Malaysia Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

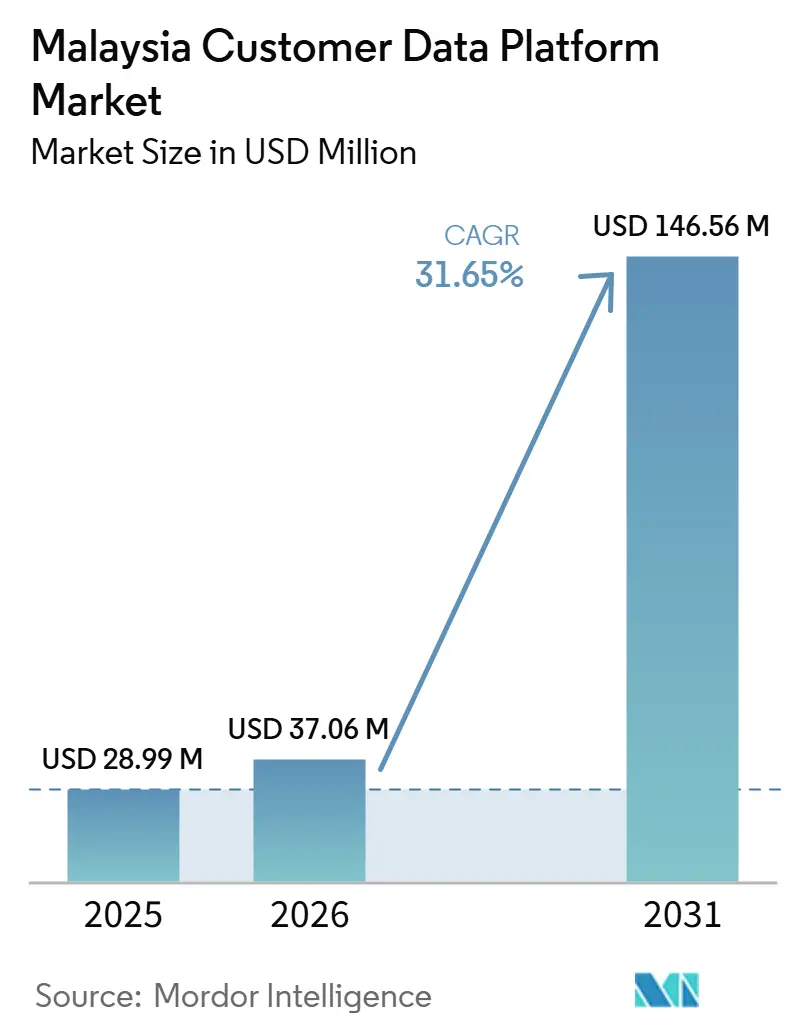

| Base Year Market Size (2025) | USD 28.99 Million |

| Market Size (2026) | USD 37.06 Million |

| Market Size (2031) | USD 146.56 Million |

| Growth Rate (2026 - 2031) | 31.65% CAGR |

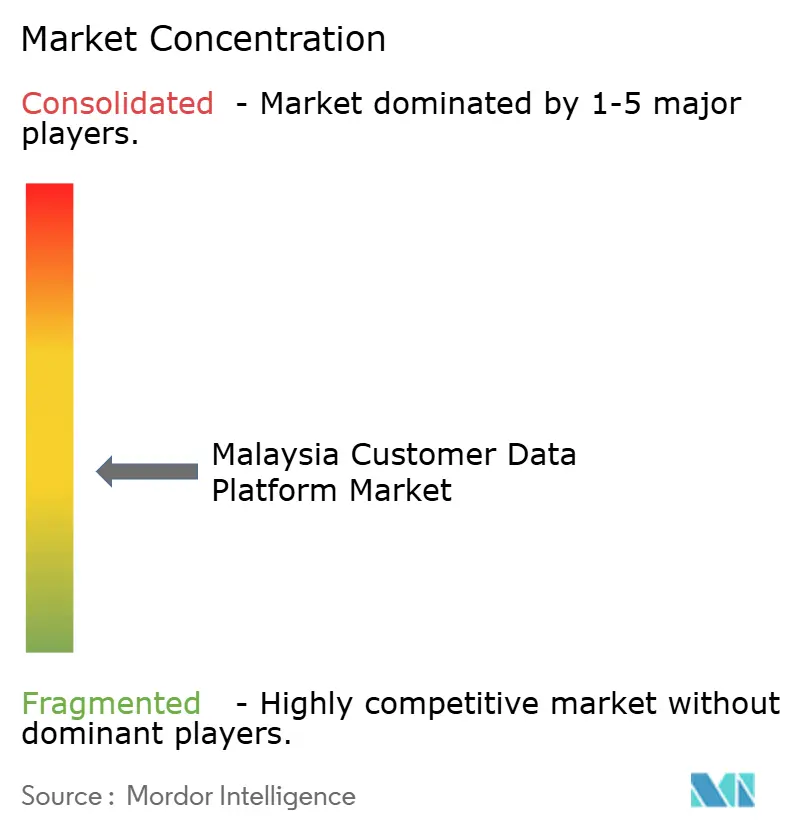

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Customer Data Platform Market Analysis by Mordor Intelligence

The Malaysia customer data platform market size is projected to expand from USD 28.99 million in 2025 and USD 37.06 million in 2026 to USD 146.56 million by 2031, registering a CAGR of 31.65% between 2026 to 2031. The Malaysia customer data platform market is moving forward as enterprises put more weight on first-party data, because customer interactions now sit across digital commerce, loyalty programs, mobile apps, and physical channels. The updated personal data protection framework has also heightened the importance of structured data governance, pushing customer data platform buying decisions beyond marketing teams into technology, compliance, and data leadership functions. The market is also benefiting from stronger cloud readiness, as large infrastructure commitments in Malaysia make local deployment and data residency options more practical for enterprise buyers. Competition remains active around platform breadth, AI-enabled activation, and implementation flexibility, which is shaping a market where vendors need both product depth and local execution strength. At the same time, the Malaysian customer data platform market still faces slower deployment cycles, with legacy systems, limited specialist talent, and cost sensitivity holding back faster adoption.

Key Report Takeaways

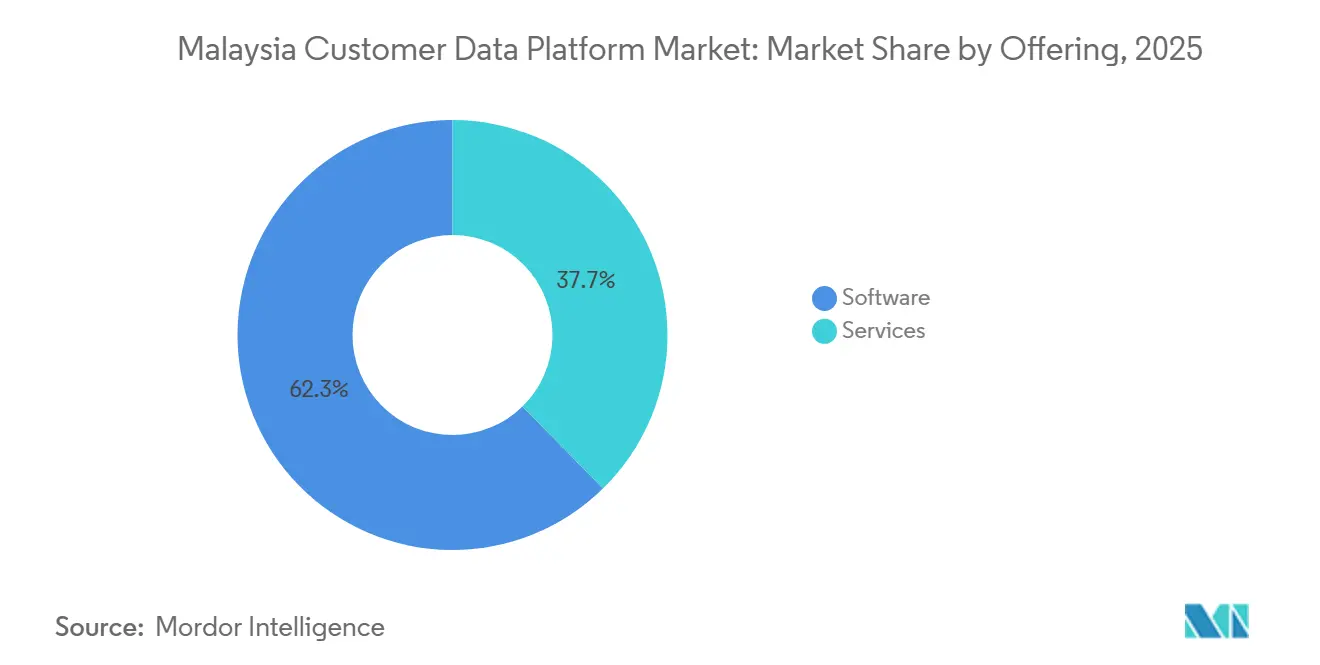

- By offering, software held 62.34% of the Malaysia customer data platform market share in 2025, while services are projected to expand at a 34.81% CAGR through 2031.

- By deployment mode, cloud accounted for 71.28% of the market share in 2025, while hybrid is expected to record the highest CAGR of 36.42% through 2031.

- By organization size, large enterprises accounted for 59.16% of the market in 2025, while SMEs are projected to grow fastest at a 35.73% CAGR through 2031.

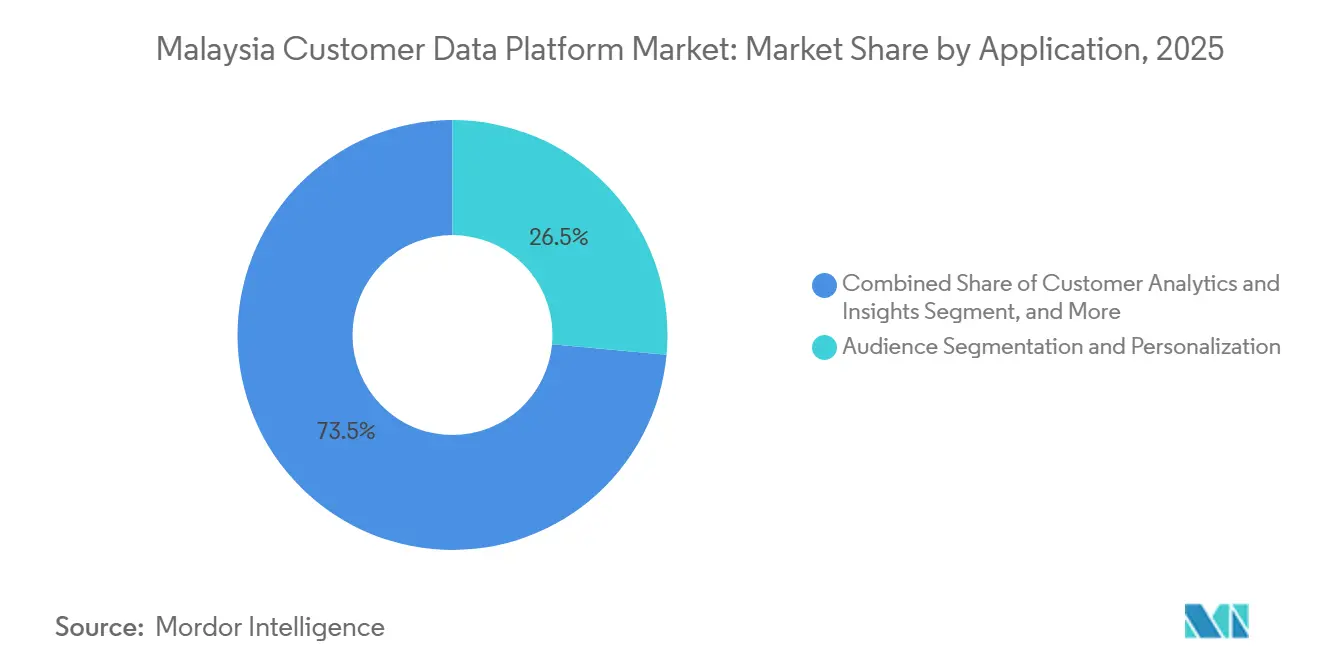

- By application, audience segmentation and personalization captured 26.47% share in 2025, while customer analytics and insights are projected to advance at a 38.19% CAGR through 2031.

- By end-user industry, retail and e-commerce held 28.93% share in 2025, while media and entertainment is expected to expand at a 33.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-Party Data Unification Across Retail and BFSI | +8.2% | National, concentrated in Klang Valley and Penang corridors | Short term (≤ 2 years) |

| Real-Time Personalization in E-Commerce and Super-Apps | +6.8% | National, with early gains in urban centers | Short term (≤ 2 years) |

| Cloud-Hosted Customer Engagement Stack Expansion | +5.4% | National | Medium term (2-4 years) |

| Tighter Privacy Rules and Data Governance | +3.9% | National, with spillover to cross-border ASEAN operations | Short term (≤ 2 years) |

| Composable CDP Adoption for Faster Stack Integration | +2.8% | National, early adoption in enterprise technology clusters | Medium term (2-4 years) |

| Marketing ROI Pressure from Fragmented Omnichannel Journeys | +2.1% | National, strongest in Klang Valley retail and e-commerce hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for First-Party Data Unification Across Retail And BFSI

The Malaysia customer data platform market is gaining from a clear move away from third-party tracking toward first-party customer data programs. Retailers, banks, and insurers now need a single view of customer activity across payments, loyalty, online browsing, and offline transactions to support better targeting and service design. This need is becoming more important in financial services, where the Open Finance direction is building a consent-based data-sharing structure that will require stronger identity, permission, and profile management capabilities. The Open Finance pilot with seven banks and the Employees Provident Fund shows that data sharing in Malaysia is becoming more structured and operational, not just a matter of policy discussion.[1]Conventus Law, “Malaysia - Save The Dates: Personal Data Protection Amendments Now In Operation,” Conventus Law, conventuslaw.com. The result is that customer data platform spending is becoming part of broader enterprise architecture planning, especially in organizations that need both personalization and compliance discipline. In the Malaysia customer data platform market, that shift widens the buyer base and supports demand from business units that did not previously treat CDPs as core infrastructure.

Growth of Real-Time Personalization in E-Commerce and Super-Apps

Rising expectations for real-time customer engagement across digital commerce and platform ecosystems are also lifting the Malaysia customer data platform market. Grab showed how fast activation has become a competitive standard, with its CDP Scenarios capability enabling personalized messages and offers within 15 seconds of a trigger event. That operating model matters in Malaysia because retailers and service providers are competing in an environment where customers shift quickly between apps, marketplaces, payments, and messaging channels. Once that behavior becomes normal, slower campaign logic results in lower response quality and lower conversion value. This is why the Malaysia customer data platform market is moving toward platforms that support live event ingestion, fast audience refresh, and immediate downstream activation. It also explains why customer data platform adoption is spreading from reporting use cases into journey execution and decisioning use cases.

Expansion of Cloud-Hosted Customer Engagement Stacks in Malaysia

The Malaysia customer data platform market is benefiting from a broader cloud infrastructure buildout that makes enterprise deployment easier and more acceptable. Oracle committed more than USD 6.5 billion to open a public cloud region in Malaysia, providing enterprises with stronger local support for data-intensive workloads and data residency requirements.[2]Oracle Corporation, “Oracle Named a Leader in the Gartner Magic Quadrant for Customer Data Platforms,” Oracle, oracle.com. Tealium also expanded on the AWS Singapore Region in March 2026, with a direct focus on trusted, AI-ready data and support for ASEAN data governance expectations. This cloud foundation matters because many Malaysian buyers want lower deployment friction, faster time to use, and fewer infrastructure constraints than on-premises models can offer. The Malaysia customer data platform market is therefore seeing cloud remain dominant, while hybrid options are gaining more attention in regulated sectors. Government support for SME digitalization is also helping to expand the future buyer pool by making more businesses more comfortable with software-led operating models.[3]New Straits Times, “Nearly 39,000 SMEs Adopt Digitalisation Through GDPM Scheme,” New Straits Times, nst.com.my.

Tightening Privacy Expectations Under Malaysia's Data Governance Environment

The Malaysia customer data platform market is being pushed by a more demanding privacy and compliance environment. Malaysia's Personal Data Protection framework underwent a major update between January 2025 and June 2025, introducing breach notification, mandatory DPO appointments, data portability, and a risk-based approach to cross-border transfers. Those changes make structured consent, identity governance, and customer record management much harder to handle through disconnected systems. That is especially relevant for sectors such as BFSI, healthcare, and retail, where customer data flows are broad, and response obligations are more serious. Malaysia Digital 2030 aligns with this direction by treating data as a strategic national asset and establishing a National Data Commission, thereby elevating the policy importance of enterprise-grade data handling. In the Malaysia customer data platform market, this means compliance capability is increasingly part of the product value proposition, not an optional add-on around the core platform.[4]Bernama, “MyDIGITAL, Oracle to Train 300,000 Malaysians in AI Skills by 2029,” Bernama, bernama.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy CRM, ERP, and Analytics Systems | -4.3% | National, pronounced in BFSI, manufacturing, and government sectors | Long term (≥ 4 years) |

| Shortage Of CDP Implementation Skills and Data Engineering Talent | -3.2% | National, most acute in Klang Valley and Penang | Medium term (2-4 years) |

| Budget Sensitivity Among SMEs and Mid-Market Buyers | -2.1% | National, pronounced outside major urban centers | Medium term (2-4 years) |

| Data Quality Gaps Across Disconnected Customer Touchpoints | -1.5% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy CRM, ERP, and Analytics Systems

The Malaysian customer data platform market continues to face delays, with buyers still running fragmented core systems. Banks often operate on older payment and banking architectures, while retailers and manufacturers still rely on a mix of local ERP tools, customized point-of-sale systems, and disconnected CRM platforms. That makes real-time profile unification harder because schema mapping, middleware work, and ongoing reconciliation all add time and cost before a CDP can deliver value. CIMB Bank's 2025 decision to modernize payment processing with ACI Worldwide shows the scale of upstream system work that many large organizations still need to complete. When a customer data platform arrives before those foundations are aligned, data quality and identity resolution can disappoint business teams. In the Malaysia customer data platform market, this mismatch keeps some projects moving more slowly even when the strategic case for investment is already clear.

Shortage of CDP Implementation Skills and Data Engineering Talent

The availability of skilled implementation talent also limits the Malaysia customer data platform market. Malaysia attracted more than RM 250 billion in approved digital investments between 2024 and 2026, which boosted demand for data engineers, integration architects, and platform specialists across many technology areas. Oracle and MyDIGITAL launched a skills initiative to train 300,000 Malaysians in AI skills by 2029, but that program will take time to expand the near-term delivery base for CDP projects. CDP deployment requires a specific mix of streaming, identity, orchestration, and governance capabilities, and that mix remains limited in the local labor pool. Buyers who lack those skills often depend more heavily on vendors and service partners for configuration, maintenance, and change management. In the Malaysian customer data platform market, vendors with pre-built connectors, managed services, and lower-complexity deployment models are therefore in a stronger position with mid-market customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads While Services Build Momentum

Software held 62.34% of the market in 2025, indicating that Malaysian buyers initially focused on securing a usable platform layer for collection, identity stitching, profile management, and activation. In the Malaysia customer data platform market, that buying pattern reflects a practical sequence, because enterprises usually purchase the platform core before they expand spending on customization and managed support. Large organizations in retail, BFSI, telecommunications, and digital services have been the main software buyers, as they already operate broader customer engagement stacks and can place CDP licensing into existing procurement cycles. Software demand is also supported by the need to centralize customer records as businesses handle more interactions across apps, e-commerce, service portals, and loyalty systems. The result is a market structure where platform ownership remains the first spending priority before deeper transformation work begins.

That lead in software does not reduce the importance of services, because services are projected to grow at a 34.81% CAGR through 2031. Malaysian buyers often need outside support for integration design, data mapping, consent workflows, dashboard configuration, and user training, especially when internal teams are still building platform skills. Tealium's March 2026 launch on the AWS Singapore Region shows how vendors are expanding their delivery readiness for ASEAN buyers that need both technology and implementation support. The services opportunity grows further when organizations move from basic activation into predictive analytics, composable architecture, and broader orchestration across teams. This means the Malaysia customer data platform market is likely to keep software as its revenue base, while services become more important as deployments mature and use cases expand.

By Deployment Mode: Cloud Remains The Core While Hybrid Gains Ground

Cloud accounted for 71.28% share in 2025, which confirms that the Malaysia customer data platform market already aligns closely with cloud-first technology adoption. Cloud deployment is attractive because it reduces infrastructure burden, shortens setup time, and aligns with the subscription model that many enterprises and growing digital businesses now prefer. It also gives vendors a cleaner path to roll out platform updates, AI features, and connector support without long customer-side upgrade cycles. In many commercial settings, speed matters more than the control advantages of fully on-premises systems. The cloud lead, therefore, reflects both technical convenience and a broader shift in how Malaysian businesses now consume enterprise software.

Hybrid is projected to expand at a 36.42% CAGR through 2031, which makes it the fastest-growing deployment type. This growth is strongest in regulated environments where businesses want to retain tighter control over sensitive profile data while still using cloud infrastructure for analytics and activation. Oracle's planned local cloud region adds to that shift by making local hosting and data-residency arguments easier for enterprise buyers to address. The legal changes under Malaysia's updated privacy framework also support hybrid interests, as organizations need greater confidence in how data is stored, governed, and transferred across systems. For the Malaysia customer data platform market, that means cloud remains the default model, while hybrid becomes the preferred path for buyers balancing activation needs with stronger governance and residency expectations.

By Organization Size: Large Enterprises Hold Revenue Leadership While SMEs Scale Faster

Large enterprises represented 59.16% share in 2025, showing that the Malaysia customer data platform market still relies heavily on big-ticket deployments from banks, telecom groups, retailers, and large digital platforms. These organizations have broader customer data volumes, more channel complexity, and stronger budgets for multi-source ingestion, identity resolution, and AI-enabled segmentation. They also tend to work through longer procurement cycles, which supports larger contract values and more formal implementation programs. In many cases, the CDP sits inside a wider transformation agenda that includes customer experience, analytics modernization, and compliance readiness. That is why large enterprises remain the revenue anchor, even as adoption widens.

SMEs are projected to grow at a 35.73% CAGR through 2031, suggesting a strong expansion path from a smaller base. The Malaysia customer data platform market is opening to smaller businesses because digital tools have become easier to access through SaaS pricing, simpler interfaces, and a wider set of packaged integrations. MDEC reported that nearly 39,000 SMEs had adopted digital solutions through the Geran Digital PMKS Madani scheme by August 2025, demonstrating how public support is broadening technology readiness across the business base. Alibaba Cloud and MDEC also launched an SME Digitalization Program in December 2025 to build awareness, skills, adoption, and innovation capacity among Malaysian SMEs. In the Malaysia customer data platform market, this segment is growing faster because even smaller retailers and service firms now create enough multi-touchpoint data to justify profile unification and targeted engagement.

By Application: Personalization Stays Largest While Analytics Pulls Ahead

Audience segmentation and personalization accounted for 26.47% of the market share in 2025, making it the largest application area in the Malaysia customer data platform market. That lead is logical because segmentation and personalization are the most visible and fastest-to-prove uses for customer data platforms in consumer-facing organizations. Marketers can connect app behavior, campaign response, purchase history, and loyalty activity into practical audience groups without waiting for a full enterprise data overhaul. This also helps explain why CDP adoption initially gained traction in functions tied directly to conversion, retention, and campaign efficiency. In that sense, segmentation remains the main doorway through which many Malaysian organizations enter the category.

Customer analytics and insights are projected to grow at a 38.19% CAGR through 2031, which signals that buyers are moving toward more advanced decision support and predictive use cases. This part of the Malaysia customer data platform market size is being supported by demand for churn prediction, lifetime value scoring, next-best-action logic, and faster learning from cross-channel behavior. CelcomDigi's early 2026 campaign through Astro Media Solutions generated 1.3 million targeted impressions and a 96% video completion rate, demonstrating how first-party audience intelligence is moving closer to driving revenue outcomes. At the same time, consent and preference management have become more important under the updated privacy framework, which keeps compliance-linked applications relevant across sectors. The Malaysia customer data platform market is therefore shifting from static audience building toward a broader analytics role that can guide engagement, risk decisions, and customer lifecycle actions.

By End-User Industry: Retail And E-Commerce Sets The Pace While Media Expands Fastest

Retail and e-commerce accounted for 28.93% of the Malaysia customer data platform market in 2025, making it the clearest demand center. These businesses operate under constant pressure to improve personalization, raise repeat purchase rates, reduce acquisition cost, and coordinate activity across online stores, marketplaces, apps, and physical outlets. Because their transaction and engagement data is broad and frequent, they often feel the value of profile unification earlier than other sectors. The retail and e-commerce lead also reflects the role of loyalty programs, digital payments, and promotional intensity in Malaysia's consumer economy. In practical terms, that makes retail a strong reference point for how the Malaysia customer data platform market continues to develop.

Media and entertainment is projected to grow at a 33.56% CAGR through 2031, which reflects the increasing value of subscriber-level behavior data in streaming and digital advertising. Astro said in 2026 that Sooka's VIP subscriber base grew 29% year over year, and streaming minutes rose 48%, showing why audience intelligence has become more important for monetization and retention. ThinkAnalytics also said Astro selected ThinkMediaAI to support personalized content discovery and engagement on Sooka. The Star reported in April 2026 that iQIYI expanded its local content investment as C-drama popularity rose in Malaysia, suggesting a more competitive content environment and stronger pressure to closely understand viewer behavior. For the Malaysia customer data platform market, this means media companies are becoming more active buyers as they connect viewing data, advertising outcomes, and subscription retention into a single customer view.

Geography Analysis

The national backdrop is supportive because Malaysia Digital 2030 set a target for the digital economy to contribute 30% of GDP by 2030 and established a National Data Commission, which raises the strategic role of data across public and private organizations. Malaysia also attracted more than RM 250 billion in approved digital investments between 2024 and 2026, indicating a broader buildout of technology capacity to support enterprise software adoption. That policy and investment combination supports the Malaysia customer data platform market because it normalizes spending on systems that improve governance, interoperability, and customer intelligence. It also gives vendors a stronger case for positioning CDPs as operational infrastructure rather than campaign software.

Within the country, adoption remains most concentrated in the Klang Valley, where large enterprises, financial institutions, digital commerce operations, and regional business offices are clustered. Penang forms another important pocket of opportunity because its manufacturing and technology base creates demand for structured customer and partner data management in more complex operating environments. East Malaysia, including Sabah and Sarawak, still has a smaller installed base, but the future pipeline is meaningful as digitalization programs reach more businesses beyond the main peninsular hubs. The Open Finance pilot, led by PayNet and involving seven banks, plus the Employees Provident Fund, will likely deepen the role of consent-based customer data architecture within the financial system. Updated cross-border data transfer guidance and broader PDPA changes also make locally governed deployment models more relevant for enterprises operating across ASEAN.

The Malaysia customer data platform market share of demand is still largely shaped by enterprise activity in retail, BFSI, and digital media, as those sectors generate dense, recurring customer interactions. Oracle's local cloud region investment improves Malaysia's position as a stronger home base for data-sensitive enterprise workloads. Consumer-facing platform activity also matters, and Grab said in April 2026 that it unveiled 13 AI-powered experiences at GrabX 2026, while Malaysia remained a significant geography in its regional operations. Streaming growth adds another layer, because Astro and iQIYI both showed stronger local content and engagement momentum during 2026.

Competitive Landscape

The Malaysia customer data platform market is moderately fragmented overall, but enterprise demand is centered on a relatively small set of global vendors with broader product ecosystems. These vendors compete on data unification, AI support, connector depth, orchestration capability, and the ability to address local or regional governance requirements. In this environment, product quality alone is not enough, because buyers also look for implementation support and a credible regional delivery setup. That is why global providers with cloud scale and partner networks continue to hold an advantage in large accounts. At the same time, the Malaysia customer data platform market still leaves room for smaller regional players in mid-market deployments that need faster rollout and better local channel alignment.

Oracle strengthened its position in April 2026 when it was named a Leader in the Gartner Magic Quadrant for Customer Data Platforms, and it linked that standing to its ability to unify customer, account, and business data from broader enterprise systems. Salesforce also remained commercially visible in Malaysia, and Vetece Holdings secured a RM 39.63 million contract in April 2026 to provide Salesforce cloud software to a leading Malaysian utility company over FY2026 to FY2029. Tealium's March 2026 launch on the AWS Singapore Region was another strategic move because it directly addressed regional data governance and low-latency deployment needs for ASEAN customers. These steps show that leading vendors are using infrastructure access, enterprise integration, and governance readiness as competitive levers. In the Malaysia customer data platform market, those levers matter most in large accounts where platform choices become part of a wider digital transformation program.

The mid-market competitive space is more open because implementation complexity and total ownership cost can still limit the appeal of global full-stack platforms. Antsomi showed this in March 2025 when Star Media Group selected Antsomi CDP 365 to support its first-party data strategy across web, app, and offline channels. Regional players can benefit from providing built-in support for Southeast Asian channels, faster onboarding, and closer local guidance. Composable approaches are also becoming more relevant as some organizations separate the data layer from the activation layer and rely on broader cloud foundations. That keeps the Malaysia customer data platform market competitive, because buyers can now choose between integrated suites, regional specialists, and modular architectures based on their internal maturity and use-case priority.

Malaysia Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Twilio Inc.

Tealium, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Prime Minister Anwar Ibrahim launched the Malaysia Digital 2030 (MD2030) national action plan, establishing the National Data Commission and targeting a 30% digital economy GDP contribution and 500,000 high-value digital jobs by 2030. The plan designates data as a strategic national asset and is expected to drive enterprise-grade data management investment across all sectors, directly expanding the CDP addressable market.

- June 2026: Maybank unveiled the next-generation Maybank2E (M2E) platform, an integrated business banking solution that processed approximately MYR 3 trillion (USD 736.94 billion) in transaction value across 122 million transactions in Malaysia in 2025, as part of its ROAR30 commitment of MYR 10 billion (USD 2.46 billion) over five years in technology, data, and AI. The platform's unified customer data layer creates a structural demand signal for BFSI CDP deployments seeking to activate transaction data for personalized financial services.

- April 2026: Grab unveiled 13 AI-powered experiences at GrabX 2026, including cash loans underwritten by first-party Grab data and a Virtual Store Manager pilot in Malaysia, deepening real-time customer data utilization across financial services, mobility, and food delivery. Malaysia accounts for approximately 30.83% of Grab's geographic revenue, making these data-driven product expansions directly relevant to the Malaysia customer data platform market.

- April 2026: Oracle and MyDIGITAL Corporation launched the Oracle Skills Development Initiative (SDI) to train 300,000 Malaysians in AI skills including Oracle Cloud Infrastructure, OCI Generative AI, and OCI Data Science by 2029. The program targets the talent gap that currently constrains CDP implementation velocity in Malaysia.

Malaysia Customer Data Platform Market Report Scope

The Malaysia customer data platform market refers to the ecosystem of software and associated services that enable organizations in Malaysia to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of large, small, and medium enterprises across sectors such as retail, BFSI, healthcare, and IT. By integrating consent and preference management capabilities, CDPs help Malaysian businesses comply with evolving local data protection regulations (such as the PDPA) while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The Malaysia Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Malaysia customer data platform market size in 2026 and where is it headed by 2031?

The Malaysia customer data platform market stands at USD 37.06 million in 2026 and is forecast to reach USD 146.56 million by 2031 at a 31.65% CAGR.

Which deployment model leads customer data platform adoption in Malaysia?

Cloud leads with 71.28% share in 2025, supported by faster implementation, SaaS delivery, and stronger local cloud infrastructure options.

Which application area is growing fastest in Malaysia customer data platforms?

Customer analytics and insights is the fastest-growing application, with a projected 38.19% CAGR through 2031 as buyers move toward predictive and decision-driven use cases.

Which end-user segment generates the most demand in Malaysia?

Retail and e-commerce leads with 28.93% share in 2025 because it relies heavily on personalization, loyalty data, and cross-channel engagement.

Why are privacy rules becoming important for CDP adoption in Malaysia?

The updated PDPA framework added mandatory DPO appointments, breach notification, data portability, and stronger cross-border transfer discipline, which raises the value of structured customer data systems.

What is pushing SME adoption of customer data platforms in Malaysia?

SMEs are projected to grow at a 35.73% CAGR through 2031, helped by digitalization grants, SaaS delivery models, and the rising need to unify customer data from multiple digital touchpoints.

Page last updated on: