Malaysia Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

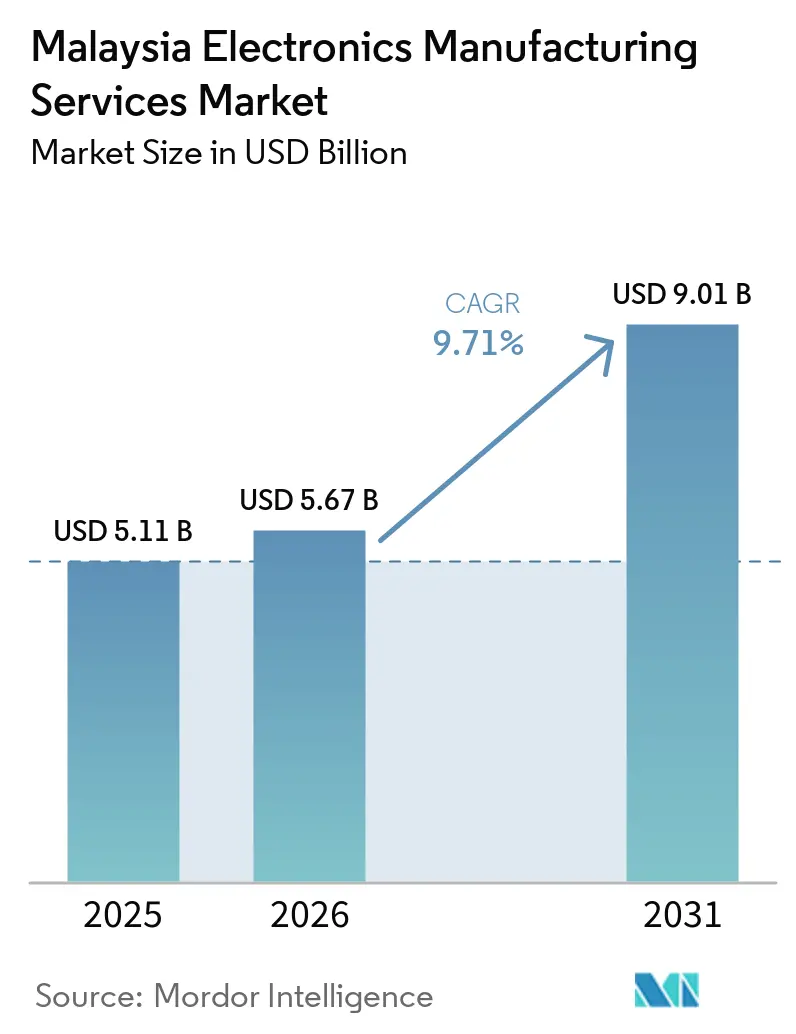

| Base Year Market Size (2025) | USD 5.11 Billion |

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 9.01 Billion |

| Growth Rate (2026 - 2031) | 9.71% CAGR |

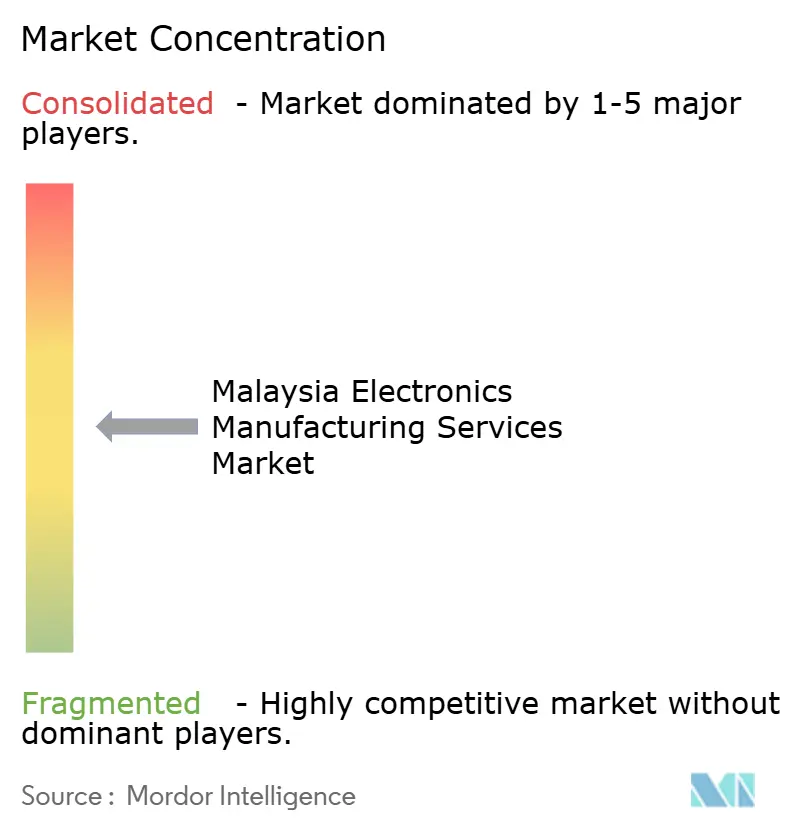

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Malaysia Electronics Manufacturing Services Market size is expected to grow from USD 5.11 billion in 2025 to USD 5.67 billion in 2026 and is forecast to reach USD 9.01 billion by 2031 at 9.71% CAGR over 2026-2031.

The Malaysia electronics manufacturing services market is expanding as more global electronics programs are being shifted into Malaysia under China-plus-one sourcing plans, while Penang keeps drawing large manufacturing commitments and supplier follow-on investments. The market is also being supported by a policy shift toward outcome-based incentives, which is pushing producers to move beyond low-cost assembly and build stronger automation, local sourcing, and workforce capabilities. Demand is becoming more complex as AI server assembly, advanced packaging, 5G radio-frequency work, and higher-value box-build programs grow in parallel and pull local providers into work that was once closer to the OSAT scope. The Malaysian electronics manufacturing services market also benefits from stronger trade positioning for US-bound electronics flows, which supports order visibility for suppliers already operating in Penang and Johor. At the same time, talent shortages in advanced manufacturing and rising operating costs are limiting how quickly providers can scale new capabilities, which keeps competitive pressure elevated across the forecast period.

Key Report Takeaways

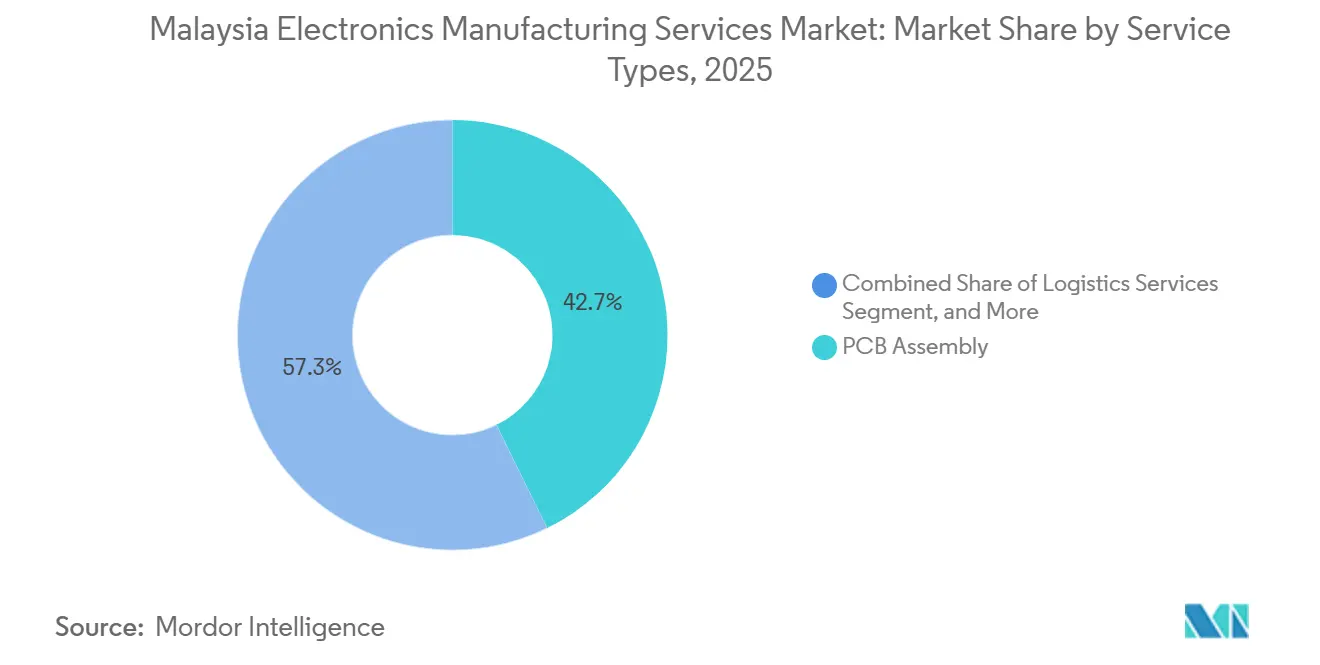

- By service type, PCB Assembly held 42.73% of revenue in 2025, while Electromechanical Assembly and Box Build is projected to grow at a 9.86% CAGR through 2031.

- By business model, Contract Manufacturing accounted for 60.91% of the Malaysia electronics manufacturing services market in 2025, while Hybrid/Turnkey/Other Business Models is set to record the fastest CAGR at 10.13% through 2031.

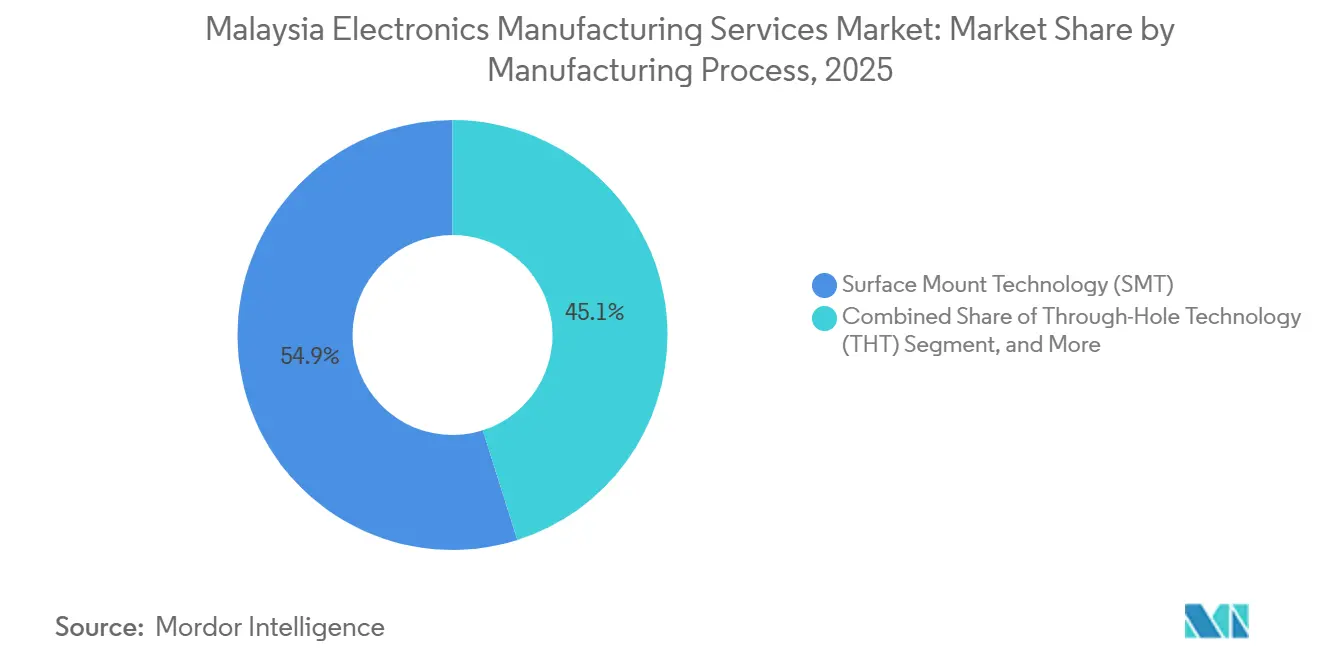

- By manufacturing process, Surface Mount Technology represented 54.88% of revenue in 2025, while Advanced Packaging/Hybrid Processes is projected to expand at a 10.73% CAGR through 2031.

- By end-user, Consumer electronics captured 31.46% of revenue in 2025, while Automotive is forecast to grow at a 10.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Understanding the full system requires moving beyond Malaysia boundaries into a wider international view. Mordor Intelligence captures the global electronics manufacturing services market scope in its worldwide coverage.

Malaysia Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Diversification Away from Mainland China | +2.3% | Global, with concentrated gains in Penang and Johor | Long term (≥ 4 years) |

| Growing Foreign Direct Investment in Penang's EMS Corridor | +1.9% | Penang, with spillover to Kedah and Perak | Medium term (2-4 years) |

| Government Incentives Under National Investment Aspirations | +1.6% | National, with early wins in Penang, Selangor, Johor | Medium term (2-4 years) |

| Expansion of 5G Handset Exports from Malaysia | +1.1% | Penang and Klang Valley, spill-over to Johor | Short term (≤ 2 years) |

| Rising Demand for High-Mix, Low-Volume Production | +0.9% | Penang core, secondary uptake in Johor | Medium term (2-4 years) |

| Emergence of Smart Factory 4.0 Adoption Among Tier-2 EMS | +0.7% | National, with early gains in Penang industrial parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Diversification Away from Mainland China

Sustained US-China trade tension has pushed the Malaysia electronics manufacturing services market from a secondary backup location into a core production option for global electronics supply chains. Cumulative US foreign direct investment in Malaysia reached MYR 218.2 billion (USD 49.37 billion), by 2024, and approved US investments in the first half of 2025 totaled MYR 10.4 billion (USD 2.35 billion), which points to a structural shift rather than a short-term hedge. Malaysia then strengthened that position when the US-Malaysia trade agreement was finalized in April 2026, securing a 19% reciprocal tariff rate and 1,711 tariff-line exemptions worth MYR 22 billion (USD 4.98 billion), based on 2024 export value. That arrangement also benefits Chinese EMS investors who have already set up Malaysian operations, because they can continue serving US customers from a lower-tariff production base while keeping supplier continuity in place. This helps explain why China ranked among the top 3 foreign investment sources for Penang manufacturing in 2025. As the China-plus-two model becomes more common, the Malaysia electronics manufacturing services market is likely to see broader demand across SMT, box-build, and advanced assembly lines, not just basic outsourced assembly.

Growing Foreign Direct Investment in Penang's EMS Corridor

Penang's current investment cycle is changing the Malaysia electronics manufacturing services market in a deeper way than earlier waves of labor-focused expansion. Approved manufacturing investments in Penang reached MYR 22.4 billion (USD 5.07 billion) in 2025, up 29% from 2024, and foreign direct investment contributed MYR 15.2 billion (USD 3.44 billion), or 68% of the total. Intel's advanced packaging complex in Penang carries a MYR 12 billion (USD 2.71 billion) commitment and was reported as 99% complete ahead of first-phase operations in 2026, which raises the bar for local yield control and quality systems. South Korea's Sustio completed a MYR 326 million (USD 73.76 million), second expansion phase in May 2026, while Chipbond opened a MYR 800 million (USD 200 million), advanced OSAT facility in Batu Kawan in February 2026. A denser anchor-supplier ecosystem shortens sourcing lead times and improves co-location for high-mix runs where speed matters as much as cost. That makes Penang the strongest cluster effect inside the Malaysia electronics manufacturing services market and gives surrounding states more spillover potential as land and utility constraints rise in the core corridor.

Government Incentives Under National Investment Aspirations

Malaysia's incentive framework is now steering the Malaysia electronics manufacturing services market toward higher-value programs instead of pure low-cost assembly. The New Incentive Framework took effect for the electrical and electronics manufacturing sector on March 1, 2026, and links benefits to economic complexity, high-income job creation, domestic linkage depth, and ESG performance. The National Investment Aspirations also includes a MYR 1 billion (USD 226.2 million) strategic investment fund for IC design services and high-value manufacturing, while the Industry4WRD Intervention Fund provides a 70:30 matching grant of up to MYR 500,000 for eligible manufacturing SMEs adopting Industry 4.0 tools.[1]Ministry of Investment, Trade and Industry, “Industry4WRD,” Ministry of Investment, Trade and Industry, miti.gov.my This is important for Tier-2 EMS operators because it reduces some of the cost barriers that have slowed automation and smart factory upgrades. The cluster development pillar also gives early weight to Penang, Johor, and the Klang Valley, which means geographic concentration is now part of policy design instead of an accidental outcome. Since enhanced allowances depend on MIDA oversight and minimum Manufacturing Technology Score performance, the Malaysia electronics manufacturing services market is being pushed toward operators that can prove automation, local procurement, and workforce upgrading at the same time

Expansion of 5G Handset Exports from Malaysia

5G device output is moving the Malaysia electronics manufacturing services market into more demanding radio-frequency sub-assembly and precision soldering work. Malaysia's electrical and electronics exports reached MYR 601.21 billion (USD 136.02 billion), in 2024, and shipments during January to July 2025 rose 17.3% year on year to MYR 391 billion (USD 88.46 billion). In 2025, total E&E exports expanded 18.4%, while exports of AI-related components such as integrated circuits, printed circuits, and semiconductor manufacturing equipment surged 54.7% year on year in the first 11 months. The revenue effect is not only a volume story, because ViTrox pointed to strong second-half 2025 demand tied to AI infrastructure, 5G devices, EVs, and advanced medical technology, which shows bill-of-materials complexity is also increasing. Malaysia also confirmed 32 ARM chip design licenses at SEMICON SEA 2026, which supports a broader domestic design base behind future 5G and AI hardware programs. As more local design work is pulled into the production cycle, the Malaysia electronics manufacturing services market should benefit from a wider pipeline of prototype, validation, and early-stage manufacturing programs rather than only final assembly work

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages in Advanced Packaging | -1.3% | National, most acute in Penang and Klang Valley | Long term (≥ 4 years) |

| Energy-Cost Volatility Affecting SMT Lines | -1.1% | National, primarily industrial users in Peninsular Malaysia | Short term (≤ 2 years) |

| Currency Fluctuation Risk Versus USD-Denominated Components | -0.7% | National, most exposed in import-dependent Tier-2 EMS | Medium term (2-4 years) |

| Intensifying Regional Competition From Vietnam and Thailand | -0.5% | National, with highest exposure in labor-intensive sub-segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages in Advanced Packaging

The talent shortage facing the Malaysia electronics manufacturing services market is structural and is strongest in the same advanced processes that are growing the fastest. High-tech manufacturing recorded a 5.2% vacancy rate in the first quarter of 2025, the highest among all manufacturing sub-sectors, with 5,782 open positions. Bank Negara Malaysia found that 72% of electrical and electronics firms treated recruitment as their main operating challenge, while industry data pointed to 15% annual attrition to higher-paying markets, especially Singapore. Salary gaps help explain the migration pressure, with Singapore IT graduates starting pay reported above USD 3,770 per month compared with USD 1,100 to USD 1,560 in Malaysia's IC design field. This is starting to affect contract economics because retention cost is now entering pricing discussions for multi-year production programs. The government's plan to train 60,000 semiconductor engineers under the National Semiconductor Strategy will help over time, but the multi-year horizon means the Malaysia electronics manufacturing services market still has to bridge the gap through automation spending that smaller providers struggle to fund.

Energy-Cost Volatility Affecting SMT Lines

Energy use has become a sharper cost issue for the Malaysia electronics manufacturing services market because SMT lines are among the most electricity-intensive assets on the factory floor. Malaysia's base electricity tariff for industry rose 14.2% to 45.62 sen per kWh in July 2025 under Regulatory Period 4 after rates had been held flat since 2014. The Federation of Malaysian Manufacturers warned that the new structure could weaken competitiveness for energy-intensive operations, and electricity can account for up to 40% of production cost in some high-throughput assembly environments. Cost pressure then became harder to predict when the Automatic Fuel Cost Adjustment started in July 2025, and the projected AFA rate for August 2026 stood at +3.93 sen per kWh. Malaysia's producer price index for electricity and gas also rose 9.6% year on year in March 2026, which confirms that utility pressure is still feeding through operating budgets. That creates a double burden for operators still running legacy SMT equipment because they face both higher unit costs and weaker monthly cost visibility, which is speeding up investment in more efficient reflow ovens and digital power management systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Types: PCB Assembly Leads While Box-Build Moves Up The Value Chain

PCB Assembly retained 42.73% of Malaysia electronics manufacturing services market share in 2025, which reflects the long-standing strength of board-level assembly across consumer and communications programs. Electromechanical Assembly and Box Build is projected to grow at a 9.86% CAGR through 2031 as customers place more value on fully tested, shipment-ready units instead of bare board output. The Malaysia electronics manufacturing services market is also seeing stronger demand for Engineering Services and Test and Development Implementation as programs arriving from China require more design-for-manufacture input and validation support. Logistics Services remains smaller in revenue terms, but it is becoming more important as providers use bonded warehousing and customs capabilities to help customers manage tariff uncertainty and delivery risk. The broad direction is a move from single-step outsourcing to multi-service contracts that cover prototyping, production, testing, and fulfillment inside one relationship.

That shift is visible in the way global firms are using Malaysia. Syntiant opened a USD 15 million manufacturing and R&D campus in Penang in January 2026, expanded its footprint to 220,000 square feet, and lifted annual production capacity to 1.6 billion units.[3]InvestPenang, “Syntiant Launches New Manufacturing and R&D Campus in Penang, Doubling Production Capacity and Creating 800 High-Tech Jobs,” InvestPenang, investpenang.gov.my Early engineering involvement matters because providers that enter the program at prototype stage are in a stronger position to hold later production volumes once the product moves into scale. The Malaysia electronics manufacturing services industry is therefore rewarding service breadth more than pure assembly depth, especially where incentive eligibility now favors local sourcing and stronger domestic linkages.

By Business Model: Contract Manufacturing Still Dominates While Hybrid And Turnkey Grow Faster

Contract Manufacturing accounted for 60.91% of the Malaysia electronics manufacturing services market size in 2025 because global OEMs in consumer electronics, communications, and industrial equipment still rely on long-established outsourcing models with major Penang-based operators. Hybrid and Turnkey is forecast to expand at a 10.13% CAGR through 2031 as more North American and European customers ask local providers to handle a greater share of procurement and materials management. This shift reflects the growing difficulty of running independent sourcing teams across Asia-Pacific component markets at a time when lead times, tariffs, and qualification standards all change quickly. Original Design Manufacturing occupies a separate strategic position, with Taiwanese players such as Wistron Corporation and Universal Scientific Industrial Co., Ltd. using Malaysia as a manufacturing base for products linked to their own design assets. For pure-play contract manufacturers, that means standard programs are becoming harder to defend on margin unless they also build purchasing capability and supplier qualification depth.

Mid-tier companies have started to adapt faster than some larger rivals. Cape EMS Bhd's CEB 2.0 roadmap, announced in February 2026, repositioned the company toward engineering-led work, Battery Energy Storage System assembly, and AI-oriented intelligent manufacturing networks across Johor and the United States. That kind of move shows that business model change in the Malaysia electronics manufacturing services industry is no longer limited to global Tier-1 groups. It is also becoming a practical route for Malaysian-listed operators that want more wallet share from the same customer base while reducing exposure to basic build-to-print work.

By Manufacturing Process: SMT Remains Core While Advanced Packaging Gains Speed

Surface Mount Technology held 54.88% of the Malaysia electronics manufacturing services market in 2025, which keeps it as the main production process across consumer electronics, communications, and computer assembly programs. Advanced Packaging and Hybrid Processes is the fastest-growing category with a 10.73% CAGR through 2031, and this part of the Malaysia electronics manufacturing services market size is rising as AI servers, 5G base stations, automotive electronics, and industrial IoT devices carry more complex semiconductor content. Through-Hole Technology still matters in industrial, medical, and aerospace applications where mechanical strength and long product cycles remain important. Even so, new product revisions continue to move toward surface mount and more compact package formats as miniaturization requirements deepen. The investment case for advanced packaging is also supported by a MYR 185.8 million (USD 47.3 million), public-private consortium approved in 2026 to help Malaysia reach a 7% share of the global advanced packaging segment by 2035.

The transition is already visible in operating assets. Chipbond opened its Batu Kawan facility in February 2026 with wafer bumping, wafer-level chip-scale packaging, and flip-chip capability, alongside an initial capacity of 10,000 wafers and 100 million WLCSP units per month. That reduces the distance between OSAT activity and downstream assembly in the Malaysia electronics manufacturing services industry. Providers with only SMT-heavy footprints now face a clearer risk of losing complex programs to competitors that can cover more of the process chain from die-attach to final test and box-build.

By End-User: Consumer Electronics Leads While Automotive Reframes Future Demand

Consumer electronics held 31.46% of the Malaysia electronics manufacturing services market in 2025, supported by the country's existing base in smartphones, tablets, wearables, and related device assembly. Automotive is forecast to grow at a 10.55% CAGR through 2031, and that part of Malaysia electronics manufacturing services market size is being lifted by EV power electronics, ADAS modules, and in-vehicle infotainment assemblies. Industrial, medical, and communications programs sit in the middle of the demand mix and add a useful balance between volume and engineering complexity. Medical device assembly has also benefited from the Penang MedTech corridor, where the presence of firms such as Abbott, Boston Scientific, and Dexcom supports nearby contract manufacturing demand. Computer-related work still matters, but growth is now more closely tied to AI server rack assembly than to traditional client devices facing mature demand patterns.

Automotive growth is being reinforced by new supplier investment. Trensor Electronics broke ground in May 2025 on a MYR 100 million (USD 22.62 million) factory in Penang for automotive pressure sensors and targeted mass production before the second quarter of 2026 for customers including Ford and Geely.[2]Trensor Co., Ltd., “Trensor Breaks Ground on First Factory in Malaysia,” PR Newswire, prnewswire.com Entry barriers are higher here because IATF 16949 quality management compliance is effectively required for serious automotive programs. That gives certified operators in the Malaysia electronics manufacturing services market some protection on margin even as competition intensifies in other end-user categories

Geography Analysis

Penang remains the center of the Malaysia electronics manufacturing services market, and its weight is visible in both investment flow and capability density. Approved manufacturing investments in Penang reached MYR 22.4 billion (USD 5.07 billion) in 2025, and foreign capital made up 68% of that total, which confirms that the state remains the main landing point for new electronics programs. Penang also contributes more than half of Malaysia's total electrical and electronics exports, which gives it the strongest operating base in the national manufacturing network. The Penang Automation, Test and Equipment Campus was launched in April 2026 on 10 acres of government land valued at MYR 40 million (USD 9.05 million) and is intended to strengthen co-development between multinational electronics players and local equipment suppliers. New projects from Intel, Sustio, Chipbond, Syntiant, Bosch, and AIXTRON show that Penang is no longer serving only final assembly, because it is adding advanced packaging, test, process equipment, and automotive-grade back-end work into one cluster.

Johor is the second major pillar in the Malaysia electronics manufacturing services market and is developing a different role from Penang. Its advantage comes from Singapore's proximity, data-center adjacency, and a growing base for interconnect, box-build, and specialty assembly rather than a copy of Penang's semiconductor-heavy model. Cape EMS established GrandCape in Senai through a joint venture with New Grand Tech in April 2026 to produce flexible flat cable and advanced interconnect products for AI data centers, EV systems, and Battery Energy Storage Systems. SP Manufacturing had already opened a Senai facility in late 2024 to serve automotive, aerospace, medical device, and industrial machinery customers, which showed that Johor's appeal extends well beyond light consumer assembly.

Beyond Penang and Johor, the rest of the country plays a supporting but important role in the Malaysia electronics manufacturing services market. The Klang Valley is moving toward higher-value digital manufacturing and semiconductor-adjacent functions, helped by the opening of Arm's first ASEAN office in Kuala Lumpur under the March 2026 partnership with Malaysia. Kedah and Perak are acting as overflow and extension zones for Penang, especially where larger footprints and more cost-sensitive PCB or PCBA work are required. This role was reinforced in 2025 when Ichia Technologies opened a MYR 490 million (USD 110.86 million) PCB and PCBA facility in Kulim Hi-Tech Park with IoT-enabled Industry 4.0 production systems. The geographic pattern is therefore tiered, with Penang focused on premium and technology-intensive work, Johor tied to cross-border and data-infrastructure demand, and the northern corridor helping deepen volume capacity and supplier coverage.

Mordor Intelligence examines the electronics manufacturing services market across diverse other regional markets as well, including Europe, Asia, and North America, while also offering granular country-level perspectives for Taiwan, Vietnam, France, United States, South Korea, and Japan and more.

Competitive Landscape

The Malaysia electronics manufacturing services market is moderately fragmented and shows a clear two-tier structure. Global Tier-1 providers such as Flex Ltd., Jabil Inc., Celestica Inc., and Sanmina Corporation compete on program complexity, technology range, and multinational customer ties, while Malaysia-listed mid-tier firms rely more on speed, local relationships, and focused automation decisions. That balance keeps rivalry high because global firms have scale and engineering depth, but domestic names can still move faster in selected niches. Policy design is also starting to favor larger and better-organized players, because the New Incentive Framework links benefits to local content, skilled employment, and supply-chain spillovers that are easier to prove when a company has stronger procurement and compliance teams. Smaller providers therefore face pressure not only from pricing, but also from a higher reporting and capability threshold within the Malaysia electronics manufacturing services market.

Technology spending is widening the gap between leaders and followers. Global operators are deploying AI-led predictive maintenance, digital twin environments, and autonomous mobile robot material handling, and AMR deployments in Malaysian electronics facilities have achieved utilization rates above 90%. Intel's advanced packaging buildout in Penang is also raising local performance benchmarks in yield control, assembly precision, and test discipline, which makes it harder for mid-tier firms to enter the most demanding programs without partner support. At the same time, the line between EMS and adjacent semiconductor services is narrowing as advanced packaging, RF assembly, and AI server box-build become more integrated inside the same customer programs. This is one reason the Malaysia electronics manufacturing services market is moving faster toward higher-complexity work than its talent pipeline can comfortably support.

Several company moves show where competition is shifting. Cape EMS has been especially active, first through its February 2026 CEB 2.0 roadmap and then through its March 2026 collaboration with Guardian South East Asia and its April 2026 GrandCape joint venture in Johor, all of which point to a strategy built around engineering integration, interconnects, and infrastructure-linked demand. NationGate has shown how AI server assembly can rapidly reshape revenue exposure, but that same concentration also increases vulnerability when geopolitical scrutiny rises around AI hardware supply chains. VS Industry's multi-country footprint offers a different playbook built on geographic risk spread, while new Chinese EMS entrants in Malaysia are using the country's tariff position to target US-facing business in standard electronics programs. Mi Technovation Berhad is better viewed as an automation and semiconductor back-end equipment supplier to EMS and OSAT players rather than as a direct EMS provider, while Season Group is a more relevant EMS peer because it operates Malaysian SMT, box-build, and precision assembly activities across consumer, EV, and industrial demand areas.

Malaysia Electronics Manufacturing Services Industry Leaders

VS Industry Berhad

Flex Ltd

NationGate Holdings Berhad

Jabil Inc.

Plexus Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bosch opened one of Asia's most advanced semiconductor back-end sites in Penang, representing an investment of EUR 350 million (USD 379 million), focused on final testing of automotive chips and sensors. The 100,000 m² facility is Bosch's first of its kind in Southeast Asia and is expected to employ up to 400 associates by mid-2030, reinforcing Penang's role as a preferred destination for automotive-grade electronics production.

- May 2026: MIDA and AIXTRON SE signed an agreement at SEMICON Southeast Asia 2026 to build a greenfield semiconductor manufacturing facility on 8.5 acres at Bandar Cassia Technology Park in Penang. The plant will manufacture AIXTRON's 100 mm, 150 mm, and 200 mm deposition systems for power electronics, advanced communication, and optoelectronics, providing critical upstream process equipment to EMS and OSAT operators in the Penang cluster.

- April 2026: Intel's advanced packaging complex in Penang, representing a capital commitment of MYR 12 billion (USD 2.71 billion), commenced first-phase operations with a focus on assembly and test for advanced packaging, a program that positions Malaysia as Intel's global assembly and test hub and will set local supplier capability benchmarks.

- March 2026: Malaysia signed a MYR 1.11 billion (USD 250 million) 10-year partnership with Arm Holdings, granting access to Arm's IP and compute subsystems, targeted training for 10,000 IC design engineers, and the opening of Arm's first ASEAN office in Kuala Lumpur. The collaboration aims to build local chip design capability and deepen Malaysia's semiconductor value-chain participation beyond back-end assembly.

Malaysia Electronics Manufacturing Services Market Report Scope

Electronics Manufacturing Services refer to organizations that specialize in designing, manufacturing, testing, distributing, and repairing electronic components and assemblies for Original Equipment Manufacturers (OEMs). By leveraging EMS providers, brands can streamline their operations and allocate greater focus to research, development, and marketing activities.

The Malaysia Electronics Manufacturing Services Market Report is Segmented by Service Types (Electronic Manufacturing Services (PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, and Other Electronics Manufacturing Services), Engineering Services, Test and Development Implementation, Logistics Services, and Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid/Turnkey/Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging/Hybrid Processes), and End-User (Mobile Devices (Smartphones and Tablets), Consumer Electronics, Computer (PCs / Desktops / Laptops), Industrial, Automotive, Communication, Lighting, Medical, and Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs / Desktops / Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-Users |

| By Service Types | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-User | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs / Desktops / Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-Users |

Key Questions Answered in the Report

What is the current size of the Malaysia electronics manufacturing services market?

The Malaysia electronics manufacturing services market stands at USD 5.67 billion in 2026 and is forecast to reach USD 9.01 billion by 2031 at a CAGR of 9.71%, according to the Mordor Intelligence.

Which service segment leads electronics manufacturing services in Malaysia?

PCB Assembly led in 2025 with a 42.73% share, reflecting Malaysia's deep installed base in circuit board production and related assembly work.

Which business model is growing fastest in Malaysia's EMS space?

Hybrid and Turnkey is the fastest-growing model with a 10.13% CAGR through 2031, as OEMs increasingly ask providers to manage sourcing and broader program execution.

Why is Penang so important for electronics production in Malaysia?

Penang remains the main cluster because it draws the largest investment flows, hosts advanced packaging and test capacity, and anchors a dense supplier network that supports higher-value manufacturing.

Which end-user group is creating the strongest future demand?

Automotive is the fastest-growing end-user at a 10.55% CAGR through 2031, supported by EV electronics, ADAS modules, and automotive-grade testing requirements.

What is the main risk that could slow future growth?

The biggest structural risk is the shortage of skilled talent in advanced packaging and complex assembly, which is already raising retention costs and slowing capacity expansion.

Page last updated on: