Medical Drone Delivery Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 4.07 Billion |

| Growth Rate (2026 - 2031) | 32.46% CAGR |

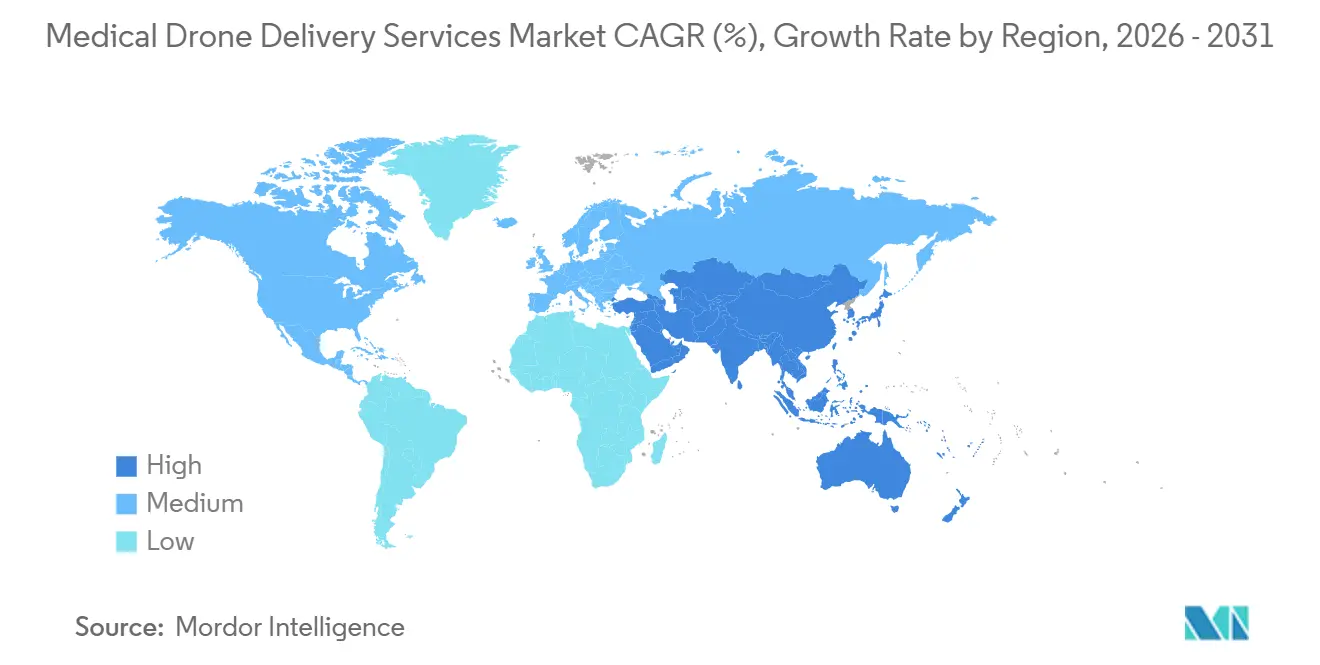

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Drone Delivery Services Market Analysis by Mordor Intelligence

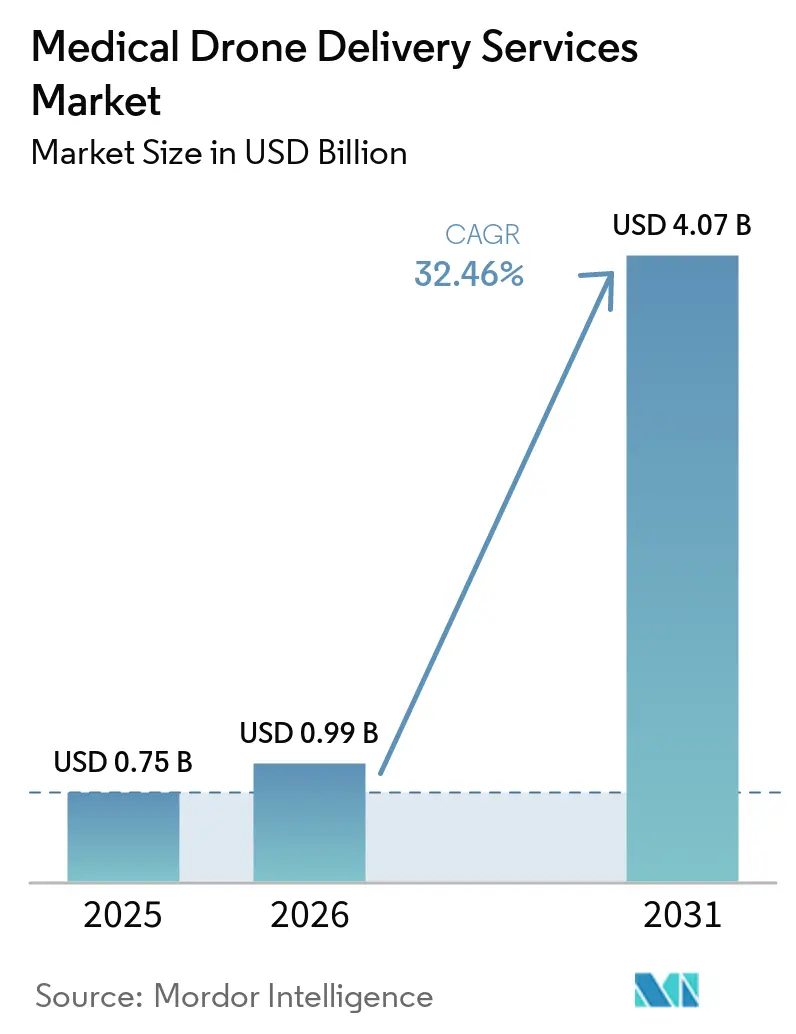

The Medical Drone Delivery Services Market size is expected to increase from USD 0.75 billion in 2025 to USD 0.99 billion in 2026 and reach USD 4.07 billion by 2031, growing at a CAGR of 32.46% over 2026-2031.

Converging forces, routine BVLOS approvals, national public-health mandates, and the economics of hospital-at-home care, have moved the service from pilot projects to mission-critical logistics infrastructure. In the near term, performance-based regulations such as the FAA’s proposed Part 108 and the UK CAA’s phased BVLOS roadmap lower compliance friction, letting operators shift from single-route waivers to autonomous, multi-facility networks. Hospital systems pairing telehealth with automated inventory triggers now treat drones as the default courier for time-critical, small-batch payloads, especially blood components and high-value biologics. Platform economics also favor fixed-wing and hybrid VTOL designs that stretch range to 100 km while tripling daily launch capacity, unlocking hub-and-spoke models that match airline utilization levels. Finally, capital flows are accelerating as municipalities fund AED and trauma-kit dispatch programs, and as donor-backed African networks prove that predictable demand turns drones into a lower-cost alternative to four-by-four fleets.

Key Report Takeaways

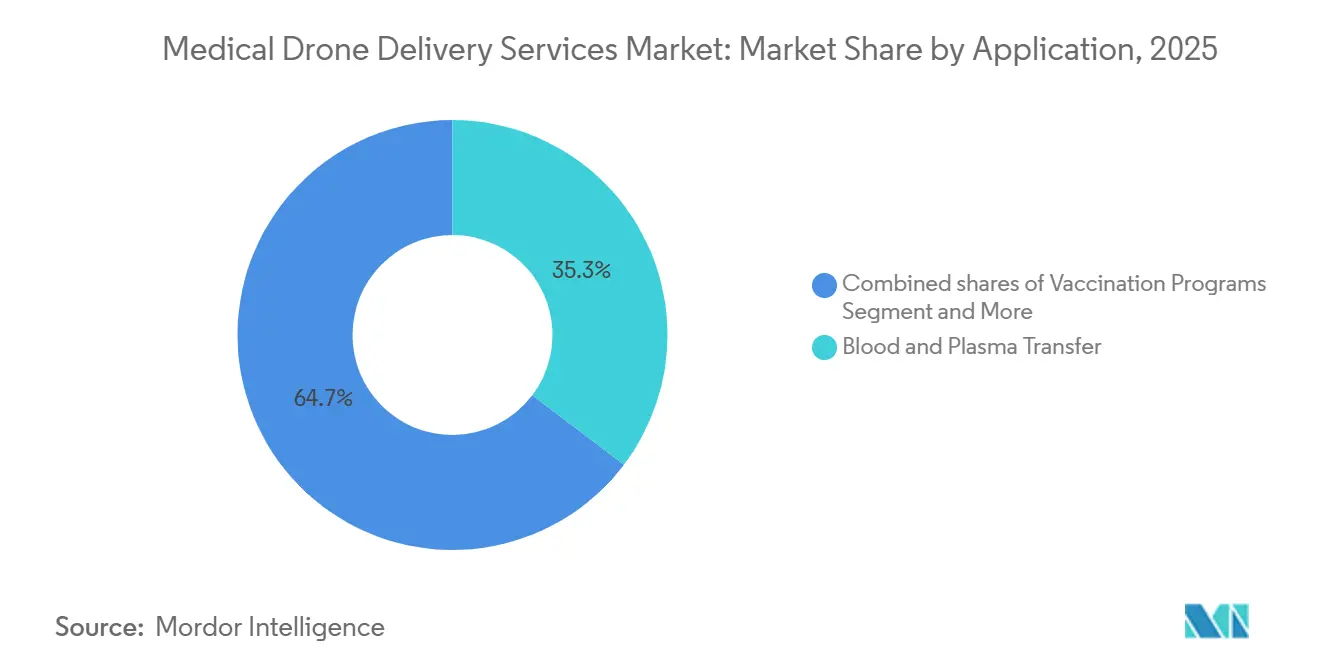

- By application, blood and plasma transfer led the medical drone delivery services market with 35.31% of the market share in 2025, while organ & tissue transport is advancing at a 33.64% CAGR through 2031.

- By platform, fixed-wing systems captured 45.21% of the market in 2025; hybrid VTOL is the fastest-growing configuration, with a 34.31% CAGR to 2031.

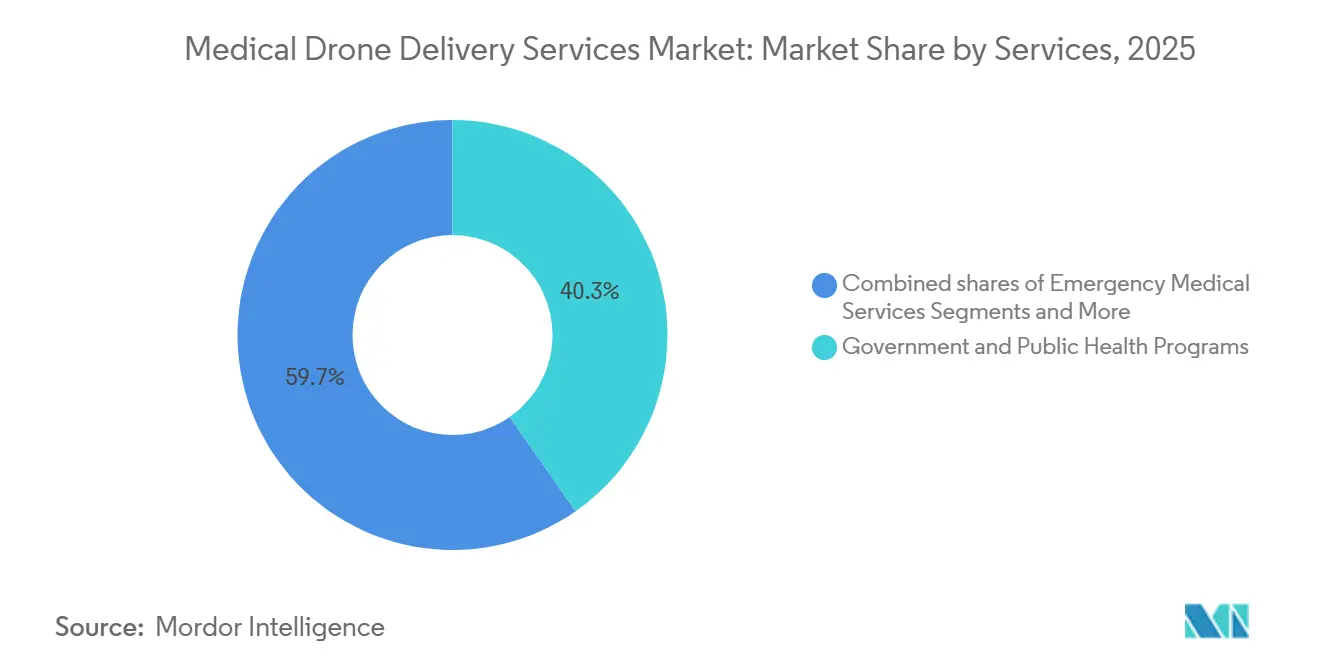

- By end-user, government and public-health programs commanded a 40.31% share in 2025; emergency medical services networks are rising fastest, with a 34.94% CAGR.

- By delivery model, the B2B facility-to-facility route accounted for 49.56% of the medical drone delivery services market in 2025, and B2C Home & Hospital-at-Home is set to grow at a 34.41% CAGR to 2031.

- By geography, North America retained a 39.23% share in 2025; Asia-Pacific is forecast to grow at a 35.61% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Drone Delivery Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National-scale public health programs adopting routine drone logistics | +8.2% | Sub-Saharan Africa, South Asia, with spillover to Latin America | Medium term (2-4 years) |

| BVLOS normalization enabling 1-to-many operations and scale | +9.5% | North America, Europe, Australia | Short term (≤ 2 years) |

| Hospital-at-home and telehealth driving small-batch prescription fulfillment | +5.1% | North America, Western Europe | Medium term (2-4 years) |

| Cold-chain last-mile for temperature-sensitive vaccines and biologics | +4.3% | Global, with concentration in tropical and remote regions | Long term (≥ 4 years) |

| Integration with hospital/LIS/ERP for automated replenishment | +3.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| UTM/ADSP services reduce airspace friction and operational cost | +6.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

National-Scale Public-Health Programs Adopting Routine Drone Logistics

Government-funded networks in Ghana, Rwanda, and India have moved from demonstrations to institutional procurement, cutting vaccine spoilage by up to 80% and blood waste by 67% while achieving nationwide coverage within five years. These outcomes show that the medical drone delivery services market can displace ground fleets when demand is predictable, roads are poor, and clinical urgency is high. WHO’s 2024 ultra-cold-chain guidance further legitimizes drones for mRNA campaigns, providing a template for budget allocation. Ministries are therefore bundling drones into their essential-health-services line items, ensuring steady flight volumes that underpin commercial sustainability.

BVLOS Normalization Enabling 1-to-Many Operations and Scale

The proposed U.S. Part 108 rule and the UK CAA’s 2025 roadmap codify performance criteria for detect-and-avoid, C2 links, and air-risk assessment, turning waiver-only permissions into repeatable certifications. DroneUp’s BVLOS approval in 2024 let it serve multiple Walmart pharmacies from one hub, slashing per-delivery labor costs by 60%. In Europe, U-space regulations mandate electronic conspicuity across 27 countries, letting cross-border operators treat the EU as a single market. These aligned frameworks accelerate the medical drone delivery services market because route expansion now scales through software updates rather than new exemptions.

Hospital-at-Home and Telehealth Driving Small-Batch Prescription Fulfillment

Medicare’s 2025 reimbursement expansion spiked the hospital-at-home population by 40%, creating hour-level delivery windows that ground couriers cannot meet economically. Walmart, CVS, and regional health systems therefore turned to drones for antibiotics, anticoagulants, and biologics, achieving sub-30-minute lead times in Dallas-Fort Worth pilots. Secure drop-boxes and HL7 FHIR-based notifications close the last-50-meter gap, while state regulators are finalizing residential airspace guidance, unlocking broader B2C scale.

Cold-Chain Last-Mile for Temperature-Sensitive Vaccines and Biologics

UPS Flight Forward’s FDA-cleared temperature-monitoring payload keeps vaccines between –80 °C and –60 °C for six hours, meeting GDP and chain-of-custody standards. Zipline’s combination of phase-change materials plus active Peltier cooling delivered five million ultra-cold doses in Ghana without a single excursion[1]Zipline, “National Service Impact Ghana & Rwanda,” flyzipline.com. These proofs reduce spoilage in tropical zones where road delays and inconsistent refrigeration erode potency, giving the medical drone delivery services industry a clear advantage over van-based couriers during outbreaks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex, evolving BVLOS/airspace approvals limit routine ops | -5.4% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Weather, payload, and battery-energy-density constraints | -3.8% | Global, with higher impact in extreme climates | Long term (≥ 4 years) |

| Community noise/acceptance constraints in dense areas | -2.1% | Urban North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Unit economics sensitive to labor intensity until 1-to-many is routine | -4.2% | Global, particularly in high-labor-cost markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex, Evolving BVLOS/Airspace Approvals Limit Routine Ops

Even with rulemaking underway, operators still navigate 12- to 24-month certification cycles under FAA waivers and EASA SORA, depressing ROI by 40–60% versus pre-approved corridors. Smaller firms lack the capital to endure multi-year burn, tilting the medical drone delivery services market toward well-funded incumbents until automated approval portals mature

Weather, Payload, and Battery-Energy-Density Constraints

Most drones ground at winds above 20 knots or in heavy rain, shaving 20–60% off availability depending on the climate [2]IEEE, “Weather Impact on Unmanned Aircraft Operations,” ieee.org. Payload ceilings of 3.5 kg for Zipline P2 exclude larger organs, while lithium-ion energy density caps keep multirotor endurance near 45 minutes. Solid-state batteries may double range, but commercial certification is unlikely before 2028, limiting near-term service breadth within the medical drone delivery services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Blood Transfer Anchors Utilization

Blood transfer controls the largest share of the medical drone delivery services market, with 35.31% in 2025, as golden-hour trauma protocols and OB hemorrhage cases demand sub-hour replenishment [3]Rwanda Ministry of Health, “Blood Transfusion Service 2024,” moh.gov.rw. Rwanda’s network delivered three-quarters of national blood outside Kigali by air in 2024, halving mortality and slashing waste. Vaccination programs rank second, leveraging WHO-endorsed ultra-cold drone corridors to remote clinics. Diagnostic samples gain momentum as lab turnaround drives oncology and cardiac outcomes, and emergency AED drops post the steepest volume growth, as municipalities target 10% gains in cardiac-arrest survival.

The growth spotlight, however, is shifting to organ and tissue consignments, which are projected to expand at a 33.64% CAGR through 2031, the fastest rate among all applications in the medical drone delivery services market size. Next-generation airframes such as Wingcopter 198 can carry up to 6 kg and support triple-drop missions, enabling transplant networks to test cornea, skin-graft, and bone-marrow runs while meeting cold-chain requirements. Momentum also comes from the FDA’s 2024 green light for battery-powered temperature loggers on drones, a change that gives hospital procurement teams the documentation trail they need for high-value organs.

By Platform: Fixed-Wing Dominates Range Economics

Fixed-wing designs held 45.21% of platform share in 2025 and still set the benchmark for cost per ton-kilometer on rural hub-and-spoke lanes, with some routes posting longer endurance than multirotors on identical battery packs. Zipline’s P2 Zip flies 100 km with 3.5 kg payloads, servicing dozens of clinics from a single dock and pushing utilization rates high enough to drop per-delivery costs into single-digit territory. The medical drone delivery services market, however, is increasingly influenced by hybrid VTOL airframes, which are forecast to grow at a 34.31% CAGR to 2031 as operators seek a single fleet that can land on tight urban rooftops while still reaching distant rural posts.

Wingcopter 198 typifies this hybrid appeal: it lifts vertically, cruises 75 km with a 6 kg payload, and can make three sequential drops without recharging, a profile now in use in Malawi and Ireland’s public health systems.

By End-User: Government Programs Lead, EMS Accelerates

Government and public-health programs underpin 40.31% of the 2025 volume, driven by donor financing and UN-level procurement that treats drones as infrastructure rather than pilots. These contracts insulate operators from consumer-demand volatility and lock in five-year minimum-volume clauses. EMS applications, though smaller, clock a 34.94% CAGR because every minute shaved off response saves life-years valued in six figures. Sweden’s AED network and North Carolina’s trauma-kit flights validate the societal ROI that justifies public spending, a halo effect spreading across OECD municipalities.

Hospitals, pharmacies, laboratories, and blood banks follow distinct digital-integration roadmaps, but all converge on automated dispatch once ERP and LIS links mature. The medical drone delivery services market, therefore, balances policy-driven rural coverage with economics-driven metropolitan corridors, creating complementary revenue layers instead of competing silos.

By Delivery Model: B2B Facility-to-Facility Captures Economics

B2B facility-to-facility routes accounted for 49.56% of 2025 revenue thanks to predictable, high-frequency movements among hospitals, labs, and blood banks, enabling operators to run thousands of flights per year off a single pad and beat courier vans by on cost and turnaround time.

Regulators also clear these paths faster because both ends of the flight are on controlled property with no residential overfly, streamlining risk assessments and insurance quotes. Yet B2C and hospital-at-home missions are gaining speed, set to post a 34.41% CAGR as Medicare’s 2025 rule change swelled the eligible at-home acute-care pool by 40%.

Geography Analysis

North America generated the highest regional revenue, holding 39.23% share, underwritten by Part 135-certified operators and statewide rural-health programs. North Carolina’s 2024 rollout links Appalachia to tertiary centers in under an hour, confirming drones’ comparative advantage over winding mountain roads. The U.S. VA’s 2025 pilot adds federal heft and may scale to 50 centers by 2027. Canada’s first BVLOS approval in the same year serves Indigenous communities, while Mexico explores sandbox corridors from Guadalajara medical districts to regional clinics.

Asia-Pacific posts the steepest outlook, expanding at 35.61% CAGR through 2031. India’s 2024 Drone Rules amendments let Skye Air Mobility replicate Telangana successes across 19 states, while CAAC-backed low-altitude pilot zones in Shenzhen and Hangzhou test urban corridors at megacity scale. Japan solves island medicine gaps via ANA and Yamato flights, mirroring Australia’s CASA-approved Queensland network.

Europe benefits from 2024 U-space enforcement. The UK NHS slices the majority off pathology transit times with Apian routes, Germany funds cross-state organ sample pilots, and Ireland’s HSE adopts Wingcopter hybrids for rural GPs. Middle East & Africa host the oldest national drone grids; Ghana’s six hubs, Rwanda’s countrywide coverage and Kenya’s radiotherapy sample lanes demonstrate year-round resilience even through monsoons. Latin America lags but Brazil’s ANAC is drafting BVLOS norms, hinting at new frontiers for the medical drone delivery services market.

Competitive Landscape

Moderate concentration prevails: Zipline, Wing, Matternet, Wingcopter, and UPS Flight Forward form the top quintet, together controlling a majority of global revenue. Zipline alone runs more than 700 daily flights across five nations, leveraging Platform 2 to boost dock throughput 10-fold and reach 100 km. Wing, backed by Alphabet, corners suburban B2C with precise hover drops. Matternet secures European hospital clusters through ERP-native APIs, while Wingcopter’s triple-drop hybrid surfaces in Ireland and Malawi. UPS integrates drones into its cold-chain backbone, pitching one-invoice simplicity to pharmacy chains.

Smaller challengers thrive on geographic arbitrage. Swoop Aero dominates Pacific islands, TechEagle rides India’s regional tenders, and Skye Air Mobility wraps district-level exclusivity before global majors arrive. Technology differentiation now orbits around detect-and-avoid certification, battery density and seamless hospital-IT plug-ins. Operators able to clear Part 108 or EASA SORA benchmarks earliest stand to capture long-tail contracts as routine BVLOS becomes table stakes for the medical drone delivery services market.

Medical Drone Delivery Services Industry Leaders

Zipline

Wing

Matternet

Wingcopter

UPS Flight Forward

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Zipline secured USD 600 million in new funding to speed up its U.S. rollout, aiming to add service in at least four additional states, including high-volume hubs planned for Houston and Phoenix.

- December 2025: Meituan Drone opened Shanghai’s first scheduled medical drone routes, cutting transit times for blood supplies and diagnostic samples moving between city hospitals.

- January 2025: Arrive AI joined forces with Skye Air Mobility to extend their autonomous, secure drone-delivery platform nationwide across India.

Global Medical Drone Delivery Services Market Report Scope

As per the scope of the report, medical drone delivery services represent a transformative leap in healthcare logistics, utilizing unmanned aerial vehicles (UAVs) to transport critical supplies such as vaccines, blood products, medications, and diagnostic samples. These services are particularly vital for bridging geographical gaps in remote or underserved areas where traditional road infrastructure is often inadequate or impassable due to seasonal weather and difficult terrain.

The medical drone delivery services market is segmented by application, platform type, service model, delivery model, and geography. By application, the market is segmented into blood & plasma transfer, vaccination programs, drugs/pharmaceuticals, organ & tissue transport, diagnostic samples & lab logistics, emergency kits/AED/Antivenom. By platform type, the market is segmented into multirotor, fixed-wing, and hybrid VTOL. By service model, the market is segmented into hospitals & health systems, emergency medical services /ambulance, blood banks & transfusion centers, government & public health programs, pharmacies & distributors, and laboratories/pathology networks. By delivery model, B2B facility-to-facility, B2C home & hospital-at-home, and emergency dispatch to the scene. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Blood & Plasma Transfer |

| Vaccination Programs |

| Drugs/Pharmaceuticals |

| Organ & Tissue Transport |

| Diagnostic Samples & Lab Logistics |

| Emergency Kits/AED/Antivenom |

| Multirotor |

| Fixed-Wing |

| Hybrid VTOL |

| Hospitals & Health Systems |

| Emergency Medical Services (EMS)/Ambulance |

| Blood Banks & Transfusion Centers |

| Government & Public Health Programs |

| Pharmacies & Distributors |

| Laboratories/Pathology Networks |

| B2B Facility-to-Facility |

| B2C Home & Hospital-at-Home |

| Emergency Dispatch to Scene |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Blood & Plasma Transfer | |

| Vaccination Programs | ||

| Drugs/Pharmaceuticals | ||

| Organ & Tissue Transport | ||

| Diagnostic Samples & Lab Logistics | ||

| Emergency Kits/AED/Antivenom | ||

| By Platform Type | Multirotor | |

| Fixed-Wing | ||

| Hybrid VTOL | ||

| By Service Model | Hospitals & Health Systems | |

| Emergency Medical Services (EMS)/Ambulance | ||

| Blood Banks & Transfusion Centers | ||

| Government & Public Health Programs | ||

| Pharmacies & Distributors | ||

| Laboratories/Pathology Networks | ||

| By Delivery Model | B2B Facility-to-Facility | |

| B2C Home & Hospital-at-Home | ||

| Emergency Dispatch to Scene | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is demand for medical drone delivery growing?

Global revenue is forecast to rise from USD 0.99 billion in 2026 to USD 4.07 billion in 2031, a 32.68% CAGR.

Which use case leads current flight volumes?

Blood and plasma transfers held 35.31% share in 2025 and will keep expanding due to trauma-care urgency and rural stock-out risks.

Which region is expanding quickest?

Asia-Pacific posts the fastest outlook at 35.61% CAGR through 2031, propelled by India’s liberal regulations and China’s urban trials.

Why do fixed-wing drones dominate long routes?

They fly 100 km with 3–6 kg payloads at lower energy cost, letting one launch site serve dozens of clinics

Page last updated on: