Middle East and Africa AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

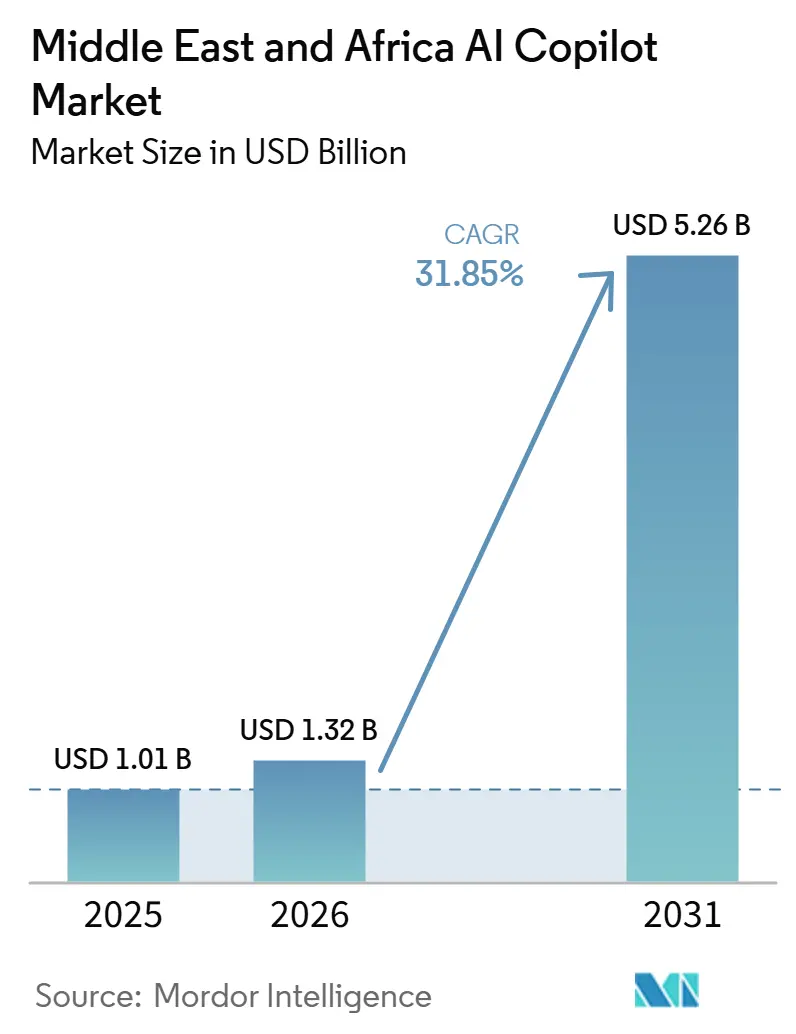

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 5.26 Billion |

| Growth Rate (2026 - 2031) | 31.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa AI Copilot Market Analysis by Mordor Intelligence

The Middle East and Africa AI copilot market size is projected to expand from USD 1.01 billion in 2025 and USD 1.32 billion in 2026 to USD 5.26 billion by 2031, registering a CAGR of 31.85% between 2026 and 2031. The growth path reflects a shift from pilot use to broader operational use, especially as public institutions and large enterprises turn AI policy into active procurement and deployment. Demand is also moving toward tools that can work within daily systems such as email, collaboration suites, ERP platforms, and customer workflows, making adoption easier within existing software estates. Compliance, data residency, and language fit are becoming core buying conditions, so products with sovereign cloud alignment and stronger Arabic support are gaining better acceptance. The competitive field, therefore, includes not only global software and cloud vendors but also regional infrastructure players that can support local hosting and public sector requirements. This setup keeps the Middle East and Africa AI copilot market on a high-growth track while also prioritizing governance, integration depth, and workflow relevance over pure model novelty.

Key Report Takeaways

- By geography, the Middle East held 68.42% of the Middle East and Africa AI copilot market in 2025, while Africa is projected to expand at a CAGR of 36.43% during 2026-2031.

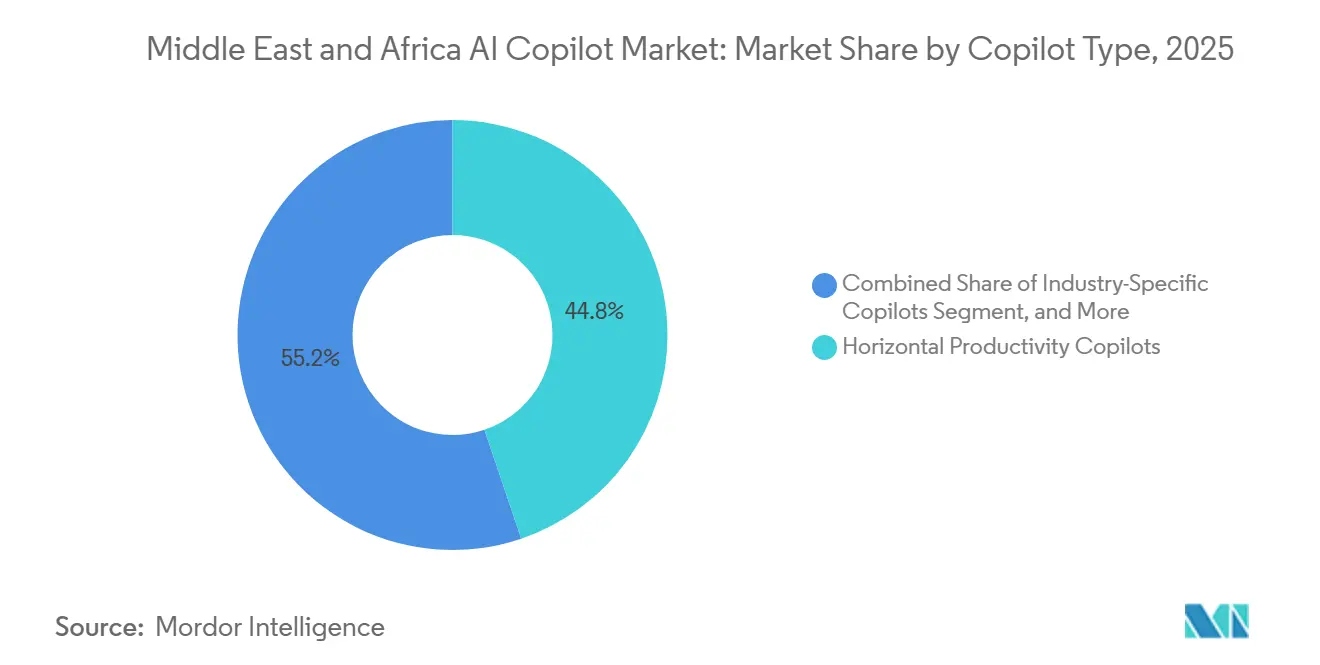

- By copilot type, Horizontal Productivity Copilots held 44.82% of the Middle East and Africa AI copilot market in 2025, while Industry-Specific Copilots are projected to expand at a CAGR of 34.24% during 2026-2031.

- By deployment mode, Cloud-Based accounted for 75.16% of the market in 2025, while Hybrid is projected to expand at a 33.91% CAGR through 2031.

- By organization size, Large Enterprises held 68.43% of the market in 2025, while Small and Medium Enterprises are expected to expand at a CAGR of 34.62% during 2026-2031.

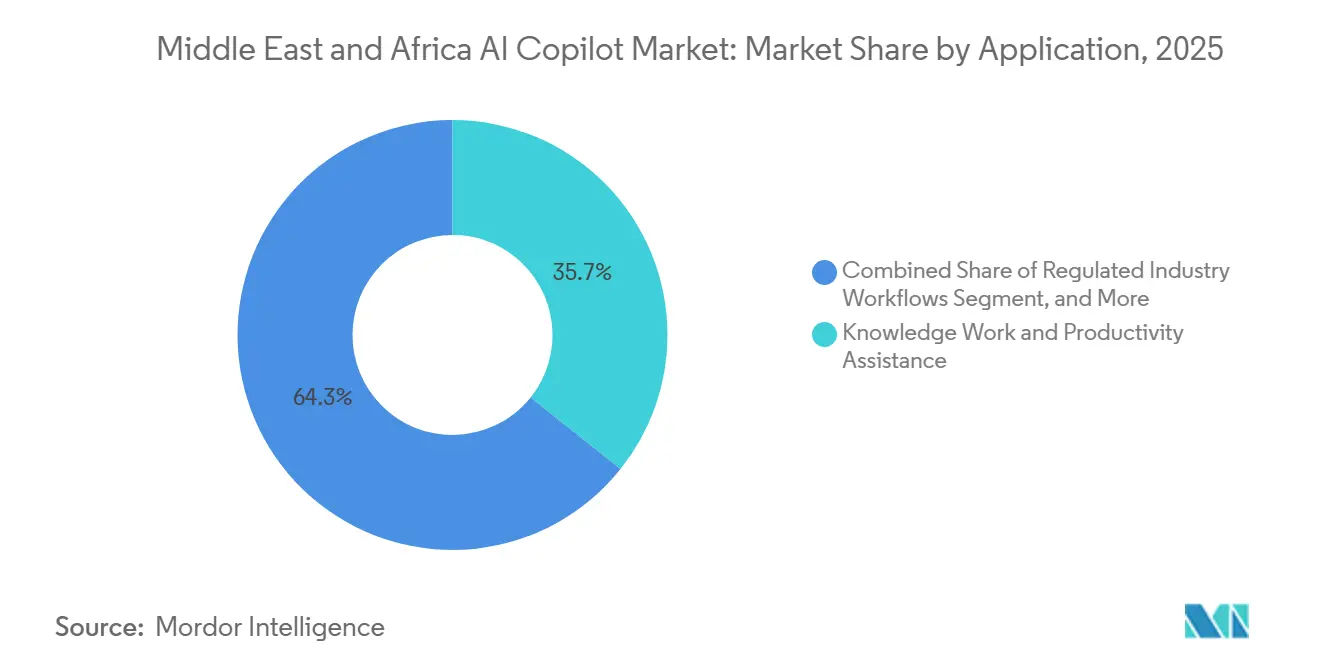

- By application, Knowledge Work and Productivity Assistance accounted for 35.72% of the market in 2025, while Regulated Industry Workflows are projected to expand at a CAGR of 34.18% through 2031.

- By end-user industry, the Government and Public Sector held 21.34% of the market in 2025, while IT and Telecommunication are expected to expand at a CAGR of 35.43% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Government-Led AI Sovereignty Programs in Saudi Arabia and the UAE | +8.5% | Saudi Arabia and UAE, primary, Qatar and Bahrain, secondary | Short term (≤ 2 years) |

| Rapid Enterprise Shift From Chatbots to Context-Aware Copilot Workflows | +7.2% | GCC-led, spill-over to South Africa and Egypt | Short term (≤ 2 years) |

| Growth of Regulated Industry Use Cases in BFSI, Government, and Healthcare | +5.8% | UAE, Saudi Arabia, and South Africa, primary, Egypt and Nigeria, secondary | Medium term (2-4 years) |

| Demand for Arabic-First and Multilingual Copilot Interfaces | +4.1% | Middle East, core, North Africa, secondary | Medium term (2-4 years) |

| Copilot Adoption Inside Cloud-Based SaaS and CRM Suites | +3.2% | MEA enterprise-wide | Short term (≤ 2 years) |

| Use of Copilots for Internal Knowledge Retrieval and Employee Productivity | +2.4% | MEA enterprise-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Government-Led AI Sovereignty Programs in Saudi Arabia and the UAE

Government action is creating a direct demand base for the Middle East and Africa AI copilot market. The UAE approved a federal framework for the deployment of agentic AI in May 2026, and the program includes structured training for 80,000 federal employees while targeting agentic AI across 50% of government services by 2028.[1]UAE Cabinet Media Office, “UAE Cabinet, Chaired by Mohammed Bin Rashid, Approves Federal Framework for Agentic AI Project Implementation,” UAE Cabinet Media Office, mediaoffice.ae Abu Dhabi then moved from policy to scale deployment by extending Microsoft 365 Copilot to 35,000 civil servants across 27 government entities through the Frontier Employee Program. These moves show that public buyers in the region are treating copilots as part of administrative modernization rather than optional experimentation. That procurement stance spills over into the wider Middle East and Africa AI copilot market, as vendors now need stronger governance controls, local hosting options, and enterprise implementation capacity to compete for large institutional contracts.

Rapid Enterprise Shift From Chatbots to Context-Aware Copilot Workflows

The Middle East and Africa AI copilot market is also advancing as enterprises move beyond simple chat interfaces toward tools embedded in work systems. Dubai Holding announced an enterprise AI partnership with Microsoft in May 2026 to deploy Microsoft 365 Copilot across large employee populations in hospitality, real estate, telecom, investment, and entertainment operations. Abu Dhabi's program followed the same direction because the deployment was tied to a sovereign cloud environment that already supports more than 11 million daily digital interactions, which shows that the tool is being connected to real operating environments rather than isolated pilots. SAP's Joule rollout at Red Sea Global also supports this shift, as the product was deployed within human capital management functions across a large workforce rather than positioned as a stand-alone chatbot. This pattern matters for the Middle East and Africa AI copilot market because embedded workflow use raises switching costs and improves the case for larger seat expansions after early deployment.

Growth of Regulated Industry Use Cases in BFSI, Government, and Healthcare

Regulated use cases are adding depth to the Middle East and Africa AI copilot market, as buyers in sensitive sectors need controls that general-purpose tools do not always offer. The UAE federal framework places clear weight on structured implementation, human oversight, and public service deployment, which supports broader comfort with AI tools in high-accountability environments. Abu Dhabi's large civil service rollout shows that copilots are already being used in settings where process consistency, auditability, and administrative discipline matter. In the private sector, SAP deployed Joule at Red Sea Global across human capital management functions for 10,500 employees, which confirms that large employers in structured environments are willing to take approved copilots into production. As this behavior spreads, the Middle East and Africa AI copilot market is likely to see stronger demand for tools designed around traceability, approval workflows, and role-based use rather than generic prompt response alone.

Demand for Arabic-First and Multilingual Copilot Interfaces

Language fit remains a direct growth factor for the Middle East and Africa AI copilot market. Research presented at ACL 2025 introduced the PALM dataset to address cultural and dialectal gaps across all 22 Arab countries, which shows that Arabic language coverage is being treated as a serious technical requirement rather than a minor localization issue. A 2025 study in Neural Computing and Applications found that Arabic text augmentation methods can sharply expand data volume, but the average accuracy gain of 42% still leaves meaningful room for improvement in sensitive use cases.[2]Proceedings of the Association for Computational Linguistics, “PALM: A Culturally Inclusive and Linguistically Diverse Dataset for Arabic LLMs,” ACL 2025, aclanthology.org A July 2026 review of Arabic post-training datasets also found persistent gaps in task diversity and cross-dialect consistency, especially for dialect speech and technical content. That combination keeps demand high for copilots who can handle Modern Standard Arabic, regional dialects, and sector-specific vocabulary with greater consistency across the Middle East and Africa AI copilot market.[3]Springer Nature, “A Comprehensive Survey on Arabic Text Augmentation: Approaches, Challenges, and Applications,” Neural Computing and Applications, doi.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency and Sovereignty Constraints Across Public and Regulated Sectors | -3.8% | UAE, Saudi Arabia, and Qatar, primary, Egypt and South Africa, secondary | Short term (≤ 2 years) |

| Limited Availability of High-Quality Arabic Domain Data for Model Tuning | -2.9% | Middle East, core, North Africa, secondary | Long term (≥ 4 years) |

| High Integration Effort With Legacy Enterprise Systems and Local Workflows | -2.1% | MEA enterprise-wide | Medium term (2-4 years) |

| Talent Gaps in Prompt Engineering, AI Governance, and Copilot Administration | -1.6% | MEA enterprise-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Residency and Sovereignty Constraints Across Public and Regulated Sectors

Data residency remains a practical brake on the Middle East and Africa AI copilot market because many buyers cannot move sensitive workloads freely across borders or clouds. Abu Dhabi's Frontier Employee Program was built on a sovereign cloud environment supporting more than 11 million daily digital interactions, demonstrating that trusted deployment often depends on locally governed infrastructure before scale can occur. The UAE's federal framework for agentic AI also makes governance and controlled rollout central to implementation, which reinforces the need for compliance-ready operating models. These conditions add time to vendor qualification, architecture design, and rollout approval in public and regulated settings. As a result, the Middle East and Africa AI copilot market is growing quickly, but buyers still favor providers that can provide clear answers on hosting, access control, and operational accountability.

Limited Availability of High-Quality Arabic Domain Data for Model Tuning

The shortage of high-quality Arabic domain data continues to slow the Middle East and Africa AI copilot market in sectors that need high factual precision. The ACL 2025 PALM project demonstrated the extent of work still required to address cultural and dialectal diversity across Arabic-speaking countries. The Springer study on Arabic text augmentation showed that a large increase in dataset volume does not automatically produce enough accuracy for demanding use cases. The July 2026 review of Arabic post-training datasets found continuing gaps in task breadth, dialect consistency, and domain-specific material. This prolongs validation cycles for Arabic copilots in legal, financial, clinical, and public-sector work, which, in turn, slows seat expansion in the most sensitive parts of the Middle East and Africa AI copilot market.[4]arXiv Authors, “Mind the Gap: A Review of Arabic Post-Training Datasets,” arXiv, arxiv.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Productivity Tools Lead, but Vertical Specialization Is Accelerating

Horizontal Productivity Copilots held 44.82% of the Middle East and Africa AI copilot market share in 2025, which made them the largest type in the region. Their position stems from existing workplace software deployments where AI can be activated as part of a familiar productivity stack rather than through a full platform replacement. This setup lowers change management friction and makes broad first-wave adoption easier across government entities and large enterprises. It also means that the early expansion of the Middle East and Africa AI copilot market has been shaped by installed software footprints as much as by pure model preference.

Industry-Specific Copilots are projected to grow at a CAGR of 34.24% during 2026-2031, making them the fastest-growing segment in the Middle East and Africa AI copilot market. Buyers are showing more interest in tools that can work with sector rules, formal document structures, approval paths, and domain language without heavy manual adjustment. SAP's July 2025 deployment of Joule at Red Sea Global across human capital management functions for 10,500 employees shows how a more specialized copilot can move into production once it fits a defined operating environment. Technical and engineering copilots remain smaller in current share, but their role is strengthening as enterprises look for tools that can support task-specific execution instead of only broad drafting and summarization. Over time, this should shift a larger part of the Middle East and Africa AI copilot market toward vertical workflows where accuracy, auditability, and contextual fit matter more than general productivity features alone.

By Deployment Mode: Cloud Dominates, but Hybrid Is the Strategic Direction

Cloud-based deployment accounted for 75.16% of the Middle East and Africa AI copilot market in 2025, keeping it well ahead of other deployment modes. The reason is simple because most leading copilots are delivered through cloud software environments that enterprises already use for communication, storage, and workflow management. This makes the cloud the default entry point for many deployments, especially in non-regulated functions and among organizations seeking faster activation. It also explains why the Middle East and Africa AI copilot market has expanded rapidly, driven by use cases tied to standard office and business software.

Hybrid deployment is projected to expand at a CAGR of 33.91% during 2026-2031, which shows where buyer preference is moving as data controls become stricter. Abu Dhabi's sovereign cloud architecture and large public-sector copilot rollout illustrate why many institutions want a model that combines strong local governance with scalable access to AI. The UAE federal framework for agentic AI also supports this direction by placing governance and managed implementation at the center of deployment. On-Premises remains the smallest mode because it can be slower and more expensive to scale, but it still has a place in highly sensitive workloads. For that reason, the Middle East and Africa AI copilot market is likely to remain cloud-led in volume while hybrid becomes the preferred strategic model for controlled expansion in regulated environments.

By Organization Size: Large Enterprises Drive Volume, SMEs Form the Next Growth Layer

Large Enterprises held 68.43% of the Middle East and Africa AI copilot market in 2025, which reflects the buying power of government institutions, state-linked organizations, and major telecom and enterprise groups. Large deployments are easier in this part of the market because enterprise-wide software contracts, stronger IT teams, and formal governance structures reduce the barriers to rollout. Abu Dhabi's deployment of Microsoft 365 Copilot to 35,000 civil servants across 27 entities is the clearest example of how quickly large institutions can convert strategy into live usage. This concentration at the top end continues to shape the present revenue base of the Middle East and Africa AI copilot market.

Small and Medium Enterprises are projected to grow at a CAGR of 34.62% during 2026-2031, making them the fastest-growing segment by organization size. Their growth reflects better product packaging, easier activation inside existing office suites, and rising interest in immediate productivity use cases that do not require a long transformation cycle. Dubai Holding's enterprise-wide deployment also matters indirectly because it normalizes Copilot use across multiple business lines and raises visibility for similar tools among mid-sized firms in the region. Even so, many smaller firms still face constraints in data readiness, governance, and internal administration. That means the next stage of the Middle East and Africa AI copilot market will depend not only on affordable access but also on whether SMEs can adopt structured policies that support broader use beyond basic drafting and summarization.

By Application: Knowledge Work Anchors Current Demand, While Regulated Workflows Lead Growth

Knowledge Work and Productivity Assistance accounted for 35.72% of the market in 2025, which made it the largest application area in the Middle East and Africa AI copilot market. This segment includes drafting, meeting support, summarization, and document handling, which are usually the easiest functions to scale first. Organizations favor these uses because they produce visible time savings without changing core operating models at the start. That is why the Middle East and Africa AI copilot market still has a strong foundation in general workplace assistance.

Regulated Industry Workflows are projected to expand at a CAGR of 34.18% during 2026-2031, indicating the next stage of application maturity. The UAE's federal framework for agentic AI and Abu Dhabi's public-sector rollout both show that buyers are willing to place copilots inside structured environments once governance and operating discipline are defined. SAP's Joule deployment at Red Sea Global follows the same pattern by embedding AI into human capital workflows for a large workforce, rather than limiting it to loose experimentation. Software engineering, service operations, and revenue enablement use cases are also progressing, but the strongest growth signal is coming from applications where rules, review paths, and business context shape the output. This shift should make the Middle East and Africa AI copilot market less dependent on generic productivity alone over the forecast period.

By End-User Industry: Government Holds the Lead, While Telecom Expands the Fastest

Government and Public Sector held 21.34% of the Middle East and Africa AI copilot market in 2025, making it the largest end-user industry. Public institutions are leading because AI deployment is increasingly linked to digital service reform, administrative efficiency, and policy execution, rather than solely to IT modernization. The UAE federal framework and Abu Dhabi's rollout both show how public agencies are funding and organizing copilot adoption at scale. This makes the government the anchor customer group in the current structure of the Middle East and Africa AI copilot market.

IT and Telecommunication are projected to expand at a CAGR of 35.43% during 2026-2031, which gives them the fastest growth outlook among end-user industries. Telecom operators are important because they adopt copilots internally while also shaping how enterprise customers encounter AI tools through bundled software and service channels. BFSI, healthcare, and other regulated verticals are also moving forward because they need controlled workflow support, stronger record handling, and closer governance over generated outputs. SAP's rollout at Red Sea Global confirms that large organizations with structured systems can scale approved copilots when the tool fits an operational need and a trusted software environment. Retail, manufacturing, education, media, and energy are expanding from smaller bases, but the strongest near-term direction in the Middle East and Africa AI copilot market still comes from government-led demand and communications-led distribution.

Geography Analysis

The Middle East accounted for 68.42% of the Middle East and Africa AI copilot market in 2025, keeping the regional revenue base concentrated in the Gulf. Saudi Arabia and the UAE remain the core demand centers because they combine public digitization agendas, enterprise software depth, and stronger institutional buying capacity. The UAE Cabinet approved a federal framework for agentic AI in May 2026, providing the market with a clear policy signal and a long deployment runway across government services. Abu Dhabi strengthened that position by deploying Microsoft 365 Copilot to 35,000 civil servants under a sovereign cloud environment that supports more than 11 million daily digital interactions. Dubai also added to the region's scale through a major enterprise deployment at Dubai Holding, which supports the wider commercial base of the Middle East and Africa AI copilot market.

Africa is projected to grow at a CAGR of 36.43% during 2026-2031, which makes it the fastest-growing geography in the Middle East and Africa AI copilot market. The growth rate reflects a lower starting base, but it also points to stronger enterprise AI readiness, rising infrastructure activity, and broader interest in applied productivity tools. Morocco is emerging as an important infrastructure node because TEAM NAVER joined a consortium in 2026 to build a next-generation AI data center in the country, with the first phase targeted for Q4 2026. South Africa, Nigeria, and Egypt also remain important demand centers in the regional discussion, as enterprise adoption and AI literacy are advancing faster than in many other African markets.

The geographic pattern of the Middle East and Africa AI copilot market, therefore, combines a mature Gulf demand base with a faster African expansion curve. The Middle East offers a stronger immediate scale, as public-sector deployment and large-enterprise contracting are already active. Africa offers more upside because infrastructure, skills, and commercial adoption are still building from a smaller base. As more local capacity comes online and regional buyers gain confidence in governed deployments, the balance of the Middle East and Africa AI copilot market should become less concentrated than it was in 2025.

Competitive Landscape

The Middle East and Africa AI copilot market is moderately concentrated, with Microsoft holding the strongest installed-base advantage because many large buyers already use its workplace and cloud stack. That position was reinforced by Abu Dhabi's 35,000-seat public-sector rollout and by Dubai Holding's enterprise AI partnership, both of which demonstrate the company's presence in major institutional deployments. Alphabet, Amazon Web Services, and IBM compete through platform and infrastructure relationships, while SAP, Salesforce, ServiceNow, Oracle, and Workday compete by embedding copilots inside enterprise applications. Regional firms such as G42, Core42, and HUMAIN are also changing the field because local compute, hosting, and governance support matter more in this market than in many other software categories. The result is a competitive landscape in which distribution strength and sovereign alignment are often as important as the underlying model.

Strategic moves in the Middle East and Africa AI copilot market are increasingly tied to deployment scale and infrastructure positioning. Microsoft and Abu Dhabi's Department of Government Enablement launched one of the region's largest public-sector AI productivity rollouts, which gives Microsoft a strong reference point for other government and enterprise buyers. Microsoft also expanded its regional presence through its partnership with Dubai Holding, which extends Copilot use across multiple commercial sectors within a single large business group. SAP took a different route by deploying Joule at Red Sea Global, which strengthens its position in structured enterprise workflows and demonstrates that embedded copilot value can be sold through existing application relationships.

Another competitive layer is forming around infrastructure and local capacity. TEAM NAVER joined a Moroccan AI data center consortium in 2026, indicating that vendors and partners are racing to secure regional compute footprints rather than waiting for demand to fully mature. That matters because buyers in the Middle East and Africa AI copilot market are increasingly asking where their data sits, who operates the environment, and how the system is governed after deployment. White-space opportunities remain strongest in Arabic-first vertical copilots and in more accessible offerings for smaller enterprises that need easier adoption paths. Competitive advantage in this market is therefore built through a mix of installed software presence, sovereign infrastructure access, workflow fit, and the ability to move large deployments from announcement to active use.

Middle East and Africa AI Copilot Industry Leaders

Microsoft Corporation

OpenAI, L.L.C.

Alphabet Inc.

Salesforce, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Abu Dhabi Government deployed Microsoft 365 Copilot to 35,000 civil servants across 27 government entities under the Frontier Employee Program, adding 26,000 new licences to the 9,000 already in use, underpinned by a sovereign cloud environment processing over 11 million daily digital interactions. The initiative is one of the world's largest public-sector AI productivity rollouts and directly advances Abu Dhabi's goal of becoming an AI-native government by 2027.

- July 2026: TEAM NAVER joined a consortium with NVIDIA, Nexus Core Systems, and Lloyds Capital to build a next-generation AI data center in Morocco, with NAVER Cloud serving as platform operator offering sovereign AI computing services across the EMEA region and the first phase targeted for Q4 2026.

- May 2026: UAE Cabinet approved a federal framework for agentic AI deployment, committing to train 80,000 federal employees in agentic AI workflows and targeting agentic AI across 50% of government services by 2028, with Microsoft, IBM, Google, and OpenAI as named technical partners.

- May 2026: Dubai Holding announced a landmark enterprise AI partnership with Microsoft to deploy Microsoft 365 Copilot across its tens of thousands of employees spanning hospitality, real estate, telecom, investment, and entertainment subsidiaries, described by both companies as the first enterprise-scale MEA deployment of its kind.

Middle East and Africa AI Copilot Market Report Scope

The Middle East and Africa AI copilot market refers to the ecosystem of artificial intelligence-driven intelligent assistants integrated into enterprise and consumer software applications to enhance human capabilities and automate complex tasks within the region. These copilots leverage advanced foundation models, including large language models (LLMs) and generative AI, to provide real-time contextual suggestions, generate content, analyze data, and execute workflows seamlessly within existing digital tools. The market encompasses various copilot types ranging from general horizontal productivity tools to specialized functional, technical, and industry-specific solutions. Deployed across cloud-based, hybrid, and on-premises environments, these AI systems cater to organizations of all sizes across the MEA region. They are used across diverse applications, including knowledge work assistance, software development, customer service, and sales enablement, in industries such as IT, BFSI, healthcare, and government. Driven by aggressive national digital transformation agendas (such as Saudi Vision 2030 and the UAE's National AI Strategy), rapid smart city developments, and a growing focus on economic diversification, AI copilots help organizations in the Middle East and Africa drive operational efficiency, reduce manual cognitive load, and accelerate their transition into knowledge-based digital economies.

The Middle East And Africa AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries), and Geography (Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other End-User industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Copilot Type | Horizontal Productivity Copilots | |

| Functional Workflow Copilots | ||

| Technical and Engineering Copilots | ||

| Industry-Specific Copilots | ||

| By Deployment | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Knowledge Work and Productivity Assistance | |

| Software Engineering and Technical Operations | ||

| Customer and Employee Service Operations | ||

| Sales, Marketing and Revenue Enablement | ||

| Business Process and Enterprise Operations | ||

| Regulated Industry Workflows | ||

| By End-User Industry | IT and Telecommunication | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Retail and E-Commerce | ||

| Industrial Manufacturing | ||

| Education and Research Institutions | ||

| Media and Entertainment | ||

| Government and administration | ||

| Energy and Utilities | ||

| Other End-User industries | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the Middle East and Africa AI copilot space?

The Middle East and Africa AI copilot market size was USD 1.01 billion in 2025, is projected at USD 1.32 billion in 2026, and is forecast to reach USD 5.26 billion by 2031 at a CAGR of 31.85%.

Which geography leads current revenue and which one is growing the fastest?

The Middle East led with 68.42% share in 2025, while Africa is projected to record the fastest growth at a 36.43% CAGR through 2031.

Which copilot type is generating the most revenue today?

Horizontal Productivity Copilots led with 44.82% share in 2025 because many organizations could activate AI inside existing workplace software environments.

Where is the strongest future demand expected by application?

Regulated Industry Workflows are projected to grow at a 34.18% CAGR through 2031 as buyers look for more controlled AI use in structured and sensitive work settings.

Why are public institutions so important in this region?

Government and Public Sector held 21.34% share in 2025, and large public deployments in the UAE show that policy-led procurement is a major driver of adoption.

What is the main deployment shift to watch over the next 5 years?

Cloud-Based remained the largest mode with 75.16% share in 2025, but Hybrid is projected to grow faster at a 33.91% CAGR as buyers balance scale with local control and governance.

Page last updated on: