Medical Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.21 Billion |

| Market Size (2031) | USD 37.65 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

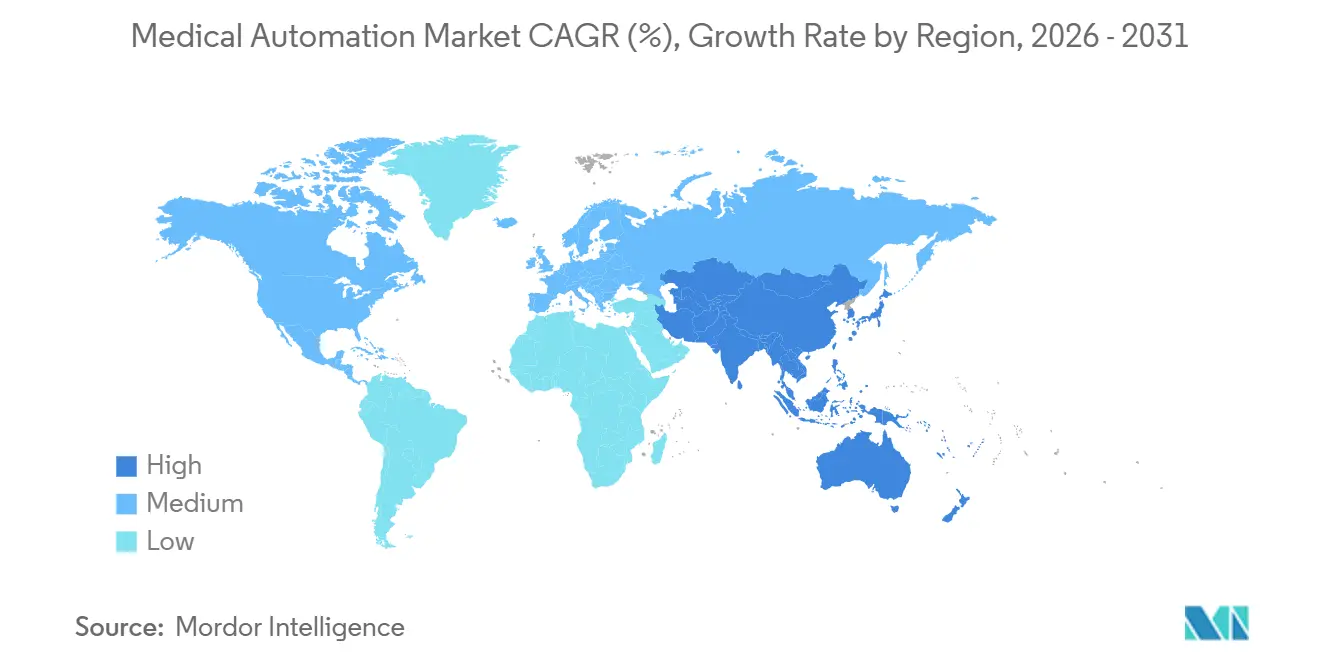

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

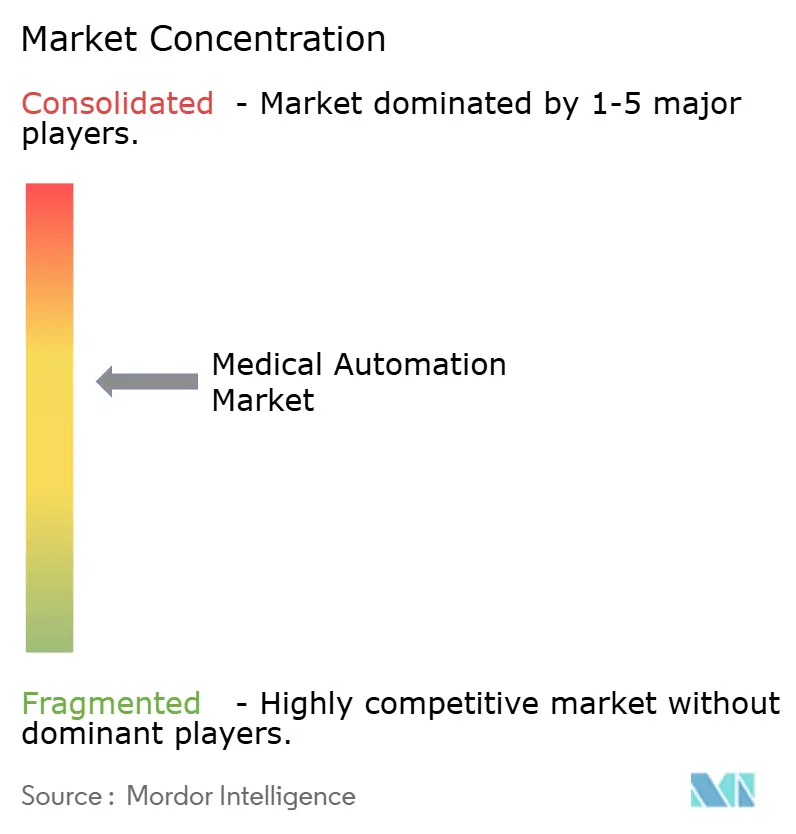

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Automation Market Analysis by Mordor Intelligence

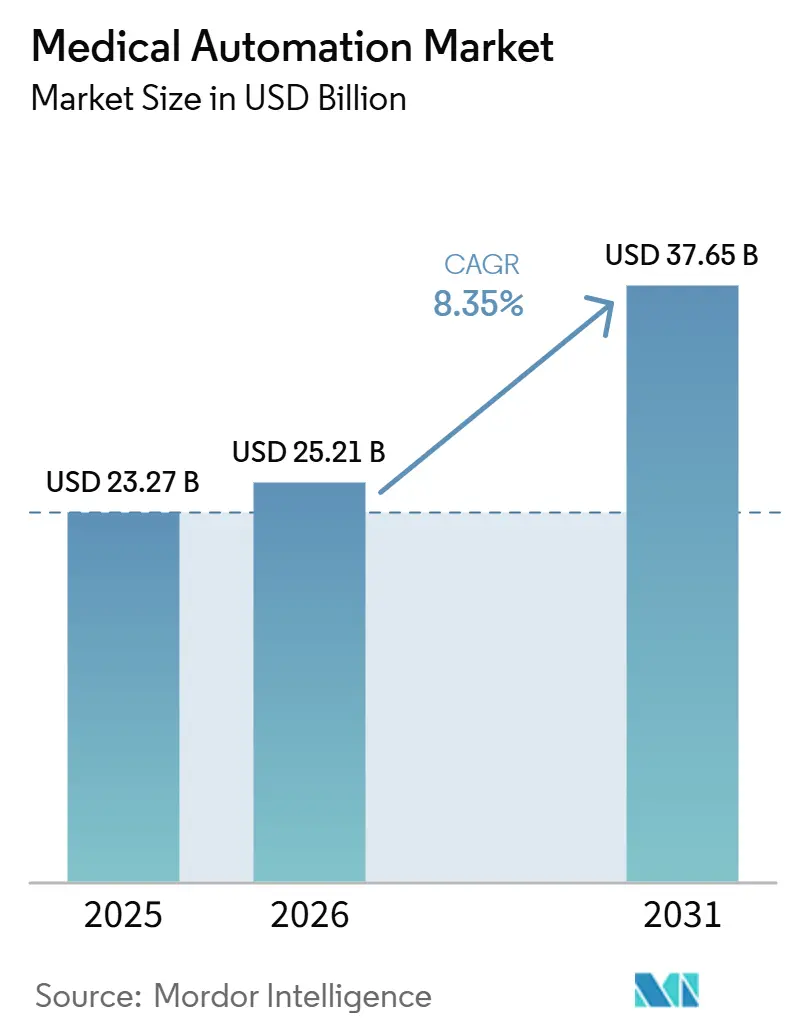

The Medical Automation Market size is expected to increase from USD 23.27 billion in 2025 to USD 25.21 billion in 2026 and reach USD 37.65 billion by 2031, growing at a CAGR of 8.35% over 2026-2031.

The market is being pushed by persistent staffing gaps that are moving automation from a productivity tool to a continuity requirement in care delivery. The medical automation market is also benefiting from broader use of AI systems that connect imaging, laboratory, and surgical workflows under one operating layer. Medication safety pressure is widening demand across hospitals, outpatient settings, and pharmacies, where automated dispensing and digital pharmacy platforms are being used to reduce error exposure. The competitive field is becoming more active as large medtech companies widen their regulatory and product pipelines in surgery, imaging, and pathology, which reduces the white space that single-specialty vendors once held. Growth still faces limits because hospital capital budgets are under strain and integration with legacy systems continues to slow deployment outside large and well-funded health systems.

Key Report Takeaways

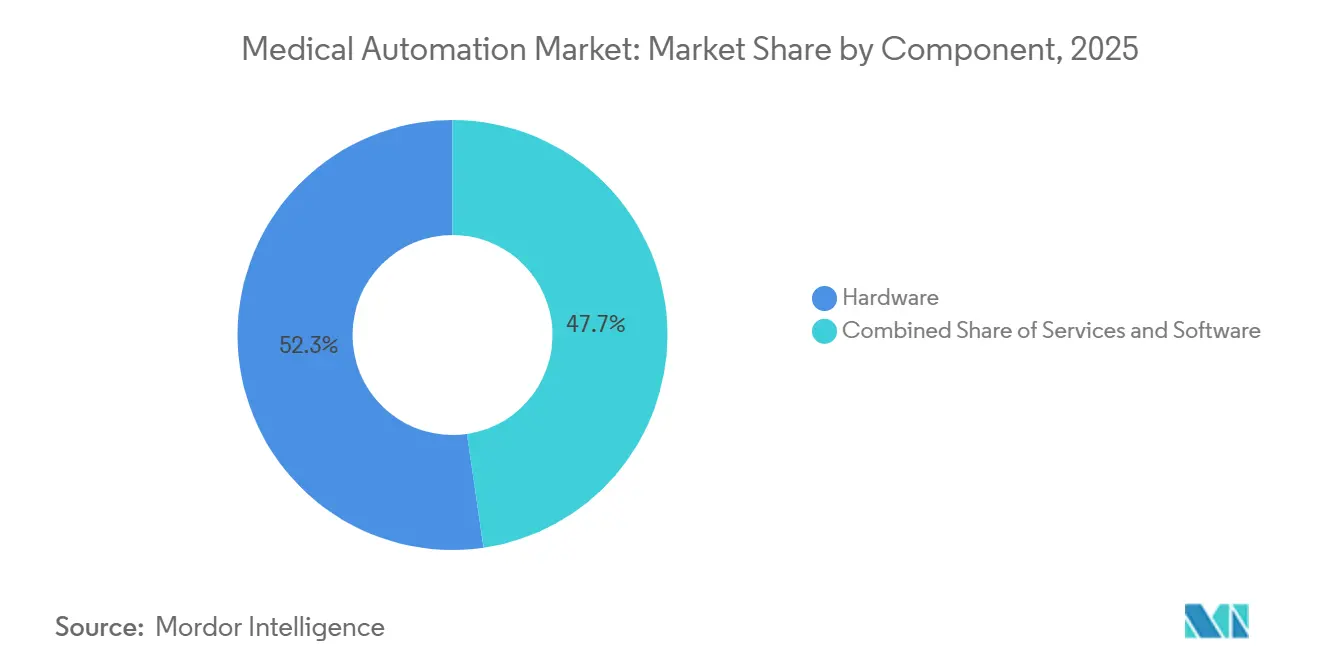

- By component, hardware led with 52.31% revenue share in 2025, while services is forecast to expand at a 10.38% CAGR through 2031.

- By application type, Therapeutic Automation accounted for 53.24% of the medical automation market size in 2025, while Laboratory and Pharmacy Automation is advancing at an 11.52% CAGR through 2031.

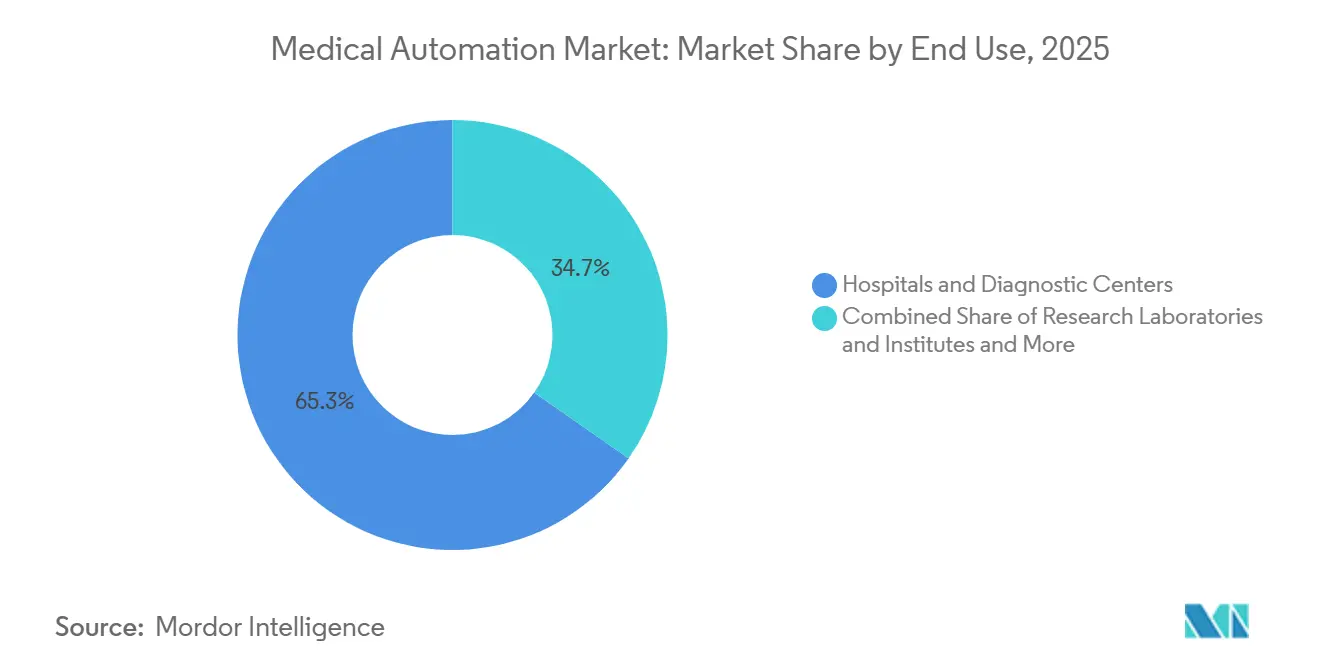

- By end use, Hospitals and Diagnostic Centers held 65.26% revenue share in 2025, while pharmacies recorded the highest projected CAGR at 12.55% through 2031.

- By geography, North America represented 42.62% share in 2025, while Asia-Pacific is expected to expand at 11.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce Shortages in Clinical Operations | +2.0% | Global | Short term (≤ 2 years) |

| Rising Error Sensitivity in Medication and Procedure Workflows | +1.2% | Global | Medium term (2-4 years) |

| AI-Enabled Workflow Orchestration Across Imaging, Lab, and Surgery | +1.8% | Global | Short term (≤ 2 years) |

| Unplanned Automation Retrofit Demand in Aging Hospital Infrastructure | +1.0% | North America & Europe | Medium term (2-4 years) |

| Expansion of Surgical and Laboratory Automation | +1.5% | Global | Medium term (2-4 years) |

| Cost Pressure on Healthcare Providers | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages in Clinical Operations

Workforce shortages have become a structural demand base for the medical automation market, especially where hospitals need stable care delivery with fewer available clinicians. Health systems are now treating automation purchases as protection against staffing risk rather than as optional efficiency projects. In the United States, workforce projections continue to point to physician and nursing shortfalls through the next decade, which keeps automation high on executive agendas[1]American Hospital Association, “2025 Health Care Workforce Scan,” AHA, aha.org. That shift changes the budget conversation because automation is increasingly reviewed alongside resilience and service continuity needs. Vendors that present their platforms as staffing support tools are gaining better traction in the medical automation market than vendors that position them only as productivity upgrades.

AI-Enabled Workflow Orchestration Across Imaging, Lab, and Surgery

AI orchestration is moving the medical automation market beyond single-use tools and toward systems that manage multiple clinical workflows together. Vendors are using this shift to build recurring revenue through software, analytics, and enterprise workflow management rather than relying only on device sales. Roche stated that its navify digital ecosystem exceeded 1,500 clinical placements by 2025, while GE HealthCare’s Edison AI Orchestrator is designed to unify AI applications across radiology workflows. A 2026 Nature paper described autonomous medical AI agents that can interface with EHR environments through FHIR standards to coordinate scheduling, diagnostics, and documentation. Vendors already present across imaging, laboratory, and surgical settings are better placed to capture this demand in the medical automation market because orchestration value rises with integration breadth.

Expansion of Surgical and Laboratory Automation

Expansion in surgical and laboratory automation is reinforcing the medical automation market by widening the installed base and by increasing the number of workflows that can be automated inside one health system. Intuitive Surgical reported USD 10.1 billion in revenue in 2025, more than 3.1 million da Vinci procedures, and more than 140,000 Ion lung biopsies, which shows that automation is scaling across both treatment and diagnostic-adjacent use cases. Intuitive Surgical also spent more than USD 1 billion on R&D in 2025, and its da Vinci 5 platform was installed across more than 1,200 systems by year-end[2]Intuitive Surgical, “2025 Annual Report,” Intuitive Surgical, isrg.intuitive.com. Roche received FDA 510(k) clearance in March 2026 for the cobas c 703 and cobas ISE neo analytical units, which are built for high-throughput laboratories facing staff shortages and heavier test loads. As hospitals prepare space for robotic operating rooms and modular laboratory lines, the medical automation market is pulling in related demand for construction, systems integration, and post-installation support.

Rising Error Sensitivity in Medication and Procedure Workflows

Error reduction in dispensing and procedures is now a direct purchasing trigger for the medical automation market, especially in high-volume medication workflows where liability exposure is high. BD launched the Pyxis Pro Dispensing Solution and the Incada Connected Care Platform in Europe in April 2026, using AI-enabled medication inventory analytics and broad language support to strengthen medication management. Ireland’s Health Service Executive agreed in June 2026 to roll out CareFlow Pharmacy across public hospitals, with 9 sites live and 12 more scheduled in 2026. These moves show that pharmacy automation is spreading beyond isolated cabinets and toward connected national or enterprise platforms. IV compounding robotics remains one of the more urgent areas inside the medical automation market because contamination risk, process complexity, and liability exposure are high in sterile pharmacy operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity for Integrated Automation Suites | -1.5% | Global, most acute in small and mid-tier health systems | Medium term (2-4 years) |

| Interoperability Friction With Legacy Hospital Systems | -1.1% | Global | Long term (≥ 4 years) |

| Clinical Validation and Medico-Legal Approval Lag | -0.9% | Global | Long term (≥ 4 years) |

| Data Privacy, Cybersecurity, and Liability Concerns | -0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity for Integrated Automation Suites

High capital intensity remains the clearest near-term limit on the medical automation market, especially for community, rural, and mid-tier hospitals. The American Hospital Association reported that hospital expenses rose 5.1% in 2024 while general inflation was 2.9%, and it also noted that the average age of hospital plant infrastructure increased more than 10% over the prior 2 years. That pressure reduces the room for large automation purchases even when clinical need is clear. It also pushes smaller providers toward phased deployments, narrower scopes, or deferred decisions instead of full integrated suites. Vendors are responding with subscription and managed service models, but the medical automation market still faces slower decision cycles where procurement rules are strict and capital availability is weak.

Interoperability Friction With Legacy Hospital Systems

Interoperability friction with legacy hospital systems continues to slow the medical automation market because automation tools cannot deliver full value when data remains locked in older architectures. Many providers still operate with proprietary workflows, partial standards adoption, and fragmented interfaces that complicate automation across departments. The shift toward FHIR-based connectivity is improving the long-term outlook, but it remains a multi-year effort for health systems with deep legacy dependencies. FDA cybersecurity guidance issued in June 2025 and the Quality Management System Regulation effective February 2, 2026 increased the documentation and validation burden for connected medical devices and software. Vendors without native interoperability and strong cybersecurity design are likely to face weaker procurement competitiveness in the medical automation market as buyers ask for deeper integration proof.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Leads Revenue While Services Lift Recurring Value

Hardware held 52.31% of the medical automation market share in 2025, reflecting the high value of robotic surgical systems, automated dispensing cabinets, and high-throughput laboratory instruments being installed across care settings. Intuitive Surgical placed 1,721 da Vinci systems in 2025, and its installed base exceeded 11,100 systems by year-end, which shows how hardware continues to define revenue scale in the medical automation market. These placements build the installed foundation that supports later software, maintenance, and analytics revenue. Software remains important because providers want interoperable control layers that can manage automation across multi-site networks.

Services is the fastest-growing component of the medical automation market at a CAGR of 10.38% through 2026 to 2031, showing where post-deployment revenue is expanding fastest. Managed services, remote monitoring, AI analytics, and platform subscriptions are growing because vendors are attaching these offerings to installed hardware bases. This model improves retention and margin quality for suppliers while giving providers a way to expand functionality after initial deployment. That keeps services central to future value capture in the medical automation industry as health systems look for support beyond the hardware layer.

By Application Type: Therapeutic Systems Keep the Largest Revenue Base

Therapeutic Automation commanded 53.24% of the medical automation market size in 2025, supported by the high contract value and long replacement cycle of robotic-assisted surgical systems. Intuitive Surgical reported 19% total procedure growth in 2025, and international da Vinci procedures exceeded 1.1 million with 23% growth, which supports the depth of therapeutic demand. The segment benefits from durable procedure economics and rising hospital willingness to expand minimally invasive capabilities. That keeps therapeutic systems at the center of revenue generation in the medical automation market.

Laboratory and Pharmacy Automation is the fastest-growing application type at a CAGR of 11.52% through 2026 to 2031. Growth in this segment is being driven by higher diagnostic volumes, more complex specialty drug handling, and tighter expectations on dispensing accuracy[3]Becton, Dickinson and Company, “BD Launches AI-Enabled Medication Dispensing System to the European Market,” BD, investors.bd.com. Imaging automation is also advancing as vendors add workflow intelligence, and examples include Siemens Healthineers’ self-driving Ciartic Move and GE HealthCare’s ProtégéAI+ 2.0 clearance in June 2026. The mix of a large therapeutic base and faster growth in lab and pharmacy automation gives the medical automation market more balanced demand across clinical functions.

By End Use: Hospitals Hold Scale While Pharmacies Grow Fastest

Hospitals and Diagnostic Centers held 65.26% of the medical automation market in 2025, reflecting their scale and their need to manage surgery, imaging, intensive care, and laboratory workflows together. Large institutions remain the primary buyers because they can absorb higher upfront costs and because they run enough volume to justify integrated automation. Research Laboratories and Institutes form an important secondary group where genomics, oncology, and high-throughput testing require precision handling and automated processing. This makes institutional scale a core demand condition across the medical automation market.

Pharmacies are the fastest-growing end-use segment in the medical automation market with a CAGR of 12.55% through 2026 to 2031. Growth is being supported by central-fill models, specialty drug dispensing complexity, and wider adoption of connected pharmacy platforms. That changes the value case because pharmacy automation can support revenue expansion as well as error reduction, especially where specialty and distributed fulfillment models are expanding. The medical automation industry is therefore seeing pharmacies move beyond a support function and into a more strategic position in automation spending.

Geography Analysis

North America held 42.62% of the medical automation market share in 2025, which kept it as the largest regional contributor on the strength of hospital capital capacity, established reimbursement, and a deep installed base. The United States remains the main regional driver because large health systems continue to fund robotic surgery, imaging automation, and pharmacy automation even as smaller hospitals stay more selective. FDA cybersecurity guidance and the QMSR now shape procurement more directly because connected devices need stronger quality, software, and lifecycle documentation. Europe remains an advanced but uneven region, with Western Europe showing stronger adoption conditions than Southern and Eastern Europe. BD’s April 2026 Pyxis Pro launch, the March 2026 BD and Sinteco partnership, the March 2026 IMARA initiative in Strasbourg, and Ireland’s national CareFlow Pharmacy rollout all show that medication, logistics, and operating room automation continue to gain institutional backing across Europe.

Asia-Pacific is the fastest-growing regional slice of the medical automation market, with a CAGR of 11.15% through 2026 to 2031. The region benefits from greenfield hospital investment, state-backed modernization programs, and expanding domestic medical technology capabilities. China held the largest regional share in 2025, supported by smart hospital spending, AI-enabled diagnostics initiatives, and local robotics manufacturing, while India is the fastest-growing country market within the region. Those conditions are widening adoption beyond imported surgical systems and toward broader automation stacks across modernizing hospital networks. Japan remains a mature high-value market for laboratory and pharmacy automation, which adds stability to regional demand while newer systems scale elsewhere.

The Middle East and Africa remains earlier stage in the medical automation market, but GCC countries are actively linking hospital automation spending to wider health system transformation agendas. Saudi Arabia and the UAE are leading that regional activity, while South Africa remains a key anchor in sub-Saharan demand for laboratory and imaging automation. South America is led by Brazil and followed by Argentina, where premium private hospital networks are using robotic surgery and laboratory automation as competitive tools despite currency and reimbursement pressure. These regions are smaller today, but they extend the long-run addressable base of the medical automation market as infrastructure and capital access improve.

Competitive Landscape

The medical automation market has a two-tier competitive structure, with a concentrated upper tier and a broader field of specialty and regional challengers. Intuitive Surgical, Siemens Healthineers, GE HealthCare, Roche Diagnostics, Becton Dickinson, Medtronic, and Stryker form the strongest upper tier across surgery, imaging, laboratory, and pharmacy automation. Intuitive Surgical held the most entrenched position in soft-tissue surgical robotics after reporting USD 10.1 billion in 2025 revenue, more than 3.1 million procedures, and R&D spending above USD 1 billion. Medtronic’s December 2025 FDA clearance for Hugo in urologic procedures and its June 2026 filings for general and gynecologic surgery marked a major challenge to that position. Johnson & Johnson’s 2026 OTTAVA submission adds another large-scale entrant with the resources to compete on distribution, service, and multi-product hospital relationships.

Competition is also widening outside surgery as vendors build stronger positions in imaging, pathology, and medication management across the medical automation market. Roche’s planned acquisition of PathAI in May 2026 would combine its installed diagnostics base with AI-driven digital pathology capabilities. GE HealthCare received FDA 510(k) clearance in June 2026 for MIM Contour ProtégéAI+ 2.0, which strengthens its role in radiation oncology workflow automation. Stryker introduced the Mako RPS handheld robotic system in limited release in February 2026, showing that orthopedic automation is also moving into new device formats. These moves reduce the room for single-modality vendors and support broader platform competition across the medical automation market.

Beneath the upper tier, the medical automation market still includes a fragmented mid-tier of specialty robotics firms, regional suppliers, and software-led entrants. White-space demand remains strongest in ambulatory surgery center robotics, modular community hospital solutions, and AI-native orchestration layers that can work across hardware brands. Viz.ai’s March 2026 launch of Agent Studio reflects this software-first direction by letting health systems build and scale their own AI care pathways on top of existing workflows. That leaves the medical automation market competitive, but not fully consolidated, because scale leaders are strong while newer entrants still have room in specific modalities and care settings.

Medical Automation Industry Leaders

Intuitive Surgical, Inc

Siemens Healthineers AG

GE HealthCare Technologies Inc.

Medtronic plc

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Medtronic submitted 510(k) filings to the FDA to bring its Hugo RAS system into general surgery and gynecologic surgery in the United States. The filings came after the system received FDA clearance for urologic procedures in December 2025 and placed Medtronic in a stronger position to compete in two of the highest-volume soft-tissue surgical specialties.

- June 2026: Surrey Memorial Hospital in British Columbia, Canada, performed its first robotic-assisted procedure using the da Vinci Xi system. Royal Columbian Hospital plans to add a second Xi system by fall 2026, supporting a phased expansion of minimally invasive surgical access across British Columbia.

Global Medical Automation Market Report Scope

As per the scope of the report, medical automation is the use of technology, software, and machinery to perform tasks and processes within healthcare settings with minimal human intervention. It aims to improve efficiency, accuracy, and safety in medical procedures, diagnostics, patient management, and administrative functions.

The medical automation market is segmented by component into hardware, software, and services; by application type into imaging automation, therapeutic automation, laboratory and pharmacy automation, and other application types; by end use into hospitals and diagnostic centers, research laboratories and institutes, pharmacies, and other end uses; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Hardware |

| Software |

| Services |

| Imaging Automation |

| Therapeutic Automation |

| Laboratory and Pharmacy Automation |

| Other Application Types |

| Hospitals and Diagnostic Centers |

| Research Laboratories and Institutes |

| Pharmacies |

| Other End Uses |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application Type | Imaging Automation | |

| Therapeutic Automation | ||

| Laboratory and Pharmacy Automation | ||

| Other Application Types | ||

| By End Use | Hospitals and Diagnostic Centers | |

| Research Laboratories and Institutes | ||

| Pharmacies | ||

| Other End Uses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the medical automation market by 2031?

The medical automation market is projected to reach USD 37.65 billion by 2031 from USD 25.21 billion in 2026, at a CAGR of 8.35%.

Which region leads medical automation spending today?

North America led with 42.62% share in 2025, supported by hospital capital capacity, reimbursement depth, and a large installed base.

Which application area generates the most revenue?

Therapeutic Automation led with 53.24% of revenue in 2025, driven by robotic-assisted surgical systems and durable procedure economics.

Which application area is growing the fastest?

Laboratory and Pharmacy Automation is the fastest-growing application type, with an 11.52% CAGR through 2031.

Why are pharmacies becoming more important in automation spending?

Pharmacies are growing at a 12.55% CAGR through 2031 because central-fill models, specialty drug complexity, and connected medication platforms are expanding.

What is the biggest challenge slowing adoption?

High capital intensity remains the clearest brake, especially for community and mid-tier hospitals that face tighter budgets and slower procurement cycles.

Page last updated on: