Mexico Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

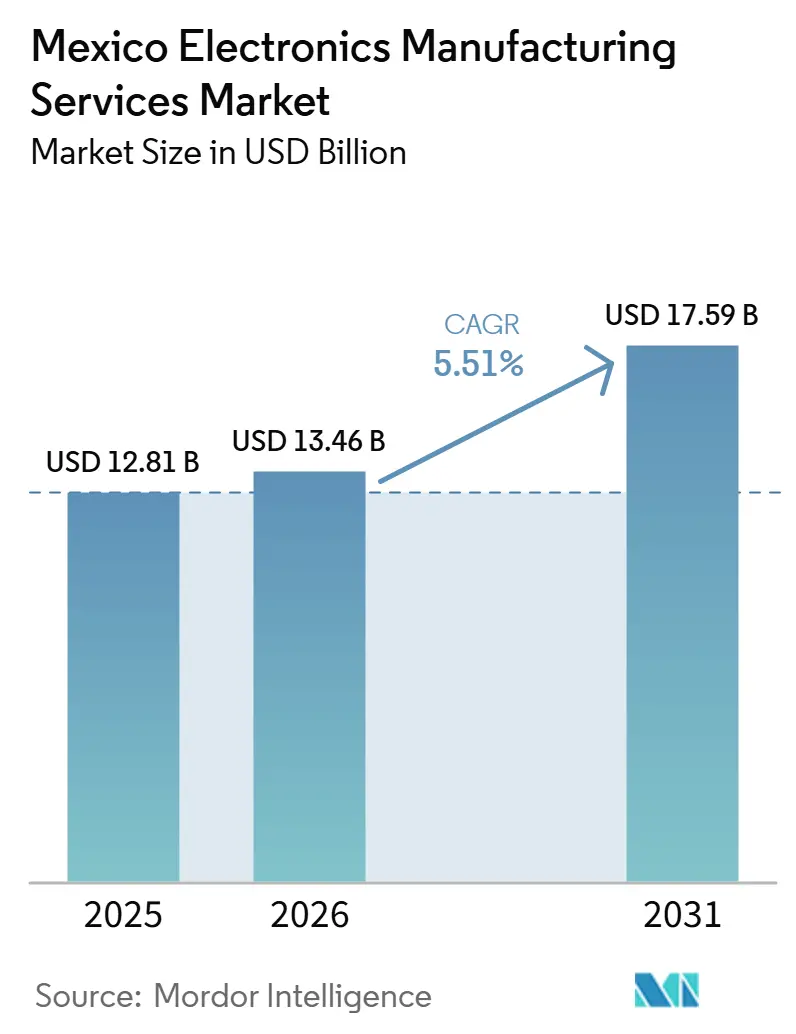

| Base Year Market Size (2025) | USD 12.81 Billion |

| Market Size (2026) | USD 13.46 Billion |

| Market Size (2031) | USD 17.59 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Mexico Electronics Manufacturing Services Market size is expected to grow from USD 12.81 billion in 2025 to USD 13.46 billion in 2026 and is forecast to reach USD 17.59 billion by 2031 at 5.51% CAGR over 2026-2031.

Nearshoring remains the primary growth engine as North American brands re-route printed circuit board assembly, advanced packaging, and box-build programs from Asia into certified Mexican campuses. Demand is being reinforced by tougher USMCA local-content thresholds, the federal semiconductor master plan, and a deepening electric-vehicle production base that already lifts electronic content per car above USD 1,000. At the same time, the Mexico electronics manufacturing services market encounters friction from skilled-labor gaps, sporadic grid interruptions, and lingering exposure to global chip shortages that temporarily idle surface-mount lines in Jalisco and Nuevo León. The net effect is a measured but steady expansion path that favors providers able to couple engineering services with cost-competitive throughput.

Key Report Takeaways

- By end-user, the automotive segment held 44.75% of Mexico electronics manufacturing services market share in 2025, while its value is forecast to grow at a 5.80% CAGR through 2031.

- By business model, contract manufacturing accounted for 62.34% share of the Mexico electronics manufacturing services market size in 2025, whereas hybrid and turnkey models are projected to post the fastest 5.74% CAGR to 2031.

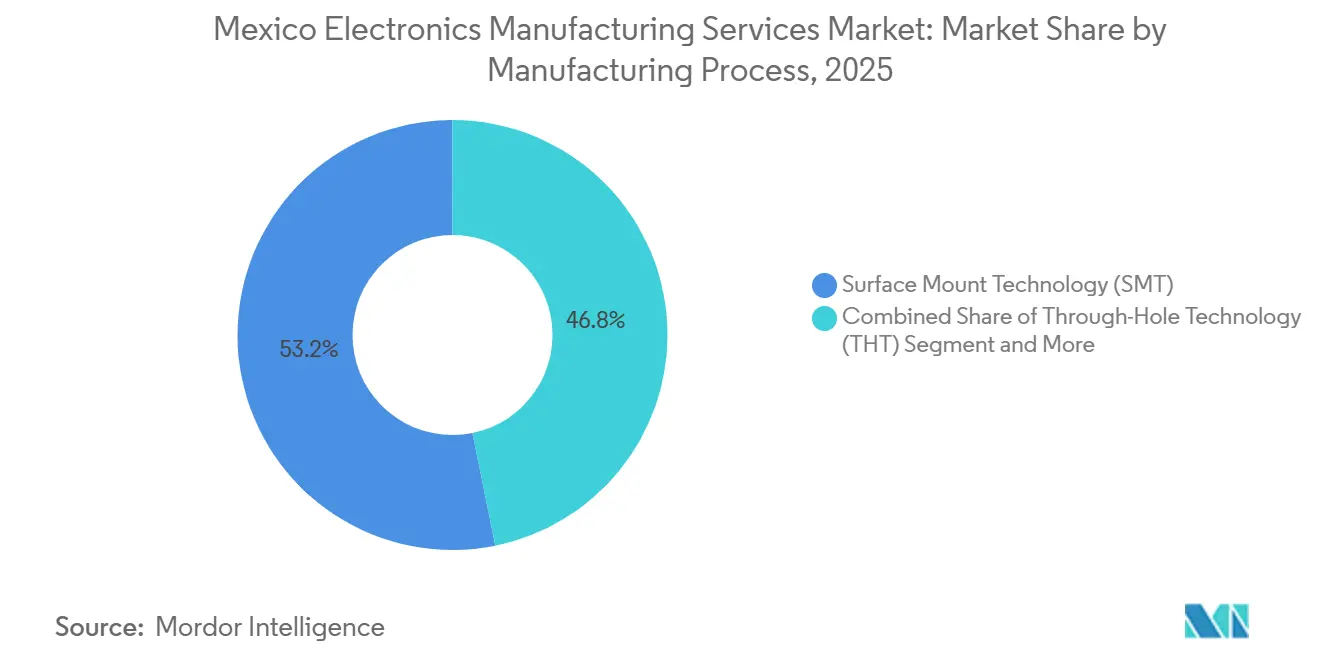

- By manufacturing process, surface-mount technology led with 53.19% share in 2025 and advanced packaging is set to expand at a 5.90% CAGR over the same horizon.

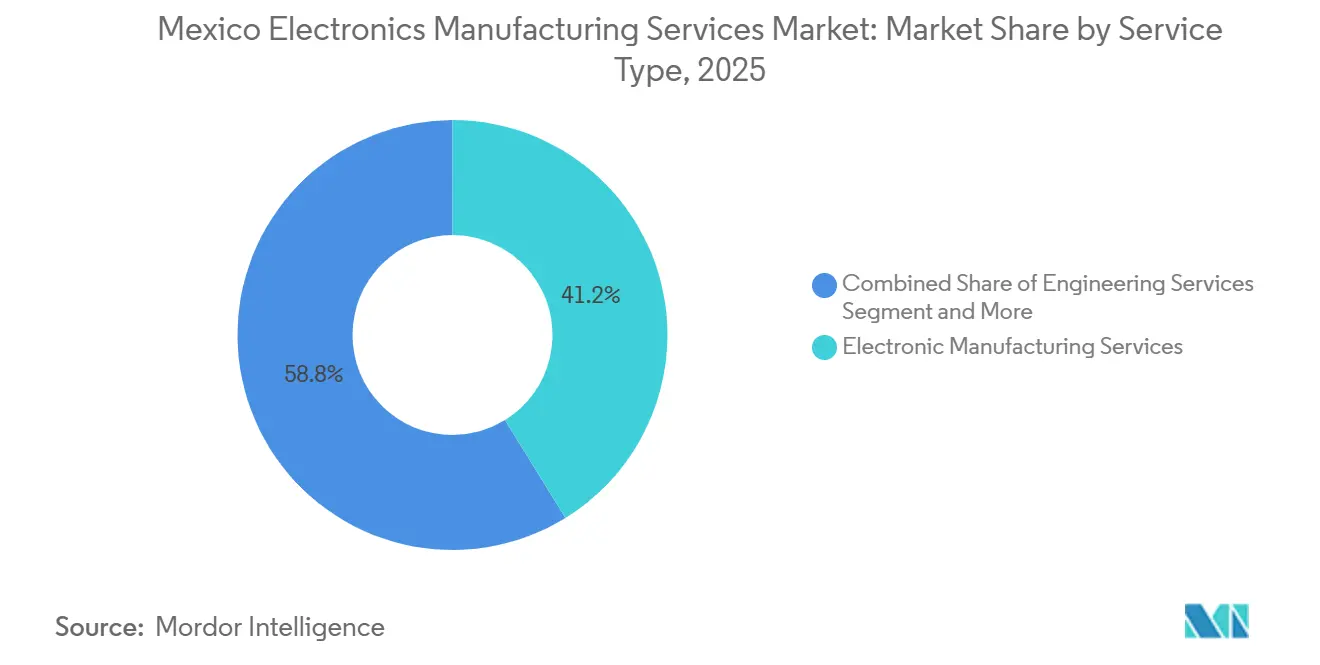

- By service type, Electronic Manufacturing Services contributed 41.20% of 2025 revenue, while Engineering Services are tracking a 6.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Dynamics observed within Mexico present a country level view when set against the broader international context. The electronics manufacturing services market analysis by Mordor Intelligence provides that expanded global perspective.

Mexico Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring trend accelerating electronics manufacturing services investments post-2025 | +1.4% | National, led by Jalisco, Nuevo León, Chihuahua, Querétaro, Baja California | Medium term (2-4 years) |

| USMCA rules of origin boosting local electronics assembly | +1.2% | National, with spillover to broader North American supply chains | Long term (≥4 years) |

| Government incentives for semiconductor packaging and electronics manufacturing services clusters | +0.9% | Jalisco, Nuevo León, Querétaro | Medium term (2-4 years) |

| Rapid growth of electric-vehicle and automotive electronics production in Mexico | +1.1% | National, early gains in Nuevo León, Guanajuato, Querétaro | Long term (≥4 years) |

| Rising demand for Internet of Things devices requiring quick-turn prototyping | +0.6% | National, concentrated in Jalisco, Baja California | Short term (≤2 years) |

| Increased adoption of advanced packaging in high-end consumer electronics | +0.8% | Jalisco, Baja California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nearshoring Trend Accelerating Electronics Manufacturing Services Investments Post-2025

Mexico secured 17 electronics nearshoring announcements during 2024 that together pledged more than USD 8 billion in capital, and commissioning accelerated after 2025 as U.S. buyers sought parts traceable to North American plants. Jalisco alone hosts over 600 electronics firms and attracted Foxconn’s USD 900 million AI-server campus plus ASE Group’s USD 200 million advanced-packaging line. Nuevo León and Chihuahua complement this network by leveraging cross-border trucking corridors that feed Texas distribution hubs. Industry estimates indicate that Mexico could lift annual electronics exports to USD 35 billion before 2030 if infrastructure keeps pace. The influx of high-mix programs explains the 1.2-percentage-point boost assigned to the forecast CAGR, peaking once most 2025-2026 builds run at full load[1]Source: Secretaría de Economía, “Plan México Infrastructure Initiative,” gob.mx.

USMCA Rules of Origin Boosting Local Electronics Assembly

USMCA lifted mandatory North American value content for automotive and select electronics to 75% and 70%, respectively, pushing OEMs to relocate printed circuit board assembly, cable harnesses, and power supplies south of the Rio Grande. Labor costs remain roughly 40% below United States plants while ISO 9001 and IATF 16949 compliance is widespread, prompting suppliers such as Bosch and Aptiv to expand Mexican footprints. Section 301 tariffs on China-sourced electronics further incentivize “Made in North America” final assembly. This regulatory tailwind adds 0.9 percentage points to long-run growth as supply chains fully reconfigure[2]Source: Office of the United States Trade Representative, “USMCA Rules of Origin,” ustr.gov.

Government Incentives for Semiconductor Packaging and Electronics Manufacturing Services Clusters

The semiconductor master plan launched in 2024 grants accelerated depreciation, import duty deferrals, and streamlined permitting under the IMMEX 4.0 scheme. Intel committed USD 3.5 billion to expand test and advanced-packaging space in Jalisco, while ASE Group’s USD 200 million Guadalajara plant delivered Mexico’s first commercial flip-chip line in 2025. Complementary state-level programs in Querétaro and Nuevo León offer subsidized land and decade-long property-tax abatements. Together with the USD 277 billion Plan México infrastructure package, these incentives have a 0.8% medium-term lift on CAGR.

Rapid Growth of Electric-Vehicle and Automotive Electronics Production in Mexico

Vehicle output hit 4 million units in 2024, and the portion carrying advanced electronics climbed to 70%. BMW, Volvo, Ford, and BYD have all slated battery-electric builds in Mexican plants, bumping electronics content per car from USD 400 pre-pandemic to about USD 1,200. Kimball Electronics alone reported USD 445.7 million in Mexico automotive revenue for fiscal 2025, evidencing demand for IATF 16949 and ISO 26262 compliant lines. Forecasts put electric-vehicle penetration in North America at 25% by 2031, underpinning a 1.0% long-term push to Mexico’s CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain vulnerability to North American semiconductor shortages | -0.6% | National, acutest in automotive and industrial programs | Short term (≤2 years) |

| Skilled labor shortage amid surging electronics manufacturing services capacity expansion | -0.7% | Jalisco, Nuevo León, Chihuahua, Querétaro | Medium term (2-4 years) |

| Energy infrastructure constraints in key industrial parks | -0.4% | Nuevo León, Jalisco | Short term (≤2 years) |

| Heightened cybersecurity compliance costs for OEMs and EMS providers | -0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerability to North American Semiconductor Shortages

Despite local packaging incentives, most microcontrollers and power devices still arrive from Asia or the United States. Shortfalls in 2024-2025 forced automakers to idle Mexican final-assembly lines for up to three weeks and pushed EMS providers to carry 90 days of buffer inventory, tying up working capital. Although incremental foundry capacity is coming online in Arizona and Texas, analysts expect a tight market for 65-nanometer and older nodes to persist through 2027, trimming near-term growth by 0.6%.

Skilled Labor Shortage Amid Surging Electronics Manufacturing Services Capacity Expansion

The electronics labor pool expanded 12% between 2023 and 2025, yet demand for IPC-A-610 and J-STD-001 certified technicians outpaced supply by roughly one-fifth. Wage bids rose 15%-25% in Jalisco, while turnover surpassed 30% in Nuevo León, delaying new line qualifications. Federal and state programs aim to train 100,000 additional technicians by 2030, but until cohorts graduate the constraint shaves 0.7 percentage points off forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Electromechanical Assembly Gains as Box-Build Complexity Rises

Engineering Services are expanding at 6.80% CAGR, the fastest pace among service lines, as OEMs outsource full subsystem integration that marries printed circuit boards, enclosures, cabling, and firmware. The shift adds engineering-service margin and helps Mexican plants capture higher-value contracts for industrial controllers and automotive infotainment modules. Electronic Manufacturing Services maintained a 41.20% slice in 2025, yet margin pressure from Asian rivals continues to steer providers toward higher-mix niches that lift average selling prices.

The trend also raises demand for design-for-manufacturability reviews, failure-mode analysis, and compliance validation, combining to deepen customer lock-in. SMTC’s Chihuahua site now runs Class 10,000 cleanrooms enabling in-house accelerated life testing, demonstrating how turnkey test capabilities strengthen revenue density. As these contracts mature, electromechanical work is poised to account for a larger share of the Mexico electronics manufacturing services market size, supported by mounting Internet of Things gateway orders.

By Business Model: Hybrid and Turnkey Models Capture Design-Intensive Projects

Contract manufacturing still represented 62.34% of 2025 revenue, yet hybrid and turnkey structures are charting a 5.74% CAGR through 2031 as brands seek single-source partners that manage everything from schematic capture to box-build fulfillment. Providers such as Benchmark Electronics co-locate design centers with high-mix production bays, shortening new-product-introduction cycles by several weeks.

Original design manufacturing remains a niche focused on regulated verticals such as medical diagnostics, where IP ownership and FDA submissions create entry barriers. Even so, rising collaboration between Foxconn, Intel, and General Motors on AI-enabled vehicle compute modules confirms that design sharing will rise. The hybrid shift is expected to raise the Mexico electronics manufacturing services market share of value-added engineering revenue at the expense of pure labor-arbitrage models.

By Manufacturing Process: Advanced Packaging Emerges for High-Density Interconnects

Surface-mount technology commanded 53.19% of 2025 volume, but demand for system-in-package modules and fan-out wafer-level builds propels advanced packaging to a 5.90% CAGR. ASE Group’s Guadalajara plant already runs Mexico’s first high-volume flip-chip line, while Foxconn uses hybrid flows that solder peripheral devices via surface-mount stations before attaching Nvidia GB200 dies with thermally efficient underfills[3]Source: ASE Group, “Guadalajara Advanced-Packaging Facility,” aseglobal.com.

Through-hole insertion persists in power equipment requiring mechanical robustness, yet its relative footprint will keep shrinking as surface-mount parts improve vibration tolerance. Taken together, advanced packaging lines are set to capture a larger fraction of the Mexico electronics manufacturing services market size as AI servers, 5G radios, and silicon-carbide vehicle inverters proliferate.

By End-User: Automotive Segment Accelerates with Electric-Vehicle Proliferation

Automotive electronics absorbed 44.75% of 2025 billings and is expected to climb at a 5.80% CAGR, reflecting traction-inverter, battery-management, and advanced driver-assistance workloads tied to the region’s swelling electric-vehicle output. Industrial automation ranks next but grows at a tempered 4.10% pace because many factories retrofit existing equipment instead of greenfield builds.

Consumer electronics and mobile devices exhibit mature trajectories near 3.20% CAGR, as cost-sensitive volume smartphones stay anchored in Asia. Communication equipment posts a healthier 4.50% CAGR on the back of 5G backhaul projects, while medical electronics in Baja California log a 4.70% expansion helped by FDA-registered sites. Collectively, automotive and communication programs will drive incremental uplift in Mexico electronics manufacturing services market size through 2031.

Geography Analysis

The national footprint of the Mexico electronics manufacturing services market is heavily centered in Jalisco, Nuevo León, Chihuahua, Querétaro, and Baja California. Jalisco alone generates roughly 30% of national output, buoyed by Foxconn’s AI-server campus and Intel’s packaging lines that cement the state as Mexico’s compute-infrastructure hub. Nuevo León follows, propelled by a USD 1 billion Hyundai Mobis complex producing advanced driver-assistance modules that feed General Motors, Kia, and Tesla vehicle plants across the state line.

Chihuahua leverages Ciudad Juárez border logistics to specialize in high-mix, low-volume runs for industrial and aerospace clients needing four-week lead times. Querétaro and Baja California round out the cluster map with strong medical-device and lighting specialization, supported by ISO 13485 and ITAR credentials, respectively. Although Asia Pacific still commands 88.10% of global electronics output, Mexico’s 4.40% CAGR within that grouping underscores its emerging role as the preferred nearshore node for North American supply chains seeking shorter transit cycles and tariff predictability.

Infrastructure quality varies by corridor. Jalisco and Nuevo León benefit from four-lane highways, dual-feed electricity substations, and multiple technical universities, while Guanajuato and San Luis Potosí remain in earlier development stages. The IMMEX 4.0 customs program is a pivotal equalizer because it allows duty-free imports of semiconductors and passives that are assembled and re-exported within 18 months, protecting gross margins even when upstream dice originate in Taiwan or South Korea.

Coverage of the electronics manufacturing services market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, Asia, and North America, alongside detailed country-level intelligence for United States, Germany, Thailand, India, Singapore, and United Kingdom, each shaped by local operating conditions.

Competitive Landscape

Five global providers, Flex, Jabil, Foxconn, Sanmina, and Celestica, are amongstsignificant contributor of Mexico electronics manufacturing services market revenue, leaving a broad mid-tier of specialists and indigenous firms to address design-intensive or quick-turn niches. Scale players emphasize automation and sustainability, with Flex achieving zero-waste-to-landfill certification at multiple campuses and deploying machine-learning inspection loops that cut rework scrap by 18% between 2023 and 2025.

Foxconn is pivoting toward compute-heavy systems, investing USD 900 million in Guadalajara to assemble Nvidia GB200 AI modules and another USD 168 million in Chihuahua for electric-vehicle power electronics. Mid-tier contenders such as Kimball Electronics and Plexus focus on medical and automotive devices where ISO and FDA badges create durable moats. Domestic firms like Circuitec and Honpe exploit bilingual engineering benches and sub-1,000-unit minimum order quantities to woo Internet of Things startups that cannot meet the 10,000-unit thresholds typical of global giants.

Technology adoption is now the principal separator. Providers that integrate digital twins, predictive-maintenance analytics, and automated optical inspection into production cells deliver tighter tolerances and shorter validation cycles, attributes increasingly demanded by automotive Tier 1 and medical clients. Membership in the Responsible Business Alliance, alongside ISO 9001, ISO 14001, IATF 16949, and ISO 13485, has evolved into table stakes for winning regulated business and defending share.

Mexico Electronics Manufacturing Services Industry Leaders

Flex Ltd.

Jabil Inc.

Hon Hai Precision Industry Co., Ltd. (Foxconn)

Sanmina Corporation

Celestica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Foxconn’s Guadalajara AI-server plant started mass production of Nvidia GB200 modules and plans to scale from 500 to 2,000 units per month by Q3 2026.

- December 2025: Lightera completed a USD 200 million expansion of its Mexicali optical-cable operation, adding capacity for 288-fiber cables and earning “Hecho en México” certification.

- November 2025: Super Lighting broke ground on a Monterrey facility slated to create 400 jobs making automotive and architectural lighting modules.

- September 2025: LG Electronics confirmed a MXN 3.5 billion (USD 205 million) investment in Querétaro to build automotive cameras, light-emitting diodes, and small electric motors, with launch set for Q2 2026.

Mexico Electronics Manufacturing Services Market Report Scope

The Mexico Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronic Manufacturing Services[PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, and Other Electronic Manufacturing Services], Engineering Services, Test and Development Implementation, and Logistics Services), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid/Turnkey), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging/Hybrid Processes), and End-User (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, and Medical). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users (Aerospace, Defense, etc.) |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-User | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users (Aerospace, Defense, etc.) |

Key Questions Answered in the Report

How large is the Mexico electronics manufacturing services market in 2026?

The market is valued at USD 13.46 billion in 2026 and is forecast to reach USD 17.59 billion by 2031.

Which end-user segment grows the fastest through 2031?

Automotive electronics leads with a projected 5.80% CAGR as electric-vehicle programs scale.

What factors make Mexico attractive for nearshoring electronics production?

Competitive labor costs, USMCA local-content rules, expanding semiconductor incentives, and proximity to U.S. customers drive relocation from Asia.

How severe is the skilled-labor gap in Mexican electronics plants?

Demand for certified technicians outstrips supply by roughly 20%, pushing wages up 15%-25% and delaying new-line qualifications.

Page last updated on: