Mexico Irrigation Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

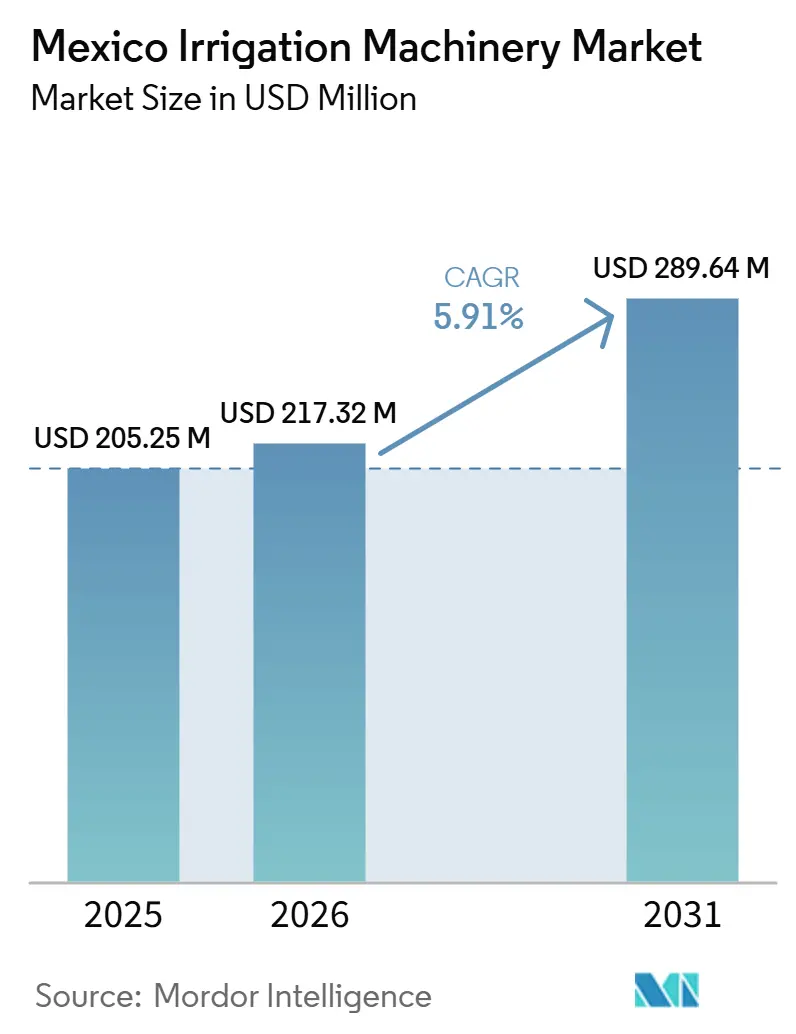

| Base Year Market Size (2025) | USD 205.25 Million |

| Market Size (2026) | USD 217.32 Million |

| Market Size (2031) | USD 289.64 Million |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

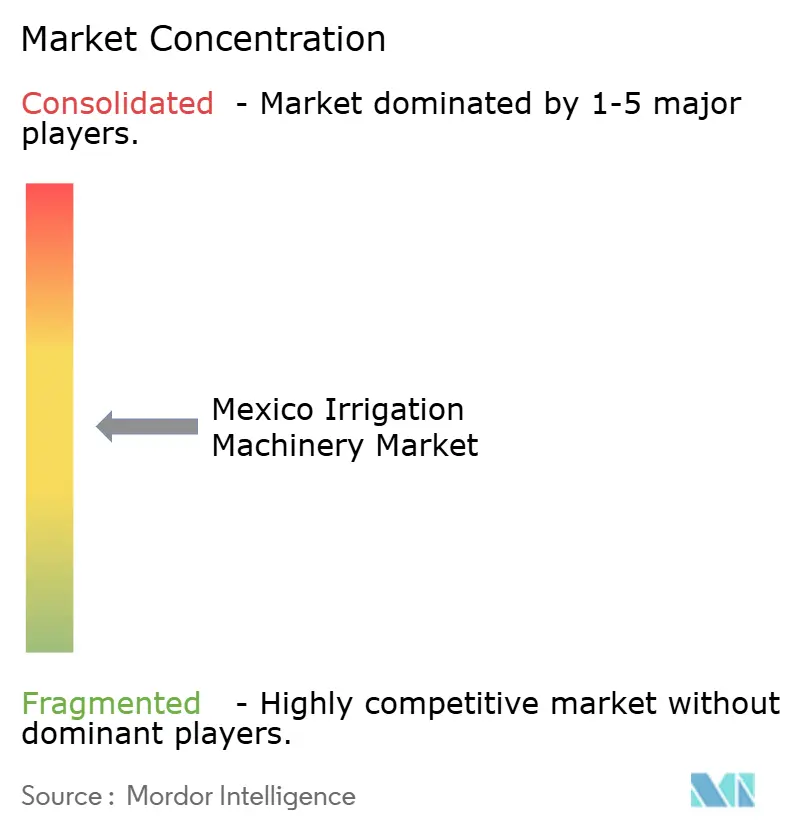

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Irrigation Machinery Market Analysis by Mordor Intelligence

The Mexico irrigation machinery market size is projected to expand from USD 205.25 million in 2025 and USD 217.32 million in 2026 to USD 289.64 million by 2031, registering a CAGR of 5.91% during 2026-2031. Agriculture used 76% of Mexico’s water resources, and 34% of irrigation water was wasted through deteriorated hydraulic infrastructure, which kept irrigation modernization high on the policy agenda in the Mexico irrigation machinery market [1]Source: Pamela Cruz, “Unprecedented Worldwide, Mexico National Irrigation Modernization Program, Says Conagua,” mexicanpressagency.org. The Comisión Nacional del Agua (CONAGUA) launched its national irrigation technification program in 2025, and the six-year investment pool exceeded USD 3.7 billion (MXN 63 billion), across 18 irrigation districts with 40.0% physical progress recorded by November 2025. That spending is pulling demand toward drip systems, sprinklers, pressurized pipes, automated gates, flow measurement units, photovoltaic pumping, and telemetry-linked controls across the country. Competition is also shifting because Rivulis Irrigation Limited (Temasek Holdings) added local manufacturing capacity in León and Tijuana in 2024, while Netafim Ltd. (Orbia) moved further into digital irrigation management with GrowSphere, which pushes the market beyond hardware-only competition. The main constraints come from water-right reform uncertainty and exposure to imported technology, but official support of up to USD 5,971 (MXN 107,478) per hectare for collective parcel technification and up to 100% project support for renewable-energy pumping materially lower adoption risk for participating users.

Key Report Takeaways

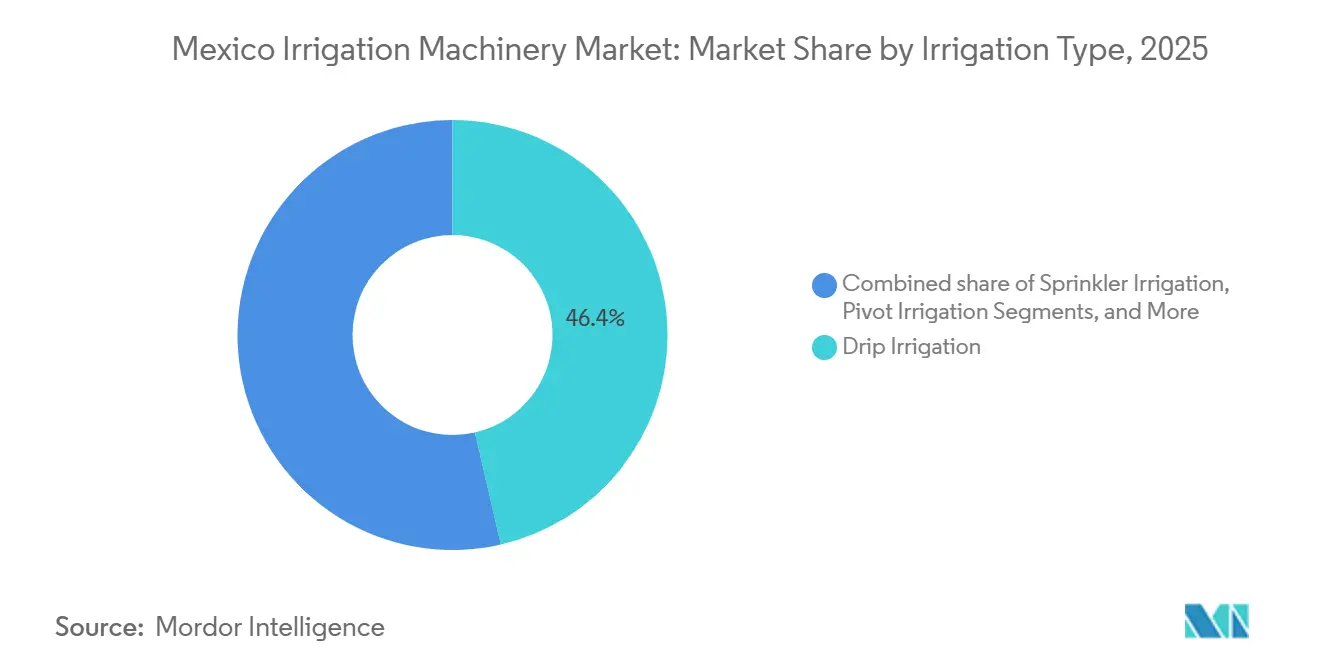

- By irrigation type, drip irrigation held 46.4% of the Mexico irrigation machinery market share in 2025 as the largest segment, while pivot irrigation is the fastest-growing segment and is forecast to expand at an 8.1% CAGR during 2026-2031.

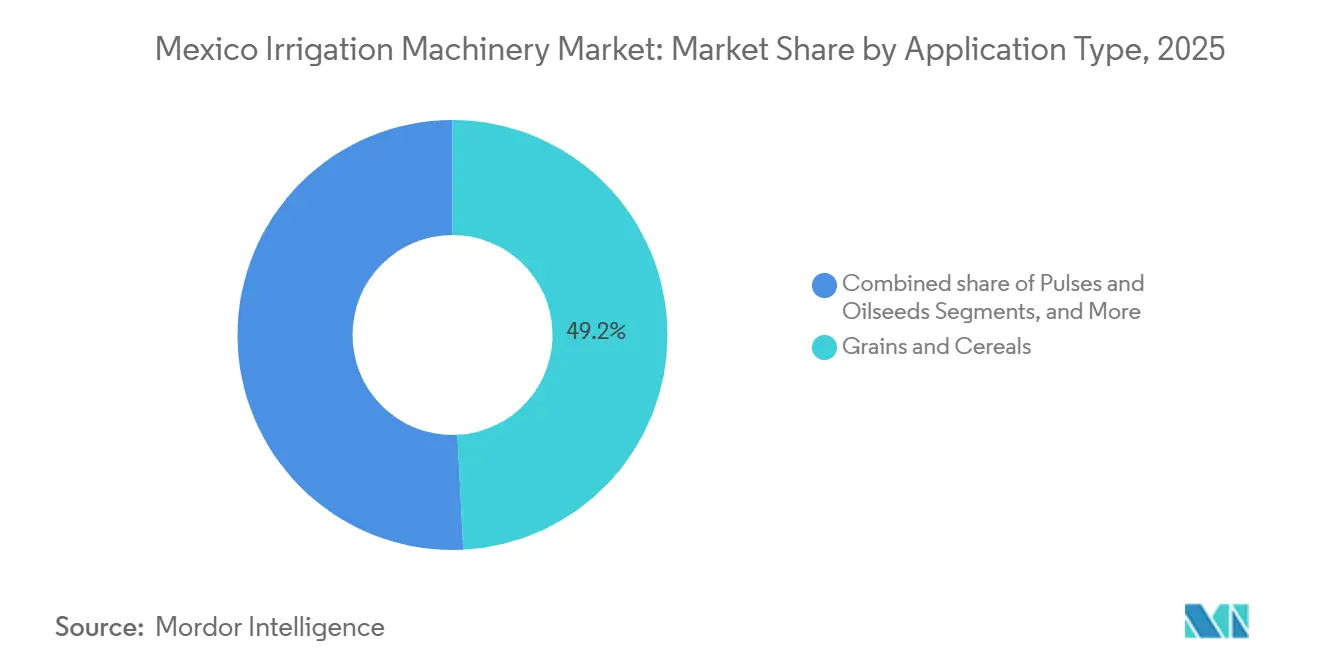

- By application type, grains and cereals accounted for 49.2% of the Mexico irrigation machinery market size in 2025 as the largest segment, while fruits and vegetables are the fastest-growing segment and are projected to grow at a 9.4% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water scarcity and irrigation-loss reduction mandate | +1.40% | Strongest in Sinaloa, Sonora, Chihuahua, and Tamaulipas where water stress and canal losses are accelerating irrigation upgrades | Short term (≤ 2 years) |

| Federal irrigation technification spending acceleration | +1.60% | Highest relevance in Sonora, Sinaloa, Tamaulipas, Guanajuato, Chihuahua, Hidalgo, and Aguascalientes under active federal modernization projects | Short term (≤ 2 years) |

| Export horticulture and protected farming expansion | +1.10% | Strongest across Northern and Central Mexico’s fruit, vegetable, and protected farming clusters with high irrigation intensity | Medium term (2-4 years) |

| Precision irrigation and automation uptake | +0.80% | Concentrated in export-oriented commercial farming regions adopting fertigation, automation, and remote irrigation management | Medium term (2-4 years) |

| Water-title regularization improving project bankability | +0.30% | National relevance, especially in irrigation districts undergoing registry, metering, and compliance modernization | Long term (≥ 4 years) |

| Solar well retrofits and telemetry-led modernization bundles | +0.50% | Growing relevance in rural irrigation regions and off-grid farming areas adopting solar pumping and monitoring systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water Scarcity and Irrigation-Loss Reduction Mandate

Modernization of irrigation infrastructure has become a national priority to improve agricultural water-use efficiency and address persistent conveyance losses. The Comisión Nacional del Agua (CONAGUA) stated that modernization of agricultural irrigation districts is anticipated to recover more than 2.8 billion m3 of water, while major infrastructure works can recover up to 40% of the water transported, and parcel-level technification can recover up to 55%. This changes purchasing behavior because irrigation equipment is now tied to water security and regulatory pressure, rather than solely to yield improvement. The strongest pull is visible in northern districts where drought exposure and canal losses are already constraining farm operations. As more districts move from open conveyance to pressurized delivery, the Mexico irrigation machinery market is seeing increased demand for pipes, gates, valves, filters, meters, and field application systems.

Federal Irrigation Technification Spending Acceleration

Expansion of the national irrigation technification program is accelerating demand for modern irrigation equipment, with project coverage increasing from 13 to 18 irrigation districts[2]Source: Itzel Vázquez, “Conagua Presenta Avances del Programa Nacional de Tecnificación de Riego,” aneas.com.mx. The National Association of Water and Sanitation Utilities (ANEAS) reported that 2025 goals included more than 500 km of canal lining and piping, 6,000 hectares of land leveling and parcel technification, 139 rehabilitated wells with photovoltaic systems, 11 pumping plants, and 41 measurement structures. Procurement is increasingly bundled, so suppliers are now asked to support canal automation, measurement systems, pumping upgrades, and parcel irrigation within the same contract structure. Pabellón irrigation district in Aguascalientes reached 76.0% progress in 2025 and has become a practical reference point for districts now moving into similar upgrade cycles. Because program rules also prioritize volumetric measurement and automation, spending extends well beyond basic irrigation hardware in Mexico's irrigation machinery industry.

Export Horticulture and Protected Farming Expansion

Export horticulture and protected farming continue to move the Mexico irrigation machinery market toward higher-value systems with tighter water control. Scientific evidence cited in the user draft showed that advanced greenhouse tomato production can use 4 liters of water for 1 kg of tomatoes, while basic technology can require 300 liters for the same output [3]Source: Francisco Suazo-López et al., “Socioeconomic Analysis of the Use of Water Management Technology by Mexican Greenhouse Tomato Farmers Toward Sustainable Production,” frontiersin.org. That performance gap pushes growers toward emitters, pressure regulators, filters, fertigation injectors, and sensors where water use must be managed at plant level. Protected operations also rely on more frequent irrigation decisions, which raises the value of controllers and advisory software compared with broad-acre field crops. This keeps fruits and vegetables closely linked to incremental equipment demand within the Mexico irrigation machinery market even when total installed acreage remains larger in staple crops.

Precision Irrigation and Automation Uptake

Precision irrigation and automation are becoming standard in the Mexico irrigation machinery market for commercial farms that need closer control over water, fertilizer, labor, and system performance. Netafim Ltd. launched GrowSphere in October 2024 as an all-in-one irrigation and fertigation management platform with crop advisor tools for more than 30 crop types. The platform also connects plant and hydraulic system monitoring, turning irrigation management into a recurring service layer rather than a one-time equipment sale. Frontiers in Sustainability found that 90% of low-yield farmers still relied on experience to determine irrigation timing and volume, indicating that a large productivity gap remains for digital tools. As that gap narrows, the market should continue shifting toward connected controllers, data-linked fertigation, and remote monitoring platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost for smallholders and ejidos | -1.50% | Strongest in Southern Mexico and ejido-dominated farming regions with limited financing access and weaker farm cash flows | Short term (≤ 2 years) |

| Limited technical service depth outside major clusters | -0.80% | Highest impact in remote rural regions and Southern Mexico where maintenance and technical support networks remain limited | Medium term (2-4 years) |

| Water-concession reform uncertainty | -0.60% | Strongest in water-stressed northern states where regulatory uncertainty affects irrigation investment timing | Short term (≤ 2 years) |

| Imported-system dependence and exchange-rate exposure | -0.50% | National relevance due to dependence on imported irrigation components, controls, and cross-border supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost for Smallholders and Ejidos

The high upfront cost remains the largest adoption barrier for smaller farms across the country. Frontiers in Sustainability found that low- and medium-yield producers often lacked the financial capacity to purchase water measurement and control equipment, and much of their income was spent on household needs rather than on farm modernization. The same study showed that many small-scale producers were not organized in a way that improved access to government or private financing for machinery and equipment. Subsidy support helps, but program access still depends on documentation, group participation, and administrative readiness that smaller communities do not always have. The result is a dual-speed upgrade cycle in which export-oriented operators move first, while smallholders advance more slowly within the Mexico irrigation machinery market.

Water-Concession Reform Uncertainty

Water-concession reform uncertainty is a near-term restraint for the Mexico irrigation machinery market because investment timing depends on the stability of water-use rights. Holland and Knight reported that the Mexican Senate approved the General Water Law and amendments to the National Water Law in December 2025, with the reform restricting private-party concession transfers and placing reassignment processes under the control of the Comisión Nacional del Agua (CONAGUA). The user draft also stated that the new framework took full effect on July 1, 2026, and tightened the timing for concession extensions, potentially delaying machinery purchases for users approaching renewal. The reform also created a new registry structure and stricter enforcement expectations, requiring farms to spend more time on compliance before new projects proceed. The restraint is real in the short run, even though tighter measurement and reporting requirements may later support replacement demand for compliant equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Irrigation Type: Drip Irrigation Commands the Largest Installed Base and Pivot Irrigation Shows the Fastest Momentum

Drip irrigation held 46.4% of the Mexico irrigation machinery market share in 2025, which made it the largest irrigation type in the country. Its position is strongest in export vegetables, berries, orchards, and other cropping systems where water placement and fertigation precision directly affect yield and operating cost. Sprinkler irrigation held the next largest position and continues to benefit from district modernization programs that specify pressurized field systems for crop conversion and water control.

Pivot irrigation is the fastest segment, and it is projected to advance at a 8.1% CAGR during 2026-2031 in the Mexico irrigation machinery market. Large grain and oilseed farms in Chihuahua, Tamaulipas, and Sonora are leading that move as they replace gravity-fed methods with mechanized field systems. Lindsay Corporation supports this shift with FieldNET connectivity, while Valmont Industries, Inc. extends a similar remote-control value proposition through its Valley telemetry platforms. Within drip systems, replacement demand is moving beyond commodity tubing and into emitters, pressure regulators, sensors, controllers, filters, and valves that improve system performance. Netafim Ltd. launched the Hybrid Dripline in February 2025 as an integral dripline with a built-in outlet, which directly addressed manual hole-punching and fitting migration issues in higher-precision applications. Rivulis Irrigation Limited (Temasek Holdings) reinforced local supply in 2024 through its León and Tijuana operations, which improved delivery responsiveness for drip and micro-irrigation products used across the Mexico irrigation machinery industry.

By Application Type: Grains and Cereals Form the Largest Revenue Base and Fruits and Vegetables Deliver the Fastest Expansion

Grains and cereals accounted for 49.2% of the Mexico irrigation machinery market size in 2025, which made them the largest application segment. This position reflects the wide irrigated area committed to corn, wheat, sorghum, and rice across Northern and Central Mexico. Much of the spending in this segment is tied to modernizing existing district infrastructure rather than greenfield expansion. Pulses and oilseeds remain a smaller revenue segment, but they continue to receive targeted irrigation support as crop diversification and district modernization move together.

Fruits and vegetables is the fastest application segment, and it is projected to advance at a 9.4% CAGR during 2026-2031. This crop group creates disproportionate demand for emitters, pressure regulators, fertigation injectors, filters, sensors, and digital controllers because water and nutrient delivery must be managed more precisely. Protected growing systems also require closer irrigation scheduling, which lifts equipment value per hectare in this part of the industry. Scientific evidence cited in the draft showed that advanced greenhouse tomato production can operate with 4 liters of water per kilogram, compared with 300 liters under basic technology, which explains why higher-value crop systems pull faster upgrades. That keeps fruits and vegetables central to incremental revenue growth even while grains and cereals continue to anchor the largest installed base in the Mexico irrigation machinery market.

Geography Analysis

Northern Mexico was the largest regional base of the Mexico irrigation machinery market in 2025. Sinaloa, Sonora, Chihuahua, and Tamaulipas combine large irrigated farming areas with the strongest pressure to reduce conveyance loss and improve parcel efficiency. The National Association of Water and Sanitation Utilities (ANEAS) reported progress of 55.0% in Río Mayo and Río Yaqui in Sonora, 47.0% in Culiacán in Sinaloa, and 39.0% in Valle de Juárez in Chihuahua by November 2025. Those districts create steady demand for drip systems, pivots, pumping upgrades, automated gates, and measurement structures as works move from canals into parcel equipment. Recurrent drought and tighter water management rules keep efficiency-centered procurement at the core of regional demand.

Central Mexico is the fastest-growing regional cluster in the Mexico irrigation machinery market during 2026-2031. Guanajuato, Hidalgo, Aguascalientes, Michoacán, and Morelos sit at the overlap of federal modernization work and higher-value crop systems that require closer irrigation control. Pabellón in Aguascalientes reached 76.0% progress in 2025, which made it the clearest operating reference point for district-wide modernization under the national program. ANEAS also reported that Alto Río Lerma in Guanajuato reached 39.0% progress and that Valle del Mezquital in Hidalgo remained one of the major interventions within the program pipeline. This mix of public works, commercial farming, and protected cultivation gives Central Mexico the strongest acceleration profile over the forecast period.

Southern Mexico remains the smallest current footprint in the country for irrigation machinery, but it still holds meaningful expansion potential. Lower starting penetration means that even smaller irrigation projects can change equipment demand quickly in Oaxaca, Guerrero, Chiapas, and the Yucatán Peninsula. A photovoltaic irrigation project in Quintana Roo reported 1.30 megawatts of installed capacity and irrigation coverage of more than 80 hectares, showing that solar-powered pumping can support farm development where grid access is weaker. The same project used 2,487 solar panels and supplied water for sugarcane, papaya, and vegetable production, which highlights the close link between energy access and irrigation adoption. As federal modernization gradually spreads into additional districts, the southern states should see a broader rise in pumps, parcel systems, controls, and monitoring equipment.

Competitive Landscape

The Mexico irrigation machinery market is moderately concentrated, with leading companies such as Netafim Ltd., Rivulis Irrigation Limited, Valmont Industries, Inc., Rain Bird Corporation, and Lindsay Corporation competing across major irrigation equipment categories. Competitive advantage is increasingly determined by localized manufacturing, digital irrigation capabilities, regulatory compliance, and comprehensive after-sales support rather than product hardware alone. Public irrigation modernization programs and large-scale agricultural projects increasingly favor suppliers capable of delivering integrated solutions encompassing irrigation infrastructure, pumping systems, automation, monitoring, and water measurement technologies, allowing regional system integrators to remain competitive alongside global manufacturers.

Rivulis Irrigation Limited made the most significant localization investment during 2024 by expanding its manufacturing footprint in Mexico. The company inaugurated a new production facility in León in August 2024, followed by North America's largest micro-irrigation manufacturing facility in Tijuana in September 2024. These investments substantially increase domestic production capacity for drip irrigation products, improve product availability, shorten delivery lead times, and strengthen supply chain resilience for the Mexican market while reinforcing Mexico's role as a manufacturing hub for the Americas. In contrast, Netafim Ltd. strengthened its competitive positioning through global technology innovation, launching GrowSphere in October 2024 and the Hybrid Dripline in February 2025. Although these product introductions were not Mexico-specific, they raise the competitive benchmark for suppliers operating in the country by accelerating the adoption of connected irrigation management platforms and higher-performance drip irrigation technologies.

Competition is also expanding beyond equipment sales toward integrated service and digital agriculture offerings. In April 2024, rieggo acquired a 51% stake in Irrigación de Vanguardia (IrriVan) and increased its ownership in the Rotoplas Agricultural Water joint venture to 88%, strengthening its domestic irrigation engineering and project execution capabilities. Further supporting this trend, Irritec México partnered with Hydrosat in December 2025 to integrate irrigation systems with seven-day irrigation planning, soil moisture monitoring, and crop intelligence powered by high-resolution thermal satellite imagery and artificial intelligence. Meanwhile, Lindsay Corporation and Valmont Industries, Inc. continue to benefit from growing demand among large commercial farms for connected center-pivot irrigation ecosystems, while specialized suppliers remain competitive in retrofit solutions, filtration, valves, and irrigation control components. As a result, competition is increasingly centered on delivering integrated irrigation solutions, digital decision-support capabilities, and localized technical services, creating opportunities for both established global manufacturers and agile regional players.

Mexico Irrigation Machinery Industry Leaders

Netafim Ltd. (Orbia Advance Corporation)

Rivulis Irrigation Limited (Temasek Holdings)

Valmont Industries, Inc. (Valley Irrigation)

Rain Bird Corporation

Lindsay Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Netafim Ltd. expanded deployment of its GrowSphere precision irrigation platform across commercial berry and vegetable farms in Sinaloa and Jalisco states of Mexico. The system integrates real-time sensor monitoring, automated fertigation control, and cloud-based irrigation analytics designed to reduce water and fertilizer consumption while improving export-crop yields.

- December 2025: Irritec S.p.A. Mexico partnered with Hydrosat to integrate satellite thermal imagery and artificial intelligence-driven 7-day irrigation planning into Irritec’s Mexico service offering. Hydrosat stated that the combined solution is designed to support yield gains of up to 50.0% and water-use reductions of up to 30.0% in the drought-stressed region.

- August 2025: Netafim Ltd. launched Mega-PULSAR, a full-coverage pulsing sprinkler designed to protect orchards from extreme heat stress. The company stated that initial installations began in Spring 2025 for avocado, mango, and lychee crops and that the product uses low-volume pulses to create a localized cooling microclimate.

Mexico Irrigation Machinery Market Report Scope

The Mexico irrigation machinery market covers equipment used to apply, control, measure, and optimize water delivery in agricultural production across irrigated farming systems. It includes sprinkler, drip, and pivot irrigation, and related control and monitoring equipment used across broadacre crops, horticulture, and other irrigated applications in Mexico.

The Mexico irrigation machinery market is segmented by Irrigation Type (Sprinkler Irrigation, Drip Irrigation, Pivot Irrigation, and Other Irrigation Types), and by Application Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Other Applications). The Market Forecasts are Provided in Terms of Value (USD)

| Sprinkler Irrigation | Pumping Unit |

| Tubing | |

| Couplers | |

| Spray or Sprinkler Heads | |

| Fittings and Accessories | |

| Sensors | |

| Controllers | |

| Injectors | |

| Flow Meters | |

| Drip Irrigation | Valves |

| Backflow Preventers | |

| Pressure Regulators | |

| Filters | |

| Emitters | |

| Tubing | |

| Other Drip Irrigation Components | |

| Pivot Irrigation | |

| Other Irrigation Types |

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Other Applications |

| By Irrigation Type | Sprinkler Irrigation | Pumping Unit |

| Tubing | ||

| Couplers | ||

| Spray or Sprinkler Heads | ||

| Fittings and Accessories | ||

| Sensors | ||

| Controllers | ||

| Injectors | ||

| Flow Meters | ||

| Drip Irrigation | Valves | |

| Backflow Preventers | ||

| Pressure Regulators | ||

| Filters | ||

| Emitters | ||

| Tubing | ||

| Other Drip Irrigation Components | ||

| Pivot Irrigation | ||

| Other Irrigation Types | ||

| By Application Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Other Applications | ||

Key Questions Answered in the Report

How large was the Mexico agricultural irrigation machinery market in 2025, and what is its projected growth through 2031?

The Mexico irrigation machinery market is projected to grow from USD 205.25 million in 2025 to USD 217.32 million in 2026 and reach USD 289.64 million by 2031.

Which irrigation type leads sales in Mexico?

Drip irrigation was the largest segment in 2025 with 46.4% share because it is widely used in horticulture, orchards, and other water-sensitive cropping systems.

Which application is growing the fastest?

Fruits and vegetables is the fastest-growing application segment, with a projected 9.4% CAGR during 2026-2031 because these crops need tighter control over water and fertigation.

What are the main barriers to wider adoption?

The main barriers are high upfront cost for smallholders, limited service support outside major clusters, water-right reform uncertainty, and dependence on imported technology and parts.

Page last updated on: