MHealth Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 46.16 Billion |

| Market Size (2031) | USD 92.69 Billion |

| Growth Rate (2026 - 2031) | 14.96% CAGR |

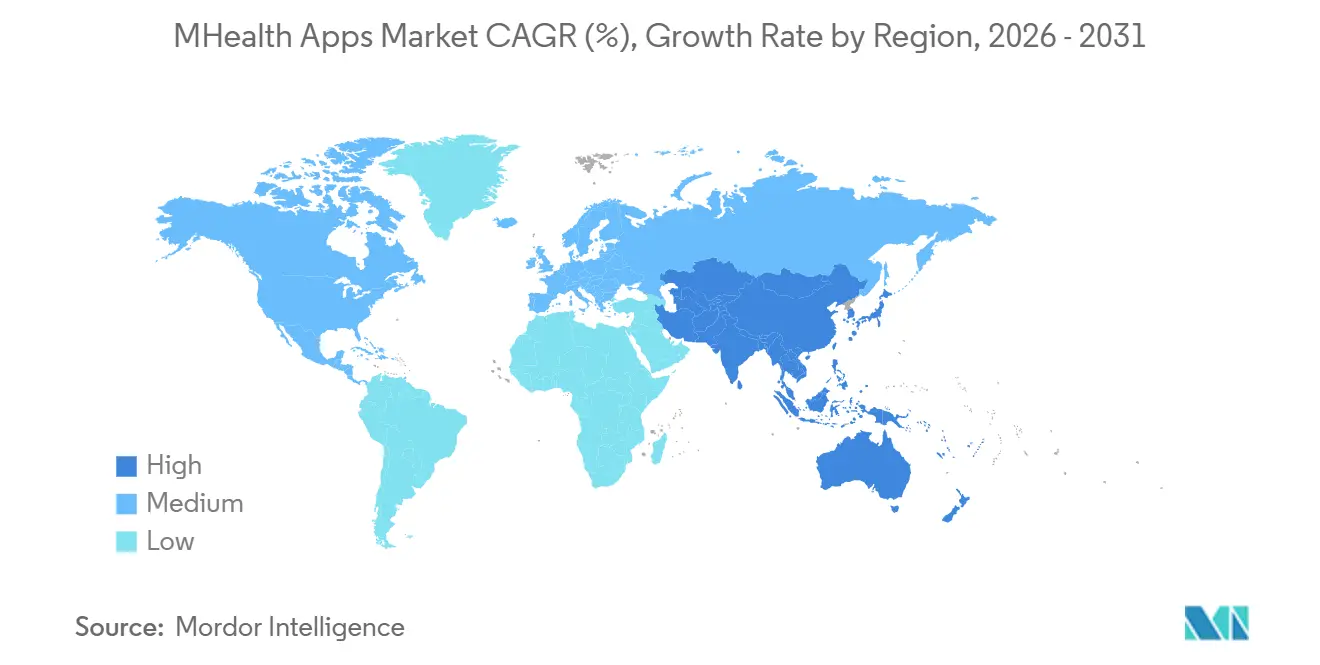

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MHealth Apps Market Analysis by Mordor Intelligence

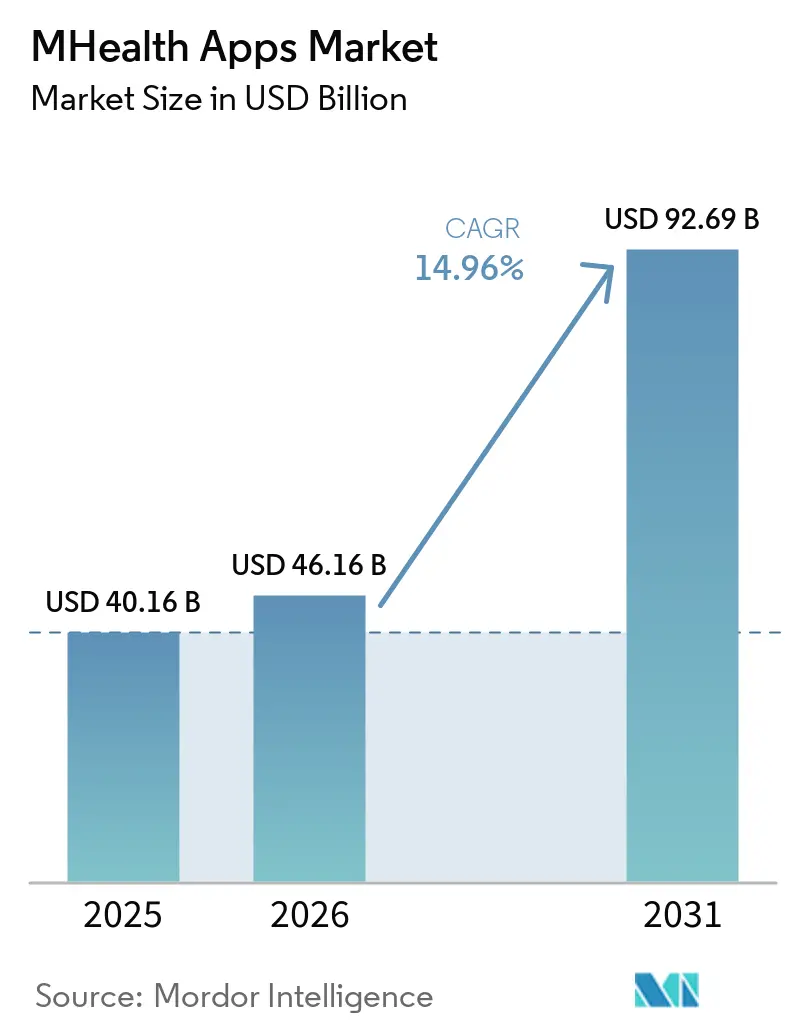

The MHealth Apps Market size is expected to increase from USD 40.16 billion in 2025 to USD 46.16 billion in 2026 and reach USD 92.69 billion by 2031, growing at a CAGR of 14.96% over 2026-2031.

The mHealth apps market is experiencing growth driven by the need for chronic disease management, widespread smartphone usage, increased wearable adoption, and advancements in regulated mobile health tools within formal care. Wearable device shipments are projected to reach 611.5 million units in 2025, expanding the data available for mHealth apps and raising user expectations for continuous health tracking. Reimbursement support is reshaping the commercial model, particularly with the implementation of HCPCS codes G0552 to G0554 by CMS in January 2025 for qualifying digital mental health treatment devices. This shift is steering the market from basic wellness apps to advanced tools integrated into monitoring, therapy, and provider-led care pathways.

Key Report Takeaways

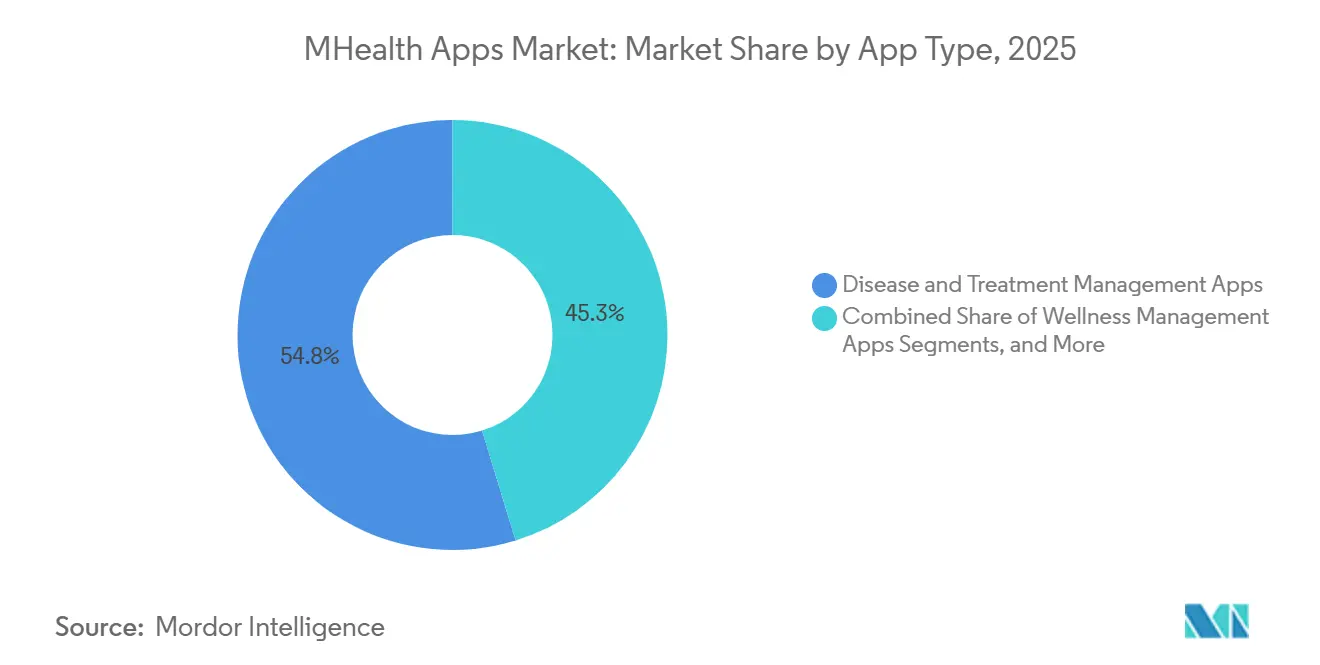

- By app type, disease and treatment management Apps held 54.75% of revenue in 2025 in the mHealth apps market, while Wellness Management Apps are projected to grow at a 16.70% CAGR from 2026 to 2031.

- By platform, iOS accounted for 48.75% of revenue in 2025 in the mHealth apps market, while Android is expected to expand at a 17.45% CAGR through 2031.

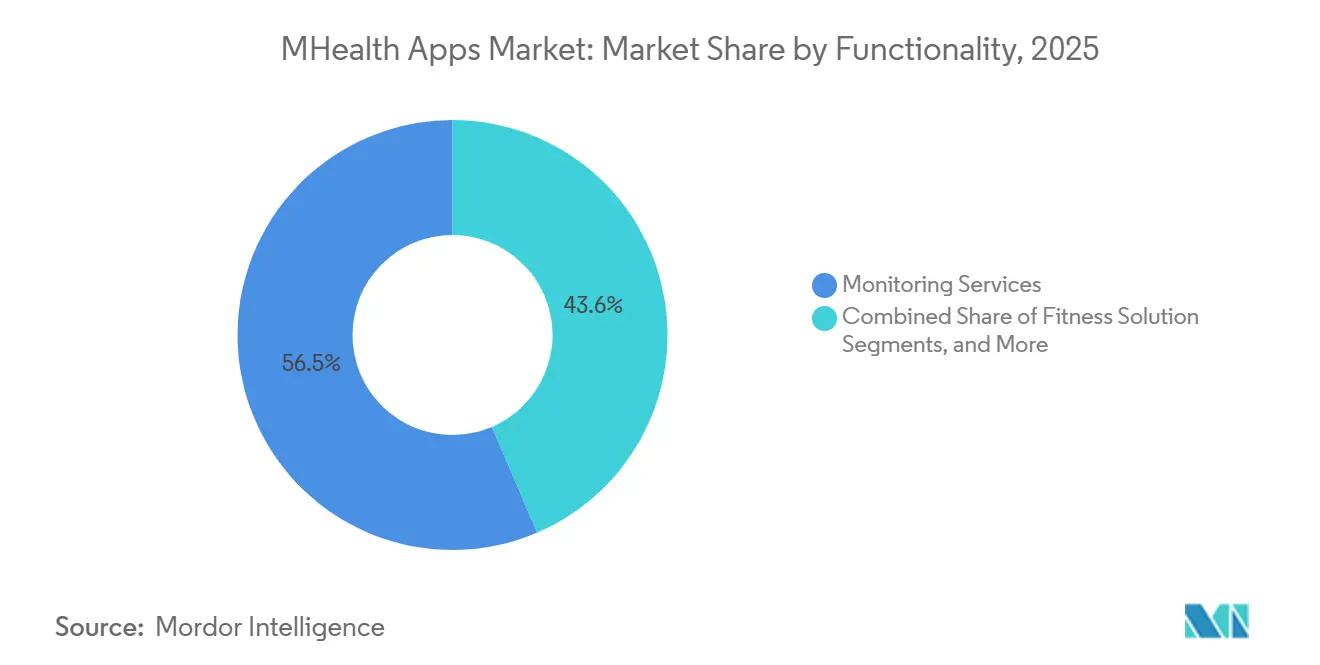

- By functionality, monitoring Services held 56.45% of revenue in 2025 in the mHealth apps market, while fitness solutions are forecast to grow at a 15.25% CAGR from 2026 to 2031.

- By end user, patients and consumers represented 52.66% of revenue in 2025 in the mHealth apps market, while healthcare providers are projected to grow at a 15.96% CAGR through 2031.

- By geography, North America held 41.61% of revenue in 2025 in the mHealth apps market, while Asia-Pacific is projected to expand at a 15.66% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global MHealth Apps Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| smartphone and wearable penetration | +3.5% | Global, with concentrated gains in South and Southeast Asia and Sub-Saharan Africa | Short term (≤ 2 years) |

| rising chronic disease self-management demand | +2.8% | Global, with North America and Europe for medically managed apps and Asia-Pacific for user volume | Medium term (2-4 years) |

| telehealth and remote monitoring normalization | +2.1% | North America and Europe, with rapid adoption in Asia-Pacific | Short term (≤ 2 years) |

| AI-enabled personalization and analytics | +2.4% | Global, with strongest monetization in North America and Europe | Medium term (2-4 years) |

| reimbursable digital therapeutics pathways | +1.6% | North America, with early signals in Europe and Asia-Pacific | Medium term (2-4 years) |

| EHR-embedded digital prescribing workflows | +1.4% | North America, Europe, and emerging adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone and Wearable Penetration Extends the mHealth Apps Market's Addressable Base

In 2025, global wearable device shipments reached 611.5 million units, a 9.1% increase from the previous year, significantly expanding the user base for mHealth apps. Policy support and diverse price tiers in China drove connected devices into mainstream adoption, especially in high-volume consumer markets. Apple’s approval for its Hypertension Notification Feature in September 2025 highlighted the role of consumer hardware as a regulated screening tool.[1]Misun Hwang, Yaguang Zheng, Youmin Cho, and Yun Jiang, “AI Applications for Chronic Condition Self-Management Scoping Review,” Journal of Medical Internet Research, jmir.org With wearables capturing more clinically relevant signals, app developers are enhancing monitoring and coaching products, reducing user input effort and increasing engagement. By 2026, 40% of new wearables are expected to feature AI-enabled functions, driving personalization and performance expectations.

AI-Enabled Personalization Shifts the Engagement Model From Reminders to Anticipatory Care

A 2025 review of 66 studies showed machine learning algorithms delivered personalized recommendations in 61% of cases and improved medication adherence in trials. The mHealth apps market is under pressure to deliver measurable value beyond reminder-based interactions.[2]Apple Inc., “Hypertension Notification Feature on Apple Watch Validation Paper,” Apple, apple.com AI is also improving provider workflows by enhancing triage and risk prioritization, reducing alert fatigue. Tempus AI launched 'olivia' in January 2025, integrating with over 1,000 health systems and generating AI-driven clinical summaries. This shift towards coordinated care combines records, device data, and predictive analytics, moving personalization from reminders to proactive interventions and workflow optimization.

Reimbursable Digital Therapeutics Pathways Create a Structural Revenue Floor

CMS introduced HCPCS codes G0552, G0553, and G0554 in the 2025 Medicare Physician Fee Schedule, creating reimbursement pathways for digital mental health devices. This provides a stable financial base for regulated software products previously reliant on consumer spending.[3]Centers for Medicare and Medicaid Services, “CMS Manual System, Summary of Policies in the Calendar Year 2025 Medicare Physician Fee Schedule Final Rule,” CMS, cms.gov In April 2025, Click Therapeutics received De Novo authorization for CT-132, the first prescription digital therapeutic for episodic migraine prevention, reducing monthly migraine days by 3.04 in trials. While Medicare coding remains limited to mental health devices, other categories like cardiometabolic and respiratory products still depend on commercial payer negotiations. Reimbursement progress is strengthening provider billing models and stabilizing enterprise revenue streams.

EHR-Embedded Digital Prescribing Workflows Convert App Downloads Into Care Pathways

EHR-linked prescribing and monitoring workflows are becoming critical as health systems seek tools that integrate with clinical software. These integrations enhance user retention by initiating engagement through clinician relationships rather than app searches. They also drive higher contract values, as hospitals and physician groups purchase these tools as part of broader care management programs. Tempus AI’s 2025 launch of 'olivia,' integrated with over 1,000 health systems, exemplifies this trend. Clinical connectivity is now a key differentiator in the mHealth apps market, favoring vendors with embedded workflow placements over standalone apps reliant on consumer discovery.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy and cybersecurity scrutiny | -2.2% | Global, with acute exposure in Europe, North America, and Asia-Pacific | Short term (≤ 2 years) |

| Low long-term engagement and app abandonment | -1.9% | Global, with highest attrition in consumer wellness segments | Medium term (2-4 years) |

| Rising clinical evidence burden for samd and ai claims | -1.5% | North America and Europe, with emerging adoption in regulated Asia-Pacific markets | Long term (≥ 4 years) |

| App-store data-sharing enforcement and cross-border data rules | -1.0% | Global, with immediate compliance pressure in U.S. states and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Scrutiny Elevate the Cost of Trust

A 2025 audit of 272 Android mHealth apps revealed an average security score of 47 out of 100, with 42.6% using outdated SHA-1 encryption and 42 apps transmitting unencrypted data. Privacy complaints and technical issues were linked to over 553,000 user reviews, highlighting how trust issues can lead to user abandonment. The mHealth apps market faces rising costs for encryption, consent management, and vendor oversight as platforms collect more complex data. Expanding into multiple regions further complicates compliance due to varying data regulations, increasing operating costs and slowing market scalability.

Low Long-Term Engagement Undermines Clinical Outcome Evidence and Commercial Viability

A study on SMARTDiabetes in China showed monthly active users dropped from 56.3% at launch to 42.2% by the 16th month, with only 32.9% remaining active for a year. Users in the highest engagement quartile achieved a 44.9% success rate on glycemic and cardiovascular targets, compared to 31.0% in the lowest quartile.[4]Xiong Zheng, “Patterns of Long-Term Engagement With an mHealth Intervention for Type 2 Diabetes Management,” JMIR mHealth and uHealth, mhealth.jmir.org Sustained usage is critical for proving clinical value and securing contract renewals in the mHealth apps market. A national rollout of Asthmahub in Wales found 47.7% of registered users never engaged with the app, emphasizing how user attrition limits the potential of digital care tools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By App Type: Clinical Monetization Anchors Revenue While Wellness Drives Volume Growth

In 2025, Disease and Treatment Management Apps accounted for 54.75% of the mHealth apps market, driven by chronic condition use cases like CGM-linked diabetes management, medication adherence, and remote monitoring tools. Clinically validated products dominate revenue channels such as reimbursement and employer benefits, keeping medically oriented applications ahead of lifestyle offerings as the market expands.

Wellness Management Apps are projected to grow at a 16.70% CAGR from 2026 to 2031, fueled by fitness tracking, nutrition support, mental wellness, sleep monitoring, and weight management. This category broadens the market by engaging users earlier in the prevention journey. DexCom launched its G7 15 Day CGM system in 2025 with companion app features, balancing clinical monetization with prevention-led adoption.

By Platform: iOS Leads in Revenue Density but Android Defines Market Scale

In 2025, iOS captured 48.75% of revenue in the mHealth apps market, driven by higher revenue per user, integration with Apple Watch, and strong positioning in North America and Western Europe. The platform excels in premium chronic care and employer-sponsored programs, where users value its seamless ecosystem.

Android is forecast to grow at a 17.45% CAGR from 2026 to 2031, supported by widespread smartphone adoption in South and Southeast Asia. Affordable devices expand the addressable market, particularly in regions with rising demand for scalable mobile health tools, making Android pivotal for market scale.

By Functionality: Continuous Monitoring Dominates but Active Intervention Scales Fastest

Monitoring Services accounted for 56.45% of revenue in 2025, driven by passive data collection from CGM systems, heart rate wearables, and sleep trackers. These tools align with reimbursement models and remote care, offering continuous oversight and higher perceived value among users.

Fitness Solutions are expected to grow at a 15.25% CAGR from 2026 to 2031, supported by employer wellness programs and activity tracking in cardiometabolic care. Active coaching tools linked to measurable behavior support are driving engagement and bridging gaps between clinical visits.

By End User: Patient Volume Leads but Provider Adoption Is the High-Stakes Growth Frontier

In 2025, Patients and Consumers held 52.66% of revenue in the mHealth apps market, driven by wellness, fitness, and self-management applications. Chronic care categories dominate revenue, with Teladoc Health reporting over 1 million active enrollees in its chronic care programs in 2025, achieving significant health outcomes.

Healthcare Providers are projected to grow at a 15.96% CAGR from 2026 to 2031, driven by demand for diagnostic aids, clinical decision support, remote monitoring dashboards, and point-of-care tools. This shift reflects longer contracts tied to care delivery and population management, narrowing the growth gap with consumer-facing applications.

Geography Analysis

In 2025, North America accounted for 41.61% of the mHealth apps market, maintaining its position as the largest regional contributor. The region benefits from widespread internet access, a high prevalence of chronic diseases, and a reimbursement structure supporting digital therapeutics under the 2025 Medicare Physician Fee Schedule. In the United States, 14.9% of commercially insured patients had telehealth claims in January 2025, with mental health conditions comprising 58.5% of telehealth diagnostic encounters. High payer density and mature EHR adoption further enhance the region's suitability for reimbursable and integrated application models.

Europe remained the second-largest region in the mHealth apps market, driven by stringent data governance and device regulations that favor well-capitalized operators. Frameworks like GDPR and the Medical Device Regulation raise compliance standards, creating barriers for smaller vendors. Public payer pathways, such as the NHS App in the UK and Germany's DiGA framework, support sustainable growth by aligning reimbursement with compliance requirements.

Asia-Pacific is projected to grow at a 15.66% CAGR from 2026 to 2031, making it the fastest-growing region in the mHealth apps market. China leads the region, supported by strong adoption of wearable devices, with its wrist-worn device market expected to reach 79.58 million units by 2026. Huawei shipped 25.5 million smartwatches in 2025, reflecting a 21.7% year-over-year increase. India is the fastest-growing country market, driven by digital health policies and payment infrastructure enabling low-cost subscription models. The Middle East and Africa, though smaller in revenue, are on a growth trajectory due to digital health investments in GCC countries and emerging care delivery models.

Competitive Landscape

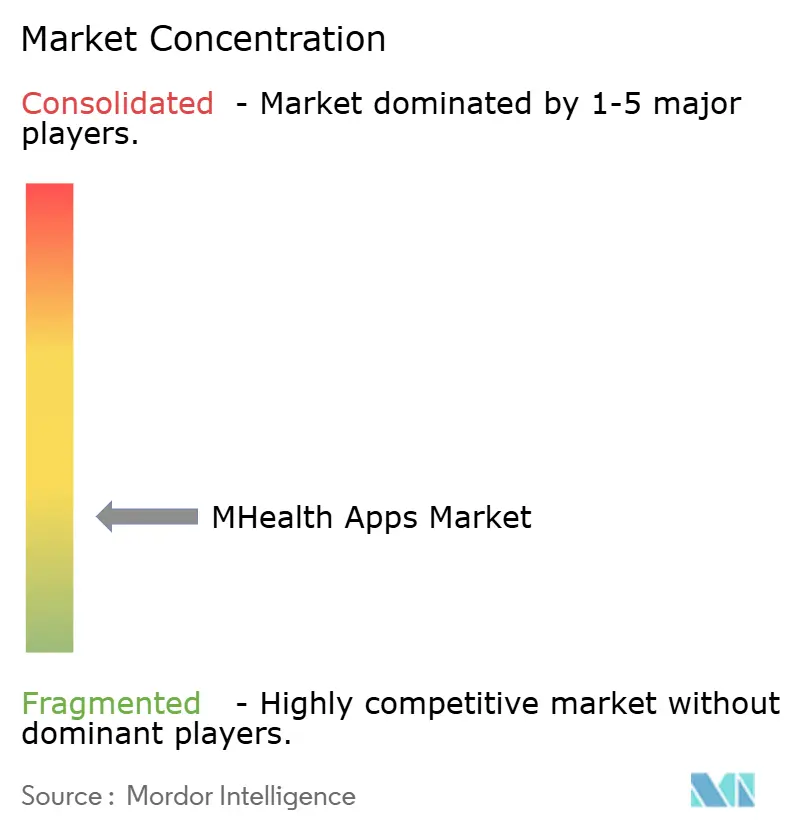

No single company dominates the fragmented mHealth apps market, which spans devices, virtual care, chronic disease management, and wellness. Competition includes consumer electronics leaders like Apple, Samsung, Google, Fitbit, Garmin, and Withings; virtual care providers such as Teladoc Health and Omada Health; and condition-specific specialists like DexCom, Abbott, Medisafe, Noom, Calm, and Headspace. Companies adopt varied strategies, focusing on hardware ecosystems, clinical outcomes, subscriptions, or employer contracts. Fragmentation is more pronounced in broader categories, making cross-category leadership challenging even for major vendors.

In 2025, Teladoc Health advanced value-based chronic care by launching its next-generation Cardiometabolic Health Program, tying all program fees to outcomes. Leading vendors are shifting from standalone digital products to contract-backed care models. Consolidation is rising in the mid-market as companies integrate software, monitoring, and care management. For instance, Health Recovery Solutions acquired Rimidi in March 2026, combining chronic disease management workflows with device integrations for DexCom G7, FreeStyle Libre, and Eversense into EHR-connected programs. Controlling the device-to-EHR pipeline strengthens payer value and provider workflow alignment.

Despite product diversity, gaps remain in care navigation and long-term user engagement, as many apps struggle to retain users after initial needs are met. This gap impacts clinical outcomes and contract renewals. In April 2026, OURA expanded strategically by acquiring Galen AI to integrate clinical records and lab results with real-time biometric data from the Oura Ring. Future market leaders will likely be those who combine connected data, clinical workflow access, and sustained user engagement into scalable platforms.

MHealth Apps Industry Leaders

Apple Inc.

Teladoc Health, Inc.

Google LLC

Epic Systems Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ŌURA acquired Galen AI, a health data aggregation platform connecting to over 10,000 healthcare systems, to integrate clinical records and lab results with continuous biometric data from the Oura Ring.

- March 2026: Health Recovery Solutions acquired Rimidi, a chronic disease management company, integrating DexCom G7, FreeStyle Libre, and Eversense CGM data into EHR workflows, achieving a 2.8% reduction in HbA1c for high-risk type 2 diabetes patients.

- March 2026: MyFitnessPal acquired Cal AI, an AI-powered nutrition tracking app with over USD 40 million in trailing 12-month sales, strengthening its position within a 280-million-member global community.

- November 2025: Validic acquired assets of Trapollo to expand its EHR-integrated remote patient monitoring platform, which supported over 300,000 enrolled patients at a West Coast integrated delivery network.

- September 2025: Apple received FDA clearance for the Hypertension Notification Feature on Apple Watch Series 9 and later, expected to notify over 1 million users with undiagnosed hypertension within its first year across more than 150 countries.

Global MHealth Apps Market Report Scope

As per the scope of the report, mHealth apps (short for mobile health applications) are software programs designed for smartphones, tablets, or wearable devices that support health and wellness management. They combine digital technology with healthcare services, making medical information and monitoring more accessible to patients and providers.

The mHealth apps market is segmented by app type, platform, functionality, end-user, and geography. By app type, the market includes disease & treatment management apps (chronic disease management apps, medication adherence apps, remote monitoring apps, women’s health & pregnancy apps, diagnostic & symptom checker apps), wellness management apps (fitness & exercise tracking apps, nutrition & diet apps, mental wellness & mindfulness apps, sleep tracking apps, weight management apps), and other app types (personal health record apps, telehealth & virtual consultation apps, health education & awareness apps, professional reference & networking apps). By platform, the market is segmented into Android, iOS, and other platforms. By functionality, the market is categorized into monitoring services, fitness solutions, diagnostic services, treatment services, and care navigation & engagement. By end-user, the market is segmented into patients & consumers, healthcare providers, payers & employers, and life sciences & research organizations. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Disease & Treatment Management Apps | Chronic Disease Management Apps |

| Medication Adherence Apps | |

| Remote Monitoring Apps | |

| Women's Health & Pregnancy Apps | |

| Diagnostic & Symptom Checker Apps | |

| Wellness Management Apps | Fitness & Exercise Tracking Apps |

| Nutrition & Diet Apps | |

| Mental Wellness & Mindfulness Apps | |

| Sleep Tracking Apps | |

| Weight Management Apps | |

| Other App Types | Personal Health Record Apps |

| Telehealth & Virtual Consultation Apps | |

| Health Education & Awareness Apps | |

| Professional Reference & Networking Apps |

| Android |

| iOS |

| Other Platforms |

| Monitoring Services |

| Fitness Solutions |

| Diagnostic Services |

| Treatment Services |

| Care Navigation & Engagement |

| Patients & Consumers |

| Healthcare Providers |

| Payers & Employers |

| Life Sciences & Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By App Type | Disease & Treatment Management Apps | Chronic Disease Management Apps |

| Medication Adherence Apps | ||

| Remote Monitoring Apps | ||

| Women's Health & Pregnancy Apps | ||

| Diagnostic & Symptom Checker Apps | ||

| Wellness Management Apps | Fitness & Exercise Tracking Apps | |

| Nutrition & Diet Apps | ||

| Mental Wellness & Mindfulness Apps | ||

| Sleep Tracking Apps | ||

| Weight Management Apps | ||

| Other App Types | Personal Health Record Apps | |

| Telehealth & Virtual Consultation Apps | ||

| Health Education & Awareness Apps | ||

| Professional Reference & Networking Apps | ||

| By Platform | Android | |

| iOS | ||

| Other Platforms | ||

| By Functionality | Monitoring Services | |

| Fitness Solutions | ||

| Diagnostic Services | ||

| Treatment Services | ||

| Care Navigation & Engagement | ||

| By End User | Patients & Consumers | |

| Healthcare Providers | ||

| Payers & Employers | ||

| Life Sciences & Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the mHealth apps market

The mHealth apps market size stands at USD 46.16 billion in 2026 and is forecast to reach USD 92.69 billion by 2031 at a 14.96% CAGR.

Which app category leads revenue in mobile health applications

Disease and Treatment Management Apps led with 54.75% of revenue in 2025, reflecting the stronger monetization of clinically oriented use cases.

Which segment is growing fastest in mHealth applications

Wellness Management Apps are growing fastest by app type at a 16.70% CAGR, while Android is the fastest-growing platform at 17.45% CAGR through 2031.

Why is North America ahead in this space

North America held 41.61% of revenue in 2025 because of high chronic disease prevalence, strong telehealth usage, and reimbursement support for qualifying digital therapeutics.

What is driving provider adoption of mobile health tools

Healthcare Providers are projected to grow at a 15.96% CAGR as hospitals and physician groups adopt remote monitoring, decision support, and EHR-connected applications.

What is the biggest operating challenge for app developers

Long-term engagement and data trust remain major challenges, with studies showing a sharp decline in active use over time and clear links between engagement levels and clinical outcomes.

Page last updated on: