Medical Device Labeling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.84 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

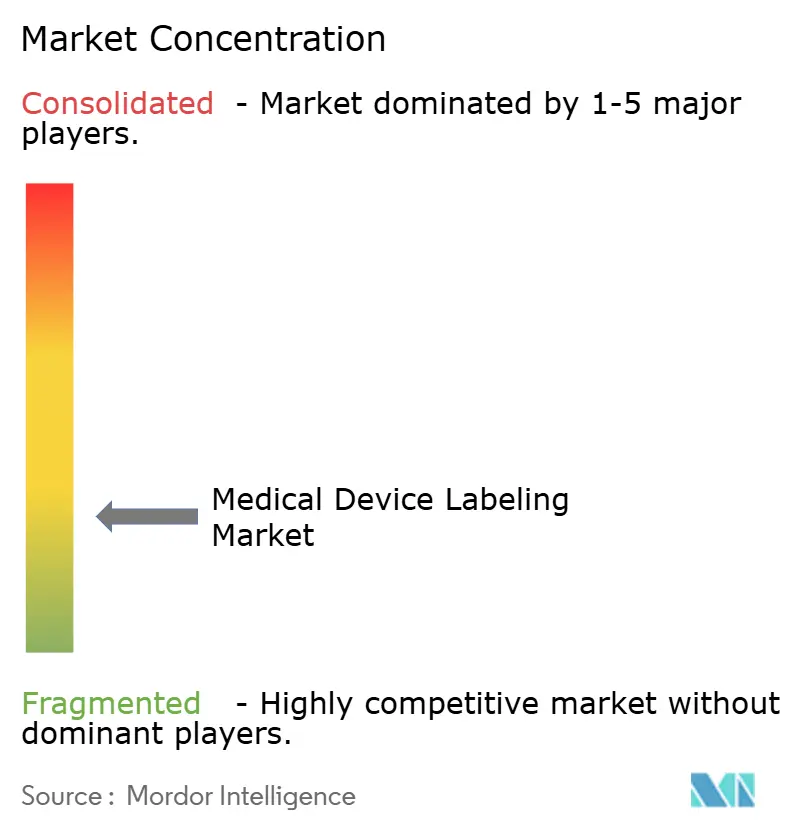

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Device Labeling Market Analysis by Mordor Intelligence

The Medical Device Labeling Market size was valued at USD 1.33 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 1.84 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

Demand growth reflects accelerating unique-device-identification (UDI) mandates, wider adoption of electronic instructions for use (eIFU), and rising multi-language compliance that turns labels into critical data carriers rather than passive tags [1]U.S. Food and Drug Administration, "UDI Basics - Unique Device Identification System," fda.gov. Hospitals rely on serialized QR or Data Matrix codes to automate recall workflows, while manufacturers face swelling stock-keeping-unit counts as every language variant now needs a dedicated label design. Consolidation among label converters is underway because device companies negotiate volume rebates and demand ISO 13485-certified sterilization-compatible printing. At the same time, direct part marking on reusable instruments is reducing external-label usage for orthopedic and endoscopy devices, forcing converters to pivot toward RFID encoding and multi-substrate printing to defend share.

Key Report Takeaways

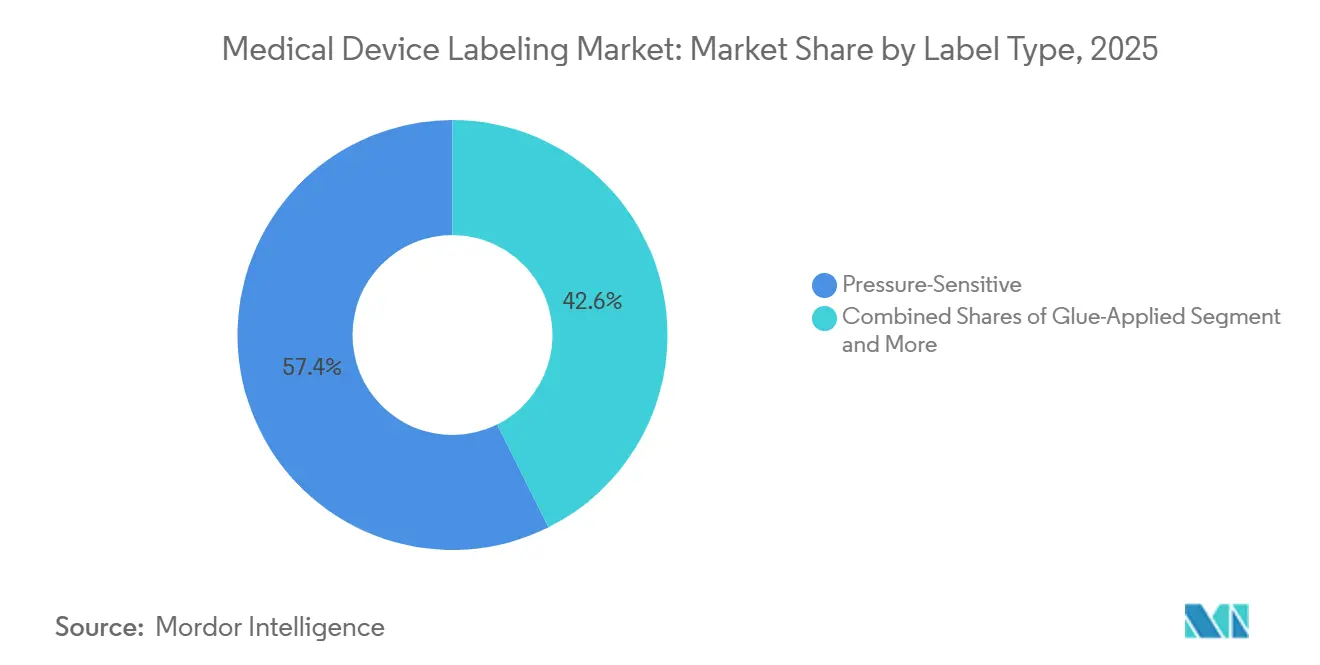

- By label type, pressure-sensitive constructions led with 57.37% of the medical device labeling market share in 2025, while wet-glue labels posted the fastest 5.89% CAGR forecast to 2031.

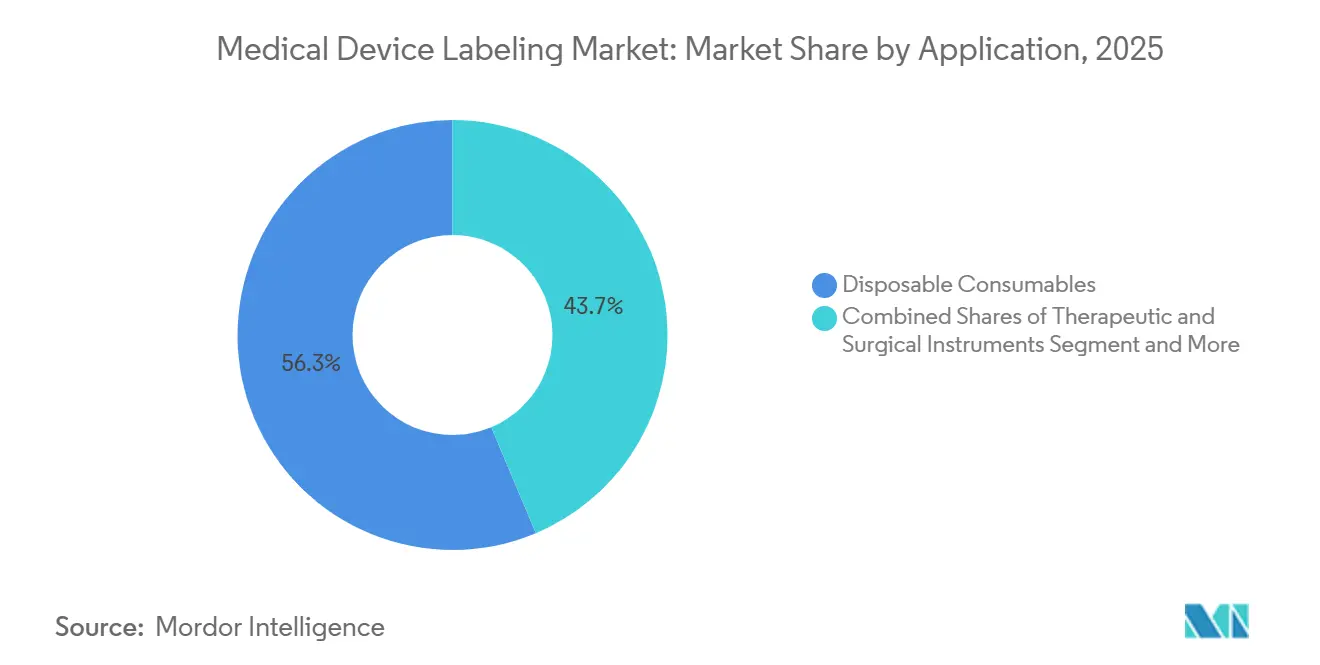

- By application, disposable consumables accounted for 56.34% share of the medical device labeling market size in 2025, whereas therapeutic and surgical instruments are advancing at a 6.12% CAGR through 2031.

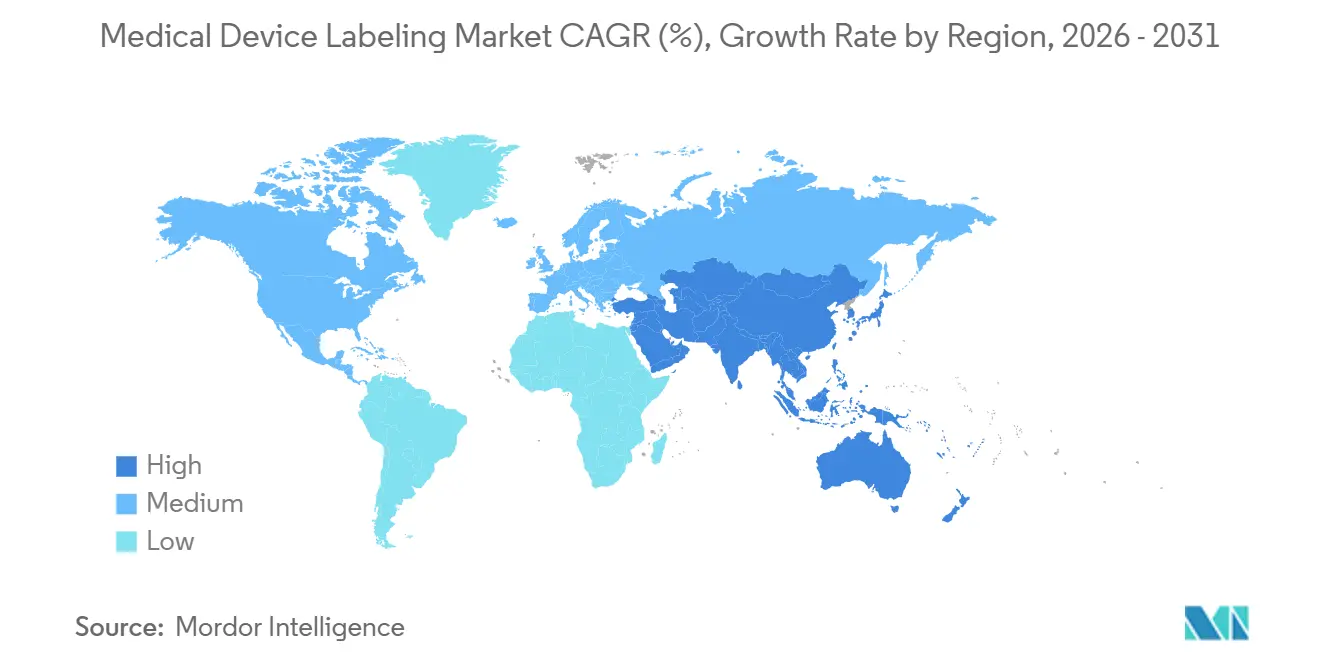

- By geography, North America commanded 45.85% revenue in 2025, yet Asia-Pacific is expected to grow at a 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device Labeling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global UDI mandates and database submissions expand label data and dual-format barcode requirements | +1.2% | Global; North America & EU lead | Medium term (2-4 years) |

| MDR/IVDR multi-language and translation rules increase label SKUs and content volume | +0.9% | Europe; spillover to UK & Switzerland | Short term (≤ 2 years) |

| Rising home-use, wearable, and POCT devices elevate demand for durable, patient-friendly labels | +0.8% | North America & Europe core; Asia-Pacific urban centers | Medium term (2-4 years) |

| Increased recall and track-and-trace needs accelerate 2D-barcode-rich UDI labeling | +0.7% | Global; tightest enforcement in FDA & EU jurisdictions | Short term (≤ 2 years) |

| Adoption of RFID/NFC smart labels for item-level traceability in surgical kits and implants | +0.6% | North America & Europe hospitals; Asia-Pacific pilots | Long term (≥ 4 years) |

| Sterile-processing workflows boost usage of indicator labels and documentation | +0.5% | Global hospital and ASC settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global UDI Mandates and Database Submissions Expand Label Data and Dual-Format Barcode Requirements

The U.S. FDA intensified GUDID enforcement in 2025, issuing warning letters when barcode content and database fields diverged, so converters now validate 2D symbols down to 10 mm × 15 mm labels. China finished its phased UDI rollout in 2024, requiring Class I devices to carry machine-readable identifiers, driving exporters to redesign labels for bilingual text and GS1 or HIBC symbologies [2]National Medical Products Administration, "Unique Device Identification (UDI) System," nmpa.gov.cn. Japan, Singapore, Malaysia, and Brazil adopted similar frameworks, meaning one device model may ship with five or more regional label variants. These mandates push device firms toward cloud label-management systems that automate artwork versioning and regulatory change tracking.

MDR/IVDR Multi-Language and Translation Rules Increase Label SKUs and Content Volume

Under EU Regulation 2025/1234, effective July 2025, professional-use devices may replace paper booklets with eIFU, but each language still needs a unique QR link on the label, multiplying SKUs [3]European Commission, "Medical Devices - New Regulations - Guidance," ec.europa.eu. A single infusion pump can require 24 label designs for the bloc, inflating inventory risk because German-printed stock cannot legally ship to Spain. Translation suppliers report a 30% surge in device-label projects since 2024, and converters that offer in-house language validation win contracts by shortening certification timelines.

Rising Home-Use, Wearable, and POCT Devices Elevate Demand for Durable, Patient-Friendly Labels

FDA guidance published in 2024 obliges manufacturers to test readability with lay users, pushing font sizes from 6-point to at least 8-point and demanding plain-language warnings. Continuous glucose monitors and wearable pumps need labels that survive sweat, disinfectants, and 10-14 day wear periods without skin irritation. U.S. home-use device sales rose 12% in 2025 following reimbursement expansion for remote monitoring, directly lifting label volumes.

Increased Recall and Track-and-Trace Needs Accelerate 2D-Barcode-Rich UDI Labeling

The FDA recorded 87 Class I device recalls in 2024, and hospitals responded by embedding barcode scans into admission and sterilization routines. GS1’s application identifiers allow one Data Matrix to carry serial number, lot, and expiry, minimizing label real estate while maximizing data density. The European EUDAMED database, mandatory for new registrations since 2024, further ties physical labels to cloud records for post-market surveillance

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance burden and frequent regulatory updates raise cost/time-to-market for labelers | -0.6% | Global, with acute pressure in EU (MDR/IVDR) and China (NMPA) | Short term (≤ 2 years) |

| Fragmented label converting landscape intensifies pricing pressure and margin squeeze | -0.4% | Global, most severe in North America and Europe where buyer consolidation is advanced | Medium term (2-4 years) |

| Direct part marking (permanent UDI) displaces some external labels for reusable instruments | -0.5% | North America and Europe, driven by FDA and EU MDR direct marking guidance | Medium term (2-4 years) |

| eIFU adoption reduces paper booklet/leaflet labeling for professional-use devices | -0.3% | Europe leading post-Regulation 2025/1234; North America and Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compliance Burden and Frequent Regulatory Updates Raise Cost/Time-to-Market for Labelers

The EU issued 89 guidance documents between 2021 and 2025, each potentially altering label content, while notified-body backlogs stretch to 12 months, forcing multiple artwork revisions that cost USD 5,000–15,000 per iteration. China published 14 UDI circulars in 2024, and inconsistent provincial enforcement adds uncertainty for exporters. Small manufacturers spend up to a notable share of sales on regulatory affairs versus 2% for multinationals, accelerating industry consolidation.

Fragmented Label-Converting Landscape Intensifies Pricing Pressure and Margin Squeeze

More than 300 regional converters compete, many single-site operators with limited bargaining power. Group-purchasing contracts concentrate a significant share of label spend with five converters, while customers demand 2–3% annual price cuts despite rising ISO 13485 certification and clean-room costs. Gross margins compressed from 28% in 2020 to 22% in 2025, prompting exits and private-equity roll-ups. Direct part marking further erodes demand for reusable-instrument labels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Label Type: Adhesive Chemistry Dictates Sterilization Compatibility

Pressure-sensitive labels held 57.37% of the medical device labeling market in 2025, driven by compatibility with 300–600 labels-per-minute application lines and gamma, ethylene-oxide, and steam sterilization. Acrylic or rubber adhesives maintain bond strength through 50 kGy irradiation without yellowing. Glue-applied or wet-glue labels are forecast to grow at 5.89% through 2031, the fastest rate, as pharmaceutical firms package liquid injectables in glass vials where permanent adhesion outweighs peel-and-reseal convenience. Wet-glue systems create mechanical bonds by penetrating substrates, preventing lift during cold-chain condensation, yet they require 10–15 second dwell times that slow lines to 150–250 units per minute.

Shrink sleeves represented a notable share of volume in 2025, favored for combination products such as pre-filled syringes with integrated safety needles, where 360-degree graphics justify a 30–40% premium. In-mold labels remain niche, applied during blow or injection molding of specimen cups, eliminating post-molding steps. The EU Single-Use Plastics Directive, effective in 2024, exempts medical devices but has prompted evaluation of recyclable face stocks that match container resin. UPM Raflatac launched a linerless construction in 2025 that cuts material waste by 15% and lowers freight costs, appealing to sustainability-focused manufacturers.

By Application: Surgical Instruments Outpace Consumables on RFID Integration

Disposable consumables commanded 56.34% share of the medical device labeling market size in 2025, reflecting the 16 billion syringes used annually in the U.S. alone. Yet therapeutic and surgical instruments are expanding at 6.12% through 2031, the fastest application growth, as hospitals buy capital equipment and embed RFID tags in reusable trays. A single orthopedic procedure consumes 40–60 instruments, each labeled and sterilized 200–300 times over five years, generating recurring demand that dwarfs one-time syringe labeling. Monitoring and diagnostic equipment represented notable shares of volume in 2025, requiring durable labels that survive years of isopropyl-alcohol cleaning and UV exposure.

Home-use and wearable devices are reshaping consumables specifications. Continuous glucose monitors need silicone or hydrocolloid adhesives that balance 10–14 day wear with pain-free removal, replacing aggressive acrylics. The FDA's 2024 patient-labeling guidance mandates comprehension testing, leading to larger fonts and plain-language warnings. Point-of-care testing devices grew significantly in 2025 as distribution shifted to pharmacies, multiplying label variants because over-the-counter devices require consumer-friendly disposal instructions absent from professional equivalents. The convergence of UDI serialization, RFID adoption, and patient-centric design is elevating technical complexity and unit value across all applications, even as competitive pricing compresses converter margins.

Geography Analysis

North America held 45.85% of the medical device labeling market share in 2025, anchored by FDA UDI enforcement and GUDID synchronization requirements. The agency issued 14 warning letters in 2024 for non-compliance, targeting domestic and foreign manufacturers. Canada aligned its Medical Devices Regulations with FDA standards in 2024 and introduced mandatory label-related adverse-event reporting, compelling bilingual French-English labeling for Quebec. Mexico's COFEPRIS adopted UDI in 2025, creating a North American regulatory bloc that simplifies design yet imposes trilingual English-French-Spanish obligations for USMCA distribution.

Europe navigates MDR and IVDR transitions that mandate local-language instructions in Germany, France, Italy, Spain, and Poland, fragmenting label SKUs. The UK's UKCA marking, mandatory in 2024, requires separate labels for Great Britain versus Northern Ireland, which follows EU MDR, forcing parallel inventories. Regulation 2025/1234, effective July 2025, permits eIFU for professional devices but retains QR-code and URL requirements for each language, multiplying designs without reducing print costs.

Asia-Pacific is forecast to grow at 6.08% through 2031, the fastest regional CAGR. China completed UDI rollout in 2024, mandating Class I device identifiers in the NMPA database and driving dual-format barcode adoption. India's Production Linked Incentive scheme channels USD 1.4 billion into domestic manufacturing, favoring local label procurement and attracting multinational converter investment in Pune, Ahmedabad, and Chennai. Japan's PMDA accepted eIFU in 2024, aligning with FDA and EU precedents, yet retained strict on-label Japanese-language and kanji legibility standards. Middle East and Africa, South America, and smaller Asia-Pacific markets collectively represented notable share of revenue in 2025. Brazil's ANVISA published UDI guidelines in 2024, requiring GS1 or HIBC coding for Class III and IV devices by 2026. Australia's TGA harmonized UDI requirements with FDA and EU frameworks in 2024, simplifying Pacific-region design, while South Korea's MFDS mandated Korean-language labeling for imports.

Competitive Landscape

The medical device labeling market remains fragmented, with the top 10 converters capturing the majority of global revenue. CCL Industries acquired three medical-label converters in North America and Europe during 2024–2025, integrating customer lists into its Healthcare & Specialty division and cross-selling RFID solutions. Avery Dennison invested USD 25 million in RFID infrastructure in 2025, installing inlay-encoding lines at Oegstgeest, Netherlands, and Mentor, Ohio, facilities to serve surgical-instrument and implant manufacturers. Smaller converters carve niches in high-complexity applications such as multi-layer booklet labels, linerless constructions, and hybrid indicator-barcode products, where technical differentiation offsets commodity pricing pressure.

White-space opportunities emerge at the intersection of digital labeling and connected devices. Schreiner Group filed four patents in 2024–2025 for RFID constructions that survive 1,000 sterilization cycles and for antenna designs optimized for metal-instrument traceability. Blockchain integration remains nascent, yet pilot projects by Johnson & Johnson and Medtronic in 2025 demonstrated immutable ledgers linking serialized UDI to manufacturing records and clinical outcomes. ISO 13485 certification has become table stakes, with device manufacturers requiring converters to demonstrate validated artwork change control, lot genealogy tracking, and sterility assurance, favoring scale players with dedicated regulatory-affairs teams and automated inspection over smaller shops reliant on manual quality checks.

Medical Device Labeling Industry Leaders

-

CCL Industries

-

Avery Dennison

-

Schreiner Group

-

Brady Corporation

-

All4Labels Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Danaher completed a USD 9.9 billion acquisition of Masimo, a major move into monitoring and data-driven patient care.

- March 2025: CCL Industries completed the acquisition of CleanMark Labels, a U.S. converter specializing in clean-room pressure-sensitive labels for Class II and III devices, adding ISO 13485-certified capacity in North Carolina.

- January 2025: Schreiner Group's MediPharm division launched a hybrid chemical-indicator and 2D-barcode label that integrates steam-sterilization validation with automated tray tracking, reducing sterile-processing documentation time by 40% in pilot deployments at 12 European hospitals.

Global Medical Device Labeling Market Report Scope

As per the scope of the report, medical device labeling is a comprehensive communication framework that extends far beyond the physical stickers affixed to a product. It encompasses all written, printed, or graphic information provided with a device, including its packaging, instructions for use (IFU), user manuals, and even promotional materials.

The medical device labeling market is segmented by label type, applications, and geography. By label type, the market is segmented into pressure-sensitive, glue-applied, shrink sleeves, and in-mold labels. By platform type, the market is segmented into disposable consumables, monitoring & diagnostic equipment, and therapeutic & surgical instruments. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Pressure-sensitive |

| Glue-applied |

| Shrink sleeves |

| In-mold labels |

| Disposable consumables |

| Monitoring & diagnostic equipment |

| Therapeutic & surgical instruments |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Label Type | Pressure-sensitive | |

| Glue-applied | ||

| Shrink sleeves | ||

| In-mold labels | ||

| By Application | Disposable consumables | |

| Monitoring & diagnostic equipment | ||

| Therapeutic & surgical instruments | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value by 2031?

The medical device labeling market is expected to reach USD 1.84 billion by 2031, growing at a 5.58% CAGR from 2026.

Which label type holds the largest share?

Pressure-sensitive labels commanded 57.37% share in 2025, driven by compatibility with high-speed lines and sterilization cycles.

What application segment is growing fastest?

Therapeutic and surgical instruments are expanding at 6.12% through 2031, fueled by RFID integration in reusable instrument trays.

Which region leads in revenue?

North America accounted for 45.85% of revenue in 2025, anchored by FDA UDI enforcement and GUDID submission audits.

Page last updated on: