Metallurgical Coal Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 132.46 Billion |

| Market Size (2031) | USD 154.37 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metallurgical Coal Market Analysis by Mordor Intelligence

The Metallurgical Coal Market size is projected to expand from USD 128.37 billion in 2025 and USD 132.46 billion in 2026 to USD 154.37 billion by 2031, registering a CAGR of 3.11% between 2026 to 2031. The metallurgical coal market continues to depend on the slow replacement cycle of blast furnace steelmaking, as most operating blast furnaces use coke as both a fuel input and a reducing agent in daily production. Demand remains supported by the blast furnace-basic oxygen furnace route, which accounts for more than 70% of the steel sector’s energy use and links the metallurgical coal market to industrial activity across major steel-producing economies. The U.S. Department of Energy’s May 2025 decision to place metallurgical coal on the critical material list would provide policy support, as the designation recognizes its limited substitutability in blast furnace operations. Premium reserve quality, port access, and blending value continue to influence the metallurgical coal market, with acquisition activity focused on large, established assets rather than early-stage projects. Steel decarbonization plans, weak profitability due to excess steel capacity, and recurring supply disruptions continue to pressure the metallurgical coal market, slowing capital rotation while maintaining the strategic importance of high-quality supply.

Key Report Takeaways

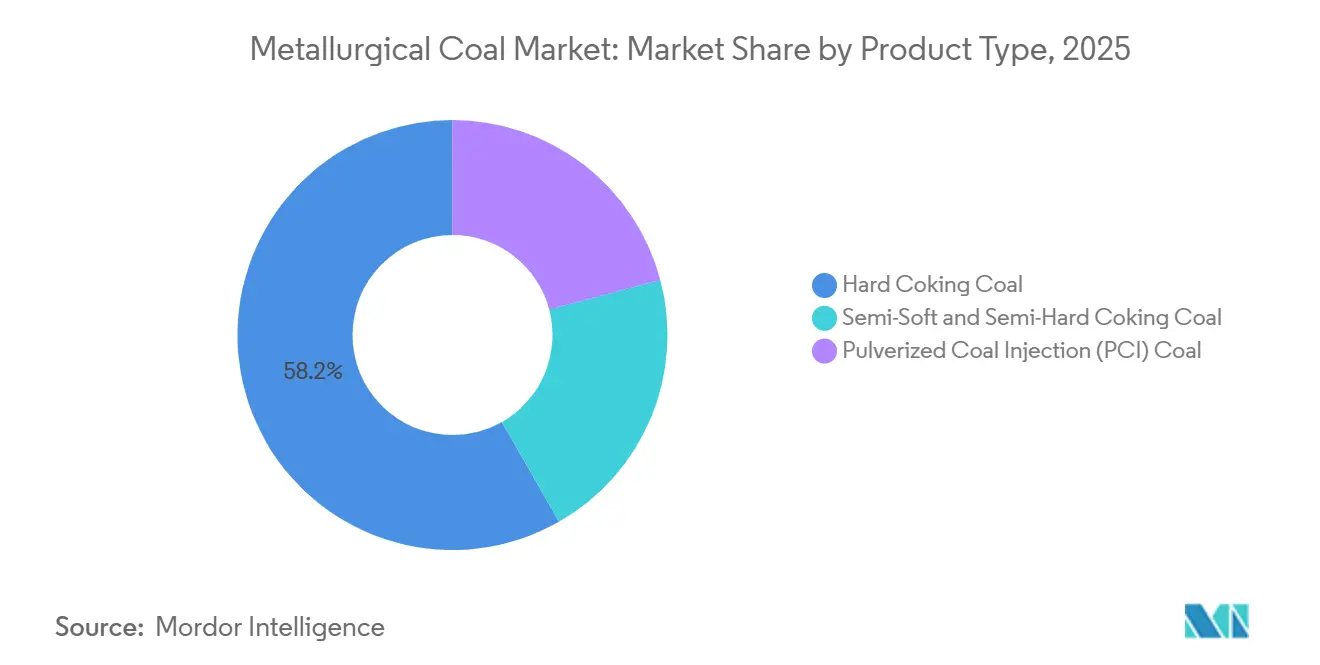

- By product type, Hard Coking Coal held 58.24% of the metallurgical coal market share in 2025, while Pulverized Coal Injection (PCI) Coal is forecast to expand at a 3.87% CAGR through 2031.

- By mining method, Underground Mining accounted for 65.49% of the metallurgical coal market in 2025, while Surface Mining recorded the highest projected CAGR at 3.57% through 2031.

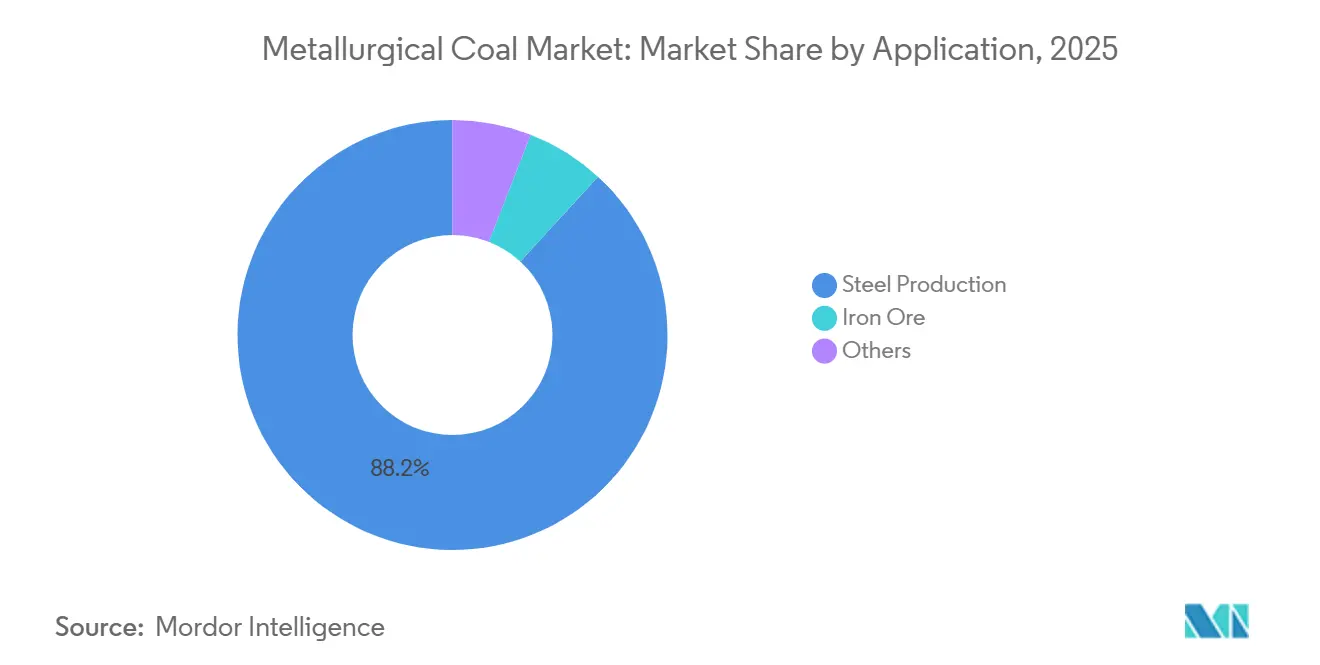

- By application, Steel Production accounted for 88.16% of the metallurgical coal market size in 2025, while Iron Ore Processing is advancing at a 3.92% CAGR through 2031.

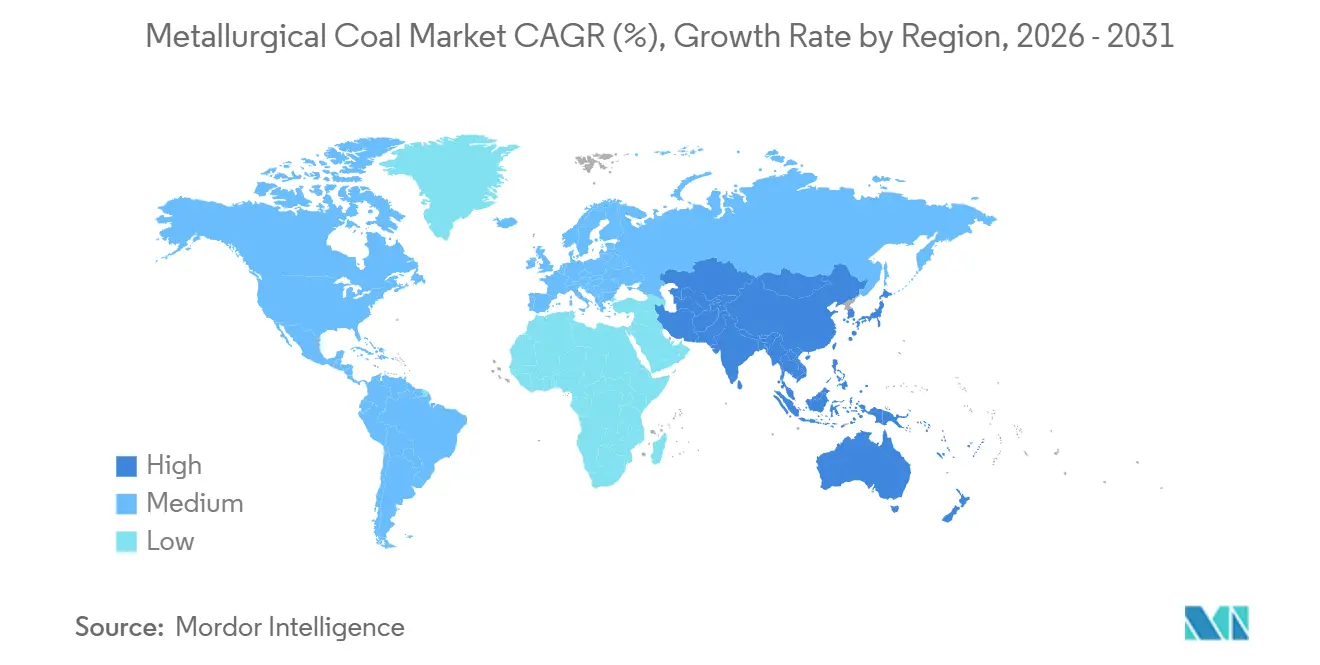

- By geography, Asia-Pacific captured 57.28% of the metallurgical coal market share in 2025, and it is forecast to grow at a 4.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metallurgical Coal Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural Dependency of Steelmaking on Metallurgical Coal | +1.3% | Global | Long term (≥ 4 years) |

| Limited Commercial Substitutes in Blast Furnace Steelmaking | +0.9% | Global | Long term (≥ 4 years) |

| Need for High-Quality and Consistent Coking Coal Supply | +0.6% | APAC core, spillover to North America and Europe | Medium term (2-4 years) |

| Mining Automation and Productivity Improvement | +0.4% | Australia, China, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural Dependency of the Steel Industry on Metallurgical Coal

Blast furnaces have long asset lives and, once commissioned, typically remain in service for decades. This keeps the metallurgical coal market linked to installed steelmaking capacity, rather than only to short-term sentiment. Producing 1 ton of steel through the Blast Furnace-Basic Oxygen Furnace (BF-BOF) route still requires nearly 0.86 tons of metallurgical coal, as coke plays both a chemical and structural role in the furnace burden. The OECD stated that more than 40% of the 165 million metric tons of global steelmaking capacity planned for 2025-2027 remains BF-BOF-based, with India and ASEAN accounting for much of that pipeline. This capacity mix keeps the metallurgical coal market tied to physical operating requirements, even when steel profitability remains uneven across mature regions. Supply conditions add another factor, as World Steel has highlighted resource and supply chain constraints around the grades most valued in coke making. As a result, the metallurgical coal market can remain firm even when capacity utilization softens, since existing blast furnaces still require high-grade input coal to maintain output quality.

Limited Commercial Substitutes for Metallurgical Coal in Steelmaking

The metallurgical coal market continues to reflect the lack of a broadly commercial substitute that can match coal’s combined fuel and reduction functions at the scale required for blast furnace steelmaking. OECD research on hydrogen in steelmaking shows that green steel pathways face capital, profitability, and overcapacity barriers, which delay their ability to replace coal-intensive routes at the required pace. The steel decarbonization outlook for 2025 is expected to remain gradual, as newly announced blast furnace capacity continues to exceed newly announced Direct Reduced Iron (DRI) capacity, while emissions intensity remains largely flat. The International Energy Agency (IEA) also expects hydrogen-based steelmaking adoption to remain limited over the medium term due to cost pressures and constraints on scrap availability. This leaves the metallurgical coal market less exposed to immediate substitution and more dependent on the slower economics of steel plant turnover, financing, and feedstock readiness. It also means quality producers continue to hold negotiating leverage in long-term contracts, as steelmakers cannot rapidly redesign existing blast furnaces to accommodate alternative inputs.

Steelmakers' Need for High-Quality, Consistent Coking Coal Supply

Steel mills operating large blast furnaces require coal blends with tight ash, sulfur, and volatile matter specifications. This anchors the metallurgical coal market to a narrow pool of premium supply basins. India’s coking coal imports are projected to rise 32% year over year in 2025 to 73.5 million tons, as domestic coal quality remains unsuitable for direct blast furnace use without costly treatment. The same quality gap is expected to keep the country heavily import dependent, even as steel capacity development remains active, strengthening the role of United States, Australian, and Canadian exporters in supply planning. In practical terms, the metallurgical coal market rewards reserve quality more than simple output volume, as poor-quality domestic alternatives still require premium imported blends to meet furnace performance targets. This pattern narrows purchasing options to regions such as Queensland’s Bowen Basin, Canada’s Elk Valley, and the Appalachian Basin in the United States. It also explains why buyers prefer long-term procurement and supply diversification over spot exposure, as blast furnace uptime and coke quality directly affect steel output.

Mining Automation and Productivity Enhancement

Mine-level productivity gains are also shaping the metallurgical coal market, as automation helps larger producers reduce unit costs and maintain output during weaker pricing periods. In May 2025, China Huaneng Group is expected to commission 100 autonomous all-electric trucks at the Yimin open-pit mine, using a 5G-Advanced network designed for real-time coordination across a remote fleet[1]Huawei, “North China’s Yimin Mine Deploys World’s First Fleet of 100 5G-A Connected, Self-Driving Electric Trucks,” Huawei, huawei.com. Anglo American also reported that remote dozer automation reduced in-cab exposure by 45,000 to 75,000 hours each year across its Bowen Basin steelmaking coal sites. These gains matter because the metallurgical coal market rewards not only reserves but also operators that can sustain safe, predictable throughput across multi-year price cycles. Improved automation can extend reserve life and strengthen cost positions, giving well-capitalized firms more flexibility when weaker players reduce spending. Over time, this operating advantage supports further consolidation in the metallurgical coal market, as productivity investments are becoming a stronger barrier to entry in both surface and underground mining.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization Policies Against Carbon-Intensive Steelmaking | -0.9% | EU, UK, North America | Long term (≥ 4 years) |

| Price Volatility and Cost Inflation Pressures | -0.5% | Global | Short term (≤ 2 years) |

| Permitting Delays and Environmental Approval Constraints | -0.5% | North America, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Policies Targeting Carbon-Intensive Steelmaking

The metallurgical coal market faces a long-term restraint from decarbonization regulations that aim to reduce the role of coal-intensive steelmaking routes in developed economies. From 2026, the revised EU Emissions Trading System (ETS) benchmark definitions will cover sintered ore, hot metal, and hydrogen, strengthening policy support for H2-Direct Reduced Iron-Electric Arc Furnace (H2-DRI-EAF) pathways over traditional blast furnace production[2]International Energy Agency, “Coal Mid-Year Update 2025 – Prices,” International Energy Agency, iea.org . The EU Carbon Border Adjustment Mechanism adds another layer of pressure by imposing carbon-related costs on imported steel, encouraging non-EU producers to accelerate cleaner production plans. The UK Steel Strategy, expected to be published in 2025, also points to EAF as the long-term domestic direction, with DRI positioned as a bridge for primary steelmaking. However, the metallurgical coal market does not face an immediate demand decline, as Organization for Economic Co-operation and Development (OECD) data still indicates large excess capacity and weak profitability, which delays capital spending on green transitions. As a result, the market is likely to experience a gradual demand headwind over time rather than a near-term break in blast furnace coal use.

Price Volatility and Cost Inflation Pressures on Producers

The metallurgical coal market remains exposed to price volatility because a few geographies with recurring weather, logistics, and safety disruptions account for a large share of premium seaborne supply. Australian premium hard coking coal prices are expected to stay below USD 200 per ton through much of 2025, compressing producer margins after earlier periods of stronger pricing. The hedging market also remains thin relative to total production, limiting many producers’ ability to protect revenues during sudden price declines. Freight cost volatility creates an additional challenge, as delivered coal prices can shift quickly when shipping costs and fuel prices move in the same direction. These conditions make new project development harder to justify, especially for producers near the upper end of the cost curve. For the metallurgical coal market, this means supply may remain disciplined, but operational stress can still rise when prices weaken and costs remain sticky.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Hard Coking Coal Anchors Demand, PCI Grades Drive Cost Optimization

Hard coking coal is projected to hold 58.24% of the metallurgical coal market in 2025, reflecting its continued role as a key feedstock for blast furnace coke making. Its position is supported by low sulfur content, strong caking properties, and higher coke strength after reaction, which remain difficult to replace in premium furnace operations. As a result, the metallurgical coal market continues to prioritize grade quality, as operators are unlikely to compromise blast furnace stability for cheaper coal blends. Pulverized Coal Injection (PCI) coal is forecast to expand at a 3.87% CAGR through 2031, supported by steelmakers seeking to reduce coke rates without lowering hot metal output. Semi-soft and semi-hard grades remain relevant in blend optimization, especially in India and Southeast Asia, where mills balance technical performance against import costs.

PCI coal is expected to record the fastest growth in this segment, and its projected 3.87% expansion in the metallurgical coal market through 2031 reflects its role as a cost-control lever within the existing Blast Furnace–Basic Oxygen Furnace (BF-BOF) system. Modern blast furnaces can use PCI coal to replace a meaningful portion of coke in the burden mix, helping mills improve raw material economics without moving away from coal-based ironmaking. This makes PCI growth complementary to the metallurgical coal market, as the segment still depends on active blast furnace operations. Supply risk supports hard coking coal’s pricing position, as Australia’s Bowen Basin and the Appalachian Basin remain central to seaborne quality supply, and both regions face periodic disruptions. The result is a product mix in which the largest segment remains tied to quality assurance, while the fastest-growing segment gains traction as mills seek lower coke intensity within the same process route.

By Mining Method: Underground Reserves Dominate Quality, Surface Automation Closes the Cost Gap

Underground mining is projected to account for 65.49% of the metallurgical coal market by mining method in 2025, as many of the world’s highest-grade coking coal seams remain accessible only through subsurface development. Queensland’s Bowen Basin, parts of Appalachia, and Canada’s Elk Valley support this pattern, as reserve quality and seam position continue to favor underground extraction across many premium deposits. This keeps the metallurgical coal market closely linked to longwall and room-and-pillar investment across key coking coal corridors. Surface mining, however, is forecast to grow at a 3.57% CAGR through 2031, as autonomy and remote operations reduce labor exposure and support more stable utilization at open-pit sites. This shift allows surface assets in selected geographies to narrow part of the cost and productivity gap that once favored underground operations.

Surface mining leads the growth outlook in this category, and the projected CAGR shows how digital operations are improving cost discipline in the metallurgical coal market. The Yimin mine’s autonomous electric truck fleet illustrates how 24-hour operation and real-time coordination can improve output consistency at remote surface mines. Underground mining remains central to the metallurgical coal industry because reserve quality is concentrated there. Warrior Met Coal’s Blue Creek operation is expected to reach longwall production in October 2025 before delivering a sharp production increase in the first quarter of 2026. The growing use of digital twins, adaptive controls, and predictive maintenance raises the capital threshold for both mining methods, strengthening the position of firms with larger balance sheets. This leaves the metallurgical coal market with a clear split: underground mining holds the largest share due to geology, while surface mining gains momentum as automation improves its economics.

By Application: Steel Production Commands the Market, Iron Ore Sintering Accelerates

Steel production is projected to account for 88.16% of the metallurgical coal market in 2025, keeping this segment aligned with blast furnace operating rates rather than steel output figures alone. The segment’s weight reflects that the metallurgical coal market remains centered on primary steelmaking, especially in countries where Blast Furnace–Basic Oxygen Furnace (BF-BOF) technology still dominates integrated mill design. Global Energy Monitor’s 2026 work is expected to identify 319 million tons per annum (MTPA) of blast furnace capacity under active development, with net BF additions projected through 2030 and 2035. China remains a key anchor for this use pattern, as more than 90% of its steel output still uses BF-BOF technology and sustains a large base of coke demand. The Others category continues to hold a residual role across ferroalloys, carbon electrodes, and industrial chemicals, but it does not change the metallurgical coal market’s core dependence on steelmaking.

Iron ore sintering is projected to grow at a 3.92% CAGR through 2031, making it the fastest-expanding application in the metallurgical coal market. This growth is tied to sintering demand and to steel plants expanding ironmaking flexibility across raw material inputs in Southeast Asia and the Middle East. India’s restrictions on low-ash metallurgical coke imports have added support, as domestic mills are using more coking coal in their own coke ovens instead of relying on imported processed coke. As a result, the metallurgical coal market is seeing growth from both stable blast furnace steel production and surrounding ironmaking processes that still require coal-based inputs. This combination keeps application demand broad enough to support volume even as decarbonization pressure rises more quickly in parts of Europe and North America.

Geography Analysis

Asia-Pacific is projected to account for 57.28% of the metallurgical coal market in 2025 and is expected to be the fastest-growing regional block, registering a CAGR of 4.21% through 2031. China provides the largest demand base, as more than 90% of its steel production still uses the Blast Furnace-Basic Oxygen Furnace (BF-BOF) route. This keeps the metallurgical coal market closely tied to blast furnace utilization in the country. India is a key growth market, with the Ministry of Steel reporting 57.1 million tons of coking coal imports in FY2024-25 and continued steel capacity expansion into 2026. Japan and South Korea support regional procurement activity, as their buying patterns continue to influence seaborne quality benchmarks and blend preferences. As a result, Asia-Pacific remains central to the metallurgical coal market, as both mature and expanding steel systems in the region continue to rely on coal-based ironmaking.

North America remains relevant in the metallurgical coal market, as it combines export capacity with domestic policy support for coal’s role in steelmaking. The Department of Energy's (DOE's) May 2025 critical material designation is expected to support that position, while federal permitting support is set to cover additional reserve development in Alabama by early 2026. Canada also remains active through its premium steelmaking coal reserves in British Columbia and Alberta, which continue to attract development interest despite tighter environmental reviews. Europe, by contrast, is moving toward slower structural demand, as Emissions Trading System (ETS) reform and CBAM increase pressure on coal-intensive steelmaking routes, although residual blast furnace capacity continues to support near-term consumption.

South America and the Middle East and Africa represent smaller demand pools, but both remain relevant to the metallurgical coal market because integrated steel assets in Brazil and South Africa continue to require coal-based inputs. Brazil supports import demand through its integrated blast furnace producers, while South Africa maintains domestic usage linked to its BF-based steel system. Parts of the Middle East are investing more in Direct Reduced Iron (DRI)-based steelmaking, which limits direct coal demand growth compared with Asia-Pacific. Across regions, metallurgical coal market growth follows new BF-BOF additions, while pressure increases where EAF and DRI routes displace older blast furnace capacity.

Competitive Landscape

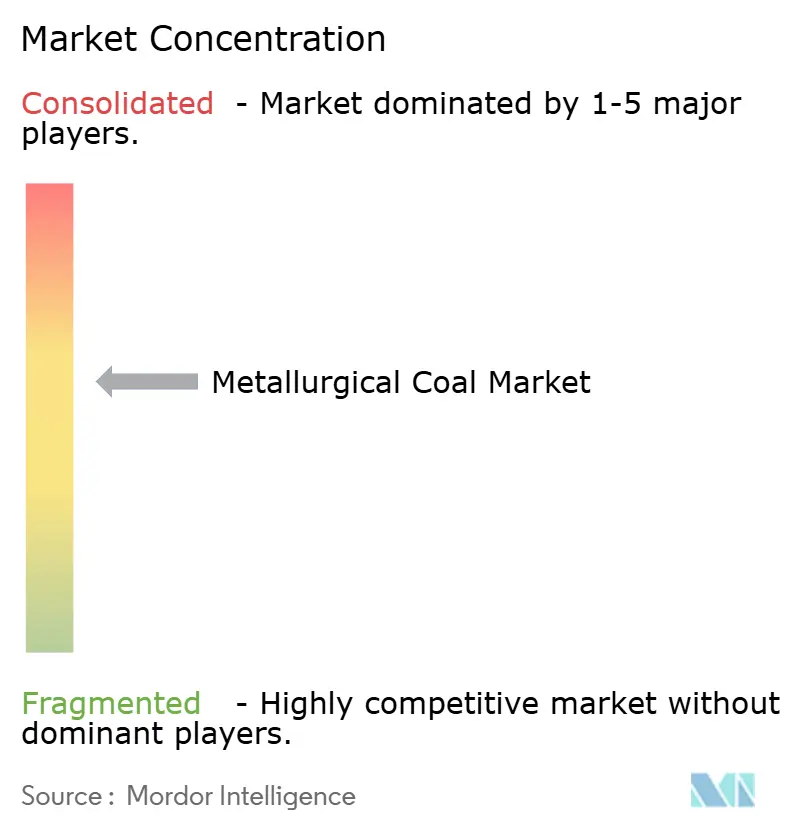

The metallurgical coal market is moderately consolidated. The market is undergoing consolidation, as ownership of premium reserves shifts toward fewer companies with the financial capacity to fund acquisitions, infrastructure, and long-term mine plans. In July 2024, Glencore completed its acquisition of a 77% interest in Teck’s steelmaking coal business for USD 6.9 billion, creating one of the largest seaborne steelmaking coal platforms. Whitehaven Coal’s April 2024 acquisition of the Daunia and Blackwater mines from BHP and Mitsubishi also strengthened its position across Australian coal grades and improved its blending flexibility. As a result, the metallurgical coal market is placing greater value on companies that control both premium reserves and reliable export corridors. This trend has also encouraged private and strategically aligned buyers to pursue assets that listed owners may no longer want to hold amid stricter ESG pressure.

Yancoal Australia’s April 2026 agreement to acquire an 80% interest in the Kestrel Coal Mine for up to USD 2.4 billion would indicate that premium Queensland assets continue to attract strategic interest. The deal would also highlight the growing importance of Asian-linked offtake structures, particularly when portfolio strategies remain tied to Chinese steel demand. Anglo American’s May 2026 agreement to sell its Australian steelmaking coal business for up to USD 3.9 billion would further indicate that some public miners are continuing to exit the market while other owners expand their positions. In the metallurgical coal market, this asset transfer can extend mine investment cycles, as private buyers often face fewer public market disclosure and ESG-related constraints.

Pure-play producers are adopting a different strategy by focusing on reserve quality, cost control, and export-backed contract discipline instead of broad portfolio diversification. Alpha Metallurgical Resources’ 2026 domestic sales commitments, at an average price of USD 136.8 per ton, indicate the pricing value that stable, quality-assured supply can still capture. Warrior Met Coal’s Blue Creek ramp-up also demonstrates how expanding established premium assets can increase output faster than riskier greenfield development. Overall, the metallurgical coal market remains competitive, but companies with the strongest positions now combine reserve quality, production reliability, and access to major seaborne customers.

Metallurgical Coal Industry Leaders

BHP

Glencore

Anglo American plc

Peabody Energy, Inc.

Whitehaven Coal Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Anglo American is expected to sell its entire portfolio of Australian steelmaking coal mines to Dhilmar Limited for up to USD 3.87 billion in cash. The transaction would complete Anglo American’s exit from steelmaking coal as part of its portfolio restructuring ahead of its announced merger with Teck Resources. The deal would transfer premium hard coking coal capacity to private ownership, with Dhilmar expected to pursue a long-term development strategy.

- April 2026: Yancoal Australia is expected to acquire an 80% interest in the Kestrel Coal Mine, one of Australia’s largest producing underground coal mines, located 40 km north of Emerald in central Queensland, for up to USD 2.4 billion. The transaction remains subject to regulatory approvals, which are expected by the end of Q3 2026. The acquisition would expand Yancoal’s exposure to premium hard coking coal and strengthen its integration with Chinese steelmaker demand streams.

Global Metallurgical Coal Market Report Scope

Metallurgical coal is a high-carbon, low-impurity grade of coal used in primary steelmaking. When heated in the absence of oxygen, it converts into hard, porous coke, which serves as a reducing agent and fuel in blast furnaces to convert iron ore into iron.

The metallurgical coal market is segmented by product type, mining method, application, and geography. By product type, the market is segmented into hard coking coal, semi-soft and semi-hard coking coal, and pulverized coal injection (PCI) Coal. By mining method, the market is segmented into underground mining and surface mining. By application, the market is segmented into steel production, iron ore, and others. The report also covers market size and forecasts for metallurgical coal across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Hard Coking Coal |

| Semi-Soft and Semi-Hard Coking Coal |

| Pulverized Coal Injection (PCI) Coal |

| Underground Mining |

| Surface Mining |

| Steel Production |

| Iron Ore |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Hard Coking Coal | |

| Semi-Soft and Semi-Hard Coking Coal | ||

| Pulverized Coal Injection (PCI) Coal | ||

| By Mining Method | Underground Mining | |

| Surface Mining | ||

| By Application | Steel Production | |

| Iron Ore | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Metallurgical Coal Market?

The Metallurgical Coal Market size is projected to expand from USD 128.37 billion in 2025 and USD 132.46 billion in 2026 to USD 154.37 billion by 2031, registering a CAGR of 3.11% between 2026 to 2031.

Which region leads to demand for metallurgical coal?

Asia-Pacific leads with a 57.28% share in 2025 and is also the fastest-growing region, with a 4.21% CAGR through 2031.

Why does blast furnace steelmaking still support coal demand?

Blast furnaces still require coke as both a reducing agent and a structural input, which keeps coal demand tied to installed BF-BOF capacity.

Which product category is growing the fastest?

PCI Coal is the fastest growing product type, with a projected 3.87% CAGR through 2031 as steelmakers work to reduce coke intensity.

Page last updated on: