Middle East AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

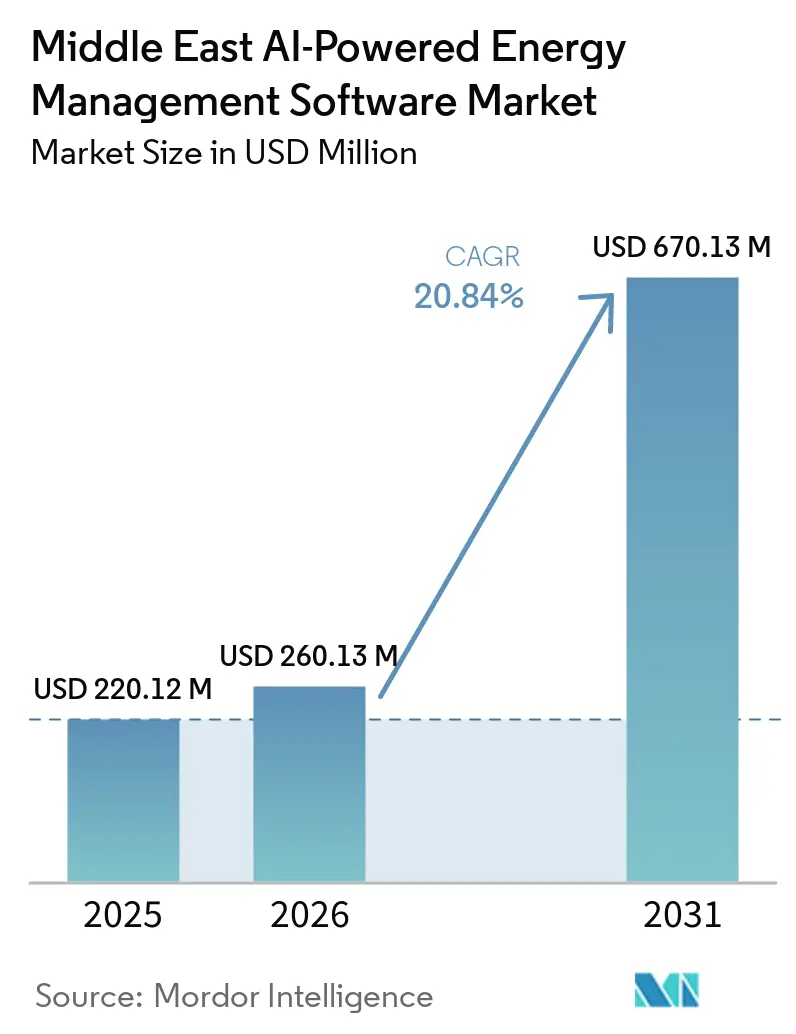

| Base Year Market Size (2025) | USD 220.12 Million |

| Market Size (2026) | USD 260.13 Million |

| Market Size (2031) | USD 670.13 Million |

| Growth Rate (2026 - 2031) | 20.84% CAGR |

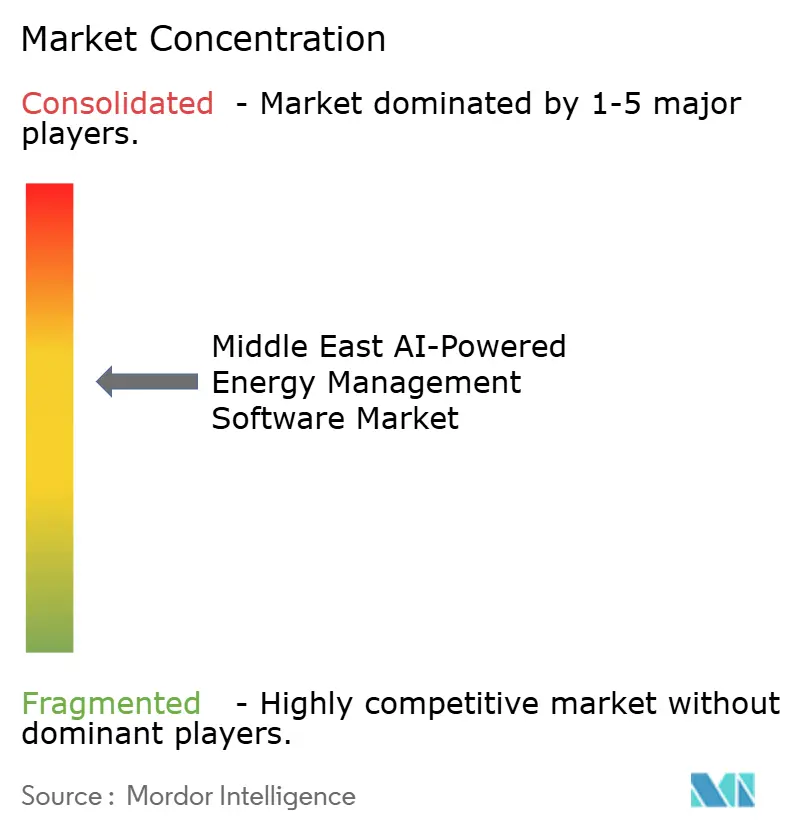

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Middle East AI-powered Energy Management Software Market size is projected to expand from USD 220.12 million in 2025 and USD 260.13 million in 2026 to USD 670.13 million by 2031, registering a CAGR of 20.84% between 2026 and 2031. The growth path reflects a clear move away from reactive energy monitoring and toward software-led optimization across utilities, commercial assets, and industrial facilities. National energy transition programs in Saudi Arabia and the UAE are making digital energy management more central to compliance, operating discipline, and long-term competitiveness. Renewable capacity additions, grid digitization programs, and rising volumes of operating data are increasing the need for platforms that can convert data into practical actions across forecasting, load balancing, and maintenance planning. Competition is now shaped less by basic platform availability and more by hybrid deployment design, regulatory fit, and the ability to support enterprise-wide rollouts with service layers. The strongest opportunities are forming where large users need better visibility across multiple sites, tighter control over energy intensity, and stronger integration between traditional infrastructure and AI-led analytics.

Key Report Takeaways

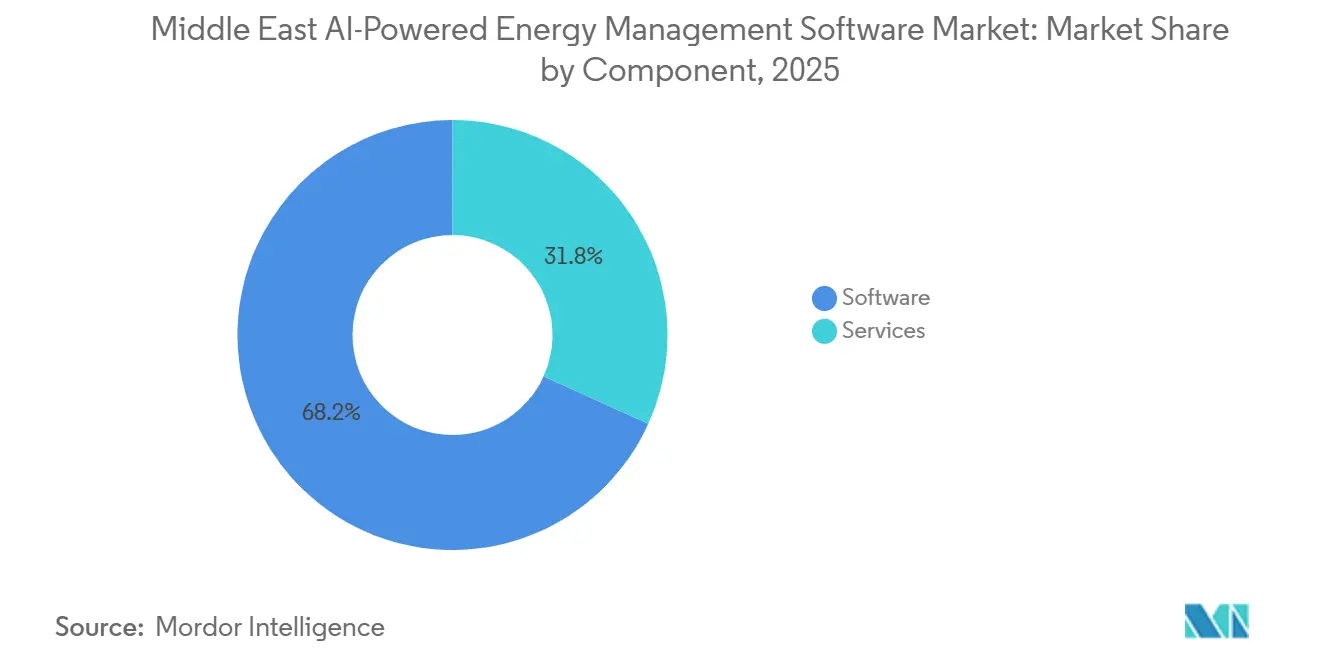

- By component, software held 68.22% of the Middle East AI-powered Energy Management Software Market share in 2025, while services are projected to expand at a 20.91% CAGR through 2031.

- By deployment mode, cloud-based accounted for 58.14% of the Middle East AI-powered Energy Management Software Market size in 2025, while hybrid is projected to grow at a 21.02% CAGR through 2031.

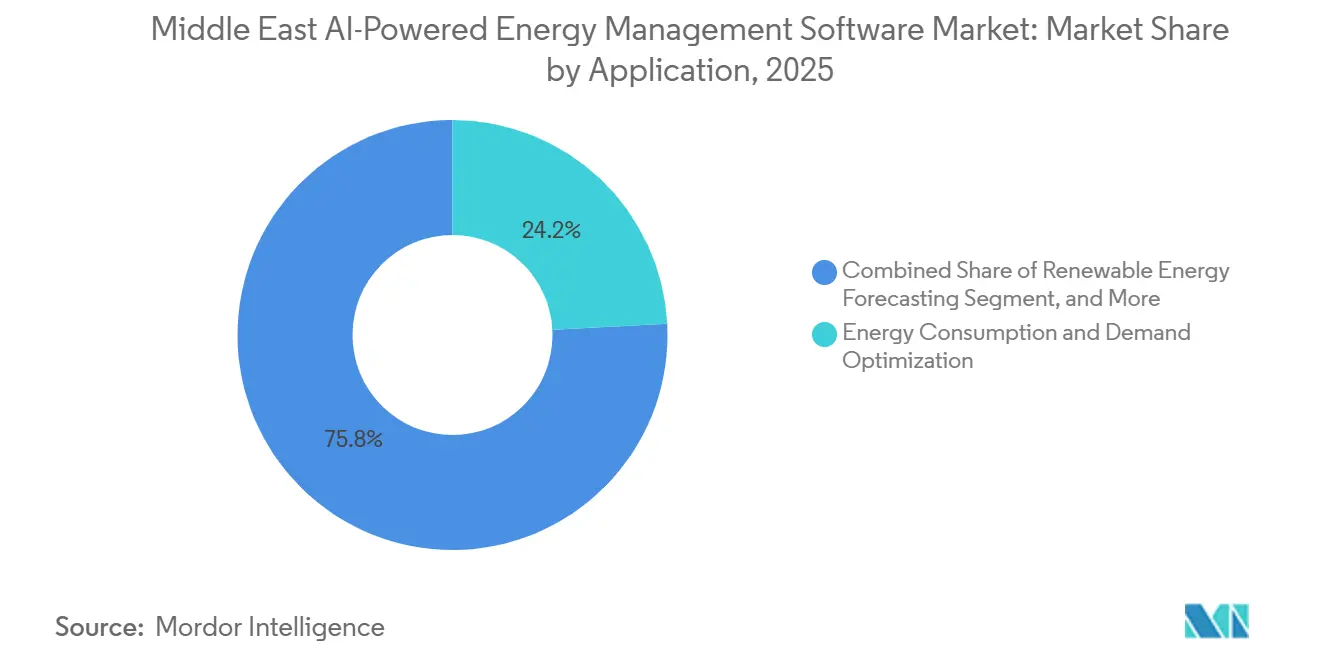

- By application, energy consumption and demand optimization accounted for 24.17% of the Middle East AI-powered Energy Management Software Market size in 2025, while renewable energy forecasting and integration are projected to expand at a 21.13% CAGR through 2031.

- By end user, utilities accounted for 33.12% of the Middle East AI-powered Energy Management Software Market in 2025, while industrial facilities are projected to grow at a 21.24% CAGR through 2031.

- By geography, Saudi Arabia held 34.18% of the Middle East AI-powered Energy Management Software Market share in 2025, while the UAE is projected to record the fastest growth at a 21.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Smart Grid and Utility Digitization In GCC States | +5.5% | GCC-wide, concentrated in Saudi Arabia and the UAE | Short term (≤ 2 years) |

| Rising Demand for AI-Driven Load Forecasting in Commercial Buildings | +4.2% | UAE, Saudi Arabia, Qatar core, with spillover to the rest of the Middle East | Short term (≤ 2 years) |

| Mandatory Energy Efficiency Targets Under National Decarbonization Programs | +3.8% | GCC-wide, with early gains in Saudi Arabia, the UAE, and Qatar | Medium term (2-4 years) |

| Expansion of Cloud-Native Enterprise Energy Platforms | +3.2% | Regional, with concentrated uptake in the UAE and Saudi Arabia | Short term (≤ 2 years) |

| Increasing Need for Predictive Maintenance Across Energy-Intensive Assets | +2.1% | Saudi Arabia, the UAE, and Kuwait across oil and gas and petrochemicals | Medium term (2-4 years) |

| Greater Deployment of Submetering And IoT Sensor Networks in Large Facilities | +1.5% | UAE, Saudi Arabia, and Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Smart Grid and Utility Digitization in Gulf Cooperation Council States

The Middle East AI-powered Energy Management Software Market is gaining direct support from utility digitization programs because grid operators now need software that can interpret high-frequency operational data rather than simply collect it. Saudi Arabia and the UAE are moving ahead with grid modernization agendas that place predictive analytics, automation, and digital operating tools closer to core utility processes rather than in pilot-stage experimentation. Abu Dhabi's Department of Energy signed an agreement with Google Cloud in October 2025 to apply AI and machine learning to grid management, demand forecasting, and predictive maintenance, which shows how grid digitization is translating into software procurement.[1]Abu Dhabi Media Office, “Abu Dhabi Department of Energy Signs Agreement With Google Cloud at GITEX Global 2025, Advancing Digital Transformation in the Energy Sector,” Abu Dhabi Media Office, mediaoffice.abudhabi The same shift is expanding AI's role from back-office reporting to real-time operational support across power plants, renewable assets, and distribution systems. As utilities build larger digital control environments, vendors that can integrate forecasting, maintenance, and energy optimization into a single operating layer are likely to gain an advantage in the Middle East AI-powered Energy Management Software Market. Procurement is also becoming broader across the GCC because software requirements now come from system visibility, operating resilience, and renewable balancing needs simultaneously.

Rising Demand for AI-Driven Load Forecasting in Commercial Buildings

The Middle East AI-powered Energy Management Software Market is seeing stronger demand from commercial buildings because energy use in offices, retail sites, hospitality assets, and mixed-use properties is increasingly tied to cooling loads, compliance targets, and utility cost management. Building owners are no longer looking only for monitoring dashboards, and they increasingly want forecasting tools that can help manage peak demand, schedule consumption, and improve operational control without replacing entire building systems. The UAE's push toward broader energy visibility and emissions accountability from 2026 is strengthening the commercial case for digital energy platforms that can organize site-level performance data into usable decisions. Schneider Electric expanded its EcoStruxure Building platform across 26 Brands For Less stores in the UAE in May 2026, demonstrating that software-led building optimization is moving beyond flagship properties into multi-site commercial portfolios.[2]Schneider Electric, “Schneider Electric and Brands For Less Group Partner to Advance Low Carbon, Smart Retail Environments in the UAE,” mid-east.info, mid-east.info This matters for the Middle East AI-powered Energy Management Software Market because mid-market property operators usually need faster payback and less disruption than large custom projects can offer. As a result, vendors that provide modular forecasting, remote optimization, and easier integration with existing building systems are gaining a wider addressable base in the region.

Mandatory Energy Efficiency Targets Under National Decarbonization Programs

The Middle East AI-powered Energy Management Software Market is also being supported by policy frameworks that treat energy efficiency as a measurable obligation rather than a voluntary improvement program. Abu Dhabi's Demand Side Management and Energy Rationalization Strategy targets a 22% reduction in electricity consumption by 2030, keeping energy measurement and optimization high on the agenda for both public and private assets. Saudi Arabia's National Sustainability Strategy established sector-based emissions budgets and a monitoring, reporting, and verification framework, underscoring the need for granular, machine-readable energy data across buildings, infrastructure, and industrial operations.[3]Abu Dhabi Media Office, “Abu Dhabi Aims to Cut Power Sector Emissions Intensity 75% by 2035,” Zawya, zawya.com This policy setup changes buying behavior because software shifts from being a discretionary efficiency tool to part of the reporting and control framework behind national targets. The same pattern is visible across hydrocarbon operations, where energy intensity, carbon accounting, and process efficiency are increasingly linked in one operating discussion. In practical terms, these programs support the Middle East AI-powered Energy Management Software Market, even when broader spending conditions are uneven, because compliance-driven projects tend to remain on procurement roadmaps longer than purely optional technology upgrades.

Expansion of Cloud-Native Enterprise Energy Platforms

The Middle East AI-powered Energy Management Software Market is benefiting from the growth of cloud-native platforms, as multi-site operators seek a unified view across assets previously managed in separate systems. Cloud architecture helps aggregate information from refineries, substations, commercial towers, data centers, and renewable assets into a single operating environment, improving benchmarking and decision speed across large portfolios. Abu Dhabi's Department of Energy moved in this direction through its Google Cloud agreement, and the UAE Ministry of Energy and Infrastructure also backed a February 2026 pilot with Khazna Data Centers, Agility, and Phaidra AI to optimize energy efficiency in hyperscale data center campuses.[4]A. Hamdan et al., “AI-UBREM Data-Driven Model Using Neural Networks for Energy Digital Twining,” Journal of Umm Al-Qura University for Engineering and Architecture, springer.com Academic work is also reinforcing market confidence, as a peer-reviewed study validated neural network-based building energy prediction and solar potential estimation for digital twinning applications, thereby strengthening the technical basis for these deployments. The commercial advantage is now shifting toward vendors that can combine the scale benefits of cloud platforms with configurations that comply with local data-handling rules. That is why a sovereign-ready and hybrid-ready design is becoming a more important competitive factor in the Middle East AI-powered Energy Management Software Market than basic cloud availability alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Sovereignty Concerns Slowing Cloud Migration | -2.4% | GCC-wide, most acute in Saudi Arabia and Qatar | Short term (≤ 2 years) |

| Integration Complexity With Legacy Building And Industrial Control Systems | -1.8% | GCC-wide, most pronounced in older petrochemical and utility assets | Medium term (2-4 years) |

| Limited AI Skills And Implementation Capacity Among End Users | -1.3% | Rest of Middle East, with moderate pressure in Saudi Arabia and Qatar | Medium term (2-4 years) |

| Fragmented Utility Tariff And Regulatory Structures Across The Region | -0.9% | Cross-border operators, most acute for pan-GCC deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Sovereignty Concerns Slowing Cloud Migration

The Middle East AI-powered Energy Management Software Market faces a real constraint due to data sovereignty, as many buyers handle sensitive grid data, plant telemetry, building controls, and infrastructure information. Saudi Arabia's localization rules have increased the cost of cross-border cloud design, and the broader GCC environment remains uneven because residency expectations differ by country and by application. The draft Global AI Hub Law in Saudi Arabia suggests that more flexible structures may emerge over time, but the current period still leaves vendors navigating compliance uncertainty when they architect regional offerings. This slows adoption because enterprises often choose hybrid or country-specific deployments that are legally safer but less efficient than a single regional cloud environment. Smaller specialists are affected more than incumbents because building sovereign-compliant infrastructure and certification layers requires capital, local presence, and longer sales support. The result is not a collapse in demand, but a slower transition path for fully cloud-native models in the Middle East AI-powered Energy Management Software Market.

Integration Complexity With Legacy Building and Industrial Control Systems

The Middle East AI-powered Energy Management Software Market is also constrained by the age and diversity of legacy operational technology across utilities, petrochemical plants, and older large buildings. Many facilities still use control systems that were never designed for continuous data exchange with modern AI applications, making integration a staged engineering task rather than a simple software deployment. Industry discussions at ADIPEC 2025 highlighted unsupported operating systems, cybersecurity exposure, and disruption risk as core barriers to connecting new analytics layers to long-running industrial environments. The cybersecurity backdrop adds further caution, as ransomware activity targeting energy and utilities systems increased in 2024, prompting operators to be more selective about when and how they expose older control assets to new software layers. This extends implementation cycles and shifts buying preference toward modular deployment models that can sit alongside existing systems before deeper integration. Vendors that reduce disruption and limit downtime are therefore in a stronger position than vendors that require broad infrastructure replacement at the start of the project.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Holds The Lead, Services Expand Faster

Software held 68.22% of the Middle East AI-powered Energy Management Software Market share in 2025, which confirms that buyers still place the greatest value on platforms that can centralize analytics, forecasting, optimization, and control workflows. The leading role of software also reflects the region's preference for scalable platforms that can serve large utilities, commercial portfolios, and industrial networks without being confined to a single site deployment. In the Middle East AI-powered energy management software industry, platform breadth matters because customers increasingly want one operating layer that can support demand management, maintenance planning, renewable balancing, and reporting requirements at the same time. This explains why software demand remains strongest where procurement decisions are tied to enterprise licenses, integrated dashboards, and long-term digital transformation programs rather than narrow application tools. It also means that product depth, ease of integration, and compliance fit are becoming as important as core analytics performance when buyers evaluate suppliers.

Services is projected to expand at a 20.91% CAGR through 2031, which shows that many deployments still need outside support for integration, model tuning, change management, and ongoing optimization. This growth pattern suggests the Middle East AI-powered Energy Management Software Market is moving beyond first-stage software rollout and toward a longer cycle of recalibration, site expansion, and operational support. A peer-reviewed study validated a multi-agent framework for automating building load forecasting model development, which points to the kind of service-intensive use cases vendors can package around software subscriptions in coming years. The same logic is visible in enterprise contracts, where buyers increasingly value expert support that helps internal teams move from data collection to measurable operational improvement. C3.ai's June 2026 expansion of its agreement with Shell, including AI agent-based root cause analysis across more than 13,000 pieces of equipment, illustrates how long-term service engagement can deepen once the platform is already embedded.

By Deployment Mode: Cloud Leads Adoption, Hybrid Gains Momentum

Cloud-based deployment accounted for 58.14% of the Middle East AI-powered Energy Management Software Market in 2025, indicating that buyers still favor scalability, update speed, and lower upfront infrastructure costs where regulation allows. Cloud adoption has been strongest where organizations manage multiple assets and need centralized visibility across large operating footprints. In the Middle East AI-powered energy management software industry, this model is attractive because it helps standardize performance tracking across buildings, grids, industrial sites, and energy-intensive service environments. It also aligns with procurement preferences among enterprises that want subscription models, remote management capability, and quicker platform upgrades than older on-premises environments can usually support. At the same time, cloud leadership in 2025 does not mean regulation is no longer a barrier, because deployment choices still depend heavily on where operational data sits and how sensitive that data is deemed to be.

Hybrid deployment is projected to expand at a 21.02% CAGR through 2031, underscoring how the region is settling on a middle path between cloud efficiency and sovereignty requirements. The appeal of hybrid design lies in its ability to keep sensitive telemetry close to the asset while still enabling broader analytics, optimization, and portfolio reporting across a wider enterprise. The February 2026 Phaidra AI pilot involving the UAE Ministry of Energy and Infrastructure, Khazna Data Centers, and Agility showed how energy optimization can be advanced within a compliant local operating structure rather than through a purely offshore cloud setup. This architecture is becoming increasingly strategically important in the Middle East AI-powered Energy Management Software Market, as buyers increasingly seek flexibility without incurring unnecessary regulatory exposure. Vendors that built hybrid capability into the core product are therefore better placed than those now trying to retrofit limited on-premises features onto a cloud-first offering.

By Application: Demand Optimization Anchors Revenue, Renewable Forecasting Rises Fastest

Energy consumption and demand optimization accounted for 24.17% of the Middle East AI-powered Energy Management Software Market in 2025, reflecting the immediate value buyers place on reducing peak demand charges and improving load control. This application remains central because it delivers results that operating teams can track more directly than some longer-cycle decarbonization tools. Demand optimization is also relevant to a broader range of end users than many other applications, since utilities, commercial buildings, and industrial facilities all face pressure to manage power use more efficiently. Asset performance and predictive maintenance remain close behind in strategic importance because operators increasingly link energy waste, equipment reliability, and maintenance planning in a single performance discussion. Saudi Aramco expected USD 3-5 billion of technology-realized value in 2025 from AI-led predictive maintenance and reservoir management, which strengthens the business case for connected energy and asset intelligence across industrial operations.

Renewable energy forecasting and integration is projected to grow at a 21.13% CAGR through 2031, making it the fastest-moving application in the Middle East AI-powered Energy Management Software Market. The main reason is structural rather than cyclical, as larger renewable pipelines increase the operational need for generation forecasting, ramp management, and grid-balancing support. Saudi Arabia's renewable program has reached 43.2 GW of signed capacity, with 12.3 GW already connected to the grid, creating a much larger operating base for AI-led forecasting tools. A peer-reviewed study covering all 6 GCC countries validated a deep hybrid forecasting framework using nearly 49 million hourly observations from 2018 to 2024, which confirms that regional solar forecasting models are becoming more robust for dust-affected and arid conditions. EWEC and Khalifa University also partnered on machine learning modules for grid technologies, demonstrating that utilities are aligning research and operational needs as renewable penetration rises.

By End User: Utilities Lead Revenue, Industrial Facilities Advance Fastest

Utilities accounted for 33.12% of the Middle East AI-powered Energy Management Software Market in 2025, reflecting the scale of grid modernization programs and the central role of state-backed energy enterprises in regional procurement. Large utilities have broader data environments, more complex load-balancing needs, and larger capital programs than most other buyers, which gives them a natural lead in software adoption. Their position is also reinforced by the fact that utilities are often closest to regulatory expectations for reliability, efficiency, renewable integration, and demand forecasting. Commercial buildings remain an important user group because the need for energy visibility is spreading across office, retail, hospitality, and mixed-use assets that want lower operating costs and stronger emissions reporting. Residential demand is still smaller in revenue terms because household adoption depends more heavily on smart meter reach, digital interfaces, and broader building automation maturity than enterprise categories do.

Industrial facilities are projected to grow at a 21.24% CAGR through 2031, making them the fastest-expanding end-user segment in the Middle East AI-powered Energy Management Software Market. The growth is strongest where petrochemicals, upstream oil and gas, desalination, and manufacturing operations are trying to reduce energy intensity without losing process stability or reliability. Kuwait Oil Company's USD 300 million, 5-year predictive maintenance program launched in 2026 shows how industrial users are now committing at a scale that materially raises software demand across engineering, analytics, and operating support layers. The industrial case is also strengthened by the fact that energy efficiency, downtime reduction, and emissions management often improve together when predictive and optimization tools are deployed well. That makes industrial adoption less dependent on a single narrow use case and more tied to broader operating performance, which supports a durable growth profile for this segment over the forecast period.

Geography Analysis

Saudi Arabia accounted for 34.18% of the Middle East AI-powered Energy Management Software Market share in 2025, maintaining its leading geographic position across the region. Its lead comes from the scale of its utility modernization agenda, the depth of its industrial energy base, and the policy weight behind long-term decarbonization and digital transformation efforts. The Middle East AI-powered Energy Management Software Market has a strong anchor in Saudi Arabia, as large public and industrial operators are under pressure to improve efficiency, integrate more renewable capacity, and support broader national transformation targets. Saudi Arabia's National Sustainability Strategy created a monitoring, reporting, and verification framework with sector-based emissions budgets, which supports recurring software demand tied to data quality and compliance discipline. The country's renewable buildout also supports application growth, as signed renewable capacity has already reached 43.2 GW, with 12.3 GW connected to the grid, underscoring the need for generation forecasting and balancing tools.

The UAE is projected to record the fastest growth at a 21.31% CAGR through 2031, which reflects a more diversified demand base across utilities, buildings, renewable assets, and data centers. Abu Dhabi's electricity demand reached 155 TWh in 2025 and is projected to rise to 184 TWh by 2030, underscoring the need to keep forecasting, optimization, and grid efficiency at the center of investment priorities. The UAE is also moving quickly to adopt digital operating models, as seen in Abu Dhabi's agreement with Google Cloud to support AI and machine learning for grid management, demand forecasting, and predictive maintenance. This combination of high power demand growth, active digital partnerships, and broader non-oil commercial demand gives the UAE a wider adoption base than many neighboring markets.

Qatar and the Rest of the Middle East remained earlier-stage contributors to the Middle East AI-powered Energy Management Software Market, but their roles are broadening as digital utility programs and renewable energy plans advance. Qatar's Kahramaa is expanding renewable energy integration and digital transformation of subscriber services, which supports demand for forecasting, billing accuracy, and grid management software. Oman also strengthened its long-term direction in 2026 through an updated net-zero roadmap and a carbon market framework, which improve the case for renewable forecasting and distributed energy management applications. These markets remain smaller than Saudi Arabia and the UAE, but they are expanding the regional demand base and reducing the risk that future growth remains concentrated in only 2 countries.

Competitive Landscape

The Middle East AI-powered Energy Management Software Market is moderately consolidated at the platform level, with Schneider Electric, Siemens, Honeywell, and ABB holding strong positions in large utility and industrial opportunities. Their advantage comes from established customer relationships, regional delivery capability, and the ability to combine hardware, software, and managed support into one commercial offering. This matters because many buyers prefer a supplier that can address integration, compliance, and long-cycle service needs together, rather than sourcing each layer from a separate specialist. Large incumbents are also better prepared for sovereign and hybrid deployment requirements because they have more resources to localize infrastructure and support. As a result, the Middle East AI-powered Energy Management Software Market still rewards scale, but that scale must be matched by strong execution of AI use cases rather than legacy presence alone.

Strategic moves in 2025 and 2026 show how leading vendors are defending and extending their position. C3.ai and Shell expanded their collaboration in June 2026 to scale reliability AI and add agent-based root-cause analysis across more than 13,000 pieces of equipment, highlighting the value of deeper enterprise penetration after an initial deployment succeeds. Honeywell and Kortech signed an MoU in February 2026 to automate and digitize critical infrastructure projects across Egypt, Saudi Arabia, and the UAE, which shows how global firms are pairing software and analytics with regional engineering channels. The UAE Ministry of Energy and Infrastructure's pilot with Khazna, Agility, and Phaidra AI also showed that regional programs are creating space for specialized AI partners within larger energy optimization initiatives.

Smaller, AI-native vendors are still finding room in targeted use cases, especially where speed, model specialization, or application focus matter more than a broad installed base. Bidgely's acquisition of Grid4C in 2025 reflected the need for smaller players to combine capabilities as utility buyers seek broader functionality in a single offering. BrainBox AI's continued expansion under Trane Technologies also showed how building-focused AI tools are becoming part of broader equipment and services platforms rather than staying independent point solutions. The competitive pattern, therefore, remains balanced, where large incumbents dominate framework-scale contracts while specialized vendors gain ground in narrower building, forecasting, or analytics applications that can later become acquisition targets.

Middle East AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens Aktiengesellschaft

Honeywell International Inc.

ABB Ltd

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: C3.ai and Shell extended their multi-year AI reliability collaboration to incorporate AI agent-based root cause analysis and remediation across more than 13,000 pieces of equipment on the C3 Agentic AI Platform deployed on Microsoft Azure, advancing the scope of enterprise AI energy management platforms beyond anomaly detection into autonomous operational decision support.

- February 2026: Honeywell and Kortech (a subsidiary of Hassan Allam Holding) signed an MoU to automate and digitize critical infrastructure projects across Egypt, Saudi Arabia, and the UAE, combining Honeywell's global automation software and analytics with Kortech's regional engineering and turnkey delivery capability across data centers, buildings, and smart-city developments.

- February 2026: The UAE Ministry of Energy and Infrastructure, Khazna Data Centers, and Agility announced a pilot to deploy Phaidra AI's reinforcement-learning agents across UAE hyperscale data center campuses for energy efficiency optimization in cooling and workload management, aligned with the UAE Net Zero 2050 Strategy and the Ministry's Energy Efficiency Strategy.

- October 2025: Abu Dhabi's Department of Energy signed a strategic agreement with Google Cloud at GITEX Global 2025 to advance digital transformation in the energy sector, covering AI and machine learning for grid management, demand forecasting, and predictive maintenance of power plants and renewable assets across Abu Dhabi's portfolio.

Middle East AI-powered Energy Management Software Market Report Scope

The Middle East AI-powered Energy Management Software Market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management across the region. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Middle East AI-powered Energy Management Software Market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Saudi Arabia, United Arab Emirates, Qatar and Rest of Middle East)

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Rest of Middle East |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the Middle East AI-powered Energy Management Software Market size in 2026 and where is it heading by 2031?

The market stands at USD 260.13 million in 2026 and is projected to reach USD 670.13 million by 2031, growing at a 20.84% CAGR over 2026-2031.

Which component category leads revenue in this space?

Software led with a 68.22% share in 2025 because buyers continue to prioritize scalable platforms for forecasting, optimization, and performance monitoring.

Why is hybrid deployment growing faster than other delivery models?

Hybrid is projected to expand at a 21.02% CAGR because organizations want cloud-level analytics while keeping sensitive operational data in compliant local environments.

Which application area is expanding the fastest across the region?

Renewable energy forecasting and integration is the fastest-growing application at a 21.13% CAGR, supported by rising renewable capacity across Saudi Arabia and the UAE.

Which end users are creating the strongest new demand through 2031?

Industrial facilities are projected to grow the fastest at a 21.24% CAGR as oil and gas, petrochemicals, desalination, and manufacturing operators push for better efficiency and reliability.

Which country currently leads regional demand and which one is growing the fastest?

Saudi Arabia held the largest share at 34.18% in 2025, while the UAE is projected to post the fastest growth at a 21.31% CAGR through 2031.

Page last updated on: