Mesh Wi-fi Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.82 Billion |

| Market Size (2031) | USD 13.34 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mesh Wi-fi Systems Market Analysis by Mordor Intelligence

The Mesh Wi-Fi system markets size is projected to expand from USD 7.23 billion in 2025 and USD 7.82 billion in 2026 to USD 13.34 billion by 2031, registering a CAGR of 11.27% between 2026 to 2031. Demand accelerates as single-router architectures struggle to serve today’s density of connected devices, prompting households and businesses to adopt multi-node topologies. Hardware still generates most revenue, yet subscription-based services tied to network security and AI optimization are reshaping vendor economics while lifting average revenue per user. Multi-band architectures are becoming the default because they segment traffic for 4K video, cloud gaming, and low-latency conferencing, avoiding bottlenecks that once characterized extender-based coverage. Regional momentum comes from telco fiber rollouts, government broadband funds, and the Matter 1.4.2 specification, which removes interoperability friction and lets one mesh platform control lights, thermostats, and cameras across brands. Together, these shifts confirm that the Mesh Wi-Fi system market is no longer a niche upgrade path but a baseline requirement for gigabit households and smart facilities.

Key Report Takeaways

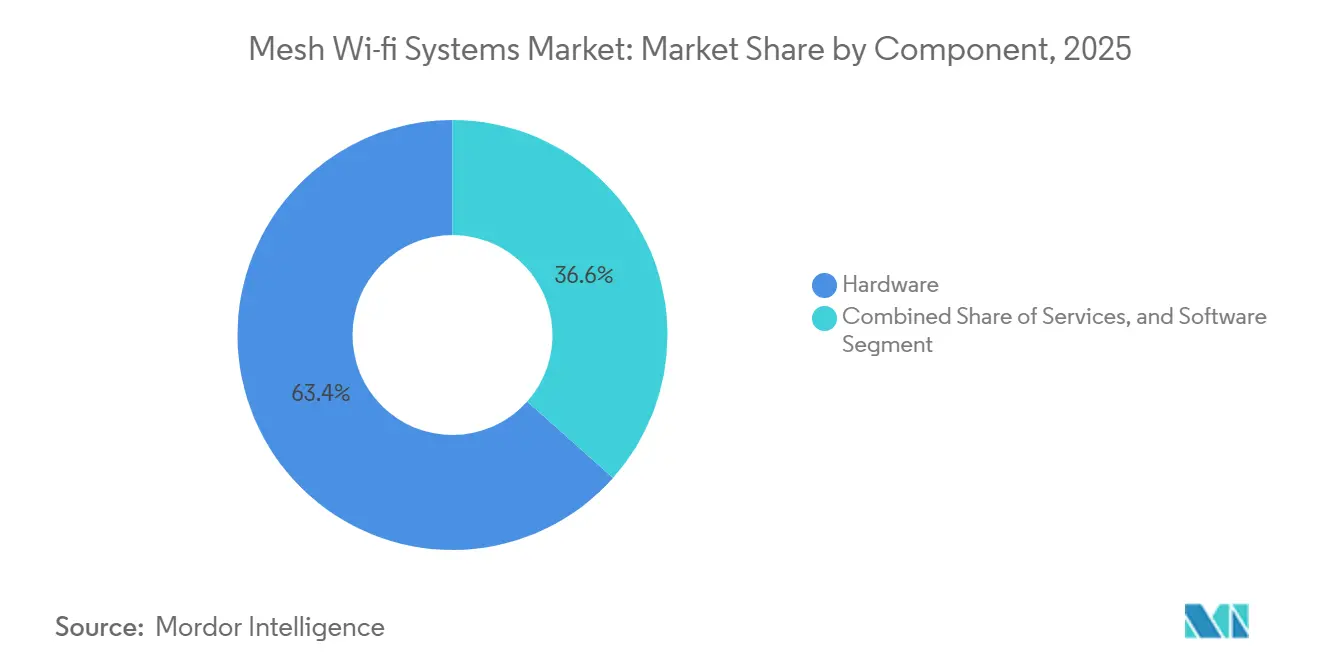

- By component, hardware led with 63.4% of the Mesh Wi-Fi systems market share in 2025, while services are forecast to grow at a 13.81% CAGR through 2031.

- By band count, dual-band products accounted for 48.19% of the Mesh Wi-Fi system market in 2025, yet quad-band and higher configurations are advancing at a 15.62% CAGR through 2031.

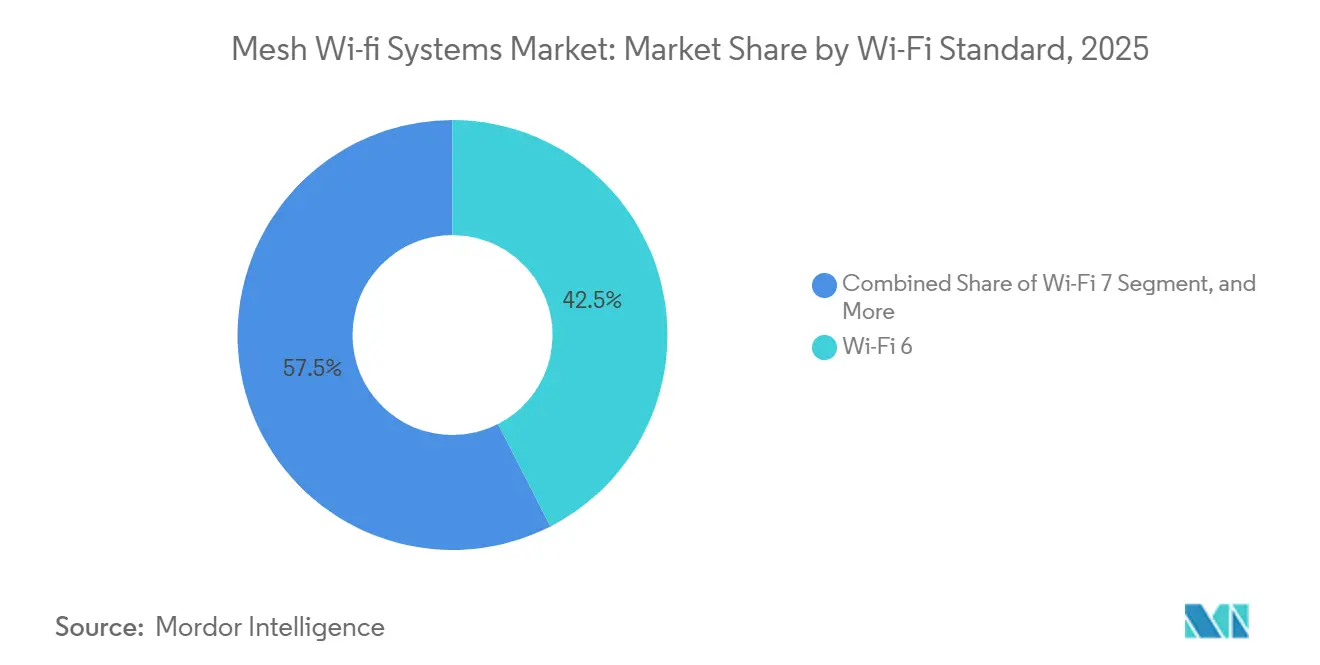

- By Wi-Fi standard, Wi-Fi 6 captured 42.47% share in 2025, whereas Wi-Fi 7 is projected to expand at a 17.41% CAGR over 2026-2031.

- By application, residential deployments held 57.32% share in 2025, while industrial and logistics installations are growing at a 14.64% CAGR through 2031.

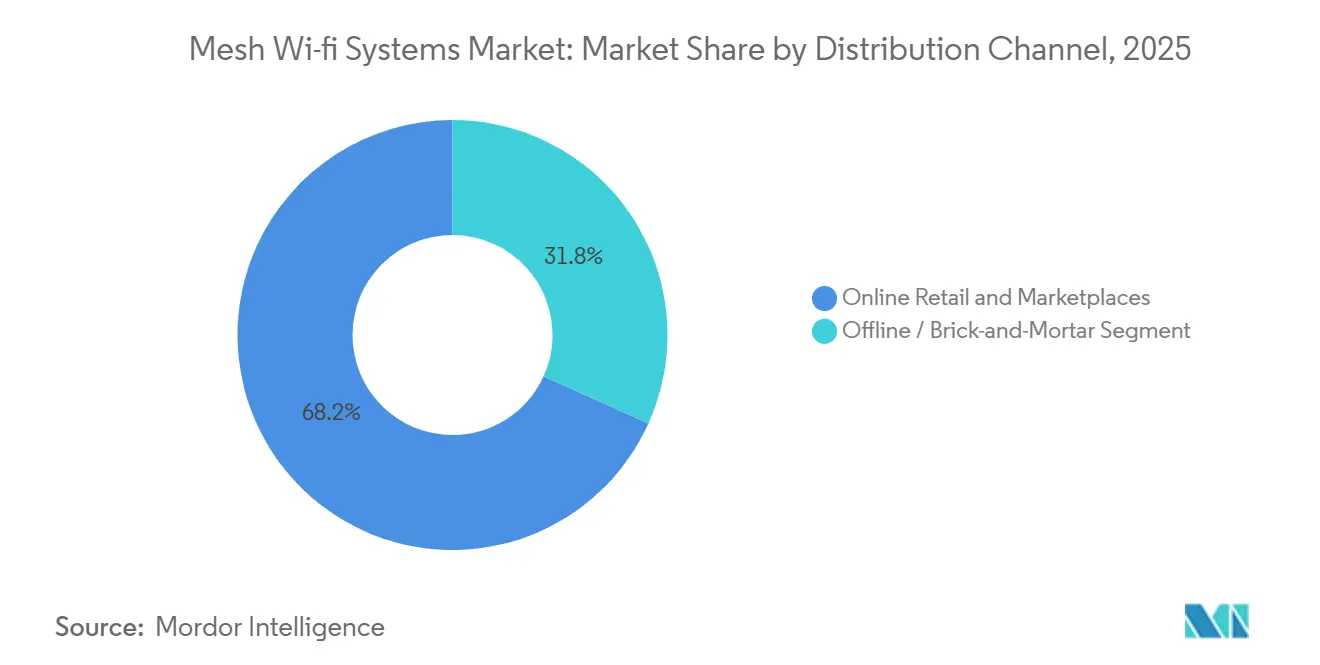

- By distribution channel, online retail and marketplaces dominated with 68.24% share in 2025 and will sustain a 12.94% CAGR to 2031

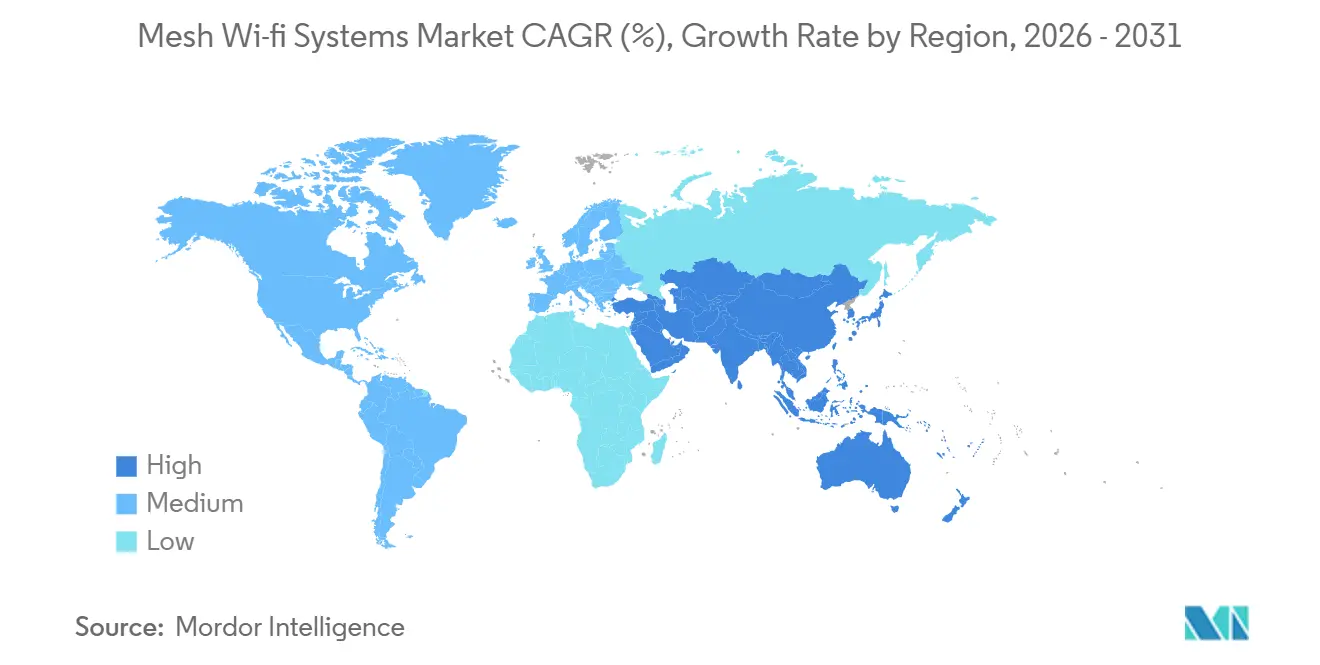

- By geography, North America commanded 38.96% share in 2025, whereas the Asia-Pacific is set to grow at a 14.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mesh Wi-fi Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth in Smart-Home Device Installations | +2.8% | Global, concentrated in North America, Western Europe, urban Asia-Pacific | Short term (= 2 years) |

| Rapid Roll-Out of Gigabit and Fibre-to-the-Home Internet | +2.5% | North America, Europe, China, South Korea, Japan | Medium term (2-4 years) |

| Price Erosion in Wi-Fi 6/6E Chipsets | +1.9% | Global, fastest in Asia-Pacific | Short term (= 2 years) |

| Telco Adoption of Mesh CPE for Whole-Home Coverage | +1.7% | North America, Western Europe, parts of Asia-Pacific | Medium term (2-4 years) |

| Government-Funded Digital-Inclusion Programs | +1.2% | United States, European Union, India | Long term (= 4 years) |

| AI-Driven Self-Healing Network Algorithms | +1.1% | Global, early in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in Smart-Home Device Installations

Households now host 15-20 connected devices, from speakers to appliances, all vying for bandwidth. Matter 1.4.2 certification across more than 500 devices lets homeowners unify control, so mesh systems become the logical backbone.[1]FTTH Council Europe, “FTTH Market Panorama 2025,” ftthcouncil.eu Compared with extenders, Thread-based mesh cuts packet loss by 40%, improving user satisfaction and slashing ISP support calls. As a result, retailers promote “whole-home bundles” that pair mesh kits with smart bulbs and locks. The Mesh Wi-Fi systems market, therefore, expands in lockstep with every incremental camera or voice assistant added to a residence.

Rapid Roll-Out of Gigabit and Fibre-to-the-Home Internet

Operators in South Korea, Japan, and large U.S. metros deliver symmetrical gigabit services that expose weak Wi-Fi links inside the home. To preserve promised speeds, telcos package mesh nodes into premium fiber plans, charging USD 5-10 per month and converting capital expenditure into subscription revenue. Europe’s 295 million homes passed by fiber, and China’s 206.8 million gigabit users repeat the pattern, proving that last-mile performance is now a competitive differentiator. Consequently, the Mesh Wi-Fi systems market captures value every time a new fiber strand reaches a front door.[2]Thread Group, “Thread Network Performance in Multi-Story Residential Environments,” threadgroup.org

Price Erosion in Wi-Fi 6/6E Chipsets

Second-generation silicon from Broadcom and Qualcomm shaved 25% off bill-of-materials costs in 2025, pushing tri-band kits below USD 300 retail. MediaTek’s Filogic 880 brought Wi-Fi 7 to mid-tier price points, letting brands like TP-Link release sub-USD 400 quad-band systems in Asia-Pacific. Lower entry costs broaden household adoption beyond early adopters, accelerating refresh cycles and nudging existing Wi-Fi 5 routers toward retirement. The effect funnels millions of mainstream buyers into the Mesh Wi-Fi system market each year.[3]NTIA, “BEAD Program State Allocations,” broadbandusa.ntia.doc.gov

Telco Adoption of Mesh CPE for Whole-Home Coverage

Comcast’s xFi Complete, Verizon’s Fios router upgrades, and European fiber bundles collectively push tens of millions of subscribers onto operator-branded mesh hardware. Churn falls once coverage issues disappear, so carriers can upsell parental controls and IoT management features. Vendors that pass stringent telco certification gain high-volume deals, while retail-only brands see shelf space shrink. This channel shift realigns bargaining power and injects recurring revenue into the Mesh Wi-Fi system market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Semiconductor Supply Constraints | -1.4% | Global, with acute impact in Asia-Pacific manufacturing hubs (Taiwan, South Korea) | Short term (≤ 2 years) |

| Rising Cyber-Security Vulnerabilities in Home Networks | -0.9% | Global, with heightened regulatory focus in North America and Europe | Medium term (2-4 years) |

| Consumer Confusion Over Wi-Fi Standards (6E vs 7) | -0.7% | Global, with pronounced impact in North America and Western Europe where multiple standards coexist | Short term (≤ 2 years) |

| Import Tariffs on Networking Hardware | -0.6% | United States, European Union, select Asia-Pacific markets with protectionist trade policies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Supply Constraints

Advanced 6 nm and 5 nm semiconductor capacity remains constrained as smartphone and data-center customers outcompete consumer networking vendors for wafer allocation. Wi-Fi 7 chipsets carry a 40-50% cost premium over Wi-Fi 6E, forcing vendors to prioritize flagship mesh systems and delay broader portfolio rollouts. Lead times extending beyond 30 weeks strain working capital, disrupt inventory planning, and limit peak-season availability. Until additional fabrication capacity comes online, supply bottlenecks will continue to suppress unit shipments, delay price normalization, and moderate near-term growth in the Mesh Wi-Fi systems market.

Rising Cyber-Security Vulnerabilities in Home Networks

Mirai botnet variants exploited default credentials in January 2025, prompting proposed FCC labeling rules that require five-year security support for connected devices. Implementing secure boot, encrypted firmware updates, and formal vulnerability disclosure programs increases engineering costs and operational complexity, disproportionately impacting smaller vendors. By end-2025, only 60% of new nodes shipped with WPA3, leaving a meaningful installed base exposed to legacy vulnerabilities. Rising consumer awareness of security risks can delay upgrade cycles and purchasing decisions, creating short-term demand friction and moderating growth momentum in the Mesh Wi-Fi system market.[4]CISA, “Alert AA25-010A: Mirai Botnet Variants Targeting Consumer Routers,” cisa.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Monetize a Hardware Foundation

Hardware accounted for 63.4% of the Mesh Wi-Fi market share in 2025, as customers still purchase physical nodes as the first step toward reliable coverage. Yet service revenue, growing at a 13.81% CAGR, signals a pivot to recurring revenue as ISPs and vendors sell security subscriptions, parental controls, and analytics. The Mesh Wi-Fi systems market size tied to services is projected to outpace hardware incrementally each year between 2026 and 2031 as telcos bake USD 5-15 monthly charges into fiber bundles.

Software innovation underpins this shift. Cloud dashboards give homeowners device-level visibility, while AI engines orchestrate channel selection without user input. Vendors that master over-the-air updates and data analytics increase lifetime customer value, mitigating the 4- to 5-year replacement cycle that still governs node refreshes. The winner’s playbook, therefore, combines affordable hardware with sticky cloud features that users pay for long after the initial install.

By Band Count: Quad-Band Rises to Meet High-Density Demand

Dual-band kits held 48.19% share of the Mesh Wi-Fi system market in 2025 because cost-sensitive buyers needed only 2.4 GHz and 5 GHz coverage for email, streaming, and smart speakers. As bandwidth demand balloons, tri-band models add a second 5 GHz radio for dedicated backhaul, balancing price and performance. Quad-band systems are now expanding at a 15.62% CAGR, leveraging 6 GHz channels unlocked by global regulators.

With Wi-Fi 7, vendors dedicate one 6 GHz radio to backhaul and a second to clients, while legacy devices remain on 2.4 GHz and 5 GHz. Interference drops, latency sinks, and 8K streaming coexist with cloud gaming. As chipset pricing falls, quad-band premiums narrow, nudging power users, remote workers, and gamers toward higher-tier bundles. The Mesh Wi-Fi systems market size for quad-band products is therefore set to grow faster than any other configuration through 2031.

By Wi-Fi Standard: Wi-Fi 7 Becomes the Aspirational Upgrade

Wi-Fi 6 captured 42.47% share in 2025 due to its mature ecosystem of smartphones and laptops, but Wi-Fi 7’s 17.41% CAGR makes it the headline growth engine. Features such as 320 MHz channels and multi-link operation aggregate bandwidth across three bands, halving latency in congested neighborhoods. Early adopters install Wi-Fi 7 mesh to future-proof against augmented reality workloads and real-time collaboration tools.

Wi-Fi 6E remains a bridge technology for buyers who want 6 GHz access at a lower cost. Wi-Fi 5 is available only in entry-level SKUs and emerging markets, and chipset vendors are already reallocating wafer starts to newer standards. As consumer devices with Wi-Fi 7 radios proliferate, the market share of older Wi-Fi protocols in the Mesh Wi-Fi system market will steadily compress, cementing Wi-Fi 7 as the de facto standard by the end of the decade.

By Application: Industrial and Logistics Post Double-Digit Growth

Residential deployments accounted for 57.32% of 2025 revenue, driven by work-from-home trends and the proliferation of smart-home gadgets across suburbs and cities. Yet warehouses, distribution centers, and factories will post a 14.64% CAGR by 2031, overtaking corporate offices as the fastest-moving vertical. Battery-powered scanners and autonomous guided vehicles roam vast concrete spaces, making seamless roaming a mission-critical requirement.

The Mesh Wi-Fi systems market size for industrial premises is expected to grow as operators replace legacy AP grids that suffered from dead spots and hand-off delays. Vendors differentiate through ruggedized enclosures, extended temperature ratings, and support for time-sensitive networking. Government and public buildings also adopt mesh under digital-inclusion grants, ensuring full-campus coverage in libraries and schools with complex layouts.

By Distribution Channel: Online Retail Keeps Its Lead

Online marketplaces accounted for 68.24% of Mesh Wi-Fi system revenue in 2025 and will maintain a 12.94% CAGR through 2031. Algorithm-driven recommendations, time-bound discounts, and bundle promotions make e-commerce the most efficient path to scale. Offline electronics chains still serve tactile shoppers, yet showrooming behavior erodes margins as customers test in-store then buy online.

Telco retail physical stores and carrier websites form a hybrid model that locks subscribers into multi-year contracts, with mesh hardware rolled into monthly bills. Direct-to-consumer brands leverage their own portals for higher margins, while social commerce in Asia-Pacific introduces live demonstrations that convert instantly within the app. The Mesh Wi-Fi system market, therefore, evolves into a multi-channel battlefield where convenience, not shelf space, decides winners.

Geography Analysis

North America generated 38.96% of the Mesh Wi-Fi systems market revenue in 2025, underpinned by gigabit fiber coverage, smart-home penetration, and telco mesh bundles that now serve tens of millions of subscribers. The United States dominates regional value, backed by USD 42.45 billion in BEAD program funding that supports networks in every state. Canada’s 12 million fiber homes and CAD 10 (USD 7.90) monthly managed Wi-Fi premiums add steady uptake, while Mexico’s 8 million FTTH lines cluster mesh demand in its three largest cities.

Europe follows, buoyed by 160 million fiber subscribers and a 54% take-up rate that spotlights the inadequacy of legacy routers once speeds exceed 1 Gbps. Operators such as Deutsche Telekom and Orange integrate mesh networking into gigabit plans, while the EU’s Cyber Resilience Act requires 5-year security support, boosting consumer trust. Russia deploys distributed nodes in concrete apartment blocks, highlighting how building stock shapes architectural choices in the Mesh Wi-Fi market.

Asia-Pacific is the fastest climber at a 14.28% CAGR, propelled by China’s 206.8 million gigabit users and India’s BharatNet project linking 250,000 villages. Japan’s 85% fiber penetration and South Korea’s 95% FTTH reach foster early adoption of Wi-Fi 7, as gamers demand stable, low-latency links. Southeast Asian capitals layer mesh onto new fiber backbones priced below USD 150 per kit, pushing affordable coverage into rising middle-class homes. Outside the top three regions, the Middle East modernizes broadband for Saudi Vision 2030, South America scales slowly amid macroeconomic stress, and sub-Saharan Africa remains early-stage, favoring 4G fixed wireless over FTTH for now.

Competitive Landscape

The Mesh Wi-Fi system market is moderately fragmented. NETGEAR, TP-Link, and Amazon’s Eero anchor the retail tier, while Xiaomi, Huawei, and Tenda leverage integrated smart-home ecosystems and aggressive sub-USD 200 price points to expand in Asia-Pacific and Latin America. Carrier-certified specialists such as CommScope and Zyxel secure high-volume contracts that guarantee remote management and security compliance, thereby insulating their share from price wars in big-box retail.

Strategic momentum centers on vertical integration and recurring revenue. Amazon bundles Eero with Alexa and Prime, driving lock-in beyond hardware. NETGEAR captures annuity streams by pairing Armor security subscriptions at USD 99 annually with every Orbi sale. Qualcomm and Broadcom supply Wi-Fi 7 chipsets with on-device AI, letting vendors market “self-healing” networks that reduce support calls by up to 30%. Smaller brands confront rising regulatory costs from WPA3 and secure-boot mandates, which raise the bar for firmware maintenance and accelerate consolidation.

The industrial and logistics segments offer white-space potential because few vendors offer IP67-rated, extended-temperature mesh nodes. Ubiquiti targets prosumers and small businesses with affordable yet scalable architectures, while Vilo Living adopts a direct-to-consumer model that sidesteps traditional distribution fees. Overall, competitive differentiation gravitates toward cloud analytics, AI optimization, and security guarantee length rather than raw throughput alone.

Mesh Wi-fi Systems Industry Leaders

NETGEAR Inc.

TP-Link Corporation Limited

Google LLC

Eero LLC

ASUStek Computer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TP-Link introduced the Deco BE85 Wi-Fi 7 quad-band mesh kit, promising 50% lower latency than Wi-Fi 6E in congested homes.

- November 2025: Qualcomm unveiled the FastConnect 7900 Wi-Fi 7 chipset with integrated AI that extends battery life for portable mesh nodes by 30%.

- September 2025: Google Nest partnered with U.S. ISPs to bundle its Nest Wifi Pro 6E mesh with gigabit fiber plans at USD 10 monthly for managed service.

- July 2025: NETGEAR launched the Orbi 970 quad-band Wi-Fi 7 system delivering 27 Gbps aggregate throughput and shipping with Armor security.

Global Mesh Wi-fi Systems Market Report Scope

The Mesh Wi-Fi systems market comprises hardware, software, and associated services that enable seamless, whole-home or enterprise wireless connectivity through multiple interconnected nodes operating as a unified network. Unlike traditional single-router setups, mesh systems use distributed nodes with dynamic routing, self-healing capabilities, and centralized management to eliminate dead zones and optimize bandwidth across devices. The market includes dual-band, tri-band, and quad-band configurations across standards such as Wi-Fi 5, 6, 6E, and 7, serving residential, commercial, and industrial use cases, with growing integration of cloud management, security subscriptions, and AI-driven network optimization.

The Mesh Wi-Fi System Market Report is Segmented by Component (Hardware, Software, and Services), Band Count (Dual-Band, Tri-Band, Quad-Band and Higher), Wi-Fi Standard (Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Application (Residential, Commercial and Enterprise, Industrial and Logistics, and Government and Public Sector), Distribution Channel (Online Retail and Marketplaces, Offline/Brick-and-Mortar), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Dual-Band Mesh Systems |

| Tri-Band Mesh Systems |

| Quad-Band and Higher Mesh Systems |

| Wi-Fi 5 (802.11ac) |

| Wi-Fi 6 (802.11ax) |

| Wi-Fi 6E (802.11axe) |

| Wi-Fi 7 (802.11be) |

| Residential |

| Commercial and Enterprise |

| Industrial and Logistics |

| Government and Public Sector |

| Online Retail and Marketplaces |

| Offline / Brick-and-Mortar |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Oceania | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| North Africa | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Band Count | Dual-Band Mesh Systems | |

| Tri-Band Mesh Systems | ||

| Quad-Band and Higher Mesh Systems | ||

| By Wi-Fi Standard | Wi-Fi 5 (802.11ac) | |

| Wi-Fi 6 (802.11ax) | ||

| Wi-Fi 6E (802.11axe) | ||

| Wi-Fi 7 (802.11be) | ||

| By Application | Residential | |

| Commercial and Enterprise | ||

| Industrial and Logistics | ||

| Government and Public Sector | ||

| By Distribution Channel | Online Retail and Marketplaces | |

| Offline / Brick-and-Mortar | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Oceania | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| North Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the Mesh Wi-Fi systems market expected to grow between 2026 and 2031?

The Mesh Wi-Fi systems market size is projected to reach USD 13.34 billion by 2031, advancing at an 11.27% CAGR over 2026-2031, according to Mordor Intelligence.

Which component segment is expanding the quickest?

Services revenue tied to managed Wi-Fi and security subscriptions is growing at 13.81% CAGR, the fastest among all components, per Mordor Intelligence.

What share do online retailers hold in global sales?

Online retail and marketplaces commanded 68.24% of Mesh Wi-Fi system market share in 2025, leading all channels, per Mordor Intelligence.

Which Wi-Fi standard will dominate new mesh deployments by 2031?

Wi-Fi 7 is forecast to grow at 17.41% CAGR and is positioned to become the prevailing standard for next-generation mesh networks.

Why are telcos important to mesh Wi-Fi adoption?

Operators bundle carrier-grade mesh CPE with fiber subscriptions, reducing churn and creating recurring revenue, which steers significant volume into the Mesh Wi-Fi system market.

Which region shows the highest growth potential?

Asia-Pacific is projected to post a 14.28% CAGR through 2031, fueled by massive fiber build-outs in China and India, according to Mordor Intelligence.

Page last updated on: