Manufacturing IT Sustainability and Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 12.16 Billion |

| Growth Rate (2026 - 2031) | 16.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

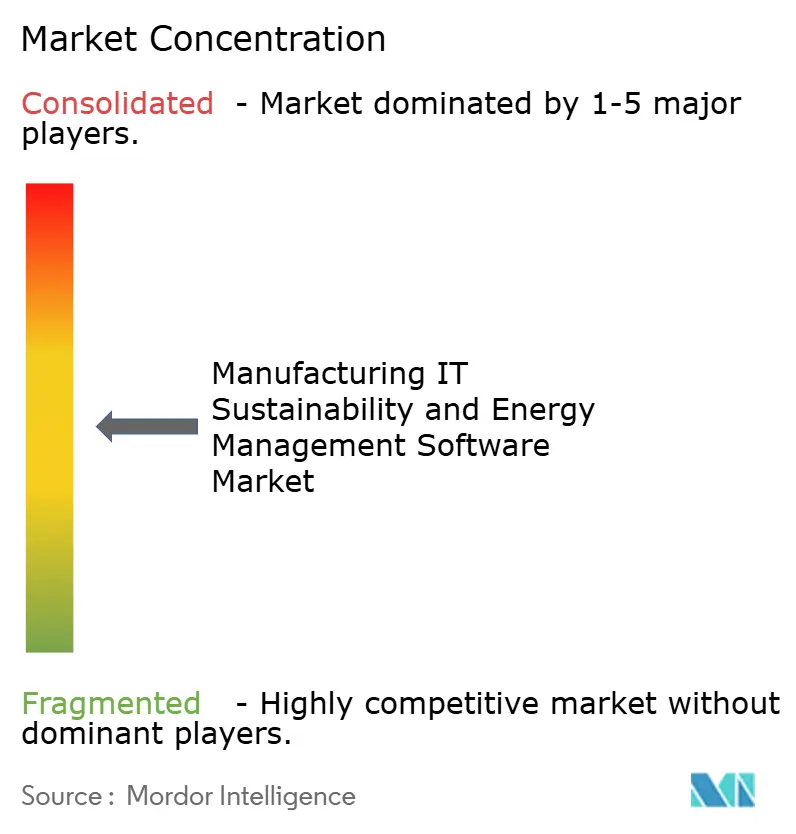

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manufacturing IT Sustainability and Energy Management Software Market Analysis by Mordor Intelligence

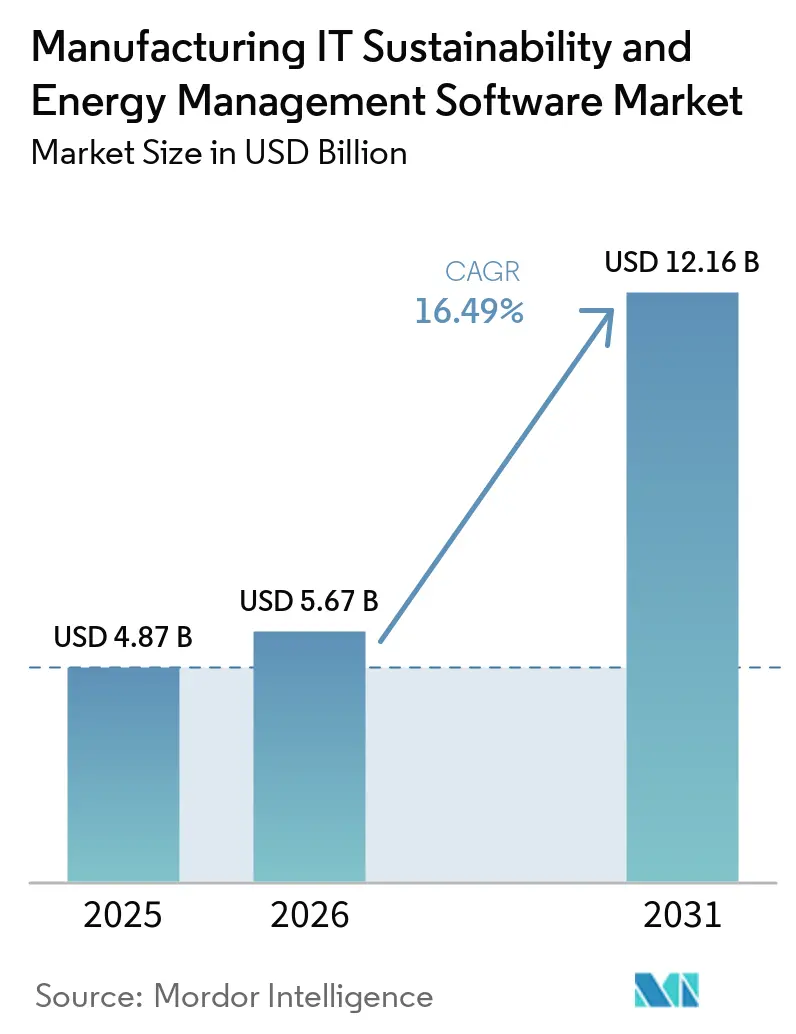

The manufacturing IT sustainability and energy management software market size is projected to expand from USD 4.87 billion in 2025 and USD 5.67 billion in 2026 to USD 12.16 billion by 2031, registering a CAGR of 16.49% over 2026-2031. This pace reflects a deeper shift in factory economics, where energy, emissions, and plant utility decisions are now tied more closely to financial control and production planning. The manufacturing IT sustainability and energy management software market is moving beyond basic metering and reporting, because buyers now expect carbon accounting, forecasting, and workflow integration inside the same software environment. Demand is also being shaped by unstable power costs, the need to manage energy use across multiple sites, and rising pressure to keep sustainability data audit-ready. Competition is tightening as industrial automation vendors, ERP providers, and dedicated sustainability platforms move into the same buying space and reduce room for narrow point solutions. The strongest openings remain in cloud deployments, carbon management modules, automotive manufacturing, and high-power facilities such as data centers, while adoption still slows where legacy plant systems, cybersecurity rules, and regional data controls complicate rollout.

Key Report Takeaways

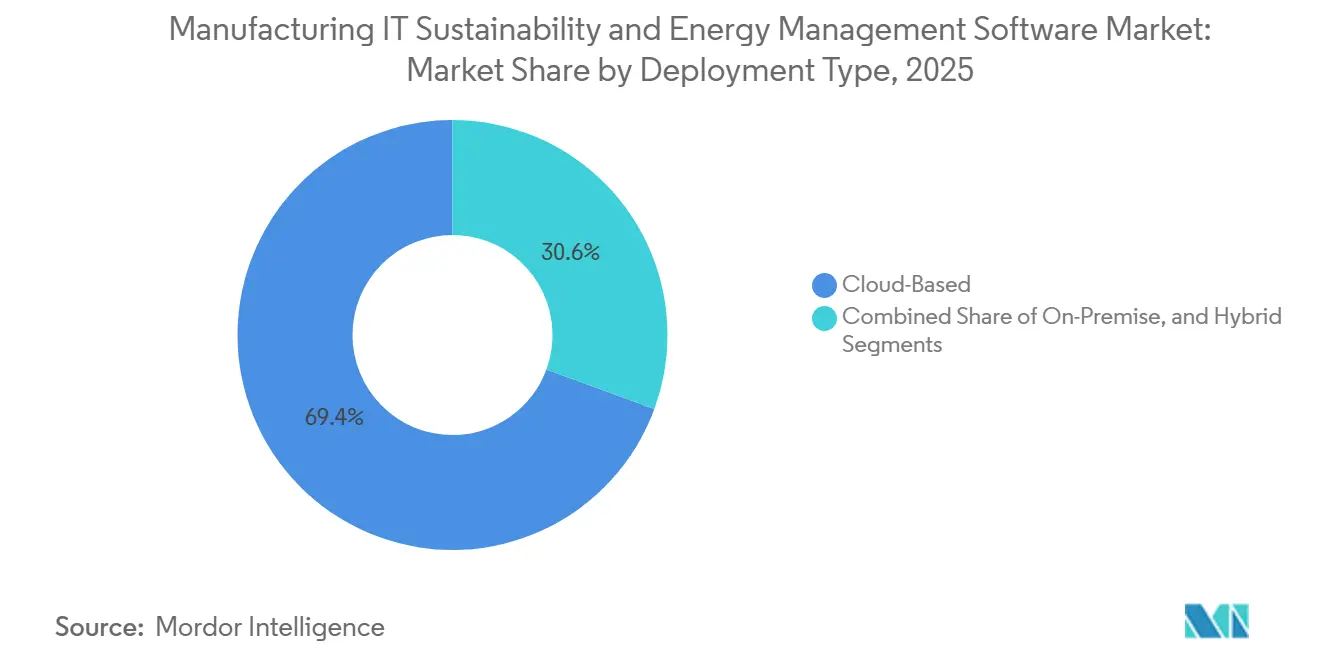

- By deployment type, cloud-based platforms held 69.41% share of the manufacturing IT sustainability and energy management software market in 2025, while cloud-based deployment is also projected to expand at a 19.67% CAGR through 2031.

- By module, industrial energy and utility management accounted for 26.92% of the manufacturing IT sustainability and energy management software market size in 2025, while carbon reporting and management is projected to expand at an 18.51% CAGR through 2031.

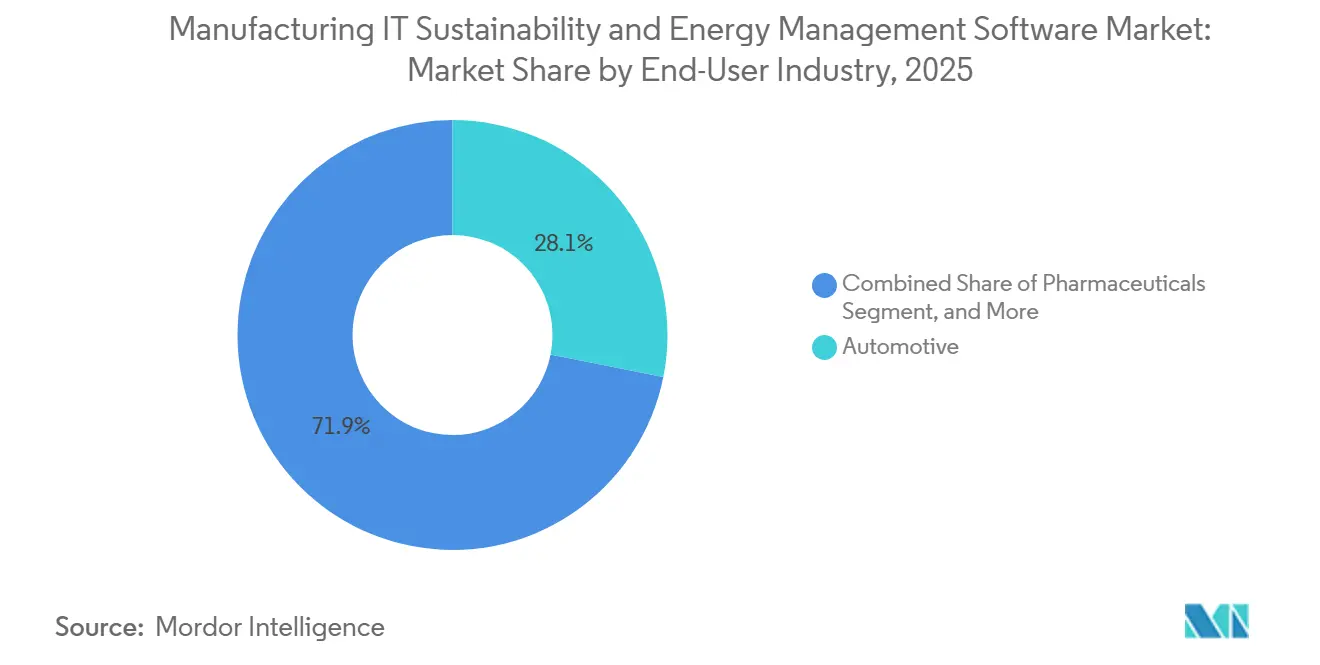

- By end-user industry, automotive manufacturing held 28.13% of the manufacturing IT sustainability and energy management software market share in 2025, while data centers and IT infrastructure are expected to record the highest growth at a 17.46% CAGR through 2031.

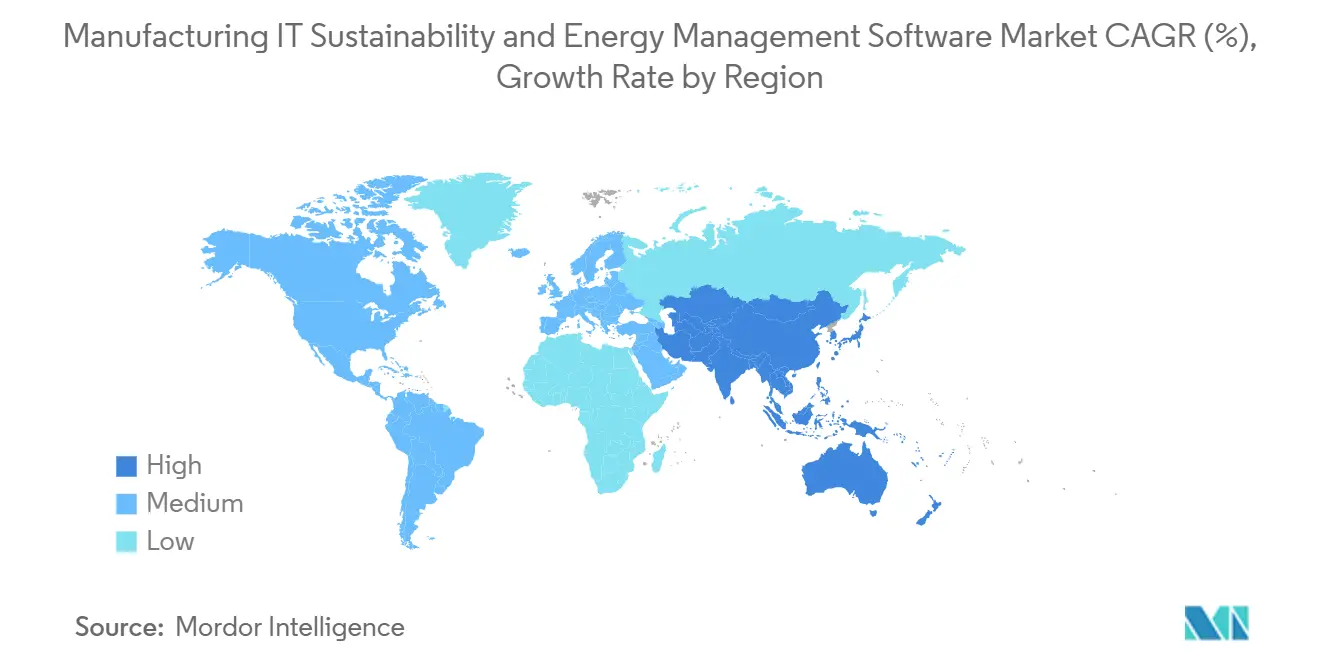

- By geography, North America led with a 34.14% share in 2025, while Asia-Pacific is projected to expand at an 18.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Manufacturing IT Sustainability and Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-Based Energy Optimization Across Industrial Assets | +2.8% | Global, highest deployment density in North America, Germany, and Japan | Medium term (2-4 years) |

| Compliance-Driven Sustainability Reporting Automation | +2.6% | EU core, including Germany, France, and Italy, and the UK, with spillover to North America and Asia-Pacific | Short term (≤ 2 years) |

| Carbon Accounting Integration With ERP and MES Stacks | +2.3% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Rising Energy Costs and Plant Utility Volatility | +2.1% | Europe, India, Southeast Asia, and North America | Short term (≤ 2 years) |

| Electrification of Manufacturing Operations and Process Heat | +1.8% | North America, Europe, and Japan, with early gains in Saudi Arabia and the UAE | Long term (≥ 4 years) |

| Edge-to-Cloud Industrial Energy Visibility for Multi-Site Plants | +1.5% | Global, with Asia-Pacific and the Middle East and Africa growing fastest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Based Energy Optimization Across Industrial Assets

AI-based energy optimization is becoming more practical inside plant operations, because manufacturers now want software that can respond to live production conditions instead of only reporting yesterday’s usage. In the manufacturing IT sustainability and energy management software market, this matters most when production schedules, utility signals, and plant assets need to be managed at the same time. Hitachi Plant Services stated that it strengthened the energy management functions of its FEMS platform from April 2026 for factories and research facilities, which supports the wider move toward more active plant-level control rather than passive monitoring. Honeywell also commercially launched its AI-powered control room assistant in March 2026, showing that operators are being given software tools that can surface actions faster inside industrial environments.[1]Honeywell International Inc., “Honeywell Unveils Commercial Launch of AI-Powered Control Room Assistant Following Successful Pilot,” Honeywell, honeywell.com The commercial value is shifting toward systems that sit inside day-to-day operations, because energy performance now depends on how well software can connect production, utilities, and plant response. That is why the manufacturing IT sustainability and energy management software market is increasingly rewarding vendors that can embed AI into plant workflows instead of keeping it separate from the operating stack.

Compliance-Driven Sustainability Reporting Automation

Mandatory sustainability reporting is one of the clearest near-term buying triggers in the manufacturing IT sustainability and energy management software market. Manufacturers are under pressure to collect plant data across many facilities, maintain audit trails, and reduce manual work that breaks down as reporting cycles become more demanding. SAP said in May 2026 that its new sustainability AI agents reduced scenario simulation time from 1 day to 20 minutes in beta use cases and cut packaging compliance review hours by more than 50%, demonstrating how software demand is moving toward automation rather than manual file handling.[2]SAP, “Autonomous Enterprise: New Sustainability AI Agents,” SAP News Center, news.sap.com This matters because reporting systems are no longer purchased solely for annual disclosures, as the same data structure is also needed for live monitoring and operational decisions. In practice, once manufacturers build verified, site-level data flows for compliance, they also lay the foundation for stronger energy visibility across production networks. The manufacturing IT sustainability and energy management software market is therefore benefiting from a link between compliance spending and longer-term operating software investment.

Carbon Accounting Integration With Erp and Mes Stacks

Carbon accounting is moving closer to core enterprise and production systems, and that shift is changing how the manufacturing IT sustainability and energy management software market is being bought. Buyers increasingly want emissions data to sit near finance, production orders, procurement records, and operational events, rather than inside a stand-alone reporting tool. IFS launched IFS Zero in May 2026 as an emissions operating system integrated with IFS Cloud ERP, enterprise asset management, and service management modules, and the company said the system reduces data collection effort by an estimated 30% while producing audit-ready outputs aligned with major reporting frameworks. SAP’s sustainability AI rollout also points in the same direction, because buyers are being offered automation inside an enterprise software environment instead of through disconnected overlays. This is important for the manufacturing IT sustainability and energy management software market because procurement decisions increasingly favor platforms that already sit in plant and enterprise workflows. The result is a market where integration depth matters as much as reporting functionality.

Rising Energy Costs and Plant Utility Volatility

Rising plant utility pressure is pushing the manufacturing IT sustainability and energy management software market toward a more operational role. When electricity costs move sharply, and multi-site facilities face different tariffs and load conditions, software becomes part of financial control rather than an efficiency reporting layer. Audi said it reduced energy consumption at its production sites by 73,965 MWh in 2025 through more than 400 efficiency measures under its Mission: Zero program, which shows how large manufacturers are treating structured monitoring and control as a direct cost issue. Stellantis also said its European manufacturing sites sourced 68% of their electricity from decarbonized sources in 2025 and is deploying battery energy storage systems across 20 plants as part of a 200 MWh program, reflecting the scale of energy planning now tied to industrial operations. In this setting, manufacturers need software that can connect site demand, energy sourcing, and facility performance across a wider operating footprint. That is why the manufacturing IT sustainability and energy management software market is seeing stronger demand from buyers that now view energy volatility as a recurring business constraint.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Integration Effort With Legacy OT and Control Systems | -2.8% | Global, highest friction in brownfield plants across South America, the Middle East and Africa, and Eastern Europe | Medium term (2-4 years) |

| Cybersecurity and Data Residency Constraints in Industrial Clouds | -2.2% | China, India, Russia, Germany, and North America | Short term (≤ 2 years) |

| Limited Standardization of Industrial Energy Data Models | -1.7% | Global, most acute in the Middle East and Africa and South America | Long term (≥ 4 years) |

| Change-Management Friction in Plant-Level Adoption | -1.3% | Global, most pronounced in food and beverage and chemicals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Effort With Legacy OT and Control Systems

Integration remains one of the hardest obstacles in the manufacturing IT sustainability and energy management software market. Many industrial sites still run a mix of control systems, data historians, and sub-metering setups that do not connect cleanly to modern cloud software. This forces project teams to spend more time on middleware, custom mapping, and data cleaning before any value can be shown to plant managers. The burden grows further when a facility discovers that existing sensor data is too coarse for tighter forecasting, demand response, or carbon tracking at the production-line level. That makes first deployments slower and more expensive, especially in brownfield facilities where energy and sustainability software must adapt to older plant conditions. As a result, the manufacturing IT sustainability and energy management software market still sees adoption delayed, not by lack of interest, but by the practical effort needed to connect software to the plant floor.

Cybersecurity and Data Residency Constraints in Industrial Clouds

Cybersecurity and data residency limits are also slowing parts of the manufacturing IT sustainability and energy management software market. Operational data can reveal production patterns, capacity usage, and energy behavior, so many manufacturers treat it as commercially sensitive even before formal privacy rules apply. Honeywell’s September 2025 battery energy storage automation launch highlighted ISA Secure 2 cybersecurity standards inside its software-linked architecture, which shows that secure-by-design positioning is already central to industrial energy offerings. Honeywell’s February 2026 collaboration with TCS around autonomous operations also reflects how vendors are pairing operational technology and enterprise IT expertise as data handling becomes more demanding across buildings and industries. These conditions push some buyers toward regional data storage, hybrid architectures, or slower cloud rollouts, which weaken the scale benefits that cloud platforms usually promise. The manufacturing IT sustainability and energy management software market, therefore, remains exposed to a constraint that is technical, regulatory, and operational at the same time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Platforms Set the Core Adoption Pattern

Cloud-based deployment held 69.41% share of the market in 2025, which made cloud the default architecture for the manufacturing IT sustainability and energy management software market rather than a premium option. The main reason is practical, because manufacturers need one environment that can ingest data from plants, meters, utility feeds, enterprise systems, and site users without rebuilding the stack at every location. In the manufacturing IT sustainability and energy management software industry, cloud also fits multi-site operating models better, since energy and sustainability teams are expected to compare performance across facilities in real time. That model becomes more attractive when reporting, carbon data collection, and operating analysis all depend on the same flow of information. Cloud-based deployment is also projected to expand at a 19.67% CAGR through 2031, which shows that this architecture is gaining share even as the overall manufacturing IT sustainability and energy management software market grows quickly.

Cloud platforms are also being favored because buyers want fewer breaks between finance systems, asset systems, plant dashboards, and sustainability reporting tools. The case for cloud is stronger when enterprise software vendors and industrial software providers both position their offerings as connected service layers instead of isolated applications. Hitachi Plant Services’ 2025 update to strengthen the energy management functions of its FEMS platform for factories and research facilities supports this shift toward more connected and scalable deployment models across site networks.[3]Hitachi Plant Services Co., Ltd., “2026年4月より、FEMSのエネルギー管理機能を強化,” Hitachi Plant Services, hitachi-hps.co.jp Honeywell’s software-linked control and operations launches also show that vendors are presenting digital layers as ongoing operating systems rather than one-time site tools. Even so, the manufacturing IT sustainability and energy management software market still leaves room for hybrid and on-premises choices in defense-linked operations, critical facilities, and locations with strict controls on operational data. Those models remain relevant, but they are gradually becoming exceptions as cloud defines the baseline for new investment.

By Module: Carbon Management Changes Platform Priorities

Industrial energy and utility management held the largest module share at 26.92% in 2025, which confirms that energy tracking, load visibility, utility monitoring, and demand management still form the installed base of the manufacturing IT sustainability and energy management software market. This module remains central because it is closest to daily plant economics and usually enters operations before broader sustainability tools do. At the same time, carbon reporting and management are projected to expand at an 18.51% CAGR through 2031, which shows where software budgets are now starting to shift. In one instance, carbon reporting and management are becoming more important because companies want emissions data to move through the same systems that already carry production and financial records. That change is lifting the strategic role of modules that can connect operational activity to verified emissions outputs inside the manufacturing IT sustainability and energy management software market.

IFS Zero reflects that direction clearly, because the platform links Scope 1, 2, and 3 calculations with ERP, asset, and service modules and reduces data collection effort by an estimated 30%.[4]IFS, “IFS Launches IFS Zero,” IFS, ifs.com SAP’s 2026 sustainability AI agent launch points to the same buying pattern, where regulatory readiness, footprint optimization, and packaging compliance are handled inside a broader software environment. Sphera also said it was named a leader in the 2026 Green Quadrant for enterprise carbon management software, which supports the continued relevance of specialized sustainability platforms in areas where compliance and environmental workflows remain complex. The manufacturing IT sustainability and energy management software market is therefore not abandoning legacy energy modules, but it is clearly reordering platform priorities around carbon, compliance, and integration. Over time, buyers are likely to prefer fewer modules that cover wider workflows, because the value of the system depends more on connected execution than on stand-alone reporting screens.

By End-User Industry: Automotive Manufacturing Leads While Data Centers Rise Fast

Automotive manufacturing held 28.13% of the manufacturing IT sustainability and energy management software market share in 2025, which placed it well ahead of other end-user groups. The sector already works with deeper MES, ERP, and supply-chain data structures than many other industries, so it can layer energy and carbon management onto systems that are already digital. This gives automotive manufacturers a practical advantage when they need to connect plant energy use, production activity, and supplier-facing sustainability requirements. The manufacturing IT sustainability and energy management software market also benefits from the scale of electrification planning inside automotive facilities, where operating decisions increasingly depend on site-level energy coordination. That is why automotive remains the clearest large user base in this market.

Stellantis said its European manufacturing sites sourced 68% of their electricity from decarbonized energy in 2025 and is deploying battery energy storage systems across 20 plants in a 200 MWh program, which shows how automotive operators are linking procurement, storage, and plant performance under one energy agenda. Audi’s disclosure that it cut site energy consumption by 73,965 MWh in 2025 through more than 400 efficiency measures points to the same pattern of structured factory-level management. Beyond automotive, food and beverage, chemicals and materials, pharmaceuticals, and heavy industrial manufacturing remain meaningful demand pockets because each has site processes that can benefit from stronger monitoring and compliance control. Data centers and IT infrastructure is projected to expand at a 17.46% CAGR through 2031, making it the fastest-growing end-user segment as AI compute facilities put more pressure on power use, cooling loads, and uptime discipline. In the manufacturing IT sustainability and energy management software market, this means growth is spreading from traditional factories toward power-intensive digital infrastructure that now behaves like an energy-critical operating environment.

Geography Analysis

North America held 34.14% share of the market in 2025, which gave the region the lead in the manufacturing IT sustainability and energy management software market. The region benefits from a broad mix of automotive production, high-value manufacturing, and large-scale digital infrastructure that creates demand across more than one end-user group. Enterprise software adoption is also more mature in many North American industrial settings, which supports cloud migration and software integration across site portfolios. This has helped the manufacturing IT sustainability and energy management software market size build on existing IT and operational data foundations instead of starting from manual systems in every facility. The United States remains the center of this demand pattern, while Canada and Mexico add support through cross-border manufacturing linkages and shared supply-chain requirements.

Europe remains one of the most policy-driven regions in the manufacturing IT sustainability and energy management software market, because industrial companies there face stronger pressure to manage verified sustainability data and plant energy use together. Germany stands out in Europe due to its large manufacturing base and its need for more structured energy management across industrial operations. Automotive decarbonization efforts in the region also reinforce software demand, as shown by Stellantis’ expansion of decarbonized electricity sourcing and storage across manufacturing plants. Europe therefore continues to shape the manufacturing IT sustainability and energy management software market through a mix of compliance pressure, industrial scale, and stronger links between plant operations and environmental reporting.

Asia-Pacific is projected to expand at an 18.12% CAGR through 2031, making it the fastest-growing regional block in the manufacturing IT sustainability and energy management software market. Japan is showing one of the clearest examples of active deployment, with Hitachi Plant Services strengthening the energy management functions of its FEMS platform from April 2026 for factories and research facilities. The region also benefits from expanding manufacturing capacity, new digital infrastructure, and rising energy management needs across industrial sites. China and India add scale, while South Korea supports demand through electronics and semiconductor operations that already depend on structured energy tracking. South America remains led by Brazil’s industrial base, and the Middle East and Africa are seeing demand tied to national decarbonization programs and newer industrial projects. This keeps the manufacturing IT sustainability and energy management software market geographically broad, even though maturity levels still vary sharply by region.

Competitive Landscape

The manufacturing IT sustainability and energy management software market shows moderate-to-high concentration at the top, but it is still structurally fragmented across industrial automation vendors, ERP providers, and dedicated sustainability software players. That means large vendors hold strong positions, yet no single group fully controls all buyer needs across modules, deployment models, and regions. The market is becoming harder for point solutions because buyers want tighter links between operational data, enterprise systems, compliance workflows, and plant decision support. This is reducing the separation that once existed between automation software and sustainability software in the manufacturing IT, sustainability, and energy management software market. As a result, competition is shifting from feature lists toward integration depth, installed base leverage, and the ability to support multi-site operating models.

Several company actions in 2026 show how this competitive pattern is developing. SAP announced sustainability AI agents in May 2026 that work across regulatory readiness, footprint optimization, and packaging compliance, which strengthens its position among buyers who already run enterprise workflows inside SAP environments. IFS launched IFS Zero in May 2026 to tie emissions management to ERP, enterprise asset management, and service management, which broadens its relevance in asset-intensive sectors. Honeywell’s commercial launch of an AI-powered control room assistant in March 2026 also shows that operational technology vendors are moving further into software-led decision support for industrial environments. In the manufacturing IT sustainability and energy management software market, these moves matter because they bring software control, sustainability tasks, and plant operations closer together inside the same vendor ecosystem. That dynamic makes installed relationships more valuable and raises the switching cost for customers who want end-to-end platforms.

At the same time, focused vendors still have room in parts of the manufacturing IT sustainability and energy management software market where buyers need specialized energy accounting or carbon management. Sphera’s 2026 leader recognition in enterprise carbon management software supports the strength of specialized platforms in sectors where environmental data workflows remain complex.[5]Sphera Solutions, Inc., “Sphera Named a Leader in the 2026 Green Quadrant for Enterprise Carbon Management Software,” Sphera, sphera.com Johnson Controls also disclosed in April 2026 that 77% of new product R&D in 2025 was directed toward sustainability and climate-related innovation, which signals how established industrial companies are shifting investment toward software-linked and efficiency-oriented offerings. The result is a field where scale matters, but differentiation still depends on whether a vendor can connect industrial operations, energy management, and reporting into one usable system. Buyers in the manufacturing IT sustainability and energy management software market are therefore likely to keep favoring vendors that can combine credibility at the plant floor with enterprise-level integration.

Manufacturing IT Sustainability and Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

IBM Corporation

SAP SE

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IFS launched IFS Zero, an agentic Emissions Operating System for asset-intensive industries providing a unified Scope 1, 2, and 3 carbon calculation platform integrated with IFS Cloud ERP, Enterprise Asset Management, and Service Management modules. The solution reduces data collection effort by an estimated 30% and produces audit-ready outputs aligned with the GHG Protocol, CSRD, and Carbon Border Adjustment Mechanism requirements. Research from Generation Investment Management indicates full adoption across IFS's three largest industrial sectors could abate over 2% of global CO2 emissions.

- May 2026: SAP announced sustainability AI agents, including a Sustainability Regulatory Readiness Agent, a Footprint Optimization Agent, and a Packaging Compliance Agent, for general availability by the end of 2026. Beta results showed scenario simulation time cut from approximately one day to 20 minutes, packaging compliance review hours reduced by more than 50%, and GHS classification effort lowered by up to 80%, with agents operating within SAP Sustainability Control Tower and the SAP Autonomous Suite.

- March 2026: Honeywell commercially launched Experion Operations Assistant, an AI-powered control room advisor that monitors plant performance and provides proactive guidance on impending incidents following a successful pilot phase, integrating with the existing Honeywell Experion PKS distributed control system infrastructure.

- February 2026: Honeywell and Tata Consultancy Services (TCS) announced a collaboration to enhance autonomous operations for buildings and industries using Honeywell Forge IoT analytics, combining Honeywell's OT-layer technology with TCS's IT and consultancy capabilities, initially offered in India before extending to the United States and the Middle East.

Global Manufacturing IT Sustainability and Energy Management Software Market Report Scope

Manufacturing IT Sustainability and Energy Management Software refers to a specialized category of digital solutions designed to assist industrial and manufacturing enterprises in achieving energy efficiency, monitoring carbon emissions, and embedding sustainability into their operational processes. These platforms integrate real-time monitoring, predictive analytics, and automated controls with compliance reporting. They enable manufacturers to optimize utility usage, manage industrial assets effectively, and adhere to ESG and regulatory requirements, all while enhancing overall operational efficiency.

The Manufacturing IT Sustainability and Energy Management Software Market is Segmented by Deployment Type (Cloud-Based, On-Premise, and Hybrid), Module (Industrial Energy and Utility Management, Carbon and Sustainability Management, Industrial Asset and Facility Sustainability Management, and Compliance and Regulatory Management), End-User Industry (Automotive, Food and Beverage, Chemicals and and Materials, Pharmaceuticals, Heavy Industrial Manufacturing, Oil and Gas, Energy and Utilities, Commercial Facilities and Buildings, and Data Centers and IT Infrastructure), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Industrial Energy and Utility Management |

| Carbon and Sustainability Management |

| Industrial Asset and Facility Sustainability Management |

| Compliance and Regulatory Management |

| Automotive |

| Food and Beverage |

| Chemicals and Materials |

| Pharmaceuticals |

| Heavy Industrial Manufacturing |

| Oil and Gas |

| Energy and Utilities |

| Commercial Facilities and Buildings |

| Data Centers and IT Infrastructure |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Middle East |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Type | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Module | Industrial Energy and Utility Management | |

| Carbon and Sustainability Management | ||

| Industrial Asset and Facility Sustainability Management | ||

| Compliance and Regulatory Management | ||

| By End Use Industry | Automotive | |

| Food and Beverage | ||

| Chemicals and Materials | ||

| Pharmaceuticals | ||

| Heavy Industrial Manufacturing | ||

| Oil and Gas | ||

| Energy and Utilities | ||

| Commercial Facilities and Buildings | ||

| Data Centers and IT Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the manufacturing IT sustainability and energy management software market?

The manufacturing IT sustainability and energy management software market stood at USD 5.67 billion in 2026 and is projected to reach USD 12.16 billion by 2031 at a CAGR of 16.49%.

Which deployment model leads this software space?

Cloud-based platforms led with a 69.41% share in 2025 and are also the fastest-growing deployment type with a 19.67% CAGR through 2031.

Why are manufacturers investing more in sustainability and energy management software now?

The main drivers are rising energy cost pressure, the need for audit-ready sustainability data, and tighter links between emissions management, ERP workflows, and plant operations.

Which module is seeing the strongest growth through 2031?

Carbon and sustainability management is the fastest-growing module, with an 18.51% CAGR, as buyers move from stand-alone reporting toward connected carbon data management.

Which end-user group creates the largest demand today?

Automotive led with a 28.13% share in 2025, supported by stronger MES, ERP, electrification, and plant energy coordination capabilities.

Which region is growing the fastest over the forecast period?

Asia-Pacific is projected to grow at an 18.12% CAGR through 2031, supported by factory upgrades, digital infrastructure buildout, and stronger energy management adoption.

Page last updated on: