Medical Device CRO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

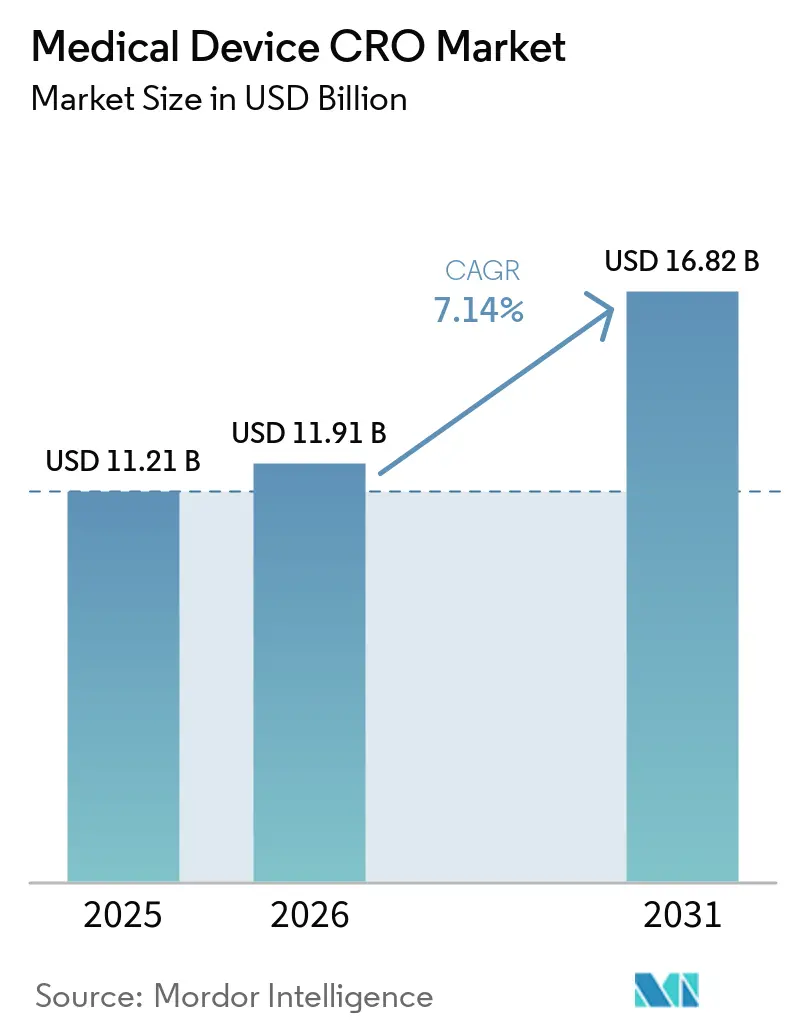

| Market Size (2026) | USD 11.91 Billion |

| Market Size (2031) | USD 16.82 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

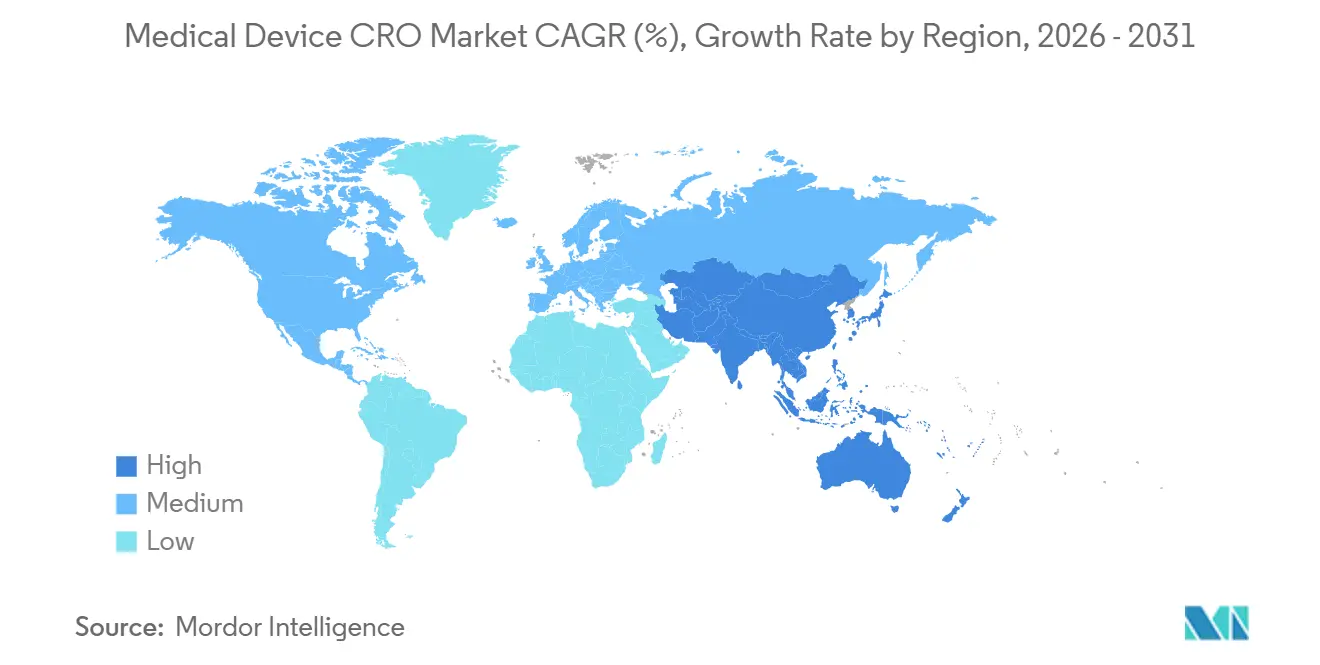

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device CRO Market Analysis by Mordor Intelligence

The Medical Device CRO Market size is expected to increase from USD 11.21 billion in 2025 to USD 11.91 billion in 2026 and reach USD 16.82 billion by 2031, growing at a CAGR of 7.14% over 2026-2031.

The medical device CRO market differs from pharmaceutical outsourcing because device sponsors often need hardware validation, software verification, usability work, and biocompatibility testing within the same submission package, which makes outsourcing needs more fragmented and more technically demanding. The shift to FDA QMSR in February 2026 and the continuing burden of EU MDR and IVDR are pushing sponsors toward specialist partners that can connect engineering, clinical execution, and regulatory work within one program rather than in separate handoffs. The medical device CRO market also stays engaged for longer periods because device development is iterative, and design updates often trigger new rounds of documentation, testing, and revalidation instead of following a clean phase-by-phase model. Cross-border data governance demands and Europe’s certification bottlenecks still slow timing for multinational workstreams, especially when sponsors need aligned evidence packages across regions. Competitive pressure remains moderate to high in the medical device CRO market, and recent consolidation by larger testing and service providers is narrowing the space for mid-sized firms that cannot offer integrated delivery across the lifecycle.

Key Report Takeaways

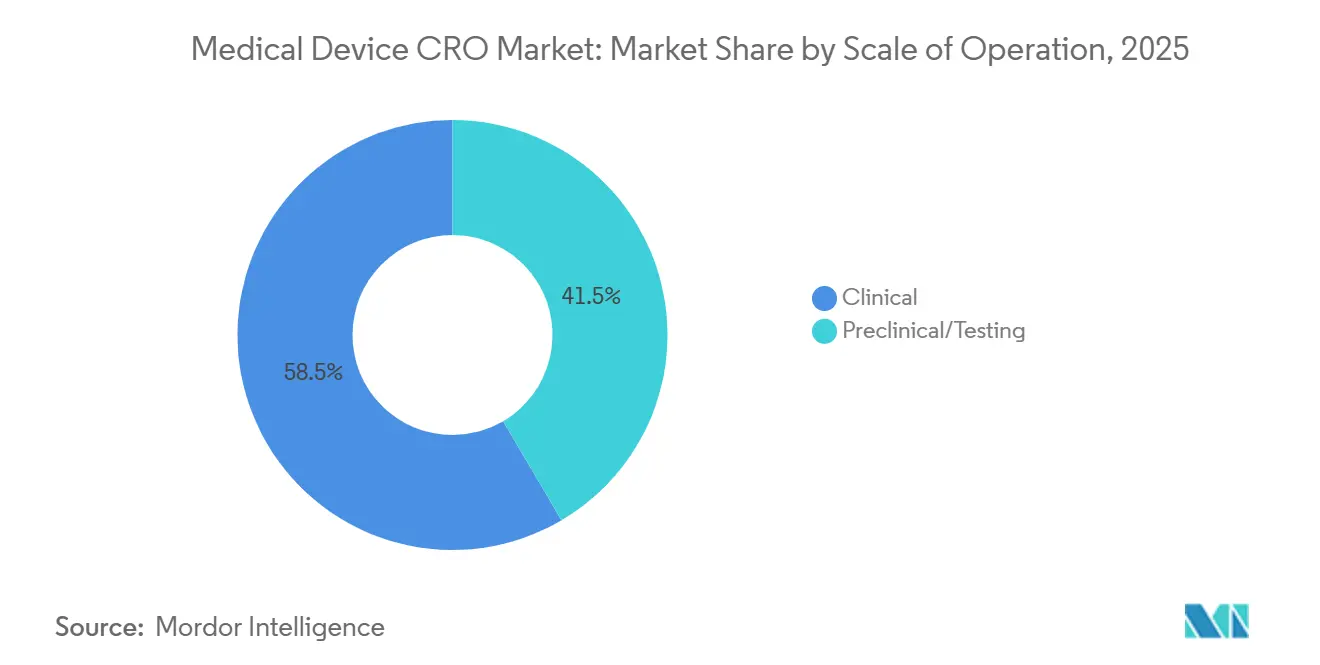

- By scale of operation, clinical services held 58.46% of the market in 2025, and the same sub-segment is projected to expand at a 7.67% CAGR through 2031.

- By service type, Clinical Monitoring led with a 21.29% share in 2025, while Regulatory & Medical Affairs is forecast to grow fastest at a 7.82% CAGR through 2031.

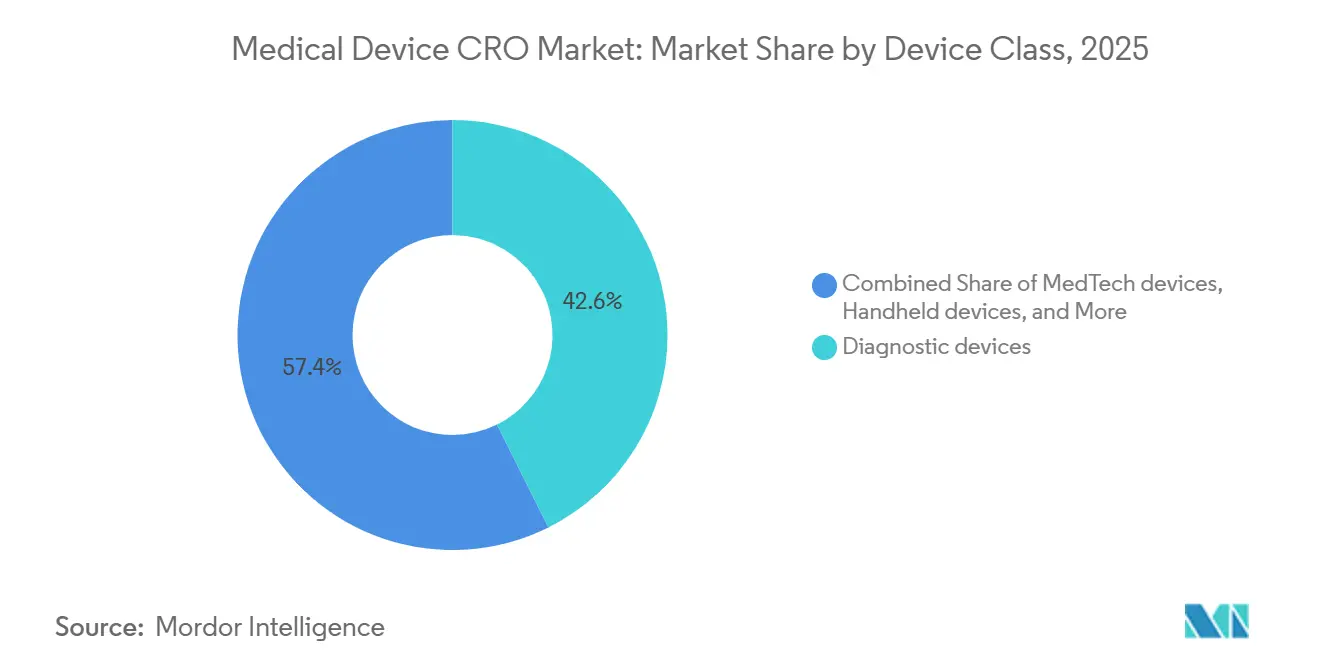

- By device class, diagnostic devices accounted for a 42.64% share in 2025, while MedTech devices are projected to record the highest CAGR at 7.42% through 2031.

- By geography, North America held 45.34% of the market in 2025, while Asia-Pacific is expected to post the fastest regional CAGR at 8.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device CRO Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing Intensifies As Device Trials Grow In Volume And Complexity | +2.0% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| EU MDR And IVDR Evidence And PMCF Requirements Expand Demand | +1.8% | Europe primary, spillover to APAC and North America for global registrations | Medium term (2-4 years) |

| FDA Cybersecurity Requirements And QMSR Alignment Elevate Software Validation Needs | +0.9% | North America primary, EU and APAC follow-on | Medium term (2-4 years) |

| Decentralized Trial Adoption In Devices Increases DHT And eClinical Outsourcing | +1.2% | North America and Europe core, early adoption in APAC | Short term (≤ 2 years) to Medium term (2-4 years) |

| Cross-Border Data Transfer Constraints Drive Privacy Engineering Services | +0.7% | EU, with relevance for North America to EU cross-border programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Intensifies as Device Trials Grow in Volume and Complexity

The medical device CRO market is gaining from a clinical evidence model that now stretches far beyond premarket submission, because post-market surveillance and PMCF are continuous obligations rather than one-time activities. MDCG 2025-10 states that PMS must actively gather and analyze data throughout the life of the device, and that this information must feed back into risk management, clinical evaluation, technical documentation, and corrective action processes. That requirement makes it harder for manufacturers to keep all regulatory, biostatistics, monitoring, and reporting tasks inside their own teams, especially when higher-risk products also require structured reports and ongoing updates.

The medical device CRO market therefore benefits from recurring work on legacy products as well as new launches, since older devices moving into newer frameworks can reopen evidence gaps and trigger fresh outsourcing mandates. Medpace reported full-year 2025 revenue of USD 2,530.2 million, up 20%, and guided for USD 2.755 billion to USD 2.855 billion in 2026, which supports the view that outsourcing demand remained healthy across the broader development services base[1]Medical Device Coordination Group, “MDCG 2025-10 Guidance on Post-Market Surveillance of Medical Devices and In Vitro Diagnostic Medical Devices,” European Commission, health.ec.europa.eu.

EU MDR/IVDR Evidence and PMCF Requirements Expand Demand

MDCG 2025-10 makes the PMS system an integral part of the quality management system, which means clinical evidence work now sits inside a continuous compliance loop instead of a standalone filing exercise. The guidance also states that a PMCF or PMPF plan must be included within the PMS plan, or the manufacturer must justify why that activity is not applicable. Findings from PMCF and PMPF then have to update clinical or performance evaluation, benefit-risk assessment, labeling, technical documentation, and other ongoing compliance records. In the medical device CRO market, that structure increases demand for monitoring, data management, medical writing, vigilance support, and regulatory maintenance because sponsors must keep evidence current after launch and not only before approval. Providers that can combine real-world evidence capabilities with documentation workflows are better positioned as sponsors transfer more of this work outside internal teams that are already stretched by MDR and IVDR obligations.

FDA Cybersecurity Requirements and QMSR Alignment Elevate Software Validation and Cyber Testing Needs

The FDA’s February 2026 cybersecurity guidance gives recommendations on design, labeling, and submission content for devices with cybersecurity risk, and it addresses section 524B expectations for cyber devices. That document replaced the June 2025 guidance, which signals that cybersecurity expectations are moving into a more formal and updated operating standard for device submissions. At the same time, QMSR became effective on February 2, 2026 and incorporated ISO 13485:2016, while emphasizing risk management through design, development, production, and other life-cycle processes. The Federal Register rule also added detailed complaint files, servicing records, and UDI-linked documentation requirements that raise the workload for connected and software-rich device programs. This combination is widening the role of specialized software validation and cyber testing vendors in the medical device CRO market, because many sponsors do not have the internal tools or staff to keep these workflows current at scale[2]Food and Drug Administration, “Medical Devices, Quality System Regulation Amendments,” Federal Register, govinfo.gov.

Decentralized Trial Adoption in Devices Increases DHT/eClinical and Remote-Operations Outsourcing

Decentralized trial adoption is becoming more relevant for the medical device CRO market because devices accounted for 21% of interventional decentralized clinical trial registrations in a global review of 1,370 studies. The same analysis showed that only a small minority of DCTs operated without digital tools, which confirms that remote trial execution now depends on data systems, communication tools, and digital workflows. At the same time, DCT activity remained concentrated in high-income countries, which suggests that remote models are expanding within established research systems before they fully widen access to new patient pools. That pattern still supports outsourcing demand, because sponsors need help with eClinical systems, remote site coordination, distributed data handling, and hybrid monitoring methods across several geographies. The medical device CRO market therefore gains from DCT adoption, but the winners are likely to be providers that can combine digital trial operations with the practical handling needs that device studies still require.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Notified Body Capacity Bottlenecks Elongate EU Certifications | -0.8% | Europe core, secondary impact on North America to EU dual submissions | Short term (≤ 2 years) to Medium term (2-4 years) |

| DCT Patient Recruitment, Tech Access, And Data Governance Hurdles Slow Execution | -0.5% | Global, more pronounced in lower-income and APAC emerging markets | Medium term (2-4 years) |

| Cybersecurity SBOM And Patching Obligations Add Recurring Revalidation Burden | -0.4% | North America primary, EU emerging compliance factor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Notified Body Capacity Bottlenecks Elongate EU Certifications

Notified Body capacity remains one of the clearest timing risks for the medical device CRO market in Europe because certification flow still lags the volume of work moving through MDR and IVDR pathways. MedTech Europe has described notified bodies as a regulatory bottleneck, and that framing aligns with the sustained pressure on sponsors that need approvals, renewals, and evidence updates under tighter rules. When certification timing slips, milestone-linked contracts can delay revenue recognition for CROs even if clinical or documentation work has already been completed. This does not remove demand from the medical device CRO market, but it does make European delivery schedules harder to predict and increases the value of providers that can combine clinical work with close regulatory coordination. In practical terms, the bottleneck shifts competition toward firms that can manage backlog risk, sequence workstreams carefully, and maintain sponsor confidence during long review cycles[3]MedTech Europe, “Notified Bodies Are Becoming a Regulatory Bottleneck,” MedTech Europe, medtecheurope.org.

DCT Patient Recruitment, Tech Access, and Data Governance Hurdles Slow Study Execution

Decentralized models can extend trial reach, but the evidence still shows that most single-country DCT activity is clustered in high-income settings rather than in underserved patient pools. That concentration means the benefits of remote execution are uneven, especially when sponsors expect rapid enrollment gains across markets that have very different digital access and site capabilities. The European Commission has clarified that both the Clinical Trials Regulation and GDPR apply at the same time, which adds obligations on legal basis, storage, archiving, subject rights, security measures, and international data transfers. The EDPB also treated this interplay as a distinct compliance issue, which reinforces how data governance can slow study startup when several parties, systems, and countries are involved. For the medical device CRO market, that means DCT execution still needs more legal, operational, and technical support than many sponsors first assumed, and this narrows the speed advantage that remote models can otherwise offer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scale of Operation: Clinical Services Define the Outsourcing Agenda

Clinical services held 58.46% of the medical device CRO market share in 2025, and the same segment is projected to grow at a 7.67% CAGR through 2031. This lead position reflects more than simple trial volume, because manufacturers now face clinical obligations that continue into the post-market period and feed back into risk management and technical documentation. MDCG 2025-10 makes that continuity explicit by treating PMS as an active, ongoing system that must update benefit-risk assessment, clinical evaluation, and corrective actions throughout the device lifetime. For the medical device CRO market, that means clinical work is no longer concentrated only around the first submission, since PMCF and related evidence maintenance extend activity well after launch. The result is a larger and more durable outsourcing pool for sponsors with Class IIb, Class III, implantable, and software-heavy products that cannot support these tasks internally at the required pace.

Preclinical and testing services remain smaller within the medical device CRO market, yet they are becoming more strategically important because they sit upstream of many later regulatory and clinical decisions. Device sponsors still need biological evaluation plans, chemical characterization, toxicological assessments, and gap analyses that align with current regulatory expectations rather than older approval assumptions. Labcorp’s stated biocompatibility offering shows how these services already cover ISO 10993 testing, chemical characterization, toxicological risk assessment, and support for legacy-device gap reviews tied to current regulatory standards. This keeps the medical device CRO industry dependent on testing providers that can connect bench work to submission strategy, rather than acting only as isolated laboratories at the start of development.

By Service Type: Regulatory & Medical Affairs Outpaces All Other Service Lines

Clinical Monitoring retained a 21.29% share of the medical device CRO market size in 2025, while Regulatory & Medical Affairs is projected to expand at a 7.82% CAGR through 2031. That growth pattern reflects the depth of current regulatory change across the United States and Europe, where sponsors now need more ongoing support on documentation, quality alignment, submissions, and post-market maintenance. QMSR became effective in 2026 and brought ISO 13485:2016 into 21 CFR Part 820, while also preserving FDA-specific record controls such as complaint files, servicing records, and UDI-linked documentation. These requirements make regulatory work more continuous, because sponsors must maintain compliant systems and records across the life of the product instead of assembling a narrow submission file at one point in time. In the medical device CRO market, that turns Regulatory & Medical Affairs into a growth engine for providers that can combine quality, labeling, documentation, and regulator-facing support in one operating model.

Clinical Monitoring still underpins revenue in the medical device CRO market because every broader regulatory shift still depends on reliable site oversight, data flow, and issue escalation during active studies. The growing use of digital tools and remote models is changing how monitoring is delivered, yet it has not reduced the need for disciplined operational control across device programs. Data Management & Biostatistics, Medical Writing, and Patient & Site Recruitment continue to act as enabling functions that make both clinical and regulatory delivery possible at scale. Within the medical device CRO industry, service providers that integrate these functions tightly are in a better position than firms that sell each workstream as a separate task with separate teams and timelines.

By Device Class: Diagnostic Devices Lead, but MedTech Devices Accelerate

Diagnostic devices accounted for 42.64% of the market in 2025, which kept them as the largest device class within the medical device CRO market. Their lead is closely tied to IVDR pressure, because a much larger share of in vitro diagnostics now requires notified body involvement than under the earlier directive. That change increases the amount of performance evidence, documentation work, and quality-system preparation that manufacturers must complete before and after market access. The medical device CRO market therefore sees strong diagnostics demand not only from new products, but also from products moving through reclassification and transition pathways that create additional evidence work. This is one reason diagnostics continue to generate steady outsourcing demand even when certification timing remains uneven across Europe.

MedTech devices are projected to grow fastest at a 7.42% CAGR through 2031, which reflects rising activity around connected systems, software-driven products, and complex implantable platforms. The FDA’s current cybersecurity and QMS expectations raise the amount of validation, documentation, and life-cycle risk management required for these products before sponsors can move efficiently through review and post-market upkeep. Handheld and home-use products are also adding work in the medical device CRO market because they often need evidence packages that connect real-world use conditions with regulatory and quality expectations. Within the medical device CRO industry, the mix is therefore shifting toward providers that can handle software validation, biological safety, clinical evidence, and regulatory writing without forcing sponsors to coordinate several disconnected specialists.

Geography Analysis

North America held 45.34% of the medical device CRO market share in 2025, which made it the largest regional contributor. The United States accounts for most of this position because the regulatory calendar compressed several compliance demands into a short period, especially through QMSR implementation and updated cybersecurity expectations. QMSR now incorporates ISO 13485:2016 by reference, and it also keeps FDA-specific record controls in place, which means manufacturers must manage harmonization without assuming that ISO certification alone replaces FDA inspection or documentation duties. Many sponsors are filling this gap through outsourcing rather than by relying only on internal QA and RA hiring, which helps sustain the North American medical device CRO market even in a more disciplined spending environment. This makes the region the clearest example of how regulation can expand outsourcing demand through compliance complexity rather than through trial volume alone.

Europe remains the second-largest regional cluster in the medical device CRO market, and it is the geography where regulation most directly reshapes the service mix. MDR and IVDR have pushed more post-market evidence, documentation maintenance, and notified body interaction into the operating model, which increases dependence on CROs that can combine clinical and regulatory work. At the same time, notified body bottlenecks continue to complicate timing, which means CRO demand stays strong even while contract conversion and milestone pacing become harder to predict. This leaves Europe as a region with structural demand strength in the medical device CRO market, but also with more visible revenue-timing risk than North America.

Asia-Pacific is forecast to record the fastest 8.32% CAGR in the medical device CRO market size through 2031. The region benefits from expanding device development activity, but local regulatory pathways still make on-the-ground capability important rather than optional. PMDA maintains formal clinical trial notification and consultation structures for medical devices, and those processes reinforce the need for localized regulatory handling rather than a single global template. This supports demand in the medical device CRO market for providers that can combine regional site access, language support, and regulator-facing execution in Japan and neighboring markets. China and India are also broadening the future demand base as domestic manufacturing pipelines create more clinical and regulatory work that sponsors may prefer to outsource. South Korea adds to this regional appeal because a more efficient approval environment can support hybrid trial models and broader regional study footprints. Middle East and Africa, along with South America, remain smaller in the medical device CRO market, yet multinational registration programs in GCC countries, Brazil, and Argentina still create room for international providers with local operating reach.

Competitive Landscape

The medical device CRO market is moderately fragmented, with a limited number of full-service global organizations and a much wider field of specialized firms focused on testing, regulatory affairs, or digital validation. That structure matters because device sponsors often need several disciplines at once, and not every provider can bridge biological safety, clinical operations, software validation, and submission support in one engagement. Consolidation is therefore becoming a practical competitive tool in the medical device CRO market, especially for companies trying to move from narrow capability sets toward end-to-end delivery. NAMSA’s acquisition of WuXi AppTec’s U.S. medical device testing operations in February 2025 expanded laboratory capacity and service breadth, while its January 2026 deal for Labcorp’s early development medical device testing business strengthened testing depth across microbiology, biocompatibility, and related areas. NAMSA also states that more than 70% of global biocompatibility studies are conducted by its organization, which shows how concentrated some compliance-critical niches have already become even though the broader medical device CRO market remains more dispersed.

Other large providers are also broadening reach through targeted portfolio moves rather than relying only on organic expansion. ICON disclosed its USD 92.5 million acquisition of KCR S.A. Group in 2024, and in December 2025 it announced an agreement to acquire ClinicalRM to deepen its position in government-sponsored research and infectious disease work that can also support device programs. The March 2025 full integration of Medidata Clinical Data Studio by ICON also points to a technology-based differentiation path, since the platform brings data from Medidata and non-Medidata sources into a single workflow for data management, review, and central monitoring. These steps show that the medical device CRO market is not competing only on headcount or geographic reach, because platform depth and workflow integration are becoming part of the commercial offer.

Technology is becoming a more visible competitive boundary in the medical device CRO market because sponsors increasingly want one partner that can work across data review, monitoring, quality records, and regulatory documentation without repeated handoffs. At the same time, specialized providers still matter because device work includes narrow but essential categories such as biocompatibility, extractables and leachables, and cyber-focused validation that larger generalist firms do not always control internally. The market is therefore seeing two paths at once, with large firms expanding through acquisition and integration while niche firms defend position through technical depth and faster response in targeted service lines. White space remains most visible where software-rich devices require aligned support across clinical evidence, privacy-aware data handling, and life-cycle quality maintenance. This keeps the medical device CRO market competitive, active, and only moderately concentrated despite the stronger role of a few scaled players in certain testing niches.

Medical Device CRO Industry Leaders

IQVIA

NAMSA

Medpace

Charles River Laboratories

Avania

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: FDA's QMSR (21 CFR Part 820 as amended) became effective on February 2, incorporating ISO 13485:2016 by reference, retiring the Quality System Inspection Technique (QSIT) in favor of an updated inspection process under Compliance Program 7382.850. The QMSR introduces mandatory risk management integration throughout the product lifecycle and new UDI-linked record-keeping requirements, expanding CRO demand for QMS gap assessment and revalidation services.

- January 2026: Labcorp announced the sale of its Early Development medical device testing business to NAMSA. The transaction expands NAMSA's testing capacity across microbiology, biocompatibility, and extractables/leachables, reinforcing its position as the dominant preclinical testing CRO in the medical device sector.

Global Medical Device CRO Market Report Scope

As per the scope of the report, a medical device Contract Research Organization (CRO) is a specialized company that provides outsourced services to medical device manufacturers. These services support the development, testing, and regulatory approval of medical devices. CROs help streamline clinical trials, regulatory submissions, and compliance activities, enabling manufacturers to bring their devices to market more efficiently.

The medical device CRO market is segmented by scale of operation into preclinical/testing phase and clinical phase. By service type, the market is categorized into clinical monitoring services, clinical trial management services, data management & biostatistics services, regulatory & medical affairs services, medical writing services, patient & site recruitment services, safety & pharmacovigilance services, and other services. By device class, the segmentation includes MedTech devices, diagnostic devices, handheld devices, and other devices. By geography, the market is divided into the North American region, European region, Asia-Pacific region, Middle Eastern and African region, and South American region. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Preclinical/Testing |

| Clinical |

| Clinical Monitoring |

| Clinical Trial Management |

| Data Management & Biostatistics |

| Regulatory & Medical Affairs |

| Medical Writing |

| Patient & Site Recruitment |

| Safety & Pharmacovigilance |

| Others (DCT Enablement & eClinical Platforms, Imaging/Core Lab, etc.) |

| MedTech devices |

| Diagnostic devices |

| Handheld devices |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Scale of Operation | Preclinical/Testing | |

| Clinical | ||

| By Service Type | Clinical Monitoring | |

| Clinical Trial Management | ||

| Data Management & Biostatistics | ||

| Regulatory & Medical Affairs | ||

| Medical Writing | ||

| Patient & Site Recruitment | ||

| Safety & Pharmacovigilance | ||

| Others (DCT Enablement & eClinical Platforms, Imaging/Core Lab, etc.) | ||

| By Device Class | MedTech devices | |

| Diagnostic devices | ||

| Handheld devices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in medical device CRO services through 2031?

Growth is being supported by rising regulatory workload, longer post-market evidence needs, and the move from USD 11.91 billion in 2026 to USD 16.82 billion by 2031 at a 7.14% CAGR.

Which service area leads outsourced demand for device sponsors?

Clinical services lead with 58.46% share in 2025, and they are also the fastest-growing scale-of-operation segment with a 7.67% CAGR through 2031.

Why are regulatory and medical affairs growing faster than other service lines?

QMSR, MDR, and IVDR have increased the amount of documentation, quality alignment, and life-cycle compliance work, which is why Regulatory & Medical Affairs is projected to grow at 7.82% through 2031.

Which device class creates the biggest outsourcing opportunity today?

Diagnostic devices held the largest share at 42.64% in 2025 because IVDR has expanded evidence and documentation needs for a wider portion of the category.

Which region is expanding fastest for outsourced device development work?

Asia-Pacific is forecast to grow fastest at 8.32% through 2031, supported by rising regional development activity and the need for localized regulatory execution.

How concentrated is competition among medical device CRO providers?

Competition is moderate rather than highly concentrated, because full-service global firms are active, but many specialized providers still hold important positions in testing, regulatory work, and digital validation.

Page last updated on: