Middle East and Africa 5G Fiber Backbone Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

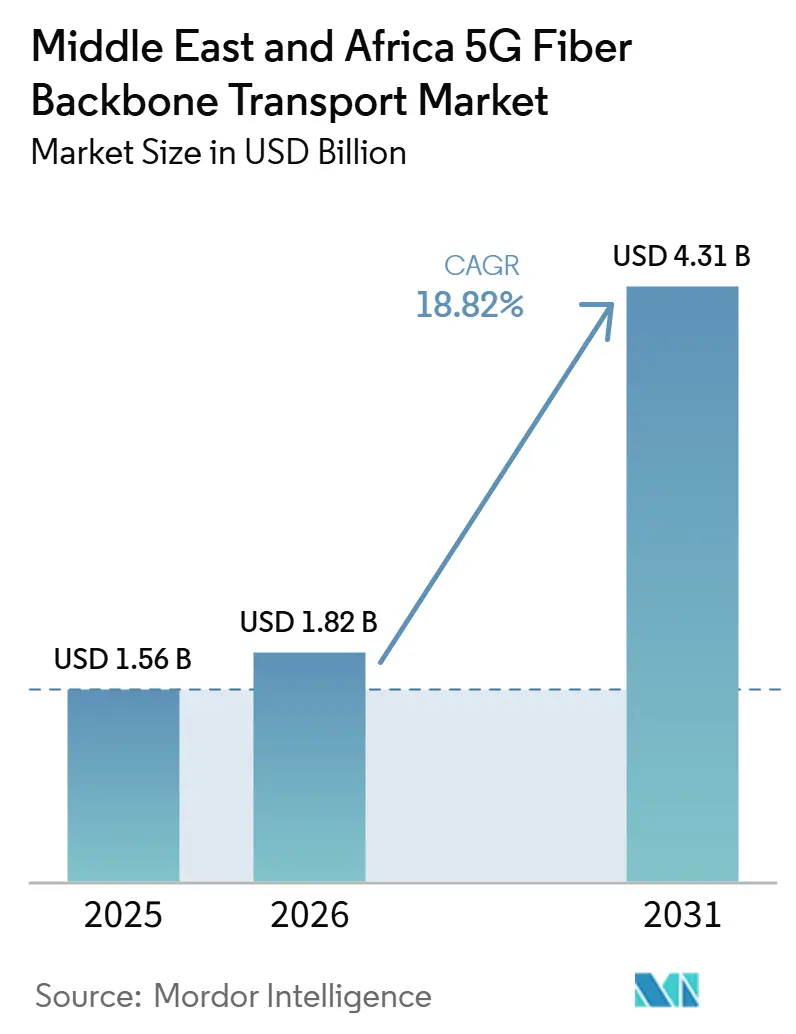

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 4.31 Billion |

| Growth Rate (2026 - 2031) | 18.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa 5G Fiber Backbone Transport Market Analysis by Mordor Intelligence

The Middle East and Africa 5G Fiber Backbone Transport Market size was valued at USD 1.56 billion in 2025 and is estimated to grow from USD 1.82 billion in 2026 to reach USD 4.31 billion by 2031, at a CAGR of 18.82% during the forecast period (2026-2031). The Middle East and Africa 5G fiber backbone transport market is growing as 5G rollouts across the GCC and early African deployments keep raising the need for high-capacity optical transport, while data center interconnect traffic is also rising across the region. Government-backed digital infrastructure programs in Saudi Arabia, the UAE, Qatar, Kuwait, Algeria, and Morocco continue to support fiber buildouts and shorten upgrade cycles for national transport networks. Competition remains active between Chinese vendors, which compete on cost and scale, and Western suppliers, which focus on coherent optics and software-led network control. Demand is also expanding beyond telecom operators, as hyperscale cloud commitments in GCC data center hubs create guaranteed bandwidth requirements and support long-term procurement for advanced backbone networks. Civil works costs, permitting delays, foreign exchange pressure, and multi-vendor integration issues still slow execution in some markets, but these factors remain manageable within the current forecast period.

Key Report Takeaways

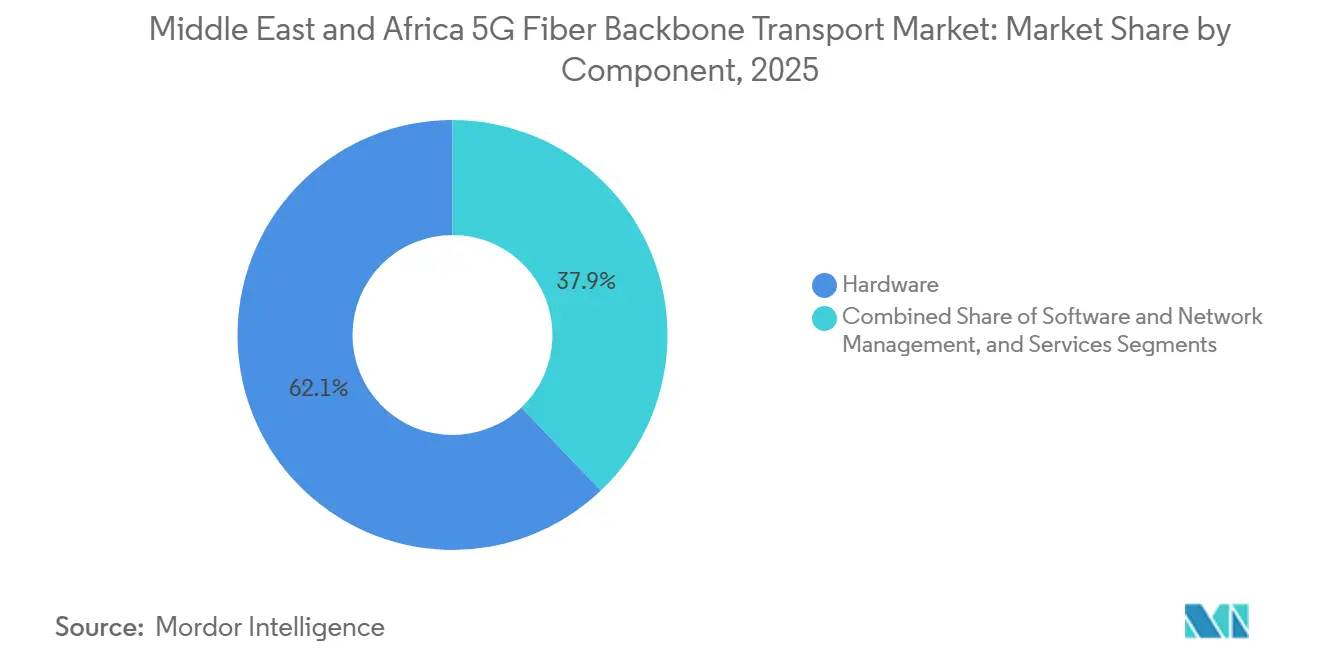

- By component, hardware held 62.12% of revenue share in the Middle East and Africa 5G fiber backbone transport market in 2025, while the software and network management segment is projected to expand at a 24.57% CAGR through 2031.

- By capacity, 10 to 100 Gbps accounted for 50.59% of revenue share in the Middle East and Africa 5G fiber backbone transport market in 2025, while above 100 Gbps is projected to expand at a 20.20% CAGR through 2031.

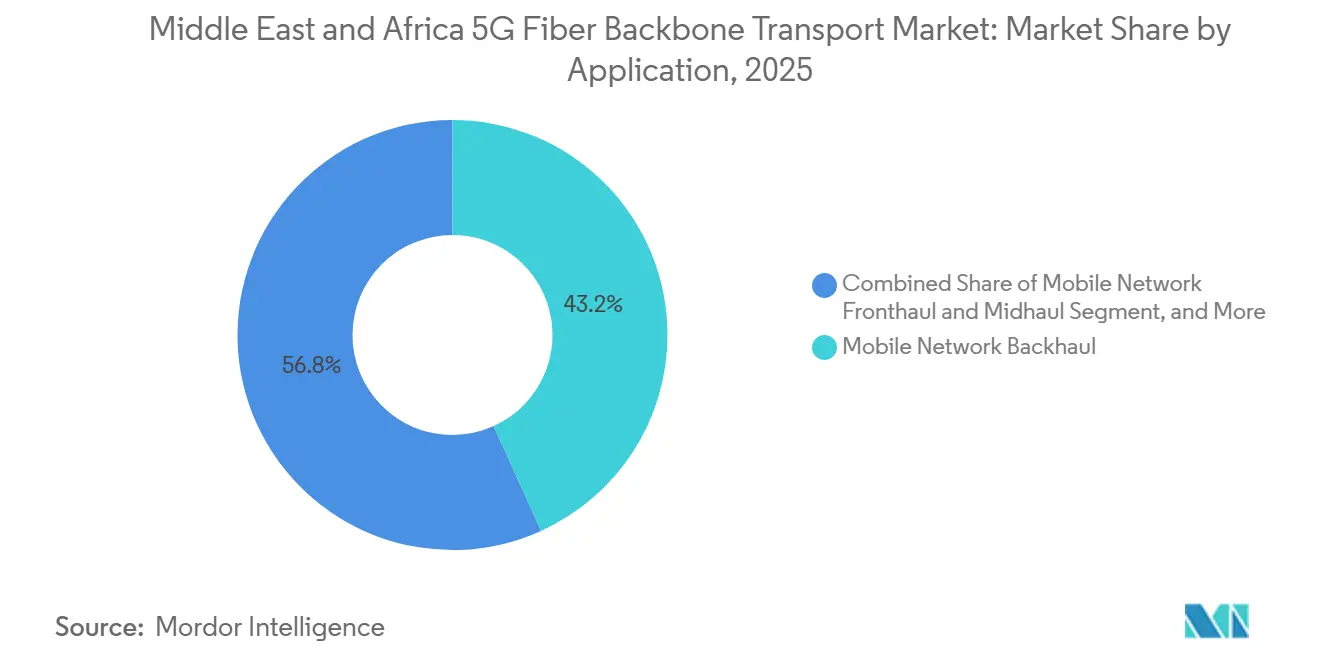

- By application, mobile network backhaul captured 43.24% of revenue share in the Middle East and Africa 5G fiber backbone transport market, while the mobile fronthaul and midhaul segment is projected to expand at a 27.12% CAGR through 2031.

- By end user industry, mobile network operators held 56.67% of revenue share in the Middle East and Africa 5G fiber backbone transport market, while cloud and hyperscale providers are projected to expand at a 26.47% CAGR through 2031.

- By geography, the Middle East held 66.46% of revenue share in the Middle East and Africa 5G fiber backbone transport market in 2025, while Africa is projected to expand at a 20.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa 5G Fiber Backbone Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud and Data Center Interconnect Demand for 400G and 800G Backbones | +4.2% | UAE, Saudi Arabia, Qatar, expanding to Egypt and South Africa | Medium term (2-4 years) |

| 5G Small-Cell and Urban Macro Densification | +3.5% | GCC urban cores, Nairobi, Lagos, Cairo | Short term (≤ 2 years) |

| Sovereign Digital Infrastructure Programs in GCC and North Africa | +3.1% | Saudi Arabia, UAE, Qatar, Algeria, Morocco | Long term (≥ 4 years) |

| Open RAN and eCPRI Disaggregation of Transport Layers | +2.8% | UAE, Saudi Arabia, Kenya, South Africa | Medium term (2-4 years) |

| Route Design Shift Toward Multi-Tenant Wholesale Fiber Backbones | +2.4% | Pan-Africa core corridors, GCC wholesale carriers | Long term (≥ 4 years) |

| Utility-Grade Fiberization of Ports, Industrial Zones, and Energy Corridors | +1.9% | UAE, Saudi Arabia, Oman, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud and Data Center Interconnect Demand for 400G and 800G Backbones

Cloud and data center traffic is a major near-term support factor for the Middle East and Africa 5G fiber backbone transport market, as GCC operators are already moving beyond trial conditions into live, high-capacity deployments. Nokia and stc Group completed the region’s first 1Tbps long-haul field trial in January 2025 over 850 km, which showed that very high-capacity backbone performance is already practical for commercial use in Saudi Arabia.[1]Nokia Corporation, “Nokia and stc Group Set Middle East Record with 1Tbps Data Center Connectivity Across 850km Network,” Nokia, nokia.com e& UAE then deployed Ciena’s WaveLogic 6 Extreme in February 2025 and reached 1.6Tbps per wavelength within its existing footprint, which strengthened the case for rapid optical scaling around AI and cloud hubs.[2]Ciena Corporation, “e& UAE First in Middle East and Africa to Deploy Ciena’s WaveLogic 6,” Ciena Investor Relations, ciena.com MTN Nigeria and Huawei also launched Nigeria’s first hybrid 400G-800G Automatically Switched Optical Network in July 2025, including the country’s first single-wavelength 800G optical channel, which showed that the same capacity shift is now reaching frontier African markets as well. e& UAE further demonstrated in November 2025 that dual-800GE over DWDM can reduce latency and lower cost per bit, which improves the business case for early backbone investment before subscriber traffic fully matures.

5G Small-Cell and Urban Macro Densification

The Middle East and Africa 5G fiber backbone transport market is also benefiting from dense 5G site rollouts, because small-cell and advanced macro architectures require much more fiber than legacy mobile layouts. Safaricom’s 5G deployment in Nairobi has been supported by small-cell and DAS installations that delivered typical speeds of 400 Mbit/s to 700 Mbit/s in dense commercial areas, underscoring the need for direct fiber support at the radio level. Algeria added another clear example when Ooredoo, Djezzy, and Mobilis launched commercial 5G in December 2025 after Algerie Telecom and Huawei had upgraded the national optical backbone to 400G WDM across all 58 wilayas in February 2025. The transport requirement rises sharply because each 5G small-cell activation under eCPRI option 7.2x shifts latency-sensitive processing closer to the radio unit, tightening the end-to-end latency budget to 100-150 microseconds. Nokia’s MEA Mobile Broadband Index 2025 also pointed to accelerating 5G investment, with operators adding 5G-Advanced capabilities, industrial use cases, and network slicing, all of which require tighter transport precision than standard consumer broadband services.

Sovereign Digital Infrastructure Programs in GCC And North Africa

Government-backed infrastructure programs remain a major foundation for the Middle East and Africa 5G fiber backbone transport market because they create demand before private traffic volumes fully build up. Kuwait signed a KD 825 million (USD 2.69 billion) 50-year public-private partnership in 2026 to design, build, operate, and maintain the national fixed telecommunications network and extend high-speed fiber to 90% of homes. Morocco followed a different model when ANRT authorized the Uni Fiber and Uni Tower joint ventures between Maroc Telecom and Inwi on June 18, 2025, with a MAD 4.4 billion (USD 450 million) first-phase investment in passive infrastructure aimed at 1 million FTTH connections within 2 years and 3 million by 2030.[3]Agence nationale de réglementation des télécommunications, “Authorization of Uni Fiber and Uni Tower Joint Ventures,” ANRT Morocco, anrt.ma These programs matter because they create a minimum level of transport demand that supports procurement even before private AI, cloud, and enterprise workloads fully ramp up. They also shorten the risk period for suppliers because capacity is often committed 18-36 months before commercial traffic reaches full scale.

Open RAN and eCPRI Disaggregation of Transport Layers

Open RAN and eCPRI adoption are changing procurement patterns in the Middle East and Africa 5G fiber backbone transport market, as transport layers now require tighter timing, lower latency, and more flexible network control. The O-RAN Alliance Working Group 4 specification requires eCPRI over Ethernet or UDP/IP to operate with sub-100 microsecond latency and microsecond-level jitter tolerance, which pushes operators toward dedicated fiber or time-sensitive networking-compliant Ethernet in the fronthaul segment. du added a practical example in December 2025, demonstrating the world’s first 25Gbps E-band link integrated into a 5G-Advanced site rollout, which delivered fiber-like transport in dense urban areas where physical fiber is harder to deploy. It then signed a 3-year strategic framework with Huawei, demonstrating that disaggregated transport can support both fiber and high-capacity wireless backhaul procurement simultaneously. This shift also helps explain why software and network management is the fastest-growing component in the Middle East and Africa 5G fiber backbone transport market, because open interfaces reduce lock-in at the hardware layer and make SDN control and AI-based optimization more important.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Civil Works Cost and Right-of-Way Delays | -1.8% | Sub-Saharan Africa, secondary Saudi cities, Turkey rural zones | Short term (≤ 2 years) |

| Power, Cooling, and Site Access Constraints in Remote African Markets | -1.2% | Nigeria, DRC, remote East Africa, Algeria’s Saharan south | Long term (≥ 4 years) |

| Interoperability Friction Across Multi-Vendor Optical and Packet Layers | -0.8% | Global, with acute impact in multi-vendor GCC deployments | Medium term (2-4 years) |

| FX Pressure and Import Dependency for Coherent Optics and Line Systems | -0.6% | Nigeria, Egypt, Kenya, Turkey | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Civil Works Cost and Right-Of-Way Delays

Civil works costs and permitting delays remain the most immediate brake on the Middle East and Africa 5G fiber backbone transport market, especially across sub-Saharan Africa and secondary cities, where approvals move slowly. Africa’s terrestrial fiber footprint passed 2.1 million km, with 1.3 million km active as of the Africa Broadband Outlook 2024, and 58,000 km entered service in the 12 months to June 2024, yet this pace still falls short of the density required for full 5G transport readiness at scale. The main issue is not a lack of capital alone, because projects in Nigeria and secondary Saudi cities can still face overlapping approvals from telecom regulators, planning bodies, and road authorities that stretch for 18-24 months. Ciena stated at AfricaCom 2025 that AI infrastructure is increasing data volumes across data centers, even as some of the most important transport routes still face long delivery schedules.[4]Ciena Corporation, “AfricaCom 2025 Keynote Participation, Joe Marsella,” Ciena, ciena.com This is one reason shared trench and open-access fiber models are gaining support: a single concessionaire can move through a single permitting process and lease capacity to several operators.

Power, Cooling, And Site Access Constraints In Remote African Markets

Remote African routes pose a different operating challenge for the Middle East and Africa 5G fiber backbone transport market, as long-haul amplification sites often rely on difficult power and cooling conditions rather than just trench access. MTN Group stated at its 2026 Capital Markets Day that its African fiber footprint is expected to rise from 140,000 km to between 420,000 km and 560,000 km by 2030, yet this expansion is still affected by off-grid hut power needs and the cooling load of coherent DWDM transponders in high-temperature environments. The issue is especially relevant in Saharan Algeria and remote East and Central Africa, where site access and maintenance conditions raise the cost of keeping long-haul equipment stable. Nokia, NPS, and e& UAE also ran a 2026 laboratory trial on hollow-core fiber at 153Tb/s of bidirectional C+L-band traffic, pointing to a future option that could improve latency and amplifier spacing economics on remote routes. In the near term, operators still need solar-powered hut designs and lower-heat equipment profiles, which add upfront costs and weigh on project returns in frontier markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Intelligence Reshapes a Hardware-Led Market

Hardware held a 62.12% share in 2025, indicating that the Middle East and Africa 5G fiber backbone transport market is still in a build phase, with operators spending first on physical optical layers. Optical transport systems, DWDM and ROADM platforms, and packet-optical equipment remain the main items in procurement cycles across GCC backbone routes and African long-haul corridors. This pattern reflects the fact that carriers are still expanding network reach and raw transport capacity before they shift a larger share of spending toward software layers. Services are also gaining relevance because operators in frontier African markets often rely on vendors for planning, deployment, integration, and managed operations. Software and network management is projected to expand at a 24.57% CAGR from 2026 to 2031, which makes it the fastest-growing component category in the Middle East and Africa 5G fiber backbone transport market.

That faster software growth reflects a broader change in how the Middle East and Africa 5G fiber backbone transport industry is competing, because value is moving toward network control, orchestration, and optimization rather than hardware alone. Nokia completed its acquisition of Infinera for USD 2.3 billion in January 2025, combining coherent photonics with cloud-native network management and demonstrating that major vendors are strengthening both layers simultaneously. Omantel’s 2025 launch of its Managed Optical Fiber Network with Ciena also showed that operators are buying real-time SLA monitoring, bandwidth-on-demand, and automated provisioning under a network-as-a-service model, not just raw optical capacity. Standards such as ITU-T G.709 optical transport network framing and IETF YANG data models are also shaping software architecture choices in regional tenders, as operators seek interoperability across expanding transport estates. As a result, the component mix in the Middle East and Africa 5G fiber backbone transport market is still led by hardware, but future differentiation is increasingly moving toward software-defined management layers.

By Capacity: Installed 100G Networks are Giving Way to Higher-Capacity Routes

The 10 to 100 Gbps segment accounted for 50.59% of the Middle East and Africa 5G fiber backbone transport market in 2025, reflecting the large installed base of coherent 100G systems built during the 4G-to-5G transition. Many carriers across the region are still running these systems near capacity, so this tier remains the present backbone of commercial operations. At the same time, above 100 Gbps is projected to expand at a 20.20% CAGR from 2026 to 2031 as data center interconnect traffic rises in the GCC and 5G transport loads increase in major African metros. The up to 10 Gbps tier still has a role in remote terrestrial links and early-stage backhaul routes in frontier African markets where traffic density has not yet justified a move to higher-capacity platforms. This mix means the Middle East and Africa 5G fiber backbone transport market has both a large legacy installed base and a fast upgrade cycle.

Commercial moves in 2025 and 2026 show that the shift toward higher-capacity transport is already happening in live networks rather than remaining a plan. e& UAE upgraded its EMIX IP transit backbone to 400G in partnership with Cisco in December 2025, extending higher-capacity services to international points of presence and demonstrating that operator demand has moved beyond early pilots. Nokia, e& UAE, and NPS then used hollow-core fiber in a 2026 trial at 153 Tbps, pointing to a future where the above 100 Gbps category will also include multi-Tbps single-fiber performance. Procurement teams in the Middle East and Africa 5G fiber backbone transport market, therefore, need to plan new fiber routes against a much wider future performance range than older 100G planning models assumed. This makes capacity decisions more sensitive because fiber laid for today’s upgrade cycle will need to support much larger workloads over the rest of the forecast window.

By Application: Fronthaul and Midhaul are Moving to the Center of Spending

Mobile network backhaul held a 43.24% share in 2025, confirming that it remained the main application in the Middle East and Africa 5G fiber backbone transport market during the current build cycle. GCC 5G macro rollouts and long-haul African links between major population centers still depend heavily on backhaul spending, which continues to drive application demand. Fronthaul and midhaul, however, are projected to expand at a 27.12% CAGR from 2026 to 2031, which makes them the fastest-growing applications as operators move deeper into disaggregated 5G transport. This shift is significant because it creates a procurement category that was far less important in the 4G-era transport design. Data center interconnect is also becoming a stronger application area in the GCC as cloud and AI hubs build more direct high-capacity optical links between facilities.

Transport standards are tightening the technical needs of this application mix and raising the value of precision infrastructure. The O-RAN Alliance Working Group 4 specification requires fronthaul links to meet IEEE 802.1CM Class D timing with sub-microsecond jitter tolerance, which means many operators need to separate or upgrade infrastructure that was previously shared with backhaul traffic. ADNOC, G42, and Khazna Data Centers have all been upgrading interconnects to 400G optics, while du partnered with Datawave Networks in April 2026 to land the SING submarine cable at Kalba with 16 fiber pairs and at least 18Tbps per pair. Enterprise and private 5G transport adds another layer of demand as GCC ports, industrial zones, and large projects commission their own secure transport routes. Ducab Group’s 2025 launch of the GCC’s first high-voltage fiber-optic cable also showed that energy and digital infrastructure needs are increasingly overlapping in project planning.

By End User Industry: Hyperscale Demand is Broadening the Buyer Base

Mobile network operators held 56.67% of the Middle East and Africa 5G fiber backbone transport market share in 2025, making them the largest end-user group in the region. Their position remains strong because they still control the biggest transport budgets across GCC backbone programs and African national network expansions. Cloud and hyperscale providers, however, are projected to expand at a 26.47% CAGR from 2026 to 2031, which makes them the fastest-growing end-user category. That growth comes from pre-committed bandwidth agreements tied to new cloud zones and colocation sites, especially in the GCC, where operators often need to secure transport capacity before the service ramp is complete. This means the Middle East and Africa 5G fiber backbone transport market is no longer driven only by telecom carriers, because hyperscalers are becoming a more direct source of optical demand.

The end-user mix is also widening, as several other buyer groups are beginning to procure their own transport assets. Government AI strategies in the UAE and Saudi Vision 2030 are bringing hyperscalers into long-term co-location commitments that directly support dark fiber and wavelength service demand. Internet service providers remain an important group, and Tejas Networks reported in its Q4 FY26 results that it won a DWDM backbone buildout contract from a broadband ISP in Africa in 2026. Enterprises and private networks remain smaller in volume, but they offer higher-margin opportunities for oil and gas operators, ports, and financial institutions that need secure, low-latency transport. Public-sector and public-safety buyers are also becoming more active in the Middle East and Africa 5G fiber backbone transport industry because sovereign security rules are encouraging domestic routing of sensitive traffic in markets such as Saudi Arabia, the UAE, and Egypt.

Geography Analysis

The Middle East accounted for 66.46% of the Middle East and Africa 5G fiber backbone transport market in 2025, making it the leading regional cluster by a wide margin. Saudi Arabia remains the anchor market because national digital infrastructure programs, data center investments, and backbone upgrades are all moving at scale. Nokia and stc Group completed a 1Tbps long-haul field trial over 850 km in January 2025, demonstrating that super-coherent long-haul backbone transport is ready for commercial deployment on Saudi routes. Mobily also announced USD 905 million in investments at LEAP 2025 across data centers, subsea cables, and backbone fibers, which supported the country’s push to localize digital traffic and strengthen its hub status. The UAE is also acting as a technology proving ground, as e& UAE deployed WaveLogic 6 Extreme in February 2025 and later validated hollow-core fiber at 153Tbps with Nokia and NPS in 2026.

Turkey and Qatar continue to strengthen their roles as transit nodes in the wider Middle East transport system. Ooredoo’s Fiber in the Gulf cable was announced in 2025, with 720Tbps across 24 fiber pairs connecting all GCC states and Iraq, underscoring the scale of regional interconnection commitments now moving forward. The Iraqi-UAE World Link Transit Cable Project also moved forward in 2026, with more than 900Tbps of planned aggregate capacity and sub-100-millisecond latency between European and Middle Eastern nodes, supporting a carrier-neutral east-west corridor. Africa is the fastest-growing geography in the Middle East and Africa 5G fiber backbone transport market, projected to expand at a 20.77% CAGR through 2031. MTN Group stated in 2026 that it plans to increase its pan-African fiber footprint from 140,000 km to between 420,000 km and 560,000 km by 2030, while Bayobab is targeting a doubling of subsea capacity over the same period.

Kenya and Nigeria remain the clearest near-term African transport markets because both are combining 5G expansion with backbone investment. Ericsson deepened its transport work with Safaricom in 2025 to strengthen Kenya’s 5G network, and Seacom activated a 1Tbps Nairobi-Kampala terrestrial route that can scale to 30Tbps, which improved East African backbone readiness for cloud and AI traffic. North Africa deserves separate attention because Algeria, Morocco, and Egypt are each pursuing distinct infrastructure models. Algeria launched commercial 5G in December 2025, following the deployment of a 400G WDM national backbone by Algerie Telecom and Huawei across all 58 wilayas in February 2025. Morocco authorized Uni Fiber and Uni Tower in June 2025 with MAD 4.4 billion (USD 450 million) in first-phase passive infrastructure investment, while Egypt continues to benefit from Mediterranean cable landing activity, including the Medusa system, a EUR 342 million (USD 376 million) project with a planned Egyptian landing point.

Competitive Landscape

The Middle East and Africa 5G fiber backbone transport market concentration remains semi-consolidated, with Huawei Technologies, Nokia Corporation, Ciena Corporation, ZTE Corporation, and Telefonaktiebolaget LM Ericsson leading many of the largest tenders across GCC operators and Tier-1 African carriers. These firms anchor high-value projects by combining optical hardware, long-haul transport experience, and broader telecom relationships across the region. Chinese vendors continue to hold a cost advantage in several African markets, while Western suppliers compete more strongly on coherent optics performance, software control, and managed service layers. The result is a market where scale matters, but product roadmaps and service depth matter just as much in final vendor selection. This balance keeps the Middle East and Africa 5G fiber backbone transport market open to both large incumbents and a second tier of more targeted suppliers.

Nokia materially strengthened its position in January 2025 when it completed the USD 2.3 billion acquisition of Infinera, which expanded its coherent optics depth across metro, regional, and long-haul transport. Huawei demonstrated continued execution strength in Africa through the MTN Nigeria 400G-800G ASON deployment in July 2025 and Algerie Telecom’s national 400G WDM backbone in February 2025, confirming its ability to deliver across both frontier and large, sovereign-backed networks. Ciena has also been using a service-led approach, as shown by Omantel’s Managed Optical Fiber Network launch in 2025, which included SLA monitoring, bandwidth-on-demand, and automated provisioning. These examples show that major suppliers are not relying solely on hardware sales, because service wrappers and software capabilities now affect buying decisions more directly.

A second group, including Ribbon Communications, Ekinops, ADTRAN Holdings through its ADVA optical division, Tejas Networks, and FiberHome, is competing more actively in markets where budgets are tighter or buyers want more open architectures. Ekinops’s OpenROADM-aligned positioning and Tejas Networks’ DWDM offerings create room in ISP and enterprise projects where full Tier-1 pricing is harder to support. Gulf Bridge International’s selection of Nokia’s 1830 Global Express platform in October 2025 for a new terrestrial route in Iraq also showed that buyers are placing greater weight on future upgrade roadmaps than on current hardware specifications alone. White-box and disaggregated optical approaches are beginning to erode proprietary bundle economics, but integration complexity still limits this model to operators with deeper in-house engineering. That is why large incumbents still keep an advantage in the Middle East and Africa 5G fiber backbone transport market, where many carriers want managed support in addition to equipment delivery.

Middle East and Africa 5G Fiber Backbone Transport Industry Leaders

Huawei Technologies Co., Ltd.

Nokia Corporation

Ciena Corporation

ZTE Corporation

Telefonaktiebolaget LM Ericsson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MTN Group's Capital Markets Day 2026 announced plans to grow its pan-African fiber footprint three-fold from 140,000 km to between 420,000 km and 560,000 km by 2030, with subsidiary Bayobab targeting a doubling of subsea capacity over the same period. This commitment represented one of the largest disclosed transport infrastructure expansion programs in Africa's telecoms history and directly underpinned the region's 5G backhaul upgrade cycle.

- May 2026: Kuwait signed a KD 825 million (USD 2.69 billion) 50-year public-private partnership agreement with Bahrain's Beyon Group to design, finance, build, operate, and maintain Kuwait's national fixed telecommunications network, targeting fiber coverage to 90% of the country. The deal was signed by the Ministry of Communications, the Kuwait Authority for Partnership Projects, and Beyon, and formed the backbone of Kuwait's Vision 2035 digital transformation strategy.

- May 2026: Telecom Egypt and Huawei deepened their partnership in an accelerated national fiber push, part of Egypt's infrastructure modernization cycle tied to preparations for 5G expansion. Egypt has invested USD 6 billion in fixed and mobile internet infrastructure since 2019, aiming to strengthen its position as a regional connectivity hub.

Middle East and Africa 5G Fiber Backbone Transport Market Report Scope

The Middle East and Africa 5G fiber backbone transport market revenue is generated through the sale of optical transport hardware, transport network management and orchestration software, and professional services including network planning, deployment, integration, managed services, maintenance, and optimization, serving mobile network operators, internet service providers, cloud and hyperscale providers, enterprises, and government organizations supporting 5G connectivity and high-speed data transport. The Middle East and Africa 5G fiber backbone transport market report is segmented by component (hardware, software and network management, and services), capacity (up to 10 Gbps, 10 to 100 Gbps, and above 100 Gbps), application (mobile network backhaul, mobile network fronthaul and midhaul, data center interconnect, enterprise and private 5G transport, and other applications (submarine landing station backhaul, etc.)), end user industry (mobile network operators, internet service providers, cloud and hyperscale providers, enterprises and private networks, and other end user industry (government and public safety, etc.)), and geography (Middle East and Africa). The market forecasts are provided in value (USD).

| Hardware (Includes Optical Transport Systems, DWDM and ROADM Platforms, Packet-Optical Transport Platforms, Routers and Switches, Fiber Optic Cables, Optical Transceivers, Amplifiers, and OTN Equipment) |

| Software and Network Management (Includes Network Management Systems, SDN Controllers, Transport Orchestration Software, Analytics and Assurance Tools, Automation Platforms, and Inventory Management Software) |

| Services (Includes Network Planning and Design, Deployment and Installation, Integration and Commissioning, Managed Services, Maintenance and Support, Optimization, Consulting, and Training) |

| Up to 10 Gbps |

| 10 to 100 Gbps |

| Above 100 Gbps |

| Mobile Network Backhaul |

| Mobile Network Fronthaul and Midhaul |

| Data Center Interconnect |

| Enterprise and Private 5G Transport |

| Other Applications (Submarine Landing Station Backhaul, etc.) |

| Mobile Network Operators |

| Internet Service Providers |

| Cloud and Hyperscale Providers |

| Enterprises and Private Networks |

| Other End User Industry (Government and Public Safety, etc.) |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Kenya | |

| Rest of Africa |

| By Component | Hardware (Includes Optical Transport Systems, DWDM and ROADM Platforms, Packet-Optical Transport Platforms, Routers and Switches, Fiber Optic Cables, Optical Transceivers, Amplifiers, and OTN Equipment) | |

| Software and Network Management (Includes Network Management Systems, SDN Controllers, Transport Orchestration Software, Analytics and Assurance Tools, Automation Platforms, and Inventory Management Software) | ||

| Services (Includes Network Planning and Design, Deployment and Installation, Integration and Commissioning, Managed Services, Maintenance and Support, Optimization, Consulting, and Training) | ||

| By Capacity | Up to 10 Gbps | |

| 10 to 100 Gbps | ||

| Above 100 Gbps | ||

| By Application | Mobile Network Backhaul | |

| Mobile Network Fronthaul and Midhaul | ||

| Data Center Interconnect | ||

| Enterprise and Private 5G Transport | ||

| Other Applications (Submarine Landing Station Backhaul, etc.) | ||

| By End User Industry | Mobile Network Operators | |

| Internet Service Providers | ||

| Cloud and Hyperscale Providers | ||

| Enterprises and Private Networks | ||

| Other End User Industry (Government and Public Safety, etc.) | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the Middle East and Africa 5G fiber backbone transport market?

The Middle East and Africa 5G fiber backbone transport market was valued at USD 1.56 billion in 2025, stands at USD 1.82 billion in 2026, and is projected to reach USD 4.31 billion by 2031 at a CAGR of 18.82%.

What is driving demand for 5G fiber backbone transport across the Middle East and Africa?

Demand is being supported by 5G rollout density, data center interconnect growth, and sovereign digital infrastructure programs across the GCC and North Africa.

Which application is growing the fastest in this sector?

Fronthaul and midhaul is projected to expand at a 27.12% CAGR through 2031 as operators adopt Open RAN and tighter transport timing requirements.

Which end-user group leads spending on backbone transport?

Mobile network operators held 56.67% share in 2025, but cloud and hyperscale providers are projected to grow faster at a 26.47% CAGR through 2031.

Why is Africa the fastest-growing geography through 2031?

Africa is projected to expand at a 20.77% CAGR because mobile-led 5G densification, terrestrial fiber expansion, and subsea landing investments are all lifting backhaul demand.

What is changing vendor competition in optical transport networks?

Competition is shifting from hardware alone toward coherent optics performance, software-defined control, managed services, and future upgrade roadmaps, especially in GCC and Tier-1 African projects.

Page last updated on: