Mexico Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

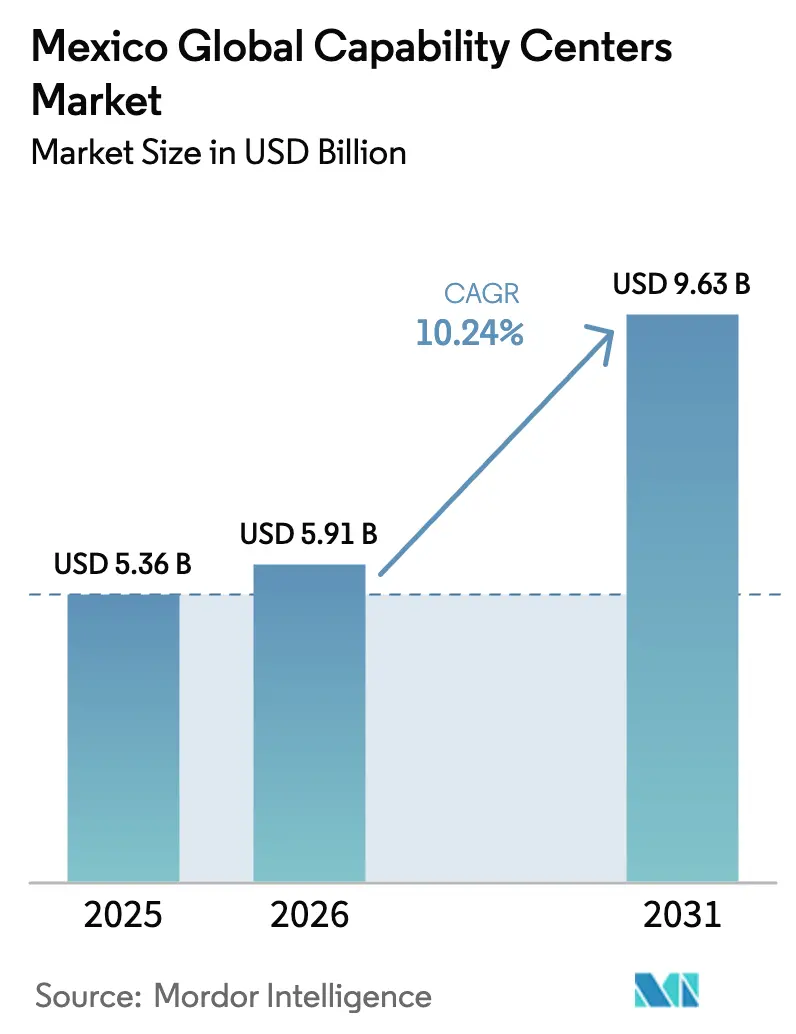

| Base Year Market Size (2025) | USD 5.36 Billion |

| Market Size (2026) | USD 5.91 Billion |

| Market Size (2031) | USD 9.63 Billion |

| Growth Rate (2026 - 2031) | 10.24% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Global Capability Centers Market Analysis by Mordor Intelligence

The Mexico global capability centers market size in 2026 is estimated at USD 5.91 billion, growing from 2025 value of USD 5.36 billion with 2031 projections showing USD 9.63 billion, growing at 10.24% CAGR over 2026-2031. Mexico’s near-shore location, a large STEM talent base, and cost advantages have created sustained momentum for enterprise investment in advanced digital, engineering, and back-office hubs. Tight U.S.–China geopolitical dynamics, renewed supply-chain resilience goals, and the operational continuity afforded by shared time zones are prompting U.S. corporations to expand their headcount in Mexico's global capability centers and market footprints. Government incentives under the IMMEX framework and the Tehuantepec Isthmus economic zone continue to compress total delivered costs, while nationwide 5G coverage is fostering the data-intensive use cases that modern capability centers now deliver. As a result, the Mexico global capability centers market is steadily shifting away from pure labor arbitrage toward higher-value digital services that align with global corporate transformation agendas.

Key Report Takeaways

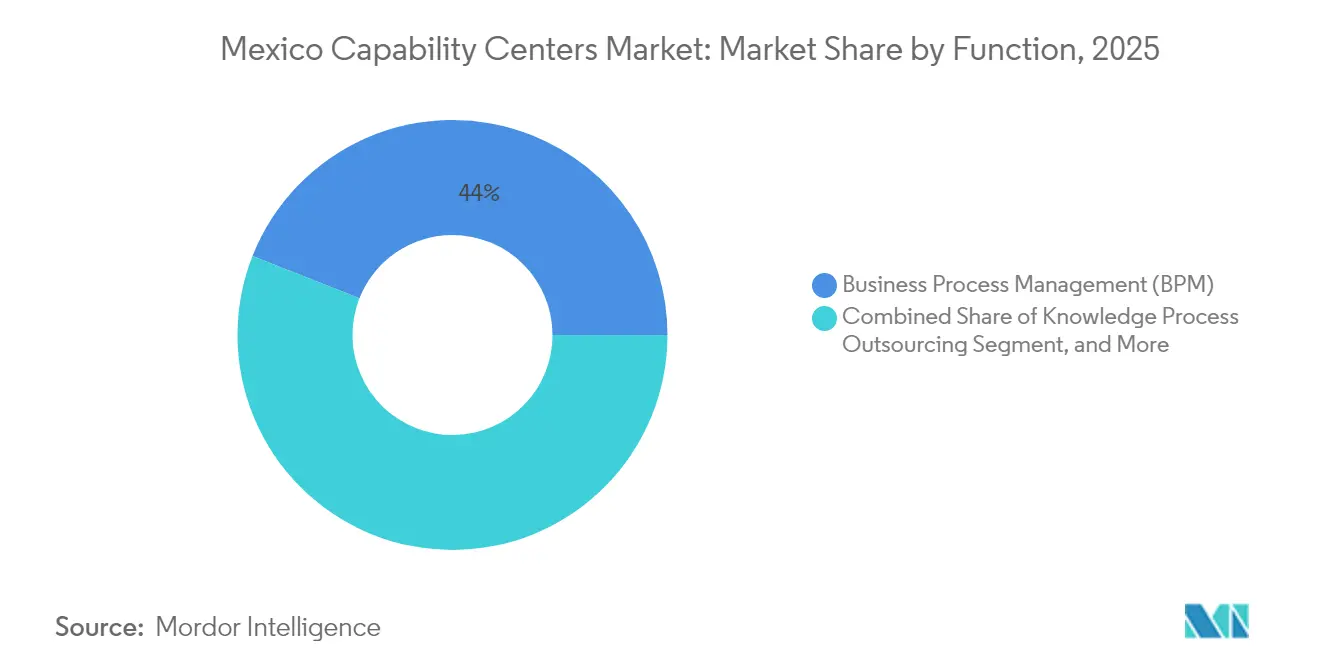

- By function, Business Process Management led with a 44.02% global market share in Mexico's capability centers in 2025, whereas Information Technology and Digital Services are projected to expand at a 10.66% CAGR through 2031.

- By engagement model, captive operations commanded 57.20% of the Mexico global capability centers market size in 2025, while hybrid build-operate-transfer structures are forecasted to grow at a 10.98% CAGR through 2031.

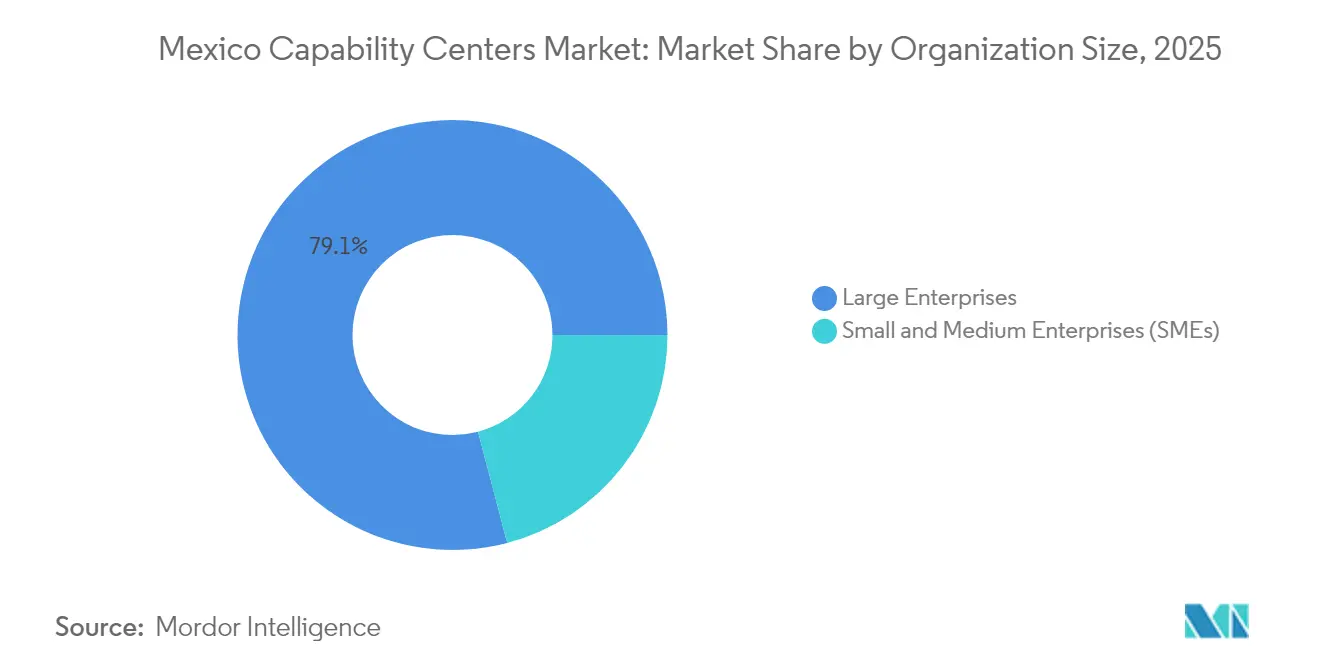

- By organization size, large enterprises accounted for 79.10% of the Mexico global capability centers market size in 2025; however, small and medium enterprises are expected to advance at an 11.46% CAGR between 2026 and 2031.

- By industry vertical, manufacturing, automotive, and industrial activities held 38.21% of the Mexico global capability centers market share in 2025, while retail and consumer goods are set to post a 10.84% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring demand from US clients | +3.2% | Mexico-US border states, Guadalajara, Mexico City | Short term (≤ 2 years) |

| Mexico's expanding STEM graduate pool | +2.1% | National, concentrated in Guadalajara, Monterrey, and Mexico City | Medium term (2-4 years) |

| Government tax incentives for IT exports | +1.8% | National, enhanced in the Tehuantepec Isthmus zone | Long term (≥ 4 years) |

| Rapid 5G rollout enabling advanced digital services | +1.5% | Tier-1 cities expanding to tier-2 locations | Medium term (2-4 years) |

| Peso cost-arbitrage versus the US and Canada | +1.2% | National with regional variations | Short term (≤ 2 years) |

| AI-based automation needs in legacy US operations | +0.7% | Technology corridors in Guadalajara, Mexico City | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nearshoring Demand From U.S. Clients

A surge in U.S. nearshoring is lifting the Mexico global capability centers market. Supply-chain upheavals and geopolitical shifts have driven American companies to relocate critical work closer to home, and the U.S.-Mexico-Canada Agreement gives investors predictable trade rules.[1]Reuters Staff, “Mexico STEM Education and Talent Pipeline Analysis,” Reuters, reuters.com Real-time collaboration across shared time zones eliminates coordination lags typical of Asian locations, and fresh manufacturing foreign direct investment of USD 45.46 billion in the first half of 2024 is spawning downstream demand for IT, engineering, and process services. Automotive and high-tech manufacturers are requesting integrated engineering and analytics support to accompany plant expansions, turning every greenfield factory into a multiplier for new service-center seats. The resulting pipeline supports larger multi-function hubs rather than small transactional units, locking in long-term enterprise commitments.

Mexico’s Expanding STEM Graduate Pool

A domestic pipeline of 130,000 STEM graduates per year is reinforcing the talent supply for Mexico's global capability centers market.[2]Financial Times Reporters, “Mexico Nearshoring Investment Surge Continues,” Financial Times, ft.com Accredited engineering programs in Guadalajara, Monterrey, and Mexico City are producing domain specialists who can handle complex digital twin modeling, embedded software, and data science assignments of global scale. Initiatives such as Tecnológico de Monterrey’s TECgpt ecosystem introduce AI tools to 90,000 students, accelerating readiness for enterprise AI workloads. Certification partnerships with Cisco and other vendors ensure a uniform standard of technical skills across the nation. Although 70% of graduates reside in tier-1 metros, firms are adopting hub-and-spoke models that tap virtual working to reach talent in secondary cities.

Government Tax Incentives For IT Exports

Federal incentive schemes cut operating costs across the Mexico global capability centers market. The IMMEX program grants duty-free import of equipment when final services are exported, shaving onboarding capex by 15-25%.[3]Wall Street Journal Bureau, “Mexico Automotive Production Growth Continues,” Wall Street Journal, wsj.com The Tehuantepec Isthmus zone offers tax reductions of up to 25% for qualifying investors, and research expenses can be deducted at double their face value. Plan Mexico, launched in 2024, streamlines permitting end-to-end, reducing go-live timelines by up to 40% and directing more high-value product engineering work to local sites. These incentives tilt the economics from a pure cost play to a sustained innovation base that holds proprietary IP.

Rapid 5G Rollout Enabling Advanced Digital Services

Nationwide 5G is now unlocking high-bandwidth, low-latency workloads inside the Mexico global capability centers market. Telcel already covers 125 cities, with AT&T Mexico and Movistar extending the footprint to another 85 combined. Thirteen million 5G lines, 9.1% of mobile connections, create fertile ground for edge analytics, augmented reality maintenance, and smart factory diagnostics. Industry surveys indicate that 70% of Mexican enterprises plan to adopt 5G by 2024, and imminent spectrum auctions are expected to widen capacity in 2025. The improved network baseline enables remote device monitoring for U.S. manufacturers and facilitates real-time collaboration across engineering teams, thereby enhancing both productivity and the breadth of services offered from Mexican hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from Colombia and Costa Rica | -1.8% | Regional competition affecting all Mexican locations | Medium term (2-4 years) |

| Persistent English-language skill gaps | -1.5% | National, most acute outside tier-1 cities | Long term (≥ 4 years) |

| Rising salary inflation in tier-1 Mexican cities | -1.2% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Regulatory uncertainty on outsourcing reforms | -0.9% | National, affecting all engagement models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition From Colombia and Costa Rica

Colombia and Costa Rica are positioning themselves as credible nearshore rivals, tempering growth in the Mexico global capability centers market. Colombia’s 15% English proficiency, three times Mexico’s, makes it attractive for voice-based customer operations, while Costa Rica’s established reputation in financial services outsourcing lures marquee banks. Currency swings have momentarily narrowed Mexico’s cost edge, and aggressive promotion by Bogotá and San José frames nearshoring as a broader Latin American phenomenon. Nevertheless, Mexico maintains scale, mature infrastructure, and direct trucking routes into the U.S. supply chain, limiting defections mainly to niche voice services rather than core digital engineering work.

Persistent English-Language Skill Gaps

Only 5% of the Mexican population is fluent in English, constraining client-facing roles and trimming the growth trajectory of the Mexico global capability centers market. Training vendors, such as Voxy and Pearson, deploy AI-driven language courses at a corporate scale, but nationwide uplift is resource-intensive. Tier-1 cities capture the majority of English-proficient graduates, leaving secondary metropolitan areas exposed to skill shortages that delay expansion plans. New public-school curricula emphasize English from early grades, yet workforce-level benefits will crystallize only after 2035. Until then, firms are combining recruitment of bilingual talent with machine translation tools to offset intercultural friction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Business Process Foundations, Digital Upshift

Business Process Management commanded 44.02% of the Mexico global capability centers market share in 2025, underpinned by established finance, HR, and procurement workflows that leverage Mexico’s cost-competitive labor and process maturity. Accounting consolidation, payables, and payroll have long moved to Mexican centers, freeing U.S. headquarters to focus on strategy. Many centers now embed robotic process automation and analytics overlays that improve first-pass yield and cycle-time benchmarks.

Information Technology and Digital Services form the fastest-growing segment, expanding at a 10.66% CAGR as enterprises demand cloud migration, DevOps, and AI model operations expertise. Agile squads located in Guadalajara and Mexico City iterate customer-facing apps synchronously with U.S. product owners, shortening release cadences. Engineering and R&D teams support silicon design, embedded firmware, and industrial IoT diagnostics, fueled by investments like Foxconn’s Nvidia superchip facility. Although knowledge process outsourcing remains sub-scale, patent searches, safety-regulation monitoring, and actuarial analytics are steadily widening the Mexico global capability centers market addressable ceiling.

By Engagement Model: Captive Depth, Hybrid Acceleration

Captive entities held 57.20% of the Mexico global capability centers market in 2025 as Fortune 500 manufacturers, banks, and technology firms pursued full control over IP, quality, and security. Dedicated centers in Monterrey handle proprietary drivetrain simulations for major automotive companies, while hubs in Mexico City manage sensitive payment network data for global card issuers. Internal academies give captives a competitive edge in retaining top engineers, despite local attrition pressures.

Hybrid build-operate-transfer models are projected to chart an 10.98% CAGR, as new entrants value phased risk transfer. Service providers set up legal entities, lease space, and seed initial governance before clients assume full reins. For mid-market technology vendors, the arrangement expedites entry without requiring in-depth local compliance expertise. The model also underpins satellite spoke launches in Querétaro and Puebla that feed into larger hubs, widening the Mexico global capability centers market fabric without heavy capex outlay.

By Organization Size: Enterprise Dominance, SME Democratisation

Large enterprises captured 79.10% of the Mexico global capability centers market size in 2025. Their financial scale enables multi-function campuses that house several thousand employees across design, cloud operations, and shared services. Microsoft’s USD 1.3 billion cloud and AI buildout exemplifies the deeper commitment of mega-caps to Mexican engineering ecosystems. Big firms also negotiate bulk telecom contracts and secure qualified vendors quicker.

Small and medium enterprises, although accounting for only 20.90% of the value, are on an 11.46% CAGR trajectory, as no-code workflow engines, public cloud, and managed Global Capability Center operators lower entry barriers. A Texas-based SaaS provider can now start with a 30-person Mexico global capability centers market pod focused on Level-2 support and scale in line with subscription growth. Government export-promotion grants and simplified customs clearance add further impetus to SME adoption.

By Industry Vertical: Manufacturing Core, Retail Momentum

Manufacturing, automotive, and industrial companies delivered 38.21% of 2025 revenue, reflecting Mexico’s position as the world’s fourth-largest auto producer with 3.03 million units built in the first three quarters. Engineering change management, plant-floor analytics, and digital twin simulations dominate workloads. Tier-1 suppliers co-locate design engineers with OEM capability centers to accelerate the introduction of new models.

Retail and consumer goods outpace all other verticals at a 10.84% CAGR as omnichannel growth mandates inventory visibility, last-mile routing analytics, and personalization engines. Mexican hubs run storefront microservices architectures for U.S. brands targeting Hispanic demographics, integrating payment, loyalty, and fulfillment data. Banking, financial services, and insurance centers anchor risk modeling and transactional compliance operations, while healthcare and life sciences clusters in Guadalajara are beginning to handle pharmacovigilance data and clinical trial analytics.

Geography Analysis

Mexico City, Guadalajara, and Monterrey together generated roughly three-quarters of 2025 revenue in the Mexico global capability centers market. Mexico City offers unrivaled headcount depth and proximity to regulators, drawing banks and telecom companies to its high-rise corridors. Guadalajara, often referred to as Mexico's Silicon Valley, hosts engineering labs for prominent companies such as Foxconn, Intel, and IBM, fostering a virtuous cycle of specialized talent and vendor ecosystems. Monterrey’s industrial heritage and proximity to the Texas border suit automotive and heavy-equipment firms that need rapid design-to-manufacture iteration.

Secondary cities are moving up the maturity curve. Querétaro secured AWS’s USD 5 billion cloud region, catalyzing a cluster of cybersecurity and DevOps roles. Puebla and León attract retail analytics and multilingual customer care, offering 30-40% lower real estate costs than tier-1 averages, which eases cost pressure as salary inflation creeps upward. Border locations such as Tijuana and Ciudad Juárez offer unparalleled physical access to U.S. clients, although companies must weigh security protocols and infrastructure gaps when planning mission-critical workloads.

An emerging hub-and-spoke model is evident. Enterprises locate leadership, solution architecture, and client engagement in tier-1 hubs, while situating repetitive analytics or 24/7 monitoring in spokes, such as Mérida or Chihuahua. Government highway upgrades and the ongoing 5G rollout are reducing response-time differentials, enabling distributed agile squads. Collectively, these dynamics broaden the geographic base of the Mexico global capability centers market without diluting operational consistency.

Competitive Landscape

Competitive intensity is rising, yet the Mexico global capability centers market remains moderately fragmented. U.S. and European consulting giants, including Accenture, IBM, and Cognizant, leverage established client portfolios to secure multi-tower deals spanning finance, cloud, and data. Indian majors such as Tata Consultancy Services, Infosys, and HCLTech are scaling rapidly; HCLTech alone hired 1,300 professionals in 2024, bringing its onshore employee count to 3,700.[4]Financial Times Technology Team, “HCLTech Mexico Expansion Strategy,” Financial Times, ft.com Local champions Softtek and Neoris differentiate through deep governmental networks, cultural alignment, and competitive bilingual rates.

Technology multinationals are shifting from vendors to competitors as they build their own captive centers. Microsoft’s hyperscale investment anchors AI research, while Google and AWS assemble cloud-region operations that double as internal support engines for North American clients. Niche digital studios specialize in UX, data engineering, or Industry 4.0 integration, capturing a significant market share within defined micro-verticals. Overall, success factors are evolving toward employer branding, specialist-skill academies, and verticalized solution offerings, rather than simply scaling seats.

Consolidation activity is limited but growing. Mid-sized U.S. cloud integrators are acquiring Guadalajara-based data engineering boutiques to secure scarce AI talent, and Mexican BPO providers are merging with near-shore peers to expand their geographic reach. The top five entities still control well under 30% of combined revenue, indicating ample opportunity for differentiated entrants with a sector or technology focus.

Mexico Global Capability Centers Industry Leaders

Accenture PLC

IBM Corporation

Tata Consultancy Services Limited

Cognizant Technology Solutions Corporation

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Tata Consultancy Services announced a USD 250 million investment to establish a new Global Capability Center in Monterrey, Mexico, with plans to hire 2,500 technology professionals by 2027. The facility focuses on advanced digital services, including artificial intelligence, cloud computing, and cybersecurity solutions for North American clients, marking TCS's largest single-location investment in Latin America.

- September 2025: Amazon Web Services completed the first phase of its USD 5 billion Querétaro data center region, launching 3 availability zones that provide cloud infrastructure services across Mexico and Central America. The infrastructure supports enterprise workloads that require low-latency connectivity and data residency compliance, with AWS projecting that the region will support 7,000 full-time equivalent jobs annually through 2030.

- August 2025: General Motors committed USD 1.2 billion to expand its technical center in Toluca, Mexico, adding 1,800 engineering positions focused on electric vehicle development and autonomous driving technologies. The investment includes advanced simulation facilities and battery testing laboratories that will support GM's global electrification strategy, with operations expected to reach full capacity by mid-2026.

- July 2025: Infosys opened a 500-seat Global Capability Center in Guadalajara, investing USD 80 million in the facility that specializes in engineering services, digital transformation, and artificial intelligence solutions. The center serves automotive, manufacturing, and financial services clients across North America, with Infosys planning to expand capacity to 1,200 seats by 2027 based on client demand.

Mexico Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the projected value of the Mexico global capability centers market by 2031?

Forecasts place the market at USD 9.63 billion by 2031, representing a 10.24% CAGR from 2026.

Which operating model is expanding fastest in Mexican capability centers?

Hybrid build-operate-transfer arrangements are growing at a 10.98% CAGR as companies seek phased risk transfer and operational flexibility.

Which industry vertical presently leads capability-center spending in Mexico?

Manufacturing, automotive, and industrial clients account for 38.21% of 2025 revenue.

Which cities host the majority of Mexican capability centers?

Mexico City, Guadalajara, and Monterrey account for approximately 75% of the market value, owing to their depth of talent and mature infrastructure.

How many STEM graduates does Mexico add annually?

Universities produce approximately 130,000 STEM graduates annually, thereby bolstering the engineering and digital talent pipeline.

What restrains growth linked to language proficiency?

Only 5% of the population is fluent in English, which limits the availability of client-facing roles and prompts firms to invest in language upskilling.

Page last updated on: