Memory Fabric Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

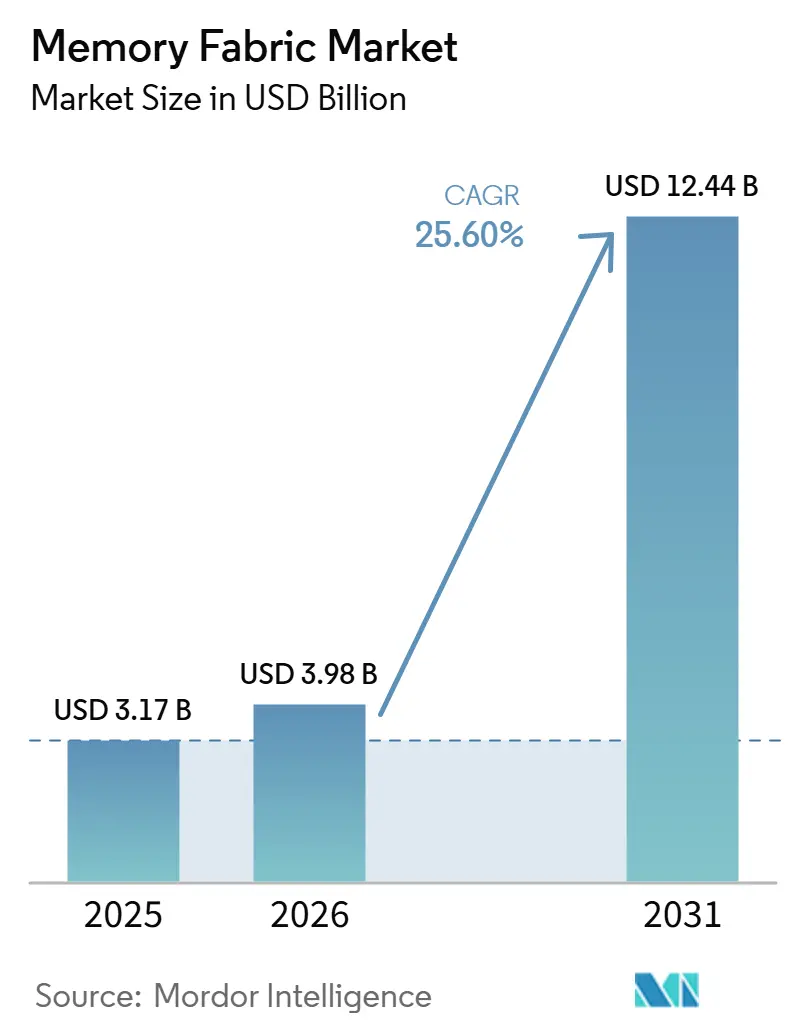

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 12.44 Billion |

| Growth Rate (2026 - 2031) | 25.60% CAGR |

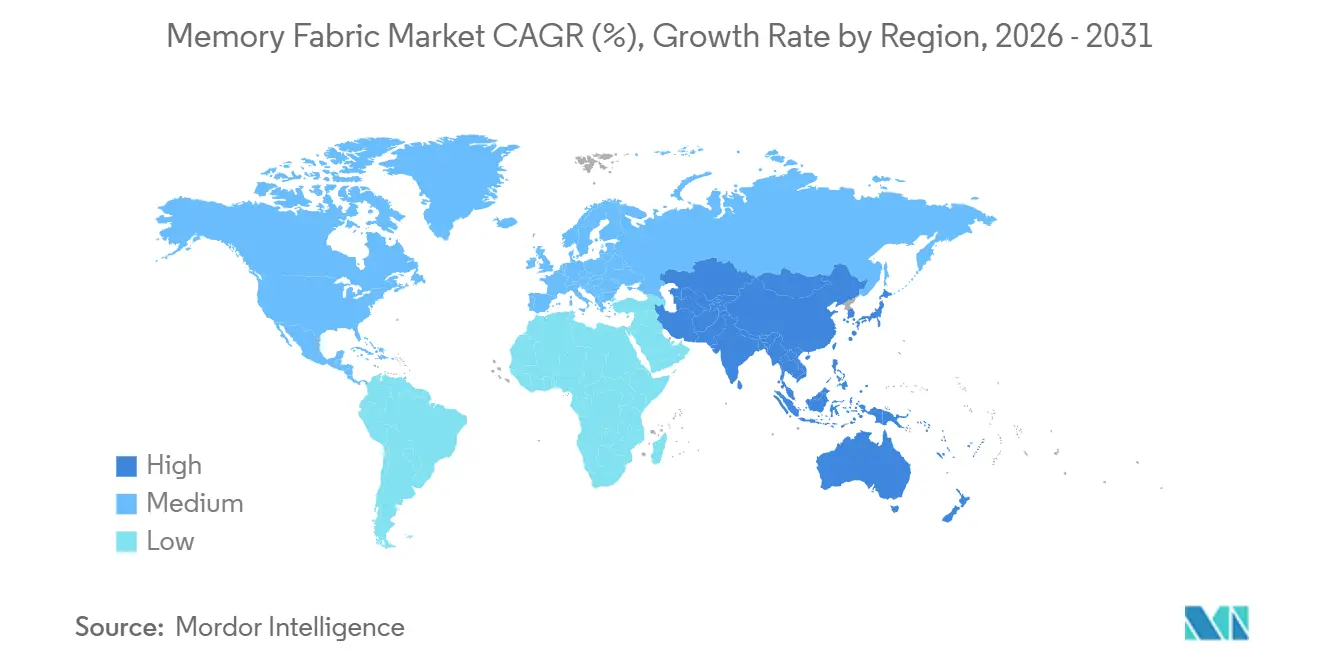

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

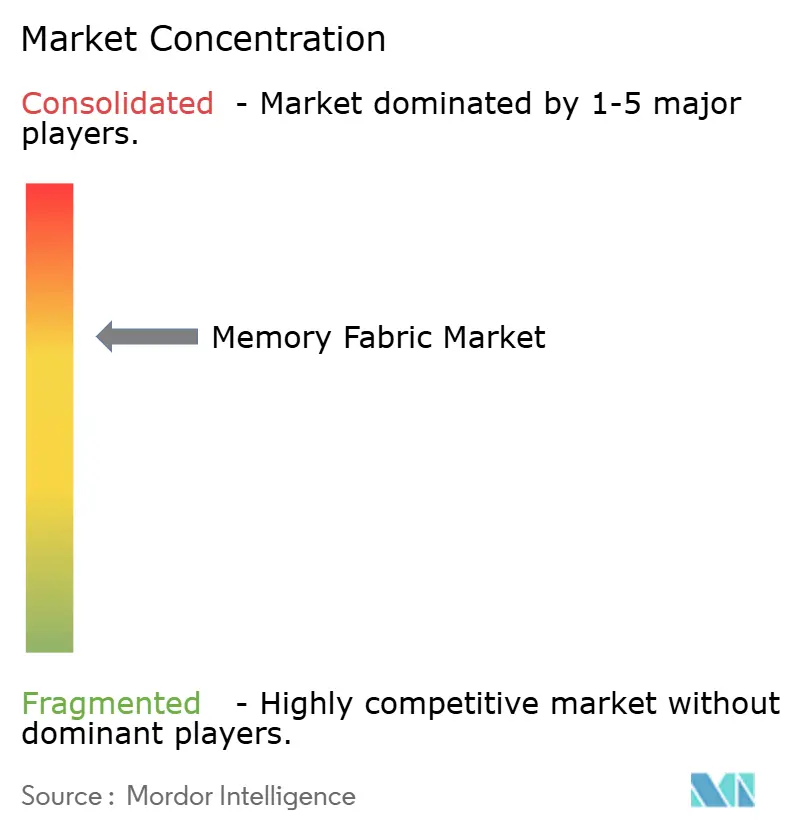

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Memory Fabric Market Analysis by Mordor Intelligence

The memory fabric market size is projected to expand from USD 3.17 billion in 2025 and USD 3.98 billion in 2026 to USD 12.44 billion by 2031, registering a CAGR of 25.60% between 2026 to 2031. Growth in the memory fabric market is being driven by a persistent bandwidth gap in AI systems, where larger models, longer context windows, and heavier inference traffic keep raising pressure on memory movement rather than only on raw compute. The memory fabric market is also widening through CXL adoption, because disaggregated and pooled memory adds a second demand path that is not tied only to stacked HBM upgrades. Asia-Pacific remains central to the memory fabric market because production capacity, advanced packaging capability, and hyperscaler buildouts are concentrated in the same regional system. Competition in the memory fabric market is becoming sharper as Samsung, SK hynix, and Micron have all moved into HBM4 production plans, which reduces single-vendor advantage and shifts attention toward yield, interoperability, and time to qualification. This keeps the memory fabric market closely tied to platform validation, open standards maturity, and the ability of suppliers to scale advanced packaging without slowing deployment cycles.

Key Report Takeaways

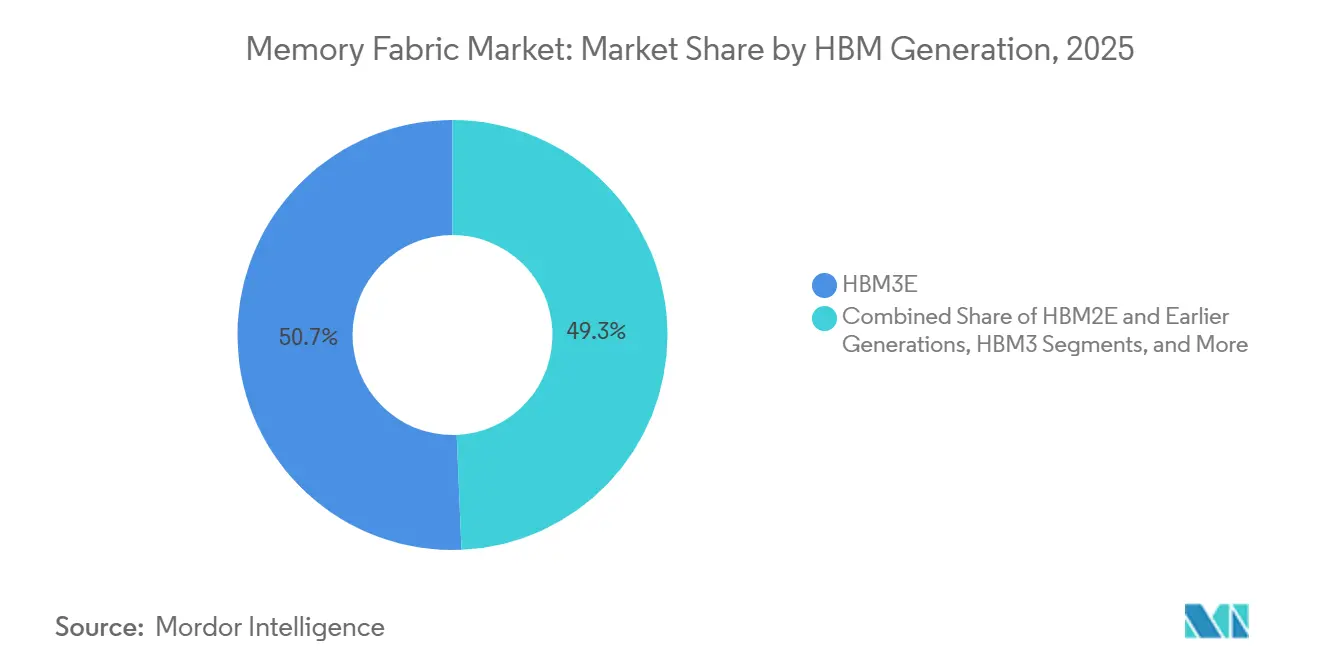

- By HBM generation, HBM3E held 50.67% share of the memory fabric market in 2025, while HBM4E and next-generation HBM are projected to expand at a 26.46% CAGR through 2031.

- By stack height, 8-High led with 42.37% share of the memory fabric market in 2025, while 16-High and Above are expected to grow at a 26.79% CAGR through 2031.

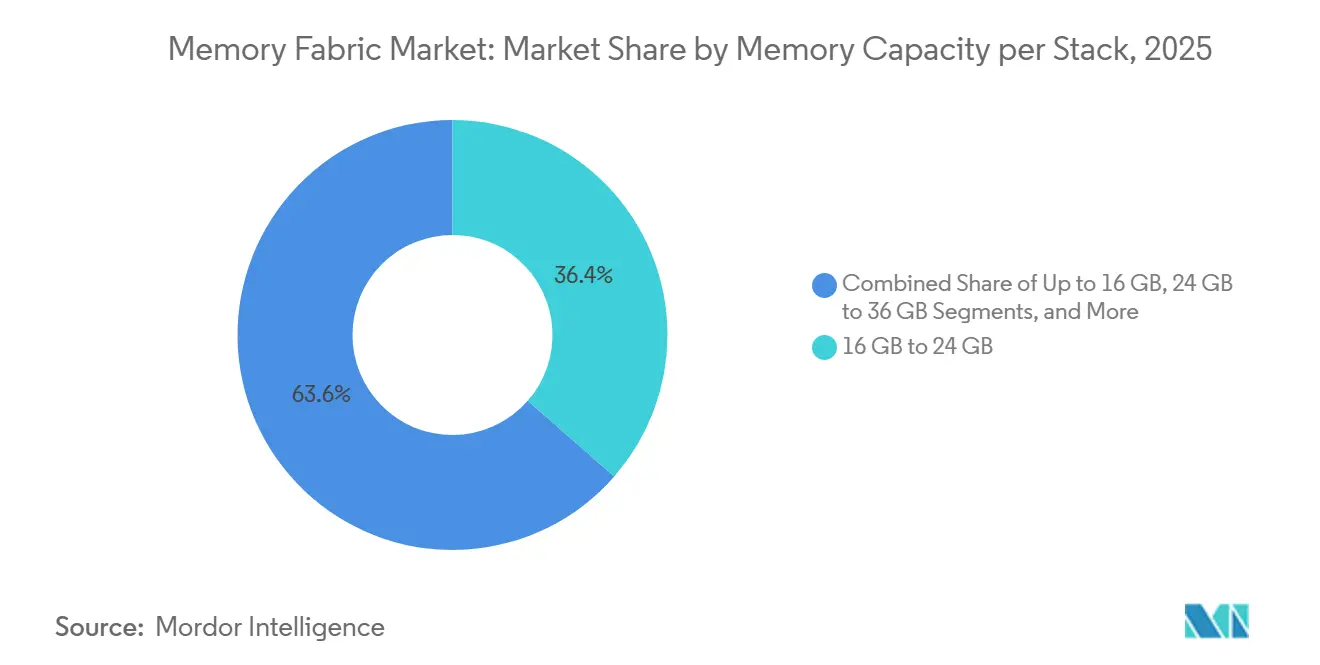

- By memory capacity per stack, the Above 16 GB to 24 GB band accounted for 36.44% share of the memory fabric market in 2025, while the Above 36 GB tier is projected to advance at a 27.12% CAGR through 2031.

- By advanced packaging integration architecture, 2.5D silicon-interposer-based integration captured 80.24% share of the memory fabric market in 2025, while 3D Logic-Memory Integration is expected to expand at a 26.88% CAGR through 2031.

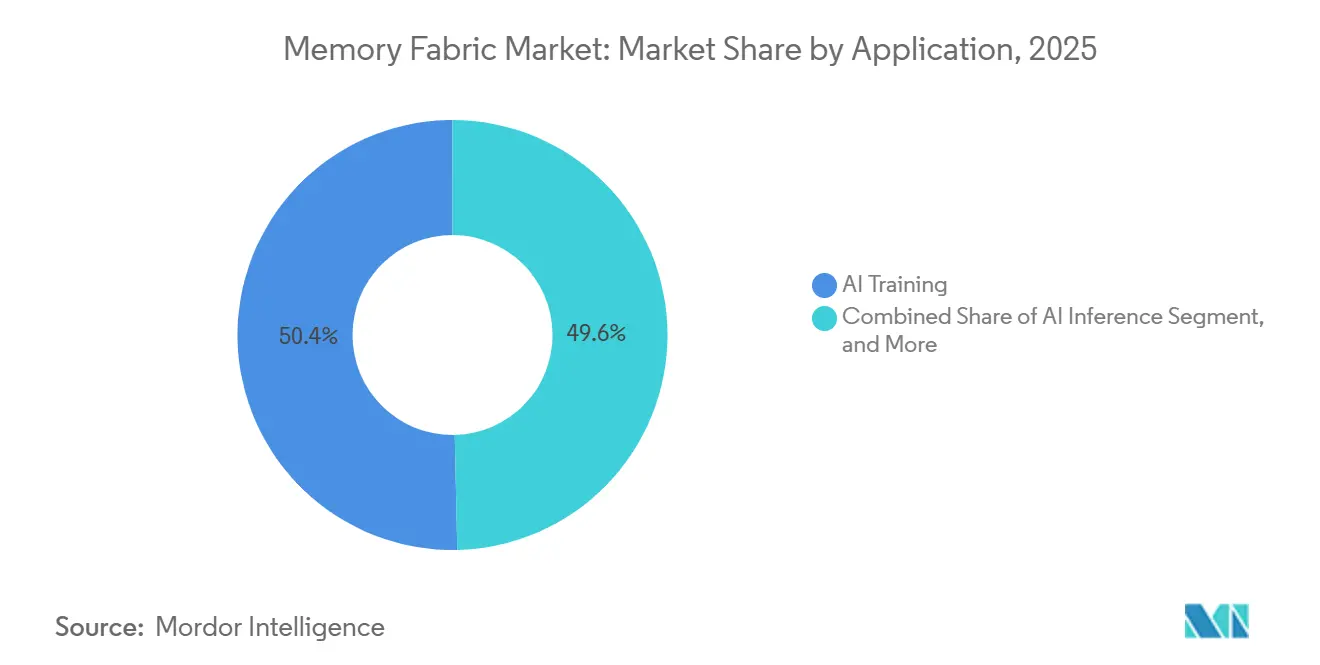

- By application, AI Training accounted for 50.36% of the memory fabric market size in 2025, while AI Inference is projected to grow at a 27.24% CAGR through 2031.

- By end user, hyperscalers and cloud service providers held 46.54% share in 2025, while AI Cloud and GPU-as-a-Service providers are expected to expand at a 27.16% CAGR through 2031.

- By geography, Asia-Pacific held 42.33% share of the memory fabric market in 2025 and is projected to grow at a 27.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Memory Fabric Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Artificial Intelligence Inference Memory Bottlenecks | +8.0% | Global, with highest intensity in North America and APAC core | Short term (≤ 2 years) |

| CXL-Based Memory Pooling Reduces Stranded Capacity | +5.2% | North America and Europe, early APAC adoption accelerating | Medium term (2-4 years) |

| Total Cost of Ownership Pressure In Hyperscale Data Centers | +4.1% | Global, North America and APAC core | Medium term (2-4 years) |

| Open Standards Adoption Across CPU, Memory, And Switch Vendors | +3.5% | Global | Long term (≥ 4 years) |

| Brownfield Server Refresh Needs For Memory Expansion | +1.9% | North America and Europe | Short term (≤ 2 years) |

| Emergence of Memory-As-A-Service Architectures | +1.4% | North America, with early gains in APAC and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Artificial Intelligence Inference Memory Bottlenecks Drive HBM Bandwidth Demand

The shift from model training toward large-scale inference is pushing the memory fabric market into a phase where bandwidth and latency matter as much as accelerator count. Micron reported that agentic AI workloads place sharply higher pressure on key-value cache movement, with KV-cache demand reaching 6.07x baseline at 10,000 concurrent requests, which shows why memory pressure rises faster as concurrency increases.[1]Micron Technology, “Agentic AI in Data Centers and the Role of HBM,” Micron Technology, micron.com The same paper showed that HBM4 delivers 2.82x higher peak theoretical bandwidth than HBM3E and supports throughput gains of up to 2.63x for agentic AI workloads at fixed compute budgets. Samsung also stated that its commercial HBM4 reached 3.3 TB/s per stack, which confirms that suppliers are already aligning products to this new demand profile.[2]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com As context lengths and request volumes keep rising together, the memory fabric market is being pulled by a recurring procurement need instead of a one-time refresh. That pattern gives the memory fabric market a demand base that stays active even when compute upgrades alone no longer solve real deployment bottlenecks.

CXL-Based Memory Pooling Reduces Stranded Capacity In Hyperscale Environments

CXL pooling is giving the memory fabric market a separate expansion path because it addresses unused memory capacity that remains locked inside underutilized servers. A 2025 IEEE Transactions on Parallel and Distributed Systems paper noted that memory can represent up to 44% of the total cost of ownership in typical compute servers, and it showed that CXL memory tiering can improve throughput by up to 1.7x for production workloads through dynamic reallocation across co-located containers.[3]Shan et al., “Equilibria: Fair Multi-Tenant CXL Memory Tiering at Scale,” IEEE Transactions on Parallel and Distributed Systems, doi.org That result matters because it changes memory from a fixed local asset into a shared infrastructure resource, which improves utilization without requiring all workloads to sit on the highest-cost local DRAM footprint. Marvell added switch-layer support to this direction with its Structera S 30260, which delivers 4 TB/s aggregate bandwidth and sub-microsecond memory access latency for rack-scale pooling designs. This means HBM demand at the hot tier and CXL pooling at the broader capacity tier can expand together rather than replace one another. As a result, the memory fabric market is increasing not only by faster stacks, but also by wider system architectures that can reuse and redistribute memory more efficiently.

Total Cost Of Ownership Pressure In Hyperscale Data Centers Accelerates Adoption

The memory fabric market is also rising because hyperscalers are treating memory efficiency as a direct capital and operating cost issue. The same IEEE TPDS work showed that memory can account for up to 44% of compute server TCO, which makes bandwidth efficiency and memory sharing important purchase criteria rather than secondary design choices. Samsung stated that its HBM4 offers a 40% power efficiency improvement over HBM3E, which strengthens the case for a new generation upgrade even before pure performance is considered. Applied Materials introduced HBM-focused PECVD, CMP, and ECD systems in June 2026 to improve yield in 12-High and 16-High stack production, which shows that cost pressure is also shaping equipment innovation. When supplier roadmaps have to improve yield, thermal behavior, and energy efficiency at the same time, the memory fabric market becomes tied to total platform economics, not only to raw technical performance. That is why the memory fabric market is benefiting from a wider spending logic that reaches from data centers into packaging and manufacturing tools.

Open Standards Adoption Across CPU, Memory, And Switch Vendors Enables Interoperability

Open standards are making the memory fabric market easier to scale because they reduce platform lock-in across processors, controllers, switches, and memory devices. The Compute Express Link Consortium stated that CXL enables load and store access to disaggregated memory at sub-microsecond latency, which is close enough to local memory behavior for many analytics and database uses. Intel said its Xeon 6 platforms support 96 lanes of PCIe Gen 5 and CXL natively, which gives ecosystem vendors a large CPU-side anchor for active procurement cycles. JEDEC HBM4 alignment across Samsung, SK hynix, and Micron also points to a more stable multi-vendor supply base at the top end of the stack, and the 2026 ISSCC paper confirmed a 36 GB 3.3 TB/s HBM4 design with deeper calibration and test features at the silicon level. Standards do not remove qualification work, but they make qualification more repeatable and less dependent on one vendor pair at a time. Over time, that reduces entry friction for the memory fabric market and allows each new generation to reach more system designs with less duplicated validation effort.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Commercial Availability of Advanced CXL Generations | -3.0% | Global | Short term (≤ 2 years) |

| Integration Complexity across Hardware, Firmware, and Software Stacks | -2.3% | Global | Medium term (2-4 years) |

| Validation and Interoperability Risk across Multi-Vendor Ecosystems | -1.7% | Global, with APAC core most affected by multi-tier qualification | Medium term (2-4 years) |

| High Dependency on Data Center Refresh Cycles and Capex Approval | -1.2% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Commercial Availability Of Advanced CXL Generations Constrains Near-Term Adoption

The memory fabric market still faces a timing constraint because the most advanced CXL generations are not yet in full commercial server deployment. The input shows that CXL 3.0 remained in sampling and early qualification through mid-2026, which limited real 2026 revenue mostly to CXL 2.0 single-host memory expansion. Marvell stated that customer sampling for its Structera S 30260 CXL 3.0 switch begins in Q3 2026, which means full rack-scale memory fabrics still depend on broader CPU and memory-expander readiness. The CXL Consortium also continues to run plugfests and conformance programs, and that adds platform-level qualification cycles before broad deployment can move ahead. This timing gap delays the higher-value pooling and sharing cases that would otherwise widen the memory fabric market faster in the short term. It also keeps enterprise adoption behind hyperscaler adoption, because larger operators can absorb qualification delays more easily within ongoing infrastructure programs.

Integration Complexity Across Hardware, Firmware, And Software Stacks Slows Deployment

The memory fabric market is also limited by the fact that deployment requires coordination across silicon, firmware, and software at the same time. A 2026 USENIX NSDI paper on switched CXL memory pooling identified 3 distinct contention points, namely intra-host contention, in-fabric congestion, and unmanaged host-to-remote DIMM interaction, which all require active transport management beyond standard PCIe quality-of-service methods. That means implementation is not only a hardware purchase, because platform software, BIOS behavior, operating system drivers, and policy controls must also be tuned for stable production use. The input shows that such complexity is manageable for hyperscalers, but much harder for mid-market enterprises that do not build custom tuning and integration teams. This slows the enterprise wave for the memory fabric market even when the technical standard is already available. It also explains why early adoption remains concentrated among well-funded cloud providers and advanced infrastructure operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Generation: HBM4E Supplants Entrenched HBM3E Leadership

HBM4E and next-generation HBM are projected to grow at the fastest CAGR of 26.46% through 2031, while HBM3E held 50.67% of the memory fabric market share in 2025. That mix reflects a market in transition, where current revenue is still anchored in the installed base, but future demand is already shifting toward faster and denser stacks. The memory fabric market kept HBM3E in a leading position because many training clusters deployed in 2024 and 2025 continue to run on normal 3-5 year refresh cycles. Those systems still meet the needs of many active deployments, especially where procurement has already been locked to HBM3E-based accelerator platforms. At the same time, the memory fabric market is clearly being pulled toward HBM4-class products by next-generation AI accelerator roadmaps.

SK hynix said in June 2026 that it shipped 12-layer HBM4E samples with 16 Gbps per pin, 48 GB capacity, more than 20% better power efficiency, and 17% lower heat resistance than HBM4 through Advanced MR-MUF packaging. Samsung stated that commercial HBM4 shipments began in February 2026, and Micron stated at GTC 2026 that it entered high-volume HBM4 production for NVIDIA Vera Rubin with 36 GB 12-High stacks and bandwidth above 2.8 TB/s. The ISSCC 2026 paper also showed how HBM4 is bringing more calibration and test sophistication into the die itself, which points to a deeper technical jump than a routine bandwidth lift. Older HBM3, HBM2E, and earlier generations remain in legacy HPC, professional visualization, and other lower-bandwidth environments, but their role inside the memory fabric industry is narrowing as platform roadmaps move upward. The manufacturing dependency is also changing, because HBM4 uses a 4 nm logic base die, which ties production readiness more closely to advanced foundry capacity than earlier generations did.

By Stack Height: 16-High Configurations Lead Next-Generation Capacity Scaling

The 16-High and Above segment is projected to grow at a 26.79% CAGR through 2031, while the 8-High configuration held 42.37% share in 2025. The 8-High format stayed dominant because it aligned with the HBM3E 24 GB standard that powered a large part of the installed AI accelerator base through 2025. That gave the memory fabric market a stable commercial geometry with established yields, packaging familiarity, and broad deployment history. The 12-High tier now represents the main HBM4 production sweet spot, especially for 36 GB stacks entering commercial volumes in 2026 and 2027. Even so, platform requirements are moving beyond what 12-High can deliver when customers want 48 GB and larger capacities per stack.

Samsung stated that it shipped 48 GB 16-High HBM4 samples in 2026, and Micron also shipped 48 GB 16-High HBM4 samples, which confirms that the format has moved from the roadmap stage into customer validation. Applied Materials added that its Producer Avila 2 PECVD system was designed to support reliable stacking at 12-High, 16-High, and future high-layer-count structures, which shows how yield support is moving in step with stack height ambition. The 4-High and Below tier still has a place in edge AI inference and cost-sensitive deployments, but its share is shrinking as mainstream accelerator designs demand more capacity. The memory fabric market is therefore shifting from a geometry led by commercial comfort toward one led by platform need. That change matters because higher stacks increase both revenue opportunity and process difficulty across the supply chain.

By Memory Capacity Per Stack: Demand Migrates Above 36 GB As AI Models Scale

The Above 36 GB tier is projected to grow at a 27.12% CAGR through 2031, while the 16 GB to 24 GB band held 36.44% share in 2025. The leading 2025 band reflected the strong installed base of HBM3E 24 GB 8-High products used in AI training clusters. That installed base gave the memory fabric market broad near-term volume in a capacity range that had already reached commercial comfort. The current transition is being driven by larger key-value caches, longer context windows, and rising model weight volumes, all of which increase the memory footprint required per accelerator. As a result, higher-capacity stacks are moving from premium options into mainstream planning assumptions for next-wave AI infrastructure.

Micron shipped 48 GB 16-High HBM4 samples in 2026, while SK Hynix stated that its HBM4E reaches 48 GB in a 12-High configuration through Advanced MR-MUF packaging. The Above 24 GB to 36 GB range now represents the main HBM4 commercial band, because 36 GB 12-High stacks are the clearest production-ready format in 2026. The Up to 16 GB segment still matters in embedded AI, professional graphics, and cost-sensitive designs, but it is losing strategic weight as mainstream AI workloads scale upward. The memory fabric market size for the Above 36 GB tier is being shaped by future accelerator requirements rather than by legacy system economics. This also shortens the commercial relevance window for mid-tier capacity bands, because a move from 24 GB to 36 GB and then 48 GB across 2 platform generations changes inventory planning and pricing behavior throughout the value chain.

By Advanced Packaging Integration Architecture: 3D Logic-Memory Integration Challenges Silicon-Interposer Dominance

2.5D silicon-interposer-based integration dominated with 80.24% share in 2025, while 3D Logic-Memory Integration is forecast to grow at a 26.88% CAGR through 2031. The lead for 2.5D reflects the maturity of the ecosystem built around commercial HBM coupling with AI accelerators. The memory fabric market has relied heavily on this route because it already supports the interconnect density needed for major accelerator programs. That position also brings supply concentration, because the interposer must be developed separately from both logic and memory and then integrated within constrained advanced packaging capacity. As long as most leading AI accelerators stay on this route, the memory fabric market remains tied to the pace and availability of high-end packaging lines.

Samsung stated that its commercial HBM4 includes a 4 nm logic base die, which signals the shift toward more functional logic inside the stack and supports the move toward 3D Logic-Memory Integration. Applied Materials also said that its NEXX acquisition broadens its capability in panel-level electrochemical deposition for fine-pitch I/O wiring, which is relevant for future hybrid-bonding and advanced heterogeneous integration approaches. Bridge or RDL-based approaches remain useful where chiplet integration does not require the full density of a silicon interposer, which keeps them relevant as lower-cost alternatives. The memory fabric industry is therefore not moving away from 2.5D in a sudden way, but it is opening a path where memory and logic boundaries become less rigid over time. That shift could reshape differentiation by moving value from packaging scale alone toward tighter co-design between memory behavior and embedded logic functions.

By Application: AI Inference Rises To Challenge AI Training Revenue Dominance

AI Inference is projected to grow at the fastest CAGR of 27.24% through 2031, while AI Training held 50.36% of the memory fabric market size in 2025. Training stayed dominant because large model development clusters still absorb a major share of HBM-equipped accelerator deployments. Those clusters require heavy upfront capital and concentrate demand in very large installations, which supported AI Training's revenue lead in 2025. Inference is now rising faster because the installed base of AI services is expanding, and serving live requests creates a different and persistent memory access burden. This keeps the memory fabric market exposed to two demand engines that behave differently in timing, hardware mix, and operational pressure.

Micron stated that agentic AI workloads push much higher concurrency and cache traffic, which helps explain why inference demand is rising on a separate path from training refreshes. High-performance computing and supercomputing remain important because government-backed systems continue to buy HBM-equipped platforms for frontier workloads, even when their refresh pattern does not fully match commercial AI cycles. Data center analytics and in-memory computing are also becoming more relevant as CXL memory expansion opens near-DRAM latency access to larger shared pools. Networking and telecommunications infrastructure, and professional graphics and visualization remain specialized outlets, but they are still adding HBM where packet processing, inference acceleration, or visualization density requires higher bandwidth. The memory fabric market is therefore gaining a more balanced demand base, because inference growth depends on broad service deployment rather than only on major model training events.

By End User: AI Cloud And GPU-As-A-Service Providers Emerge As Structural Demand Centers

AI Cloud and GPU-as-a-Service providers are expected to grow at a 27.16% CAGR through 2031, while hyperscalers and cloud service providers held 46.54% share in 2025. Hyperscalers led because they funded large AI training cluster builds and shaped the first wave of demand for leading-edge HBM systems. That kept the memory fabric market centered on large buyers with broad compute portfolios across training, inference, and general-purpose workloads. The next phase is adding a distinct group of operators that buy specifically for managed AI infrastructure, inference endpoints, and developer AI platforms. This changes procurement behavior because specialized operators tend to prioritize capacity-per-stack, service density, and latency-sensitive deployment characteristics more directly.

The difference between these 2 groups matters because GPU-as-a-Service providers buy for inference-optimized systems, while hyperscalers balance several workload classes in the same infrastructure estate. Data center and enterprise infrastructure operators form a large installed base that is moving from conventional DRAM-heavy servers toward HBM-assisted workloads and CXL expansion over time. Semiconductor and accelerator manufacturers remain a special category because they both consume HBM in development environments and enable the broader memory fabric market through product supply. Research institutions and supercomputing centers still buy at the highest performance frontier, while telecommunications, networking, government, defense, and aerospace customers add selective but high-value demand where qualification standards and deployment conditions are tighter. This mix means the memory fabric market is no longer driven by one buyer class alone, even though hyperscalers still set the pace for leading platform transitions.

Geography Analysis

Asia-Pacific led with 42.33% of the memory fabric market share in 2025 and is also projected to grow at a 27.44% CAGR through 2031. This dual lead reflects the fact that production capability and demand growth are concentrated in the same regional system. South Korea remains central because Samsung and SK Hynix anchor a large share of global HBM supply, and both companies advanced their HBM4 and HBM4E roadmaps in 2026. Taiwan also strengthens Asia-Pacific's position because advanced packaging capacity remains essential to the commercial coupling of HBM and AI accelerators. China adds strong demand through hyperscaler and cloud deployment activity, even though advanced equipment controls continue to limit domestic HBM supply expansion within the period covered by the draft.

North America remained the second-largest regional block in the memory fabric market because it combines hyperscaler spending, processor platform control, and CXL ecosystem development. The United States also anchors platform standards and system design through companies active in CPUs, controllers, switches, and memory products, including Intel, Micron, Marvell, and other infrastructure vendors. Native CXL support in Intel Xeon 6 and active commercialization of switch-layer products support North America's position as the main design and deployment center for disaggregated memory systems. The region, therefore, continues to shape technical direction even when a large share of manufacturing sits in Asia-Pacific.

Europe holds a strategic role in the memory fabric market through supercomputing, enterprise adoption, and standards-based server upgrades. EuroHPC-backed deployments and other institutional HPC programs help sustain demand for HBM-equipped accelerators, especially where performance targets stay close to exascale-class requirements. South America, the Middle East, and Africa remain early-stage regions in this market, with growth coming from cloud buildouts and data center expansion rather than from local HBM supply depth. Their absolute value is expected to rise through 2031, but the larger share of frontier AI infrastructure investment will remain concentrated in Asia-Pacific and North America.

Competitive Landscape

The memory fabric market shows very high concentration at the HBM supply layer, but it remains far more open across controllers, switches, memory expanders, and orchestration software. Samsung, SK hynix, and Micron dominate the supply side of advanced HBM, which means a small number of vendors still set the pace for bandwidth, stack height, capacity, and process transitions. At the same time, the broader memory fabric market is less closed because CXL-related hardware and software layers have drawn a wider field of participants. That split creates a structure where core memory devices are concentrated, while system-level enablement remains more fragmented and more open to new competition. It also means vendors can still win share through interoperability, qualification speed, thermal packaging performance, and platform integration rather than through scale alone.

Several strategic moves in 2026 show how leading companies are positioning themselves in the memory fabric market. Samsung shipped commercial HBM4 in February 2026 with a 4 nm logic base die, 3.3 TB/s bandwidth per stack, and a 40% power efficiency improvement over HBM3E. SK hynix followed by shipping 12-layer HBM4E samples in June 2026 with 48 GB capacity and improved thermal behavior, which pushed competition further into the next generation. Micron also entered high-volume HBM4 production in Q1 2026 and simultaneously shipped 48 GB 16-High samples, which tightened the race across both current and next-step product bands.

The next competitive layer is being shaped by supporting technology and standards participation. Marvell launched its Structera S 30260 CXL 3.0 switch in March 2026, giving hyperscalers a clearer route toward rack-scale pooling and composable memory designs. Applied Materials also broadened its role through new HBM-oriented packaging tools and the acquisition of NEXX, which ties equipment capability more directly to next-generation yield and fine-pitch interconnect needs. Compliance with JEDEC and CXL validation frameworks is also becoming a competitive filter, because operators increasingly want formal interoperability confidence before large multi-vendor rollouts. This leaves the memory fabric market with strong concentration in the component core, but also with meaningful room for differentiation in switching, qualification, packaging, and system management.

Memory Fabric Industry Leaders

Samsung Electronics Co., Ltd.

Intel Corporation

SK Hynix Inc.

Micron Technology, Inc.

Marvell Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Applied Materials introduced 6 new advanced packaging and DRAM systems at its DRAM and Advanced Packaging Master Class on June 25, including the Producer Avila 2 PECVD for HBM TSV stress management, Opta Quad CMP for interconnect planarization, and Nokota VMax 2 ECD for high-precision copper plating, directly targeting yield improvement in 12-High and 16-High HBM stack production and signaling that equipment-layer innovation is now as strategically important as silicon-layer scaling for memory fabric competitiveness.

- June 2026: SK hynix shipped 12-layer HBM4E samples to major AI customers on June 17, achieving 16 Gbps per pin and 48 GB capacity with over 20% improved power efficiency and 17% lower heat resistance versus HBM4 through Advanced MR-MUF technology, targeting the NVIDIA Vera Rubin Ultra platform with mass production planned for 2027, advancing the company's position as a full-stack AI memory provider.

- May 2026: Applied Materials completed the acquisition of NEXX Systems on May 4, broadening its advanced packaging portfolio with panel-level electrochemical deposition technology for fine-pitch I/O wiring, accelerating roadmaps for AI chipmakers requiring sub-10 µm interconnect pitches in copper-copper hybrid-bonding architectures essential for HBM5 and next-generation 3D Logic-Memory Integration.

- March 2026: Marvell Technology launched the Structera S 30260, a 260-lane CXL 3.0 switch with 4 TB/s aggregate bandwidth and sub-microsecond memory access latency on March 17, leveraging its XConn Technologies acquisition to enable rack-scale memory pooling across CPUs, GPUs, and XPUs, making composable memory a production-ready option for hyperscalers pursuing TCO optimization through disaggregated memory architectures.

Global Memory Fabric Market Report Scope

Memory Fabric Market refers to the ecosystem of networking and interconnect technologies that enable pooled, disaggregated, and shared memory across servers, accelerators, and storage systems. It is designed to improve memory utilization, reduce data movement bottlenecks, and deliver lower latency for data-intensive workloads.

The Memory Fabric Market Report is Segmented by HBM Generation (HBM2E and Earlier Generations, HBM3, HBM3E, HBM4, and HBM4E and Next-Generation HBM), Stack Height (4-High and Below, 8-High, 12-High, and 16-High and Above), Memory Capacity per Stack (Up to 16 GB, 16 GB to 24 GB, 24 GB to 36 GB, and Above 36 GB), Advanced Packaging Integration Architecture (2.5D Silicon-Interposer-Based Integration, 2.5D Bridge or RDL-Based Advanced Packaging, and 3D Logic-Memory Integration), Application (AI Training, AI Inference, High-Performance Computing and Supercomputing, Data Center Analytics and In-Memory Computing, Networking and Telecommunications Infrastructure, and Professional Graphics and Visualization), End User (Hyperscalers and Cloud Service Providers, AI Cloud and GPU-as-a-Service Providers, Data Center and Enterprise Infrastructure Operators, Research Institutions and Supercomputing Centers, Semiconductor and Accelerator Manufacturers, Telecommunications and Networking Equipment Providers, and Government, Defense, and Aerospace Organizations), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E and Earlier Generations |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E and Next-Generation HBM |

| 4-High and Below |

| 8-High |

| 12-High |

| 16-High and Above |

| Up to 16 GB |

| 16 GB to 24 GB |

| 24 GB to 36 GB |

| Above 36 GB |

| 2.5D Silicon-Interposer-Based Integration |

| 2.5D Bridge or RDL-Based Advanced Packaging |

| 3D Logic-Memory Integration |

| Other Advanced Heterogeneous Integration Architectures |

| AI Training |

| AI Inference |

| High-Performance Computing and Supercomputing |

| Data Center Analytics and In-Memory Computing |

| Networking and Telecommunications Infrastructure |

| Professional Graphics and Visualization |

| Hyperscalers and Cloud Service Providers |

| AI Cloud and GPU-as-a-Service Providers |

| Data Center and Enterprise Infrastructure Operators |

| Research Institutions and Supercomputing Centers |

| Semiconductor and Accelerator Manufacturers |

| Telecommunications and Networking Equipment Providers |

| Government, Defense, and Aerospace Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By HBM Generation | HBM2E and Earlier Generations | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| HBM4E and Next-Generation HBM | ||

| By Stack Height | 4-High and Below | |

| 8-High | ||

| 12-High | ||

| 16-High and Above | ||

| By Memory Capacity per Stack | Up to 16 GB | |

| 16 GB to 24 GB | ||

| 24 GB to 36 GB | ||

| Above 36 GB | ||

| By Advanced Packaging Integration Architecture | 2.5D Silicon-Interposer-Based Integration | |

| 2.5D Bridge or RDL-Based Advanced Packaging | ||

| 3D Logic-Memory Integration | ||

| Other Advanced Heterogeneous Integration Architectures | ||

| By Application | AI Training | |

| AI Inference | ||

| High-Performance Computing and Supercomputing | ||

| Data Center Analytics and In-Memory Computing | ||

| Networking and Telecommunications Infrastructure | ||

| Professional Graphics and Visualization | ||

| By End User | Hyperscalers and Cloud Service Providers | |

| AI Cloud and GPU-as-a-Service Providers | ||

| Data Center and Enterprise Infrastructure Operators | ||

| Research Institutions and Supercomputing Centers | ||

| Semiconductor and Accelerator Manufacturers | ||

| Telecommunications and Networking Equipment Providers | ||

| Government, Defense, and Aerospace Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the memory fabric market and where is it headed?

The memory fabric market stood at USD 3.98 billion in 2026 and is projected to reach USD 12.44 billion by 2031 at a CAGR of 25.60%, showing that AI memory infrastructure is moving into a high-growth phase.

Which region leads demand and growth in memory fabric?

Asia-Pacific led with 42.33% share in 2025 and is also the fastest-growing region at a 27.44% CAGR through 2031, supported by its strong HBM production base and packaging depth.

What is driving faster adoption of memory fabric platforms?

The biggest push is AI inference, where larger context windows and rising concurrency increase memory bandwidth and capacity pressure faster than compute alone can solve.

Which application area is growing the fastest?

AI Inference is the fastest-growing application with a 27.24% CAGR through 2031, while AI Training remained the largest application in 2025 with 50.36% share.

Which product transition matters most for suppliers and buyers?

The most important shift is from HBM3E, which led 2025 revenue, toward HBM4 and HBM4E products that bring higher bandwidth, larger capacities, and better power efficiency for next-wave AI platforms.

What is the main risk that could slow deployment?

The main near-term risk is not demand weakness, but slower commercialization and validation of advanced CXL platforms, along with the integration complexity that can delay enterprise rollout.

Page last updated on: