Magazine Publishing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 91.06 Billion |

| Market Size (2031) | USD 101.75 Billion |

| Growth Rate (2026 - 2031) | 2.24% CAGR |

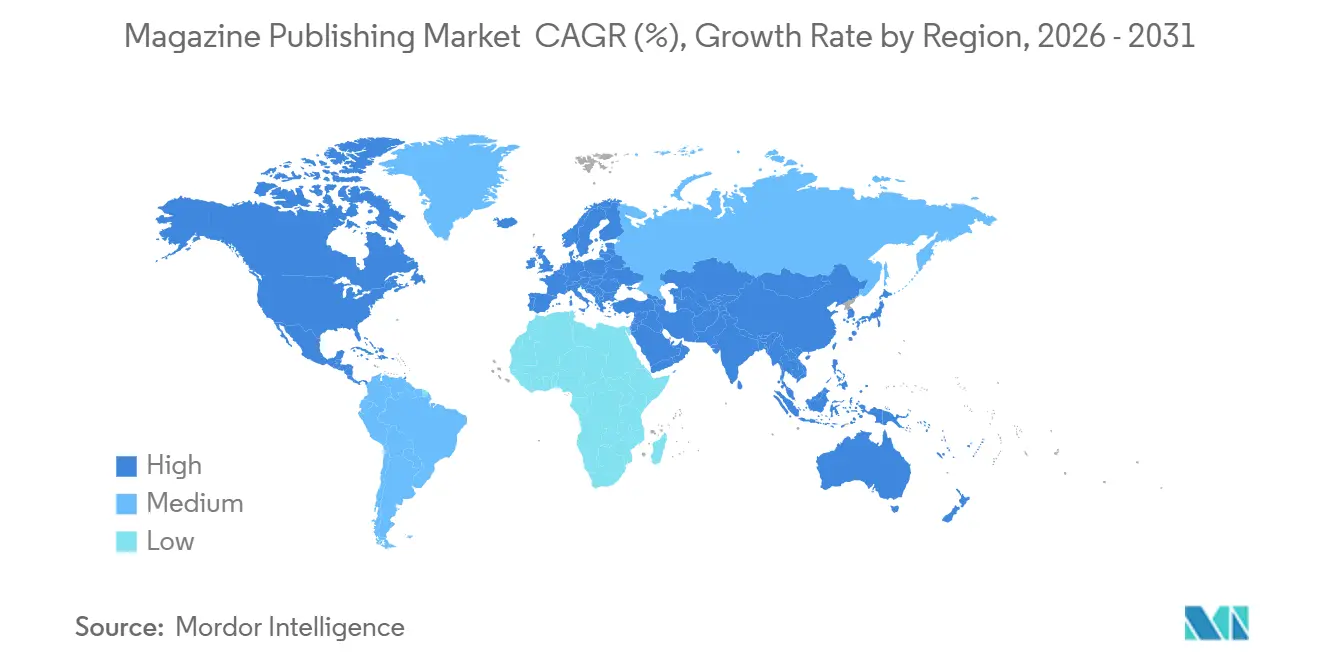

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

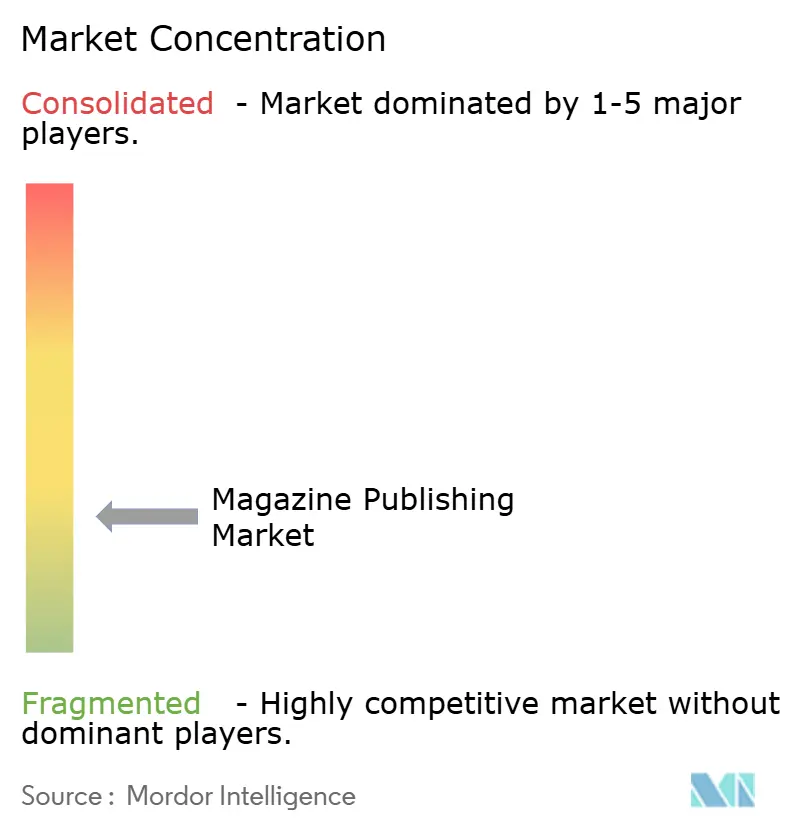

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magazine Publishing Market Analysis by Mordor Intelligence

The magazine publishing market size is projected to expand from USD 89.05 billion in 2025 and USD 91.06 billion in 2026 to USD 101.75 billion by 2031, registering a CAGR of 2.24% between 2026 to 2031. The magazine publishing market is growing at a measured pace because its revenue base is being reshaped rather than replaced, with print still supplying most current revenue while digital formats carry stronger forward growth. The magazine publishing market also reflects a clear shift toward reader revenue, as subscription-led models provide more stability than publisher dependence on traffic-sensitive advertising flows. Competitive advantages in the magazine publishing market are moving toward publishers that control direct subscriber relationships, bundled offerings, and first-party audience data, because those assets support both retention and higher-value advertising products. The magazine publishing market is also becoming more uneven across publishers, with scaled portfolio owners better placed to absorb traffic disruption, invest in product systems, and redeploy cash across print and digital brands. This leaves room for growth in premium digital memberships, specialized editorial portfolios, and carefully positioned print products that serve distinct audiences rather than broad newsstand demand.

Key Report Takeaways

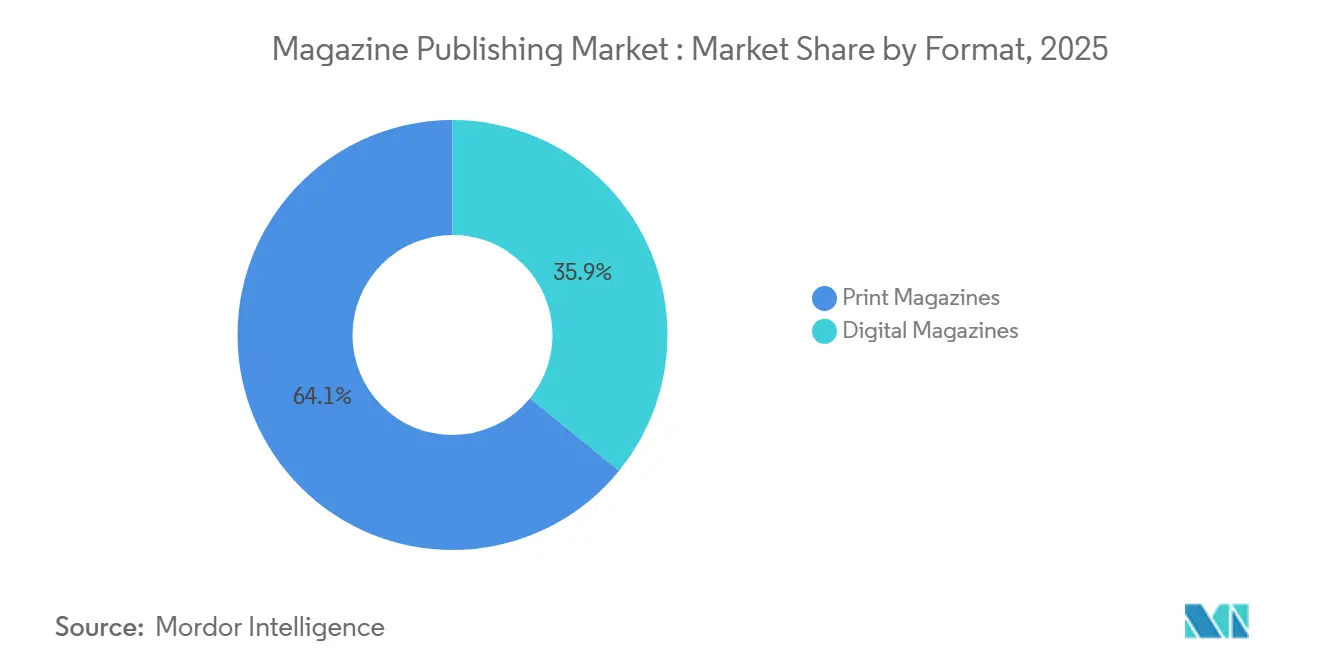

- By format, print held 64.12% share of the magazine publishing market in 2025, while digital is projected to expand at a 6.21% CAGR through 2031.

- By revenue model, subscriptions held 54.37% share of the magazine publishing market in 2025, while advertising recorded the highest projected CAGR at 5.46% through 2031.

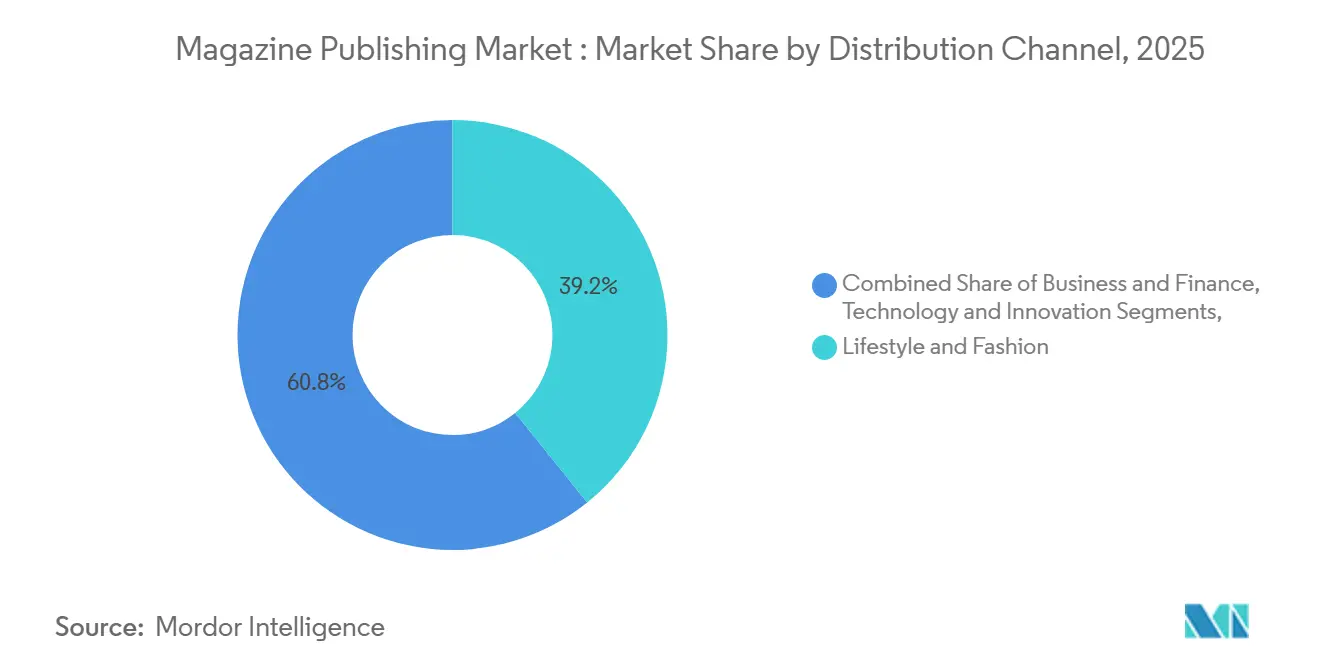

- By content genre, lifestyle and fashion accounted for 39.22% share of the magazine publishing market in 2025, while health and wellness is projected to grow at a 6.11% CAGR through 2031.

- By distribution channel, online accounted for 63.52% share of the magazine publishing market in 2025 and is also projected to advance at a 4.56% CAGR through 2031.

- By geography, North America held 36.10% share of the magazine publishing market in 2025, while Asia-Pacific is projected to expand at a 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magazine Publishing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital Subscription Adoption | +0.6% | Global, with early leadership in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| AI Assisted Editorial Personalization | +0.4% | North America and Europe core, spill-over to Asia-Pacific and Middle East | Medium term (2-4 years) |

| Growth of Niche and Special Interest Magazines | +0.3% | Global, particularly North America, Europe, and Australia | Medium term (2-4 years) |

| Direct Audience Relationships and Bundled Memberships | +0.3% | North America and Europe, early-stage expansion in Asia-Pacific | Short term (≤ 2 years) |

| Interactive and Immersive Magazine Formats | +0.2% | North America, Europe, South Korea, and Japan | Medium term (2-4 years) |

| Premium Print Positioning in Luxury and Design Niches | +0.2% | Europe, North America, and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Subscription Adoption

Digital subscriptions are changing the magazine publishing market from a model centered on advertiser funding to one where reader revenue supports operating stability. Subscription growth and rising revenue indicate that pricing strength and customer value are becoming increasingly important alongside subscriber acquisition. Leading digital publishers have expanded their subscriber bases, improved monetization efficiency, and maintained strong retention levels, supporting the durability of subscription economics once publishers establish direct audience relationships. Global digital subscription penetration remains relatively low, leaving room for further expansion in the magazine market as publishers improve conversion, engagement, and renewal models. This shift is also changing business priorities, as renewal design, pricing discipline, and product depth now carry more weight than simple audience scale. Publishers that rely heavily on discounted entry offers face greater pressure during renewal cycles, making long-term retention a central revenue focus for the magazine market.

AI Assisted Editorial Personalization

AI-assisted editorial personalization is becoming more relevant in the magazine publishing market because it helps publishers align content delivery, product design, and ad targeting around known audience behavior. The commercial benefit is strongest where publishers already hold meaningful first-party data, since automated decision tools work best when audience identity and intent are clear. This makes AI less of a standalone growth lever and more of an amplifier for publishers that already have subscription registrations and habitual users. It also narrows the operating gap between large and mid-sized publishers, because some personalization and workflow functions can now be scaled without a matching increase in editorial headcount. The magazine industry is therefore moving toward a setup where better use of audience signals can improve monetization quality even when total traffic is under pressure.

Growth of Niche and Special Interest Magazines

The magazine publishing market is also supported by specialized editorial categories that hold audience attention more effectively than broad general-interest titles. This pattern is visible in the way focused content areas continue to command stronger loyalty, better pricing, and more durable value even while mass print volumes decline. In Germany, the trade media sector generated EUR 8.75 billion (USD 9.97 billion) in 2025, and digital revenue reached EUR 4.2 billion (USD 4.78 billion) while specialist publishing remained a key part of that structure.[1]Deutsche Fachpresse, “Fachpresse-Statistik 2025,” Deutsche Fachpresse, deutsche-fachpresse.deThat pattern matters for the magazine publishing market because it shows that focused content can retain pricing strength in both print and digital forms when it serves clear professional or enthusiast demand. Publishers with narrower editorial identities also face less direct substitution from broad free content, which gives them a better base for paid access and premium advertiser alignment. The result is not a return to old print scale, but a more selective growth path inside the magazine market where specificity carries more value than volume.

Direct Audience Relationships and Bundled Memberships

Direct audience relationships are becoming one of the main structural advantages in the magazine publishing market because they reduce dependence on outside platforms and strengthen pricing power. At the INMA Media Subscriptions Summit 2025, publishers such as Condé Nast, Der Spiegel, and Newsquest identified bundling as a leading revenue architecture, and bundle subscribers generated 71% of subscription revenue while representing only 53% of the digital-only subscriber base. That revenue concentration shows why publishers are widening product offers across newsletters, audio, and multiple editorial verticals rather than relying on single-title subscriptions. FIPP also noted in 2026 that bundle-first publishers with direct audience relationships continued to grow, while single-title operators, especially in local news, faced subscriber erosion.[2]FIPP, “FIPP's Global Digital Subscription Snapshot 2026: Growing Influence of AI Search,” FIPP, fipp.com This gives the magazine Industry a clear direction, because publishers that know their paying users directly can support both stronger retention and more valuable ad products. It also supports a revenue mix that depends more on relationship quality than on pure scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Print Circulation And Newsstand Dependence | -0.5% | Global, most acute in Western Europe, North America, and Japan | Short term (≤ 2 years) |

| Rising Audience Acquisition Costs In Digital Channels | -0.3% | North America and Europe core, emerging in Asia-Pacific | Medium term (2-4 years) |

| Referral Traffic Volatility From Search And Social Platforms | -0.2% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Print Supply Chain And Paper Cost Pressure | -0.1% | Global, most severe in North America, Europe, and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Print Circulation and Newsstand Dependence

Declining print circulation remains the most direct restraint on the magazine publishing market because print still supplies most current revenue even as demand shifts toward digital access. In Germany, the BDZV 2026 trend survey projected print circulation declines of 8% and print advertising declines of 7% for 2026, while e-paper and paid digital content were expected to grow by up to 20%.[3]BDZV, “Trendumfrage 2026: Print Läuft Aus, Digital Entscheidet über die Zukunft,” Bundesverband Digitalpublisher und Zeitungsverleger, bdzv.de That combination shows the pressure clearly, because publishers are still losing print volume faster than digital growth can fully replace legacy economics in some portfolios. The problem is larger for titles that still rely on broad physical distribution, because retail consolidation weakens shelf visibility while distributors absorb a large part of cover-price economics. This forces the magazine market to support two systems at once, which are a shrinking print network and a still-maturing digital revenue stack. Titles that cannot reposition print around premium audiences or predictable subscriber bases are likely to face a more difficult transition.

Rising Audience Acquisition Costs in Digital Channels

Audience acquisition costs are rising across the magazine publishing market because publishers are competing harder for the same digital users while referral channels have become less dependent on them. Future plc reported in its HY2026 results that audience volume declined by 20% over 2 consecutive financial halves, and the company linked part of the pressure to changes in Google search traffic shaped by AI overviews.[4]Future plc, “Future Announces Half Year Results,” Future plc Investor Relations, futureplc.com FIPP also highlighted the growing influence of AI search on digital subscription performance, which reinforces the risk that publishers receive less low-cost traffic from external platforms than they did before. This raises the cost of converting users into subscribers and increases the importance of email, brand recognition, and other direct acquisition channels, which are usually more expensive to build and maintain. The same shift also forces more investment in consent systems and first-party data foundations, because publishers cannot rely as easily on third-party targeting models. The magazine publishing market therefore faces a harder digital transition where the economics of user acquisition matter almost as much as product quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Format: Digital Formats Accelerate While Print Supports Portfolio Transition

Print held 64.12% share of the magazine publishing market in 2025, which kept it as the leading format by revenue even as long-term growth moved elsewhere. That share still matters because print remains the financing base for many publishers that are reinvesting into subscription systems, audience data, and editorial product tools. In practical terms, print now carries less importance as a broad-volume engine and more importance as a funding source and brand vehicle inside the magazine publishing market. Titles with established subscriber bases, luxury positioning, or deliberate membership distribution are better placed to preserve print value than titles that depend on wide newsstand reach.

Digital formats are projected to grow at a 6.21% CAGR through 2031, making them the fastest-moving part of the format mix in the magazine publishing market. This growth reflects mobile-first reading behavior, lower distribution friction, and a better fit with recurring subscription models than legacy print logistics. The BDZV survey in 2026 also showed that German publishers expected e-paper and paid digital content to grow by up to 20%, even while print circulation and print ad revenue continued to weaken. That split supports a format structure where digital carries forward growth while print becomes more selective in role and audience. The magazine industry is therefore not moving toward a simple print replacement story, but toward a more specialized balance where each format serves a narrower commercial purpose.

By Revenue Model: Subscriptions Provide Stability While Advertising Recovers Faster

Subscriptions accounted for 54.37% of the magazine publishing market in 2025, making reader revenue the largest revenue model across the category. That lead gives publishers a steadier earnings base and reduces direct exposure to short-term advertising fluctuations. It also aligns with the broader shift toward direct audience relationships, as subscription models create identifiable users, predictable recurring revenue, and richer first-party data. Within the magazine publishing market, subscription performance has become central to portfolio resilience, even for publishers that continue to rely on advertising revenue.

Advertising is projected to grow at a 5.46% CAGR through 2031, making it the fastest-growing revenue model in the magazine publishing market. The continued expansion of programmatic advertising and data-driven digital campaigns is creating new monetization opportunities for publishers with strong online audiences and first-party data capabilities. At the same time, stricter paywalls can limit available advertising inventory, requiring publishers to balance audience reach with revenue optimization. As a result, advertising growth is increasingly driven by improved targeting, automation, and audience quality, particularly among publishers with well-established subscriber and registered user bases.

By Content Genre: Lifestyle And Fashion Lead While Health and Wellness Expands Faster

Lifestyle and fashion held 39.22% share in 2025, which kept them as the largest content genre in the magazine publishing market. Their scale reflects long-established consumer demand, strong advertising relevance, and broad demographic appeal across multiple title formats. These brands also tend to have mature subscription offers and stronger premium positioning than many smaller genre categories. That combination helps lifestyle and fashion remain the revenue anchor even while readers diversify across new interests.

Health and wellness is projected to grow at a 6.11% CAGR through 2031, making it the fastest-growing genre in the magazine publishing market. The category benefits from sustained reader interest in preventive health, fitness, and mental well-being, which has remained commercially relevant across both print and digital formats. Its strength also fits the broader move toward specialized content, because readers are often willing to pay for trusted advice and recurring guidance in focused subject areas. Other segments such as business and finance, technology and innovation, travel and leisure, sports and fitness, and entertainment and celebrity still serve distinct advertiser categories, which helps publishers manage revenue concentration across portfolios. The magazine publishing market therefore keeps its largest genre in lifestyle and fashion, but current growth favors subject areas with stronger habit formation and clearer everyday utility.

By Distribution Channel: Online Channels Deepen Control Over Access and Margin

Online distribution held 63.52% of the magazine publishing market size in 2025, which made it the largest channel in the current delivery mix. That position shows that the center of access has already moved away from physical distribution toward direct digital reach. It also gives publishers more control over subscriber data, billing relationships, and product testing than offline channels usually allow. In margin terms, online distribution reduces dependence on third-party newsstand economics and lets publishers retain a larger part of subscriber revenue.

Online distribution is also projected to grow at a 4.56% CAGR through 2031, which means it is both the largest and fastest-growing channel in the magazine publishing market. That double lead suggests that online delivery is not only replacing offline volume but also widening access for new audience groups through lower friction and broader availability. Offline distribution still matters for premium and luxury titles where physical form adds brand value, but it no longer sets the direction of the category. As digital delivery expands, publishers gain better visibility into audience behavior and more freedom to tailor offers around actual user patterns. The magazine publishing market is therefore shifting toward a channel model where direct online access supports both stronger economics and better long-term customer knowledge.

Geography Analysis

North America held 36.10% of the magazine publishing market share in 2025, which kept it as the largest regional contributor to the global magazine publishing market. The region benefits from dense premium title portfolios, a strong institutional advertiser base, and subscription systems that are already more developed than in many other markets. These features make North America important not only because of scale, but also because many of the commercial models shaping the magazine publishing market are already visible there. Canada also shows the cost side of the transition, because the MagsBC sector report cited Statistics Canada data showing that imported pulp and paper products were 57.7% more expensive in March 2025 than in December 2020, while truck transportation costs were also 57.7% higher over the same period. That pressure matters because it narrows print margins while publishers are funding digital transformation.

Europe remained one of the most established parts of the magazine publishing market, supported by long publishing traditions and a relatively high willingness to pay for quality editorial products. The region continues to demonstrate a strong readership base while publishers increasingly expand their digital offerings and subscription-driven business models. Europe also reflects the broader structural transition seen across the industry, with print remaining an important component of publisher portfolios while digital editions, premium content, and reader-supported revenue models increasingly shape future growth. This balanced evolution has enabled publishers to maintain brand value and adapt to changing consumer preferences and content consumption habits.

Asia-Pacific is projected to grow at a 4.88% CAGR through 2031, which makes it the fastest-growing geography in the magazine publishing market. The region combines large population bases, rising digital reading access, and expanding middle-class demand for premium and specialized content. Its growth profile is less uniform than North America or Europe, because local conditions differ widely across India, China, Japan, South Korea, Australia, and Southeast Asia. Even so, the broad direction is clear, as digital readership depth is rising, and publishers have more room to expand paid access and segmented content offers than in mature Western markets. The magazine publishing market in Asia-Pacific therefore stands out less for present dominance and more for the scale of future conversion opportunity, especially where smartphone-led reading behavior aligns with premium subscription products. Smaller geographies in the Middle East and Africa are also attracting selective interest from global publishers through licensed editions and premium lifestyle positioning, though they remain modest in absolute revenue compared with the largest regional blocks.

Competitive Landscape

The competitive structure of the magazine publishing market is moderately consolidated at the top and fragmented across the wider field. A small group of multi-title publishers still commands an outsized share of premium audience attention, subscription infrastructure, and advertiser relationships, while many independent operators remain concentrated in narrower content niches. This split matters because scale now creates advantages in data, product systems, bundling, and cross-title monetization that were less decisive in earlier print-led models. At the same time, fragmentation remains a real feature of the magazine publishing market because category depth, editorial identity, and specialist audiences still leave room for smaller publishers to operate with focus. That is why competition is widening by business model rather than narrowing to a single uniform structure.

The strongest operators in the magazine publishing market are those building direct audience systems instead of depending too heavily on platform traffic. FIPP reported in 2026 that bundle-first publishers with direct audience relationships continued to grow, while single-title operators, especially in local news, faced subscriber erosion. INMA also showed that bundle subscribers delivered 71% of subscription revenue while representing only 53% of the digital-only subscriber base, which explains why scaled publishers are widening product bundles across titles and formats. In practice, that gives portfolio owners a stronger base for pricing, retention, and advertising yield than publishers that still rely on single-title economics.

Recent company actions also show how major groups are repositioning inside the magazine publishing market. Future plc acquired 100% of SheerLuxe Ltd and BLUSH Talent MGMT Ltd in January 2026, which broadened its exposure to premium lifestyle publishing and creator-led engagement formats. In its HY2026 results, Future also launched Renewal as a retention solution to improve subscriber outcomes and reduce pressure from traffic-led acquisition economics. Bauer Media Group announced a realignment of its digital publishing business in May 2026 and started investing in a new software development hub, which showed a preference for owning more of its technology stack rather than relying only on outside platforms. These moves suggest that competition in the magazine publishing market is increasingly shaped by retention systems, proprietary product capabilities, and portfolio breadth rather than by title recognition alone. Mid-tier publishers that do not secure stronger direct relationships may find it harder to defend economics as acquisition costs rise and external traffic becomes less stable.

Magazine Publishing Industry Leaders

Hearst Communications, Inc.

Advance Publications, Inc.

Condé Nast

People Inc.

Future plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Lupa Systems announced the acquisition of New York Magazine, Vox Media Podcast Network, and Vox from Vox Media, with the aim expand its presence in the digital media and publishing sector. The acquisition will strengthen Lupa Systems’ media portfolio by combining established editorial brands, digital platforms, and podcast capabilities.

- January 2026: Future plc acquired 100% of SheerLuxe Ltd and BLUSH Talent MGMT Ltd, a UK-based digital publishing group combining editorial authority with creator economy engagement. The acquisition reflects Future's strategic emphasis on human-originated, trusted content in an AI-driven media environment, and positions the company to capture the growing intersection of premium lifestyle publishing and creator commerce.

- January 2026: Bauer Media Group acquired Télé 7 Jours, along with Télé 7 Jours Jeux and Télé 7 Jeux, strengthening its presence in the French magazine publishing market. The acquisition expanded the company’s portfolio with well-established television and puzzle magazine brands. Bauer Media stated that the deal would support editorial collaboration, enhance subscription offerings, and reinforce its long-term growth strategy in France.

- October 2025: Hotel Designs acquired SPACE magazine and its associated brands, including Global Design Review and HotelSpecOnline, strengthening its position in the hospitality design publishing sector. The acquisition expanded its portfolio across print, digital media, and industry events, creating broader opportunities for content delivery and audience engagement.

Global Magazine Publishing Market Report Scope

The Magazine Publishing Market Report is Segmented by Format (Print, and Digital), Revenue Model (Subscription, and Advertising), Content Genre (Lifestyle and Fashion, Business and Finance, Technology, Health and Wellness, Sports and Fitness, Travel, Entertainment and Celebrity, and More), Distribution Channel (Online, and Offline), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Print Magazines |

| Digital Magazines |

| Subscription |

| Advertising |

| Lifestyle and Fashion |

| Business and Finance |

| Technology and Innovation |

| Health and Wellness |

| Sports and Fitness |

| Travel and Leisure |

| Entertainment and Celebrity |

| Others |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Format | Print Magazines | |

| Digital Magazines | ||

| By Revenue Model | Subscription | |

| Advertising | ||

| By Content Genre | Lifestyle and Fashion | |

| Business and Finance | ||

| Technology and Innovation | ||

| Health and Wellness | ||

| Sports and Fitness | ||

| Travel and Leisure | ||

| Entertainment and Celebrity | ||

| Others | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future size of the global magazine sector?

The magazine publishing market size was USD 89.05 billion in 2025, reached USD 91.06 billion in 2026, and is forecast to reach USD 101.75 billion by 2031 at 2.24% CAGR.

Which format is growing faster, print or digital magazines?

Digital formats are growing faster, with a projected 6.21% CAGR through 2031, while print still held the largest 64.12% share in 2025.

Why are subscriptions becoming more important for publishers?

Subscriptions held 54.37% share in 2025, and INMA data showed digital-only subscription volume grew 6% while revenue grew 10% in Q3 2025, which points to stronger pricing and retention value.

Which content categories are performing best in magazine publishing?

Lifestyle and fashion remained the largest genre with 39.22% share in 2025, while health and wellness is the fastest-growing segment with a 6.11% CAGR through 2031.

Which region leads global revenue and which region is expanding fastest?

North America led with 36.10% share in 2025, while Asia-Pacific is projected to grow the fastest at a 4.88% CAGR through 2031.

What is changing competition among leading publishers?

Competition is shifting toward publishers with direct subscriber relationships, bundled products, first-party data, and proprietary digital systems, which is why companies such as Future plc and Bauer Media Group are investing in retention and internal platforms.

Page last updated on: