Mauritius Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

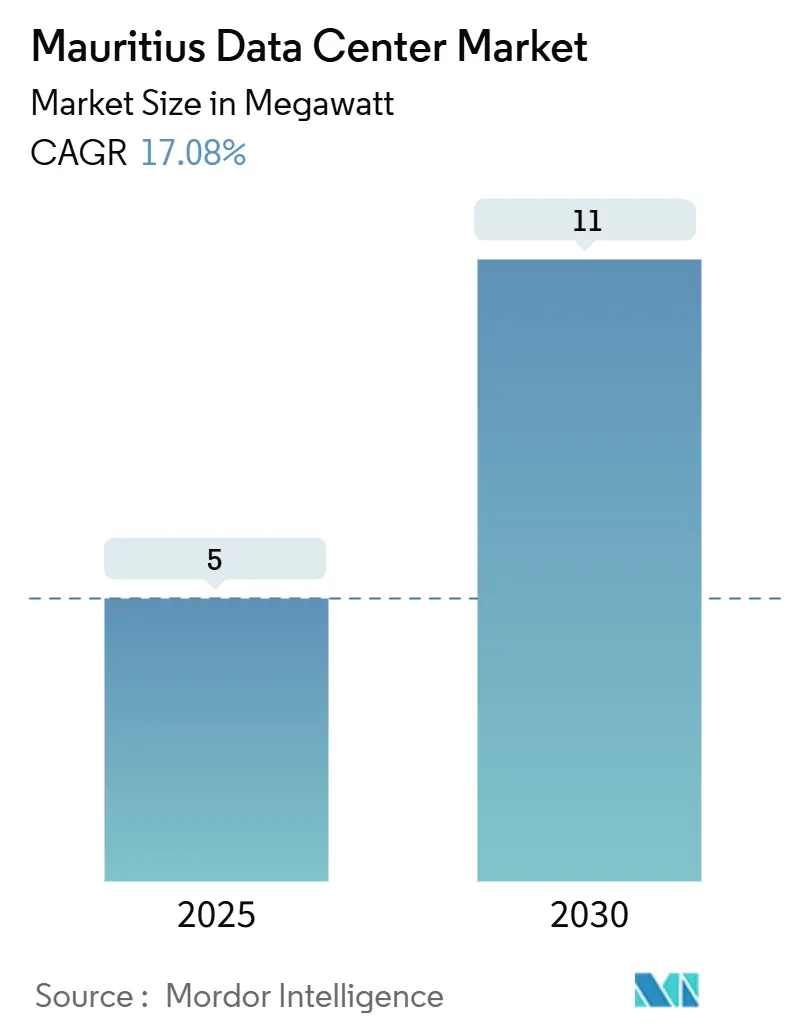

| Market Volume (2025) | 5 megawatt |

| Market Volume (2030) | 11 megawatt |

| Growth Rate (2025 - 2030) | 17.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mauritius Data Center Market Analysis by Mordor Intelligence

The Mauritius data center market size is 5 MW in 2025 and is on course to reach 11 MW by 2030, delivering a 17.08% CAGR that outpaces most African peers. This sharp expansion reflects the island’s pivot from sugar exports toward a diversified, digital-first economy supported by predictable regulation and strong rule of law that reassures foreign investors. Submarine-cable redundancy, preferential tax incentives for deep-ocean cooling, and steady public-sector cloud migration sustain multi-tenant demand while creating fertile ground for hyperscale projects. Incumbent telecom operators wield the dual advantage of nationwide fiber and long-standing landing-station control, whereas new entrants differentiate through ultra-low-PUE engineering and edge capabilities. Funding visibility has improved thanks to the Rs 128 billion infrastructure budget and concessional green-energy loans, both of which underwrite capacity additions despite elevated energy prices

Key Report Takeaways

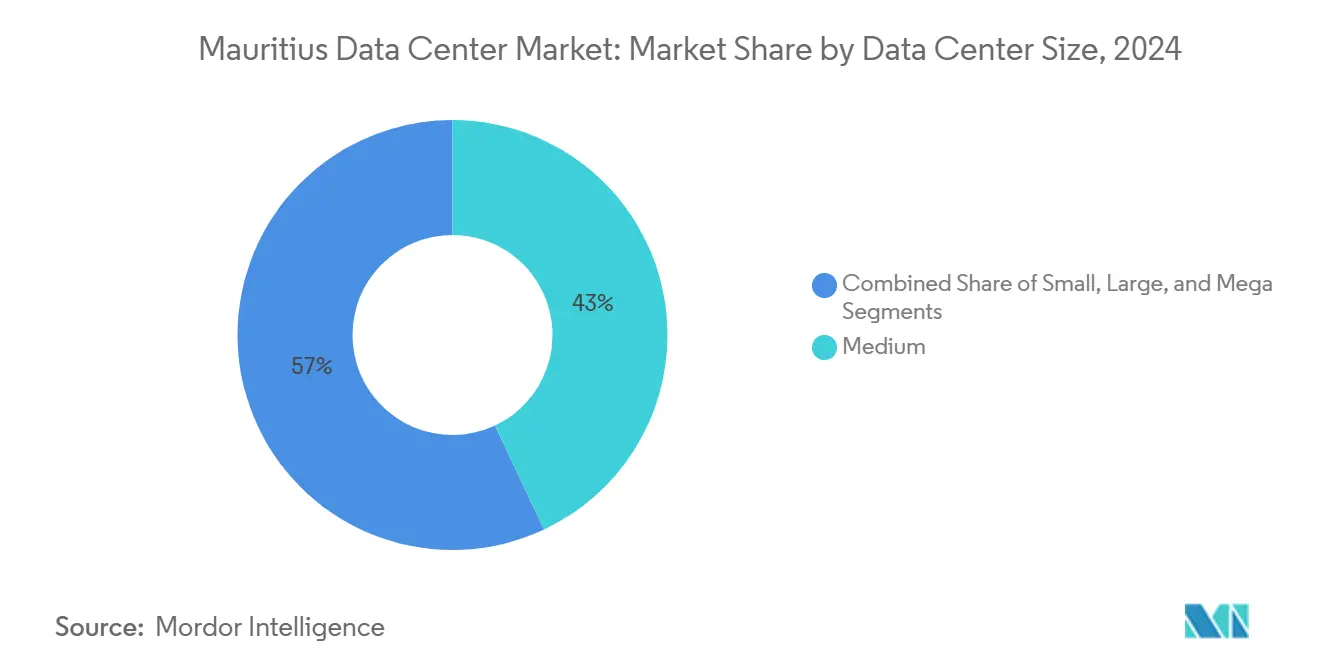

- By data center size, medium facilities accounted for 43% of the Mauritius data center market share in 2024, while mega sites are forecast to grow at a 18.2% CAGR to 2030.

- By tier, Tier III infrastructure captured a 50% share of the Mauritius data center market size in 2024, whereas Tier IV capacity is expected to advance at a 19.2% CAGR to 2030.

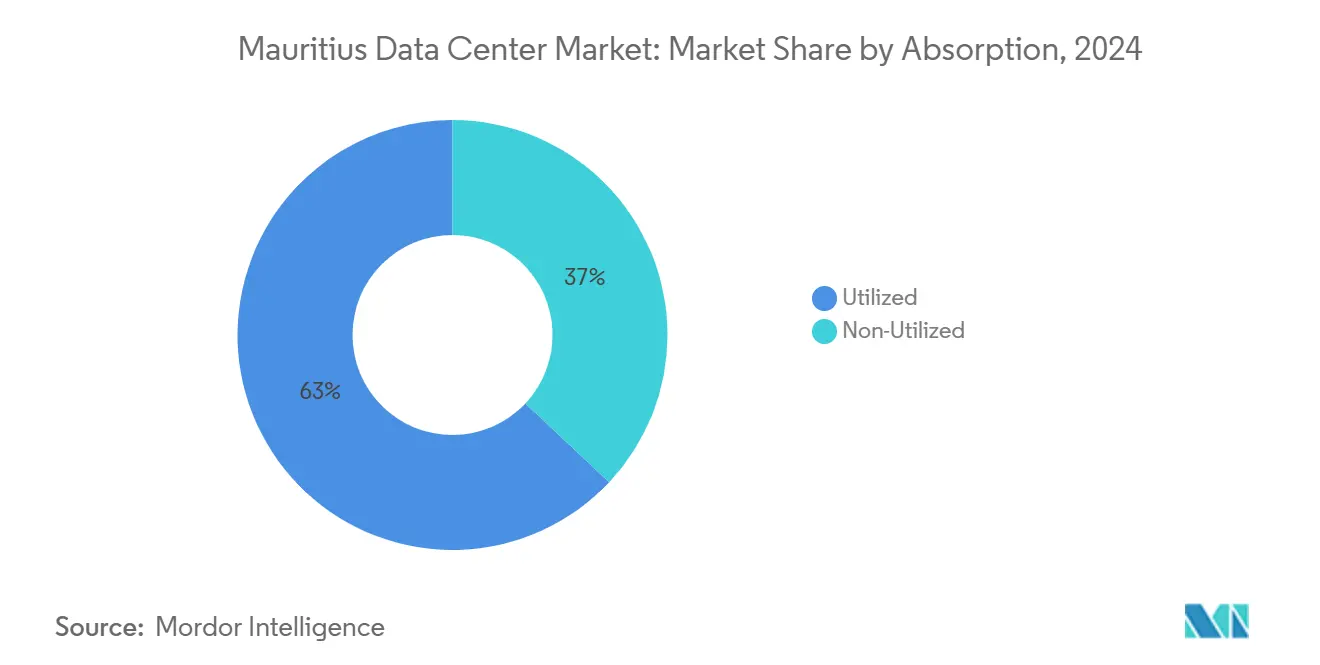

- By absorption, the utilized capacity represented 63% of the Mauritius data center market size in 2024 and is progressing at an 18.1% CAGR through 2030.

- By hotspot, Ebene Cybercity led with 50% revenue share in 2024; Phoenix and Quatre Bornes is projected to expand at a 17.59% CAGR through 2030.

Mauritius Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Mauritius Digital Agenda 2030 | +3.2% | National; concentrated in Ebene Cybercity | Medium term (2-4 years) |

| Submarine-cable redundancy (METISS, SAFE, T3) | +2.8% | National; Port Louis and Ebene | Long term (≥ 4 years) |

| Fintech and ICT-BPO demand | +2.1% | Ebene Cybercity; Phoenix and Quatre Bornes | Short term (≤ 2 years) |

| Tax incentives for Ebene DC assets | +1.9% | Ebene Cybercity and select zones | Medium term (2-4 years) |

| Ocean-based cooling pilots | +1.5% | Coastal sites near Port Louis | Long term (≥ 4 years) |

| Disaster-recovery hub positioning | +1.3% | National; Tier IV facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Smart Mauritius Digital Agenda 2030 Accelerates Cloud Adoption

The Digital Mauritius 2030 blueprint elevates ICT to a 5.6% GDP contributor and mandates a national e-platform roll-out that forces ministries to repatriate workloads into sovereign clouds. MauPass, the single-sign-on service introduced in 2020, now authenticates more than 1 million citizens and drives persistent compute loads that local operators convert into long-term contracts. Thales’ 2024 digital-ID modernization illustrates the standard of Tier III and Tier IV resiliency required for mission-critical workloads.[1]Thales Group, “Thales Leads Innovative Digital Transformation of the Mauritius National Identity System,” thalesgroup.com SME digital-onboarding programs backed by UNDP further broaden the domestic client base, insulating the Mauritius data center market from sole reliance on international tenants.

Submarine-Cable Redundancy Lowers Latency and Boosts Resiliency

The METISS, SAFE, and T3 systems together furnish 24 Tbps+ of active capacity, cutting latency to Johannesburg to 45 ms and enabling seamless traffic rerouting during faults.[2]Submarine Networks, “METISS,” submarinenetworks.comMauritius Telecom’s 2023 T3 landing adds a third path, raising operator confidence in the Mauritius data center market for high-frequency trading and real-time analytics. Cable ownership also acts as a barrier to entry, consolidating bargaining power around incumbents that can bundle cross-connects and international bandwidth.

Fintech and ICT-BPO Boom Driving Low-Latency Hosting Demand

Over 950 ICT firms employ 33,000 staff and intensify need for colocation that meets both PCI-DSS and ISO-27001 frameworks. Mauritius Commercial Bank’s award-winning 2024 trade-finance portal exemplifies latency-sensitive fintech workloads anchored in Ebene for sub-millisecond settlements. Emtel’s 5G rollout covering 80% of the island extends cloud-edge demand to Phoenix and Quatre Bornes, accelerating take-up of micro-data-centers that localize video streaming and AR-commerce.

Tax Incentives Under Investment Promotion Act Enable Ultra-Low-PUE Facilities

Developers adopting seawater air-conditioning enjoy eight-year income-tax holidays plus double depreciation, making PUE levels below 1.15 economically feasible. The Eco-Park pilot recorded 86% cooling-energy savings, validating the model and providing operators with a hedge against volatile electricity tariffs. When combined with a 3% corporate rate for export entities, the Mauritius data center market gains a price-performance advantage over many mainland African locations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity tariffs | -2.4% | National; energy-intensive facilities | Short term (≤ 2 years) |

| Scarce developable land | -1.8% | Ebene Cybercity; Port Louis; Phoenix and Quatre Bornes | Medium term (2-4 years) |

| Cyclone-season structural hardening | -1.2% | Nationwide; coastal zones | Long term (≥ 4 years) |

| Limited local demand | -0.9% | National; all facility types | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Electricity Tariffs from Imported Fossil Fuels

Average industrial power costs hover around USD 0.10/kWh, compressing margins for megawatt-scale deployments until renewable projects reach critical mass. The Rs 128 billion budget channels capital into solar and wind farms, yet grid parity is unlikely before 2027, leaving data-center P&L exposed in the interim.[3]Government Information Service, “Economic Renewal, Fiscal Consolidation and A New Social Order at the core of Budget 2025-2026,” govmu.org Operators counteract by over-sizing photovoltaic arrays and using SWAC to slash cooling load.

Cyclone-Season Structural Hardening Raises Capex

Building codes stipulate wind-resistance speeds of 250 km/h, which inflates steel and concrete requirements by up to 20%. Redundant diesel tanks must cover multi-day outages due to the Central Electricity Board’s restoration timelines, adding both capex and fuel logistics complexity. Nonetheless, past performance, such as uninterrupted operations during a 7.3-magnitude quake, proves the resilience payoff outweighs upfront costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega Facilities Usher in Hyperscale Era

Medium sites (1-10 MW) still account for 43% of the installed power, while the Mauritius data center market size for mega campuses (>25 MW) is projected to accelerate at an 18.2% CAGR as global cloud anchors negotiate turnkey land grants. Mauritius Telecom’s 400-rack Tier IV hall exemplifies the breadth of the medium segment, while Africa50’s USD 15 million backing for a 30 MW build signals imminent scale shifts. Operators emphasize modular electrical blocks to de-risk capex, enabling fast expansion when anchor tenants sign.

Edge suites below 500 kW flourish inside telecommunication exchanges, serving 5G low-latency zones. Large facilities, bridging 10-25 MW, act as staging grounds for overseas players testing the market waters before making a full hyperscale commitment. The Mauritius data center industry thereby evolves into a barbell structure of mega and edge nodes, with mid-range footprints gradually tapering post-2028.

By Tier Type: Tier IV Adoption Rises on Compliance Needs

Tier III offers the sweet-spot 99.982% availability at sustainable opex, justifying its 50% hold over the Mauritius data center market size. Yet Basel III and GDPR-equivalent statutes compel banks and cloud providers to insist on fault-tolerant Tier IV halls, propelling a 19.2% CAGR through 2030. Mauritius Telecom’s live Tier IV site showcases N+2 architecture and two independent utility feeds that mitigate single-point failures.

Lower-tier halls recede to non-critical dev-test workload enclaves. Over time, AI-driven predictive maintenance trims Tier IV operating overhead, narrowing cost gaps and accelerating migration of latency-sensitive fintech processes into higher-tier environments. The Mauritius data center market consequently witnesses a quality-over-quantity pivot as clients prioritize SLA assurances.

By Absorption: Utilized Capacity Signals ROI Discipline

Utilized racks captured 63% Mauritius data center market share in 2024 and will climb due to prudent supply discipline. Operators shun speculative shell builds, focusing on pre-let phases with committed contracts that convert directly into recurrent revenue streams. Hyperscale colocation bars pre-paid for 5-year terms dominate new booking pipelines, ensuring that fresh megawatts achieve 70% fill factors within 18 months.

Retail suites remain relevant for under-500 kW enterprise demands, especially in the accounting and legal fraternity migrating from on-premises closets. Wholesale colocation occupies the middle ground, supporting managed-services resellers keen to bundle connectivity. The Mauritius data center industry thus maintains balanced absorption, shielding asset owners from the vacancy cycles seen in larger metros.

By Hotspot: Ebene Cybercity Maintains Digital Primacy

Ebene’s 50% market share in Mauritius' data center market in 2024 underscores its entrenched ecosystem of global banks, software firms, and consultancies. The Mauritius data center market size, tied to Ebene, benefits from dual cable paths and a 15 km proximity to Port Louis airport, which accelerates equipment imports. Spill-over demand pushes Phoenix and Quatre Bornes to a 17.59% CAGR, aided by lower land costs and adjacency to Smart-City green-field plots. Emerging micro-edge nodes along coastal resorts feed tourism analytics and IoT applications, rounding out the hotspot hierarchy without threatening Ebene’s dominance.

Growth prospects hinge on municipal incentives that compress permit cycles from six to three months, a boon for hyperscale timelines. As mega facilities co-locate near the cable landing, cross-connect fees diminish, reinforcing Ebene’s gravitational pull on regional traffic. However, limited developable parcels may trigger vertical builds beyond eight floors, introducing engineering complexity.

Geography Analysis

Ebene Cybercity anchors half of the installed power thanks to cable adjacency, tax-holiday status, and ready access to bilingual IT talent. The Mauritius data center market size associated with Ebene enjoys 45 ms latency to Johannesburg, an edge that cements its role in disaster-recovery architectures for South African banks. Its clustering of vendors, integrators, and regulators slashes onboarding friction and continues to attract fintech sandboxes seeking tight compliance oversight.

Phoenix and Quatre Bornes are expected to record the highest geographic CAGR of 17.59% through 2030. Competitive land pricing, proximity to Smart-City consumer hubs, and seamless 5G coverage create fertile ground for edge-native architectures. The government’s Smart-City Scheme confers VAT waivers on imported ICT equipment, lowering build costs and attracting second-wave investors who view Ebene rents as prohibitive.

Port Louis retains strategic gravity as the regulatory and maritime capital. The Mauritius data center market in Port Louis benefits from customs clearance efficiency, enabling same-day part replenishment for mission-critical equipment. Its role as the main landing station sustains colocation uptake for international content providers who value immediate backhaul into African IXPs. Peripheral coastal towns host experimental SWAC pods, widening the geographic tapestry while validating marine-energy cooling economics.

Competitive Landscape

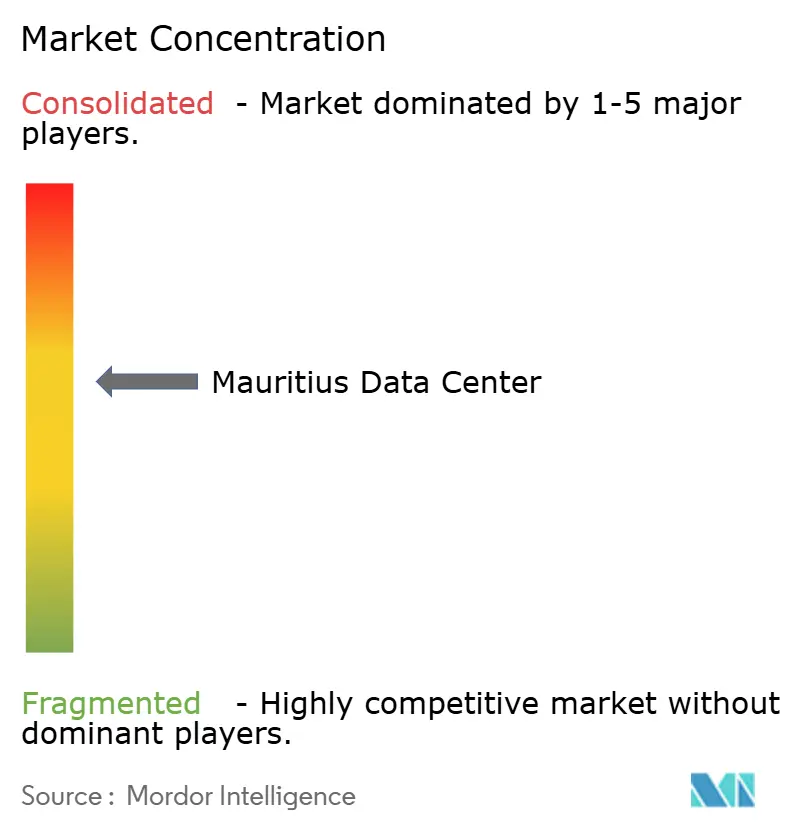

Market structure skews toward telecom incumbents—Mauritius Telecom and Emtel—whose dark-fiber footprints and landing-station rights underpin bundled colocation offers. Specialized entrants such as Rogers Capital position themselves on Tier IV uptime and ISO-certified security to court multinational banks. The Mauritius data center market remains moderately fragmented, yet concentration inches upward as hyperscale alliances deepen and submarine-cable equity stakes solidify incumbent moat width.

Strategic differentiation now revolves around cooling innovation, AI-based energy orchestration, and sovereign-cloud attestations. Operators piloting seawater loops report 75% cooling-energy savings, enabling price cuts that smaller rivals cannot replicate. Compliance capabilities anchored in ISO 27001 and SOC 2 frameworks further elevate switching costs for regulated tenants.

M&A chatter focuses on edge-asset roll-ups that can deliver sub-10 ms regional round-trips for 5G content. Africa Data Centres scouts joint ventures with local ISPs to pool land banks, while overseas funds eye greenfield plays in Phoenix for Smart-City adjacency. Despite these maneuvers, regulatory screening of foreign ownership ensures gradual, orderly consolidation, preserving service diversity within the Mauritius data center industry.

Mauritius Data Center Industry Leaders

Mauritius Telecom

Emtel Ltd

Rogers Capital Technology Services

Africa Data Centres (Mauritius)

Liquid Intelligent Technologies (Mauritius)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Raxio secured USD 100 million in debt financing from IFC to expand pan-African capacity, indirectly enhancing regional interconnect routes beneficial to Mauritius.

- February 2025: CSquared Link Holdings raised USD 25 million in new equity from Convergence Partners and IFC to extend open-access broadband, including spur links into Mauritius.

- December 2024: Google joined a USD 90 million investment into Cassava to augment African digital infrastructure that interfaces with Mauritius cable systems.

- December 2024: Mauritius Commercial Bank won African Bank of the Year, highlighting fintech-driven hosting demand.

Mauritius Data Center Market Report Scope

Mauritius Data Center Market Report is Segmented by (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, and Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot (Vilnius, Kaunas, Klaipėda, Rest of Lithuania). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| Small |

| Medium |

| Large |

| Mega |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Ebene Cybercity |

| Port Louis |

| Phoenix and Quatre Bornes |

| Rest of Mauritius |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| By Tier Type | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Ebene Cybercity | ||

| Port Louis | |||

| Phoenix and Quatre Bornes | |||

| Rest of Mauritius | |||

Key Questions Answered in the Report

What is the current installed power capacity in the Mauritius data center market?

The total live IT load is 5 MW in 2025, with committed projects lifting capacity to 11 MW by 2030.

How fast is capacity expected to grow?

Installed power is forecast to expand at a 17.08% CAGR between 2025 and 2030.

Which hotspot commands the largest share of facilities?

Ebene Cybercity accounts for 50% of operational capacity and remains the anchor location for new builds.

What tier level is most common in Mauritius facilities?

Tier III dominates at 50% share, offering 99.982% uptime suited for enterprise workloads.

Are tax incentives available for data-center investors?

Yes, investors using deep-ocean cooling receive eight-year income-tax holidays and double depreciation allowances.

How do submarine cables influence the market?

Three diverse systems—METISS, SAFE, T3—provide latency under 45 ms to Johannesburg and create strong redundancy, making Mauritius attractive for regional disaster-recovery nodes.

Page last updated on: