Medical Device CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

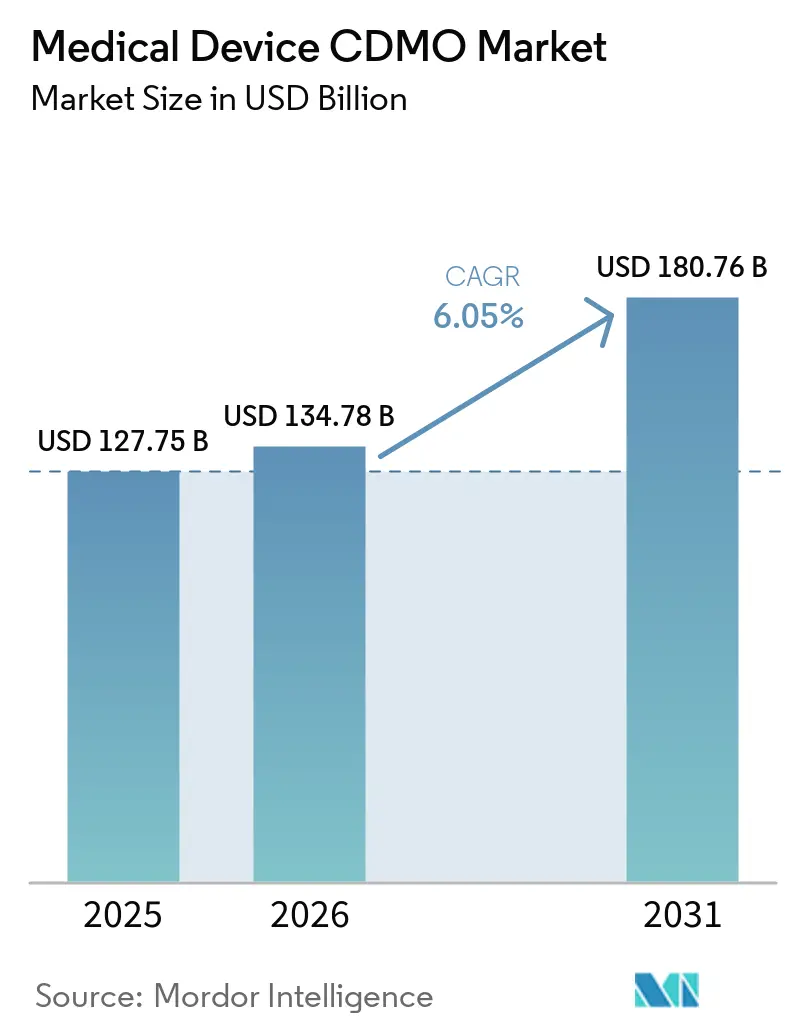

| Market Size (2026) | USD 134.78 Billion |

| Market Size (2031) | USD 180.76 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

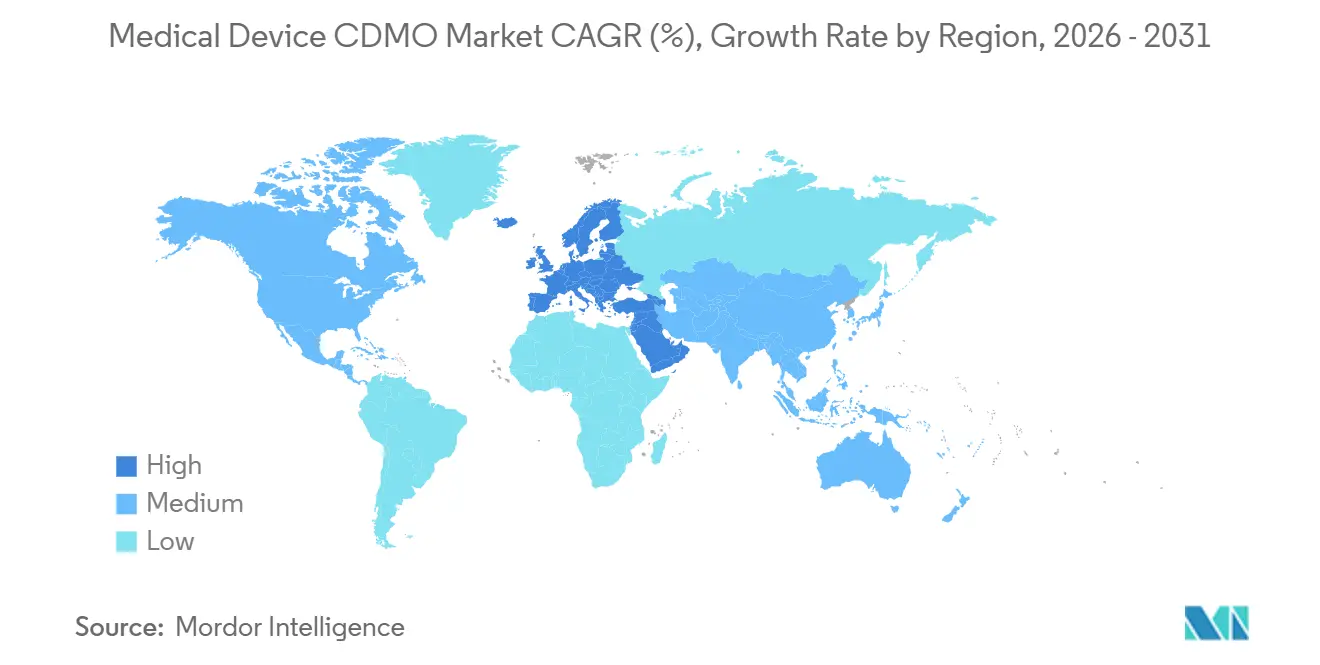

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

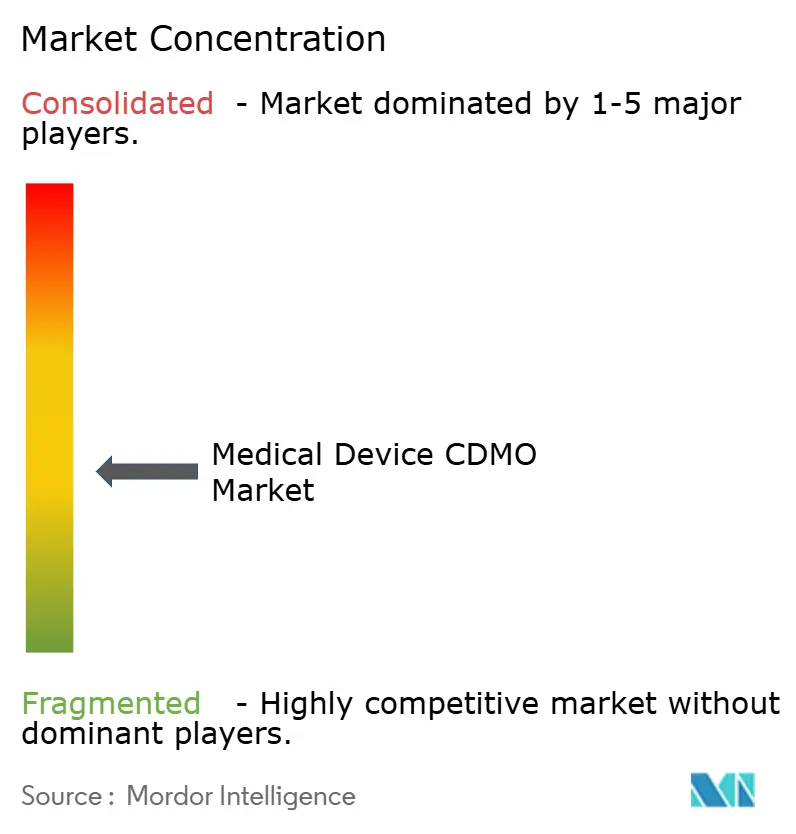

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device CDMO Market Analysis by Mordor Intelligence

The Medical Device CDMO Market size was valued at USD 127.75 billion in 2025 and is estimated to grow from USD 134.78 billion in 2026 to reach USD 180.76 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

The medical device CDMO market is moving from volume-led outsourcing toward capability-led outsourcing, as OEMs place greater value on specialized engineering, cleanroom control, and regulatory execution than on cost arbitrage alone. The February 2026 rollout of the FDA Quality Management System Regulation increased attention on outsourced process control and purchasing controls, which makes compliance depth a larger part of supplier selection. Cleanroom and sterile production capacity remains tight in North America and Europe, which is pushing manufacturers to commit capital earlier and favoring operators that already have validated space. The medical device CDMO market is also benefiting from nearshoring and dual-site manufacturing strategies, especially where suppliers can support North American and European programs from compliant regional footprints. These conditions keep demand favorable, but they also raise the bar for execution in the medical device CDMO market.

Key Report Takeaways

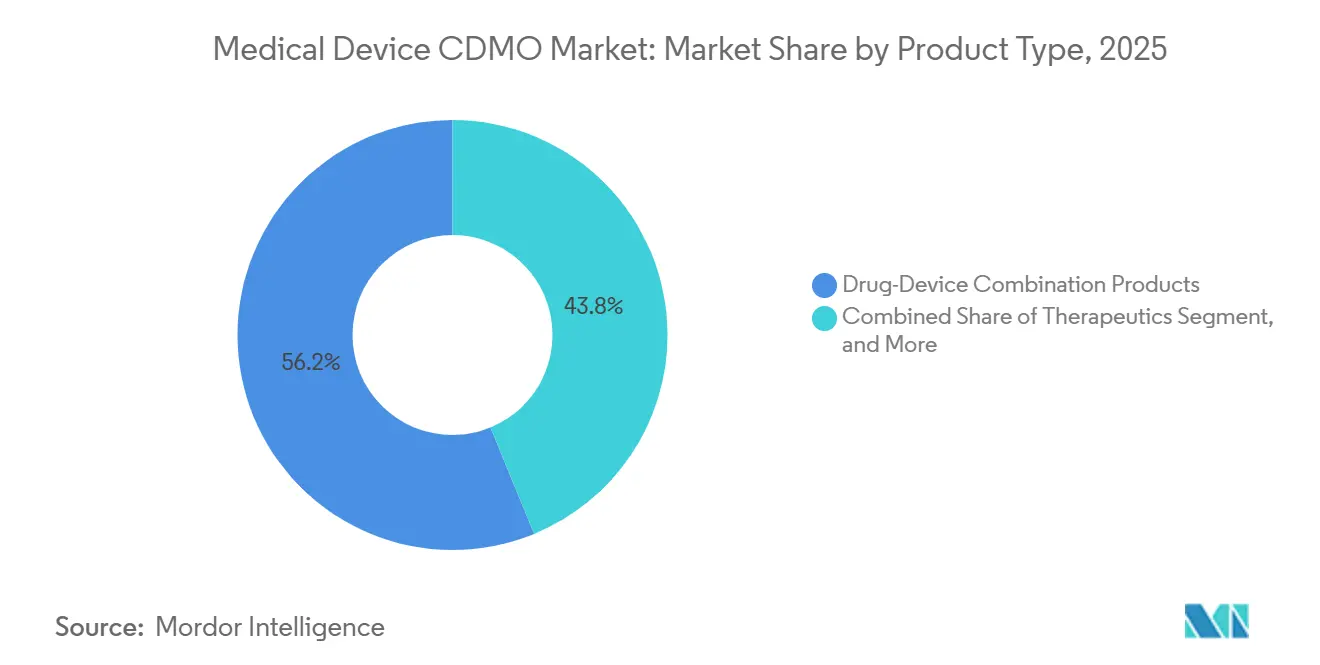

- By product type, drug-device combination products held 56.21% of revenue in 2025, while therapeutics are projected to expand at a 6.81% CAGR through 2031.

- By service, contract development held 42.83% of revenue in 2025, while contract manufacturing is projected to expand at a 7.94% CAGR through 2031.

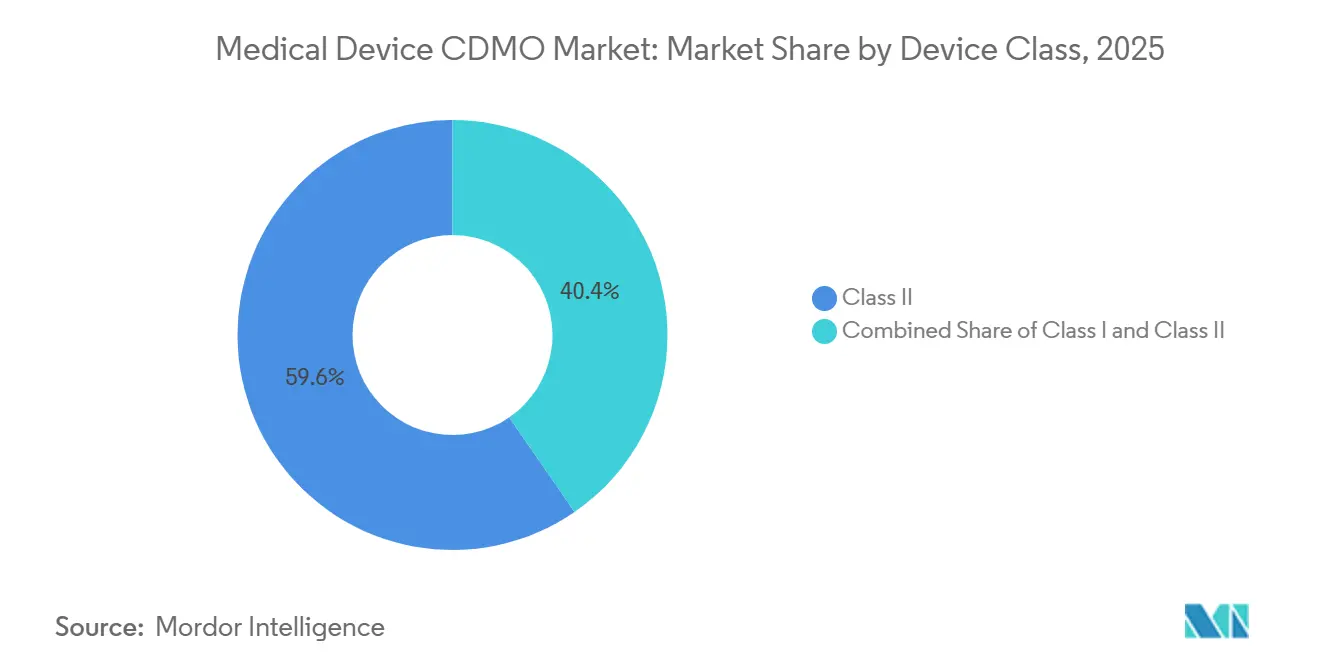

- By device class, class II held 59.64% of revenue in 2025, while class III is projected to expand at a 7.33% CAGR through 2031.

- By application, cardiovascular devices held 33.2% of revenue in 2025, while surgical instruments are projected to expand at an 8.6% CAGR through 2031.

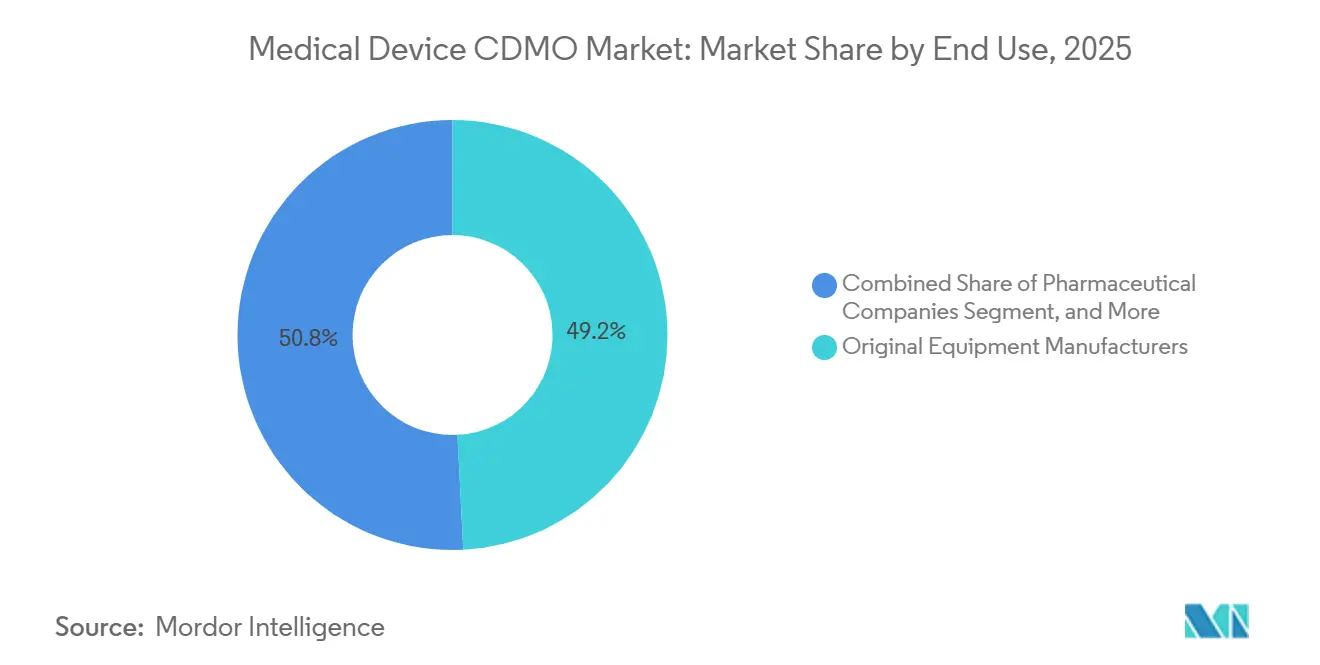

- By end use, original equipment manufacturers held 49.19% of revenue in 2025, while pharmaceutical and biopharmaceutical companies are projected to expand at a 6.73% CAGR through 2031.

- By geography, Asia-Pacific held 39.41% of revenue in 2025, while Europe is projected to expand at a 7.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device CDMO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing of Complex Device Development and Manufacturing | +2.1% | Global | Medium term (2-4 years) |

| Rising Demand for Combination Products and Drug Delivery Systems | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Expansion of High-Precision, Low-Touch Manufacturing Capabilities | +0.8% | North America, Europe, APAC core | Long term (≥ 4 years) |

| Pharma-Medtech Convergence and Integrated Development Models | +0.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Sustainability-Led Material Substitution in Device Components | +0.3% | Europe-led, APAC adoption | Long term (≥ 4 years) |

| Reshoring and Supply Chain Risk Rebalancing for Critical Devices | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Outsourcing of Complex Device Development and Manufacturing

The medical device CDMO market is gaining support from the steady rise in complex programs that many OEMs no longer want to manage fully inside their own networks. Miniaturization, connectivity, and mixed electromechanical design are making it harder for internal plants to cover every manufacturing step with the needed validation discipline. Integer Holdings stated in its first quarter 2026 earnings release that customers are continuing to look for more outsourcing, which shows that this shift is still active in 2026. Plexus also reported Healthcare and Life Sciences revenue growth ahead of its target range in fiscal second quarter 2026, which points to healthy demand for specialist external production support. Once OEMs narrow internal tooling depth and process engineering coverage, the ability to bring those programs back in-house becomes weaker. That creates a longer relationship cycle in the medical device CDMO market, and it favors suppliers that can take a program from design transfer into validated production without a break in responsibility.

Rising Demand for Combination Products and Drug Delivery Systems

The medical device CDMO market is seeing stronger demand from drug-device combinations because these programs require device engineering, sterile process control, and drug-side compliance at the same time. The FDA Quality Management System Regulation became effective in February 2026, and that raised the compliance standard for manufacturers operating across device and drug requirements. The FDA Office of Combination Products also issued draft guidance on Unique Device Identifier requirements for combination products in June 2025, which signaled continued regulatory attention on this category. That dual burden makes scale and integrated quality systems more valuable in the medical device CDMO market because smaller specialists often lack matching pharmaceutical infrastructure. Jabil’s February 2025 acquisition of Pharmaceutics International showed how established device-focused suppliers are building drug manufacturing capability before competitive pressure becomes harder to manage.[1]ProMed Molded Products, “ProMed Molded Products Establishes Silicone Molding Operations in Costa Rica,” BusinessWire, businesswire.com As a result, growth is moving toward suppliers that can handle both the physical device and the regulated drug interface within one operating model.

Pharma-Medtech Convergence and Integrated Development Models

The medical device CDMO market is also being reshaped by the closer link between pharmaceutical delivery systems and medtech development. In practice, buyers now want support that extends beyond fabrication and into testing, fill-finish coordination, digital integration, and commercial launch readiness. Gerresheimer’s March 2026 launch of Gx InMonit and Gx AdheraLink showed that suppliers are moving into connected adherence support and real-world usage monitoring, not just device production. That move matters because it places the supplier deeper inside the product experience, which can strengthen switching costs and lengthen contract duration. The medical device CDMO market, therefore, rewards platforms that can support both the therapy container and the patient-facing device workflow. This is turning integrated development into a competitive requirement instead of a premium add-on for only a few flagship programs.

Reshoring and Supply Chain Risk Rebalancing for Critical Devices

The medical device CDMO market is benefiting from reshoring and nearshoring decisions that followed earlier supply chain disruptions and a broader push for dual-site resilience. Costa Rica stands out because several companies expanded there in 2025, including Freudenberg Medical, DuPont, ProMed Molded Products, and Forj Medical, which together reinforced the country’s role as a compliant production base tied closely to North American demand. These investments matter because they shorten qualification paths for OEMs that want regional alternatives without stepping outside FDA-ready manufacturing environments. Quasar Medical’s September 2025 acquisition of facilities in Galway and Tecate showed the same logic in a different form, with one platform positioned to support European innovation work and North American volume production. The medical device CDMO market is therefore gaining from site networks that balance compliance, logistics, and customer proximity. Over time, this should direct more outsourcing toward companies that can offer location diversity without forcing OEMs to manage multiple disconnected suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Validation Burden Across Multi-Jurisdiction Programs | -1.2% | Global, highest in Europe and North America | Medium term (2-4 years) |

| IP Leakage Risk in Shared Design and Tooling Environments | -0.5% | Global | Short term (≤ 2 years) |

| Long Qualification Cycles for High-Risk and Class III Devices | -0.8% | North America, Europe | Long term (≥ 4 years) |

| Capacity Bottlenecks in Sterile, Cleanroom, and Specialized Assembly | -0.6% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Validation Burden Across Multi-Jurisdiction Programs

The medical device CDMO market still faces a heavy regulatory burden when one program must satisfy the FDA, EU MDR, and national requirements at the same time. The FDA Quality Management System Regulation took effect in February 2026 and incorporated ISO 13485 by reference, which increased the importance of documented control over outsourced processes and supplier management.[2]U.S. Food and Drug Administration, “Quality Management System Regulation (QMSR),” U.S. Food and Drug Administration, fda.gov RAPS reported that outsourcing and purchasing controls appeared among the main Form 483 observation areas during early QMSR-era inspections, which reinforces how directly regulators are reviewing external manufacturing oversight.[3]Regulatory Affairs Professionals Society, “FDA Official Details Top Observations from QMSR Inspections,” Regulatory Affairs Professionals Society, raps.org BVMed data published in the 2026 German MedTech outlook showed that 93% of German MedTech manufacturers are SMEs, and that matters because smaller organizations feel the documentation burden more sharply. In the medical device CDMO market, the environment favors providers with in-house regulatory teams, but it also raises fixed operating costs across the sector. The result is a market where compliance capability is becoming as important as factory footprint.

Long Qualification Cycles for High-Risk and Class III Devices

The medical device CDMO market also faces long qualification cycles for high-risk programs, especially in Class III outsourcing. These projects can take 18 to 36 months before meaningful production revenue is recognized, because validation, documentation, and customer approval are much deeper than in lower-risk categories. That delay can hold back investment decisions, especially when cleanroom buildouts or specialized tooling must be funded well before stable demand is visible. The issue is more important because Class III programs are also among the most attractive parts of the medical device CDMO market from a growth and margin standpoint. This creates a gap where customer interest rises faster than qualified capacity. It also helps explain why large or highly specialized suppliers keep an advantage over newer entrants that cannot absorb a long pre-revenue qualification period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Products Anchor Market, While Therapeutics Builds Momentum

Drug-device combination products held 56.21% of the medical device CDMO market share in 2025, which made them the clear center of product demand. That leadership reflects the wider use of autoinjectors, pre-filled syringes, inhaled drug-device systems, and implant-linked delivery formats. In the medical device CDMO market, these programs carry more than volume, because they also combine device engineering with pharmaceutical compliance and sterile process expectations. Suppliers that serve this category must maintain aligned quality systems across both sides of the product, which narrows the pool of eligible vendors. That narrower supplier base supports stronger customer dependence on operators that already passed qualification for integrated programs.

Therapeutics is projected to grow at a 6.81% CAGR from 2026 to 2031, which shows that future demand is moving toward chronic disease delivery and implant-enabled treatment formats. Biosimilar wearable delivery platforms and newer implantable therapeutic modalities are expanding the need for manufacturing partners that can manage precision assembly over longer product lifecycles. Diagnostics remains smaller in revenue terms, but it is becoming more relevant where point-of-care platforms include microfluidics, compact sensing, and embedded analytics. Jabil’s January 2026 manufacturing partnership with TxSphere, including fill-finish support for primary drug packs, showed how the medical device CDMO market is moving toward one coordinated production chain for combination programs. Taken together, product demand is increasingly favoring suppliers that can manage therapy, device, and packaging interfaces as one integrated operating model.

By Service: Development Services Lead, Contract Manufacturing Grows Fastest

Contract development accounted for 42.83% share of the medical device CDMO market size in 2025, while contract manufacturing is projected to grow at a 7.94% CAGR through 2031. The larger development base shows that OEMs still depend heavily on outside support for design transfer, testing, validation planning, and quality documentation. These services reduce time-to-market pressure without requiring customers to keep full engineering depth across every program type. They also create early engagement points that can later convert into long production contracts. In the medical device CDMO market, front-end involvement often shapes supplier selection well before a commercial manufacturing award is finalized.

Contract manufacturing is growing faster because OEMs continue to shift fixed production assets and specialized assembly work toward external partners with existing infrastructure. Device manufacturing and assembly still cover the broadest range of projects, from finished units to advanced subassemblies that need traceability and controlled process discipline. Component manufacturing is gaining importance in cardiovascular and neuromodulation work, where tolerance control and precision machining are harder to scale inside generalist plants. Packaging and regulatory affairs are also becoming more strategic, because customers increasingly want submission support and manufacturing coordination under one commercial agreement. That keeps the medical device CDMO market oriented toward full-service platforms that can move from development into supply continuity without handing the program across multiple vendors.

By Device Class: Class II Dominates, While Class III Lifts Value Growth

Class II devices held 59.64% of revenue in 2025, while Class III devices are projected to grow at a 7.33% CAGR through 2031. Class II remains the broadest base because it covers a large installed pool of moderate-risk products such as imaging systems, diagnostic instruments, infusion pumps, and many surgical tools. These devices are outsourced often enough to create recurring demand, but they usually do not require the same capital intensity as the most advanced implantable categories. In the medical device CDMO market, Class II is the main volume foundation across many supplier portfolios. It also provides the operating cash flow that can support later expansion into higher-risk niches.

Class III is growing faster because pacemakers, implantable defibrillators, structural heart products, and neurostimulation platforms require validated environments and specialized process control that few OEMs want to replicate internally. Premarket approval discipline, design history rigor, and deeper process validation create a higher barrier to entry for suppliers that want to move into this category. That barrier supports premium positioning for the limited group already active in these programs. Class I remains the smallest class in revenue terms, but it still contributes a stable baseline demand through high-volume accessory and lower-complexity production. Overall, the device-class mix in the medical device CDMO market shows a clear split between the large outsourced base in Class II and the higher-value growth lane in Class III.

By Application: Cardiovascular Devices Lead, While Surgical Instruments Grow Fastest

Cardiovascular devices accounted for 33.23% of the medical device CDMO market size in 2025, while surgical instruments are projected to grow at an 8.62% CAGR through 2031. Cardiovascular demand remained strong because catheters, stent delivery systems, leadless pacing systems, and structural heart products depend on precision tooling and controlled assembly environments. Those requirements fit well with specialist contract manufacturers that built expertise around tight tolerances and cleanroom execution. In the medical device CDMO market, this makes cardiovascular programs both sticky and technically demanding. It also supports longer customer qualification cycles that can translate into more durable revenue once production stabilizes.

Surgical instruments are growing faster because robotic-assisted surgery platforms need precise electromechanical subassemblies that standard factory layouts do not always support well. Plexus reported a significant award tied to a robotic surgical platform for its Neenah facility in the second quarter of fiscal 2026, which is a useful signal of demand moving into advanced instrument builds. Orthopedic, diagnostic, and ophthalmic devices remain established applications with steady outsourcing demand and defined supplier ecosystems. Respiratory devices normalized in 2024 and 2025 after the unwind of pandemic-driven ventilator demand, which reduced the earlier volume spike. Dental applications are still smaller, but they are gaining specialist interest where additive manufacturing and precision milling create room for differentiated service models in the medical device CDMO market.

By End Use: OEMs Anchor Demand, While Pharma Companies Expand Faster

Original equipment manufacturers held 49.19% of end-use demand in 2025, while pharmaceutical and biopharmaceutical companies are projected to grow at a 6.73% CAGR through 2031. OEMs remain the largest customer group because they outsource components, subassemblies, and finished production across a wide range of device categories. Their scale gives them the largest ongoing pull on the medical device CDMO market, especially where supplier continuity and quality records matter more than one-time project cost. OEM demand also tends to cover the full service chain, from early development support to commercial supply. That makes them the core of current utilization across most established CDMO platforms.

Pharmaceutical and biopharmaceutical companies are growing faster because they increasingly need delivery systems that sit outside their traditional manufacturing skill base. Instead of building dedicated device operations internally, many of these companies are turning to partners already qualified in combination-product manufacturing and connected delivery formats. Gerresheimer’s September 2025 expansion of its collaboration with Portal Instruments for the PRIME Nexus reusable connected autoinjector is a clear example of this pattern. The Others category, including hospitals, research institutions, and early-stage medtech innovators, remains smaller but still adds incremental demand through feasibility work and regulatory preparation. Together, these end-use patterns show that the medical device CDMO market is broadening beyond traditional OEM outsourcing into a more mixed customer base built around device-enabled therapies.

Geography Analysis

North America remains one of the most value-dense parts of the medical device CDMO market because it combines large OEM presence, regulatory proximity, and a deep base of advanced manufacturing talent. The United States continues to attract premium investment in this market, and Gerresheimer’s expansion in Peachtree City, Georgia, showed continued confidence in domestic cleanroom and automated device production capacity. Integer Holdings also pointed to continued focus on electrophysiology, structural heart, neurovascular, and neuromodulation in the first quarter of 2026, which aligns with the higher-value segments that support outsourcing demand in the region. Mexico is absorbing added nearshoring interest through its established medical manufacturing clusters, and that supports cross-border production strategies for U.S. customers. Costa Rica, while outside formal North America, remains tightly linked to North American sourcing decisions and strengthens the regional supply chain through compliant, lower-cost production capacity.

Europe is projected to grow at a 7.82% CAGR through 2031, giving it the fastest regional pace in the medical device CDMO market. That growth is tied closely to the region’s compliance environment, because stricter EU MDR requirements are pushing more OEM and pharma customers toward suppliers with validated European manufacturing sites and established regulatory experience. BVMed data showed that 93% of German MedTech manufacturers are SMEs, which helps explain why external regulatory and manufacturing support is becoming more important across the region. Ireland has become a notable sub-hub, and Quasar Medical’s acquisition of the Galway facility added scale to its European position in interventional device programs. Spain, France, and Italy remain established outsourcing bases, especially where orthopedic, dental, and precision component work already has an industrial foundation.

Asia-Pacific held 39.41% of the medical device CDMO market share in 2025, which kept it as the largest regional base by revenue. That position reflects the region’s long-standing role in high-volume production for Class I and lower-complexity Class II devices, supported by facilities across China, India, South Korea, and other manufacturing centers. Plexus secured a next-generation point-of-care ultrasound program for its Xiamen facility in the fiscal second quarter of 2026, which showed that Asian sites are also winning more technically complex work. The Middle East and Africa and South America remain smaller in the medical device CDMO market, with Brazil standing out, where domestic device activity and local registration needs are supporting greater interest in regional manufacturing partnerships.

Competitive Landscape

The medical device CDMO market has many suppliers competing across specific device niches, service layers, and regional footprints rather than through one dominant global platform. This keeps competition active, but it also means buyers often choose between broad service integration and deep specialization. In the medical device CDMO market, the strongest platforms are building around either end-to-end development and production coverage or highly specialized process expertise in a narrower clinical area. Jabil represents the broader platform approach, and its February 2025 acquisition of Pharmaceutics International expanded its pharmaceutical services footprint in support of integrated drug-device programs. Quasar Medical reflects the targeted specialist model, with its Galway and Tecate acquisitions strengthening a focused interventional device network across two regulated manufacturing locations.

Technology is becoming a more visible separator in the medical device CDMO market because customers increasingly value digital connectivity, automation, and high-reliability electronics integration alongside conventional assembly skills. Gerresheimer’s Gx InMonit and Gx AdheraLink launch in March 2026 showed how suppliers are pushing into connected therapy support and patient engagement layers around drug delivery devices. Freudenberg Medical’s Costa Rica expansion and DuPont’s sterile packaging addition in Heredia both show how competitive positioning is also being reinforced through physical capacity, where customer demand is already visible. Mordor Intelligence also noted 2025 investment by EMS-linked manufacturers in APAC, which supports the view that electronics-intensive medical production is drawing more dedicated infrastructure. This means the medical device CDMO market is no longer competing only on labor or footprint, because technology depth now shapes win rates in more advanced programs.

Smaller and mid-sized operators are still active, but many are trying to sharpen a specific value proposition rather than match the full-service scale of larger rivals. Precera Medical emerged in November 2025 as an independent CDMO platform after SK Capital completed the acquisition of LISI Group’s Medical Division, which showed continued interest in building focused manufacturing platforms around established customer relationships. Vance Street Capital’s partnership with MRPC and the addition of Injectech into its medical molding platform show the same push toward tighter specialization in silicone, thermoplastic, and precision fluid management capabilities. The medical device CDMO market, therefore, remains fragmented in structure, but it is moving toward clearer competitive tiers based on integration depth, regulatory readiness, and targeted technical strength.

Medical Device CDMO Industry Leaders

Gerresheimer AG

Integer Holdings Corporation

Nipro Corporation

Jabil Inc.

Recipharm AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Gerresheimer AG launched Gx InMonit, a connected smart add-on device for self-injection therapies, alongside Gx AdheraLink, an AI-powered patient adherence messaging platform, creating a connected digital layer atop its drug delivery device manufacturing and extending its value proposition from physical production to real-world outcomes data capture.

- January 2026: Jabil Inc. entered a manufacturing partnership with TxSphere to produce reusable wearable drug injectors, with the arrangement including fill-finish for primary drug packs, marking one of the first large-scale CDMO programs integrating device manufacturing and pharmaceutical fill-finish in a single supply relationship.

- November 2025: SK Capital Partners completed the acquisition of LISI Group's Medical Division and relaunched the business as Precera Medical, establishing an independent CDMO platform for blue-chip medical device OEMs, LISI Group retained a minority stake in the new entity.

- October 2025: Vance Street Capital partnered with Molded Rubber and Plastic Corporation, extending its medical device manufacturing platform to include full-service silicone and thermoplastic molding solutions, representing the firm's sixteenth investment in the medical and life sciences manufacturing space.

Global Medical Device CDMO Market Report Scope

A Medical Device CDMO (Contract Development and Manufacturing Organization) is a strategic partner that provides end-to-end outsourcing solutions for medical device companies. They handle everything from initial product design, rapid prototyping, and regulatory compliance to scalable commercial manufacturing, sterilization, and packaging.

The Medical Device CDMO Market is segmented by product type, service, device class, application, end use, and geography. By product type, it includes Diagnostics, Therapeutics, and Drug-Device Combination Products. By service, the market covers Contract Development—encompassing Product Design and Development Services, Testing and Validation, Quality Management, and other services—as well as Contract Manufacturing, which includes Accessories Manufacturing, Assembly Manufacturing, Component Manufacturing, and Device Manufacturing. Additional services include Packaging and Regulatory Affairs. By device class, the market spans Class I, Class II, and Class III medical devices. By application, CDMO services support Cardiovascular Devices, Orthopedic Devices, Ophthalmic Devices, Diagnostic Devices, Respiratory Devices, Surgical Instruments, Dental, and other categories. By end use, the market serves Original Equipment Manufacturers, Pharmaceutical and Biopharmaceutical Companies, and other stakeholders.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United_Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Diagnostics |

| Therapeutics |

| Drug-Device Combination Products |

| Contract Development | Product Design and Development Services |

| Testing and Validation | |

| Quality Management | |

| Others | |

| Contract Manufacturing | Accessories Manufacturing |

| Assembly Manufacturing | |

| Component Manufacturing | |

| Device Manufacturing | |

| Packaging | |

| Regulatory Affairs |

| Class I |

| Class II |

| Class III |

| Cardiovascular Devices |

| Orthopedic Devices |

| Ophthalmic Devices |

| Diagnostic Devices |

| Respiratory Devices |

| Surgical Instruments |

| Dental |

| Others |

| Original Equipment Manufacturers |

| Pharmaceutical and Biopharmaceutical Companies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diagnostics | |

| Therapeutics | ||

| Drug-Device Combination Products | ||

| By Service | Contract Development | Product Design and Development Services |

| Testing and Validation | ||

| Quality Management | ||

| Others | ||

| Contract Manufacturing | Accessories Manufacturing | |

| Assembly Manufacturing | ||

| Component Manufacturing | ||

| Device Manufacturing | ||

| Packaging | ||

| Regulatory Affairs | ||

| By Device Class | Class I | |

| Class II | ||

| Class III | ||

| By Application | Cardiovascular Devices | |

| Orthopedic Devices | ||

| Ophthalmic Devices | ||

| Diagnostic Devices | ||

| Respiratory Devices | ||

| Surgical Instruments | ||

| Dental | ||

| Others | ||

| By End Use | Original Equipment Manufacturers | |

| Pharmaceutical and Biopharmaceutical Companies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of the medical device CDMO space?

It stands at USD 134.78 billion in 2026 and is projected to reach USD 180.76 billion by 2031 at a 6.05% CAGR.

Which product area leads outsourced demand?

Drug-device combination products led with 56.21% share in 2025, supported by demand for autoinjectors, pre-filled syringes, and other integrated delivery systems.

Which service area is growing the fastest?

Contract manufacturing is the fastest-growing service segment, with a projected 7.94% CAGR through 2031, as OEMs shift more production assets to specialized partners.

Why are Class III programs important for suppliers?

Class III devices are projected to grow at 7.33% CAGR, and they carry high entry barriers because of validation depth, regulated process control, and longer qualification timelines.

Which region offers the strongest growth outlook?

Europe has the fastest forecast growth at 7.82% CAGR through 2031, while Asia-Pacific remained the largest regional base with 39.41% share in 2025.

What is changing competition among medical device CDMOs?

Competition is shifting toward suppliers with integrated capabilities, strong regulatory systems, and targeted investments such as Jabil’s Pii acquisition, Quasar’s cross-border expansion, and Gerresheimer’s connected device platform moves.

Page last updated on: