Mexico Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

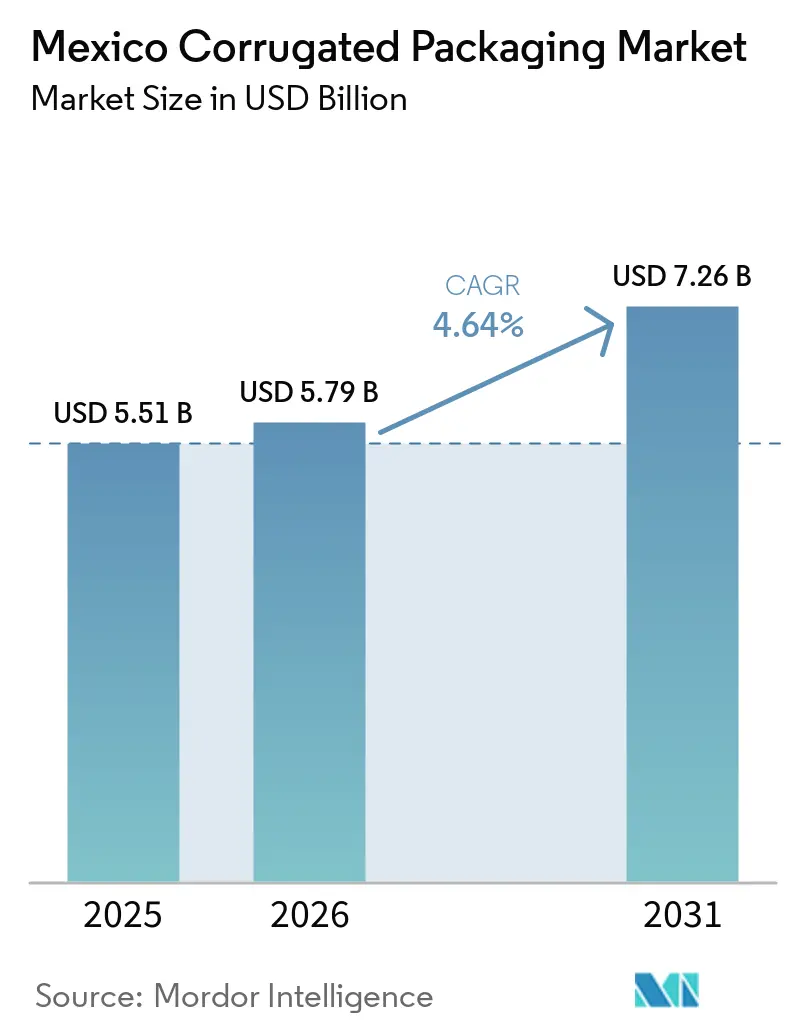

| Base Year Market Size (2025) | USD 5.51 Billion |

| Market Size (2026) | USD 5.79 Billion |

| Market Size (2031) | USD 7.26 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Corrugated Packaging Market Analysis by Mordor Intelligence

The Mexico corrugated packaging market size is projected to expand from USD 5.51 billion in 2025 and USD 5.79 billion in 2026 to USD 7.26 billion by 2031, registering a CAGR of 4.64% between 2026 and 2031. Nearshoring has realigned demand toward higher-performance boxes as multinationals move production closer to the United States, and foreign direct investment reached USD 40.9 billion in 2025. Export-oriented manufacturers concentrate in Nuevo León, Querétaro, and Baja California, where logistics parks operate at almost full capacity. Strong buying by electronics and automotive producers favors virgin kraft linerboard, while e-commerce growth increases consumption of right-sized die-cut formats. Water scarcity and imported fiber costs remain structural challenges that push mills to invest in closed-loop systems and recycled-fiber networks.

Key Report Takeaways

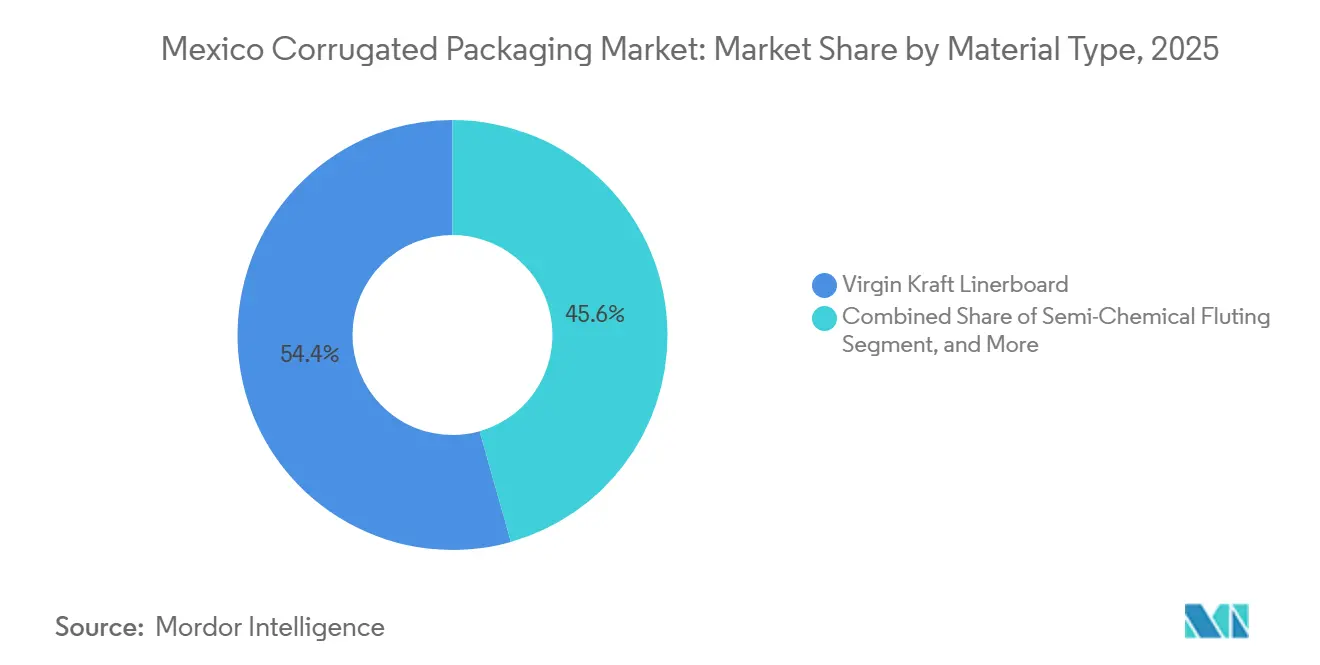

- By material type, the virgin kraft linerboard segment captured 54.38% of the Mexico corrugated packaging market share in 2025.

- By flute type, the Mexico corrugated packaging market size for e flute is projected to grow at an 5.83% CAGR through 2031.

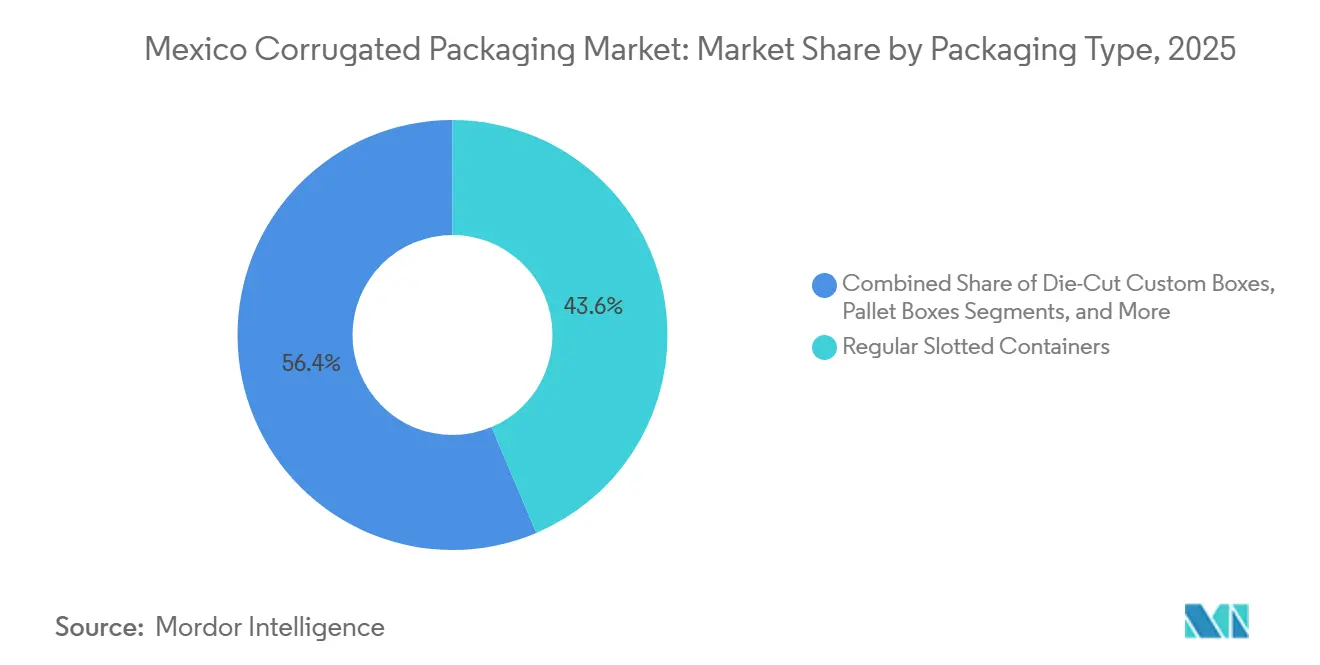

- By packaging type, the regular slotted containers segment captured 43.62% of the Mexico corrugated packaging market share in 2025.

- By wall type, the Mexico corrugated packaging market size for triple-wall is projected to grow at an 6.63% CAGR through 2031.

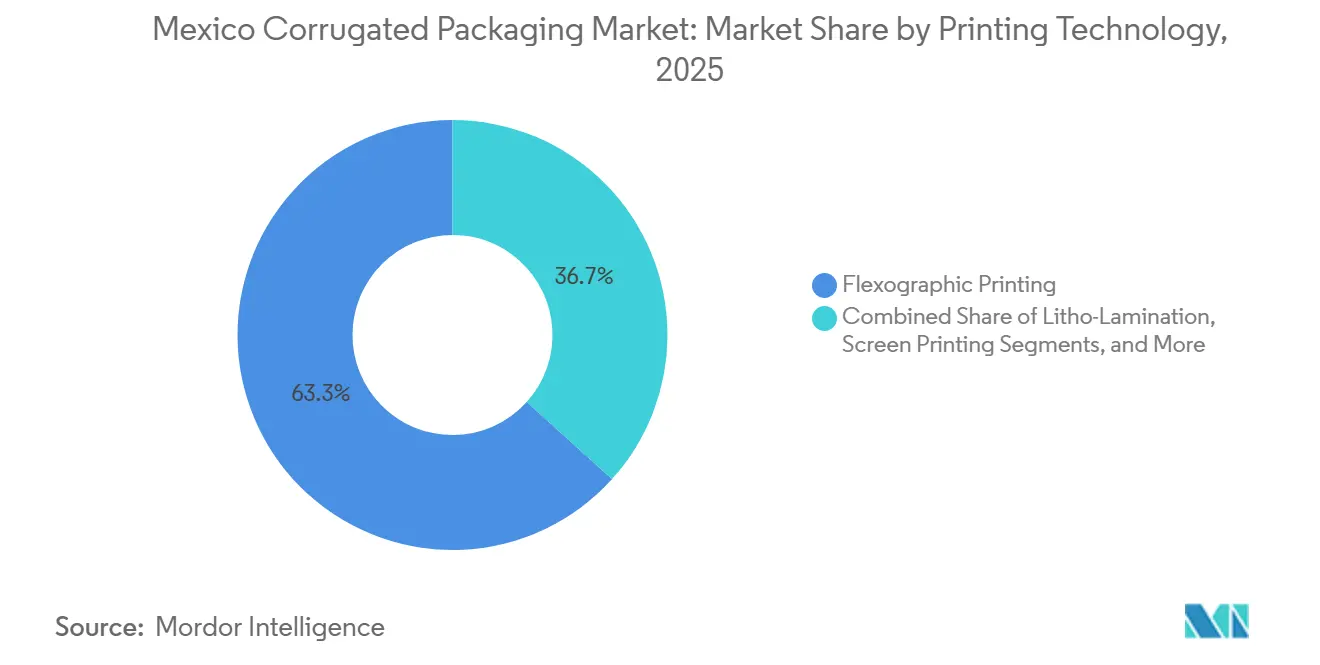

- By printing technology, the flexographic printing segment captured 63.31% of the Mexico corrugated packaging market share in 2025.

- By end-user industry, the Mexico corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Logistics Acceleration | +1.2% | National, concentrated in Estado de México, Nuevo León, Jalisco | Medium term (2-4 years) |

| Growth in Processed Food and Beverage Exports | +1.0% | National, with export corridors in Sonora, Sinaloa, and Michoacán | Long term (≥ 4 years) |

| Regulatory Shift Toward Recyclable Packaging | +0.8% | National, early enforcement in Mexico City, Estado de México | Medium term (2-4 years) |

| Nearshoring-Led Electronics Output | +1.1% | Baja California, Chihuahua, Jalisco, Querétaro | Short term (≤ 2 years) |

| Craft-Brewery Demand for Custom Boxes | +0.3% | National, concentrated in Jalisco, Baja California, and Mexico City | Medium term (2-4 years) |

| Growth in Cold-Chain Exports Requiring Moisture-Resistant Corrugated Formats | +0.5% | Sonora, Sinaloa, Michoacán, Jalisco (avocado, berry belts) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Logistics Acceleration

Mexico’s online retail penetration reached 15% of total sales in 2025, and parcel-based fulfillment drives higher box consumption per transaction. Mercado Libre opened the 80,000 m² XEM3 cross-dock capable of handling up to one million parcels per day, while Amazon added a 35,860 m² center in Apodaca. Both operators specify light single-wall or E flute cases that meet automated sortation tolerances and lower dimensional-weight charges. The shift from palletized bulk to unit-level fulfillment therefore increases demand for digitally printed, right-sized packaging.

Nearshoring-Led Electronics Output

Electronics manufacturers relocating from Asia cite two-to-five-day truck transit and zero-tariff USMCA access. Samsung’s USD 7 billion appliance expansion in Tijuana and Foxconn’s new Chihuahua line require electrostatic-discharge-safe corrugated, custom inserts, and vendor-managed inventory programs. Just-in-time delivery favors converters located within border industrial parks that can supply virgin kraft grades that meet IATF 16949 audit criteria.

Growth in Processed Food and Beverage Exports

Mexico supplied roughly half of the United States fresh produce imports in 2025, and agri-food processors continue to scale export-oriented facilities across Sonora’s tomato belt and Michoacán’s avocado orchards. Grupo Bimbo, Sigma Alimentos, and Gruma operate highly automated baking and tortilla plants, and their secondary packaging must comply with United States Food and Drug Administration indirect-food-contact guidelines. Cold-chain exporters specify wax-coated or polymer-laminated double-wall boxes that maintain torque resistance after 48 hours in refrigerated trailers, which has spurred demand for moisture-resistant fluting combinations.

Regulatory Shift Toward Recyclable Packaging

The General Law on Circular Economy, effective January 2026, introduces Extended Producer Responsibility, pushing brands toward easily recyclable substrates.[1]Hogan Lovells, “Mexico Enacts Circular Economy Law,” lexology.com Mexico City’s household separation ordinance aims to increase cardboard recovery to 75%, and ECOCE has opened new collection centers to bolster fiber feedstock. Corrugated already enjoys a 60%-plus recycling rate, positioning it as a compliance-ready solution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.6% | National, acute in import-dependent regions | Short term (≤ 2 years) |

| Competition from Returnable Plastic Crates | -0.4% | National, concentrated in the fresh produce and beverage sectors | Medium term (2-4 years) |

| Water-Scarcity Constraints on Mills | -0.3% | Valley of Mexican Basin, Nuevo León, Querétaro | Long term (≥ 4 years) |

| Dependence on Imported Virgin Fiber | -0.5% | National, particularly affecting virgin-grade producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

Old corrugated container prices, after an 18% year-over-year drop in early 2024, swung upward once the peso depreciated and freight costs stabilized. Integrated mills with in-house collection can buffer these shocks, yet hundreds of small converters must purchase spot OCC, exposing them to weekly price movements that compress already narrow margins. Contracts with supermarket produce packers often lock in box prices for entire harvest seasons, so sudden raw-material inflation can wipe out profits and delay capital spending on new equipment. Lenders now scrutinize working-capital adequacy for packaging SMEs, occasionally demanding hedging policies or fiber-supply agreements before approving credit lines. Until price transparency and domestic recovery volumes improve, volatility will persist as a notable drag on growth.

Dependence on Imported Virgin Fibre

Mexico imported USD 1.18 billion worth of pulp in 2024, mainly from the United States and Brazil, so exchange-rate shifts raise input costs for virgin linerboard grades. Currency risk is acute for exporters that require high-burst-strength boxes yet invoice in pesos, forcing hedging strategies and periodic pass-throughs to customers. Strategic inventories of high-burst kraft are costly because storage humidity risks liner-cracking defects, forcing many plants to operate on lean stocks and to import frequently, thereby amplifying currency risk. Some mills are exploring eucalyptus plantation investments in southern states, yet climatic, permitting, and transportation hurdles make local virgin-fiber projects unlikely before 2030. Consequently, import dependence remains a medium-term constraint that restricts margin expansion for virgin-grade producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Virgin Kraft Dominance Reflects Export Orientation

Virgin Kraft linerboard accounted for 54.38% of Mexico corrugated packaging market share in 2025, and is projected to grow at 6.62% through 2031. The premium grade supports cross-border shipping of appliances, electronics, and automotive parts that demand high burst strength. Import tariffs on Chinese linerboard in 2024 failed to completely dislodge lower-priced imports, yet they helped domestic producers defend their price points. Recycled linerboard remains cost-effective for local fast-moving consumer goods, but its uptake slows when peso weakness inflates OCC import bills. Smurfit WestRock plc and Bio Pappel use closed-loop fiber systems that reduce virgin fiber demand while maintaining consistent quality.

The Mexican corrugated packaging market continues to favor virgin fiber in export corridors, as OEMs adopt the IATF 16949 and ISO 13485 standards. Grupo Gondi’s Querétaro mill and Cartones Ponderosa’s San Juan plant offer semi-chemical fluting that bolsters compression strength for triple-wall boxes. Dependence on imported pulp still challenges cost predictability, although peso appreciation in 2025 temporarily trimmed landed costs for United States pulp shipments.

By Flute Type: E Flute Gains on Print Quality and Lightweighting

B flute maintained 41.92% share in 2025 due to its versatility across retail, industrial, and produce applications. E flute grows at 5.83% because craft breweries, cosmetics brands, and e-commerce sellers seek thinner calipers that improve graphics and reduce material weight. The upcoming USD 65 million Smurfit Westrock plant in Sonora will add micro-flute and high-graphic capacity to serve these markets. C flute serves fragile products such as glassware, while F flute offers ultra-thin substrates for luxury inserts. Digital print platforms like HP PageWide and Koenig and Bauer Durst enable economical short runs, and E flute’s smooth surface yields high 1200 dpi fidelity.

Converters within Bajío industrial parks deploy hybrid digital-flexo lines, enabling quick shift between mass-produced B-flute shipper cartons and premium micro-flute promotional wraps during the same shift. As e-commerce penetration deepens, parcel shippers increasingly request E flute inserts that reduce total pack weight, thereby lowering dimensional-weight charges assessed by integrated carriers. Consequently, flute-type selection now intertwines graphics requirements, freight optimization, and speed-to-market, locking E-flute onto a structurally positive trajectory within the Mexico corrugated packaging market.

By Packaging Type: Die-Cut Custom Boxes Serve E-commerce and Branding

Regular slotted containers accounted for 43.62% of 2025 volumes because they fit automated case erectors and pallet patterns. Die-cut custom boxes, growing at 6.03%, enable right-sizing, reducing dimensional-weight fees, and enhancing unboxing experiences in online retail. Folding cartons and point-of-purchase displays gain share in cosmetics and premium foods, where litho-laminated graphics drive shelf impact. Triple-wall pallet boxes ship resin pellets and automotive assemblies, combining four liners and three mediums for loads up to 5,000 lb.

Rightsizing also reduces void-fill plastics, supporting corporate sustainability scorecards aligned with Mexico’s circular-economy mandates, thereby positioning custom die-cuts as both cost-savers and compliance enablers. Retail display manufacturers increasingly integrate corrugated components with molded fiber trays, creating hybrid structures that lower total pack weight while maintaining rigidity during aisle replenishment. Overall, packaging type selection now reflects an interplay among logistics efficiency, regulatory expectations, and consumer experience, sustaining healthy growth for value-added formats in the Mexican corrugated packaging market.

By Wall Type: Triple-Wall Expands with Heavy-Duty Demand

Single-wall formats accounted for 59.48% of 2025 tonnage, thanks to lower unit costs in retail and e-commerce. Triple-wall grows 6.63% through 2031 as automotive, aerospace, and heavy machinery shippers require high compression ratings and testing per ASTM D5168. PRONAL’s new Monterrey site houses one of only two Mexican machines capable of triple-wall production and targets an annual output of 215 million m². Double-wall supports appliance and bulk-food cargo where stacking heights exceed single-wall allowances. The Mexico corrugated packaging market for triple-wall is small but is accelerating in parallel with nearshore auto-part exports that require box strengths up to 5,000 lb.

Converters therefore invest in automatic starch kitchens capable of higher-solids adhesive, enabling faster bonding of multi-wall assemblies without delamination under desert-corridor heat cycles. Supply-chain planners appreciate that triple-wall boxes can replace wooden crates, reducing phytosanitary inspection delays at border crossings while cutting tare weight up to 40%. Consequently, wall-type migration reflects combined imperatives for regulatory compliance, transport economy, and sustainability within the broader Mexican corrugated packaging market.

By Printing Technology: Digital Gains on Short Runs and Customization

Flexographic presses still account for 63.31% of 2025 output, running at up to 400 m/min with low unit costs for long jobs. Digital printers post a 6.24% CAGR as brands pursue SKU-level artwork, track-and-trace codes, and seasonal promotions. Smurfit WestRock plc installed a single-pass Barberan Jetmaster that prints six colors on 1.9-m-wide webs, offering 12 million m² of annual capacity.[2]Smurfit WestRock plc, “Sustainable Development Report 2023,” smurfitkappa.comLitho-lamination remains the choice for cosmetics and electronics gift packs requiring photographic presentation. Screen printing covers specialty metallic or tactile finishes.

Brands exploit that agility to run localized promotions for Día de los Muertos or regional soccer championships, injecting cultural relevance while avoiding obsolete inventory. As extended producer responsibility rules tighten, water-based digital inks provide a compliance hedge against photo-initiator migration concerns in UV-curable systems. Consequently, technology choice increasingly converges around run length economics, regulatory optics, and marketing agility, driving durable growth for digital within the Mexican corrugated packaging market.

By End-User Industry: E-commerce Fulfillment Leads Growth

Processed foods generated 27.39% of 2025 revenue, anchored by Grupo Bimbo and Sigma Alimentos plants that consume large volumes of secondary cartons. E-commerce fulfillment centers rise at a 5.93% CAGR, driven by Mercado Libre’s nationwide logistics expansion, including an air hub in Querétaro. Fresh-produce exporters in Sonora and Michoacán adopt moisture-resistant boxes, while craft breweries favor E flute for shelf-ready branding. Electrical and electronic goods adopt ESD-safe liners that comply with IPC-TM-650 testing, and pharmaceuticals require ISO 13485 traceability.

Pharmaceutical contract packers in the Estado de México require tamper-evident carton features and two-dimensional codes supporting serialization under the NOM-T-CIFRA guidelines issued in 2026. Automotive suppliers insist on triple-wall bins fitted with custom die-cut foam inserts that secure transmission housings and battery modules during high-vibration Laredo corridor hauls. Cross-segment interplay means that a single converter might ship lightweight E flute mailers to an e-commerce warehouse in the morning, then load heavy-duty triple-wall Gaylords for an automotive export run that same afternoon, underscoring the operational versatility demanded by the Mexico corrugated packaging market.

Geography Analysis

Nuevo León, Estado de México, and Jalisco host more than 45% of converting plants, reflecting proximity to export corridors and consumer markets. Monterrey anchors automotive and aerospace packaging, while Smurfit Westrock is spending USD 19.3 million to boost capacity in Saltillo to serve appliance makers.[3]Daily Journal Business Desk, “Smurfit Westrock investing 19.3M in Saltillo expansion,” djournal.com Baja California’s Tijuana cluster produces consumer electronics and medical devices that demand high-cleanliness corrugated. Sonora and Sinaloa dominate the fresh-produce corridors to United States grocers, so local box plants use moisture-barrier coatings and quick-vent die patterns to maintain fruit respiration rates during refrigerated trucking.

Chihuahua’s Ciudad Juárez corridor supports automotive harness and PCB assembly, drawing box suppliers that offer vendor-managed inventory. The Bajío region of Querétaro, Guanajuato, and San Luis Potosí offers diversified manufacturing with lower labor costs, helping sustain orders for bulk pallet boxes. Estado de México benefits from rail, highway, and airport linkages that feed Mexico City’s vast consumer base and e-commerce nodes. Estado de México leverages highway and rail links that converge on Mexico City’s 22-million-resident consumer basin, and recent logistics investments such as Mercado Libre’s XEM3 are catalyzing local demand for parcel-grade cartons.

Water scarcity complicates mill operations in the Mexican Valley, where the renewable supply is only 89.8 m³ per capita per year. Mills invests in closed-loop systems that cut water use sixteen-fold to comply with local regulations. Bio Pappel’s Nuevo León kraft plant tracks water footprints under the Water Action Hub to mitigate Rio Grande basin stress. Regional public-policy incentives, such as reduced water tariffs for certified reuse technologies, further shape geographic production choices and could reorient future capacity additions toward less-stressed northern border states.

Competitive Landscape

The July 2024 merger of Smurfit Kappa and WestRock created the country’s largest player with 25.7% containerboard capacity, prompting rivals to expand. Bio Pappel plans to build three new corrugated plants and to integrate 300,000 tons per year to protect its market position. International Paper’s 2025 divestiture of its Xalapa assets to APSA opened the door for regional independents to capture formerly captive business, especially among mid-sized fruit packers seeking flexible order quantities. Collectively, these moves illustrate a market transitioning from an oligopolistic containerboard supply toward a more contestable converting arena.

Cartones Ponderosa deepened its vertical integration by acquiring Cartolito for over USD 100 million in March 2026, adding high-graphic converting in the Monterrey corridor. International Paper exited Xalapa and Apodaca recycling sites in 2025, freeing space for regional converters such as APSA.[4]El Sol de México Finance Desk, “Cartones Ponderosa acquires Cartolito,” elsoldemexico.com.mx Competitive intensity also surfaces in sustainability claims, where Bio Pappel touts carbon-negative credentials based on avoided deforestation, and Smurfit Westrock publishes life-cycle assessments demonstrating model compliance with forthcoming European CBAM reporting for exports.

Technology upgrades digital printers, automated corrugators, and integrated ERP systems differentiate leading firms that can deliver 48-hour lead times. Emerging mid-tier converters partner with shelter operators to capture nearshoring start-up projects, offering rapid tooling and on-site packaging engineers. Long-term, capital intensity and fiber supply barriers suggest gradual consolidation, yet small regional players thrive on proximity and service agility.

Mexico Corrugated Packaging Industry Leaders

Smurfit WestRock plc

Bio Pappel, S.A.B. de C.V.

Envases Universales de México S.A. de C.V.

Cascades Inc.

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Mercado Libre opened the 80,000 m² XEM3 cross-dock in Estado de México, initially capable of handling 550,000 packages per day, with automation upgrades planned to reach 1 million later in 2026.

- February 2026: Smurfit Westrock issued medium-term targets that include USD 7 billion adjusted EBITDA by 2030 and a 7% EBITDA CAGR from 2026 to 2030.

- March 2026: Cartones Ponderosa completed the acquisition of Cartolito for more than USD 100 million after antitrust clearance on February 2026.

- January 2026: PRONAL inaugurated its first corrugated packaging plant in Monterrey with a capacity to convert 100,000 tons of paper annually.

Mexico Corrugated Packaging Market Report Scope

The Mexico corrugated packaging market is the industry that encompasses the design, production, and distribution of fiber-based shipping containers and protective materials. Furthermore, the study evaluates the impact of nearshoring, USMCA regulatory compliance, and sustainability mandates on the competitive landscape and regional supply chain architecture within Mexico.

The Mexico Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

How large will the Mexico corrugated packaging market be by 2031?

It is forecast to reach USD 7.26 billion by 2031, growing at a 4.64% CAGR from 2026.

Which material grade is advancing fastest?

Virgin kraft linerboard shows a 6.62% CAGR through 2031 as exporters demand higher strength.

Why is E flute gaining share?

Brands need thinner profiles with better print surfaces, making E flute ideal for e-commerce and cosmetics boxes.

Which segment records the highest growth among end users?

E-commerce fulfillment centers lead with a projected 5.93% CAGR through 2031.

What regional hotspots drive box demand?

Nuevo León, Estado de México, Jalisco, and Baja California host manufacturing clusters that concentrate packaging demand.

How does the Smurfit Westrock merger affect competition?

The merged entity holds about 25.7% of capacity, spurring rivals such as Bio Pappel and Cartons Ponderosa to expand their own integration footprints.

Page last updated on: