Magnesium Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

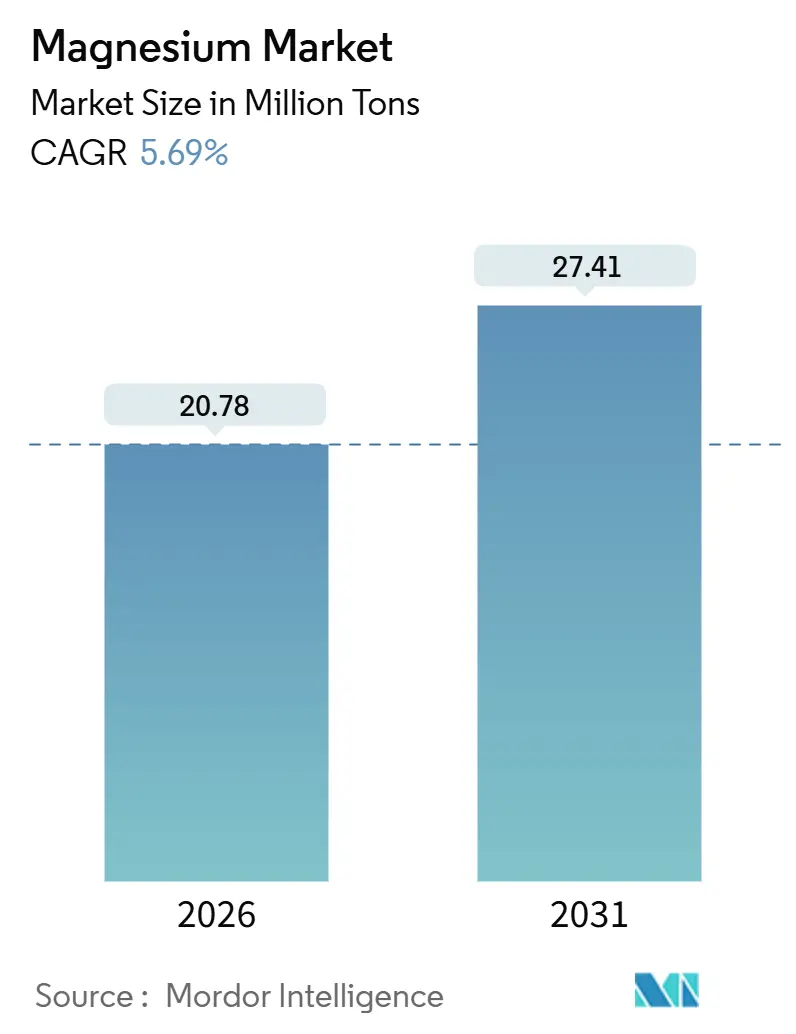

| Market Volume (2026) | 20.78 Million tons |

| Market Volume (2031) | 27.41 Million tons |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnesium Market Analysis by Mordor Intelligence

The Magnesium Market size is estimated at 20.78 million tons in 2026, and is expected to reach 27.41 million tons by 2031, at a CAGR of 5.69% during the forecast period (2026-2031). Rising electric-vehicle lightweighting needs, sustained MgO refractory demand in new steel furnaces, and government critical-mineral policies are combining to redirect trade flows, tighten regional balances, and raise average realized prices. Automakers in the European Union, the United States, and China are front-loading magnesium alloy procurement to meet 2035 internal-combustion-engine phase-out mandates, while India’s push toward increasing crude steel capacity by 2030 is bolstering short-cycle MgO volumes. Elevated spot premiums on non-Chinese ingots illustrate how VAT-rebate removal and tighter export licensing are fragmenting supply, prompting U.S. buyers to lean on Turkey, Israel, and Brazil for primary metal. At the same time, scrap recycling projects in China, North America, and the European Union are moderating supply-risk perceptions and opening a secondary pathway that may absorb incremental consumption through 2031.

Key Report Takeaways

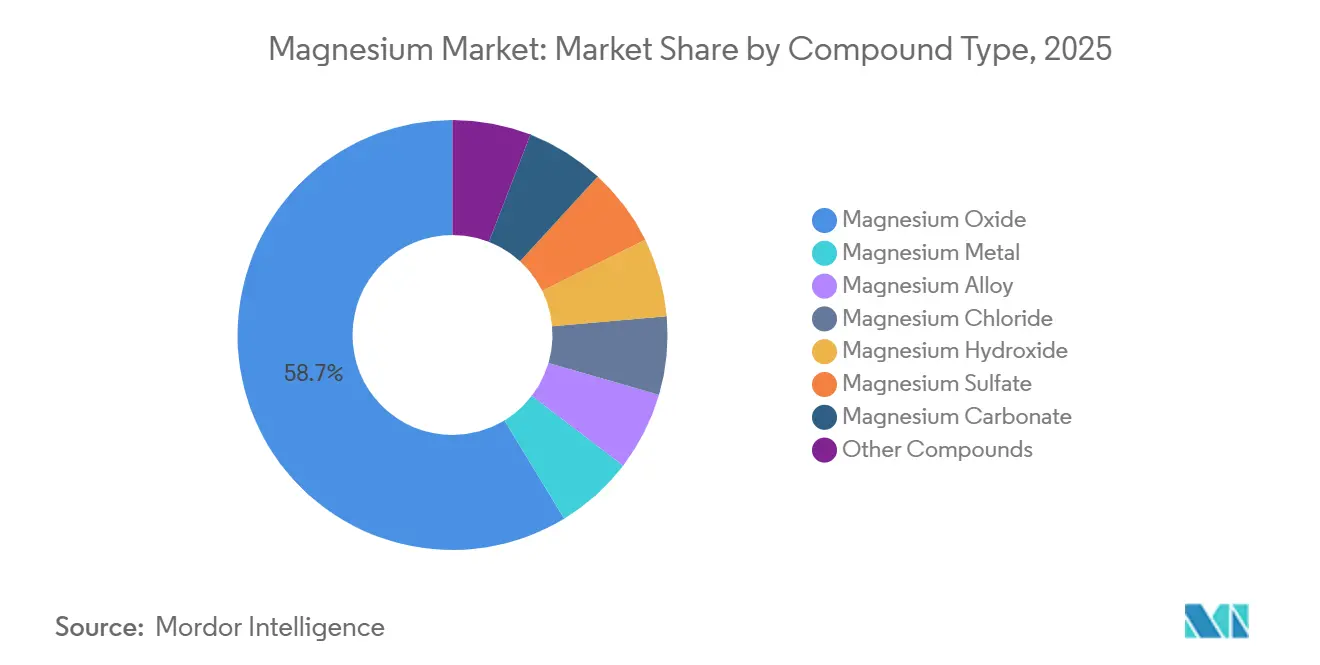

- By compound type, magnesium oxide led with 58.68% of the magnesium market share in 2025. Magnesium alloy is forecast to expand at a 6.22% CAGR through 2031, the fastest among compound types.

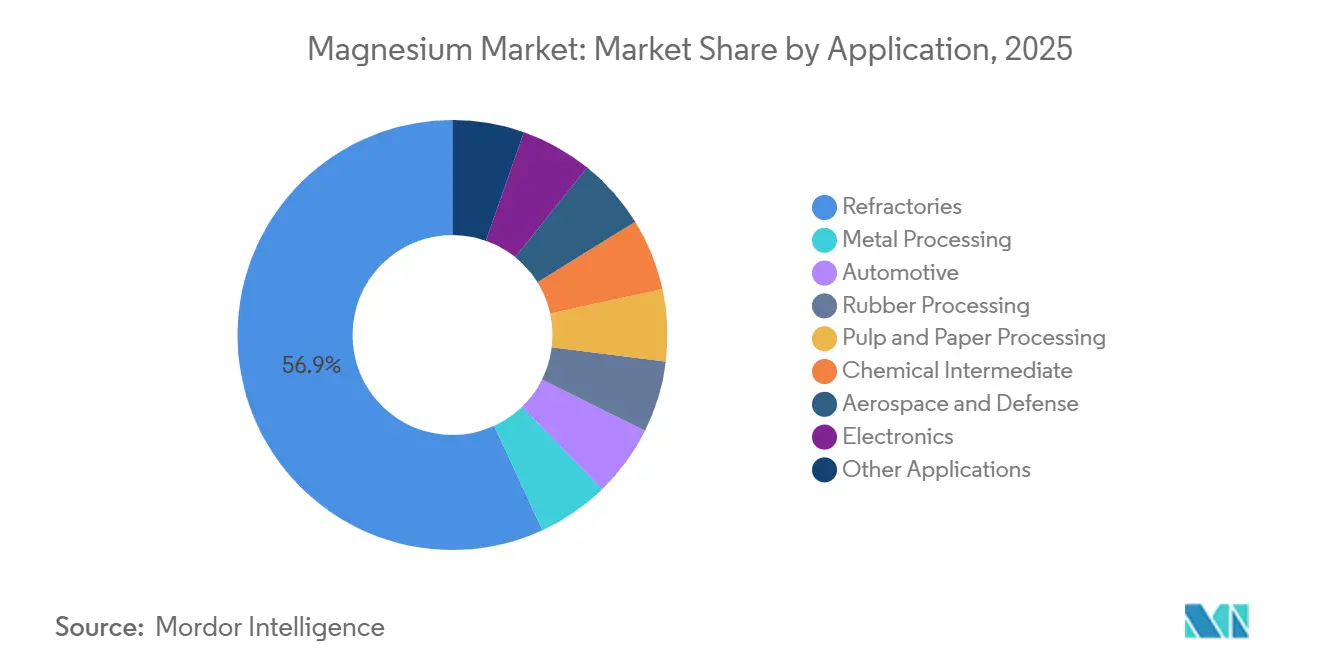

- By application, refractories accounted for 56.85% of the magnesium market size in 2025. Automotive end-uses are advancing at a 6.81% CAGR through 2031, outpacing all other applications.

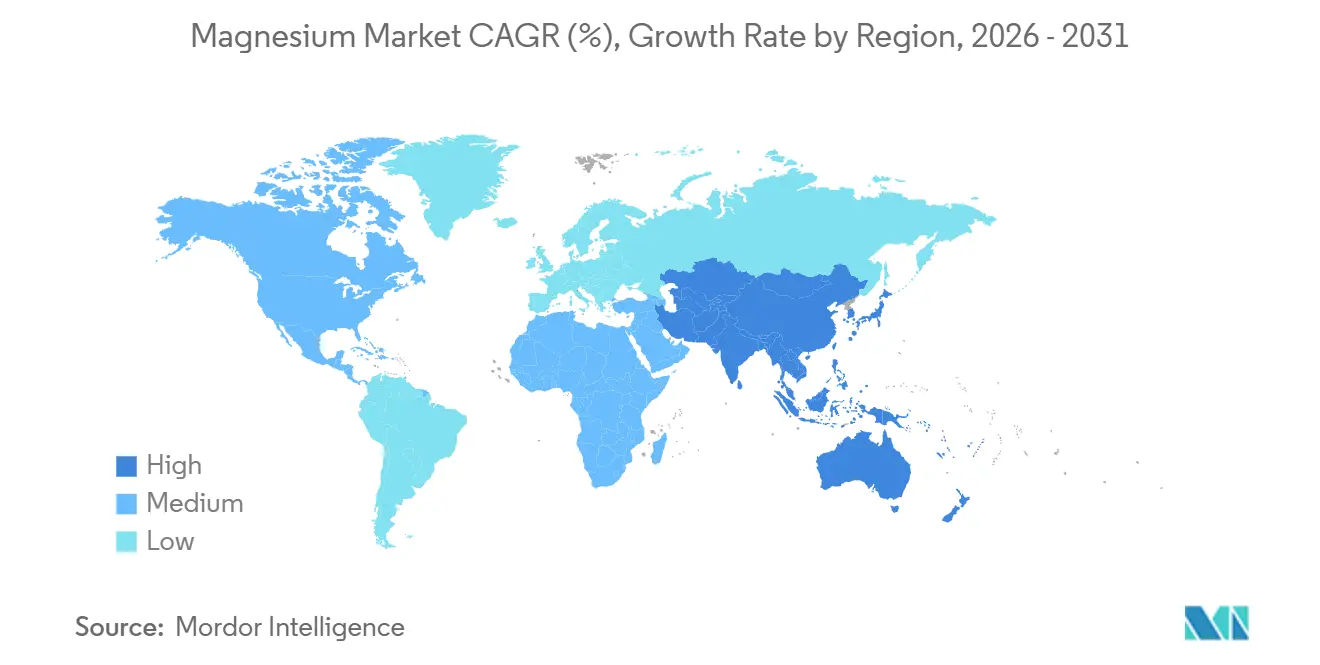

- By geography, the Asia-Pacific captured a 51.48% magnesium market share in 2025. Asia-Pacific also records the fastest regional CAGR at 6.64% through 2031, propelled by China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magnesium Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive and Aerospace Lightweighting Push | +1.2% | Global, with early gains in EU, North America, and China NEV hubs | Medium term (2–4 years) |

| Rising Use of MgO Refractories in Expanding Steel Capacities (APAC Focus) | +1.8% | APAC core (China, India, Vietnam), spill-over to Middle East | Short term (≤2 years) |

| Government Critical-Mineral Initiatives and On-shoring Incentives | +0.9% | North America, EU, selective APAC (Japan, South Korea) | Long term (≥4 years) |

| Magnesium Recycling Scale-up Projects Reduce Supply-Risk | +0.7% | Global, with North America and EU leading regulatory frameworks | Medium term (2–4 years) |

| Breakthrough Research and Development in Magnesium-Air Batteries and Hydrogen Storage | +0.5% | Global, with research and development concentrated in Japan, EU, and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Automotive And Aerospace Lightweighting Push

To counterbalance the mass increase from lithium-ion packs in electric vehicles, automotive OEMs are now using magnesium alloys in battery enclosures, seat frames, and transmission housings. Demonstrations funded by the U.S. Department of Energy have successfully reduced vehicle body weight compared to aluminum-centric designs, bolstering the push for commercialization by 2027. While aerospace demand for magnesium alloys is limited, it commands a premium; the WE43 alloy, meeting SAE standards, is being utilized in aircraft seat structures. Its density of 1.8 g/cm³ offers a direct advantage in payload capacity. Innovations in coatings, like plasma-electrolytic oxidation and metal-organic framework treatments, are extending the lifespan of components and addressing past corrosion issues. These developments are not only speeding up the adoption of magnesium alloys but also enhancing the leverage of vertically integrated die-casters. These die-casters are now positioned to provide large, near-net-shape castings, catering to the evolving demands of next-generation mobility platforms.

Rising Use Of MgO Refractories In Expanding Steel Capacities

India's National Steel Policy targets a steel capacity of 300 million tons by 2030. Each additional ton of steel requires MgO refractories, crucial for ladles and tundishes. Meanwhile, Vietnam's integrated mills are set to boost their hot-rolled-coil capacity between 2024 and 2026, increasing the region's MgO demand annually. In China, as the industry shifts from blast furnaces to electric-arc furnaces, the demand for refractories per ton of steel rises, even though the overall crude output remains steady. With a melting point of 2,852 °C, MgO faces minimal substitution risks, ensuring consistent volume visibility, even amidst concerns over the CO₂ intensity of the Pidgeon route. These factors contribute to a robust demand for MgO, accounting for a significant portion of the global compound volume.

Government Critical-Mineral Initiatives and On-Shoring Incentives

In 2024, the U.S. Defense Production Act Title III greenlit loan guarantees for domestic magnesium initiatives. Europe's Critical Raw Materials Act, aiming for self-sufficiency by 2030, has catalyzed feasibility studies for electrolytic plants in Norway and Iceland, both harnessing low-carbon hydropower. China's 2023 export-control regulations, mandating end-use disclosure, have lengthened shipment lead times and driven up spot premiums for Western purchasers. Meanwhile, Japan's recycling incentive aims to bolster circular capacity, targeting domestic recovery by 2028. These emerging regional blocs, while elevating transaction costs, also mitigate supply risks for key sectors like defense, aerospace, and advanced mobility.

Magnesium Recycling Scale-Up Projects Reduce Supply-Risk

As cars from the 2010–2015 model years, rich in magnesium, reach the end of their life cycle, the availability of scrap from these vehicles is on the rise. This uptick has propelled collection rates in the EU and the U.S. for die-cast parts. In a strategic move to sidestep anti-dumping duties on primary ingots, Chinese scrap exports significantly increased year-on-year. These exports, sold at a discount, found their way to North American secondary smelters. Magontec’s facility in Xi’an processes automotive scrap annually, achieving an impressive reduction in CO₂ emissions compared to using virgin metal. Economic indicators suggest that recycling becomes advantageous whenever spot prices are higher. While coating contamination currently limits the recycled content in structural castings, the rising demands for ISO 14001 certification and traceability are solidifying secondary pathways as integral to the supply chain.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material and Energy-Cost Volatility in Pidgeon and Electrolytic Routes | -0.8% | Global, with acute exposure in China (Pidgeon-dominant) and potential electrolytic hubs (Norway, Iceland) | Short term (≤2 years) |

| Corrosion/Flammability Concerns Limiting OEM Specifications | -0.6% | Global, with North America and EU OEMs most risk-averse | Medium term (2–4 years) |

| ESG-Driven Capital Flight from Carbon-Intensive Pidgeon Process | -0.5% | China, with spill-over to any Pidgeon-route producers globally | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Raw-Material And Energy-Cost Volatility In Pidgeon And Electrolytic Routes

In 2024-2025, the Pidgeon process, which requires coal and ferrosilicon to produce magnesium, faced squeezed producer margins due to coal prices fluctuating. For electrolytic output, which demands significant energy per ton, feasibility efforts in Norway hit a snag when power quotes surged, surpassing the breakeven point. By late 2025, cash costs increased, driven by dolomite feedstock inflation and power rationing in Inner Mongolia. The lack of hedging instruments exposes market participants to spot volatility, hindering long-cycle investments and complicating off-take negotiations.

Corrosion/Flammability Concerns Limiting OEM Specifications

Magnesium's electrochemical potential of -2.37 V makes it susceptible to galvanic corrosion, especially when placed alongside steel or aluminum[1]Society of Automotive Engineers, “SAE ARP6256—Aircraft Seat Applications,” sae.org . As a result, OEMs are compelled to apply insulating gaskets and coatings, which inflate system costs. Field audits on seat frames for the 2024 model year, after exposure to salt during winter, uncovered localized pitting. This discovery has led some automakers to reconsider aluminum alternatives, sacrificing weight savings in the process. The flammability of magnesium during machining necessitates increased capital for specialized ventilation and fire-suppression systems. Furthermore, European automakers now mandate proof of ISO 16220 compliance, extending supplier-qualification cycles. Consequently, this cost-risk assessment has hindered deeper penetration into the mass-market vehicle segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compound Type: MgO Anchors, Alloy Accelerates

Magnesium oxide commanded 58.68% of global compound volume in 2025, largely due to its pivotal role in lining electric-arc and basic-oxygen furnaces with MgO-carbon and MgO-spinel refractories, especially in Asia's burgeoning steel mills. India is ramping up its crude-steel capacity, poised to consume additional tons of MgO annually. Meanwhile, Vietnam's expanding mills are set to contribute to another demand for MgO by 2026. As regional construction booms, the magnesium market, particularly for oxide applications, is on a steady rise. However, the market share for magnesium alloys is outpacing this growth, driven by the push for lightweight materials in electrified vehicles. Notably, China's alloy exports increased during 2025, underscoring the heightened demand for battery housings and wheels[2]Foundry.com.cn, “2025年1-11月中国共出口各类镁产品40.88万吨,” foundry.com.cn .

Magnesium alloy, forecast at a 6.22% CAGR through 2031, captures price premiums that lift average realized revenue per ton. Component manufacturers are reaping the benefits of die-casting advancements, allowing for thinner wall structures and reduced machining steps. While magnesium metal ingots are a crucial feedstock, their direct consumption is declining. Steelmakers are fine-tuning desulfurization recipes, increasingly opting for calcium-silicon blends over traditional ingots. Magnesium chloride, though a minor player in de-icing and tofu coagulation, sees resilient demand in North America, thanks to weather-driven procurement spikes. The flame-retardant application of magnesium hydroxide in wire and cable insulation is witnessing modest growth, adhering to IEC 60332 and UL 94 compliance standards. Lastly, specialty sulfate and carbonate grades maintain a steady presence in pharmaceutical and agricultural sectors, closely tied to GDP fluctuations.

By Application: Refractories Lead, Automotive Surges

Refractories absorbed 56.85% of the 2025 volume, underscoring the substantial demand for MgO bricks and mixes in ladles, tundishes, and cement kilns. As China's steel output stabilizes, leadership in growth shifts to India, Vietnam, and the Middle East, pushing the global refractory market into steady growth territory. Meanwhile, automotive demand is projected to outperform at a 6.81% CAGR as the magnesium market integrates deeper into electric-vehicle platforms. In a testament to this trend, General Motors, Volkswagen, and BYD inked alloy supply contracts for 2024-2025, guaranteeing die-casters operate at near full capacity until 2027.

While metal processing, particularly steel desulfurization, sees a decline in share, it's largely due to calcium-silicon blends that reduce magnesium dosage rates. Although niche consumption in aerospace and defense remains minimal by tonnage, its premium pricing makes it strategically vital: the WE43 alloy commands a price significantly higher than the commodity AZ91D. In the electronics sector, applications like laptop, smartphone, and drone housings have witnessed notable growth. This surge is attributed to Chinese brands transitioning from plastic to magnesium casings for enhanced thermal performance. Meanwhile, sectors like rubber, pulp and paper, and chemical intermediates provide a consistent, GDP-linked baseline, stabilizing against the cyclical nature of metallurgical end-uses.

Geography Analysis

Asia-Pacific held 51.48% of global volume in 2025 and is tracking a 6.64% CAGR through 2031. This growth is largely driven by China's commanding stake in primary output and India's ambitious steel expansion. In a notable shift, China's cessation of VAT export rebates led to a dip in external shipments from January to November 2025. This was largely offset by a surge in domestic demand for EVs and electronics, which absorbed the additional alloy output. Meanwhile, India's imports of magnesium compounds increased in 2025, catering to the needs of newly established electric-arc furnace lines. On another front, Japan has introduced a recycling subsidy, targeting a significant domestic recovery rate by 2028. Concurrently, Vietnam's steel expansion and Indonesia's nickel-smelting growth are spurring a heightened demand for secondary refractories, propelling ASEAN's compound imports upward.

In 2025, North America accounted for a significant portion of the global tonnage consumption. During Q2 2025, U.S. imports saw a year-on-year uptick, with Turkey, Israel, and Brazil emerging as dominant suppliers, collectively providing the majority of the metal, as U.S. buyers shifted their focus away from Chinese ingots. US Magnesium LLC, with its electrolytic plant, caters to a substantial portion of the domestic demand and enjoys the backing of Defense Production Act guarantees. However, it's worth noting that their cost structure is still higher than China's FOB quotes. In a related development, Ontario's die-casting hub in Canada is bolstering Detroit's EV initiatives, leading to an increase in Canadian alloy imports in 2025. Simultaneously, Mexico is capitalizing on USMCA regulations to expand its Guanajuato-based magnesium casting operations, catering to U.S. OEMs.

Europe, while accounting for a notable share of the global volume in 2025, witnessed a consumption drop in H1 2025, primarily due to production delays among automakers. The EU's Critical Raw Materials Act, mandating specific sourcing, has catalyzed feasibility studies for electrolytic magnesium in Norway and Iceland. Here, the potential of hydropower to sidestep future CBAM levies is a significant draw. Germany's reduced imports hint at a strategic shift towards premium aerospace and defense components. Highlighting the importance of niche markets, both the UK and France have turned to Luxfer MEL Technologies for their high-purity WE43 alloy needs. While South America and the Middle-East and Africa combined account for a smaller share, Brazil's burgeoning export stature and Saudi Arabia's ambitious Red Sea brine project signal a potential shift in supply dynamics, moving away from the traditional Chinese-centric channels.

Competitive Landscape

The magnesium market is moderately consolidated. Technology adoption centers on plasma-electrolytic oxidation coatings and die-casting simulation that trims scrap rates, lowering the total cost of ownership for OEMs. Capital allocation patterns reflect ESG pressures: Norway’s sovereign fund divested high-carbon Pidgeon assets, and European asset managers are channeling funds toward hydropower-based electrolytic projects. Barriers to entry are climbing as ISO 16220 fire-risk, ISO 14001 environmental, and Scope 3 reporting frameworks become standard procurement prerequisites, consolidating share among incumbents able to invest in certification and emissions abatement.

Magnesium Industry Leaders

RHI Magnesita

Shanxi Yinguang Huasheng Magnesium Industry Co., LTD.

Baowu Magnesium Industry Technology Co., Ltd.

Grecian Magnesite

Tongxiang Magnesium (Shanghai) Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Magrathea Metals and Tidal Metals unveiled the United States' greenfield plans to restart domestic primary output after US Magnesium’s Great Salt Lake facility faced permit setbacks.

- July 2025: Martin Marietta Materials closed the acquisition of Premier Magnesia, boosting its position in the United States' natural and synthetic magnesia products.

Global Magnesium Market Report Scope

Magnesium (Mg) is defined as the lightest structural metal, recognized for its silvery-white appearance, high reactivity, and a density two-thirds that of aluminum. It is commonly alloyed with aluminum, zinc, and manganese to improve its strength, castability, and corrosion resistance, making it essential for industrial, automotive, and aerospace applications.

The magnesium market is segmented by compound type, application, and geography. By compound type, the market is segmented into magnesium metal, magnesium alloy, magnesium oxide, magnesium chloride, magnesium hydroxide, magnesium sulfate, magnesium carbonate, and other compounds. By application, the market is segmented into metal processing, automotive, refractories, rubber processing, pulp and paper processing, chemical intermediate, aerospace and defense, electronics, and other applications. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Magnesium Metal |

| Magnesium Alloy |

| Magnesium Oxide |

| Magnesium Chloride |

| Magnesium Hydroxide |

| Magnesium Sulfate |

| Magnesium Carbonate |

| Other Compounds |

| Metal Processing |

| Automotive |

| Refractories |

| Rubber Processing |

| Pulp and Paper Processing |

| Chemical Intermediate |

| Aerospace and Defense |

| Electronics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Compound Type | Magnesium Metal | |

| Magnesium Alloy | ||

| Magnesium Oxide | ||

| Magnesium Chloride | ||

| Magnesium Hydroxide | ||

| Magnesium Sulfate | ||

| Magnesium Carbonate | ||

| Other Compounds | ||

| By Application | Metal Processing | |

| Automotive | ||

| Refractories | ||

| Rubber Processing | ||

| Pulp and Paper Processing | ||

| Chemical Intermediate | ||

| Aerospace and Defense | ||

| Electronics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global magnesium market in 2026?

The magnesium market size stands at 20.78 million tons in 2026, and it is forecast to reach 27.41 million tons by 2031 at a 5.69% CAGR.

Which region dominates demand for magnesium products?

Asia-Pacific leads with 51.48% of global volume in 2025 and is expanding at a 6.64% CAGR through 2031, buoyed by China’s primary output and India’s steel build-out.

Which application is growing fastest through 2031?

Automotive applications are projected to grow at a 6.81% CAGR as electric-vehicle platforms intensify lightweighting with magnesium alloy castings.

What is the main restraint to wider magnesium adoption in vehicles?

Persistent corrosion and flammability concerns raise component costs and lengthen qualification cycles, slowing penetration into mass-market car segments.

How are government policies shaping magnesium supply chains?

U.S. Defense Production Act funding, the EU Critical Raw Materials Act, and Chinese export-control rules are encouraging on-shoring, diversifying imports, and fragmenting global trade flows.

Page last updated on: