Micro LED Chip Mass Transfer Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

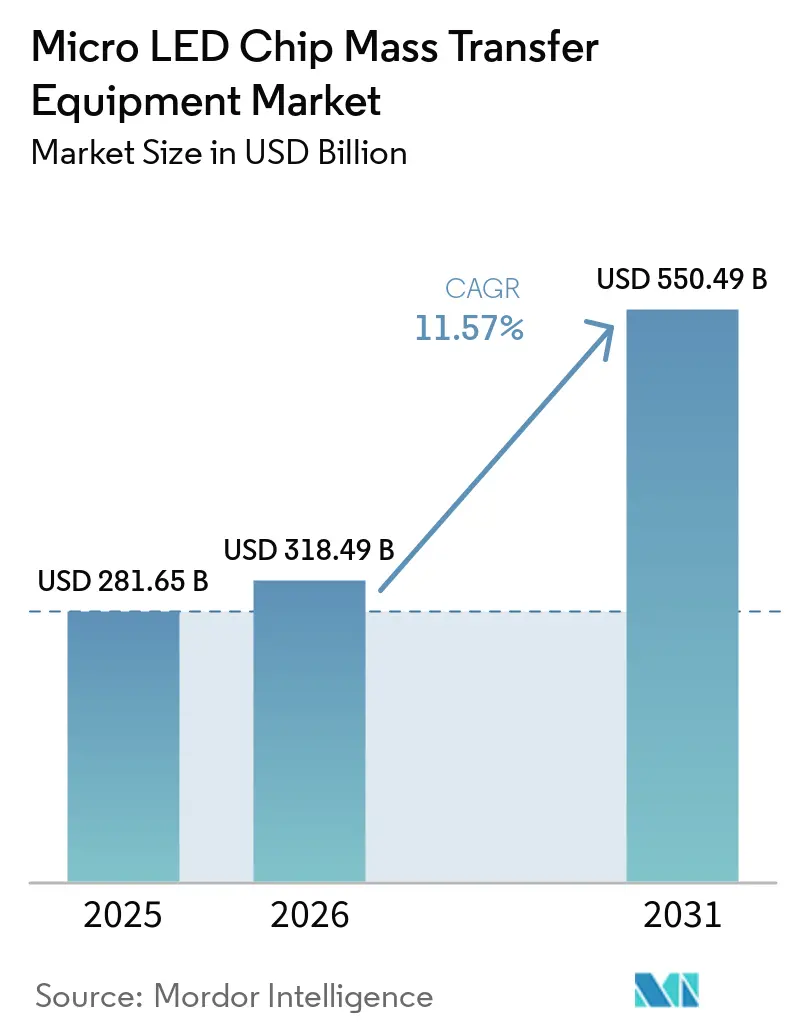

| Market Size (2026) | USD 318.49 Billion |

| Market Size (2031) | USD 550.49 Billion |

| Growth Rate (2026 - 2031) | 11.57% CAGR |

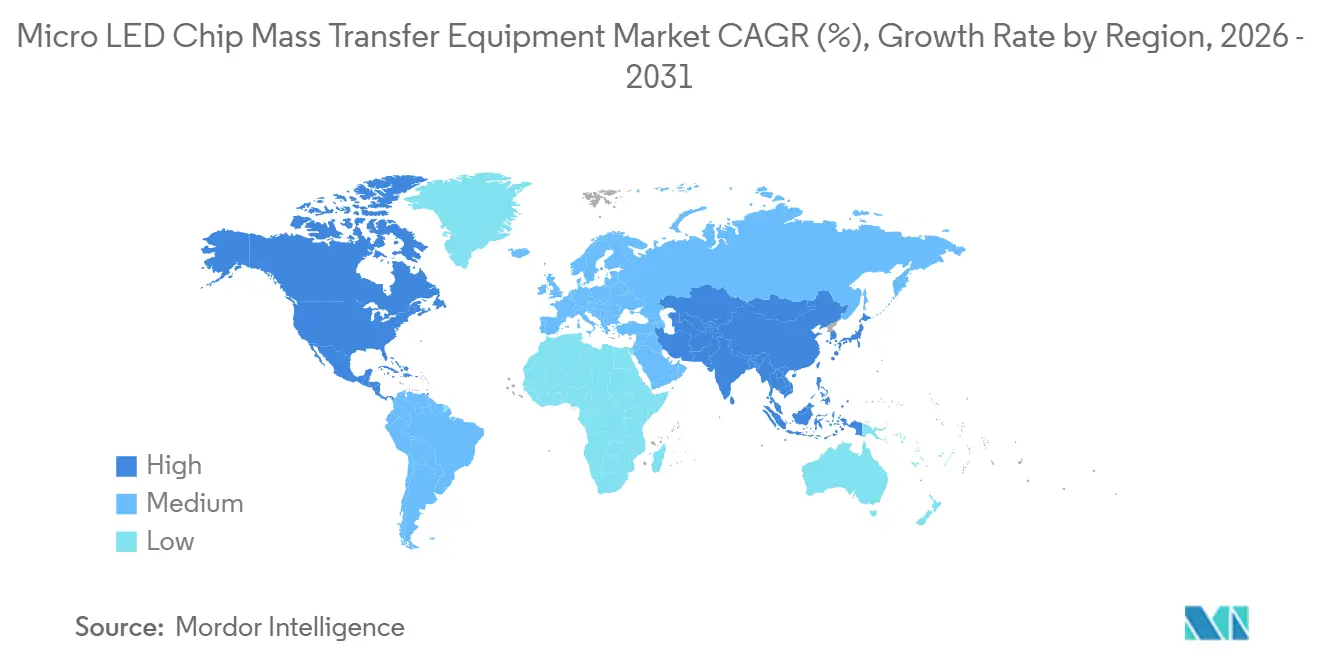

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

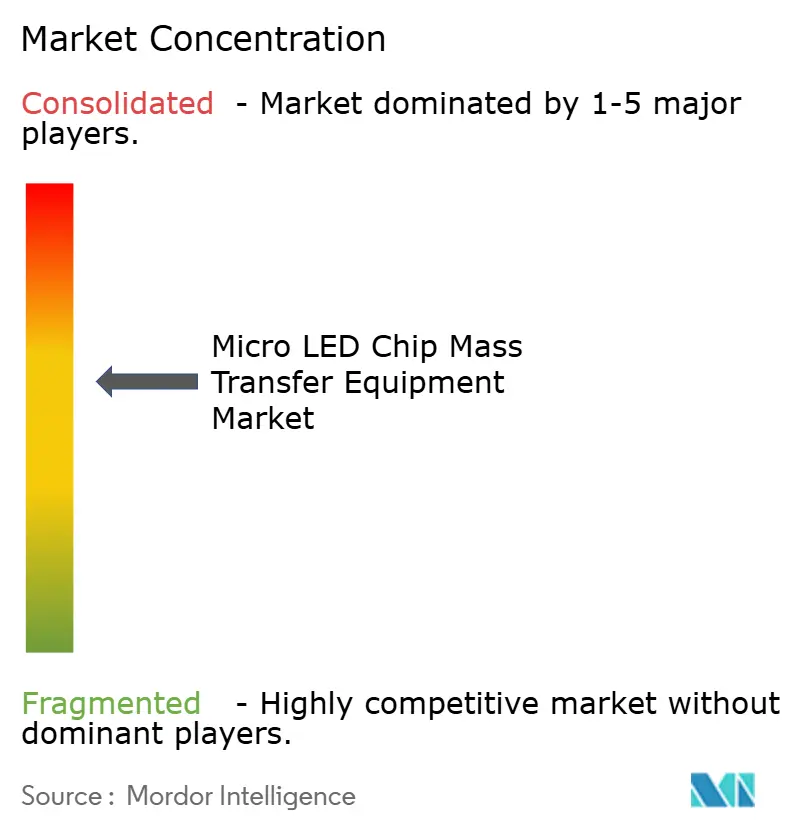

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro LED Chip Mass Transfer Equipment Market Analysis by Mordor Intelligence

The Micro LED chip mass transfer equipment market size is projected to expand from USD 281.65 billion in 2025 and USD 318.49 billion in 2026 to USD 550.49 billion by 2031, registering a CAGR of 11.57% between 2026 to 2031. Demand is accelerating as premium consumer-electronics, automotive, and augmented-reality brands shift display roadmaps toward microLED brightness and power-efficiency targets, compelling panel makers to install high-throughput transfer tools that can align sub-10-micrometer dies at near-six-sigma yields. Capital budgets are further catalyzed by proactive industrial-policy incentives in the United States, South Korea, and China that trim effective equipment prices by up to one-third, shortening payback periods and de-risking pilot lines. Technology inflection points reached in 2025-2026, such as laser-assisted transfer exceeding 50,000 dies per second and AI-supervised vision systems that slash defect rates below 0.5%, have narrowed the cost delta versus OLED deposition and positioned microLED as a commercially viable successor for 4K-plus televisions, curved cockpit clusters, and retinal-resolution AR optics. Against this backdrop, equipment builders that offer modular hybrid heads capable of wafer-to-panel, chip-to-panel, and in-situ repair modes have captured early design wins, setting the stage for multi-vendor competition over the next five years.

Key Report Takeaways

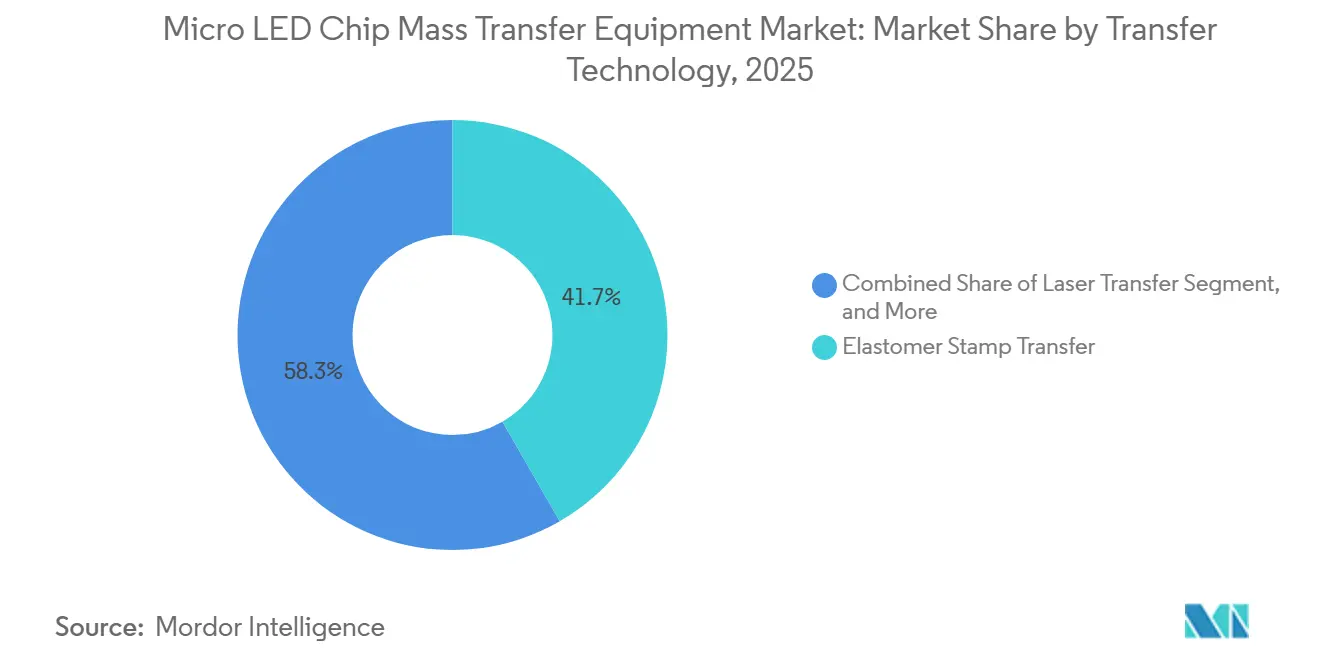

- By transfer technology, elastomer stamp platforms led with 41.68% of the Micro LED chip mass transfer equipment market share in 2025. Hybrid transfer systems are forecast to expand at an 11.95% CAGR through 2031, the fastest among technologies.

- By equipment architecture, wafer-to-panel solutions commanded 46.37% of 2025 revenue, while chip-to-panel architectures are projected to grow at a 12.33% CAGR.

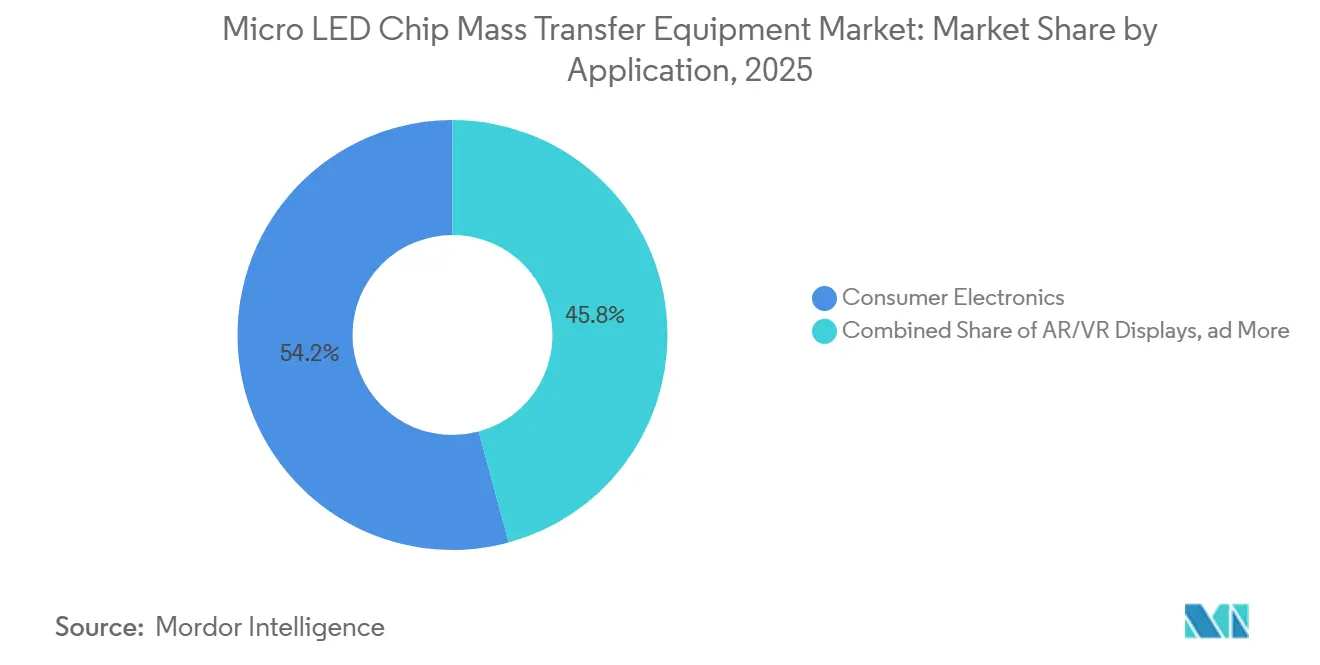

- By application, consumer electronics accounted for 54.21% of 2025 demand; AR/VR displays are advancing at an 11.95% CAGR to 2031.

- By geography, Asia-Pacific captured 62.83% of 2025 revenue, whereas North America is expected to log the highest regional CAGR at 12.16% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro LED Chip Mass Transfer Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for Micro LED displays in premium consumer electronics | +3.2% | Global - Asia-Pacific and North America hot spots | Medium term (2-4 years) |

| Ongoing investments in next-gen display manufacturing lines | +2.8% | Asia-Pacific core, spillover to North America | Short term (≤ 2 years) |

| Advancements in mass-transfer throughput and yield metrics | +2.1% | Global | Medium term (2-4 years) |

| Government incentives for domestic semiconductor-equipment production | +1.6% | North America, Europe, South Korea | Long term (≥ 4 years) |

| Adoption of chiplet-ready transfer platforms for modular AR/VR optics | +1.3% | North America, Asia-Pacific | Medium term (2-4 years) |

| Integration of AI-based vision systems for in-process defect detection | +0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Micro LED Displays in Premium Consumer Electronics

MicroLED is now the de facto successor to OLED in flagship smartphones, watches, and large-screen televisions. Samsung expanded its Micro RGB television line in 2026 to 55-115-inch sizes, normalizing millions of microLED dies per panel and boosting annual tool utilization at key outsourced assembly partners.[1]Samsung Electronics, “Micro LED TV Lineup Expansion,” news.samsung.com PlayNitride, working with AUO, scaled six-inch GaN-on-silicon wafer output for smartwatch and automotive orders, driving a 20% boost in capacity plans for 2026. Display makers are accelerating the shift from blue-chip plus quantum-dot color conversion to true RGB transfer, which demands three sequential placement cycles but increases luminous efficiency by up to 40%. LG Display demonstrated a 22.3-inch active-matrix microLED tile in 2024 that stitches into 136-inch 4K walls, a modular strategy that relies on sub-50 micrometer stamp transfer at commercial throughputs. Research firm Omdia expects microLED display revenue to double between 2025 and 2026, confirming the near-term uptick in equipment orders omdia.tech.informa.com.

Ongoing Investments in Next-Gen Display Manufacturing Lines

Asia-Pacific panel makers are repurposing legacy LTPS and a-Si fabs for microLED pilot lines, funneling more than USD 1 billion between 2024 and 2025 into wafer-to-panel and hybrid tools. BOE’s sixth-generation line in Chongqing entered production in early 2025, with 50,000 sheets per month supporting both LTPO backplanes and a separate microLED pilot zone.[2] BOE Technology Group, “Sixth-Generation Display Line Announcement,” boe.com Tianma completed a RMB 1.1 billion (USD 155 million) plant in December 2024 featuring a G3.5 full-laser transfer system rated at 40 million chips per hour. AUO’s 4.5-generation campus reached mass production in 2025, supplying Sony Mobility with cockpit modules for the 2026 AFEELA launch. HC SemiTek’s Zhuhai epi-wafer line, live since November 2024, reduces China’s import dependency and enhances wafer availability for downstream transfer qualification. While the bulk of spending centers on China, Taiwan, and South Korea, U.S. firms leverage CHIPS Act credits to co-locate pilot lines with advanced-packaging hubs.

Advancements in Mass-Transfer Throughput and Yield Metrics

Performance leaps recorded in 2025-2026 have erased many cost objections. Coherent’s UVtransfer excimer platform ships dies at 50,000-plus per second with 99.7% placement within 0.6 micrometers on both axes.[3]Coherent Corp., “UVtransfer Technical Specifications,” coherent.com ASMPT’s Vortex II die bonder achieves 99.999% yield on 50 × 100 micrometer dies, while its LT300Pro laser head integrates on-the-fly repair that swaps defective chips without substrate loss. Toray Engineering unveiled a single-pass system that processes 515 × 500 millimeter panels at ten-times prior throughput, maintaining ±2 micrometers accuracy even on warped glass. Konka’s captive laser line surpassed 36 million chips per hour at 99.999% yield, proving local Chinese innovations can rival global incumbents. Real-time AI vision trims scrap from 3-5% to below 0.5%, cutting payback periods to four-five years for high-utilization sites.

Government Incentives for Domestic Semiconductor-Equipment Production

Policy levers increasingly target display-equipment sovereignty. The U.S. CHIPS and Science Act provides a 25% tax credit plus USD 39 billion in grants; eight approved projects include advanced-packaging lines that can dual-use microLED mass-transfer tools. South Korea earmarked KRW 484 billion (USD 350 million) through 2032 to develop an indigenous inorganic LED supply chain, spanning epi-wafers, bonding, and inspection. The EU Chips Act mobilizes EUR 43 billion (USD 47 billion) in blended funds and accelerated depreciation for qualifying equipment, benefiting regional toolmakers such as Aixtron and potential future transfer-platform entrants. Veeco’s multi-tool order from Rocket Lab in 2025 illustrates how compound-semiconductor subsidies propagate backward linkages into the microLED tool ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure and process complexity vs. OLED alternatives | -2.4% | Global | Medium term (2-4 years) |

| Limited supply chain for high-uniformity microLED epitaxial wafers | -1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Thermal stress-induced warpage during wafer-to-panel transfer cycles | -0.7% | Asia-Pacific, North America | Medium term (2-4 years) |

| IP litigation risks around elastomer-stamp patents in China | -0.5% | China, spillover to Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Process Complexity vs. OLED Alternatives

A greenfield microLED line requires USD 200-300 million, roughly double the incremental cost of extending OLED evaporation and encapsulation capacity. LG Display’s W 1 trillion (USD 750 million) budget for 2025-2027 earmarks a majority for OLED, keeping microLED in pilot modules that piggyback on AMOLED backplanes lgdisplay.com. AUO’s 4.5-generation plant cost NTD 2 billion (USD 66.7 million) yet supports only 10,000 six-inch wafers per month, illustrating the constrained economies of scale auo.com. MicroLED production involves up to twelve process steps, each compounding yield loss to roughly 60-70% at early maturity, compared with OLED’s 85-90% onlinelibrary.wiley.com. Samsung mitigates the burden by segmenting its product line: ultra-luxury 110-140 inch self-emissive walls absorb higher costs, whereas cost-optimized Micro RGB televisions trade off per-pixel control for attainable price points news.samsung.com. Equipment builders respond with modular tools that allow staged investments, but this elongates payback to six-eight years for conservative panel makers.

Limited Supply Chain for High-Uniformity MicroLED Epitaxial Wafers

Mass-transfer economics break down without tight wavelength and defect controls. Commercial lines need ±2.5 nanometer uniformity across eight-inch wafers, yet most suppliers still ship ±5-10 nanometer spreads, forcing costly binning and 30-40% over-ordering. PlayNitride trimmed variation by 50% between 2021 and 2023 but still targets another 6% EQE gain to cross commercialization thresholds ieeexplore.ieee.org. Red AlGaInP chips lag with roughly one-third the efficiency of blue and green GaN dies, compelling over-drive and raising power budgets by 25-30%. Saphlux’s 4-inch GaN-on-silicon line, funded with USD 50 million in 2024, outputs fewer than 5,000 wafers per month, insufficient for a single high-volume display fab.[4]Saphlux Inc., “Series C Funding Release,” saphlux.com Without predictable epi supply, transfer-tool vendors struggle to demonstrate full-speed, full-yield metrics, stalling orders and capping near-term market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transfer Technology: Hybrid Platforms Bridge Speed and Precision

Elastomer-stamp tools dominated 2025 with 41.68% of the Micro LED chip mass transfer equipment market size, leveraging decades of printed-electronics know-how to place 10-20 micrometer dies across large signage substrates at 10,000-20,000 dies per second. Their simplicity, low consumable cost, and compatibility with curved automotive clusters sustain demand. Yet applications that push below 5 micrometers, such as retinal-resolution AR optics, expose stamp-induced edge damage and adhesion drift. Laser-assisted forward transfer therefore captured almost one-third of revenue, propelled by Coherent’s UVtransfer and similar excimer solutions that hit sub-micrometer tolerances at tenfold higher speeds. Fluidic and electrostatic approaches remain niche, but they seed patents that incumbents cannot ignore.

Hybrid designs marry the raw speed of laser release with the gentle landing control of electrostatic or vacuum pick-and-place, enabling a single frame to process die ranges from 3 to 100 micrometers. The combination lowers cycle time by roughly 40% compared with sequential tools and underpins the 12.33% CAGR expected for hybrid platforms. VueReal’s cartridge system, capable of swapping pre-filled die cassettes between builds, epitomizes high-mix agility. Meanwhile, ASMPT integrates auto-repair heads that rework sub-0.01% mismatches in-situ, an essential feature once panel die counts exceed 20 million. The performance blend positions hybrid systems as default selections for new fabs that must hedge against die-size evolution over the planning horizon.

By Equipment Architecture: Chip-to-Panel Closes the Automotive Gap

Wafer-to-panel transfer retained a 46.37% share of the Micro LED chip mass transfer equipment market in 2025, thanks to its ability to stamp tens of thousands of dies in a single shot, making it well-suited for price-sensitive signage tiles and large televisions. Tianma’s 108-inch 4K panels, stitched from G3.5 glass, rely on batch transfers that achieve 40 million chips per hour and seam gaps of less than 20 micrometers. LG Display’s 22.3-inch module likewise uses wafer arrays to populate 0.783-millimeter pitches with sub-50-micrometer dies.

Chip-to-panel architectures are projected to grow at 12.33% through 2031 as automakers and wearable brands demand free-form geometries. AUO’s curved AFEELA dashboard and BOE’s panoramic HUD demonstrate why individually placed dies enable variable pixel densities across a single glass sheet. Although cycle times lag wafer-batch methods by one-to-two orders of magnitude, AI-driven pick heads and real-time optical alignment now narrow the gap to commercially acceptable windows for high-value modules. Wafer-to-wafer continues to serve CMOS-based microdisplays, while dedicated repair stations become table stakes rather than standalone systems, embedding themselves into broader architectures to guarantee 99.99% final yields.

By Application: AR/VR Surges Beyond Niche Status

Consumer electronics retained 54.21% of equipment spend in 2025 as television and smartwatch champions embraced 1,000-nit outdoor performance with microLED backplanes. Yet price ceilings on ultra-luxury units and the need for triple-cycle RGB transfers moderate growth. The AR/VR cohort is rising from a low base but leads with an 11.95% CAGR, spurred by Meta’s 2027 glasses roadmap and Apple’s tie-up with Haylo for 300-millimeter GaN wafers. JBD’s Griffin engine produces 500-lumen images in a 0.25-inch diagonal, proving real-world brightness unattainable with OLED microdisplays. Automotive cluster orders, though lower in volume, yield premium average-selling-prices that keep utilization high for chip-to-panel tools, while commercial signage maintains steady but unspectacular replacement-cycle demand, especially for bezel-free retail walls.

Commercial signage and large‐venue video walls, which absorbed nearly 15% of 2025 equipment demand, lean on wafer-to-panel lines that stamp tens of thousands of sub-100 µm dies per cycle, keeping cost per pixel below USD 0.003 for 4K-resolution tiles. Retailers and transportation hubs now specify bezel-free walls with <20 µm seam tolerances, prompting panel makers to pair high-speed laser release with inline repair heads so that each 108-inch module ships at ≥99.995% yield, a standard validated when Tianma’s G3.5 line hit 40 million dies per hour in late 2024. Looking forward, stadium broadcasters and e-sports arenas are budgeting for 8K microLED scoreboards that could push individual panel die counts past 25 million, a scale that will further expand the Micro LED chip mass transfer equipment market size for hybrid platforms able to toggle between 50 µm TV pixels and 10 µm high-density sub-modules without head swaps.

Geography Analysis

Asia-Pacific dominated with 62.83% of Micro LED chip mass transfer equipment market revenue in 2025, anchored by Chinese and Taiwanese conglomerates that co-locate epi-growth, transfer, and backplane assembly within cluster campuses. Tianma, BOE, and Visionox collectively deployed more than USD 1.5 billion on pilot and Gen 4.5 lines between 2024 and 2025, compressing development loops and giving regional vendors first-mover runway. South Korea’s KRW 484 billion (USD 350 million) incentive blueprint adds strategic depth by plugging domestic wafer and bonding gaps, a move likely to lift local tool purchases once qualification milestones are met.

North America, forecast to expand at a 12.16% CAGR, is translating CHIPS Act tax credits and grants into green-field investments that span epi-growth through heterogeneous integration. Early awards cover Amkor, GlobalFoundries, Intel, and SK Hynix advanced-packaging hubs that can repurpose laser-transfer platforms for chiplets and microLEDs alike. Meta’s Haylo fab in New York State anchors the supply chain for sub-5 micrometer blue and green dies, while Veeco’s Lumina+ MOCVD shipments to Rocket Lab illustrate upstream-downstream pull effects that ripple into mass-transfer demand.

Europe, at roughly 8% share, lacks high-volume display makers yet benefits from EU Chips Act depreciation perks that spur R&D labs and pilot modules aimed at automotive interiors and aerospace HUDs. Rest-of-World regions, mainly Southeast Asia and the Middle East, remain niche assembly hubs that hedge geopolitical risk for Chinese and Taiwanese brands but have not yet placed substantial tool orders.

Competitive Landscape

Market rivalry sits at a moderate level: the five largest vendors, ASMPT, Kulicke and Soffa, Toray Engineering, Coherent, and VueReal, collectively delivered just under 40% of 2025 revenue. Incumbent wire-bonders and pick-and-place specialists leverage legacy service organizations to lock in repeat consumables sales, while photonics entrants use laser IP to differentiate on throughput. Kulicke and Soffa absorbed Rohinni to accelerate elastomer-stamp know-how, whereas Coherent’s USD 7 billion II-VI acquisition paved the way for an integrated excimer platform launch that posts 99.7% accuracy at unprecedented speeds.

Start-ups attack with orthogonal methods: eLux steers dies in fluid under electric fields, side-stepping heavy stamp patents, though control degrades under 10 micrometers. VueReal raised USD 40.5 million to commercialize swappable die cartridges that unlock high-mix luxury-automotive and AR programs. X-Celeprint licenses micro-transfer-printing patents for flexible and heterogeneous substrates, challenging incumbents to broaden process windows beyond rigid glass.

Vertical integration is an emerging threat. Tianma and Konka now design proprietary laser heads capable of 36-40 million die-per-hour figures, reducing their reliance on merchant suppliers, especially inside Chinese state-funded campuses. Tool makers must therefore double down on repair modules, AI vision, and fast-swap heads to stay irreplaceable in an environment where panel makers internalize core IP to secure supply resilience.

Micro LED Chip Mass Transfer Equipment Industry Leaders

ASMPT Ltd.

Kulicke & Soffa Industries Inc.

Toray Engineering Co. Ltd.

PlayNitride Inc.

Rohinni LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: JBD launched the Griffin microdisplay delivering hundreds of thousands of pixels in a 0.25-inch form factor at 500 lumens, aimed at automotive projection and AR glasses.

- February 2026: SDI Group acquired PRP Optoelectronics to extend its custom high-performance microLED portfolio.

- January 2026: PlayNitride partnered with Brillink to integrate photonic interconnects with microLED chiplets for modular AR optics.

- January 2026: ALLOS Semiconductors and Ennostar agreed to co-develop 200 millimeter GaN-on-silicon epi-wafers to trim cost per die.

Global Micro LED Chip Mass Transfer Equipment Market Report Scope

The Micro LED Chip Mass Transfer Equipment Market Report is Segmented by Transfer Technology (Elastomer Stamp Transfer, Laser Transfer, Electrostatic Transfer, Fluidic Transfer, Hybrid Transfer), Equipment Architecture (Wafer-to-Wafer, Wafer-to-Panel, Chip-to-Panel, Repair Transfer Systems), Application (Consumer Electronics, AR/VR Displays, Automotive Displays, Commercial Displays), and Geography (Asia-Pacific, North America, Europe, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Elastomer Stamp Transfer |

| Laser Transfer |

| Electrostatic Transfer |

| Fluidic Transfer |

| Hybrid Transfer |

| Wafer-to-Wafer |

| Wafer-to-Panel |

| Chip-to-Panel |

| Repair Transfer Systems |

| Consumer Electronics |

| AR/VR Displays |

| Automotive Displays |

| Commercial Displays |

| Asia-Pacific |

| North America |

| Europe |

| Rest of World |

| By Transfer Technology | Elastomer Stamp Transfer |

| Laser Transfer | |

| Electrostatic Transfer | |

| Fluidic Transfer | |

| Hybrid Transfer | |

| By Equipment Architecture | Wafer-to-Wafer |

| Wafer-to-Panel | |

| Chip-to-Panel | |

| Repair Transfer Systems | |

| By Application | Consumer Electronics |

| AR/VR Displays | |

| Automotive Displays | |

| Commercial Displays | |

| By Geography | Asia-Pacific |

| North America | |

| Europe | |

| Rest of World |

Key Questions Answered in the Report

What is driving capital investment in microLED mass-transfer lines?

Premium consumer devices and automotive cockpits need higher brightness and power savings, prompting panel makers to fund new lines despite higher upfront cost.

How fast is the North American market for transfer equipment expanding?

Incentives under the CHIPS Act support a 12.16% CAGR through 2031 as domestic fabs co-locate microLED and advanced-packaging tools.

Which transfer technologies are gaining share beyond elastomer stamps?

Hybrid laser-electrostatic platforms are the fastest-growing, projected at an 12.27% CAGR, because they balance sub-micrometer accuracy with high throughput.

Why are epitaxial wafers a bottleneck for microLED commercialization?

Few suppliers can meet ±2.5 nanometer wavelength uniformity across eight-inch substrates, forcing costly over-ordering and limiting transfer-tool utilization.

How do AI vision systems improve mass-transfer economics?

Real-time defect detection and adaptive alignment cut scrap rates below 0.5% and reduce operator training costs, trimming tool payback to four-five years.

Which regions currently dominate demand for microLED transfer equipment?

Asia-Pacific leads with 62.83% of 2025 revenue thanks to concentrated display manufacturing clusters, while North America is the fastest-growing on a percentage basis.

Page last updated on: