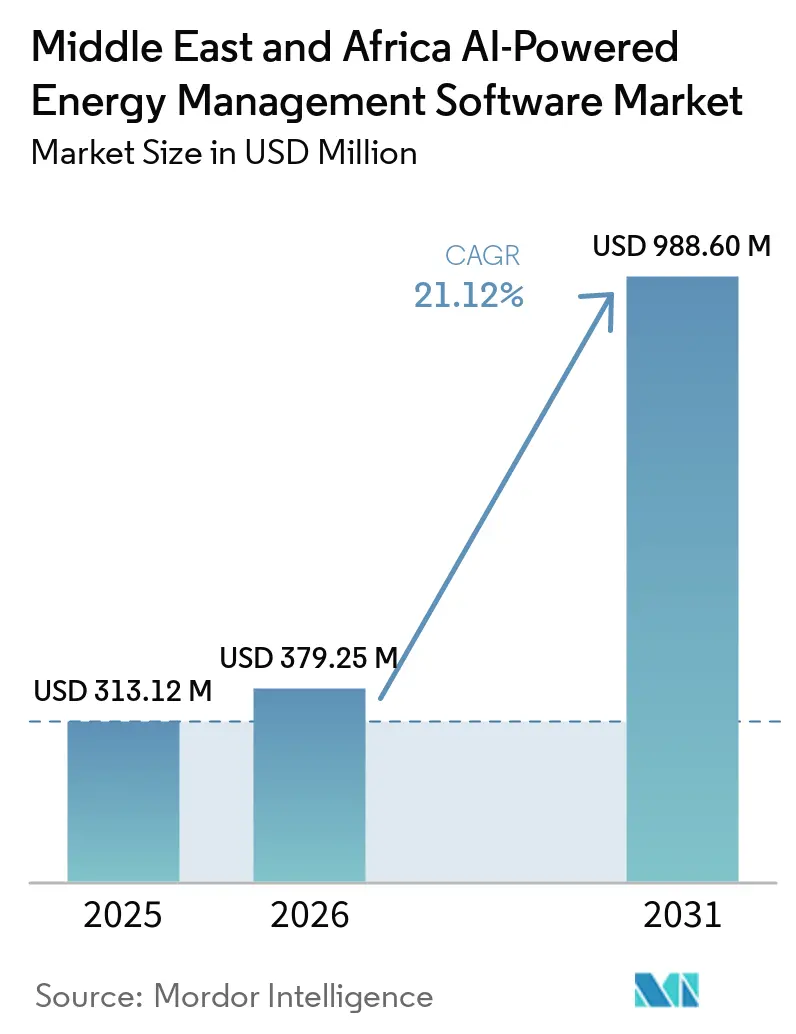

| Base Year Market Size (2025) | USD 313.12 Million |

| Market Size (2026) | USD 379.25 Million |

| Market Size (2031) | USD 988.60 Million |

| Growth Rate (2026 - 2031) | 21.12% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Middle East |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Middle East and Africa AI-Powered Energy Management Software Market size is projected to expand from USD 313.12 million in 2025 and USD 379.25 million in 2026 to USD 988.60 million by 2031, registering a CAGR of 21.12% between 2026 and 2031. National energy transition plans, faster integration of renewables, and broader software spending across utilities, commercial sites, and industrial assets are shaping growth. Operators are under more pressure to manage cooling loads, tariff exposure, and grid reliability, which is increasing demand for real-time optimization tools across the region. Data center investment in Saudi Arabia and the UAE is also increasing the value of AI-based cooling and load management, as these facilities face dense, continuous power demand. Procurement is moving from isolated pilots toward software layers that can work with installed smart meters, building controls, and grid systems, which shortens deployment timelines in many projects. Integration with legacy operational technology and the shortage of local AI and energy analytics skills have slowed execution in parts of the region, but they have not changed the overall direction of spending.

Key Report Takeaways

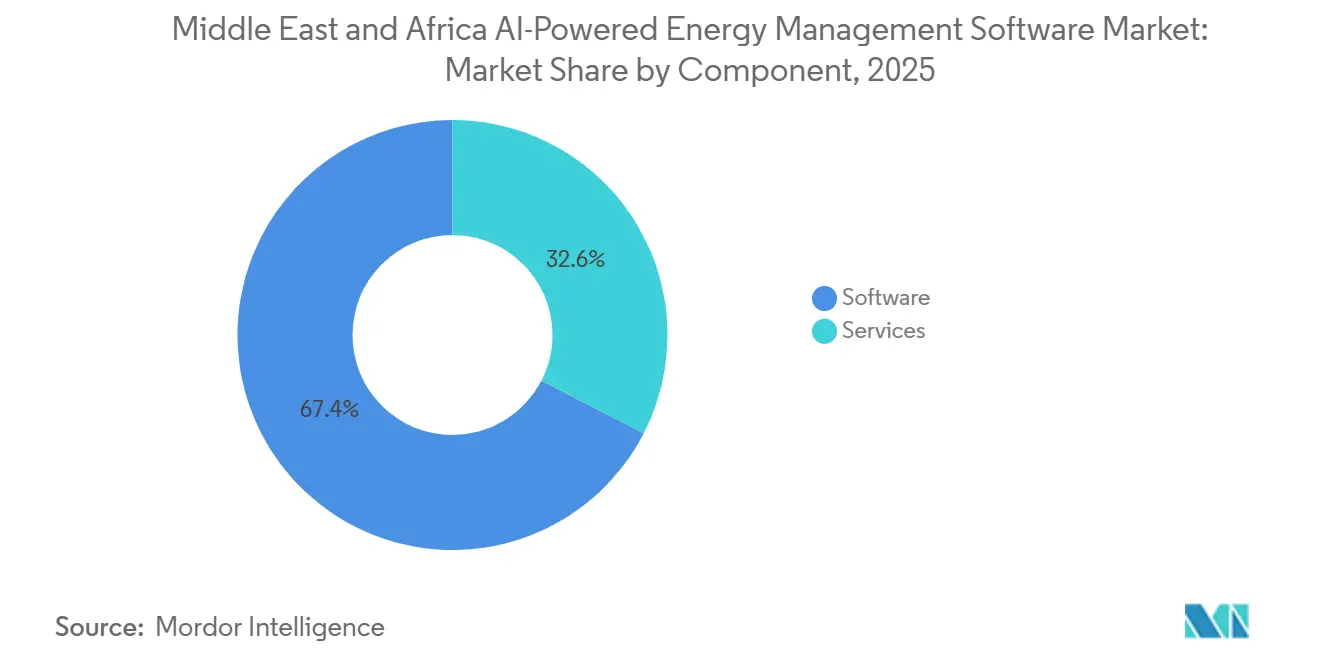

- By component, software led with 67.44% of the Middle East and Africa AI-Powered Energy Management Software market share in 2025, while services remained the fastest-growing component through 2031.

- By deployment mode, cloud-based deployment held the largest position in 2025, while hybrid deployment is projected to expand at 23.15% CAGR through 2031.

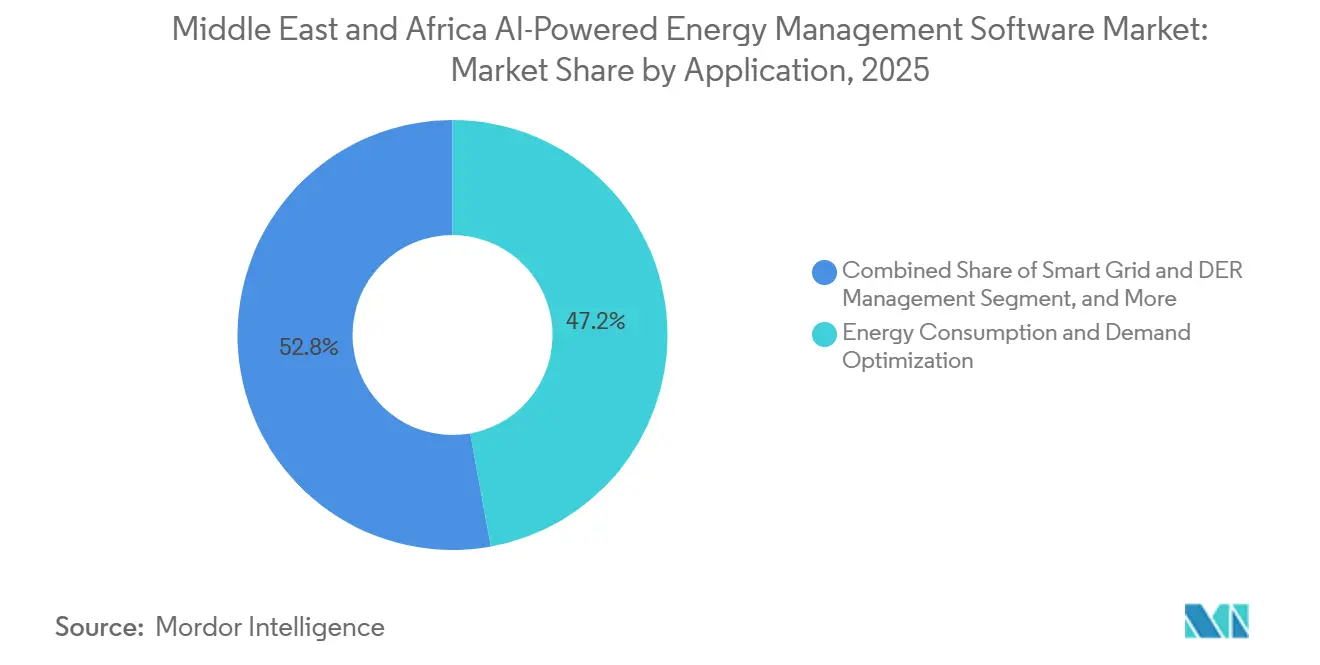

- By application, energy consumption and demand optimization accounted for 47.16% share of the Middle East and Africa Artificial Intelligence Powered Energy Management Software Market size in 2025, while renewable energy forecasting and integration remained the fastest-growing application through 2031.

- By end user, commercial buildings held the largest position in 2025, while utilities are projected to expand at 22.87% CAGR through 2031.

- By geography, the Middle East accounted for 68.19% of the Middle East and Africa AI-Powered Energy Management Software Market in 2025, while Africa is projected to expand at a 23.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Smart Grid and Distributed Energy Resource Orchestration Needs | +5.5% | GCC core, Saudi Arabia, UAE, Oman, with spillover to Egypt and South Africa | Short term (≤ 2 years) |

| Energy Cost Volatility and Peak Demand Optimization Pressure | +4.2% | Broad MEA relevance, strongest in GCC and South Africa | Short term (≤ 2 years) |

| Data Center and Commercial Real Estate Efficiency Retrofits | +3.8% | UAE and Saudi Arabia, with early gains in South Africa and Egypt | Medium term (2-4 years) |

| Utility Demand Response and Dynamic Tariff Automation Adoption | +3.1% | UAE, Saudi Arabia, and Oman, with early adoption in Abu Dhabi and Dubai | Medium term (2-4 years) |

| Cybersecure On-Premises AI Control for Critical Energy Assets | +2.4% | GCC core, with spillover to North Africa | Medium term (2-4 years) |

| Water-Energy Nexus Optimization in Desalination and District Cooling | +1.5% | Saudi Arabia, UAE, Oman, and emerging use in Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Smart Grid and Distributed Energy Resource Orchestration Needs

Rising smart grid and distributed energy resource orchestration needs remain the clearest demand driver for the Middle East and Africa AI-Powered Energy Management Software Market, as utilities need better control over expanding digital grid assets. Saudi Arabia had installed more than 10 million smart meters and automated 32% of its distribution network by 2025, expanding the usable data set for AI software in grid planning and load balancing. DEWA had already committed USD 2 billion to its smart grid program, which kept utility software procurement tied to multi-year infrastructure spending rather than short pilot budgets. Siemens reported in 2026 that 64% of Middle East organizations viewed smart grids and grid software as crucial to the energy transition, while 62% said grid limitations were holding back electrification. That mix of larger data volumes and visible grid constraints has made software capable of dispatch support, outage prediction, and DER coordination more central to procurement. In African power systems, explainable hybrid AI forecasting work for Sub-Saharan solar applications also showed why utilities are moving toward software that can improve reliability while managing renewable variability.

Energy Cost Volatility and Peak Demand Optimization Pressure

Energy cost volatility and peak demand pressure are pushing the Middle East and Africa AI-Powered Energy Management Software Market into more routine operating budgets for commercial and industrial users. Research published in Energy Strategy Reviews found that AI and the digital economy were significant positive drivers of the GCC energy transition, while higher oil prices had a negative effect at higher consumption quantiles. That result matters because tariff exposure and fuel-linked energy costs shorten the payback period for automated demand control during peak operating periods. In the Gulf, summer cooling demand narrows the margin for manual energy management and increases the value of continuous optimization across HVAC systems and load scheduling. Large sites that once treated software as an efficiency add-on now view it as protection against recurring cost swings and avoidable peak penalties. This driver is strongest where commercial portfolios and industrial facilities operate long hours and face tighter energy performance expectations.

Data Center and Commercial Real Estate Efficiency Retrofits

Data center and commercial real estate retrofits are adding another layer of demand for the Middle East and Africa Artificial Intelligence Powered Energy Management Software Market, as building operators pursue lower cooling and power intensity. UAE data centers consumed 3 TWh of electricity in 2025, equal to 2% of the country’s total electricity demand, which increased scrutiny on cooling efficiency and continuous monitoring. The UAE Ministry of Energy and Infrastructure, Khazna Data Centers, and Agility launched a pilot in February 2026 to deploy Phaidra’s reinforcement learning agents across selected hyperscale campuses, aiming to achieve up to a 40% reduction in cooling energy consumption. That initiative showed that AI energy management moved beyond monitoring and entered direct operational control in one of the region’s most power-dense environments. The same logic is carrying over into commercial buildings in Dubai and Abu Dhabi, where owners are retrofitting legacy building management systems rather than replacing entire hardware stacks. As a result, software that can sit above installed controls and learn from site behavior is gaining preference over slower, capital-heavy redesigns.

Utility Demand Response and Dynamic Tariff Automation Adoption

Utility demand response and dynamic tariff automation are broadening the Middle East and Africa AI-Powered Energy Management Software Market beyond building efficiency into grid-interactive operations. Saudi Energy and Kraken Technologies formed a joint venture in April 2026 to deploy an AI-powered utility operating system across MENA, which signaled a move toward unified platforms spanning generation, distribution, and supply data. The commercial meaning is clear: utilities are no longer testing isolated smart metering use cases and are moving toward full software environments that need constant model tuning and platform support. Once tariffs become more dynamic, customer sites need automated response capabilities to capture savings and avoid delays in manual decision-making. This shift also creates recurring revenue for vendors because tariff logic, demand patterns, and renewable inputs keep changing after the initial deployment. The addressable base, therefore, extends beyond energy-intensive buildings to utilities, aggregators, and large users seeking flexible participation in grid balancing programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy OT and Building Management System Integration Complexity | -3.2% | Most acute in brownfield-heavy GCC industrial zones and older commercial buildings across MEA | Short term (≤ 2 years) |

| Limited In-Country AI and Energy Analytics Talent | -2.1% | Strongest in Sub-Saharan Africa, with an emerging gap in GCC mid-tier markets | Medium term (2-4 years) |

| Data Sovereignty and Cross-Border Cloud Hosting Constraints | -1.4% | GCC core, with spillover to North Africa and Egypt | Medium term (2-4 years) |

| High Upfront Retrofit and Sensorization Costs for Brownfield Sites | -1.1% | Sub-Saharan Africa, mid-tier GCC, and MEA industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy OT and Building Management System Integration Complexity

The complexity of legacy OT and building management system integration remains the largest near-term brake on the Middle East and Africa AI-Powered Energy Management Software Market. Many energy and utility environments in the region still run SCADA, DCS, and building control systems installed long before AI integration became a design requirement. Vendors often face multi-protocol settings that combine Modbus, DNP3, IEC 61850, and proprietary building interfaces within a single facility, which extends integration time and testing effort. A 2026 report on OT security in the UAE highlighted the growing focus on protected operational environments and locally controlled security layers, which reflects why brownfield integrations are treated as high-risk projects rather than simple software rollouts. This pushes buyers toward vendors with proven middleware and protocol adapters, even when rival suppliers claim stronger algorithms. The effect is strongest in older industrial sites and commercial facilities where shutdowns are costly and full control system replacement remains hard to justify.

Limited In-Country AI and Energy Analytics Talent

Limited in-country AI and energy analytics talent is a structural restraint for the Middle East and Africa AI-Powered Energy Management Software Market, especially outside the largest GCC hubs. JICA reported in August 2025 that only 5% of Africa’s AI professionals had access to the computing infrastructure needed for AI research and application, which showed that the gap extends beyond workforce numbers alone.[1]JICA, “AI Talent Development Network Publication,” Japan International Cooperation Agency, jica.go.jp The grid skills shortages are constraining the pace of the energy transition across Africa, including in dispatch, modeling, and system operations roles. Even when utilities and large operators buy software, the shortage of trained users can delay model validation, reduce daily utilization, and slow the evidence needed for larger follow-on contracts. This is why vendors increasingly wrap their software with managed services, training packages, and guided analytics rather than relying solely on self-service deployment. The talent gap is less severe in Saudi Arabia, the UAE, and South Africa, but it still matters in second-tier markets where project teams remain thin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Remains the Revenue Anchor While Services Gain Strategic Weight

Software accounted for 67.44% of the component mix in 2025, making it the clearest revenue anchor in the Middle East and Africa AI-Powered Energy Management Software Market. Buyers across the GCC favored analytics, digital twin, and predictive layers that could sit above installed smart meters, SCADA assets, and building systems rather than wait for full hardware renewal cycles. This approach aligned with the region’s current investment pattern, as many operators already had partial digital infrastructure but still lacked continuous optimization and decision support. As sovereign utilities and large property owners expanded their data capture, software became the fastest route to value because it could improve scheduling, forecasting, and fault awareness without a ground-up rebuild. The component structure, therefore, reflected a market that is monetizing intelligence first and physical replacement second.

Services are expanding quickly, even though the largest 2025 revenue pool sat in software, because brownfield integration and ongoing model calibration add a labor layer to almost every deployment. DEWA deployed its AI Virtual Engineer in June 2026 to provide predictive failure alerts, root-cause analysis, and real-time scenario simulation across the power network, demonstrating how utilities are paying for embedded engineering capability alongside software functions. AI in renewable energy systems is delivering measurable operational gains, supporting stronger service attachment rates in projects that need tuning and oversight. This shift favors suppliers that can combine platform licensing with implementation, integration, and long-run support under a single contract. It also means that service quality is becoming part of vendor selection, especially where users need help converting software outputs into dispatch, maintenance, or building control actions.

By Deployment Mode: Cloud Leads Current Adoption While Hybrid Expands Fastest

Cloud-based deployment held the largest position in 2025, while the Middle East and Africa AI-Powered Energy Management Software market size for hybrid deployment is projected to expand at 23.15% CAGR between 2026 and 2031. Cloud appealed to utilities and building managers who wanted scalable analytics without the upfront burden of dedicated server builds. It also fits multi-site portfolios that need centralized dashboards and faster rollout across dispersed assets. In less sensitive use cases, cloud setups reduced internal IT workloads and made software updates easier to manage. That kept the cloud at the front of volume adoption, especially where speed and cost discipline mattered more than strict sovereignty rules.

Hybrid deployment is rising because critical energy operators want cloud flexibility for non-sensitive analytics while keeping operational control of data closer to the asset. The UAE Cybersecurity Council and Siemens formalized an OT security collaboration in 2026, with SINEC Guard deployed on the UAE cloud infrastructure, underscoring the push for protected architectures with local control over operational data. On-premises systems still hold a secure place in desalination, petrochemical, and other critical facilities where zero data egress is a contractual or regulatory requirement. The result is a three-part deployment pattern rather than a winner-takes-all model, and that keeps vendor competition open across cloud depth, local hosting, and OT integration capability. For buyers, the decision is less about ideology and more about matching risk, latency, and compliance needs to each workload.

By Application: Demand Optimization Leads Today While Renewable Integration Rises Faster

Energy consumption and demand optimization accounted for 47.16% of the Middle East and Africa AI-Powered Energy Management Software market in 2025, keeping it at the center of software buying across the region. The large share reflected the immediate pressure to manage cooling demand, tariff exposure, and HVAC performance in climates where energy costs can rise quickly during peak months. Commercial sites and industrial users both value this application because it produces visible savings through scheduling, load shaping, and anomaly detection. It also suits assets that already have meter and control data but need stronger automation to convert information into action. For many buyers, this remains the most direct entry point because the savings case is easier to explain and measure than longer-cycle grid transformation projects.

Renewable energy forecasting and integration are advancing the fastest within the application mix as utilities increase solar and wind capacity and need better tools for balancing variable output. Saudi Arabia’s 50% renewable electricity target for 2030 and the UAE's broader clean energy push are underscoring the need for software that can forecast output and stabilize operations around intermittent generation. A February 2026 paper in npj Clean Energy highlighted the importance of weather-aware optimization for resilient renewable deployment in African power systems, underscoring the need for better forecasting and dispatch software. Asset performance and predictive maintenance also remain important, as utilities and large industrial users are operating legacy generation and transmission assets that cannot afford unplanned downtime. Smart grid and DER management, along with energy trading and market intelligence, are gaining weight as regional electricity systems add distributed resources and more complex balancing needs.

By End User: Commercial Buildings Hold the Lead While Utilities Deliver the Fastest Growth

Commercial buildings held the largest share of end users in 2025, providing a strong base for the Middle East and Africa AI-Powered Energy Management Software Market across offices, retail, hospitality, and mixed-use real estate. Large property portfolios in Saudi Arabia and the UAE have been under pressure to lower electricity use without compromising tenant comfort or uptime. That made AI-based control over cooling, lighting, and occupancy-linked demand more attractive than manual monitoring or periodic audits. The segment also benefited from the fact that building owners could retrofit software onto existing control environments with less disruption than large physical upgrades. In many portfolios, the software-buying case was strengthened by internal sustainability targets and by more formal oversight of energy performance.

Utilities are projected to expand at 22.87% CAGR through 2031, making them the fastest-growing end-user segment in the Middle East and Africa AI-Powered Energy Management Software Market. EWEC and Khalifa University partnered in 2025 to develop AI modules for large-scale photovoltaic integration with storage, including tools for forecasting frequency deviations and estimating system inertia. That work reflected a broader shift in which utilities are moving beyond billing and building analytics toward system-level orchestration of DERs, demand response, and grid stability. Industrial facilities are also increasing adoption as refineries, petrochemical sites, and metals operations seek lower energy cost per unit of output through tighter OT-linked optimization. Residential buildings remain the smallest value segment today, but smart meter rollouts in the Gulf are gradually building the database needed for future household-level AI energy services.

Geography Analysis

The Middle East accounted for 68.19% of the Middle East and Africa AI-Powered Energy Management Software market share in 2025, which kept regional spending concentrated in the GCC. Saudi Arabia’s rollout of more than 10 million smart meters and automation across 32% of the distribution network by 2025 created the database that enables software-led optimization at scale. The UAE also maintained strong momentum through DEWA’s smart grid investment program and related digital grid initiatives that tied software demand to multi-year infrastructure plans. In this setting, the Middle East and Africa Artificial Intelligence Powered Energy Management Software Market has benefited from a buyer base that views grid intelligence as part of national resilience and cost control. Compliance pressure, large public utilities, and dense commercial assets have therefore kept the Middle East ahead of the rest of the region in current spending.

The Middle East and Africa AI-Powered Energy Management Software market size for Africa is projected to expand at 23.66% CAGR between 2026 and 2031, making it the fastest-growing geography in the study. Egypt is building early momentum through grid digitization work that Schneider Electric carried out with the Ministry of Electricity and Renewable Energy across Sharm El Sheik, Minya, Upper Egypt, and South Delta. South Africa also remains important because the integration of renewable energy and system balancing needs is driving interest in software for dispatch planning and operational efficiency. A 2025 South African case study in Processes used 5 years of real-world grid data to validate stochastic optimization for renewable integration under uncertainty, which supports the case for advanced operational software in that market. Across Sub-Saharan Africa, microgrid, rural electrification, and transformer monitoring use cases are still at an early stage, but they are laying the groundwork for broader adoption after 2026.

Oman, Qatar, Kuwait, and Bahrain are extending the regional opportunity through smart metering, demand flexibility planning, and the digitalization of critical infrastructure. Oman commissioned the region’s first 15 MW demand-side grid-balancing facility in April 2026, using controllable load management as a virtual power plant layer over existing industrial demand assets. The Saudi Water Authority reported in October 2025 that AI-driven efficiency tools can cut energy consumption by up to 30% of total operating costs in water transmission systems, which reinforces the long-term value of software in desalination and water networks.[2]Saudi Water Authority, “Water Horizons Report,” Saudi Water Authority, swa.gov.sa These smaller GCC markets do not yet match Saudi Arabia or the UAE in spending scale, but their current metering and flexibility programs are building future software demand.

Competitive Landscape

The Middle East and Africa AI-Powered Energy Management Software Market remains moderately consolidated, with Schneider Electric, Siemens, Honeywell, and ABB holding strong positions across utilities, major real estate portfolios, and critical infrastructure. Incumbent strength comes less from broad branding and more from installed relationships, local service capability, and the ability to integrate with national grid and building control systems. Buyers in this market are testing vendors on data residency, explainability, and OT compatibility as much as on dashboards or model claims. That favors suppliers that can prove long deployment histories and local delivery capacity in Saudi Arabia, the UAE, and Egypt. It also leaves room for specialists where projects are smaller, faster, or more focused on a single application, such as building optimization or microgrid control.

Schneider Electric reinforced its position in May 2026 through an agreement with BFL Group to deploy EcoStruxure Building solutions across 26 UAE stores, showing how commercial building demand is scaling through repeatable multi-site rollouts. Honeywell signed a February 2026 memorandum of understanding with Kortech to automate and digitize critical infrastructure across Egypt, Saudi Arabia, and the UAE, which widened its regional execution base in data centers, smart cities, and transport-linked assets.[3]Honeywell International Inc., “Honeywell Collaborates With Kortech to Automate Infrastructure Projects Across Middle East and North Africa,” Honeywell, honeywell.com Saudi Energy and Kraken Technologies also formed a Riyadh-based joint venture in April 2026, which marked a push toward sovereign-backed utility operating platforms tailored to regional energy systems. These moves show that competitive advantage is increasingly tied to platform depth plus delivery partnerships rather than software features alone. They also show why regional buyers prefer suppliers that can support the full path from deployment to ongoing model tuning and operations support.

Specialist challengers still have space in commercial buildings, light industry, and data center optimization, where procurement cycles are shorter and single-site payback is easier to prove. The February 2026 Phaidra pilot announced by the UAE Ministry of Energy and Infrastructure, Khazna, and Agility, along with the February 2026 Presight contract with Khazna for AI-optimized facility management and digital twin capabilities, highlighted how focused players can win high-value positions in targeted niches. Over time, the Middle East and Africa Artificial Intelligence Powered Energy Management Software Market is likely to maintain a moderate structure, as large incumbents dominate the most complex accounts, while smaller firms continue to find room in new use cases and less entrenched markets. Competitive outcomes will therefore continue to hinge on regional integration depth, service quality, and the ability to balance cloud scale with sovereignty needs.

Middle East and Africa AI-Powered Energy Management Software Industry Leaders

IBM Corporation

Cisco Systems, Inc.

Siemens AG

Schneider Electric SE

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: DEWA deployed the world's first AI Virtual Engineer for its power network, a system that continuously learns from operational data across generation, transmission, and distribution to deliver predictive failure alerts, root cause analysis, autonomous efficiency calculations, and real-time scenario simulations.

- May 2026: Schneider Electric signed a collaborative agreement with BFL Group to deploy its EcoStruxure Building platform, including Energy Activate, Operation, and Advisor modules, across 26 Brands For Less stores in the UAE, with a structured pilot phase followed by a full-network scalable rollout.

- April 2026: Saudi Energy and Kraken Technologies Limited established a joint venture headquartered in Riyadh to accelerate AI-powered utility digital transformation across MENA, with the joint venture designated as Kraken's exclusive regional distributor for its AI operating system, which manages over 70 million customer accounts across more than 27 countries.

- February 2026: Honeywell signed a memorandum of understanding with Kortech, a subsidiary of Hassan Allam Holding, to collaborate on automating and digitizing critical infrastructure across Egypt, Saudi Arabia, and the UAE, targeting data centers, smart city developments, and transportation projects.

Middle East and Africa AI-Powered Energy Management Software Market Report Scope

The Middle East and Africa AI-Powered Energy Management Software Market comprises advanced software solutions that leverage artificial intelligence, machine learning, and analytics to optimize energy consumption, enhance operational efficiency, and advance sustainability initiatives. These advanced platforms seamlessly integrate with smart grids, IoT devices, and the broader energy infrastructure, facilitating real-time monitoring and predictive optimization. Surging energy demand, the push for renewable energy integration, and proactive government-led sustainability programs are fueling the market's momentum. Catering to utilities, industries, and the commercial sector, these solutions not only help slash costs but also curb emissions. Moreover, the region's ongoing digitization and infrastructure development are propelling the widespread adoption of these technologies across its diverse economies.

The Middle East and Africa AI-Powered Energy Management Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Energy Consumption and Demand Optimization | |

| Asset Performance and Predictive Maintenance | ||

| Smart Grid and Distributed Energy Resource (DER) Management | ||

| Renewable Energy Forecasting and Integration | ||

| Energy Trading, Pricing and Market Intelligence | ||

| By End User | Utilities | |

| Commercial Buildings | ||

| Industrial Facilities | ||

| Residential Buildings | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size outlook for the Middle East and Africa AI-Powered Energy Management Software Market?

The market stood at USD 313.12 million in 2025, reached USD 379.25 million in 2026, and is forecast to reach USD 988.60 million by 2031 at a 21.12% CAGR.

Which component leads revenue in this space?

Software led with 67.44% of revenue in 2025 because buyers preferred analytics and optimization layers that could work with installed grid and building infrastructure.

Which deployment model is expanding the fastest?

Hybrid deployment is projected to grow at 23.15% CAGR through 2031 as operators balance cloud scalability with sovereignty and critical asset control needs.

Which end user group is creating the strongest future demand?

Utilities are expected to expand at 22.87% CAGR through 2031 as AI spending shifts toward DER orchestration, demand response, and grid stability software.

Why are data centers important to regional demand?

Data centers are raising power density and cooling pressure, especially in the UAE and Saudi Arabia, which makes AI-based energy optimization more valuable and easier to justify.

What are the main barriers to wider adoption across MEA?

The biggest barriers are legacy OT and building system integration, along with limited local AI and energy analytics talent in several African and second-tier regional markets.

Page last updated on: