Mexico Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

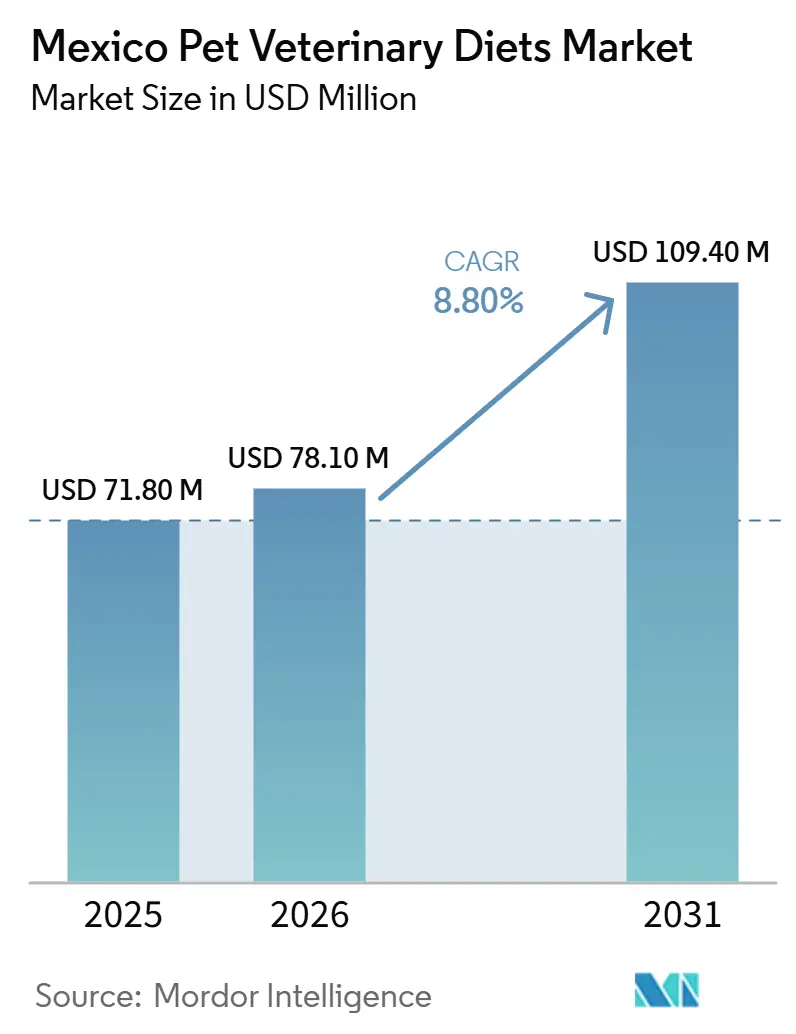

| Base Year Market Size (2025) | USD 71.80 Million |

| Market Size (2026) | USD 78.10 Million |

| Market Size (2031) | USD 109.40 Million |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

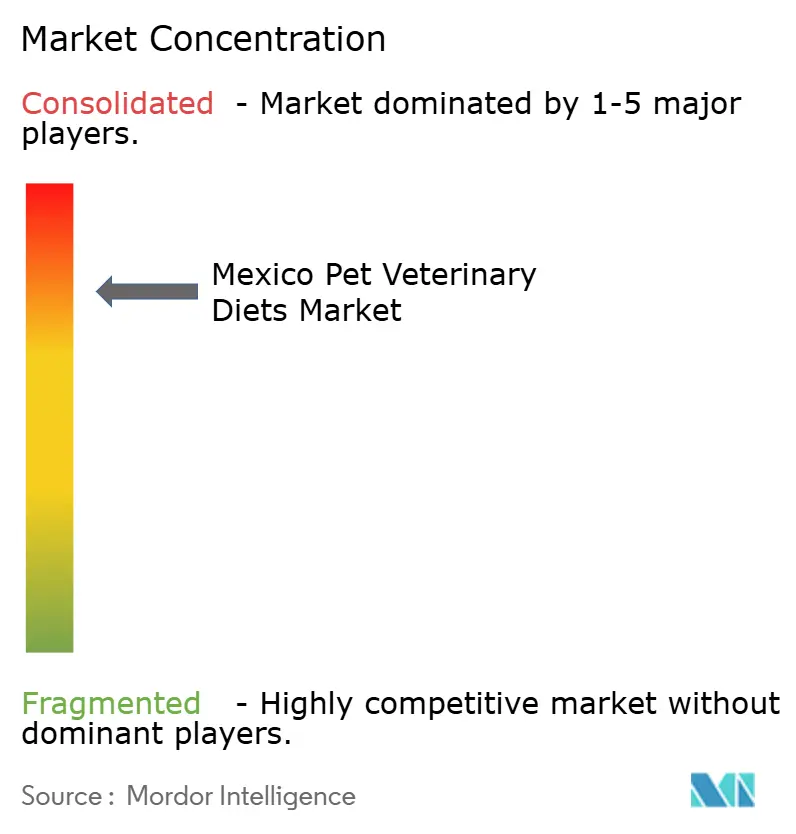

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Mexico Pet Veterinary Diets Market size is estimated to increase from USD 71.80 million in 2025 to USD 78.10 million in 2026 and reach USD 109.40 million by 2031, growing at a CAGR of 8.80% over 2026-2031. The market is expanding faster than the broader Mexico pet food market, indicating that therapeutic nutrition is becoming a more significant component of premium pet care spending. This category remains relatively insulated from the price pressures affecting mainstream pet food, as most purchases are driven by veterinary recommendations and recurring medical needs. Currently, the Mexico pet veterinary diets market has potential for further growth as clinical awareness and treatment compliance improve. Demand is concentrated in urban centers such as Mexico City, Guadalajara, and Monterrey, where higher-income households and well-established clinic networks support the adoption of prescription diets. Market competition is influenced by factors such as veterinary trust, brand credibility, and supply chain reliability. Additionally, local manufacturing investments and e-commerce refill models are creating opportunities for scaling the market, despite challenges related to regulations and import processes.

Key Report Takeaways

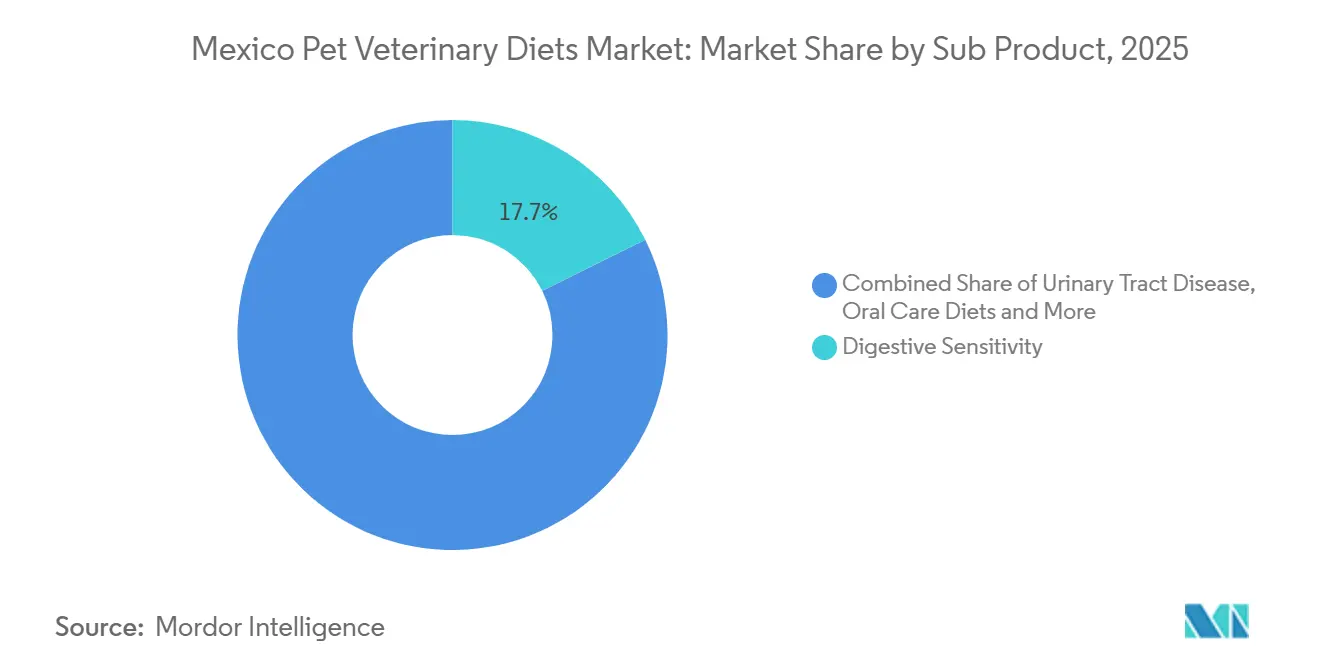

- By sub product, digestive sensitivity held 17.7% of the Mexico pet veterinary diets market share in 2025, while oral care diets is projected to grow at a 9.0% CAGR through 2031.

- By pets, dogs accounted for 79.9% share of the Mexico pet veterinary diets market size in 2025, while cats are projected to grow at a 8.4% CAGR through the forecast period.

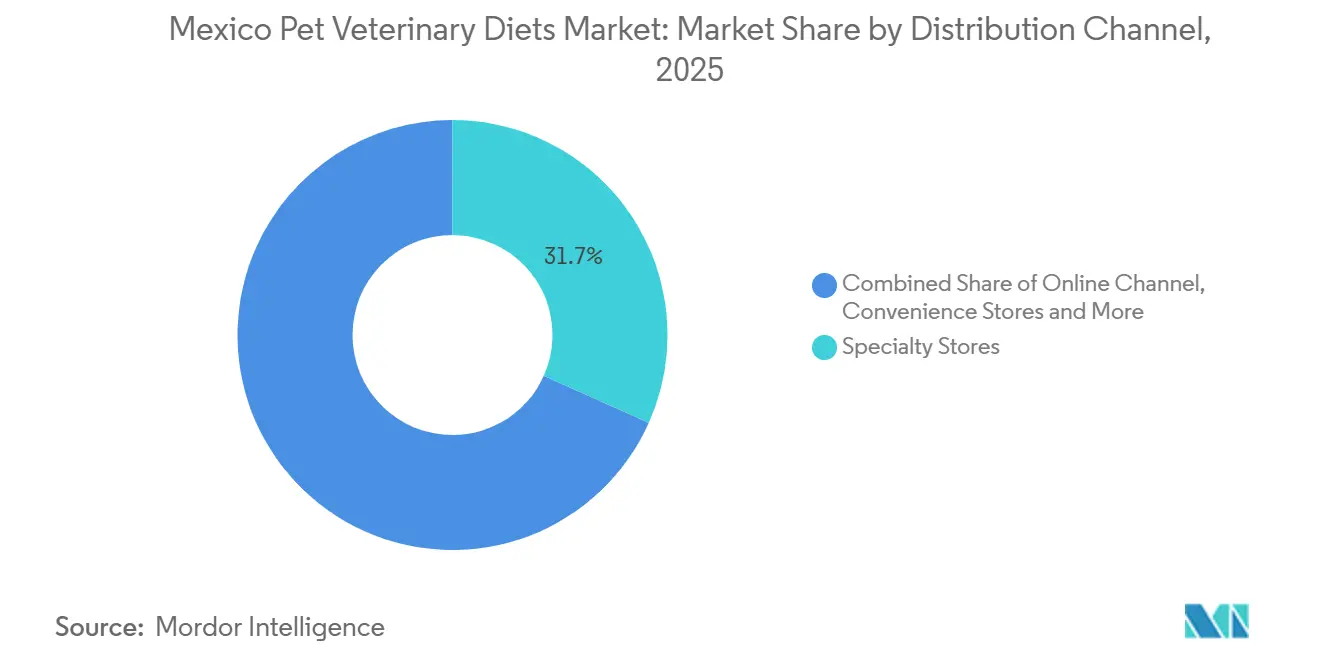

- By distribution channel, specialty stores led with 31.7% share of the Mexico pet veterinary diets market size in 2025, while the online channel is forecast to expand at a 10.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Burden In Companion Animals | +2.0% | Mexico-wide, concentrated in Mexico City, Guadalajara, and Monterrey | Medium term (2-4 years) |

| Pet Humanization And Premium Nutrition Trade Up | +1.5% | Urban Mexico, strongest in Mexico City and Monterrey | Long term (≥ 4 years) |

| Expansion Of Veterinary Clinic Led Recommendation Pathways | +1.6% | Mexico-wide, with early gains in metropolitan corridors | Medium term (2-4 years) |

| Growth Of Tele Veterinary Prescription Workflows | +0.7% | Urban and peri-urban Mexico, with spillover to secondary cities | Medium term (2-4 years) |

| Rising Demand For Condition Specific Functional Formulations | +1.2% | National, strongest in Mexico City, Guadalajara, and Monterrey | Long term (≥ 4 years) |

| Urban E Commerce And Refill Convenience For Prescription Diets | +0.9% | National, with highest digital adoption in Mexico City metro | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden in Companion Animals

Obesity, chronic kidney disease, and diabetes are increasingly prevalent among companion animals in urban areas of Mexico, driven by indoor lifestyles and calorie-dense feeding habits. These trends have a direct impact on the Mexico pet veterinary diets market, as such conditions typically require long-term nutritional management rather than short-term treatment. A 2026 study published in the Journal of the American Veterinary Medical Association (JAVMA) reported that cats on veterinary therapeutic renal diets had a 45% lower risk of progression to chronic kidney disease and a 5-month longer mean survival than untreated counterparts[1]Source: Journal of the American Veterinary Medical Association, “Use of a Veterinary Therapeutic Renal Diet in Cats with Early Chronic Kidney Disease Is Associated with Slower Disease Progression and Improved Survival,” JAVMA, avmajournals.avma.org. This evidence shifts the perception of these diets from discretionary feeding to medically necessary feeding. As more small-animal specialists operate in Mexico's larger cities, these diets are increasingly becoming part of routine clinical protocols rather than optional recommendations. As a result, renal and diabetes-specific formulas have a stronger prescription foundation compared to general wellness products. This contributes to a more stable repeat-purchase pattern in the Mexico pet veterinary diets market, particularly among households managing chronic conditions.

Pet Humanization and Premium Nutrition Trade Up

The Mexico pet veterinary diets market is benefiting from a growing trend of households viewing pets as family members, leading to increased spending on products that offer measurable health benefits rather than basic maintenance feeding. According to a Symrise insight published in 2026, 78% of Mexican pet owners expressed interest in personalized nutrition, although only 30% were familiar with the concept. This gap presents an opportunity for veterinarians and brands to educate consumers on therapeutic diets and encourage their adoption. Data from Conafab cited in 2025 indicated that the average annual spending on pet healthcare and nutrition in Mexico was MXN 15,200 (USD 760) per household. When pet owners perceive prescription diets as preventive rather than emergency expenses, it becomes easier to sustain repeat purchases. This shift in consumer behavior supports the growth of the Mexico pet veterinary diets market, particularly in areas such as digestive, renal, metabolic, and dermatological health.

Expansion of Veterinary Clinic Led Recommendation Pathways

Veterinary clinics are the most trusted point of conversion in the Mexico pet veterinary diets market, as therapeutic diets typically require explanation, diagnosis, and follow-up. Unlike in the mainstream packaged food market, where shelf visibility drives sales, this market relies on veterinarians to recommend diets, monitor patient responses, and guide owners on refills and compliance. Better access to technology in veterinary clinics can enhance diet recommendations and ensure refill continuity at scale. As management and distribution tools become more widespread in veterinary care systems, prescribing therapeutic diets becomes more streamlined, and owners will not discontinue them prematurely. This strengthens clinical adherence and supports a more stable sales base in the Mexico pet veterinary diets market.

Growth of Tele Veterinary Prescription Workflows

Tele-veterinary tools are facilitating access to the Mexico pet veterinary diets market for pet owners residing outside the primary clinic-dense metropolitan areas. This is significant as over 60% of Mexico’s estimated 80 million companion animals are located beyond the three main urban clusters. While remote consultations do not eliminate the need for in-person diagnoses, they help reduce the frequency of follow-up visits, refill approvals, and dietary monitoring. In May 2024, Nestlé S.A. (Purina) expanded the availability of Pro Plan Veterinary Diets on Amazon, demonstrating how prescription-support workflows can integrate digital consultations with home delivery to create a more streamlined model[2]Source: Nestlé Purina, “Purina Pro Plan Veterinary Diets Announces Availability in Amazon Store,” Purina News Center, newscenter.purina.com. Although Mexico’s tele-veterinary framework is still evolving, this channel is anticipated to gradually improve access to repeat prescriptions, particularly in areas where physical specialty retail options are limited.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Price Relative To Mass Market Pet Food | -1.3% | National, most pronounced outside Mexico City, Guadalajara, and Monterrey | Long term (≥ 4 years) |

| Import Duties And Compliance Costs For Specialized Imports | -0.7% | National, with stronger effect on non-metropolitan distribution chains | Medium term (2-4 years) |

| Uneven Veterinary Access Outside Major Metropolitan Areas | -0.8% | Rural and semi-urban Mexico, especially states with limited clinic infrastructure | Long term (≥ 4 years) |

| Prescription Friction And Low Awareness Among First Time Pet Owners | -0.5% | National, especially younger urban households entering pet ownership | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Product Price Relative to Mass Market Pet Food

Price remains a significant barrier to adoption in the Mexico pet veterinary diets market, particularly outside affluent urban households. Therapeutic diets in Mexico are typically priced at three to five times the cost of standard dry pet food, limiting trial usage and reducing the number of pet owners who can sustain long-term use. According to El Economista, Mexico's overall pet food market grew by only 3.9% in 2025, as household income pressures hindered the shift to premium formats. This cautious spending behavior also impacts prescription nutrition, even when there is a clear medical need. In 2025, Colgate-Palmolive Company (Hill Pet Nutrition Inc.)’s exit from private-label manufacturing indicated a stronger focus on higher-value branded products rather than expanding into more affordable mid-tier price points. As long as premium therapeutic diets remain significantly more expensive than mainstream feeding options, adoption will likely remain concentrated among higher-income households. Brands that introduce smaller pack sizes, subscription-based models, or improved refill options may help address this challenge, but the affordability gap continues to constrain the Mexico pet veterinary diets market.

Import Duties and Compliance Costs for Specialized Imports

Most therapeutic diet stock-keeping units in the Mexico pet veterinary diets market continue to rely on imports from North America or Europe. This reliance results in additional costs due to SENASICA (National Service for Agri-Food Health, Safety and Quality) clearance, labeling reviews, ingredient approvals, and transport lead times. Tariff uncertainties stemming from trade dynamics between the United States and Mexico have already led to a more cautious approach in parts of the supply chain. According to Conafab data cited by PetfoodLatinAmerica in July 2025, these uncertainties have caused delays in product launches and postponed expansion decisions as companies closely monitor the trade environment. Mexico continued expanding domestic pet food manufacturing capacity in 2024–2025, led by Nestlé S.A. (Purina)'s USD 220 million investment, reflecting manufacturers' efforts to meet growing domestic demand and enhance supply chain efficiency. Smaller foreign brands face significant challenges due to their limited scale and lack of robust regulatory infrastructure. Until local supply expands and regulatory processes become more streamlined, import-related cost pressures will continue to limit the variety of products available in the Mexico pet veterinary diets market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Sensitivity Leads Revenue, Oral Care Gains Momentum

Digestive Sensitivity accounted for 17.7% of the Mexico pet veterinary diets market share in 2025, making it the largest sub-product group by revenue. Gastrointestinal disorders are among the most common reasons for veterinary consultations, driving demand for this category due to their clinical relevance and frequent repeat purchases. A December 2025 study published in Frontiers in Veterinary Science found that a highly digestible prescription diet increased the odds of recovery from acute canine diarrhea by 1.6 times compared to standard care[3]Source: Frontiers in Veterinary Science, “A New Highly Digestible Prescription Diet Containing Bacillus velezensis DSM 15544 for the Management of Acute Diarrhea in Dogs,” Frontiers in Veterinary Science, frontiersin.org. This clinical foundation supports veterinarians' confidence and explains why digestive formulas are often the initial prescription choice for many pet owners. Renal, urinary tract disease, and obesity diets represent the next significant demand segment, driven by the increasing prevalence of chronic conditions in companion animals. While the Mexico pet veterinary diets market is diversifying in terms of treatment options, digestive formulas remain a cornerstone due to their high incidence rates and strong familiarity among clinicians.

Oral Care Diets represent the fastest-growing sub-product in the Mexico pet veterinary diets market, with a projected CAGR of 9.0% through 2031. Despite the widespread prevalence of periodontal disease in older dogs, this category remains underpenetrated, presenting significant opportunities for prescription growth. In 2025, Virbac updated its Veterinary HPM Small and Toy food with a natural ingredient targeting plaque, tartar, gum bleeding, and bad breath, highlighting increased product investment in oral-care nutrition by established suppliers. Additionally, Hill’s Pet Nutrition Inc. expanded its multi-condition feeding approach in June 2026 by introducing new renal formulas that address concurrent skin or gastrointestinal sensitivities. Diabetes and dermatological diets are also gaining traction, particularly in Mexico’s major cities, where veterinarians are increasingly prescribing condition-specific nutrition for extended treatment cycles. Although the "Other Veterinary Diets" category remains smaller, it addresses cases outside the leading categories, thereby broadening the market’s clinical scope. Overall, growth in the Mexico pet veterinary diets market is increasingly driven by formulas designed to meet more specific and complex patient needs.

By Pets: Dogs Drive Market Growth, Cats Represent Emerging Opportunity

Dogs accounted for 79.9% of the Mexico pet veterinary diets market share in 2025, reflecting their significant presence in household ownership and a well-established canine prescription culture. Data from Conafab indicated that dogs represented 71.7% of Mexico’s overall pet food volume, further supporting the demand for therapeutic nutrition in this segment. This large base underpins the importance of canine-specific formulas for digestive health, obesity, renal care, and oral care in driving revenue within the Mexico pet veterinary diets market. In April 2024, Royal Canin expanded its gastrointestinal product line with five new diets, while Hill’s Pet Nutrition Inc. continued to launch new prescription products in 2025 and 2026, maintaining a steady flow of dog-focused therapeutic feeding options. Additionally, the dog segment benefits from greater familiarity among veterinary clinics, as conditions such as obesity, orthopedic stress, gastrointestinal issues, and dental problems are widely recognized by general practitioners. As a result, dogs are estimated to remain the primary revenue driver in the Mexico pet veterinary diets market throughout the forecast period.

Although cats represent a smaller revenue base, they are gaining clinical significance in the Mexico pet veterinary diets market, with a projected CAGR of 8.4% during the forecast period. A 2026 Journal of the American Veterinary Medical Association's study revealed that cats on therapeutic renal diets had a mean survival time of 31 months compared to 26 months without dietary therapy, providing veterinarians and pet owners with a compelling reason to adopt early dietary interventions. This evidence supports improved compliance in managing chronic kidney disease, a key therapeutic area for feline nutrition. In December 2024, General Mills acquired Whitebridge Pet Brands for USD 1.45 billion to strengthen its presence in the premium cat feeding segment, highlighting the growing value of the cat market within the broader premium pet space. Consequently, cats represent a smaller but increasingly dynamic opportunity in the Mexico pet veterinary diets market.Other pets, including birds, rabbits, and small mammals, contribute marginally to the Mexico pet veterinary diets market in value terms. However, their presence indicates a gradual expansion of specialized feeding beyond the traditional focus on dogs and cats.

By Distribution Channel: Specialty Stores Lead, Online Redefines Access

Specialty stores accounted for 31.7% share of the market in 2025, reflecting their suitability for prescription verification and personalized diet guidance. These stores provide more than just shelf space, as pet owners often need help distinguishing between therapeutic products and premium general pet food. Additionally, specialty outlets benefit from their proximity to clinics or direct links with veterinary practices, enhancing conversion rates following consultations. This makes them a critical channel in the Mexico pet veterinary diets market, particularly in cases where disease management and follow-up care are prioritized over impulse purchases. Their product assortment remains focused on medically relevant stock-keeping units, a feature that mainstream mass channels find challenging to replicate. Furthermore, this channel aligns well with brands that depend on veterinarian trust rather than competing primarily on price.

The online channel is projected to grow at a CAGR of 10.6% through 2031, making it the fastest-expanding distribution channel in the Mexico pet veterinary diets market. In May 2024, Nestle S.A. (Purina) made its Purina Pro Plan Veterinary Diets portfolio available through Amazon’s Mexico store. This development highlight the market's transition from isolated purchases to digitally supported continuity. While supermarkets, hypermarkets, convenience stores, and other channels remain relevant, they primarily cater to prescription-adjacent support products rather than the core of medically managed nutrition. As e-commerce infrastructure and refill behaviors improve, the Mexico pet veterinary diets market is projected to shift further toward hybrid clinic-plus-digital models. This evolution is anticipated to enhance both market reach and compliance while maintaining the veterinarian's central role in decision-making.

Geography Analysis

The Mexico pet veterinary diets market is primarily concentrated in Mexico City, Guadalajara, and Monterrey. These metropolitan areas benefit from advanced veterinary infrastructure, higher household incomes, and access to premium retail outlets. These factors make them the primary hubs for prescription-diet demand, as they combine diagnostic capabilities with the financial capacity to support long-term therapeutic feeding. Additionally, Mexico City has a well-developed e-commerce logistics network, facilitating practical refill deliveries for diets requiring regular replenishment.

Secondary cities such as Puebla, Querétaro, León, and Tijuana represent the next phase of growth for the Mexico pet veterinary diets market. Querétaro, in particular, was noted in 2026 for its expanding formulation infrastructure, driven by increasing demand for functional pet nutrition. The growing preference for smaller-breed dogs also supports higher unit-value feeding in urban and secondary city households, even as per-animal consumption volumes decrease. These secondary cities are significant as they bridge the gap between the fully developed metropolitan areas and the underserved regions of the country.

Rural and semi-urban areas in Mexico remain the least served regions in the pet veterinary diets market. Limited clinic density restricts diagnostic capabilities, while lower disposable incomes reduce the number of pet owners who can sustain prescription diets over extended periods. This creates a disparity between areas where therapeutic diets are medically beneficial and where they are consistently accessible. Future market expansion in these regions will rely heavily on improved distribution networks, better refill accessibility, and expanded veterinary coverage beyond the main metropolitan corridors.

Competitive Landscape

The Mexico pet veterinary diets market exhibits a highly concentrated structure. Key players include Mars Incorporated (through Royal Canin), Nestlé S.A.(through Purina Pro Plan Veterinary), Colgate-Palmolive Company (through Hill’s Prescription Diet), Farmina Pet Food (through VetLife), and Virbac (through Veterinary HPM). Their competitive advantage extends beyond shelf presence, relying heavily on veterinarian trust, clinical evidence, and consistent supply chain management. For instance, Hill’s Pet Nutrition Inc.'s sales in 2025 are driven by science-based platforms like ActivBiome+, which enhance the brand’s credibility in therapeutic nutrition. In the Mexican market, this evidence-based positioning is critical, as clinicians often favor brands with a strong research and education foundation.

Competitive dynamics in the market are evolving through innovations in product design and distribution strategies. In September 2025, Virbac introduced Vikaly, the world’s first medicated feed for cats that integrates renal nutrition with a veterinary pharmaceutical, showcasing the potential for closer integration of nutrition and treatment in future therapeutic models. Farmina Pet Food expanded its North American veterinary platform in July 2025 and inaugurated its first United States manufacturing facility in June 2025 for enhancing scale, supply reliability, and professional outreach, which will support future growth in North America including Mexico. Despite the competitive nature of the market, brand trust remains a critical differentiator, making it challenging for new entrants to establish themselves without strong clinical backing.

A second wave of competition is emerging through continously research and better product formats. Royal Canin and Hill’s Pet Nutrition Inc. continued to expand their offerings for multi-condition needs. Smaller brands still have opportunities to compete, particularly in areas such as oral care, affordable multi-condition nutrition, and fresh therapeutic-adjacent products. However, entering the Mexico pet veterinary diets market at scale remains challenging without robust clinical support and disciplined channel execution.

Mexico Pet Veterinary Diets Industry Leaders

Mars Incorporated

Nestlé S.A. (Purina)

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Farmina Pet Food

Virbac

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Hill's Pet Nutrition Inc. launched Prescription Diet k/d + Derm Complete and k/d + z/d Hydrolyzed for dogs and cats with concurrent CKD and skin or gastrointestinal sensitivities, Mexico's first multi-indication wet renal diet, featuring ActivBiome+ Kidney Defense prebiotic fiber technology.

- April 2026: Hill's Pet Nutrition Inc. launched Prescription Diet Metabolic + j/d for cats, combining weight management and joint health support in a single formula clinically shown to achieve 88% feline weight loss within 2 months at home.

- March 2025: ADM officially opened its first wet pet food manufacturing plant in Yecapixtla, Morelos, Mexico, following a USD 39 million investment. The manufacturing plant will produce veterinary diets as well.

Mexico Pet Veterinary Diets Market Report Scope

Pet veterinary diets (also known as therapeutic or prescription diets) are specialized, scientifically formulated pet foods designed to treat, prevent, or manage specific medical conditions.

The Mexico Pet Veterinary Diets Market Report is segmented by sub product (Diabetes, Renal, Urinary Tract Disease, Digestive Sensitivity, Oral Care Diets, Derma Diets, Obesity Diets, and Others), by pets (Cats, Dogs, and Other Pets), by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and others). The market forecasts are provided in terms of value in USD and volume in metric tons.

| Diabetes |

| Renal |

| Urinary Tract Disease |

| Digestive Sensitivity |

| Oral Care Diets |

| Derma Diets |

| Obesity Diets |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Diabetes |

| Renal | |

| Urinary Tract Disease | |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Derma Diets | |

| Obesity Diets | |

| Other Veterinary Diets | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the projected value of Mexico pet veterinary diets by 2031?

The market is forecast to reach USD 109.40 million by 2031, rising from USD 78.10 million in 2026 at an 8.8% CAGR.

Which pet type contributes most to therapeutic diet sales in Mexico?

Dogs lead by a wide margin, with 79.9% share in 2025, supported by higher ownership and a more established canine prescribing culture.

Which sub product is growing the fastest in therapeutic pet nutrition in Mexico?

Oral Care Diets is the fastest-growing sub product, with a projected 9.0% CAGR through 2031.

Why do specialty stores still lead sales despite online growth?

Specialty stores remain important because they support prescription verification, diet counseling, and clinic-linked purchases that general retail cannot match easily.

What is the main barrier to wider adoption of prescription pet diets in Mexico?

The biggest barrier is price, since therapeutic diets often cost 3x to 5x more than standard dry pet food, especially limiting uptake outside high-income urban households.

Page last updated on: