Mexico Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

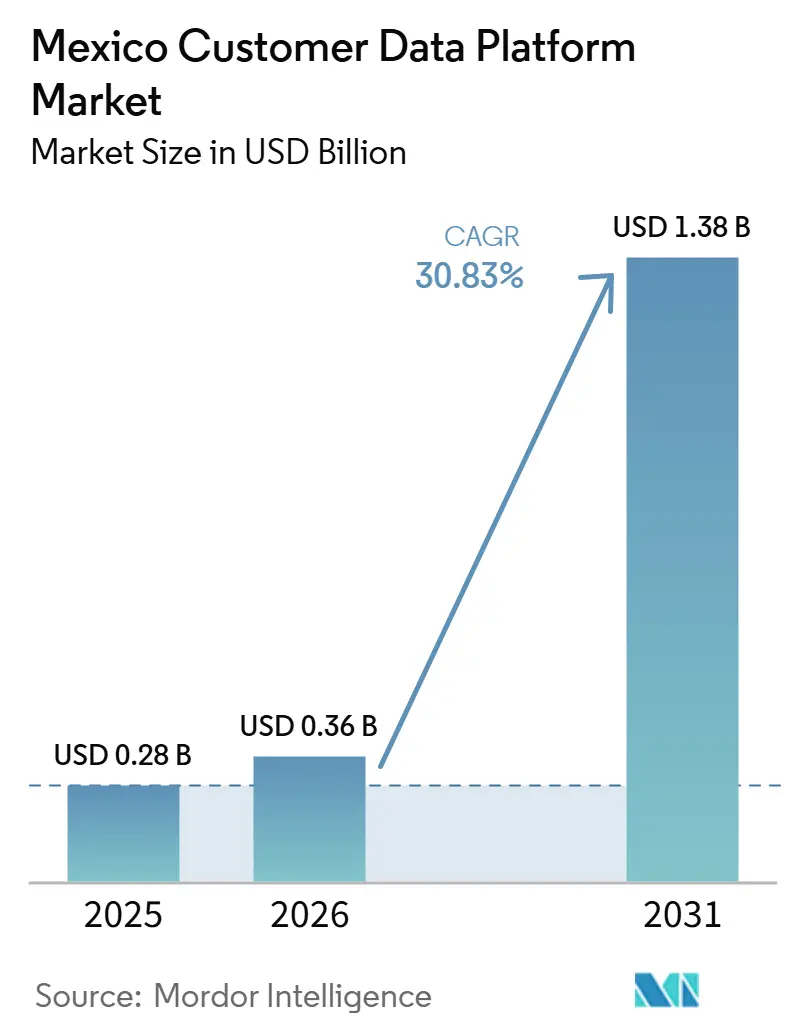

| Base Year Market Size (2025) | USD 0.28 Billion |

| Market Size (2026) | USD 0.36 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 30.83% CAGR |

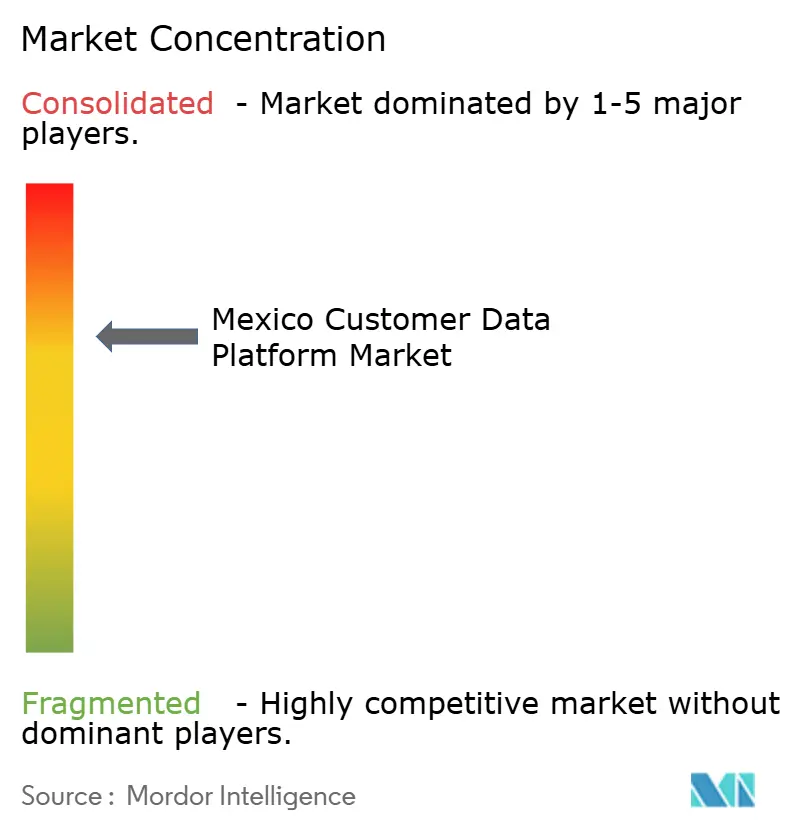

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Customer Data Platform Market Analysis by Mordor Intelligence

The Mexico customer data platform market size is projected to expand from USD 0.28 billion in 2025 and USD 0.36 billion in 2026 to USD 1.38 billion by 2031, registering a CAGR of 30.83% between 2026 and 2031. The Mexico customer data platform market is moving from early adoption toward broader enterprise adoption as brands place greater value on first-party data, stricter consent management, and more reliable customer identity management. Demand is also rising because digital commerce in Mexico continues to generate larger volumes of behavioral and transaction data, making unified customer profiles more useful across sales, service, and marketing teams. Global platform vendors remain strong in large deployments, but newer warehouse-native and composable models are expanding the addressable market by reducing integration friction for mid-sized adopters. Product direction in the Mexico customer data platform market is also shifting toward real-time activation, embedded AI, and stronger governance controls, raising the bar for vendor differentiation. This creates room for growth not only in enterprise software licensing but also in implementation, optimization, and managed services as more organizations move from pilots into daily operational use.

Key Report Takeaways

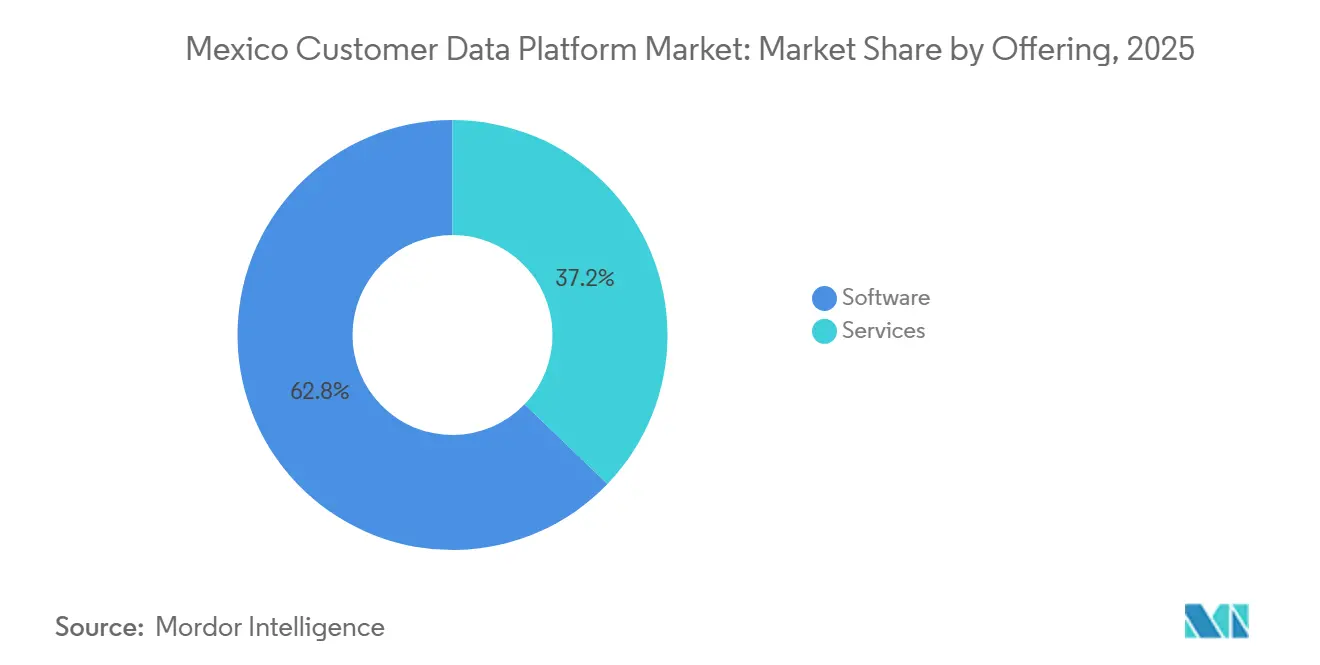

- By offering software held 62.81% of the Mexico customer data platform market in 2025, while services are projected to expand at a 33.24% CAGR through 2031.

- By deployment mode, cloud captured 70.19% share in 2025, while hybrid is expected to record the fastest growth at a 36.48% CAGR through 2031.

- By organization size, large enterprises accounted for 56.74% of the market share in 2025, while small and medium enterprises are projected to grow at a 34.81% CAGR through 2031.

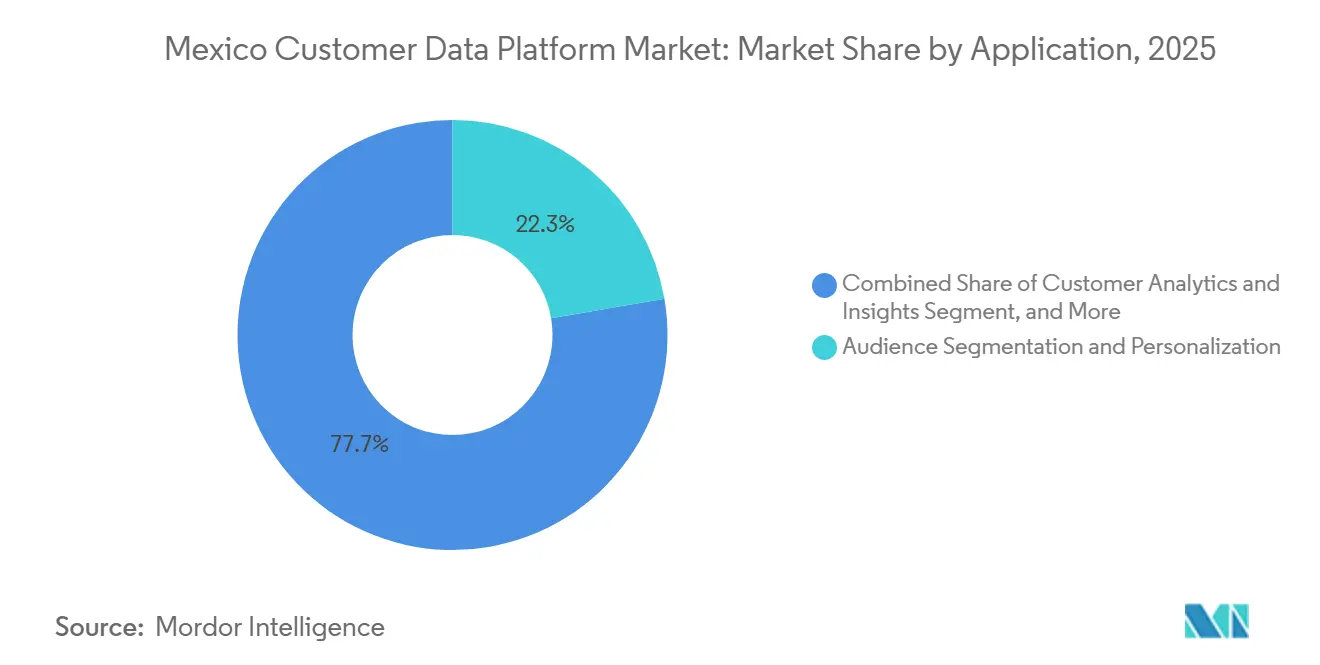

- By application, audience segmentation and personalization accounted for 22.31% of the market in 2025, while customer analytics and insights are projected to expand at a 37.62% CAGR through 2031.

- By end-user industry, retail and e-commerce held 24.83% share in 2025, while media and entertainment is expected to advance at a 35.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-Party Data Priority after Cookie Decommissioning | +5.2% | National, with concentrated adoption in Mexico City, Monterrey, and Guadalajara | Short term (≤ 2 years) |

| Real-Time Customer Profile Unification across Omnichannel Touchpoints | +4.8% | National, with spill-over to secondary cities through mobile-first commerce | Medium term (2-4 years) |

| AI-Powered Journey Orchestration and Predictive Segmentation Adoption | +4.5% | National, early concentration in BFSI and retail and e-commerce verticals | Medium term (2-4 years) |

| Warehouse-Native Activation for Lower Data Movement Costs | +3.2% | National, driven by enterprises with mature Snowflake, BigQuery, and Databricks deployments | Short term (≤ 2 years) |

| Mexico's Expanding Digital Commerce and Mobile Engagement Base | +3.8% | National, highest impact in primary metropolitan corridors and AMVO-tracked digital commerce zones | Short term (≤ 2 years) |

| Rising Demand for Privacy-First Personalization In Regulated Industries | +2.9% | National, concentrated in BFSI, healthcare and life sciences, and government and public administration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

First-Party Data Priority after Cookie Decommissioning

The Mexico customer data platform market is seeing rising demand because brands no longer treat first-party data planning as a future task. Companies in Mexico had already begun shifting budgets toward first-party data strategies before a full technical cutoff on browser cookies became universal, indicating that the buying decision was driven by operational needs rather than a single platform deadline.[1]WOM GP, “Cómo Usar Datos de Primera Parte Para Mejorar el Targeting de Anuncios,” womgp.com The 2025 revision to Mexico’s private data protection law also underscored the importance of more granular consent management, making basic retargeting approaches less comfortable for large advertisers and regulated businesses. In this setting, CDPs are being chosen because they can store, manage, and apply consent at the profile level across channels. Legacy CRM tools and campaign systems can support parts of this process, but they do not solve the same governance problem with the same depth. That combination of legal pressure and marketing change is keeping the Mexico customer data platform market on a faster path than many adjacent enterprise software categories.

Real-Time Customer Profile Unification Across Omnichannel Touchpoints

The Mexico customer data platform market is also benefiting from the growing difficulty of connecting customer activity across mobile, social, marketplace, web, and store environments. Mexico had 99 million active social media user identities in 2026, and usage patterns across short video, messaging, and app commerce continued to spread customer activity across many endpoints rather than a single owned channel.[2]DataReportal, “Digital 2026 Mexico,” datareportal.com This makes it harder for companies to distinguish new buyers from repeat buyers unless profiles are resolved in real time. The practical value of that unification is cost control: brands can reduce wasted outreach to customers who have already converted and route active customers into better retention flows. The purchasing logic has therefore shifted from a narrow focus on marketing technology to a broader focus on operating efficiency. That change matters because it shifts budget ownership higher within the organization and speeds approvals for larger accounts.

AI-Powered Journey Orchestration and Predictive Segmentation Adoption

AI capability has become one of the clearest buying filters in the Mexico customer data platform market. Mexican financial institutions showed a high level of readiness for AI deployment in 2026, and that matters because BFSI buyers often set a high standard for data architecture, governance, and measurable use cases.[3]Finastra, “Mexico Among the Leading Countries in the Application of AI to the Financial Sector,” finastra.com The interest is not limited to broad automation, as enterprises seek direct support for churn prediction, next-best action, lifetime value scoring, and adaptive journey logic. Adobe’s 2026 launch of CX Enterprise Coworker also reflected the direction of travel, with CDP, journey analytics, and orchestration moving closer together inside the same operating layer. As a result, buyers are giving less credit to vendors that treat AI as an optional add-on outside core segmentation and activation workflows. This is raising the baseline product requirement across the Mexico customer data platform market, especially in sectors where response speed and personalization quality affect revenue every day.

Mexico's Expanding Digital Commerce and Mobile Engagement Base

The Mexico customer data platform market is gaining direct support from the country’s expanding digital buyer base and wider online retail activity. Mexico ranked 8th globally in retail e-commerce penetration in 2025, and digital buying continued to deepen across everyday consumer categories, which enlarged the volume of first-party data available to merchants and brands. INEGI also reported that 104.9 million people aged 6 and above used the internet in 2025, while mobile phone usage reached 84.6% of the population in the same year. That scale creates more value in persistent customer profiles, because every additional touchpoint increases the cost of fragmented data. It also supports more use cases around loyalty, conversion recovery, and service coordination across digital and physical channels. The result is a stronger commercial base for CDP adoption in retail, payments, media, and adjacent service sectors throughout the Mexico customer data platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Effort With Legacy CRM, ERP, And Marketing Stacks | -4.2% | National, highest friction in mid-market organizations outside Mexico City's technology corridor | Medium term (2-4 years) |

| Data Privacy, Consent, And Cross-Border Governance Complexity | -2.8% | National, amplified for multinationals operating across Mexico and other jurisdictions | Medium term (2-4 years) |

| Limited CDP Talent For Implementation, Identity Resolution, And Reverse ETL | -2.1% | National, most acute in secondary cities where technology talent pools are shallower | Long term (≥ 4 years) |

| Total Cost Of Ownership Pressure For Mid-Market Buyers | -1.5% | National, concentrated in organizations with annual revenue below USD 100 million | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Effort With Legacy CRM, ERP, and Marketing Stacks

Integration effort remains the largest adoption barrier for the Mexico customer data platform market. Many enterprises still operate mixed commerce and back-office environments, which means a CDP project often has to connect store systems, ERP records, CRM data, messaging channels, and digital storefront behavior before value becomes visible.[4]Marketeros LATAM, “CRM, CDP y CEP Qué Necesita Realmente un Ecommerce Mexicano en 2026 y Qué No,” marketeroslatam.com This increases deployment time and service costs, especially when event tracking is not standardized or when identity rules require custom work. It also creates hesitation among mid-market buyers because the budget required to connect systems can feel larger than the software line item itself. Vendors with prebuilt connectors, stronger local implementation support, and cleaner onboarding pathways are therefore gaining an advantage in competitive evaluations. Until those integration demands ease further, they will continue to slow the rate at which the Mexico customer data platform market broadens beyond early enterprise adopters.

Data Privacy, Consent, and Cross-Border Governance Complexity

Governance complexity is another meaningful brake on the Mexico customer data platform market. The revised legal framework increased attention on consent changes, processor accountability, and the treatment of sensitive personal data, which means buyer teams often need legal, compliance, and IT review at the same time before major configuration choices are approved. This slows iteration because data teams cannot always modify audience logic, storage design, or transfer arrangements without wider internal checks. The issue is even more visible for multinationals that operate across several cloud regions and must align local handling rules with broader group policies. In regulated sectors, governance burden becomes part of the total cost discussion rather than a separate compliance issue. That does not stop adoption, but it shifts vendor selection toward stronger auditability, better consent controls, and cleaner data lineage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Layer Gains Ground In A Software-Led Market

Software accounted for 62.81% of the Mexico customer data platform market in 2025, reflecting an early lead in platform licensing over implementation revenue. Large organizations in retail, banking, and telecommunications were able to support this pattern because they had stronger internal data and technology teams from the start. In that setting, software adoption moved ahead first, while the local services ecosystem was still catching up to demand. The Mexico customer data platform industry therefore showed the common early-stage pattern in which product ownership is concentrated in enterprises that can absorb setup work with existing staff. That share also shows that the initial buying center remained focused on platform capability, identity architecture, and channel activation rather than on outsourced execution. It points to a market structure in which technology readiness mattered more than partner availability during the first wave of adoption.

Services are projected to grow at a 33.24% CAGR through 2031, making them the fastest-growing part of the same market structure. This reflects demand from organizations that want the benefit of CDP use cases but do not have deep in-house expertise in identity resolution, event design, and activation workflow management. The revenue mix is also being shaped by the local premium attached to implementation partners with practical knowledge of WhatsApp commerce flows, VTEX environments, CFDI-linked systems, and domestic operational requirements. Twilio’s April 2026 release of advanced Linked Audiences features in Segment showed how vendors are trying to reduce manual workload and shorten operational dependency on services over time. Even so, the near-term path still favors service growth because more Mexican adopters are entering the category from a lower internal capability base than those in the first enterprise wave.

By Deployment Mode: Hybrid Architectures Reshape The Cost And Compliance Equation

Cloud captured 70.19% of the Mexico customer data platform market in 2025, which showed how strongly SaaS delivery had already taken hold among larger buyers. Cloud also accounted for 72.19% of the Mexico customer data platform market in 2025, reflecting that many enterprise marketing stacks had already moved to hosted environments before CDP purchases accelerated. That lead was supported by easier rollout, faster access to new features, and better alignment with digital campaign tools. At the same time, on-premises setups remained relevant in sectors that were more sensitive to control, residency, and audit requirements. This created a mixed deployment environment rather than a simple replacement of one model by another. The Mexico customer data platform industry, therefore, entered 2026 with a clear cloud lead, but not with a fully cloud-only operating reality.

Hybrid is projected to expand at a 36.48% CAGR through 2031, making it the fastest-growing deployment path. This is happening because buyers want cloud-based activation and personalization, but many still prefer to keep identity graphs, consent records, and sensitive customer data within more controlled environments. SAP’s February 2026 repositioning of Emarsys into SAP Engagement Cloud, along with the launch of an enterprise edition built for centralized governance across brands and regions, closely matched that demand pattern. Hybrid adoption also makes sense for organizations that already run core ERP and operational data on long-standing SAP or Oracle estates. As compliance expectations increase, hybrid becomes less of a transitional arrangement and more of a deliberate design choice. That is why deployment competition in the Mexico customer data platform market is moving beyond basic hosting preferences toward a balance between speed, control, and accountability.

By Organization Size: SMEs Enter The Market As Composable Architectures Lower The Barrier

Large enterprises held 56.74% of the Mexico customer data platform market in 2025, and that lead came from the concentration of formal CDP programs in Mexico’s biggest corporate centers. These companies were better prepared to manage integration work, organize data ownership, and justify the investment across several departments. The Mexico customer data platform market share remained heavily weighted toward these buyers because early use cases often required stronger engineering support and clearer governance frameworks. Large accounts also had access to internal examples from retail, banking, and consumer brands, which made later expansion within the same organization easier. Their lead, therefore, reflected both budget strength and operational readiness. It also gave global vendors a stable base in the enterprise tier before the broader mid-market became more active.

Small and medium enterprises are projected to grow at a 34.81% CAGR through 2031, indicating that the next demand wave will widen the user base. Warehouse-native and composable models are important here because they reduce the need for long implementation cycles and separate infrastructure budgets. That appeal became more visible in 2026 as vendors such as Databricks and Twilio emphasized direct activation from existing data environments and more modular operating models. SMEs in Mexico still face barriers around Spanish-language technical support, localized onboarding, and integration with domestic billing or point-of-sale processes. Even so, the direction is clear, because simpler architectures are lowering the threshold for adoption. That shift matters because it broadens the commercial base of the Mexico customer data platform market beyond a narrow set of large metropolitan enterprises.

By Application: Analytics And Personalization Converge As Activation Priorities

Audience segmentation and personalization accounted for the largest share at 22.31% in 2025. This application area also accounted for 24.31% of the Mexico customer data platform market share in 2025, underscoring that immediate campaign relevance and customer-level targeting remained the most visible commercial use case. Brands continued to prioritize these functions because they directly affect conversion, repeat purchase, and promotional efficiency. The lead application still depended on the same foundation as the broader category, which meant cleaner profile unification, stronger identity logic, and faster signal handling. It was also supported by concrete retail examples, including Grupo Coppel’s 2026 digital transformation spending program and the broader push to increase digital sales contribution over time. That helps explain why application demand started from activation value rather than from back-end data management alone.

Customer analytics and insights are projected to expand at a 37.62% CAGR through 2031, making it the fastest-growing application in the Mexico customer data platform market. Buyers are increasingly seeking customer lifetime value modeling, churn scoring, and next-best-action decision support, rather than stopping at static segmentation. Adobe’s 2026 product move around CX Enterprise Coworker reflected this convergence of analytics, orchestration, and activation into a more continuous operating layer. Consent and preference management is also becoming more visible as a separate buying priority, especially where regulatory exposure is high. That widens the scope of the CDP conversation, as organizations are no longer evaluating a single isolated tool. Instead, they are deciding how analytics, personalization, governance, and execution should work together around a central customer profile.

By End-User Industry: Retail Leads, Media And Entertainment Builds From A Smaller Base

Retail and e-commerce accounted for 24.83% of the market in 2025, making it the largest end-user group in the Mexico customer data platform market. Retail and e-commerce also accounted for 26.83% of the Mexico customer data platform market size in 2025, supported by the direct value of identity unification, promotional relevance, and loyalty intelligence across online and offline channels. The segment’s lead fits the structure of Mexican commerce, where digital buying activity, app engagement, and channel overlap continue to deepen. AMVO reported that Mexico’s B2C e-commerce sector reached USD 38 billion in 2025 and that the country ranked 8th globally in retail e-commerce penetration, which reinforced the commercial logic for a stronger customer data infrastructure. Retail buyers also tend to produce faster proof points than many other sectors, which helps maintain internal support for continued CDP investment. That is why retail remains the clearest anchor vertical in the Mexico customer data platform market.

Media and entertainment is projected to grow at a 35.19% CAGR through 2031, which makes it the fastest-growing end-user industry in the forecast period. This growth rate is high because many media organizations are building first-party capability from a smaller starting base than retailers and banks. Mexico’s large online population and social platform usage create a strong operating case for audience ownership, content personalization, and better monetization of known users. Other sectors, such as healthcare and life sciences, IT and telecom, industrial manufacturing, and government and public administration, are also widening the addressable base, but their adoption paths are more uneven. Industrial manufacturing stands out as a longer-term opportunity because nearshore growth is generating more service and supply chain engagement data that can eventually support the same identity and activation logic. The result is a broader industry mix for the Mexico customer data platform market, even though retail remains the current demand center.

Geography Analysis

Mexico is the only country covered in this report, but demand within the Mexico customer data platform market remains concentrated in the country’s main metropolitan corridors. Mexico City, Monterrey, and Guadalajara continued to account for the largest share of enterprise deployments in 2025 because they host a large part of the country’s retail, banking, telecom, and digital commerce leadership base. This concentration also reflects where data engineering, implementation partners, and vendor sales teams are most visible. Salesforce strengthened that pattern in 2025 by announcing a USD 1 billion investment in Mexico over 5 years and by opening a major Mexico City office with delivery capacity tied to Data 360, Agentforce, and Einstein services. That move signaled that leading global vendors now treat Mexico as a core operating hub rather than as a small extension market. It also improved the depth of local implementation for enterprise customers who want regional support in Spanish, English, and Portuguese.

Mexico’s broader digital base continues to support growth across the Mexico customer data platform market. INEGI reported that 104.9 million people aged 6 and above used the internet in 2025, representing 86.1% of the population. The same survey showed that 84.6% of the population used a mobile phone in 2025, which reinforces the importance of mobile-led data generation for customer engagement systems. AMVO data also showed that Mexico ranked 8th globally in retail e-commerce penetration in 2025 and that B2C e-commerce value reached USD 38 billion, which supported stronger CDP demand from consumer-facing industries. These conditions matter because a larger online buyer base makes profile fragmentation more costly and makes real-time activation more valuable.

Secondary cities are becoming more relevant in the Mexico customer data platform market, even if adoption still trails that of the largest metro areas. Tijuana, Puebla, León, Querétaro, and Mérida are benefiting from wider digital commerce activity, industrial corridor growth, and stronger links to cross-border trade. Monterrey remains especially important because of its mix of industrial scale, financial services presence, and technology investment. Banorte’s 2026 partnership with Hitachi Vantara, which included a 450-terabyte data center migration and a 50% reduction in transaction response times, strengthened the infrastructure base for more advanced customer data use cases. Even so, talent availability remains less even outside the top technology corridor. That is why warehouse-native and managed delivery models may matter more in secondary markets than in Mexico City. Over time, this should help the Mexico customer data platform market diffuse more evenly across the country, but the current center of gravity still sits with the largest urban economies.

Competitive Landscape

The Mexico customer data platform market remains competitive, but the enterprise tier is still led by a relatively small set of global platforms. Adobe, Salesforce, SAP, Tealium, and Twilio continue to hold strong visibility in large-account evaluations because they combine profile management with broad activation, analytics, or ecosystem depth. Their position is reinforced by existing customer relationships in CRM, commerce, cloud infrastructure, and campaign tools, which lowers switching friction for enterprise buyers. At the same time, specialized vendors such as Bloomreach and Amperity remain relevant for buyers who want greater flexibility, a narrower use-case focus, or faster innovation in AI-linked workflows. The Mexico customer data platform market is therefore not defined by a single winner, but by a contest between broader suites and more modular operating models. That balance is keeping competition active even as global vendors remain the default shortlist for the largest enterprises.

Strategic moves in 2025 and 2026 show how vendors are trying to strengthen their position inside the Mexico customer data platform market. Salesforce expanded its local commitment through a large capital investment and a Mexico City delivery center, which improved its ability to support implementation and ongoing services at scale. SAP repositioned Emarsys as SAP Engagement Cloud and launched an enterprise edition that better aligned with large organizations that need centralized governance across brands and regions. Databricks entered the category more directly with CustomerLake in June 2026, signaling that warehouse-native design is moving from challenger logic to mainstream product direction. Twilio also kept pushing Segment toward a more unified context and activation role through product updates that reduced manual workload and improved audience handling.

Another visible competitive shift is the move from simple data aggregation toward AI-ready operating layers. Adobe’s 2026 launch tied CDP, analytics, and journey execution more closely together, supporting the idea that customer data systems should now help automate action rather than merely organize information. Tealium’s AI Partner Ecosystem and its follow-up feature launches followed a similar path, positioning the platform as a live context layer for enterprise AI systems. Bloomreach and Databricks also deepened their partnership around real-time personalization from a unified data source, demonstrating how ecosystem alliances are becoming part of the competitive model. These moves suggest that differentiation in the Mexico customer data platform market is shifting toward execution speed, deeper governance, and greater AI accessibility. That makes the field concentrated at the top end, but still open enough for newer architectures to win share where deployment simplicity and data control matter most.

Mexico Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Twilio Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Databricks announced CustomerLake on June 16, 2026, at its Data and AI Summit, an agentic CDP natively embedded in the Databricks Lakehouse that consolidates identity resolution, audience building, campaign automation, and activation under Unity Catalog governance. The platform entered private preview with general availability targeted for later in 2026, with Bloomreach joining as a launch partner for real-time personalization execution across email and web channels.

- June 2026: Twilio unveiled a unified developer console at its Signal conference, integrating Segment CDP, SendGrid, and its communications platform into a single entry point. The move repositioned Segment as a modular context layer for agentic customer engagement, with Twilio framing the offering as infrastructure for enterprises building AI-driven customer experience at scale.

- May 2026: Tealium unveiled AI at the Edge, AI Decisioning, and bidirectional connectors for OpenAI and Amazon Bedrock on May 7, 2026. The release enables enterprises to route live customer data to foundation models and return structured intelligence for immediate activation, building on its AI Partner Ecosystem of over 1,300 turnkey integrations announced in April 2026.

- May 2026: Amperity launched AI assistants and real-time customer context capabilities at Amplify 2026 on May 6, 2026, introducing its Model Context Protocol Server to connect real-time customer profiles to third-party AI tools including Microsoft Copilot and Braze AI, enabling event-driven activation in the moment of customer behavior rather than through pre-set campaign schedules.

Mexico Customer Data Platform Market Report Scope

The Mexico customer data platform (CDP) market refers to the ecosystem of software and associated services that enable organizations to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of both large enterprises and SMEs across sectors such as retail, BFSI, healthcare, and IT. By integrating strict consent and preference management capabilities, CDPs help Mexican businesses comply with local data protection regulations while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The Mexico Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and outlook for customer data platforms in Mexico?

The Mexico customer data platform market was valued at USD 0.28 billion in 2025, stands at USD 0.36 billion in 2026, and is forecast to reach USD 1.38 billion by 2031 at a 30.83% CAGR.

Which deployment model is growing the fastest in Mexico?

Hybrid is the fastest-growing deployment mode, with a projected 36.48% CAGR through 2031, as buyers balance cloud activation with stronger control over sensitive data and consent records.

Which application area is expanding the quickest?

Customer analytics and insights is projected to grow at a 37.62% CAGR through 2031, reflecting rising demand for churn prediction, next-best action, and customer value modeling.

Which end-user sector currently leads adoption?

Retail and e-commerce led with a 24.83% share in 2025 because the business case for unified identity, personalized promotions, and loyalty intelligence is strongest in high-volume consumer transactions.

Why are large enterprises still ahead of SMEs?

Large enterprises held 56.74% share in 2025 because they had stronger internal engineering capacity, broader budgets, and more experience managing integration complexity across CRM, ERP, and digital channels.

What is the biggest obstacle slowing wider rollout?

Integration complexity remains the main barrier because many Mexican organizations still operate fragmented commerce, messaging, and back-office systems that require extensive connection work before a CDP can deliver full value.

Page last updated on: