Machine Learning Operations (MLOps) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

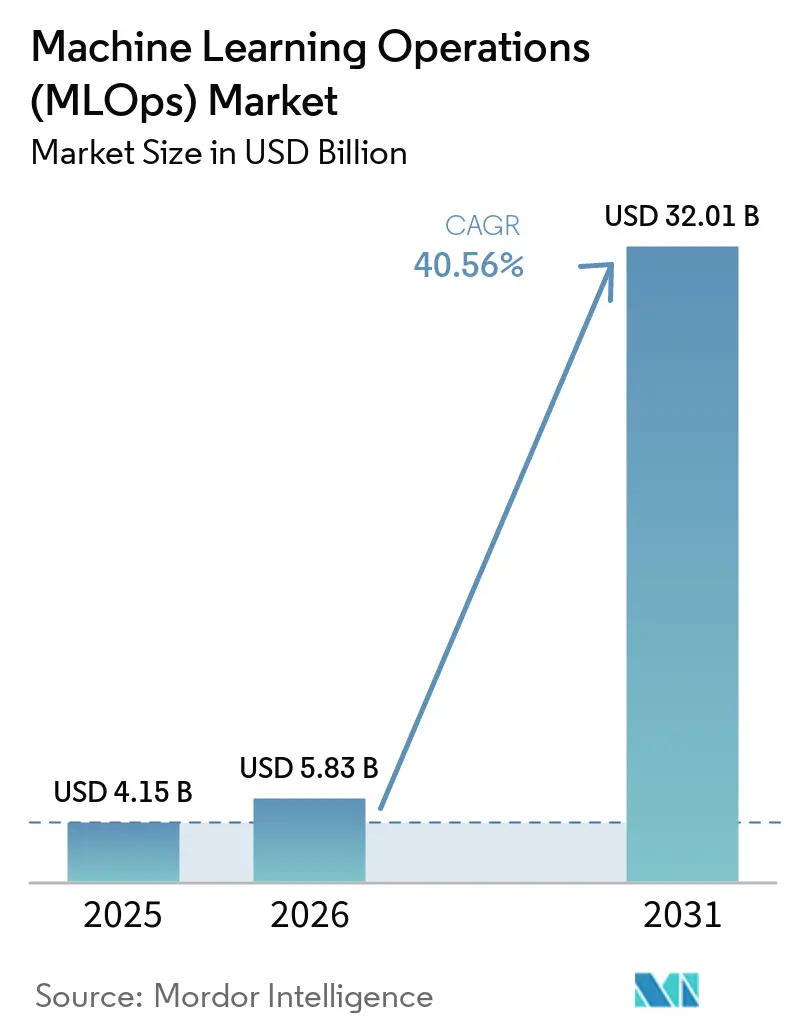

| Market Size (2026) | USD 5.83 Billion |

| Market Size (2031) | USD 32.01 Billion |

| Growth Rate (2026 - 2031) | 40.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Machine Learning Operations (MLOps) Market Analysis by Mordor Intelligence

The machine learning operations (MLOps) market size is projected to expand from USD 4.15 billion in 2025 and USD 5.83 billion in 2026 to USD 32.01 billion by 2031, registering a CAGR of 40.56% between 2026 to 2031. Growth is being shaped by a broader move from isolated model development toward repeatable deployment, monitoring, governance, and cost control across enterprise AI programs. The machine learning operations (MLOps) market is also benefiting from the fact that generative AI and agent-based systems have made the model lifecycle more complex, which increases the value of standardized pipelines, traceability, and policy controls. Demand is rising because enterprises now need a single operating layer that can connect data preparation, experimentation, deployment, monitoring, retraining, and audit workflows without relying on manual handoffs. Competitive activity is centered on integrated platform expansion, hybrid deployment support, and tools that reduce the engineering burden of production AI in regulated and cost-sensitive settings. The machine learning operations (MLOps) market is therefore moving beyond a narrow tooling category and becoming a core part of how organizations run AI systems in production.

Key Report Takeaways

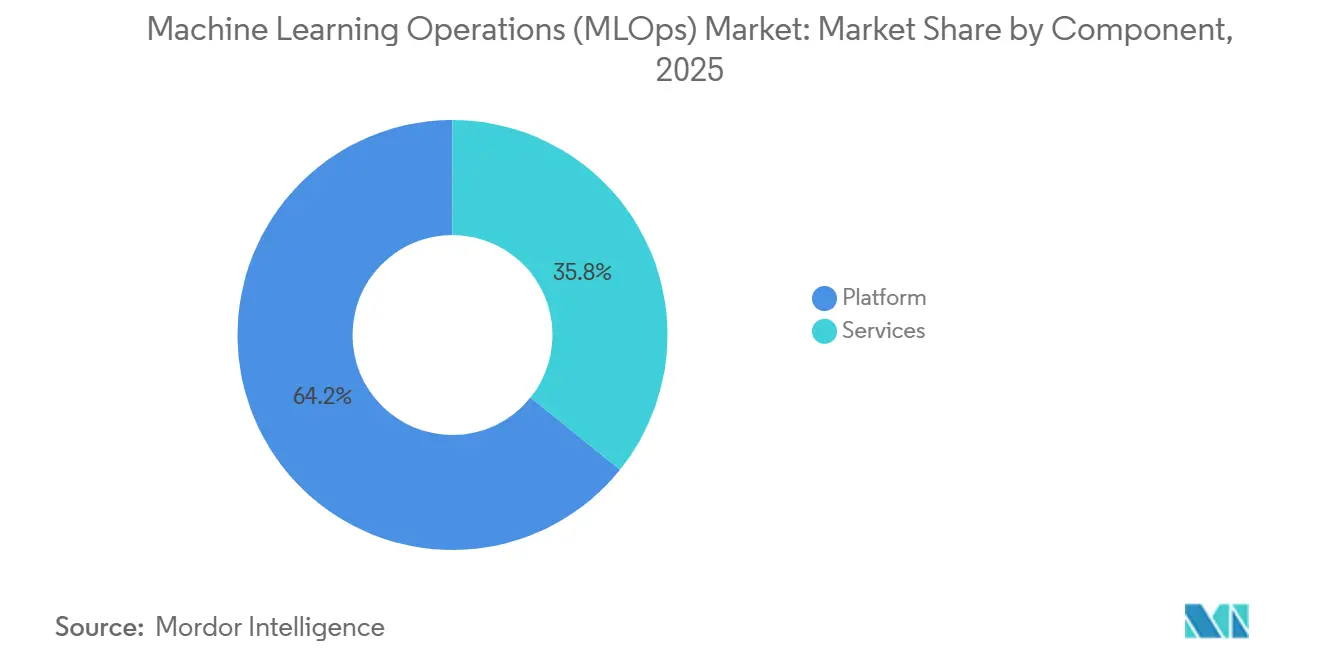

- By component, platforms led with 64.23% revenue share of the machine learning operations (MLOps) market in 2025, while services are forecast to expand at a 41.34% CAGR through 2031.

- By deployment mode, cloud held 53.44% of revenue of the MLOps market in 2025, and cloud also records the fastest projected growth at 40.87% through 2031.

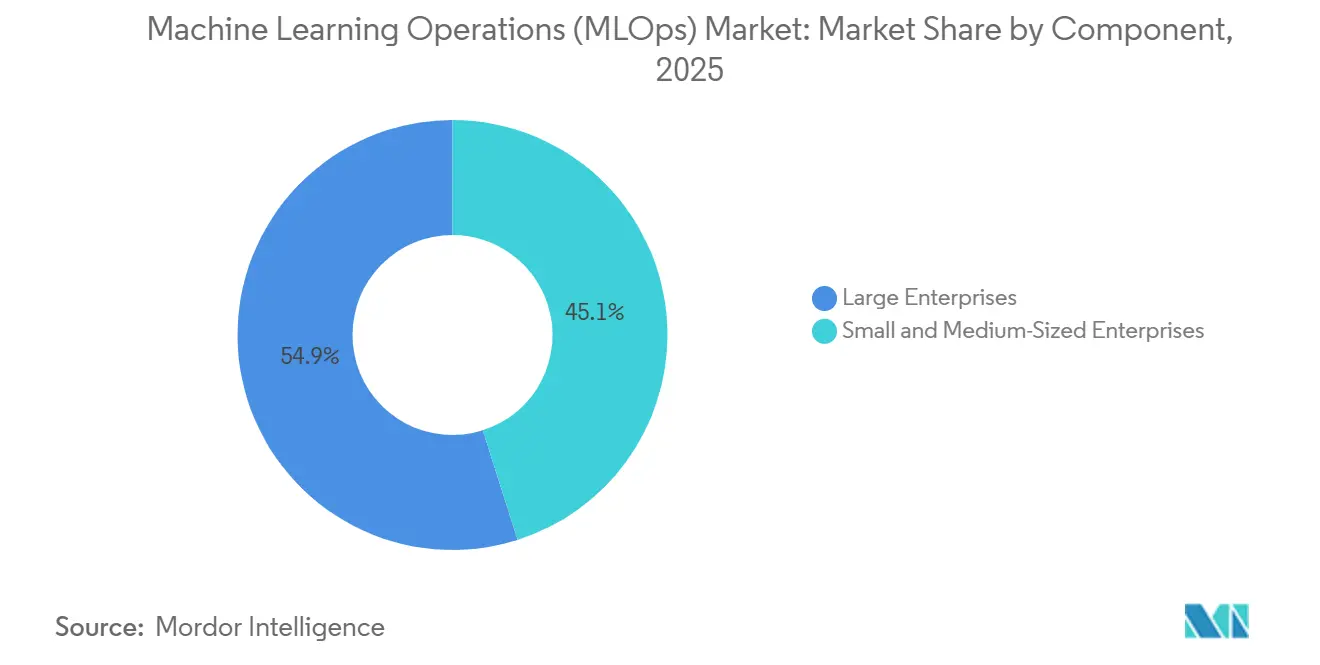

- By organization size, large enterprises accounted for 54.90% of revenue of the machine learning operations (MLOps) market in 2025, while SMEs are projected to grow at a 41.76% CAGR through 2031.

- By end-user industry, BFSI held 22.11% of revenue of the MLOps market in 2025, while healthcare and life sciences is expected to expand at a 40.43% CAGR through 2031.

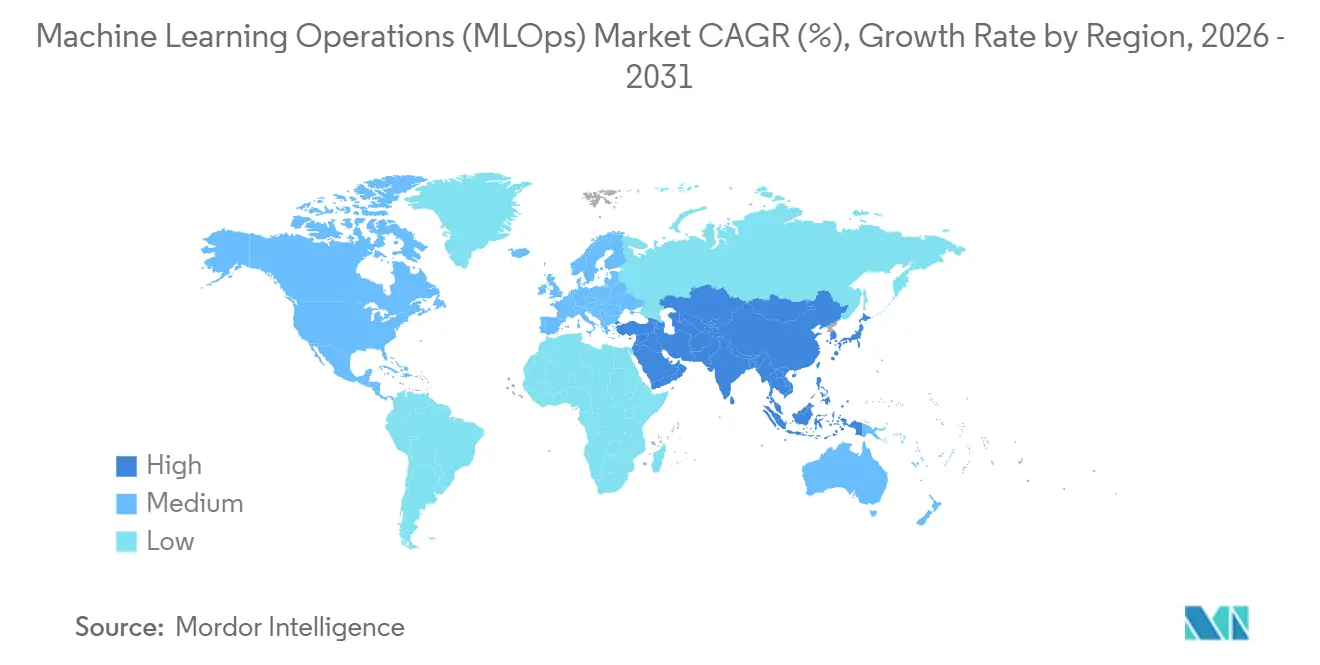

- By geography, North America captured 34.22% of revenue of the machine learning operations (MLOps) market in 2025, while Asia-Pacific is projected to advance at a 41.63% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Machine Learning Operations (MLOps) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scaling AI from Pilot to Production | +5.2% | Global | Short term (≤ 2 years) |

| Rising Need for Model Monitoring and Drift Management | +4.8% | Global | Medium term (2-4 years) |

| Expansion of Cloud-Native AI Infrastructure | +6.1% | North America and the Asia-Pacific | Short term (≤ 2 years) |

| Tightening AI Governance and Auditability Requirements | +4.2% | Europe and North America | Medium term (2-4 years) |

| LLMOps and AgentOps Convergence Raising Lifecycle Complexity | +5.7% | Global | Short term (≤ 2 years) |

| GPU FinOps and Inference Cost Control Becoming a Platform Priority | +3.8% | North America and the Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scaling AI from Pilot to Production

The machine learning operations (MLOps) market is being lifted by a basic enterprise problem, many organizations can build models, but far fewer can move them into stable production with repeatable controls. Once model counts rise across departments, manual promotion, version tracking, rollback, and retraining quickly become operational bottlenecks that slow value capture and increase release risk. This pressure is pushing buyers toward platforms that standardize handoffs across development, validation, deployment, and monitoring, rather than relying on separate point tools and custom scripts. Amazon SageMaker AI added serverless MLflow in December 2025, which shows how vendors are trying to reduce setup work and shorten the path from experimentation to managed deployment.[1]Amazon Web Services, “Amazon SageMaker AI Announces Serverless MLflow Capability for Faster AI Development,” Amazon Web Services, aws.amazon.com Microsoft Fabric also introduced cross-workspace logging for MLflow in April 2026, which supports cleaner separation across development, test, and production environments without breaking workflow continuity. As a result, the MLOps market is gaining from enterprise demand for operating discipline as much as it is gaining from demand for new AI features.

Rising Need for Model Monitoring and Drift Management

The MLOps market is also expanding because production models do not stay reliable without continuous oversight after deployment. Performance decay, changing data patterns, latency shifts, and policy failures can emerge gradually, and these issues are harder to detect in customer-facing generative systems than in traditional prediction workloads. Databricks addressed this shift in June 2025 with MLflow 3.0, which added production-scale tracing, prompt tracking, and LLM judges to support evaluation and observability across generative AI workflows.[2]Databricks, “MLflow 3.0: Build, Evaluate, and Deploy Generative AI with Confidence,” Databricks, databricks.com Amazon SageMaker AI integrated MLflow 3.10 in May 2026 with tracing for multi-turn workflows and built-in evaluation and dashboarding for latency, token use, and quality, which reflects growing demand for operational visibility after release. Arize AI also added native support for NVIDIA NIM in March 2026 so teams could monitor and evaluate models deployed through that runtime inside the same observability layer. These shifts are making monitoring a central buying criterion in the machine learning operations (MLOps) market, especially as agentic systems introduce longer decision chains and more failure points.

Expansion of Cloud-Native AI Infrastructure

The expansion of managed cloud AI services remains the most powerful growth driver for the machine learning operations (MLOps) market because it lowers operational friction and gives teams faster access to scalable compute, orchestration, and lifecycle tooling. Amazon Web Services outlined structural GPU cost controls in June 2025, including use of Spot cAsia-Pacificity and Trainium, which shows that cloud providers are positioning infrastructure economics and platform design as part of the same production AI conversation. Google Cloud expanded managed Asia-Pacifiche Airflow capabilities in May 2026 with native DAG versioning and agentic troubleshooting, which reduces the integration overhead involved in coordinating data and AI workflows at scale. Amazon Web Services also made the AWS MCP Server and Agent Toolkit generally available in May 2026, extending secure and auditable access across more than 40 AWS services for AI agents and developer workflows. Cloud adoption does not remove the need for hybrid models, but it does make the machine learning operations (MLOps) market more accessible to organizations that want fast deployment without building every control layer internally. This is why the MLOps market continues to deepen around hyperscaler ecosystems even as buyers ask for portability across cloud, on-premises, and edge environments.

LLMOps and AgentOps Convergence Raising Lifecycle Complexity

The machine learning operations (MLOps) market is increasingly shaped by the fact that large language models and agent-based systems require more than conventional training and deployment pipelines. These workloads depend on prompt versioning, workflow tracing, policy controls, tool access governance, evaluation loops, and runtime cost visibility, all of which expand the operational surface area that MLOps platforms must manage. IBM introduced watsonx Orchestrate in May 2026 as part of its AI operating model blueprint, which shows how vendors are packaging orchestration, agent governance, and real-time data controls into the same enterprise control plane. Teradata launched its Autonomous Knowledge Platform in May 2026 with an AI Studio environment and an agentic workspace across cloud, on-premises, and hybrid settings, which reflects the same move toward wider lifecycle unification.[3]Teradata, “Introducing the Autonomous Knowledge Platform,” Teradata, teradata.com Databricks MLflow 3.0 also brought generative AI experimentation, observability, and deployment controls onto one platform in June 2025, reinforcing the shift from model management toward broader AI system operations. As this complexity rises, the MLOps market is seeing stronger demand for platforms that can govern agents, prompts, models, and infrastructure inside one operational framework.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Cross-Functional MLOps Talent | -3.5% | Global | Medium term (2-4 years) |

| Fragmented Toolchains and Integration Debt | -2.8% | Global | Medium term (2-4 years) |

| Sovereign AI and Data Localization Rules Fragmenting Deployment Architectures | -2.1% | Europe, the Asia-Pacific, and Middle East and Africa | Long term (≥ 4 years) |

| Security Exposure Across Model Registries, Feature Stores, and CI/CD Supply Chains | -1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Cross-Functional MLOps Talent

The machine learning operations (MLOps) market still faces a real adoption constraint because production AI requires combined skills in data engineering, software delivery, governance, and model operations, and that blend is scarce in most organizations. Many enterprises can fund AI tools, but they still struggle to staff teams that can maintain release pipelines, monitor live systems, manage rollback processes, and document controls for regulated use cases. This shortage is especially visible when organizations move from a few isolated models to broader portfolios that demand standardized release practices and shared governance processes across business units. Platform vendors are responding by building more automation into experiment tracking, deployment templates, and managed workflow tooling, which reduces the amount of specialist labor required for basic operations. Microsoft Fabric's MLflow logging across separate workspaces also reflects this push toward reducing coordination friction for teams that do not have large dedicated platform engineering groups. Even so, the machine learning operations (MLOps) market cannot fully convert strong software demand into production adoption unless buyers can close the gap between tooling access and operational expertise.

Fragmented Toolchains And Integration Debt

Fragmented AI stacks remain another clear restraint on the machine learning operations (MLOps) market because disconnected tools create duplicated work across data preparation, experimentation, deployment, monitoring, and governance. When teams rely on separate utilities for registries, pipelines, observability, prompt management, feature serving, and policy controls, basic changes often require custom integration code and manual validation across several systems. That complexity raises operating costs, slows deployment cycles, and weakens accountability because no single control layer can provide a complete audit trail from development through production. Databricks has been responding by bringing model lifecycle, governance, and multi-model access into its broader data platform, including native partner integrations and unified control through MLflow and related services. IBM is making a similar move by tying agent orchestration, data streaming, and hybrid deployment into a larger enterprise operating model, which signals that platform breadth is now part of the value proposition. The MLOps market therefore continues to grow, but near-term spending is still moderated by the time and cost involved in consolidating tools that were adopted in separate phases of enterprise AI development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Lead, While Services Remain Essential to Production Delivery

Platforms held 64.23% of revenue in 2025, which means the platform layer remained the core spending center across the machine learning operations (MLOps) market. Platforms held 64% of the machine learning operations (MLOps) market share in 2025 because enterprises increasingly preferred one control plane for experiment tracking, model registry, deployment, monitoring, and governance. That preference reflects a broader buyer shift away from stitching together separate lifecycle tools, especially when teams need clear lineage across model releases and policy decisions. Databricks strengthened this model in June 2025 by extending MLflow 3.0 across traditional machine learning and generative AI workflows with tracing, evaluation, and deployment controls on one platform. Amazon SageMaker AI also added serverless MLflow in December 2025, which shows that large vendors see control plane simplification as a direct route to wider production adoption.

Services are forecast to expand at a 41.34% CAGR through 2031, which keeps the service layer highly relevant even in a platform-led revenue structure. The machine learning operations (MLOps) market is not shifting away from human support, because many organizations still need outside help for architecture design, workflow migration, governance setup, and operating model changes. This is especially true when AI programs move into LLMOps and AgentOps, where deployment patterns are less standardized and the cost of poor release design is higher. Microsoft Fabric's cross-workspace logging update in April 2026 illustrates how platform features can reduce complexity, but it also highlights how enterprises still need implementation support to align process, permissions, and production controls across teams. In practice, the MLOps market is moving toward blended delivery models where software and services are purchased together to shorten deployment time and reduce internal operating strain.

By Deployment Mode: Cloud Leads Spending, While Hybrid Requirements Continue to Rise

Cloud accounted for 53.44% share of the machine learning operations (MLOps) market size in 2025, and it is also the fastest-growing deployment mode with a 40.87% CAGR through 2031. The cloud lead reflects the scale advantages of managed infrastructure, faster environment setup, and tighter integration between compute, orchestration, monitoring, and governance services. Amazon Web Services continued to reinforce this direction in June 2025 by outlining ways to lower GPU training and inference costs, which directly supports cloud-based production AI economics. Google Cloud added orchestration improvements to Managed Asia-Pacifiche Airflow in May 2026, which helps teams run data and AI workloads with less custom engineering overhead. These developments show why the machine learning operations (MLOps) market continues to concentrate a large share of new deployment activity in cloud environments.

On-premises deployment still matters because data residency, sovereign AI requirements, and internal control needs remain strong in regulated and security-sensitive settings. Hybrid architectures are therefore gaining weight, not because cloud growth is slowing, but because many enterprises now need one operating model across cloud, private infrastructure, and edge nodes. Amazon Web Services reflected this broader shift in May 2026 when it made the AWS MCP Server and Agent Toolkit generally available with IAM guardrails and CloudTrail logging, underscoring how secure integration across services has become part of the deployment conversation. Teradata also launched its Autonomous Knowledge Platform in May 2026 for cloud, on-premises, and hybrid environments, which points to sustained demand for deployment consistency across different runtime locations. The MLOps market is therefore likely to remain cloud-led on revenue while becoming more hybrid in operating design over the forecast period.

By Organization Size: Large Enterprises Hold Scale, While SMEs Expand Faster

Large enterprises accounted for 54.90% share of the machine learning operations (MLOps) market size in 2025 because they run more production models, carry heavier governance obligations, and have larger budgets for platform standardization. Their scale also means that fragmented experimentation becomes costly more quickly, which pushes them toward centralized registries, formal deployment controls, and persistent monitoring workflows. In many large organizations, the MLOps decision is now tied to risk management and operating discipline rather than to standalone developer productivity. At the same time, large enterprises are not the only source of demand, because cloud-native tooling has lowered the entry barrier for mid-market adopters that do not carry the same legacy integration debt. This dynamic keeps the machine learning operations (MLOps) market broad-based, with spending led by large organizations but adoption momentum extending well beyond them.

SMEs are projected to grow at a 41.76% CAGR through 2031, which makes them the fastest-expanding organization-size segment in the MLOps market. Smaller firms are benefiting from consumption-based pricing, self-serve deployment paths, and preconfigured platform services that reduce upfront infrastructure commitments. OpenAI reported in 2025 that non-technology firm API usage had grown 5 times year over year, which supports the view that AI adoption is widening across businesses that historically lacked deep internal ML engineering teams. That usage growth matters because once these organizations move from testing to repeatable production, they still need versioning, observability, and workflow controls even if they start with smaller model portfolios. For that reason, the machine learning operations (MLOps) market is seeing vendors refine entry-level product design around templates, managed pipelines, and lower-friction deployment paths for smaller enterprises.

By End-User Industry: BFSI Leads Current Demand, While Healthcare and Life Sciences Accelerate

BFSI held 22.11% of the machine learning operations (MLOps) market share in 2025, which kept it as the largest end-user industry in the machine learning operations (MLOps) market. That lead was supported by use cases such as fraud detection, credit scoring, algorithmic decision support, and model risk management, all of which require traceability and controlled release processes. Financial institutions also tend to manage more formal approval chains for model changes, which strengthens demand for version control, monitoring, and audit documentation. Persistent Systems described a financial services deployment in March 2026 where a unified MLOps operating model helped reduce cloud and MLOps costs by 30% while supporting faster production delivery across more than 30 critical models. This helps explain why BFSI remains a steady revenue anchor for the MLOps market even as newer AI use cases spread across other sectors.

Healthcare and life sciences is the fastest-growing end-user industry with a 40.43% CAGR through 2031, reflecting the need for closer surveillance, traceability, and documented controls around clinical and diagnostic AI systems. Growth in this segment is being shaped less by raw model volume and more by the compliance burden attached to high-impact decisions, patient data handling, and post-deployment oversight. That makes the operating requirements for healthcare AI distinct from more purely productivity-led deployments in retail or media. Manufacturing, IT and telecom, and retail are also moving deeper into production AI as predictive maintenance, quality inspection, personalization, and operational automation workloads become harder to manage with ad hoc processes. Over time, the machine learning operations (MLOps) market should also widen across government, energy, transportation, education, and public sector use cases as formal AI governance programs mature and more organizations move beyond isolated pilots.

Geography Analysis

North America held 34.22% of the machine learning operations (MLOps) market share in 2025, which kept it as the largest regional contributor to the machine learning operations (MLOps) market. The region benefits from dense cloud infrastructure, large enterprise AI budgets, a deep vendor base, and a strong concentration of experienced platform and data engineering talent. Amazon said in November 2025 that it would invest up to USD 50 billion to expand AI and supercomputing infrastructure for U.S. government agencies, which supports long-run demand for production-grade MLOps in federal and defense-related environments. Canada is also strengthening its role through new AI and cloud infrastructure commitments that support enterprise adoption and public sector implementation over 2025 and 2026. The United States remains the main regional growth engine because it combines hyperscaler strength, software vendor density, and earlier enterprise adoption patterns than most other markets.

Asia-Pacific is the fastest-growing regional segment at a 41.63% CAGR through 2031, and this keeps it central to the longer-term expansion path of the machine learning operations (MLOps) market. Growth across the region is supported by a rising base of enterprise AI adoption, stronger policy attention, and more demand for cloud-native platforms that can be deployed quickly. Japan stands out for corporate API adoption, with OpenAI reporting the largest number of corporate API customers outside the United States, which suggests strong demand conditions for downstream operational tooling. China contributes significant volume through large-scale enterprise AI deployment and stronger interest in sovereign and on-premises operating models. Singapore is also influencing regional adoption patterns because governance-led AI programs in finance, healthcare, and advanced manufacturing are raising expectations around auditability and lifecycle control across Southeast Asia.

Europe remained the third-largest regional block, with Germany, the United Kingdom, and France accounting for much of regional spending in the machine learning operations (MLOps) market. Regulatory pressure is a major regional factor, because buyers in regulated sectors are placing greater emphasis on technical documentation, event logging, and human oversight in production AI systems. The appliedAI Initiative in Germany works with 23 of the 40 DAX corporations and treats AI governance as part of the operating model itself, which reflects how compliance is being built directly into MLOps practice. South America, the Middle East, and Africa remain smaller in aggregate, but sovereign AI priorities, public sector programs, and financial services digitization still create targeted opportunities for vendors that can support in-country, hybrid, or tightly governed deployment architectures.

Competitive Landscape

The machine learning operations (MLOps) market has a bifurcated structure, with hyperscaler-led platforms on one side and specialized pure-play vendors on the other. Amazon Web Services, Microsoft, and Google benefit from existing cloud relationships, broad infrastructure control, and the ability to combine data, compute, model management, and governance inside one enterprise environment. This gives them an advantage with buyers that want lower switching friction and tighter alignment between infrastructure economics and production AI workflows. Databricks is pushing from a different angle by expanding from data infrastructure into broader AI operations, including its June 2025 partnership with Google Cloud to integrate Gemini models into the Databricks Data Intelligence Platform under shared governance controls. The result is a machine learning operations (MLOps) market where platform competition is increasingly tied to who can unify data, orchestration, governance, and multi-model access with the least operational complexity.

IBM is targeting large enterprise accounts by combining hybrid cloud reach with broader operating model control for agent-based systems. Its Think 2026 announcements introduced watsonx Orchestrate as an agentic control plane and confirmed the Confluent acquisition, which together strengthen IBM's position in real-time, policy-aware AI operations for complex enterprise environments. Teradata is also competing around lifecycle breadth, using cloud, on-premises, and hybrid integration as a way to serve organizations that cannot standardize on a single runtime environment. On the specialist side, Arize AI is differentiating through observability depth, especially for organizations that need production monitoring around NVIDIA NIM deployments and closed-loop evaluation workflows. Weights and Biases has taken a similar depth-focused route in generative AI evaluation and tracing, which remains important for enterprises that need detailed visibility into model behavior after launch.

Competitive pressure is also rising because buyers increasingly want fewer tools, broader governance coverage, and better cost accountability across training and inference workflows. That preference favors vendors that can combine experimentation, deployment, monitoring, and policy controls into one operating layer while still supporting hybrid and multi-model environments. Amazon Web Services has reinforced this direction through its Agent Toolkit and MLflow-related SageMaker AI updates, both of which reduce the number of separate components enterprises need to operate agentic workloads at scale. The MLOps market therefore remains active and crowded, but the clearest advantage is shifting toward vendors that can simplify production AI without forcing customers into brittle, heavily customized toolchains.

Machine Learning Operations (MLOps) Industry Leaders

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

IBM Corporation

Databricks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IBM unveiled its AI Operating Model blueprint at Think 2026, releasing watsonx Orchestrate as a next-generation agentic control plane for multi-agent orchestration, alongside IBM Bob, an agentic development partner with security and cost controls, and IBM Sovereign Core for policy-embedded infrastructure governance. The event also confirmed the completion of IBM's acquisition of Confluent for real-time data streaming, expanding its watsonx.data capabilities.

- May 2026: Teradata launched the Autonomous Knowledge Platform on May 7, 2026, unifying production-grade AI, analytics, and data across cloud, on-premises, and hybrid environments under a single integrated system, featuring the AI Studio environment, the Tera agentic workspace, and partnerships with Pinecone and Karini AI for vector retrieval and no-code agent development.

- May 2026: Amazon Web Services made the AWS MCP Server and Agent Toolkit for AWS generally available on May 6, 2026, providing AI coding agents with secure, auditable access to over 40 AWS services via the Model Context Protocol with IAM-based guardrails and CloudTrail logging, a key infrastructure component for agentic MLOps pipelines.

- April 2026: Microsoft Fabric announced the general availability of Cross-Workspace Logging for MLflow on April 23, 2026, enabling machine learning teams to log experiments and models across Dev, Test, and Prod workspaces using standard MLflow APIs, improving governance separation for enterprise MLOps workflows.

Global Machine Learning Operations (MLOps) Market Report Scope

The Machine Learning Operations (MLOps) Market focuses on tools and platforms designed to streamline the deployment, monitoring, and management of machine learning models in production environments. By integrating data science with DevOps and IT operations, these solutions ensure that AI-driven applications are scalable, reliable, and efficient. The market's expansion is driven by the increasing adoption of artificial intelligence across various industries, the pressing need for accelerated model lifecycle management, and the growing demand for automation in managing complex workflows. These workflows include model training, versioning, governance, and the continuous integration and delivery (CI/CD) of machine learning systems.

The MLOps Market is Segmented by Component (Platform [Experiment Tracking and Collaboration, Pipeline Orchestration and CI/CD, Feature Store and Data Lineage, Model Registry and Versioning, Deployment and Serving, Monitoring and Observability, and Governance and Responsible AI], Services [Consulting and Strategy, Implementation and Integration, Training and Enablement, Managed Services, and Support and Maintenance]), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, IT and Telecom, Retail and E-commerce, Manufacturing, Government and Public Sector, Energy and Utilities, Media and Entertainment, Transportation and Logistics and Education and Research), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform | Experiment Tracking and Collaboration |

| Pipeline Orchestration and CI/CD | |

| Feature Store and Data Lineage | |

| Model Registry and Versioning | |

| Deployment and Serving | |

| Monitoring and Observability | |

| Governance and Responsible AI | |

| Services | Consulting and Strategy |

| Implementation and Integration | |

| Training and Enablement | |

| Managed Services | |

| Support and Maintenance |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Retail and E-commerce |

| Manufacturing |

| Government and Public Sector |

| Energy and Utilities |

| Media and Entertainment |

| Transportation and Logistics |

| Education and Research |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Platform | Experiment Tracking and Collaboration |

| Pipeline Orchestration and CI/CD | ||

| Feature Store and Data Lineage | ||

| Model Registry and Versioning | ||

| Deployment and Serving | ||

| Monitoring and Observability | ||

| Governance and Responsible AI | ||

| Services | Consulting and Strategy | |

| Implementation and Integration | ||

| Training and Enablement | ||

| Managed Services | ||

| Support and Maintenance | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Media and Entertainment | ||

| Transportation and Logistics | ||

| Education and Research | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the global machine learning operations (MLOps) market?

The global machine learning operations (MLOps) market stood at USD 5.83 billion in 2026 and is projected to reach USD 32.01 billion by 2031, growing at a 40.56% CAGR over 2026-2031.

Which component generates the most revenue in this space?

Platforms led revenue generation with a 64.23% share in 2025 because enterprises preferred integrated lifecycle control across tracking, deployment, monitoring, and governance.

Which deployment model is growing the fastest for MLOps adoption?

Cloud is both the largest and fastest-growing deployment mode, with 53.44% share in 2025 and a 40.87% CAGR through 2031.

Why is healthcare and life sciences gaining ground so quickly?

The vertical is projected to grow at 40.43% CAGR because clinical and diagnostic AI systems need stronger traceability, continuous monitoring, and regulatory auditability.

Which region offers the strongest long-term expansion opportunity?

Asia-Pacific is the fastest-growing region with a 41.63% CAGR, supported by broader enterprise AI adoption and a rising need for scalable operational controls.

What is shaping vendor competition in production AI operations?

Competition is being shaped by integrated platform breadth, hybrid deployment support, agent and LLM lifecycle management, and better visibility into runtime cost, governance, and monitoring.

Page last updated on: