Methyl Methacrylate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.39 Billion |

| Market Size (2031) | USD 19.42 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Methyl Methacrylate Market Analysis by Mordor Intelligence

The Methyl Methacrylate Market size is expected to grow from USD 13.72 billion in 2025 to USD 15.39 billion in 2026 and is forecast to reach USD 19.42 billion by 2031 at 4.76% CAGR over 2026-2031. The methyl methacrylate market in 2025 remained driven by downstream polymer demand, with poly(methyl methacrylate) (PMMA) and acrylic resin applications keeping the value chain focused on established end uses. Buyers have begun distinguishing between commodity supply and certified lower-impact grades. The market is also being shaped by a growing divide between producers that can meet recycled content targets, provide product declarations, and deliver specialty optical performance, and those that remain exposed to price competition in standard grades. Excess Asian supply continues to influence trade flows and pricing discipline, while integrated suppliers are responding by emphasizing specialty derivatives, supply security, and production route efficiency rather than volume growth. Demand from healthcare, electronics, and data infrastructure is broadening the market's demand base by supporting premium monomer and PMMA use beyond traditional construction cycles. The production mix is also shifting as C2 technology scales commercially and chemical recycling moves closer to procurement relevance, providing the methyl methacrylate market with a clearer path toward lower-carbon positioning over the forecast period.

Key Report Takeaways

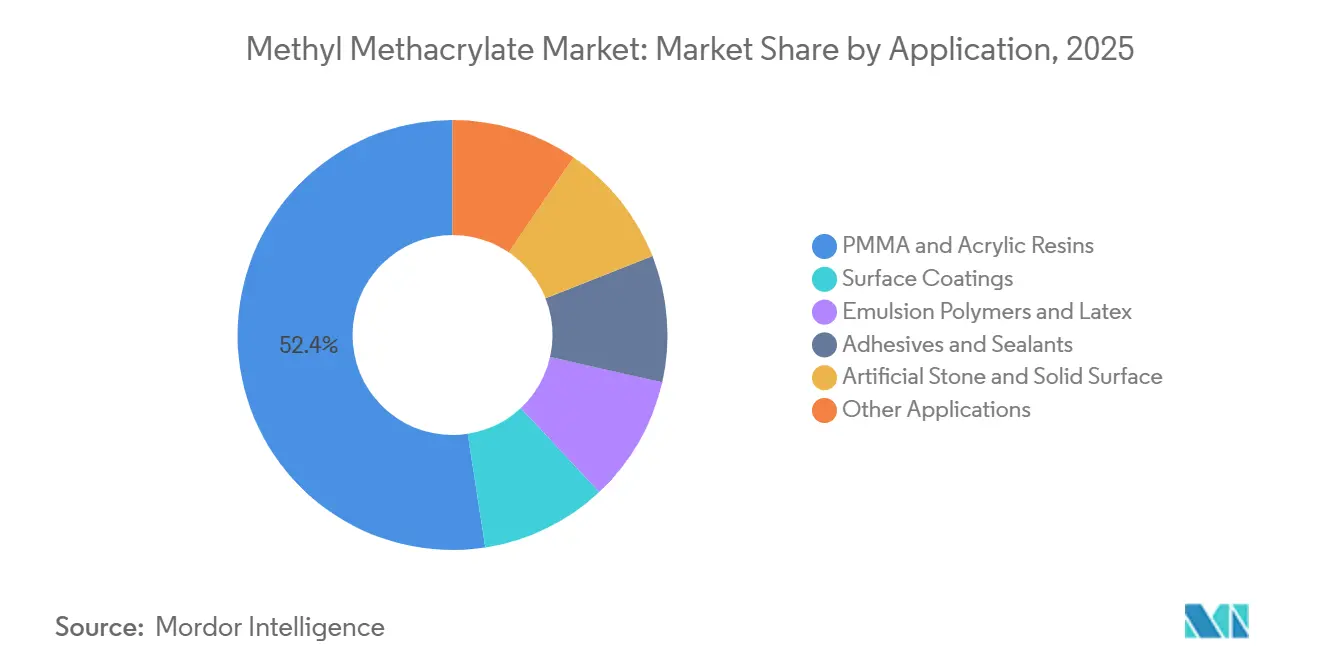

- By application, PMMA and acrylic resins led with 52.44% share in 2025, while artificial stone and solid surfaces are forecast to expand at 5.62% CAGR through 2031.

- By end-use industry, building and construction held 34.71% share in 2025, while healthcare and medical is set to record the highest projected CAGR at 5.89% through 2031.

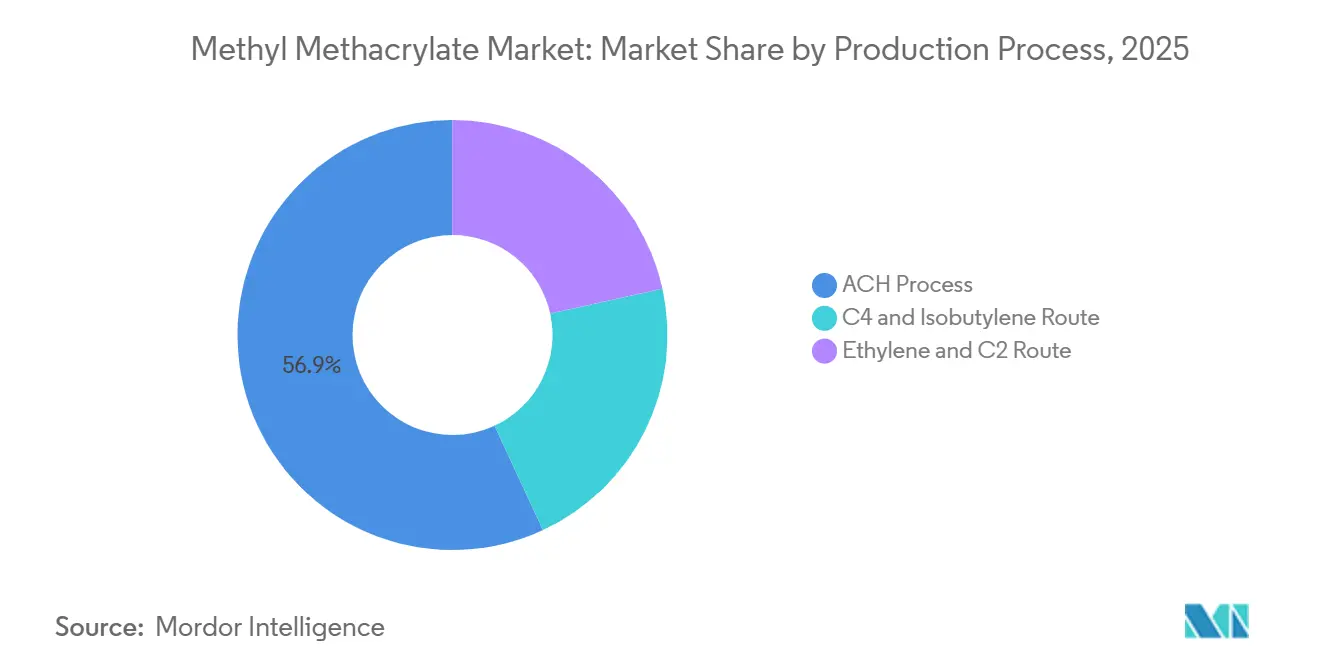

- By production process, the Acetone Cyanohydrin (ACH) route accounted for 56.92% share in 2025, while the ethylene and C2 route is projected to grow at 6.21% CAGR through 2031.

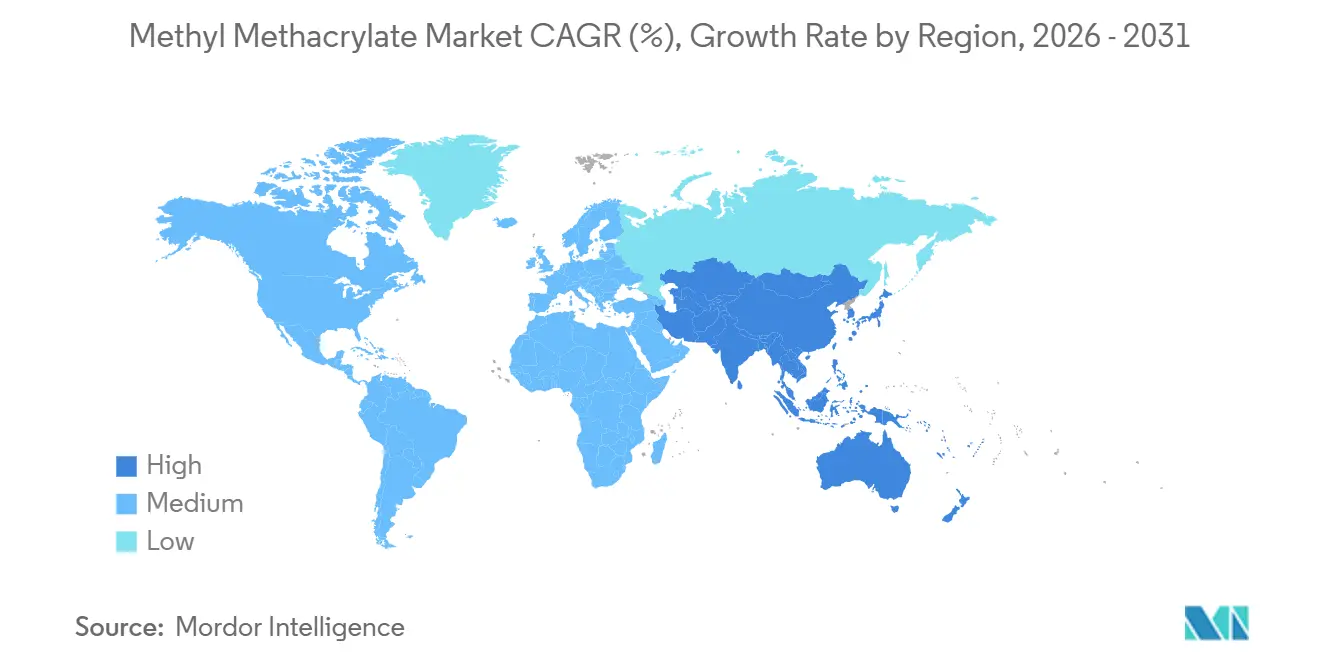

- By geography, Asia-Pacific held 46.85% share in 2025 and is projected to grow at 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Methyl Methacrylate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Building and Construction Demand for MMA-Based Glazing, Acrylic Concrete, and PMMA Cladding Panels | +1.4% | Global, most pronounced in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Automotive Lightweighting Through Structural MMA Adhesives and Optical Grade PMMA in EV Platforms | +1.0% | North America and Europe, Asia-Pacific secondary | Medium term (2-4 years) |

| Display and Electronics Demand for Optical Grade MMA in Light Guide Panels (LGPs) and Device Substrates | +0.7% | Asia-Pacific core, with spillover to North America | Medium term (2-4 years) |

| Architectural and Industrial Paints and Coatings Growth Through Waterborne MMA Emulsion Formulations | +0.6% | Global | Short term (≤ 2 years) |

| Industry Shift Toward the C2 Ethylene Route to Reduce Feedstock Risk and Carbon Liability | +0.5% | North America and Western Europe | Long term (≥ 4 years) |

| PMMA to MMA Chemical Recycling Supporting a Certified Circular Monomer Supply Chain | +0.3% | Europe and North America initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Building and Construction: Infrastructure and Digital Build-Out Extend MMA Consumption

Building and construction remains the broadest demand base for the methyl methacrylate market. MMA-based materials serve glazing, cladding, concrete repair, and other durable applications across commercial and infrastructure assets. Demand is no longer limited to standard acrylic glazing; high-molecular-weight methacrylate systems are also being used in infrastructure rehabilitation where rapid curing and crack bridging are required. PMMA-based façade and glazing specifications are advancing in commercial projects that prioritize long service life, lower structural weight, and weather resistance over long operating cycles. Additional demand is emerging from data infrastructure, where Mitsubishi Chemical Group identified PMMA use in optical fiber and water-cooled data center components as part of its FY2026 strategic direction[1]Mitsubishi Chemical Group, “Operational Summary for the Fiscal Year Ended March 31, 2026,” Mitsubishi Chemical Group, mcgc.com. This is significant because the methyl methacrylate market draws support from both physical construction and digital build-out, reducing dependence on a single construction cycle. It also helps explain why the methyl methacrylate market remains relevant in projects where durability, transparency, and lifecycle performance carry more weight than low upfront material cost.

Automotive Lightweighting: MMA Adhesives and PMMA Penetrate EV Architecture

The shift toward electric vehicles is changing the methyl methacrylate market by increasing the importance of adhesives and optical PMMA, rather than relying on older trim applications. Structural MMA adhesives are being used where manufacturers need to bond aluminum, carbon fiber-reinforced polymer, glass fiber composites, and other dissimilar materials that are not suited to conventional welding methods. ITW Performance Polymers documented this role in multi-material bonding, supporting the view that MMA demand is becoming more tied to design architecture than to unit output alone[2]ITW Performance Polymers, “CFRP Bonding Auto Parts With High Elongation Epoxy and Methyl Methacrylate Adhesives,” ITW Performance Polymers, itwperformancepolymers.com. Battery pack assemblies also require bond lines that can manage thermal expansion differences across materials, raising adhesive performance requirements in EV platforms. As EV penetration increases, the methyl methacrylate market benefits because MMA use per vehicle can grow faster than vehicle production itself in selected assemblies. This keeps automotive demand relevant even as mature PMMA trim applications contribute less incremental growth than specialty adhesive systems.

Electronics and Displays: Optical-Grade PMMA Demand Tightens Supply Specifications

Electronics and display demand is creating a more specialized tier within the methyl methacrylate market because optical-grade material requires tighter purity and processing control than commodity MMA. Light guide plates and related display components depend on PMMA with very low contamination and closely controlled molecular properties, which limits the number of qualified suppliers. Mitsubishi Chemical and other integrated producers are positioned in this space because they combine monomer production, downstream polymer capability, and established customer relationships in display applications. The commercial supply of chemically recycled PMMA into LCD backlighting and automotive headlamp applications by Sumitomo Chemical indicates that recycled content is now entering uses that were previously considered too performance-sensitive for circular feedstock. This raises the qualification bar across the methyl methacrylate market, as OEM procurement teams can now require both optical performance and recycled content documentation in the same supply discussion. It also strengthens the position of producers that can verify traceability, consistency, and product quality at a specialty level, rather than competing on bulk output alone.

PMMA-to-MMA Chemical Recycling: Circular Economy Pressure Reshapes Procurement

Chemical recycling is moving from a development theme to a commercial factor in the methyl methacrylate market as large buyers begin linking monomer sourcing to carbon and recycled content commitments. Trinseo stated that next-generation depolymerization under the MMATwo effort can lower carbon footprint by at least 70% compared to virgin MMA production, while also handling contaminated PMMA streams that might otherwise be discarded. A 2025 study in Chemical Science also showed that trityl ester modification can reduce PMMA depolymerization temperature to 270°C and deliver 94.5% MMA yield, narrowing the energy gap between recycled and fossil-based pathways. These developments are relevant because procurement decisions are increasingly influenced by supplier reporting requirements and the need to document lower upstream emissions across complex manufacturing chains. Röhm is also investing in chemical recycling capacity for its proTerra recycled content MMA, indicating that the methyl methacrylate market is treating recycling as a strategic supply position rather than a supplementary program. Over time, this is likely to differentiate producers that can offer circular monomer pathways from those that remain limited to conventional virgin supply.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material and Energy Cost Volatility Compressing Acetone Cyanohydrin (ACH) Route Producer Margins | -1.3% | Global, most acute in Asia and Europe | Short term (≤ 2 years) |

| Substitute Material Pressure From PET, Polycarbonate, and Glass in Glazing, Signage, and Coatings Applications | -0.7% | North America and Europe | Medium term (2-4 years) |

| China's Structural Overcapacity Creating Persistent Export-Led Pricing Pressure | -1.1% | Asia-Pacific core, with spillover to Europe and South America | Short term (≤ 2 years) |

| ACH Waste Burden and Rising Environmental Compliance Costs at Legacy Plants | -0.5% | Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material and Energy Cost Volatility: ACH Producers Face a Structural Input Risk

Raw material and energy cost volatility remains a restraint for the methyl methacrylate market, as ACH-based producers depend on a feedstock chain that is more difficult to balance than alternative routes. The process relies on acetone and hydrogen cyanide, which do not necessarily move in line with each other or with finished MMA selling conditions. This exposes producers to margin pressure even when only one part of the input chain tightens, and complicates planning in regions where energy costs remain elevated. Waste handling obligations tied to ammonium bisulfate add another cost layer for legacy plants that do not share the same route profile as C2 operations. As a result, the methyl methacrylate market is seeing investment redirect toward technologies that reduce feedstock exposure and environmental burden. Producers that delay these changes are more likely to face persistent margin compression rather than a short-term setback.

China Overcapacity: Export-Led Pricing Pressure Redraws the Competitive Map

China-related overcapacity continues to affect the methyl methacrylate market, as excess regional supply has moved beyond domestic boundaries and is influencing external trade flows. Mitsubishi Chemical Group stated in 2025 that excess Asian supply would continue moving into Europe until domestic Chinese absorption improved, indicating that the pressure is structural rather than temporary. Freight costs no longer provide the same degree of regional insulation when large surplus volumes seek export outlets. The result is weaker pricing discipline in standard grades and a greater need for producers to protect margins through specialty positioning, route efficiency, and downstream integration. Mitsubishi Chemical Group's plant closures, joint venture dissolution, and canceled expansion plans indicate that the methyl methacrylate market is responding through rationalization rather than waiting for a full price recovery. This environment favors companies that can defend differentiated grades and long-term customer relationships while commodity supply remains under pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Artificial Stone and Solid Surfaces Lead Growth as Application Mix Diversifies

PMMA and acrylic resins held 52.44% of the methyl methacrylate market share in 2025, confirming that the largest application base remains within the downstream polymer chain. Artificial stone and solid surfaces are projected to grow at a 5.62% CAGR through 2031, representing a faster-growing use case beyond the traditional resin segment. This shift is notable because hospital and laboratory planners are specifying PMMA composite countertops and fixtures where seamless surfaces and hygiene performance are required. That procurement pattern supports a more stable demand stream than a standard residential remodeling cycle. It also creates opportunities for suppliers that can serve both volume resin demand and more specialized surface applications with tighter performance requirements.

Surface coatings and emulsion polymers remain important, providing a broad secondary base for MMA consumption across architectural and industrial uses. The move toward waterborne and high-solids coatings is supporting methacrylate loading in binders that require gloss retention and weathering performance, giving this segment durable relevance in the methyl methacrylate market. Regulatory pressure on emissions in coatings is also supporting conversion toward formulations where MMA-based chemistry remains applicable. Adhesives and sealants represent a higher-value category, as structural bonding in electric vehicle (EV) and renewable energy assemblies requires specialized chemistries beyond standard bulk applications. Emulsion polymers continue to track broad industrial production, but the strongest application momentum in the methyl methacrylate industry is centered on solid surfaces and advanced adhesives rather than on the more mature commodity segments. The purity split within the methyl methacrylate market also means premium grades are becoming more concentrated with integrated suppliers, while standard grades face stronger price pressure.

By End-Use Industry: Building Maintains Dominant Share as Healthcare Accelerates

Building and construction accounted for 34.71% of the methyl methacrylate market size in 2025, maintaining its position as the leading end-use segment for MMA demand. The segment remained broad because MMA feeds both acrylic sheet and glazing products and reactive systems used in concrete repair and rehabilitation. Long service life specifications in sound barriers, roof glazing, and infrastructure panels continue to support repeat demand over extended asset cycles. This gives the methyl methacrylate market a steady base in projects where durability and outdoor performance are prioritized. Demand is nonetheless widening, as faster growth is coming from smaller but more specialized end uses.

Healthcare and medical is projected to grow at a 5.89% CAGR through 2031, making it the fastest-growing end-use segment in the methyl methacrylate market. Research published in 2026 showed progress in zirconium-oxide reinforced PMMA composite bone cements and in vancomycin-loaded PMMA cement performance, supporting the medical relevance of the polymer family beyond standard materials use. Dentistry is also adopting digital CAD/CAM workflows for PMMA disc blanks, raising demand for premium monomer and polymer consistency in prosthetic applications. Automotive and transportation remains the second largest revenue contributor, though its newer growth is more closely tied to structural adhesives than to mature trim applications. Electronics is also gaining weight as display manufacturers require optical-grade and recycled-content PMMA in performance-sensitive components. These changes indicate that the methyl methacrylate market is becoming more value-dense, even as some of the faster-growing end uses remain smaller in absolute volume than building and construction demand.

By Production Process: ACH Consolidates Share as C2 Route Redefines Industry Economics

The ACH route accounted for 56.92% of the methyl methacrylate market in 2025, reflecting the long-established installed base of acetone- and HCN-linked capacity across major producing regions. This position remained strong because ACH assets are deeply embedded in existing industrial networks and continue to support large-scale output. At the same time, the route carries a heavier environmental and byproduct burden, which is increasingly relevant as disposal, compliance, and carbon-related considerations become part of investment reviews. The methyl methacrylate market is not shifting rapidly, but the economics are moving in a direction that weakens the long-term case for legacy ACH dominance. Producers with older plants are under pressure to maintain utilization while preparing for a different route balance in future capacity decisions.

The ethylene and C2 route is projected to grow at a 6.21% CAGR through 2031, making it the fastest-expanding production pathway in the methyl methacrylate market. Röhm's Bay City plant reached full-scale operation in June 2026 and demonstrated commercial readiness for LiMA technology in North America. Röhm also stated that the plant can reduce CO2 emissions by up to 42% compared with conventional ACH production, giving the route a clearer sustainability and feedstock positioning. A peer-reviewed life cycle study published in ACS Sustainable Chemistry & Engineering also supported the environmental advantage of the C2 route compared with the main alternative routes. This is relevant because procurement and regulatory decisions increasingly consider product footprint and route transparency alongside output volumes. As a result, the methyl methacrylate industry is moving toward a more differentiated production landscape where route selection affects cost, carbon profile, and customer access simultaneously.

Geography Analysis

Asia-Pacific held 46.85% of the methyl methacrylate market share in 2025, and the region's market size is projected to expand at a CAGR of 5.34% through 2031. The region accounts for the largest share of both demand and supply, giving it significant influence over pricing, trade flows, and investment priorities. China remains the largest market within the region, though supply additions have outpaced local absorption in parts of the chain. This imbalance keeps standard-grade pricing under pressure and encourages producers to seek export markets when domestic conditions soften. India and Southeast Asia are becoming more important to the methyl methacrylate market, as urbanization, automotive expansion, and acrylic signage demand support steady incremental consumption. Mitsubishi Chemical Group has also identified India as a target for partnership-led supply development, reinforcing the view that regional growth is spreading beyond the traditional Northeast Asia base.

North America is moving into a different supply position as local production capability strengthens and lower-carbon route options become commercially available. Röhm's Bay City facility added 250,000 tons of C2 route capacity and brought a new domestic supply option into operation in June 2026. This gives automotive, electronics, construction, and medical customers a regional source that aligns with procurement criteria focused on route efficiency and product footprint. The methyl methacrylate market in North America also benefits from coatings and derivative demand supported by ongoing VOC-related formulation shifts. Europe presents a different picture, as demand growth is tied less to volume expansion and more to sourcing conversion. REACH-related waste handling obligations and broader sustainability reporting expectations are pushing the European methyl methacrylate market toward certified, lower-carbon, and more traceable supply pathways.

South America, the Middle East, and Africa together account for a smaller share of the methyl methacrylate market, but each carries a distinct strategic role. Saudi Arabia stands out because domestic MMA production supports regional supply and connects to large-scale infrastructure and commercial development plans. The broader Middle East construction pipeline continues to support demand for PMMA glazing, façades, coatings, and solid surfaces across commercial and hospitality projects. South American demand remains more modest and is centered on coatings, adhesives, and consumer goods, with import exposure and currency conditions limiting near-term expansion.

Competitive Landscape

The methyl methacrylate market is moderately consolidated at the top of the value chain, but competition varies between commodity supply and specialty grade positioning. Röhm GmbH, Mitsubishi Chemical Group, Lucite International, and Dow maintain their positions by combining technology, integration, and downstream application access rather than competing solely on bulk tons. Their advantages are strongest in areas where production route, polymer capability, and customer qualification matter, including display, medical, and advanced automotive applications. As a result, the methyl methacrylate market is not defined solely by nominal capacity, since technical approval and route credibility now play a larger role in account retention. Market leadership is also more durable in specialty segments than in price-exposed standard grades.

Röhm's June 2026 Bay City startup established full-scale industrial C2-based MMA production in North America and strengthened the company's position in lower-carbon routes. Mitsubishi Chemical Group took a different approach by dissolving its Taiwan joint venture, canceling the Geismar expansion, and closing the Hiroshima plant, while shifting focus toward higher-value derivatives and emerging supply opportunities. These moves indicate that the methyl methacrylate market is rewarding sharper portfolio decisions rather than volume additions alone. Lucite International remains relevant through its Alpha process, while Röhm's LiMA route adds another validated C2 option for future technology competition. In practice, this places greater strategic value on proprietary route economics, downstream integration, and customer-specific supply reliability than on undifferentiated scale.

A second competitive layer is emerging around recycled and circular supply, as premium buyers increasingly seek both performance and verified sustainability credentials. Sumitomo Chemical's commercial supply of chemically recycled PMMA to LG Display and Nissan Motor illustrates how circular materials can move into high-specification applications. Röhm's investment in proTerra-related recycling capabilities points in the same direction, suggesting that future advantage in the methyl methacrylate market may come from combining route efficiency with the availability of recycled content. This creates a gap between producers that can support premium procurement standards and those that remain more exposed to standard-grade price competition. Advances in patent and process development for depolymerization also raise the possibility that new specialized recyclers could enter the methyl methacrylate market over the forecast period.

Methyl Methacrylate Industry Leaders

Mitsubishi Chemical Group Corporation

Röhm GmbH

Dow

Sumitomo Chemical Co., Ltd.

LX MMA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Röhm opened its Bay City, Texas LiMA MMA plant at full industrial scale, marking the first commercial deployment of C2-based MMA technology in North America. The USD 1.6 billion facility produces 250,000 tons of MMA annually, reduces CO2 emissions by up to 42% compared to conventional ACH production, and strengthens domestic US MMA supply for automotive, construction, electronics, and medical customers.

- April 2026: Wanhua Chemical Group announced a capital investment plan of CNY 27.3 billion (approximately USD 3.78 billion) across 13 major projects spanning polyurethanes, petrochemical chains, fine chemicals, and emerging materials, extending its presence across MMA-relevant specialty chemical value chains.

Global Methyl Methacrylate Market Report Scope

Methyl methacrylate (MMA) is a colorless, highly flammable organic liquid with the chemical formula C₅H₈O₂. It is primarily used as a monomer in the manufacture of acrylic plastics and shatter-resistant glass (polymethyl methacrylate, or PMMA), as well as paints, adhesives, resins, and dental bone cement.

The methyl methacrylate market is segmented by application, end-use industry, production process, and geography. By application, the market is segmented into PMMA and acrylic resins, surface coatings, emulsion polymers and latex, adhesives and sealants, artificial stone and solid surface, and other applications. By end-use industry, the market is segmented into building and construction, automotive and transportation, electrical and electronics, healthcare and medical, consumer goods, and other end-use industries. By production process, the market is segmented into the ACH process, the C4 and isobutylene route, and the ethylene and C2 route. The report also covers market size and forecasts for methyl methacrylate across 21 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| PMMA and Acrylic Resins |

| Surface Coatings |

| Emulsion Polymers and Latex |

| Adhesives and Sealants |

| Artificial Stone and Solid Surface |

| Other Applications |

| Building and Construction |

| Automotive and Transportation |

| Electrical and Electronics |

| Healthcare and Medical |

| Consumer Goods |

| Other End-use Industries |

| ACH Process |

| C4 and Isobutylene Route |

| Ethylene and C2 Route |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | PMMA and Acrylic Resins | |

| Surface Coatings | ||

| Emulsion Polymers and Latex | ||

| Adhesives and Sealants | ||

| Artificial Stone and Solid Surface | ||

| Other Applications | ||

| By End-use Industry | Building and Construction | |

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Healthcare and Medical | ||

| Consumer Goods | ||

| Other End-use Industries | ||

| By Production Process | ACH Process | |

| C4 and Isobutylene Route | ||

| Ethylene and C2 Route | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Methyl Methacrylate Market?

The Methyl Methacrylate Market size is expected to grow from USD 13.72 billion in 2025 to USD 15.39 billion in 2026 and is forecast to reach USD 19.42 billion by 2031 at 4.76% CAGR over 2026-2031.

Which application is growing the fastest through 2031?

Artificial stone and solid surfaces are the fastest-growing applications, with a projected 5.62% CAGR through 2031, supported by healthcare and laboratory surface demand.

Which end-use segment remains the largest for MMA consumption?

Building and construction remained the largest end-use segment, with a 34.71% share in 2025, supported by glazing, repair systems, and long service-life specifications.

Why is the C2 route becoming more important in MMA production?

The ethylene and C2 route is projected to grow at 6.21% CAGR through 2031 and gained visibility after Röhm brought its Bay City LiMA plant to full scale in June 2026.

Page last updated on: