Medical Professional Liability Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.82 Billion |

| Market Size (2031) | USD 26.24 Billion |

| Growth Rate (2026 - 2031) | 6.87% CAGR |

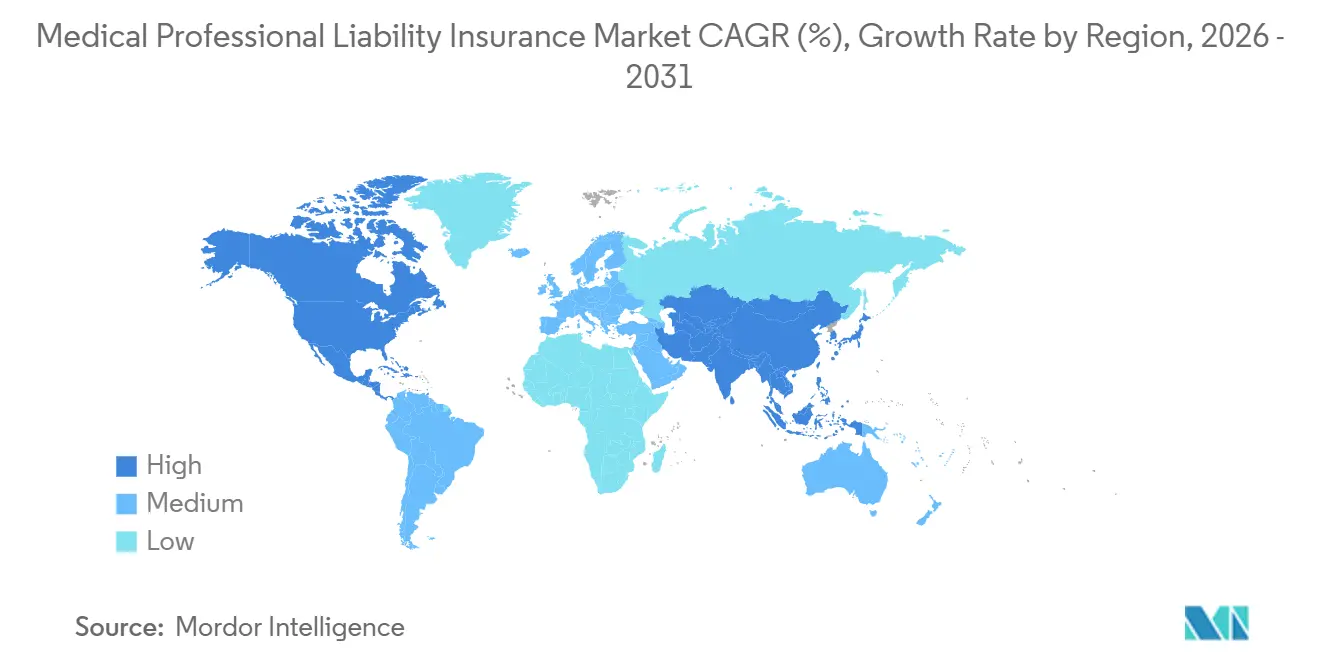

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Professional Liability Insurance Market Analysis by Mordor Intelligence

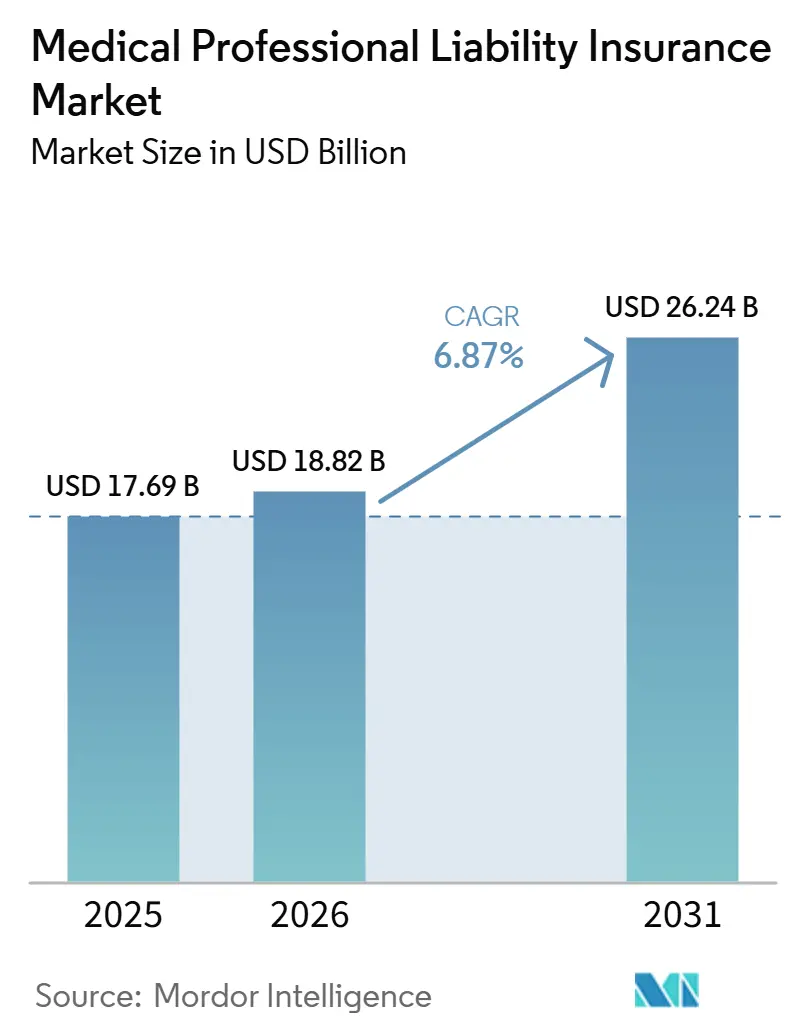

The Medical Professional Liability Insurance Market size is expected to increase from USD 17.69 billion in 2025 to USD 18.82 billion in 2026 and reach USD 26.24 billion by 2031, growing at a CAGR of 6.87% over 2026-2031.

The medical professional liability insurance market is moving higher because pricing continues to respond to claim severity, while claim frequency has stayed more stable in several major books of business. In the United States, the seventh straight year of premium increases in 2025 showed how deeply severity pressure has shaped underwriting decisions, and the American Medical Association reported that 39.9% of medical liability premiums rose in 2025. The medical professional liability insurance market is also being reshaped by record premium volumes, tighter reserving discipline, and a greater need for sustained rate action as favorable reserve development has narrowed across specialist carriers. The medical professional liability insurance market still depends heavily on North America for premium scale, yet growth is spreading into Asia-Pacific as liability frameworks formalize and private healthcare systems expand. Competitive positioning is increasingly tied to risk selection, claims automation, captive formation, and consolidation among specialist carriers that want broader scale and stronger negotiating leverage in reinsurance and physician risk management.

Key Report Takeaways

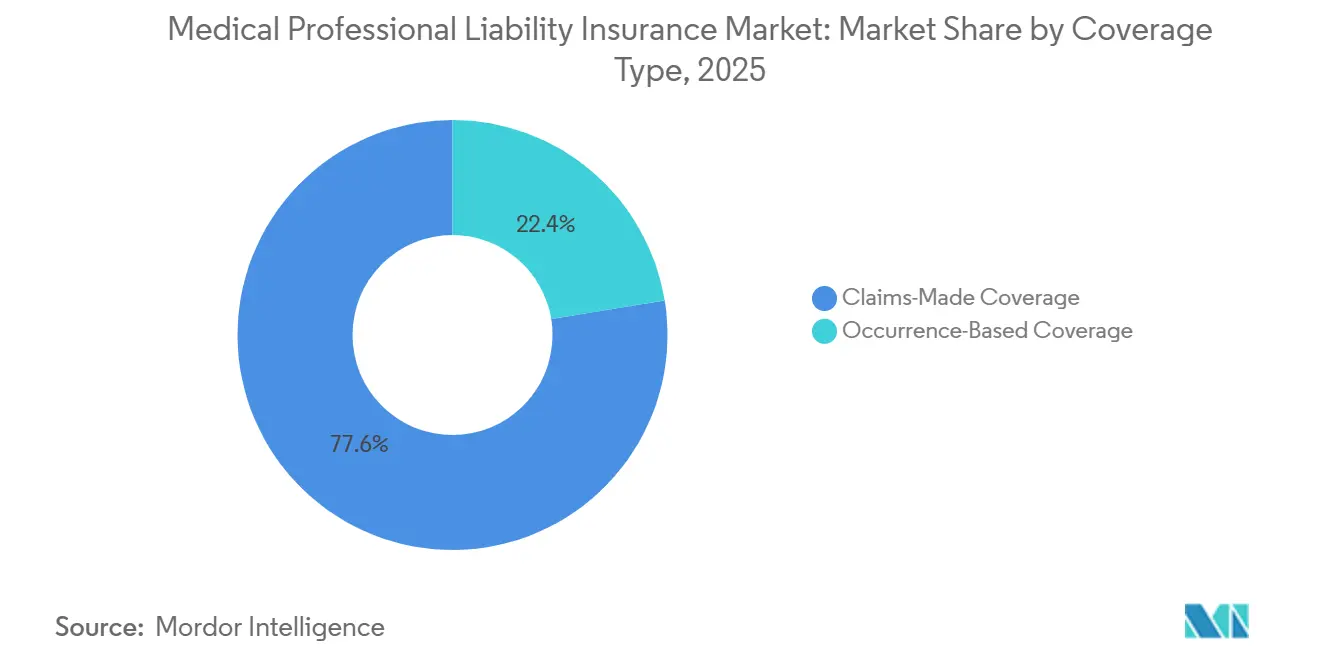

- By coverage type, claims-made coverage accounted for 77.56% of the medical professional liability insurance market share in 2025 and is projected to grow at a 7.1% CAGR through 2031.

- By claim category, diagnosis-related claims held 32.67% share in 2025 and are projected to grow at 7.6% CAGR through 2031.

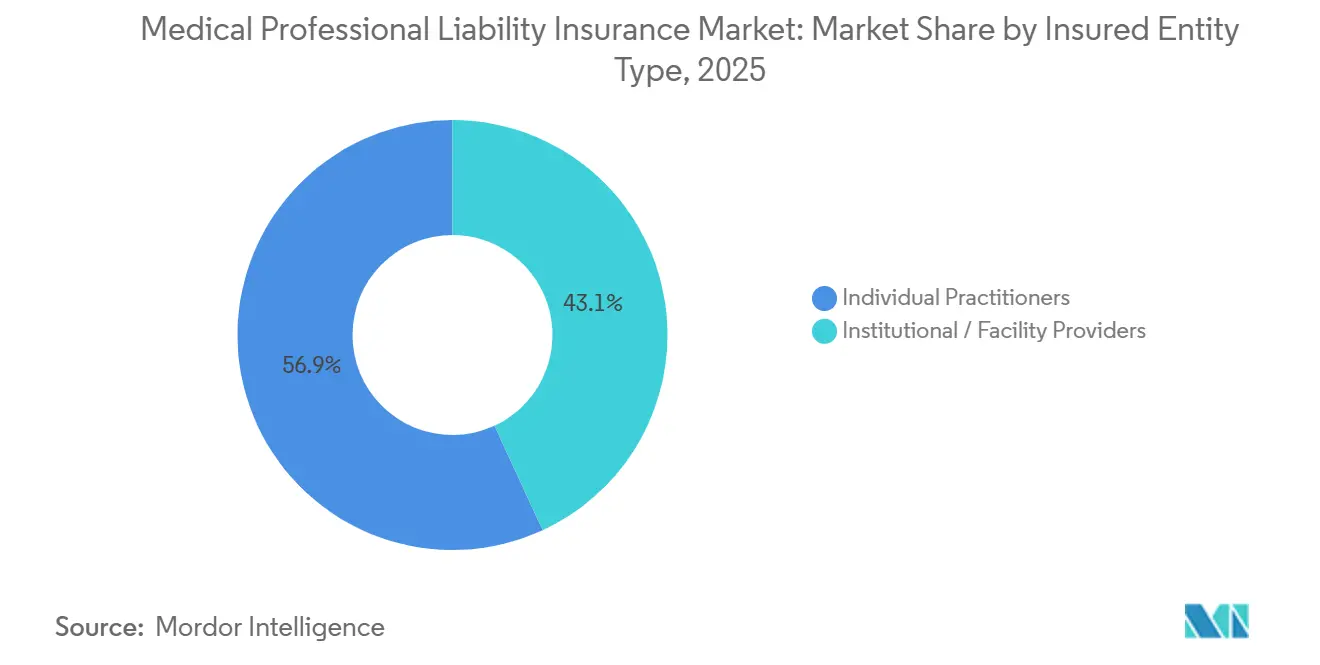

- By insured entity type, individual practitioners accounted for 56.89% revenue share in 2025, while institutional and facility providers recorded the highest projected CAGR at 8.4% through 2031.

- By distribution channel, captives, risk retention groups, and self-insurance programs led with 33.72% share in 2025 and are forecast to expand at 8.8% CAGR through 2031.

- By geography, North America captured 62.34% of the medical professional liability insurance market size in 2025, while the Asia-Pacific is projected to grow at 9.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Professional Liability Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Severity of Misdiagnosis and Treatment Error Claims | +1.8% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Expansion of High-Risk Outpatient and Ambulatory Care Settings | +1.1% | North America, with spillover to the Asia-Pacific and Middle East, and Africa | Medium term (2-4 years) |

| Mandatory Coverage Expansion in Regulated Healthcare Systems | +1.0% | Asia-Pacific, the Middle East and Africa, and South America | Medium term (2-4 years) |

| Digital Underwriting and Claims Automation Adoption | +0.6% | Global, with early adoption in North America and Northern Europe | Medium term (2-4 years) |

| Litigation Funding and Nuclear Verdict Escalation | +1.3% | North America and select European jurisdictions | Short term (≤ 2 years) |

| Telemedicine and AI-Enabled Care Creating New Liability Triggers | +0.7% | Global, with the fastest escalation in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Severity of Misdiagnosis and Treatment Error Claims

The medical professional liability insurance market continues to be driven by diagnostic failures and treatment errors, as these claims now yield larger payouts, even as overall claim frequency does not rise at the same pace. In 2024, the top 50 United States malpractice awards averaged USD 56 million, 14% above 2023, according to WTW, which showed that high-value awards have moved into a more sustained pattern[1]WTWCO.COM https://www.wtwco.com/en-us/insights/2025/10/insurance-marketplace-realities-2026-healthcare-professional-liability. Milliman also reported that indemnity payments for its composite of 170 United States specialty carriers exceeded USD 2.9 billion through the first 3 quarters of 2025, up 17%, while claim frequency remained broadly flat. That split between stable frequency and rising severity means carriers must price for larger awards, more complex expert testimony, and longer claim development periods, rather than relying on older frequency-based assumptions. The medical professional liability insurance market is therefore responding with firmer pricing, closer claims review, and more pressure on claims-made reserve assumptions. Carriers that do not keep pace with this shift in 2026 and 2027 risk weaker reserve adequacy and lower underwriting margins in later reporting periods.

Expansion of High-Risk Outpatient and Ambulatory Care Settings

The medical professional liability insurance market is gaining new exposure from outpatient and ambulatory settings, as more procedures that once took place in hospitals are now moving to centers with different staffing and monitoring models. CMS finalized the 2026 Ambulatory Surgery Center payment rule in November 2025 and added 573 procedures to the covered procedures list, including higher-acuity surgeries that expand the liability profile of outpatient providers[2]Ambulatory Surgery Center Association, “CMS Releases 2026 Final Payment Rule,” ASCA, ascassociation.org. These settings often operate with leaner staffing than hospitals, which changes the operational risks around anesthesia oversight, informed consent, documentation, and post-operative observation. Hospital-sponsored insurance programs also do not always absorb the full outpatient exposure, so standalone professional liability coverage remains necessary for many facility owners and operators. The medical professional liability insurance market benefits from this widening exposure base because ambulatory surgery centers, day-surgery sites, and similar facilities add new premium demand without fully matching the loss history of acute hospital towers. A similar expansion is also occurring across private healthcare systems in the Asia-Pacific, where new outpatient capacity is increasing before broad public indemnity protections have fully developed.

Litigation Funding and Nuclear Verdict Escalation

The medical professional liability insurance market is also being shaped by litigation funding and large court awards, as these factors extend case duration and reduce the likelihood of early settlement. WTW reported that investor-backed claims were associated with a 60.5% increase in payouts, timelines that were 140% longer than unfunded cases, and a 35.7% lower likelihood of pre-trial settlement. The same pressure shows up in state-level loss experience, where S&P Global Market Intelligence data cited by Insurance Journal showed a 2025 direct incurred loss and defense expense ratio of 128.8% in New Mexico and 143.8% in Utah, far above the United States aggregate of 75.9%[3]INSURANCEJOURNAL.COM Claim Severity Trends for Medical Malpractice ‘Stand Out’: S&P GMI. The result is a legal environment in which a carrier's geographic mix matters almost as much as its specialty mix, because verdict behavior can shift much faster than historical pricing models. The medical professional liability insurance market, therefore, rewards carriers that can limit concentration in high-verdict jurisdictions and quickly reset underwriting assumptions. This also gives larger specialist insurers an advantage because they can diversify regionally while smaller books remain more exposed to local court patterns.

Telemedicine And AI-Enabled Care Creating New Liability Triggers

The medical professional liability insurance market is beginning to price new forms of exposure arising from telemedicine and AI-supported care, as these services expand clinical activity across state lines and change how decisions are documented. The American Medical Association reported that more than 80% of United States physicians now offer some form of telehealth, yet many have not reviewed whether their malpractice coverage fully addresses virtual care exposures. The extension of federal telehealth flexibilities through December 31, 2027, keeps reimbursement support in place, sustaining virtual-care volume and preserving the related liability exposure for carriers that insure multistate practice models. At the same time, AI tools are moving deeper into diagnostic support, but legal responsibility among clinicians, software providers, and platform operators is not yet fully settled in practice or case law. That uncertainty makes policy wording, underwriting review, and provider governance more important within the medical professional liability insurance market. It also creates a feedback loop in which carriers increasingly use premium differentiation to reward stronger testing, training, and oversight around digital clinical tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-Tail Loss Uncertainty and Reserve Volatility | -0.6% | Global, most acute in North America and Western Europe | Long term (≥ 4 years) |

| Reinsurance Tightness for Catastrophic Medical Towers | -0.4% | North America and Europe, with spillover to the Asia-Pacific | Medium term (2-4 years) |

| Fragmented Legal Regimes and Cross-Jurisdiction Pricing Complexity | -0.3% | Asia-Pacific, South America, the Middle East and Africa, and parts of Europe | Medium term (2-4 years) |

| Under-Insurance and Low Penetration in Emerging Healthcare Markets | -0.2% | Emerging Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-Tail Loss Uncertainty And Reserve Volatility

The medical professional liability insurance market remains constrained by very long claim tails, as some injuries, especially those involving minors, can remain open for many years before full settlement and reserve closure. In 2025, claims-made carriers recognized USD 259 million in adverse development, with large contributions from Curi Holdings, Liberty Mutual Holding, and Farmers Insurance Group as court backlogs eased and more claims moved forward. AM Best also noted that favorable reserve development narrowed to USD 155 million in 2025, far below the larger capital cushion the line had enjoyed in earlier years. When reserve redundancy shrinks, carriers have less flexibility to compete on price because they can no longer rely on future reserve releases to offset weak underwriting periods. The medical professional liability insurance market, therefore, sees slower new capacity formation and more careful rate discipline when claim development becomes harder to predict. This reserve pressure matters most in long-tail books, where a pricing error made today can continue affecting reported results for many years.

Reinsurance Tightness for Catastrophic Medical Towers

The medical professional liability insurance market is also constrained by tighter reinsurance conditions, as catastrophic hospital risks now require more participants to assemble the same level of excess coverage. WTW reported that many excess carriers have reduced per-risk participation to USD 5 million to USD 10 million per layer, down from the USD 15 million to USD 20 million positions that were more common 5 years ago. This means health systems must build taller towers with more insurers, which increases transaction complexity and creates more negotiation points around exclusions, attachment levels, and renewal timing. In 2026, excess layer pricing was up 40% or more on standard layers in several healthcare placements, with additional pressure in programs carrying sensitive abuse-related exposures. The medical professional liability insurance market still benefits from firm pricing under these conditions, but the same capacity shortage can also suppress written premium growth when buyers cannot secure the full limits they want. Reinsurance tightness, therefore, supports rate strength while limiting coverage availability for the highest-risk hospitals and integrated systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Claims-Made Coverage Remains the Core Structure

Claims-made coverage held 77.56% of the coverage-type segment in 2025, and this part of the medical professional liability insurance market is forecast to grow at a 7.1% CAGR from 2026 to 2031. Its lead reflects the way most commercial carriers and hospital systems prefer a structure that links coverage to the reporting period and makes reserve management more responsive to current loss conditions. In the medical professional liability insurance market, that flexibility matters because carriers can respond more quickly to severity pressure rather than carrying perpetual exposure to older underwriting years. Claims-made forms also align more closely with the capital and reporting disciplines expected under state insurance supervision and risk-based capital frameworks. This is why claims-made business continues to anchor portfolio economics, even when reserve shocks persist within that structure.

The reserve record shows both the strength and the burden of this model. Claims-made carriers recognized USD 259 million in adverse development in 2025, while occurrence business posted USD 15.7 million in favorable development during the same period, which showed where severity pressure was most visible in current reporting. Occurrence coverage still has a place for hospitals and physician groups that want continuing protection without later tail purchases when a clinician exits a practice or changes employment. Even so, the pricing challenge posed by very long liability tails limits faster adoption of occurrence forms while severity is still rising. The medical professional liability insurance industry, therefore, continues to lean toward claims-made products because they provide a cleaner path for rate correction, reserve recognition, and capital planning.

By Claim Category: Diagnosis-Related Claims Continue to Lead

Diagnosis-related claims accounted for 32.67% of the segment in 2025, and this portion of the medical professional liability insurance market size is projected to expand at a 7.6% CAGR from 2026 to 2031. Misdiagnosis, delayed diagnosis, and failure to diagnose remain central because they combine high frequency with the potential for severe patient outcomes and large awards. The medical professional liability insurance market keeps this category at the front because diagnostic failures often involve complex questions of judgment, documentation, escalation, and timing rather than a single visible procedural error. Those features can make both causation and defense strategy more difficult when a case reaches litigation. The category also benefits from the broader shift toward digital and virtual care, where incomplete examination and fragmented information can complicate the diagnostic record.

Telehealth adds another layer to this pattern because virtual interactions can leave more ambiguity around physical examination, symptom interpretation, and patient follow-up. The American Medical Association's telehealth adoption data supports the view that remote care is now mainstream, which means the underlying exposure base for diagnostic disputes is no longer narrow. Treatment-related and procedure-related claims remain the second-largest block of exposure, as outpatient and ambulatory procedure volumes continue to rise across several specialties. Medication-related claims are also receiving more attention in markets that are digitizing prescribing and recordkeeping, which improves traceability but can also more clearly highlight system-based mistakes. Obstetrics continues to stand out as the highest-severity subcategory, and the American Medical Association reported that ob-gyns face a career-lawsuit probability near 60%, with premiums for the specialty reaching USD 243,988 in Florida in 2025.

By Insured Entity Type: Individual Practitioners Lead, Institutions Grow Faster

Individual practitioners held 56.89% of the insured-entity segment in 2025, making them the largest block of the medical professional liability insurance market by insured count and premium volume. This position reflects the scale of the physician and surgeon base, the broad requirement for personal professional liability coverage, and the continued need for standalone protection even when doctors work inside larger delivery systems. The medical professional liability insurance market also includes dentists, nurses, and allied health professionals, whose independent clinical responsibilities are increasing as scope-of-practice rules expand in several jurisdictions. In regulated markets, liability coverage is not discretionary, which supports steady renewal demand even in periods of tighter pricing. That is why the practitioner segment remains the volume anchor for the line.

Institutional and facility providers are projected to record the fastest CAGR of 8.4% from 2026 to 2031, indicating that organized healthcare is absorbing a greater share of aggregate exposure. Hospitals, health systems, clinics, ambulatory surgery centers, nursing homes, and diagnostic providers are all seeing broader risk-transfer needs as care shifts to more distributed settings. Germany's physician liability requirement also illustrates how regulatory frameworks sustain demand across both individual and organized care structures, even when the delivery model differs by country. Large health systems are also concentrating liability into shared programs and excess towers, which increases the premium weight of institutional placements relative to the historical physician-only model. Within the medical professional liability insurance market, that shift gives facility coverage a stronger growth path than the already mature practitioner segment.

By Distribution Channel: Captives, RRGs, and Self-Insurance Gain Ground

Captives, risk retention groups, and self-insurance programs led the distribution channel segment with a 33.72% share in 2025 and represented the fastest-growing route in the medical professional liability insurance market at an 8.8% CAGR through 2031. Their strength reflects organized healthcare's preference for retaining and managing risk when internal claims data supports more selective capital deployment than the commercial market can offer. Risk Retention Reporter stated that risk retention group premium surpassed USD 6 billion in 2025, rising 11.7% from USD 5,380 million in 2024, and healthcare contributed the largest absolute dollar increase among sectors. This confirms that alternative risk channels are no longer marginal within the medical professional liability insurance market and are instead a central part of how larger systems finance liability. These structures have gained relevance because they combine underwriting control, data ownership, and reinsurance access in ways that many hospital systems now prefer.

The strategic value of these channels is tied to information as much as cost. Large systems with deep closed-claims history can separate profitable sub-pools from weaker ones and decide which risks to retain, which to cede, and which to place into layered programs. Retail brokers and wholesale brokers still matter for smaller facilities and individual practitioners that do not have the scale to form alternative vehicles. Direct and institutional placement channels are also growing as health systems extend negotiated coverage to employed and affiliated clinicians. The medical professional liability insurance industry is therefore moving toward a more segmented placement model, where large buyers use captives and RRGs for control, while smaller insureds continue to rely on brokered and sponsored access.

Geography Analysis

North America held 62.34% of the medical professional liability insurance market share in 2025, and the region remains the primary demand center, combining a large private healthcare base with a highly developed tort environment. The United States drove most of that scale and recorded the seventh consecutive annual rise in physician premiums in 2025, while the American Medical Association reported that 36 states saw at least 1 premium increase. The medical professional liability insurance market in North America is also shaped by major differences in tort law, damage caps, and legal climate from one state to another, which makes local underwriting discipline more important than national averages. Canada follows a different model because public indemnity arrangements soften some of the private-market volatility seen in the United States. Mexico remains a smaller and less mature private liability market, but growth is linked to the expansion of private hospitals and specialist care.

Europe presents a more mandate-driven structure in the medical professional liability insurance market, as liability coverage is often anchored in professional regulation, public indemnity design, or a mix of both. Germany requires liability insurance for licensed physicians, which supports recurring premium demand even when practice settings differ across individual and group structures. The United Kingdom follows a distinct pattern in which National Health Service indemnity schemes absorb much of the hospital risk, while private demand is concentrated among independent consultants and general practice partners. France and other continental markets still face long-tail complexity because civil liability cases can take extended periods to resolve and reserve. Europe is therefore more stable in terms of mandatory demand, yet still complex in legal structure, technical margins, and cross-country claims behavior.

Asia-Pacific is the fastest-growing regional market for medical professional liability insurance and is forecast to expand at a 9.2% CAGR from 2026 to 2031. Growth is tied to greater patient rights awareness, the spread of private healthcare, and the gradual formalization of professional liability across large and mid-sized healthcare systems. In Japan, the market continues to benefit from structured physician liability arrangements, and Sompo Japan launched a medical accident data analysis service for hospital clients in June 2025 to support loss prevention through closed-claim analytics. South America, the Middle East, and Africa still account for smaller shares of the medical professional liability insurance market, but they are adding incremental volume as private hospital capacity expands in countries such as Brazil, Saudi Arabia, and the United Arab Emirates. Mandatory practitioner coverage in parts of the Gulf and the rise of organized private providers across emerging markets support long-term expansion, even though insurance penetration remains below the healthcare revenue base in many of these systems.

Competitive Landscape

The medical professional liability insurance market is moderately concentrated among specialist carriers, with physician-owned companies, mutuals, and reciprocals holding strong positions because they combine specialty underwriting with long records of closed-claim data. The most important competitive event is The Doctors Company's pending acquisition of ProAssurance, announced in March 2025 for USD 25 per share, which is expected to create the largest physician-owned medical liability carrier in the United States once approvals are completed. This deal matters because a larger scale improves reserving discipline, expands physician risk-management reach, and strengthens bargaining power in reinsurance negotiations. The medical professional liability insurance market also continues to rely on Bermuda and London participants for excess hospital capacity when admitted United States markets pull back from complex placements. That leaves the specialist leaders with an advantage in both primary underwriting depth and access to layered capacity.

Competitive pressure is also rising from new technology-led entrants at the smaller end of the medical professional liability insurance market, including physician practices and groups. Indigo raised USD 50 million in January 2026 to scale automated underwriting and expand broker distribution, and the company had already reached 20% of submissions fully automated by the end of 2025. This matters because automation can shorten placement cycles, standardize risk review, and improve operating efficiency in a line that historically depended on manual file handling and specialty coding. Some insurers are also starting to tie underwriting terms to AI governance and digital clinical controls, which moves competition beyond price and into risk-management credibility. The medical professional liability insurance market is therefore seeing a clearer split between scale-led specialists and process-led entrants, with both sides seeking to improve loss selection.

Large global carriers remain relevant where cross-border health systems need coordinated coverage, captive support, or multinational program design that a domestic specialist may not be able to provide on its own. At the same time, not every company often cited around healthcare insurance is a true primary underwriter in this line, because brokers such as Aon, Marsh McLennan, and Arthur J. Gallagher & Co. distribute and advise on medical professional liability placements without bearing the primary risk themselves. More relevant carrier references for underwriting participation include Curi Holdings, Sompo International, and Hanover Insurance Group, which are more closely aligned with risk-bearing roles in the medical professional liability insurance market. PointBridge Partners and Aspen also added new admitted physician liability capacity across 15 states in the United States from January 1, 2026, demonstrating that selective new program formation is still possible even in a disciplined pricing environment. Competition, therefore, remains active, but it favors players with either a deep specialty scale, targeted program design, or a sharper operating model.

Medical Professional Liability Insurance Industry Leaders

Berkshire Hathaway Inc.

The Doctors Company

ProAssurance Corporation

Coverys

MagMutual Insurance Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sompo Japan and SOMPO Risk Management launched the "Medical Accident Data Analysis Report" service, providing hospital clients with analytics on national malpractice trends by specialty and procedure type, aiming to reduce claim frequency through proactive clinical risk management.

- January 2026: Indigo, the AI-driven medical professional liability platform, raised USD 50 million in new funding to accelerate automated underwriting, expand its national broker distribution network, and scale operations. By the end of 2025, Indigo's Lux platform had fully underwritten 20% of all submissions without human intervention.

- January 2026: PointBridge Partners and Aspen Insurance launched an admitted physicians professional liability program across 15 states in the United States, starting January 1, 2026, targeting licensed physicians, surgeons, and professional corporations with competitively priced coverage backed by an AM Best A-rated carrier.

- June 2025: ProAssurance Corporation shareholders overwhelmingly approved the company's proposed acquisition by The Doctors Company for USD 25 per share, with regulatory approvals still pending in California and Pennsylvania, and closure anticipated by June 30, 2026

Global Medical Professional Liability Insurance Market Report Scope

| Occurrence-Based Coverage |

| Claims-Made Coverage |

| Diagnosis-Related (Misdiagnosis, Delayed Diagnosis, Failure to Diagnose) |

| Treatment / Procedure-Related (Surgical Errors, Anesthesia Errors, Wrong-Site Procedures) |

| Medication-Related Errors |

| Obstetrics / Childbirth-Related Injuries |

| Other Allegations (minimized residual category) |

| Individual Practitioners | Physicians & Surgeons |

| Dentists | |

| Nurses & Allied Health Professionals | |

| Other Individual Practitioners | |

| Institutional / Facility Providers | Hospitals & Health Systems |

| Clinics, Ambulatory Surgical Centers & Outpatient Facilities | |

| Nursing Homes / Long-Term Care Facilities | |

| Diagnostic & Ancillary Service Providers | |

| Other Institutional Providers |

| Retail Agents & Brokers |

| Wholesale / Surplus Lines Brokers |

| Captives, Risk Retention Groups (RRGs) & Self-Insurance Programs |

| Direct / Institutional Placements (including hospital-sponsored programs for employed physicians) |

| Other Channels (e.g., MGAs, affinity programs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Coverage Type | Occurrence-Based Coverage | |

| Claims-Made Coverage | ||

| By Claim Category | Diagnosis-Related (Misdiagnosis, Delayed Diagnosis, Failure to Diagnose) | |

| Treatment / Procedure-Related (Surgical Errors, Anesthesia Errors, Wrong-Site Procedures) | ||

| Medication-Related Errors | ||

| Obstetrics / Childbirth-Related Injuries | ||

| Other Allegations (minimized residual category) | ||

| By Insured Entity Type | Individual Practitioners | Physicians & Surgeons |

| Dentists | ||

| Nurses & Allied Health Professionals | ||

| Other Individual Practitioners | ||

| Institutional / Facility Providers | Hospitals & Health Systems | |

| Clinics, Ambulatory Surgical Centers & Outpatient Facilities | ||

| Nursing Homes / Long-Term Care Facilities | ||

| Diagnostic & Ancillary Service Providers | ||

| Other Institutional Providers | ||

| By Distribution Channel | Retail Agents & Brokers | |

| Wholesale / Surplus Lines Brokers | ||

| Captives, Risk Retention Groups (RRGs) & Self-Insurance Programs | ||

| Direct / Institutional Placements (including hospital-sponsored programs for employed physicians) | ||

| Other Channels (e.g., MGAs, affinity programs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in medical professional liability insurance?

Growth is being supported by rising claim severity, higher premium rates, expanding outpatient exposure, and stronger demand from institutional healthcare providers. The market is forecast to reach USD 26.24 billion by 2031 at a 6.9% CAGR.

Which coverage type leads this space?

Claims-made coverage led with 77.56% share in 2025 and is forecast to grow at 7.1% CAGR through 2031, reflecting its stronger reserve management and pricing responsiveness.

Which claim category is the most important?

Diagnosis-related claims held 32.67% share in 2025 and are projected to grow at 7.6% CAGR, making them the largest and fastest-growing claim category in the current segmentation.

Why is North America the largest regional contributor?

North America held 62.34% share in 2025 because of its large insured healthcare base, developed tort system, and sustained premium increases across many states in United States.

Which distribution channel is expanding the fastest?

Captives, risk retention groups, and self-insurance programs are growing the fastest, with 33.72% share in 2025 and an expected 8.8% CAGR through 2031.

How is technology changing underwriting and claims handling?

Digital underwriting, automation, telehealth exposure review, and AI governance are becoming more important. Indigo's funding round and Sompo Japan's new analytics service show how carriers are putting more weight on data and process efficiency.

Page last updated on: