Meditation Management Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.65 Billion |

| Market Size (2031) | USD 14.17 Billion |

| Growth Rate (2026 - 2031) | 16.32% CAGR |

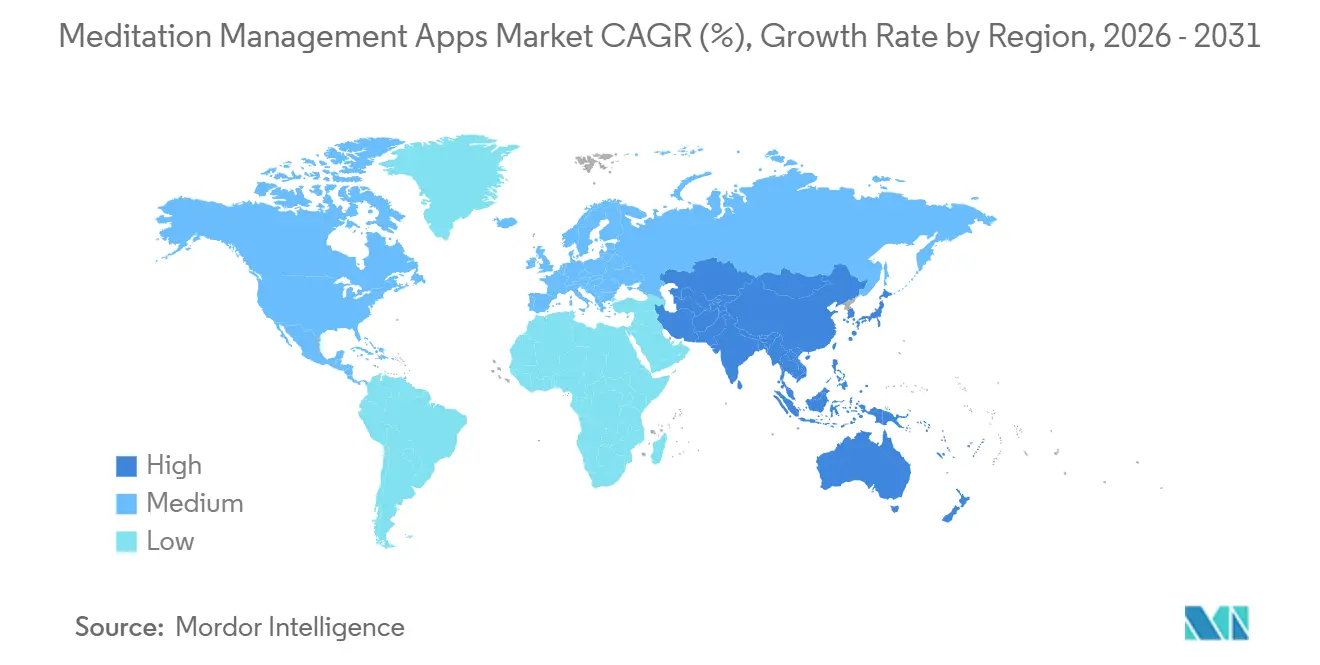

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

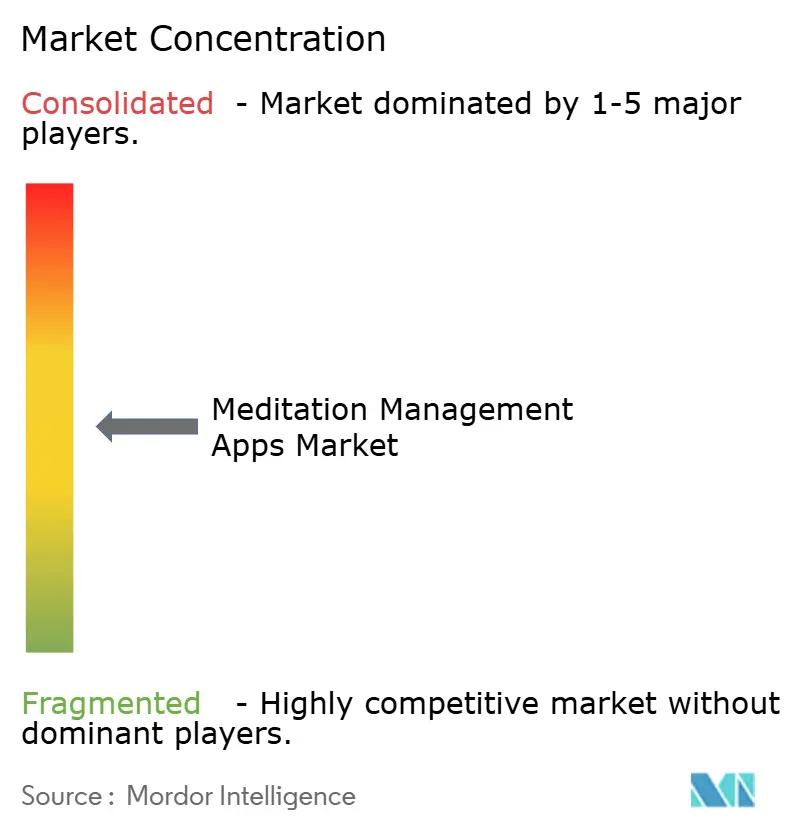

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meditation Management Apps Market Analysis by Mordor Intelligence

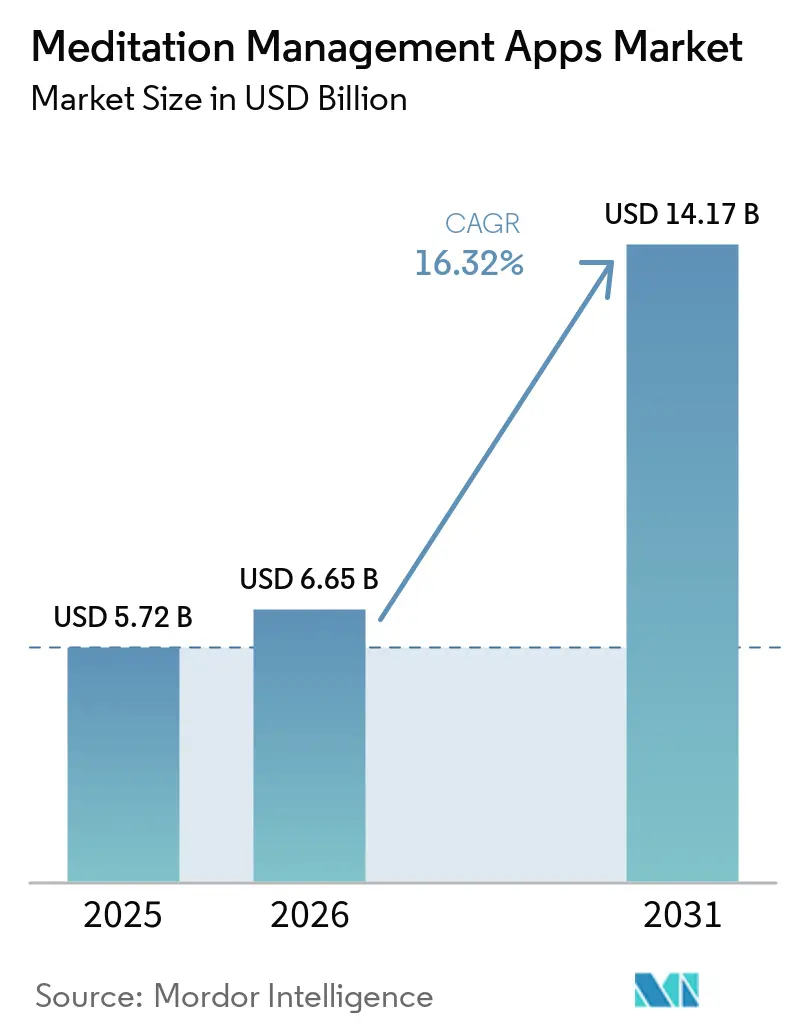

The Meditation Management Apps Market size is expected to increase from USD 5.72 billion in 2025 to USD 6.65 billion in 2026 and reach USD 14.17 billion by 2031, growing at a CAGR of 16.32% over 2026-2031.

The meditation apps market is transitioning from discretionary wellness spending to becoming an integral part of routine mental health support, as employers, health plans, and care pathways increasingly adopt digital solutions. Growth is no longer confined to premium Western users, with Android adoption expanding the market across emerging smartphone regions. AI-driven personalization, sleep-focused content, and biosensor-linked experiences are elevating user expectations and aligning the market with clinically adjacent applications. Competitive advantage now relies on retention design, localization, and institutional distribution rather than content volume alone. The primary growth challenge remains weak long-term engagement, while enterprise contracts and sleep-focused product expansion present significant commercial opportunities.

Key Report Takeaways

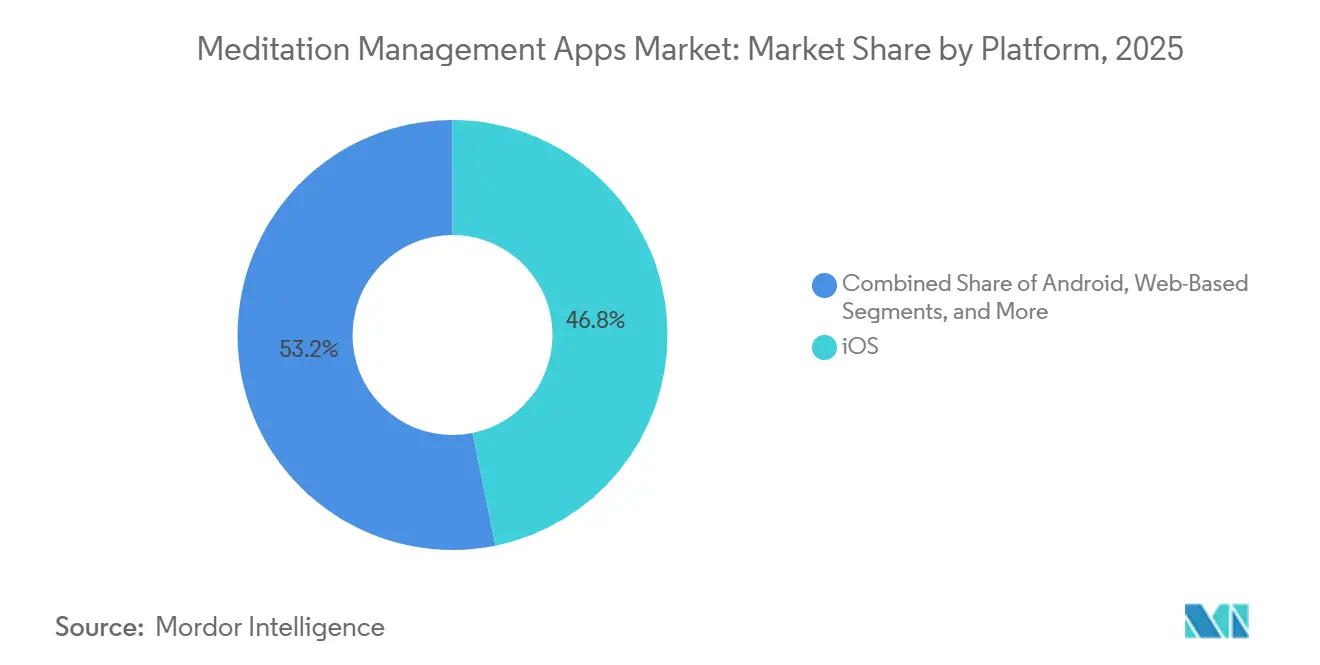

- By platform, iOS held 46.76% share of the meditation apps market size in 2025, while Android is projected to expand at a 16.90% CAGR through 2031.

- By revenue model, Freemium accounted for 45.30% share of the meditation apps market size in 2025, while subscription is forecast to grow at a 17.25% CAGR through 2031.

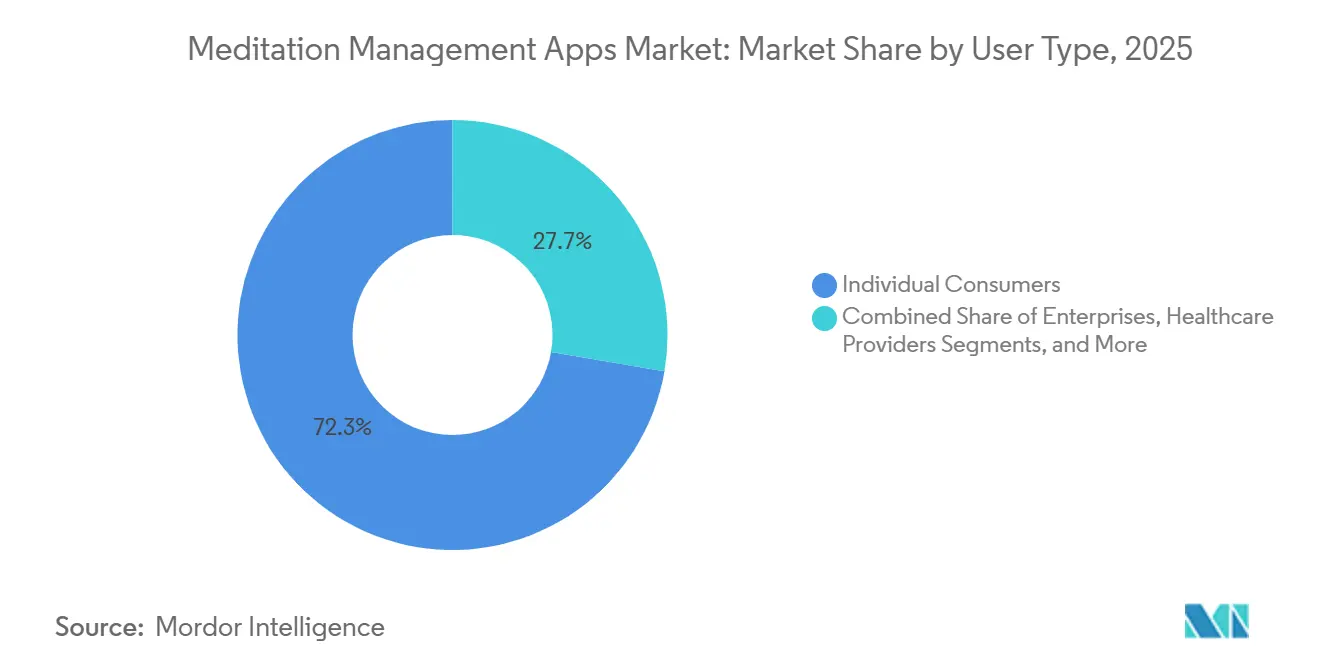

- By user type, individual consumers held 72.32% of meditation apps market share in 2025, while enterprise is projected to advance at a 17.95% CAGR through 2031.

- By content format, guided meditation accounted for 52.71% share in 2025, while Sleep and relaxation audio is forecast to grow at an 18.2% CAGR through 2031.

- By geography, North America held 42.45% of meditation apps market share in 2025, while Asia-Pacific is projected to record a 16.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meditation Management Apps Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising workplace burnout and employer wellness spending | +2.8% | Global, with strong relevance in North America, Japan, and Germany | Medium term (2-4 years) |

| Consumer shift toward low-cost, self-guided mental health tools | +2.3% | Global, with stronger pull in Asia-Pacific and South America | Short term (≤ 2 years) |

| AI-driven personalization and adaptive meditation journeys | +2.0% | North America and Asia-Pacific, with spillover into Europe | Medium term (2-4 years) |

| Wearable and biosensor integration for real-time stress monitoring | +1.4% | North America and Europe, with early uptake in Japan and South Korea | Long term (≥ 4 years) |

| Expansion of clinical adjacent use cases in sleep and anxiety | +1.7% | North America and Europe, with gradual spillover into Asia-Pacific | Medium term (2-4 years) |

| Platform bundling through super apps and wellness ecosystems | +1.5% | Asia-Pacific and North America, with early gains in Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Workplace Burnout and Employer Wellness Spending

Employer demand is a key growth driver for the meditation apps market. Starting January 2026, Headspace partnered with Cigna Healthcare to provide self-guided mental health support to over 7 million individuals through employer benefits at no direct cost to users. Similarly, Calm Health joined the Solera Network, expanding access to over 16 million people and increasing its institutional reach to 39 million across health plans, providers, and employers. This distribution model shifts revenue generation from individual purchases to benefits infrastructure, ensuring stable contract cycles and reduced acquisition pressures, supporting enterprise-driven growth during the forecast period.

AI-Driven Personalization and Adaptive Meditation Journeys

AI is becoming a central engagement tool in the meditation apps market. Headspace introduced its Ebb empathetic AI companion in May 2025, offering personalized guidance across coaching, therapy, and self-care. Insight Timer launched an AI-powered recommendation engine in January 2026 to create tailored lesson paths for users. South Korea's NP utilized AI emotion inference in its MUA XR meditation app, integrating real-time biosignals like heart rate variability and sleep quality. This shift from static content to adaptive systems enhances user engagement and creates a competitive edge for differentiated platforms.

Expansion of Clinical Adjacent Use Cases in Sleep and Anxiety

The meditation apps market is expanding into clinical applications, particularly in sleep and anxiety care. Big Health secured USD 23.7 million in February 2026 to accelerate the adoption of its FDA-cleared SleepioRx and DaylightRx, which align with the CMS reimbursement pathway. A March 2026 study demonstrated that a wearable-integrated digital mindfulness app improved sleep efficiency and heart rate variability.[1]Headspace, “Headspace Unveils Stratified Care Model Powered by Empathetic AI Companion, Ebb,” Business Wire, businesswire.com Calm launched Calm Sleep as a standalone app in September 2025, emphasizing sleep as a distinct product line. Platforms with proven outcomes in sleep and anxiety are likely to gain pricing power and institutional acceptance.

Platform Bundling Through Super Apps and Wellness Ecosystems

The meditation apps market is increasingly integrating into broader digital ecosystems. Apple Music introduced Sound Therapy in May 2025, incorporating focus and sleep support into its existing music service without requiring a separate subscription. Sleep Cycle launched its app within ChatGPT in Q1 2026, expanding its reach beyond its native platform. Embedding meditation and sleep content into established user routines reduces discovery challenges and boosts daily engagement, while standalone operators without ecosystem partnerships may face growing distribution pressures.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Subscription fatigue and weak long-term retention | -1.5% | Global, with the sharpest effect in North America and Western Europe | Short term (≤ 2 years) |

| Privacy concerns around sensitive mental health data | -1.2% | Europe and North America, with spillover into other regulated markets | Short term (≤ 2 years) |

| Low clinical differentiation among mass-market apps | -0.9% | Global, with stronger impact in highly regulated healthcare systems | Medium term (2-4 years) |

| Algorithmic content drift and quality control risks at scale | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subscription Fatigue and Weak Long-Term Retention

Retention challenges continue to hinder the meditation apps market, particularly for consumer-first platforms. A 2025 study found that digital mental health interventions have completion rates as low as 29.4% among younger users, primarily due to weak habit formation and poor integration into care pathways.[2]E. Koh et al., “Digital Wellness or Digital Dependency? A Critical Examination of Mental Health Apps and Their Implications,” Frontiers in Public Health, pmc.ncbi.nlm.nih.gov This reduces the long-term value of users and pressures marketing efficiency. Leading companies are increasingly targeting enterprise, payer, and provider channels, where enrollment is more stable. Without improving sustained engagement, the market will rely heavily on replacing churned users alongside acquiring new ones.

Privacy Concerns Around Sensitive Mental Health Data

Privacy concerns are significantly impacting the meditation apps market as platforms collect more emotional, behavioral, and biometric data. A 2025 study revealed that all surveyed apps had at least one undisclosed data practice, and 48% failed to disclose embedded tracker SDKs in their privacy policies.[3]World's Largest Free Wellness App Insight Timer Launches in India,” GainFocus PR, news.gainfocuspr.com A 2026 study indicated that stronger privacy concerns are driving users toward shorter subscription models, affecting trust and monetization strategies. As AI and biosensor technologies become more prevalent, transparent consent, data minimization, and compliance will be critical for user retention and conversion.[4]Petit BamBou Lance En 2026 Une Application Dédiée Au Sommeil,” Journal du Savoir, jds.fr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Android Growth Signals Broader Smartphone Reach

In 2025, iOS held a 46.76% share of the platform segment, maintaining its position as the top revenue generator in the meditation apps market. This dominance was driven by premium users in North America and Western Europe, where paid subscriptions and wellness spending are well-established. iOS users are more inclined to pay for premium experiences and guided programs, keeping the platform central to monetization as the market expands to new demographics.

Android is projected to grow at a 16.90% CAGR from 2026 to 2031, making it the fastest-growing platform in the meditation apps market. This growth is fueled by smartphone adoption in South and Southeast Asia, Latin America, and Sub-Saharan Africa, where Android dominates. Platforms offering local language libraries, region-specific themes, and culturally relevant instructors are expected to perform better. Web-based access is also gaining traction among enterprises due to compatibility with IT protocols. Multi-platform designs are becoming essential as they enhance user experience and support structured programs.

By Revenue Model: Freemium Drives Reach While Subscription Builds Revenue

Freemium accounted for 45.30% of the meditation apps market in 2025, making it the leading revenue model by reach and distribution. It lowers entry barriers while creating opportunities for premium conversions, referrals, and enterprise visibility. This model is crucial for scaling demand across both mature and emerging user bases.

Subscription is forecast to grow at a 17.25% CAGR through 2031, emerging as the fastest-growing revenue model. Growth is driven by enterprise and health plan contracts, where recurring payments replace discretionary renewals. Privacy-conscious users prefer flexible monthly subscriptions over lifetime access, making adaptability key in high-awareness markets. One-time purchases and ad-supported models remain relevant in price-sensitive regions but lack the recurring revenue potential of subscriptions.

By User Type: Enterprise Adoption Is Reshaping Demand Patterns

Individual consumers held a 72.32% share of the meditation apps market in 2025, remaining the largest user group. This segment drives brand visibility and supports enterprise conversions, as recognized brands are preferred by employers and partners. However, the market is diversifying beyond individual acquisition.

Enterprises are projected to grow at a 17.95% CAGR through 2031, becoming the fastest-growing user segment. Structured enterprise products now offer tailored solutions like self-guided care, coaching, therapy, or psychiatry. Healthcare providers, though smaller in share, are strategically important due to FDA-approved digital mental health treatments. Education institutions are also adopting app-based mindfulness as part of broader wellness programs, supported by evidence of improved outcomes.

By Content Format: Guided Meditation Leads, Sleep Audio Improves Staying Power

Guided meditation held a 52.71% share in 2025, making it the largest content format in the meditation apps market. Its structured approach appeals to first-time users and enhances app store visibility, keeping it central to user acquisition as the market evolves.

Sleep and relaxation audio is forecast to grow at an 18.2% CAGR through 2031, becoming the fastest-growing content segment. Sleep-focused product lines are gaining prominence, with high engagement rates and completion metrics highlighting their effectiveness. Breathwork and mindfulness exercises remain relevant for stress and focus, while unguided meditation is gaining traction among experienced users and workplace programs. Enhanced sleep content is increasingly linked to better user retention and engagement.

Geography Analysis

In 2025, North America accounted for 42.45% of the meditation apps market, maintaining its position as the largest regional player. The region benefits from mature employer wellness systems, strong health plan integration, and significant venture-backed product development. By January 2026, Headspace partnered with Cigna Healthcare to provide services to over 7 million users through employer-linked benefits. Calm Health expanded its reach via the Solera Network, adding access to 16 million individuals and increasing its institutional footprint to 39 million covered lives. The CMS reimbursement pathway for FDA-approved digital mental health solutions further strengthens the region by offering clinically differentiated platforms a clearer route to provider adoption.

Asia-Pacific is projected to grow at a 16.76% CAGR through 2031, making it the fastest-growing region in the meditation apps market. Growth is driven by digital wellness adoption, wider smartphone access, and increasing acceptance of app-based mindfulness in daily routines. Insight Timer launched in India in March 2026 with 300,000 free guided meditations from over 20,000 global instructors, showcasing the use of extensive free libraries to tap into high-demand markets. South Korea remains a key innovation hub for biosignal-linked and AI-personalized meditation experiences, supporting both product development and user growth.

Europe ranked as the second-largest regional cluster in the meditation apps market, supported by established wellness demand and localized platforms. The region’s focus on privacy, consent, and evidence-backed practices favors compliant and well-documented platforms. Outside Europe and North America, the meditation apps market is expanding in South America, the Middle East, and Africa, driven by freemium access, improved mobile connectivity, and gradual employer-led adoption.

Competitive Landscape

The meditation apps market exhibits a dual nature: a concentrated premium segment and a widely fragmented landscape featuring regional and niche players. While Calm and Headspace dominate in global brand visibility, the market is peppered with specialized operators adept in local languages, secular themes, or unique formats. This underscores that mere brand recognition doesn't ensure dominance across all use cases or regions. The market's competitive focus is shifting from merely offering diverse content to emphasizing retention strategies, clinical relevance, and institutional partnerships. Consequently, it is becoming increasingly challenging for subscription models based solely on content to maintain their supremacy.

Headspace is advancing into structured care with its Ebb AI companion and stratified care model, which directs users to appropriate support levels within enterprise and payer frameworks. Calm is expanding its offerings through Calm Sleep and its partnership with LifeStance Health, enabling in-app referrals to licensed therapists for users requiring advanced care. These strategies highlight how leading players are enhancing user engagement and care continuity, moving beyond reliance on meditation libraries. They also reflect a shift toward adjacent services that encourage broader usage beyond a single daily session.

The next tier of competitors differentiates itself by avoiding direct imitation of Calm and Headspace. These players focus on multilingual reach, free-access communities, or specialized wellness formats. Insight Timer, for example, leverages free content and AI-driven personalization instead of a strict paywall model. Healium's FDA registration of Healium Clinical in May 2026 highlights a distinct segment within the market, where immersive biofeedback and prescription-based usage enhance clinical credibility. The market remains open for strong local and format-based challengers, particularly in areas like personalization, sleep outcomes, and enterprise deployment, where platforms can offer clear competitive advantages.

Meditation Management Apps Industry Leaders

Calm Inc.

Headspace Inc.

Insight Network, Inc.

Ten Percent Happier, Inc.

Aura Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Pura and Calm launched the Pura x Calm Collection, integrating Calm’s Sleep Stories, soundscapes, and breathwork content with Pura's diffuser technology via the app.

- March 2026: Insight Timer launched in India, offering 300,000 free guided meditations from over 20,000 teachers.

- February 2026: Big Health raised USD 23.7 million in strategic funding to accelerate the adoption of SleepioRx and DaylightRx, both FDA-cleared and CMS-reimbursable digital mental health treatments.

- January 2026: Calm Health joined the Solera Network, expanding access to over 16 million individuals and enhancing Calm’s institutional reach of 39 million.

- January 2026: Headspace partnered with Cigna Healthcare, providing over 7 million customers access to science-backed self-guided resources at no additional cost.

Global Meditation Management Apps Market Report Scope

As per the scope of the report, meditation management apps are digital tools that provide guided audio, video, and text sessions to help you reduce stress, improve sleep, and practice mindfulness. They use built-in features to help you track your habits, monitor your moods, and build a consistent mental wellness routine.

The meditation management apps market is segmented by platform, revenue model, user type, content format, and geography. By platform, the market includes iOS, Android, and web-based platforms. By revenue model, the market is segmented into freemium, subscription, one-time purchase, ad-supported, and enterprise licensing. By user type, the market is categorized into individual consumers, enterprises, healthcare providers, and educational institutions. By content format, the market is segmented into guided meditation, unguided meditation, sleep and relaxation audio, and breathwork and mindfulness exercises. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| iOS |

| Android |

| Web-Based |

| Freemium |

| Subscription |

| One-Time Purchase |

| Ad-Supported |

| Enterprise Licensing |

| Individual Consumers |

| Enterprises |

| Healthcare Providers |

| Education Institutions |

| Guided Meditation |

| Unguided Meditation |

| Sleep and Relaxation Audio |

| Breathwork and Mindfulness Exercises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Platform | iOS | |

| Android | ||

| Web-Based | ||

| By Revenue Model | Freemium | |

| Subscription | ||

| One-Time Purchase | ||

| Ad-Supported | ||

| Enterprise Licensing | ||

| By User Type | Individual Consumers | |

| Enterprises | ||

| Healthcare Providers | ||

| Education Institutions | ||

| By Content Format | Guided Meditation | |

| Unguided Meditation | ||

| Sleep and Relaxation Audio | ||

| Breathwork and Mindfulness Exercises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for meditation apps?

The meditation apps market is forecast to reach USD 14.17 billion by 2031 from USD 6.65 billion in 2026, growing at a 16.32% CAGR.

Which user group is expanding the fastest?

Enterprise is the fastest-growing user type, with a projected 17.95% CAGR through 2031 as employers add digital mental health access to benefits programs.

Which content format is growing the quickest?

Sleep and Relaxation Audio is forecast to grow at an 18.2% CAGR, supported by stronger routine use and better retention potential than many other formats.

Why does North America lead revenue today?

North America held 42.45% share in 2025 because it has stronger employer wellness systems, deeper health plan integration, and clearer clinical reimbursement pathways.

What is changing competition among leading apps?

Competition is moving toward AI personalization, sleep-focused offerings, clinically adjacent services, and enterprise distribution rather than simple content volume.

What is the biggest challenge for app providers?

Weak long-term retention remains a major issue because many users do not sustain engagement, which keeps pressure on customer acquisition efficiency and renewal quality.

Page last updated on: