Mammalian Cell Fermentation Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

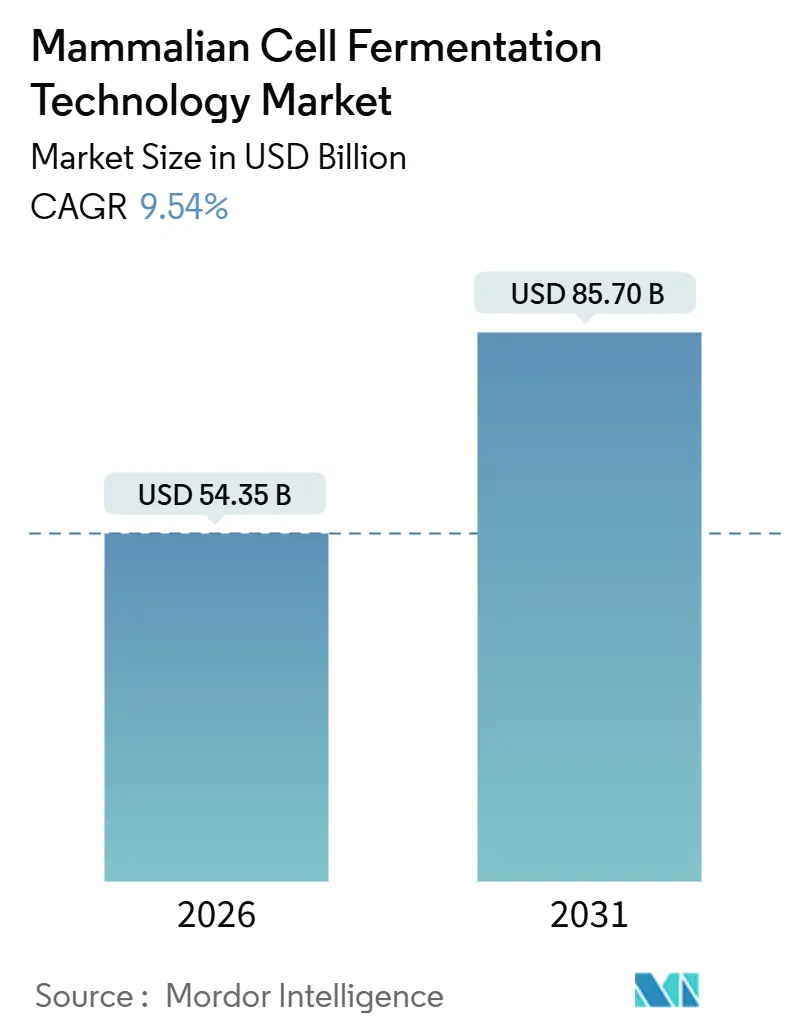

| Market Size (2026) | USD 54.35 Billion |

| Market Size (2031) | USD 85.70 Billion |

| Growth Rate (2026 - 2031) | 9.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mammalian Cell Fermentation Technology Market Analysis by Mordor Intelligence

The Mammalian Cell Fermentation Technology Market size is estimated at USD 54.35 billion in 2026, and is expected to reach USD 85.70 billion by 2031, at a CAGR of 9.54% during the forecast period (2026-2031).

Momentum stems from three structural shifts: monoclonal antibodies account for more than half of recent U.S. novel-drug approvals, single-use stirred-tank bioreactors now dominate new capacity additions, and contract development and manufacturing organizations (CDMOs) are scaling perfusion suites to win biosimilar and cell-therapy mandates. Upstream productivity gains from AI-guided media optimization, coupled with supply-chain investments in low-shear bubble-column systems, are compressing the cost of goods and reshaping site-selection strategies. Meanwhile, carbon-border tariffs in the European Union are accelerating regionalized feedstock production, and real-time analytics platforms from Thermo Fisher and Sartorius are turning bioreactors into connected assets that anticipate titer drift in advance. Competitive focus has therefore shifted from vessel scale to software intelligence, with platform leaders bundling single-use hardware, sensors, and cloud-based control loops into subscription models to lock in recurring revenue.

Key Report Takeaways

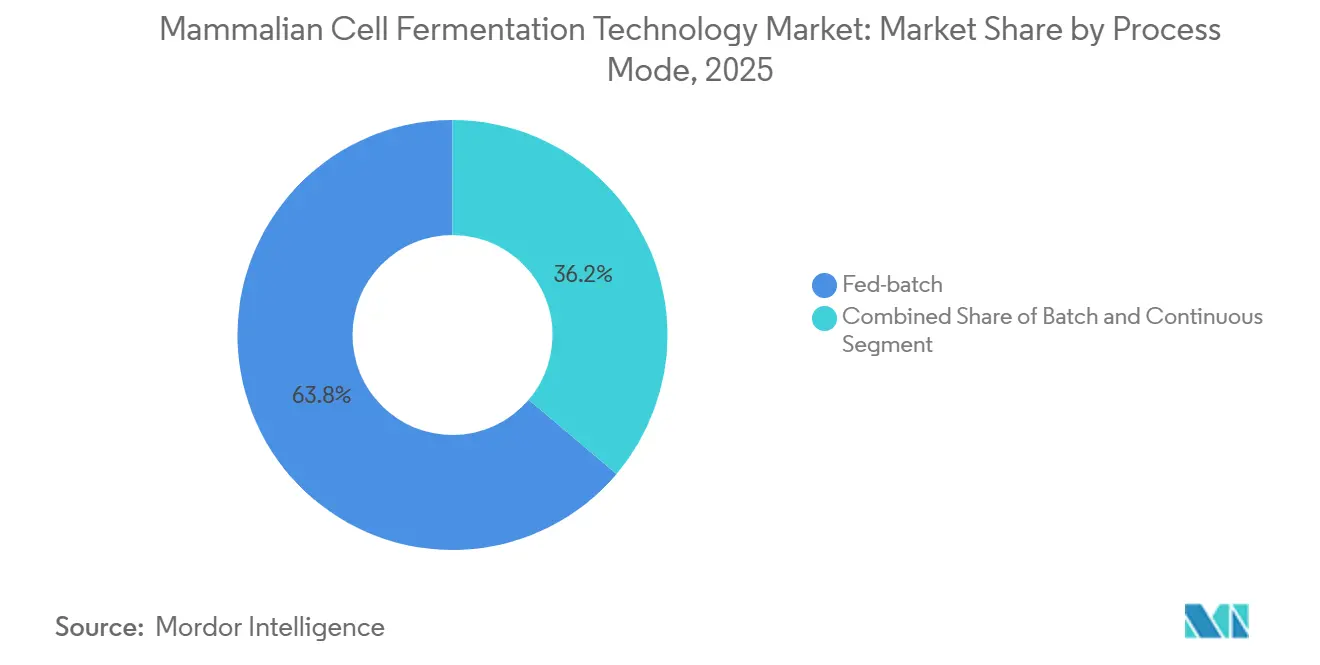

- By process mode, fed-batch accounted for 63.81% of the mammalian cell fermentation technology market share in 2025, while continuous perfusion is forecast to expand at a 9.94% CAGR through 2031.

- By bioreactor type, single-use stirred-tank systems led with 56.29% revenue share in 2025; bubble-column and air-lift designs are projected to register the fastest 10.81% CAGR through 2031.

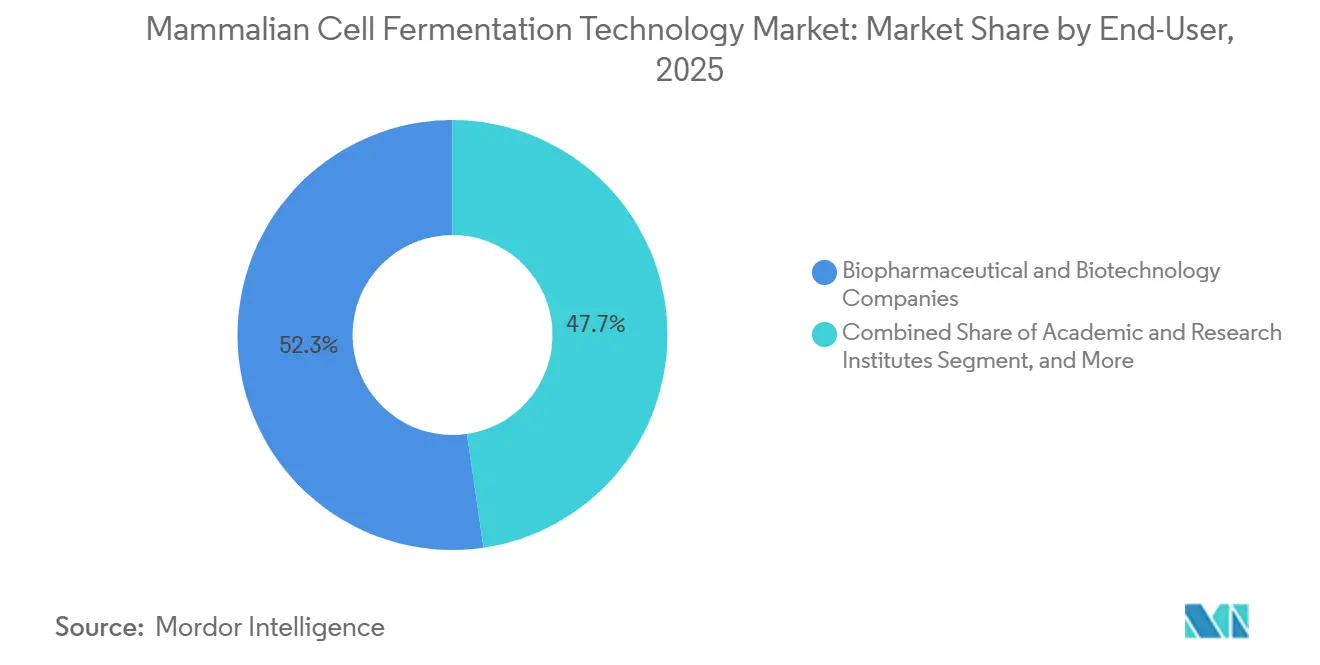

- By end user, biopharmaceutical and biotechnology companies accounted for 55.82% of spending in 2025, whereas CDMOs are set to post the highest 11.22% CAGR during the forecast period.

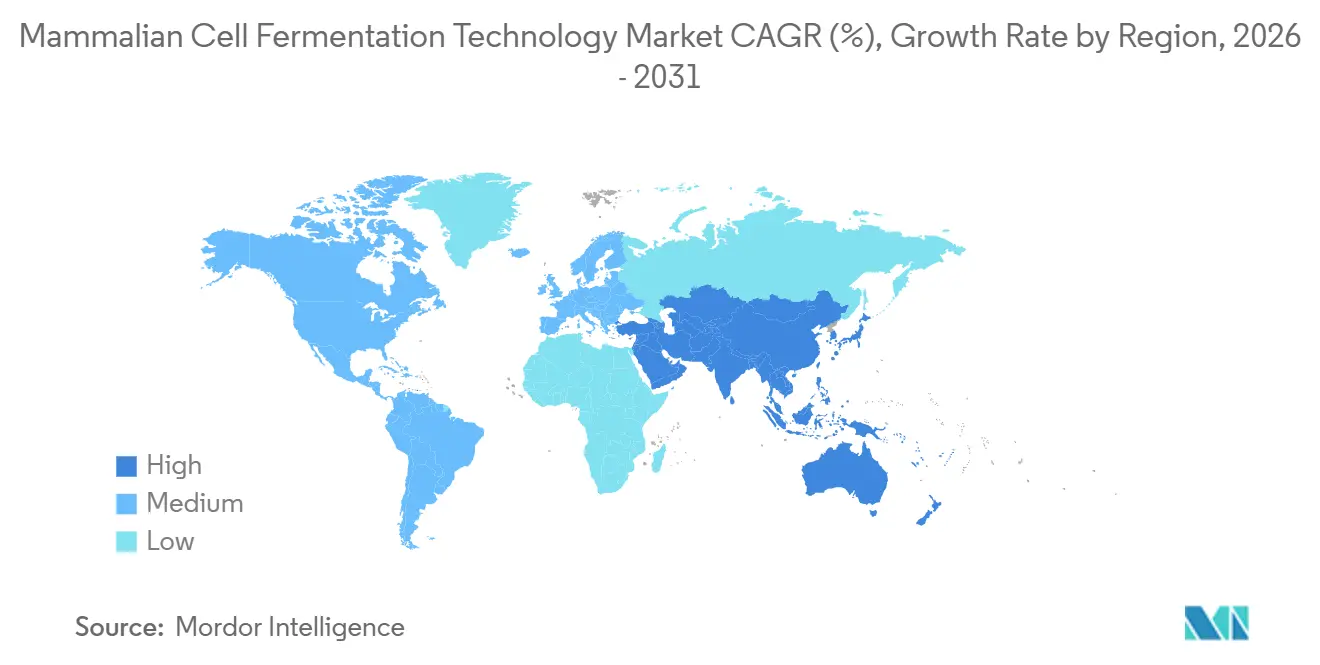

- By geography, North America retained a 40.03% share of the mammalian cell fermentation technology market in 2025, but Asia-Pacific is advancing at a 12.95% CAGR on the back of capacity expansions in China and South Korea.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mammalian Cell Fermentation Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Therapeutic Monoclonal Antibodies | +2.8% | North America, Europe | Long term (≥ 4 years) |

| Rapid Shift Toward Single-Use Bioreactors & Disposable Assemblies | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| Expansion of Biomanufacturing Capacity in Asia-Pacific | +1.9% | Asia-Pacific | Medium term (2-4 years) |

| AI-Driven Media Optimization Enabling Ultra-Low CSPR Perfusion | +1.2% | North America, Europe, China | Long term (≥ 4 years) |

| Outsourcing Boom as CDMOs Add Large-Scale Perfusion Suites | +1.6% | North America, Europe | Medium term (2-4 years) |

| Carbon-Border Tariffs Supporting Regional Fermentation Hubs | +0.8% | Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Therapeutic Monoclonal Antibodies

Thirty-one of the 55 novel drugs cleared by the U.S. Food and Drug Administration in 2024 were monoclonal antibodies, underscoring a steady shift toward complex biologics. Capacity investments keep pace: Lonza is spending USD 1.2 billion to add four 20,000-liter single-use bioreactors in Vacaville, California, and Fujifilm Diosynth has committed a similar outlay to ten perfusion suites in North Carolina.[1]Lonza Group, “Investor Presentation 2025,” lonza.com Europe mirrors the trend, as the European Medicines Agency validated 14 biosimilar antibody filings in 2025, each of which requires dedicated cell-line trains. Perfusion keeps cells in exponential growth for up to 60 days, achieving 12 g/L titers; that productivity means a single 2,000-liter perfusion reactor can displace three 10,000-liter fed-batch vessels, freeing clean-room space for fill-finish work. Sponsors are therefore locking in multi-year slots well ahead of late-stage readouts to derisk launch timelines.

Rapid Shift Toward Single-Use Bioreactors & Disposable Assemblies

Single-use stirred tanks accounted for 56.29% of global installed capacity in 2025 and eliminated the USD 18-25 million capital charge associated with stainless-steel fabrication and cleaning skids.[2]Sartorius AG, “Press Release Oct 2025,” sartorius.comWuXi Biologics installed 18 new 5,000-liter units between 2024 and 2025, which trimmed commissioning time from 24 months to 14 months and opened the door to 47 additional CDMO contracts during 2025. Regulatory pressure, however, has intensified: the U.S. FDA’s March 2024 Q3E update caps leachable concentrations at 1 ppm over 18-month stability windows, a threshold that 22% of legacy bags cannot meet. Sartorius answered with the Flexsafe Pro bag, launched in October 2025, whose three-layer co-extrusion cuts platinum residues by 85% but adds a 34% price premium. Commercial-scale manufacturers now rely on hybrid layouts that pair stainless-steel reactors with single-use harvest bags, eliminating leachable risk without sacrificing upstream volume.

Expansion of Biomanufacturing Capacity in Asia-Pacific

Asia-Pacific added 1.2 million liters of mammalian capacity during 2024–2025, spearheaded by China, India, and South Korea. Beijing’s CNY 18.6 billion subsidy pool underwrote a 240,000-square-meter WuXi Biologics campus that came online in early 2026, housing vessel arrays from 500 liters to 5,000 liters. India’s BioNEST scheme co-funded six regional hubs offering subsidized access to pilot-scale reactors, cutting seed investment for domestic start-ups by 40%. South Korea’s tax incentives helped Samsung Biologics and Celltrion extend the country’s CDMO leadership, while AGC Biologics opened a 50,000-liter plant in Yokohama targeting local sponsors that prefer domestic supply. Multinational drug makers, therefore, split their clinical-and-launch chains, producing Phase I/II material in Asia-Pacific to capture 30% labor savings, while retaining commercial supply in North America or Europe to satisfy regulators.

AI-Driven Media Optimization Enabling Ultra-Low CSPR Perfusion

Bayesian algorithms now trim media-development cycles from 18 months to six by inferring nutrient-uptake profiles from only 200 initial conditions. Thermo Fisher’s BioProduction Cloud connects Raman spectroscopy to hybrid mechanistic–machine-learning models that adjust glucose and amino acid feeds every 4 hours, boosting volumetric productivity by 22% and saving USD 180,000 per 2,000-liter batch.[3]Thermo Fisher Scientific, “BioProduction Solutions,” thermofisher.com Sartorius’ Ambr digital twin forecasts lactate spikes 36 hours ahead of manual sampling, preventing titer drift before it materializes. Such optimization achieves cell-specific perfusion rates below 0.03 nL per cell per day, halving media usage and trimming chromatography resin consumption by 28%. Adoption remains concentrated among top-tier CDMOs because mid-size providers lack the data infrastructure required for closed-loop control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Chemically-Defined Media & Feeds | –1.4% | Global | Medium term (2-4 years) |

| Extractables / Leachables Risk in Single-Use Systems | –0.9% | North America, Europe | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks for Sterile Disposable Bags & Filters | –1.1% | Global | Short term (≤ 2 years) |

| Shortage of Perfusion-Process Engineers | –0.8% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Chemically-Defined Media & Feeds

Chemically defined media cost USD 1,200–1,800 per kilogram in early 2026 and accounted for 28% of the cost of goods for monoclonal antibodies in fed-batch campaigns. Recombinant insulin prices rose 34% between 2023 and 2025 following supplier consolidation, squeezing biosimilar developers aiming for a USD 150-per-gram cost threshold. Innovator drugs can absorb that burden, but smaller sponsors increasingly revert to hydrolysate blends that introduce batch variability, attracting regulator scrutiny. The FDA’s Q3E guidance adds further cost by mandating 18-month leachable studies for each resin formulation used in single-use assemblies, delaying platform qualification and inflating inventory holding expenses. Although Sartorius’ premium Flexsafe Pro bag mitigates platinum residues, its 34% price lift confines uptake to high-value antibody-drug conjugates.

Supply-Chain Bottlenecks for Sterile Disposable Bags & Filters

Lead times for sterile bags and 0.2-micron filters stretched to 14 weeks in early 2026, more than double 2023 levels, because Sartorius, Thermo Fisher, and Merck KGaA control a combined 78% of global capacity. WuXi Biologics had to delay the start-up of four 5,000-liter reactors in Suzhou by 11 weeks in late 2025, resulting in an estimated USD 18 million in revenue foregone. The constraint stems from limited gamma-irradiation slots for polymer films. Sartorius is investing EUR 120 million to double bag throughput in Göttingen by Q3 2027, but analysts foresee double-digit week lead times persisting through 2028. Vertical integration has begun: Lonza bought a 40% stake in Repligen’s assembly business in 2024 to secure a dedicated supply for its U.S. sites. In parallel, staffing shortages push CDMOs to rely on costly external engineers, underscoring the value of internal training academies such as Thermo Fisher’s 12-week perfusion course, which graduated 140 specialists in its first year.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Mode: Continuous Gains Despite Fed-Batch Lock-In

Fed-batch processes delivered 63.81% of 2025 revenue, underscoring entrenched regulatory comfort and the familiarity of existing workforce routines. Nevertheless, continuous perfusion is advancing at a 9.94% CAGR as oncology pipelines demand tighter impurity profiles and AI increases volumetric titers toward 12 g/L. Perfusion’s edge narrows when AI-guided fed-batch hits 8 g/L: the productivity gap shrinks to 46%, making capital-heavy continuous layouts more selective for high-value molecules. Regulatory agencies have cleared 14 commercial continuous filings since 2022 under ICH Q13, but validation packages have taken an additional 6 to 9 months, tempering adoption.

Batch mode clings to 8% use, mostly in discovery and academia, where simplicity outweighs productivity constraints. U.S. National Institute of Standards and Technology hubs now offer subsidized 200-liter batch reactors, cutting early development costs by 40% and reinforcing the configuration’s relevance. Overall, process-mode choice is bifurcating: fed-batch remains the baseline for large commercial antibodies, continuous perfusion gains share in niche cell-therapy and antibody-drug-conjugate projects, and small-scale batch continues as an accessible training platform.

By Bioreactor Type: Single-Use Dominance Meets Bubble-Column Disruption

Single-use stirred tanks accounted for 56.29% of 2025 capacity, bypassing cleaning validation and shortening facility timelines by nearly a year. Yet stainless-steel systems keep 34% share at commercial scales ≥2,000 liters, where high utilization makes steam-in-place economics compelling for blockbuster antibodies produced in 12 or more cycles per year. Bubble-column and air-lift designs, posting a 10.81% CAGR, reduce shear stress by 68% and thus preserve cytotoxic payloads on antibody-drug conjugates; PBS Biotech’s vertical-wheel reactor reached 9.4 g/L titers in a 2025 pilot, matching stirred-tank output at lower energy input.

The mammalian cell fermentation technology market for single-use reactors surpassed stainless steel in 2025 and is widening its lead each year of the forecast. However, the mammalian cell fermentation technology market share for bubble-column systems remains in low single digits, suggesting room for disruptive gains if the technology scales beyond 1,000-liter prototypes. Hybrid facilities where stainless vessels couple to single-use harvest bags are now standard in late-stage perfusion, balancing throughput with control over extractability.

By End-User: CDMO Surge Reshapes Value Chains

Biopharma and biotech firms contributed 55.82% of 2025 spending, but their share is receding as outsourcing accelerates. The mammalian cell fermentation technology market size allocated to CDMOs is forecast to grow fastest, propelled by Lonza, Samsung Biologics, and WuXi Biologics pre-building suite capacity that sponsors can reserve years in advance. Academic and research institutes account for 8% of demand, typically operating 50- and 200-liter systems for early discovery. Thermo Fisher’s turnkey training addresses the skills gap that hinders academic adoption of perfusion.

Other end-users, such as government laboratories engaged in pandemic preparedness, rely on surge agreements with providers like Lonza, which maintains 40,000 liters of reserve capacity for rapid vaccine response. A clear divide is emerging: large pharmas keep in-house stainless-steel blocks for high-volume blockbusters, whereas small innovators and biosimilar houses funnel almost all volume to CDMOs to sidestep capital burden.

Geography Analysis

North America held a 40.03% share of the mammalian cell fermentation technology market in 2025, thanks to installed giants such as Lonza’s Vacaville and Portsmouth sites, as well as Thermo Fisher’s Massachusetts and North Carolina clusters. Regional growth slows relative to Asia-Pacific but remains steady as blockbuster launches, regulatory familiarity, and deep talent pools offer defensive moats.

Asia-Pacific expands fastest at a 12.95% CAGR: WuXi Biologics’ 240,000-square-meter Wuxi campus came online in 2026, and Samsung Biologics operates the world’s largest single-site total capacity at 784,000 liters in Incheon. India’s BioNEST hubs and South Korea’s generous tax credits help regional developers reduce the cost of goods while meeting local content requirements. The mammalian cell fermentation technology market share for the Middle East & Africa, plus South America, but Saudi Arabia’s USD 850 million Riyadh facility scheduled for 2027, signals gradual diversification.

Emerging carbon-border tariffs in Europe drive localized feedstock processing in Poland and Ireland, and renewable-powered sites in Singapore further redistribute supply chains. Multinationals increasingly deploy dual networks: clinical batches in Asia-Pacific for speed and cost, commercial supply in OECD territories for regulatory convenience.

Competitive Landscape

The five largest suppliers, Lonza, Thermo Fisher Scientific, Sartorius Stedim, Samsung Biologics, and WuXi Biologics, controlled a significant share of installed global capacity in 2025, giving the mammalian cell fermentation technology market a moderate concentration profile. Platform leaders pursue three converging playbooks. First, equipment and consumables specialists such as Sartorius integrate sensors, bags, and digital twins to tie users into proprietary ecosystems, evidenced by EUR 680 million in 2024 revenue from Flexsafe Pro bags and Ambr software. Second, mega-CDMOs like Samsung Biologics and WuXi Biologics pre-build 20,000-liter perfusion suites, courting biosimilar producers that need speed-to-market. Third, niche innovators, including PBS Biotech and Cellexus, attack underserved segments such as low-shear 500- to 1,000-liter perfusion for antibody-drug conjugates.

Investment remains aggressive: Lonza, Thermo Fisher, and Sartorius injected a combined USD 3.6 billion into single-use platform expansions during 2024–2025, aimed at shortening lead times and building scale economies. Sartorius filed 14 patents in polymer chemistry to strip platinum catalyst residues, directly addressing FDA concerns that stalled 22% of legacy bag validations. Smaller providers hedge against supply risk by forming strategic partnerships. Lonza’s minority acquisition of Repligen’s assembly business ensures priority bag allocation for U.S. sites.

Competitive intensity is therefore defined by software capability, supply-chain resilience, and capital depth rather than vessel volume alone. As a result, top-tier CDMOs use cloud analytics not only to boost titers but also to generate differentiated key performance indicator (KPI) dashboards that simplify regulatory submissions, creating switching costs for sponsors locked into digital ecosystems.

Mammalian Cell Fermentation Technology Industry Leaders

Getinge AB

Thermo Fisher Scientific Inc.

WuXi Biologics

Danaher Corporation

Eppendorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: A new PhD training program launches to bridge the biomanufacturing scale-up gap between academia and industry.

- October 2025: Asterix Foods emerges from stealth to unlock a second wave of animal-free proteins in plant cell culture.

- March 2025: Shilpa Medicare unveils a hybrid CDMO service by combining its mammalian and 200-kiloliter microbial capacity.

- December 2024: Sekisui Diagnostics completes a GBP 15.7 million (USD 20.7 million) cGMP expansion at its U.K. microbial CDMO site.

Global Mammalian Cell Fermentation Technology Market Report Scope

The Mammalian Cell Fermentation Technology Market refers to the global industry encompassing the development, manufacturing, supply, and use of advanced bioprocessing technologies and equipment for the fermentation (culturing) of mammalian cells in controlled bioreactor environments to produce complex biologics.

The Mammalian Cell Fermentation Technology Market Report is segmented by process mode into batch, fed-batch, and continuous; by bioreactor type into stainless-steel stirred-tank, single-use stirred-tank, bubble-column/air-lift, and other types; by end user into biopharmaceutical & biotechnology companies, CDMOs, academic & research institutes, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. Market forecasts are provided in terms of value (USD).

| Batch |

| Fed-batch |

| Continuous |

| Stainless-steel stirred-tank |

| Single-use stirred-tank |

| Bubble-column / air-lift |

| Other Bioreactor Types |

| Biopharmaceutical & Biotechnology Companies |

| Contract Development & Manufacturing Organisations |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Process Mode | Batch | |

| Fed-batch | ||

| Continuous | ||

| By Bioreactor Type | Stainless-steel stirred-tank | |

| Single-use stirred-tank | ||

| Bubble-column / air-lift | ||

| Other Bioreactor Types | ||

| By End-user | Biopharmaceutical & Biotechnology Companies | |

| Contract Development & Manufacturing Organisations | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the mammalian cell fermentation technology market?

The market was valued at USD 54.35 billion in 2026 and is projected to reach USD 85.70 billion by 2031.

Which process mode is growing fastest?

Continuous perfusion is the fastest-growing mode, forecast to advance at a 9.94% CAGR through 2031.

Why are single-use bioreactors so popular?

They eliminate the need for expensive cleaning infrastructure and cut facility timelines by nearly 1 year, giving them a 56.29% share of 2025 installations.

Which region is adding capacity most rapidly?

Asia-Pacific leads with a 12.95% CAGR, driven by incentives from China, India, and South Korea for biologics manufacturing.

How is AI being applied in mammalian fermentation?

Platforms from Thermo Fisher and Sartorius use machine learning and Raman spectroscopy to adjust nutrient feeds in real time, boosting titers by around 22%.

Page last updated on: