Mexico Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

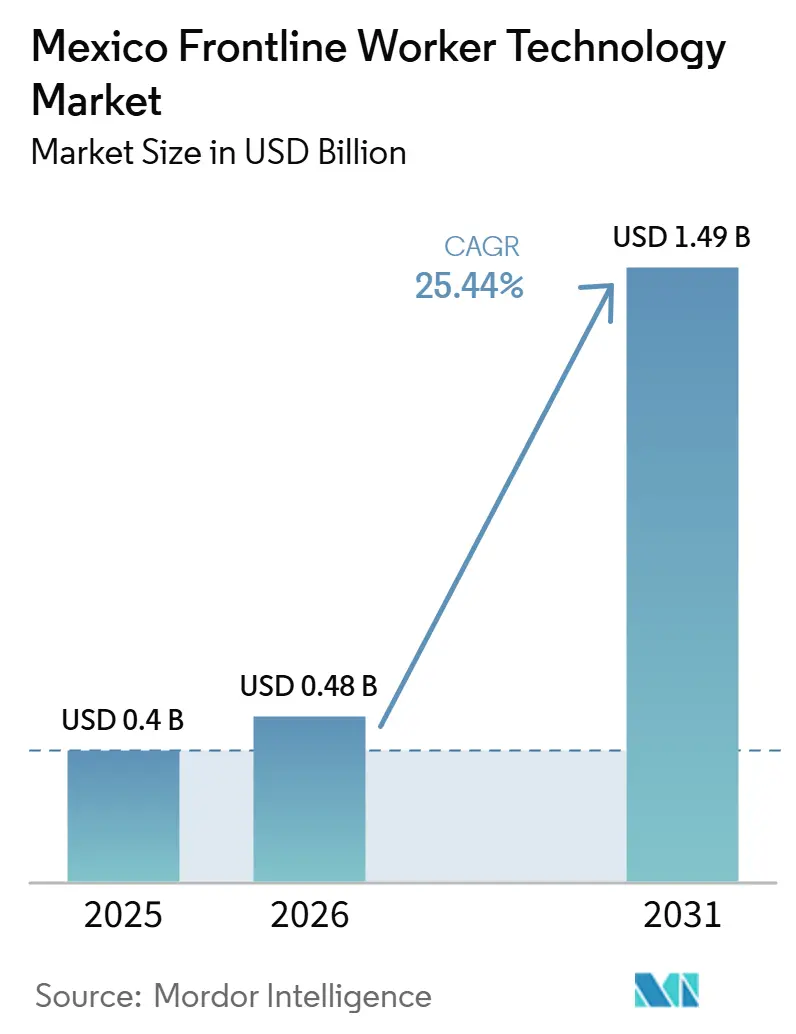

| Base Year Market Size (2025) | USD 0.4 Billion |

| Market Size (2026) | USD 0.48 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 25.44% CAGR |

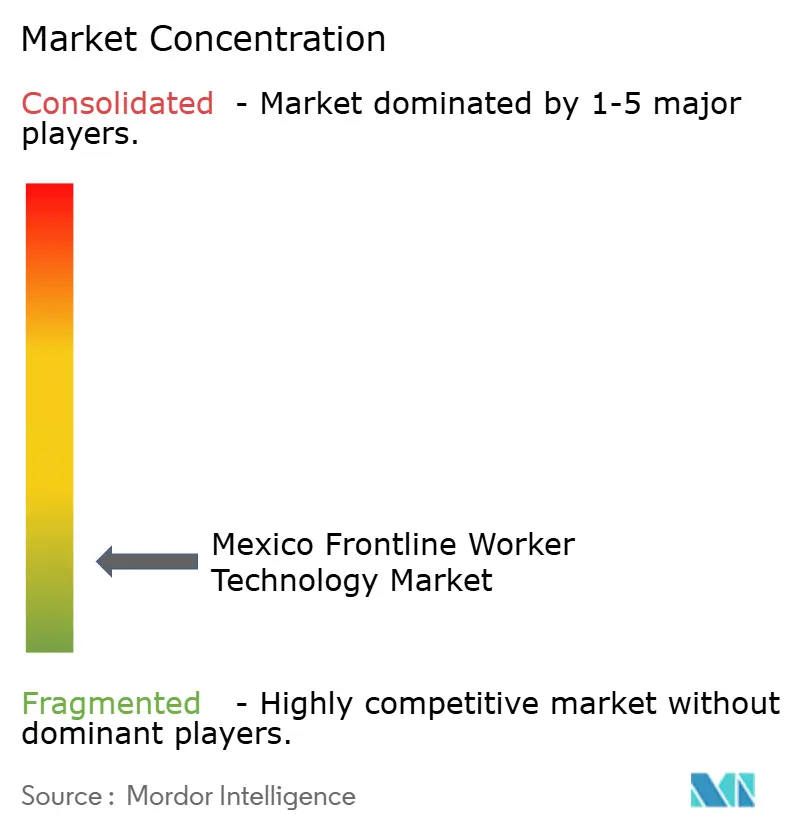

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Frontline Worker Technology Market Analysis by Mordor Intelligence

The Mexico frontline worker technology market size is projected to expand from USD 0.40 billion in 2025 and USD 0.48 billion in 2026 to USD 1.49 billion by 2031, registering a CAGR of 25.44% between 2026 and 2031. The Mexico frontline worker technology market is moving beyond isolated pilot programs as employers standardize communication, workflow execution, and compliance tracking across larger frontline workforces. Nearshoring activity continues to support demand because new and expanding industrial sites need digital processes that match the operating standards used by multinational parent facilities. The shift toward cloud-led deployments is also shortening rollout cycles and making these tools easier to extend across multiple locations with fewer local IT resources. Regulatory pressure around worker safety, documentation, and personal data handling is making frontline software part of daily operations rather than an optional administrative add-on. Competitive activity remains broad, with enterprise software firms, rugged hardware providers, and specialized application vendors all trying to secure long-term positions before category consolidation becomes more pronounced.

Key Report Takeaways

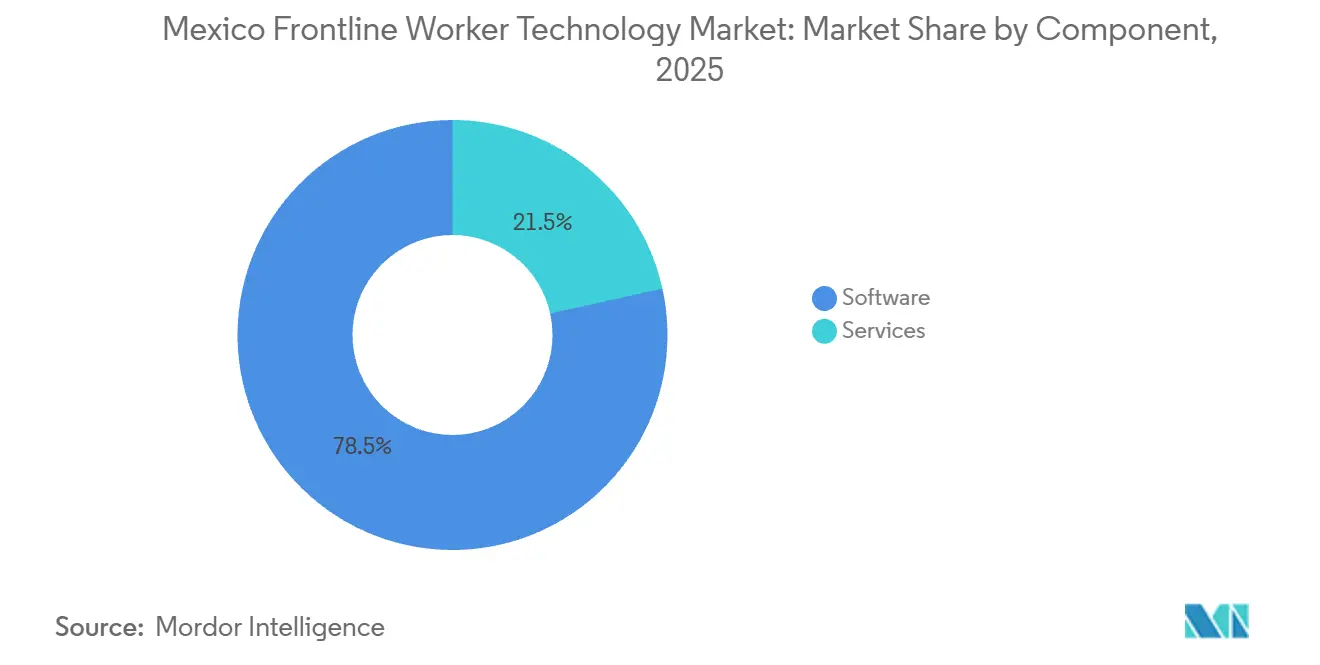

- By component, software held 79.24% revenue share in 2025, while services is projected to expand at a 28.42% CAGR through 2031.

- By deployment, cloud-based deployment held 72.36% share in 2025, and it is also projected to record the fastest CAGR at 26.18% through 2031 in the Mexico frontline worker technology market.

- By organization size, large enterprises accounted for 66.81% share in 2025, while small and medium enterprises are projected to grow at a 27.36% CAGR through 2031.

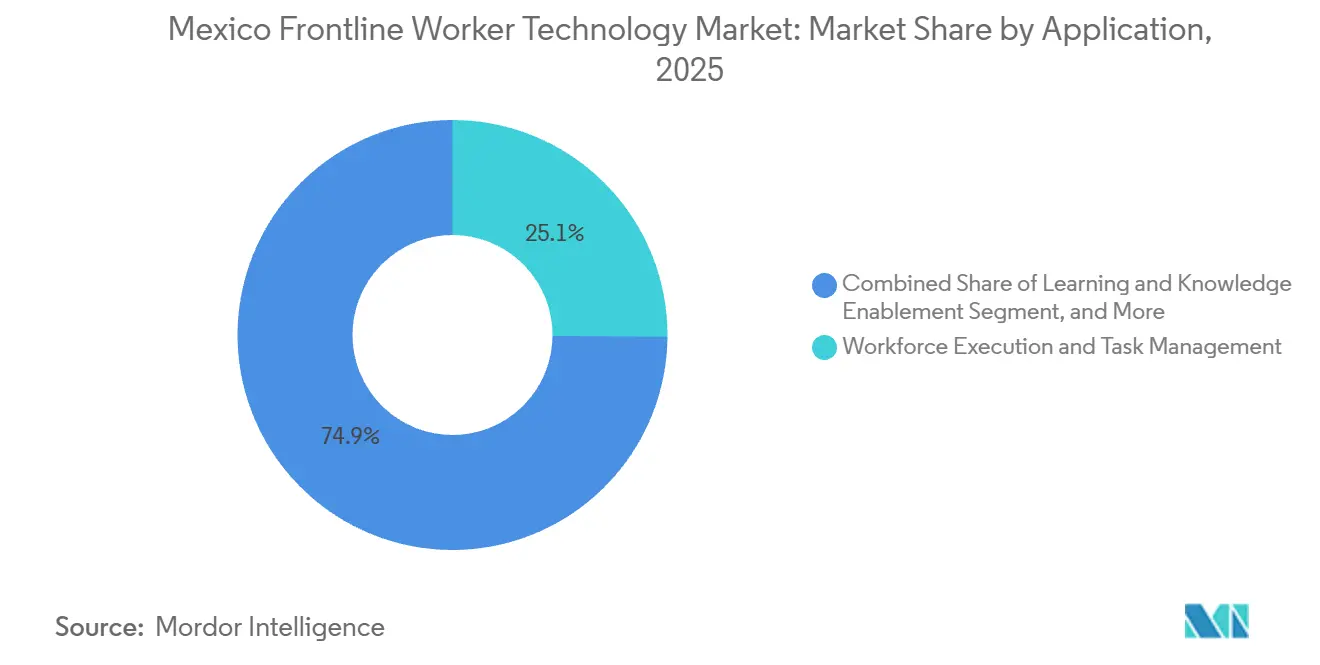

- By application, workforce execution and task management accounted for 25.14% of the market share in 2025, while safety and compliance management is projected to expand at a 29.08% CAGR through 2031.

- By end-user industry, industrial manufacturing held 29.18% share in 2025, while transportation and logistics is projected to grow at a 28.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring-Led Manufacturing Digitization | +5.8% | Bajío corridor, Monterrey, Saltillo | Medium term (2-4 years) |

| Rising Adoption of Rugged Mobile Devices and Wearables | +4.6% | Northern manufacturing zones and logistics corridors across Mexico | Short term (≤ 2 years) |

| Compliance Pressure for Real-Time Workforce Traceability and Safety Documentation | +4.2% | National, with early concentration in Nuevo León, Jalisco, and Querétaro | Short term (≤ 2 years) |

| Cloud-First Frontline Workflow Modernization Across Multi-Site Operations | +3.8% | National, concentrated in Mexico City, Guadalajara, and Monterrey | Medium term (2-4 years) |

| AI-Enabled Scheduling, Task Orchestration, and Worker Guidance | +2.9% | National, with early adoption in retail and logistics | Long term (≥ 4 years) |

| Expansion of Telecom Coverage Supporting Always-Connected Workforce Tools | +2.1% | Rural industrial corridors and secondary manufacturing cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nearshoring-Led Manufacturing Digitization in Northern Mexico

The Mexico frontline worker technology market is gaining direct support from nearshoring because new production capacity needs repeatable digital processes from the first day of ramp-up. Manufacturing investment remained concentrated in the Bajío region, Monterrey, and Guadalajara in 2026, which kept operational technology standards closely tied to the requirements of multinational parent facilities. This pattern matters because connected worker platforms are increasingly introduced alongside new quality, maintenance, and task documentation routines rather than being added much later. Domestic suppliers serving those anchor manufacturers then face pressure to align with the same execution and traceability expectations if they want to stay inside approved supply chains. Vendors that lack Spanish-language workflows, local payroll links, and regulatory alignment face a weaker position even when their global brand is well known. The operational case is strengthened further because formal workplace safety obligations apply across Mexican employers and make paper-based frontline coordination harder to sustain at larger scale.

Rising Adoption of Rugged Mobile Devices and Wearables in Field Operations

The Mexico frontline worker technology market is also benefiting from the wider use of devices that can function reliably in plants, warehouses, and field environments where consumer hardware fails quickly. Rugged hardware is becoming more important as employers move from light communication use cases toward always-on task execution, barcode workflows, image capture, and guided procedures during active shifts. Zebra reinforced this direction in March 2026 when it opened a supplies manufacturing plant in Querétaro with a USD 10 million investment and 78 jobs, which improves local support for industrial visibility and automation deployments.[1]Staff, “Zebra Opens Supplies Manufacturing Plant in Mexico, Advancing Asset Visibility and Automation Solutions in Latin America,” Zebra Technologies, zebra.com Wearable tools are also moving closer to routine enterprise use, with Vuzix launching enterprise kits in February 2026 that combined smart glasses with native Microsoft Teams and Zoom integration for hands-free remote assistance. This matters for safety-heavy settings because wearable guidance and remote support can fit better with personal protective equipment and reduce the need for informal workarounds on the factory floor. As more frontline tasks become digitally documented, durable devices increasingly support compliance as much as productivity.

Compliance Pressure for Real-Time Workforce Traceability and Safety Documentation

The Mexico frontline worker technology market is seeing a stronger pull from employers that now need real-time records of safety activity, worker presence, and corrective actions. The publication of NOM-017-STPS-2024 in March 2025 and its entry into force in September 2025 raised the practical importance of structured documentation for protective equipment selection, use, and handling. This change pushes compliance work closer to the frontline because audits depend on evidence created during normal operations rather than after-the-fact administrative reconstruction. The July 2025 biometric CURP reform added another layer by requiring employers to update onboarding, identity verification, and access procedures tied to employee records. Labor law specialists also reported stronger inspection activity in 2025, which increased the cost of weak documentation and manual recordkeeping in regulated workplaces. As a result, platforms that can log incidents, verify tasks, and produce audit-ready records are moving closer to core operational spending rather than discretionary software budgets.

Cloud-First Frontline Workflow Modernization Across Multi-Site Operations

The Mexico frontline worker technology market continues to benefit from a broader shift toward cloud-led operating models across companies that manage multiple sites and distributed worker populations. Cloud deployment fits frontline use cases well because it reduces local infrastructure burden and lets employers roll out standardized workflows faster across stores, plants, depots, and field teams. In January 2026, Microsoft highlighted new frontline capabilities inside its retail workforce tools, showing how scheduling, communication, and AI-assisted support are becoming part of broader enterprise cloud environments rather than separate point systems.[2]Staff, “Smarter Shifts Start Here: Reimagining Retail Frontline Experiences,” Microsoft Community Hub, techcommunity.microsoft.com This favors vendors that can configure usable workflows quickly and then expand into adjacent functions such as learning, compliance, or performance support without large on-site implementation teams. It also helps mid-sized employers because cloud-native tools reduce the up-front systems burden that traditionally limited advanced workforce software to larger organizations. Over time, this dynamic should support more integrated buying decisions across communication, scheduling, safety, and execution layers inside the same account base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy ERP, WMS, and Payroll Environments | -2.8% | National, concentrated in multi-site manufacturing and logistics operators | Medium term (2-4 years) |

| Data Privacy Concerns Around Location, Biometrics, and Performance Monitoring | -2.1% | National, heightened in Mexico City and industrial hub states | Short term (≤ 2 years) |

| Budget Sensitivity Among Mid-Market Employers and Multi-Site Operators | -1.5% | National, concentrated in SME-heavy sectors such as hospitality and retail | Medium term (2-4 years) |

| Device Loss, Breakage, and Lifecycle Management Cost Burden | -0.9% | Northern manufacturing zones and logistics corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy ERP, WMS, and Payroll Environments

The biggest operating challenge in the Mexico frontline worker technology market is often not the willingness to adopt, but the time and effort needed to connect new applications with older enterprise systems. This is especially visible in manufacturing and logistics groups that run global ERP platforms, local payroll systems, and older warehouse software across the same operating footprint. Solistica reported in 2025 that 74% of logistics companies had not effectively integrated their management systems, which shows how common fragmented digital environments remain. When value depends on deep bidirectional data flows, deployment timelines become longer, and implementation risk becomes harder to manage across multiple sites. Vendors that offer prebuilt connectors and clearer rollout playbooks are therefore better placed to turn pilot projects into broad contracts. ADP's October 2024 acquisition of WorkForce Software also reflects the strategic importance of tighter links between workforce management and larger HCM stacks.

Data Privacy Concerns Around Location, Biometrics, and Performance Monitoring

Data governance is another meaningful restraint in the Mexico frontline worker technology market because many frontline use cases depend on personal information that now faces tighter legal scrutiny. Mexico's new Federal Law for the Protection of Personal Data in Possession of Private Parties took effect on March 21, 2025, and requires employee consent to be free, specific, and informed. The law also gives workers a clearer basis to object to automated processing that significantly affects their rights or interests without human oversight. That creates a procurement hurdle for products built around GPS tracking, biometric authentication, or automated performance scoring, especially when vendor documentation is vague. The biometric CURP reform added pressure because it pulled identity data handling into ordinary employer workflows and forced policy updates across hiring and access processes. Vendors that can explain consent management, local data handling, and human review controls more clearly should face less friction during legal and compliance review.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leadership Remains Clear While Services Gain Importance

Software accounted for 79.24% of the Mexico frontline worker technology market size in 2025, which shows how strongly buyers favored subscription-based platforms over isolated tools and manual coordination. This lead reflects the fact that employers usually begin their digitization path with communication, task execution, scheduling, and compliance applications before they expand service spend. The software layer also benefits from standardization across multi-site accounts, because one successful deployment often creates pressure to extend the same workflow model into sister facilities. Within the Mexico frontline worker technology industry, this has helped platform vendors defend recurring revenue positions even when buyers continue to test several use cases in parallel. The Mexico frontline worker technology market, therefore, remains software-led at the value level, even though service demand is becoming harder to ignore.

Services is projected to grow at a 28.42% CAGR during 2026-2031, which places it ahead of software on a growth basis and points to a more implementation-heavy phase ahead. That pattern fits the practical reality of the Mexico frontline worker technology market, where payroll links, legacy systems, local compliance needs, and change management all create work outside the software license itself. Service providers are benefiting because many employers need help mapping workflows, integrating old systems, training supervisors, and setting audit-ready operating routines. SAP's November 2025 appearance with Walmart de México y Centroamérica at the AMEDIRH conference showed how AI-enabled talent tools and execution value depend as much on practical rollout as on application features. The same logic is visible in larger workforce software combinations, where ADP strengthened its position through the acquisition of WorkForce Software to deepen end-to-end connectivity across workforce processes.[3]Staff, “ADP Acquires WorkForce Software,” ADP Media Center, mediacenter.adp.com

By Deployment: Cloud Keeps the Lead Across Adoption and Expansion

Cloud-based deployment held 72.36% of the Mexico frontline worker technology market share in 2025, and it is projected to grow at a 26.18% CAGR through 2031. This combination is notable because the largest deployment model is also the fastest expanding one, which signals a structural preference rather than a temporary migration wave. Employers are using cloud delivery to shorten implementation cycles, reduce local infrastructure requirements, and keep updates consistent across distributed worker populations. In the Mexico frontline worker technology industry, cloud adoption also broadens the addressable market because smaller and mid-sized employers can access advanced functionality without building heavy internal IT support models. The result is a deployment environment that favors standardization and faster replication across sites.

Hybrid deployment still matters for large industrial operators that need a mix of connected administrative workflows and more controlled production environments. These buyers want frontline applications that can keep data moving where necessary without exposing sensitive operational systems to unnecessary risk. On-premises setups remain relevant for some public administration and highly controlled use cases, especially where procurement habits and internal control requirements still favor local infrastructure. At the same time, Microsoft continued to embed more frontline functionality into its broader enterprise cloud ecosystem in January 2026, which strengthens the case for integrated cloud-based workforce orchestration. That broader ecosystem effect should keep cloud deployments at the center of the Mexico frontline worker technology market as buyers consolidate communication, scheduling, and AI-assisted support.

By Organization Size: Large Enterprises Set the Pace While SMEs Close the Gap

Large enterprises accounted for 66.81% of the Mexico frontline worker technology market size in 2025, reflecting the early weight of multinational manufacturers, national retailers, and large healthcare networks. Many of these organizations already had exposure to frontline technology standards in other countries, which made local adoption easier to justify and faster to implement. Their scale also gave vendors a clear path to large contracts because one enterprise account could span many sites, thousands of workers, and several application categories. This helped the Mexico frontline worker technology market build around complex buyers first, especially in settings where governance, traceability, and process consistency matter every day. Early revenue concentration in large organizations, therefore, came from both budget capacity and organizational readiness.

Small and medium enterprises are projected to expand at a 27.36% CAGR during 2026-2031, which shows that adoption is widening beyond the largest employers. The shift reflects falling entry barriers through mobile-first products, simpler configuration, and clearer return on time savings for managers who handle multiple responsibilities. Humanforce's May 2026 launch of AI-powered Smart Scheduling illustrated this product direction by targeting roster efficiency and labor optimization for frontline employers that need faster deployment and lower manual workload. Humanforce Connect, launched in April 2026, also pointed to the same market need by bringing roster creation, internal workforce activation, and agency management into one operating environment. As pricing becomes easier to absorb and workflows become easier to configure, smaller employers should narrow the technology gap that once separated them from national and multinational accounts.

By Application: Operational Execution Holds the Base While Safety Expands Fastest

Workforce execution and task management represented 25.14% of the Mexico frontline worker technology market size in 2025, which shows that employers still begin with the core need to assign work, track completion, and reduce operational drift. These functions sit close to daily plant, warehouse, retail, and field activity, so they often become the first structured software layer for frontline teams. Once those routines are digitized, adjacent modules such as communication, learning, and analytics become easier to attach because the employer already has a working operating backbone. This helps explain why the Mexico frontline worker technology market keeps drawing investment toward platforms that can start with simple execution and then broaden into wider workforce orchestration. The base application layer remains practical, visible, and relatively easy for managers to evaluate.

Safety and compliance management is projected to grow at a 29.08% CAGR through 2031, which makes it the fastest-growing application as regulatory demands become more immediate. NOM-017-STPS-2024 raised the value of digital evidence tied to personal protective equipment processes, incident records, and corrective action tracking at the worksite level. Honeywell reinforced the commercial importance of this use case in June 2026 when it launched Safety Suite 2.0 with broader visibility, alarm history, and forecasting features for industrial safety leaders. At the same time, workforce scheduling and coordination are becoming more intelligent, with Legion releasing more than 90 AI workforce management innovations in January 2026. Learning and knowledge tools are also gaining weight because nearshoring and labor turnover create constant pressure to transfer process knowledge quickly, especially where new hires need guided support from the first shift.

By End-User Industry: Manufacturing Anchors Demand While Logistics Moves Fastest

Industrial manufacturing captured 29.18% of Mexico frontline worker technology market share in 2025, which confirms that factory environments remain the main revenue base for vendors serving connected frontline workforces. This lead came from the concentration of new production activity in automotive, electronics, and aerospace corridors where process discipline, quality documentation, and safety routines directly shape buying behavior. Manufacturing sites also provide the clearest setting for mobile work instructions, incident capture, remote support, and coordinated shift execution, so platform value is easier to prove. Within the Mexico frontline worker technology industry, industrial accounts have therefore acted as anchor customers that shape product requirements for many other sectors as well. The Mexico frontline worker technology market continues to lean on this installed base even as adoption spreads into service-heavy environments.

Transportation and logistics is projected to grow at a 28.74% CAGR through 2031, which suggests that the next wave of demand will increasingly come from movement-intensive operations. Logistics employers need stronger dispatch visibility, route-linked coordination, document handling, and exception management across large distributed workforces, which makes frontline tools highly relevant. The sector also faces persistent system fragmentation, so buyers are looking for ways to link people, tasks, and compliance records more reliably across sites and trips. Retail and e-commerce remain important for communication and scheduling demand, while healthcare and life sciences are adding momentum through tighter workforce coordination and regulated operating practices. Construction and public administration are earlier in their digitization cycle, but both are showing clearer use cases around safety documentation, workforce communication, and field execution discipline.

Geography Analysis

Northern Mexico remained the highest-density demand zone in the Mexico frontline worker technology market in 2026 because nearshoring-led production growth kept operational digitization needs concentrated in major industrial corridors. Bajío locations, Monterrey, Saltillo, and border cities such as Tijuana and Ciudad Juárez continue to attract manufacturing activity that depends on disciplined frontline execution and traceability. This concentration matters because large anchor facilities often set workflow, safety, and reporting standards that smaller suppliers then need to adopt as part of day-to-day commercial participation. Telecom readiness in the north also supports connected device usage more effectively than in less developed regions. The Instituto Federal de Telecomunicaciones reported meaningful 5G coverage gains in states such as Nuevo León and Baja California, which improve the operating environment for always-connected frontline tools.[4]Staff, “Comportamiento de los Indicadores de Mercado y la Economía Digital,” Instituto Federal de Telecomunicaciones, ift.org.mx

Central Mexico represents the most mixed demand base in the Mexico frontline worker technology market because it combines retail concentration, technology services capacity, government administration, and another layer of industrial operations. Mexico City drives adoption in communication and scheduling use cases because employers there manage large distributed labor pools across service-oriented settings. Guadalajara supports the market from a technology and electronics standpoint, which helps vendors with local commercial coverage and helps employers with access to implementation talent. Querétaro also stands out because Zebra opened a USD 10 million plant there in March 2026, strengthening the local base for industrial visibility and automation support. The region, therefore, combines enterprise demand, commercial talent, and hardware ecosystem support in a way that makes it central to vendor expansion strategies.

Southern Mexico and the Gulf states form a smaller current base in the Mexico frontline worker technology market, but they still matter because connectivity improvement can unlock new frontline software demand over time. Adoption has been slower in these areas because many employers still face narrower digital infrastructure and less standardized operating environments. Even so, energy-related deployments show that specialized use cases can emerge outside the main manufacturing belt when safety and operational control are high priorities. Honeywell's role in the AMIGO LNG export terminal project in Sonora showed how connected control and safety systems can stimulate frontline technology demand in emerging industrial nodes. As infrastructure improves, these regions are likely to start with communication and scheduling tools before moving deeper into execution, analytics, and advanced compliance workflows.

Competitive Landscape

The Mexico frontline worker technology market remains fragmented because no single vendor controls the full mix of software, hardware, and services that employers now evaluate together. Large enterprise software providers use ERP and HCM relationships to extend into frontline workflows, while specialist vendors compete through faster deployment, mobile-first design, and narrower operational focus. This structure keeps the field open because buyers often mix established platforms with focused applications during the early and middle stages of adoption. The Mexico frontline worker technology market also rewards vendors that can show measurable labor efficiency, stronger compliance records, and better worker guidance instead of broad claims about digital transformation. Competitive strength is therefore shifting toward proof of operational value rather than product breadth alone.

Consolidation is starting to reshape parts of the field, especially where communication and employee experience categories overlap with frontline execution needs. LumApps and Beekeeper merged in July 2025 to create a combined platform serving more than 7 million users across over 2,000 clients, which shows the strategic value attached to frontline communication layers. ADP's acquisition of WorkForce Software in October 2024 showed a similar move toward tighter workforce stack integration at a global scale. Microsoft added more pressure in January 2026 by bringing new frontline AI capabilities into its broader workplace environment, which raises the competitive bar for standalone software vendors. As this continues, specialists will need deeper vertical workflow relevance to protect their position.

Hardware-linked competitors are also moving upward into recurring software and service layers rather than staying limited to device sales. Zebra's Workcloud direction and Honeywell's safety software push show how industrial technology vendors are trying to own more of the workflow orchestration layer above the hardware. Augmentir's September 2025 expansion of AR-guided capabilities points in the same direction, with compliance evidence and guided work becoming a more differentiated value proposition for manufacturing settings. White-space remains strongest where execution, safety documentation, and identity-sensitive workflows come together in one mobile experience. That keeps room open for focused entrants even as larger vendors broaden their reach.

Mexico Frontline Worker Technology Industry Leaders

Microsoft Corporation

SAP SE

Oracle Corporation

Honeywell International Inc.

Zebra Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Honeywell launched Safety Suite 2.0, a software platform providing broader visibility into portable gas detection device fleets with enhanced dashboards, historical alarm data, and forecasting capabilities for safety leaders in refineries, chemical plants, and utilities. The release strengthens the company's position in safety and compliance management for industrial frontline workers, particularly relevant to Mexico's NOM-regulated energy and manufacturing sectors.

- May 2026: Humanforce launched AI-powered Smart Scheduling, an advanced AI rostering and scheduling engine that reduces roster management time by up to 70% and can lower labor costs by 15% through precise shift staffing. The product targets frontline employers managing variable demand across multiple sites, directly addressing the scheduling inefficiencies prevalent in Mexico's retail, hospitality, and logistics sectors.

- April 2026: Humanforce launched Humanforce Connect, described as the first operating system for frontline and flexible work, integrating compliant roster creation, internal workforce activation, private marketplace access, and agency vendor management in a single platform. The solution was developed through the strategic acquisitions of Emprevo and ShiftMatch and expands Humanforce's coverage of contingent and blended workforce models.

- March 2026: Zebra Technologies opened a supplies manufacturing plant in Querétaro, Mexico, with an investment of USD 10 million and the creation of 78 jobs, its first regional supply facility serving South America. The plant produces barcode labels, thermal printing ribbons, and RFID consumables under Zebra's global quality standards, improving supply availability and lead times for Mexico and South American customers in retail, logistics, and healthcare.

Mexico Frontline Worker Technology Market Report Scope

The Mexico frontline worker technology market comprises software platforms, connected applications, and associated services designed to digitally enable deskless and field-based employees across industries such as retail, industrial manufacturing, healthcare, transportation and logistics, hospitality, construction, and the public sector. These solutions improve frontline productivity, communication, task execution, workforce coordination, learning, operational visibility, safety, and compliance by integrating mobile devices, wearable technologies, artificial intelligence (AI), Internet of Things (IoT) sensors, cloud platforms, and enterprise business systems. The market includes revenue from software subscriptions and licenses, as well as professional and managed services supporting deployment, integration, customization, training, and ongoing support.

The Mexico Frontline Worker Technology Market Report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), and End-user Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the current and projected size of the Mexico frontline worker technology market?

The Mexico frontline worker technology market was valued at USD 0.40 billion in 2025, stands at USD 0.48 billion in 2026, and is projected to reach USD 1.49 billion by 2031 at a 25.44% CAGR.

What is driving growth in frontline worker technology adoption across Mexico?

Growth is being supported by nearshoring-led factory expansion, stronger workplace safety requirements, wider demand for real-time traceability, and broader use of cloud-based workforce tools.

Which deployment model leads adoption in Mexico?

Cloud-based deployment led with a 72.36% share in 2025 and is also the fastest-growing model, with a projected 26.18% CAGR through 2031.

Which application area is expanding the fastest?

Safety and compliance management is projected to grow at a 29.08% CAGR through 2031 as employers place greater weight on digital documentation, incident logging, and audit readiness.

Which end-user group contributes the most demand today?

Industrial manufacturing led with a 29.18% share in 2025 because factories remain the clearest setting for task execution, quality control, worker guidance, and compliance workflows.

What is slowing wider adoption among some employers?

Integration with legacy ERP, WMS, and payroll systems remains difficult, and newer privacy rules around biometrics, location data, and automated monitoring are extending procurement reviews.

Page last updated on: