Luxury Small Home Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

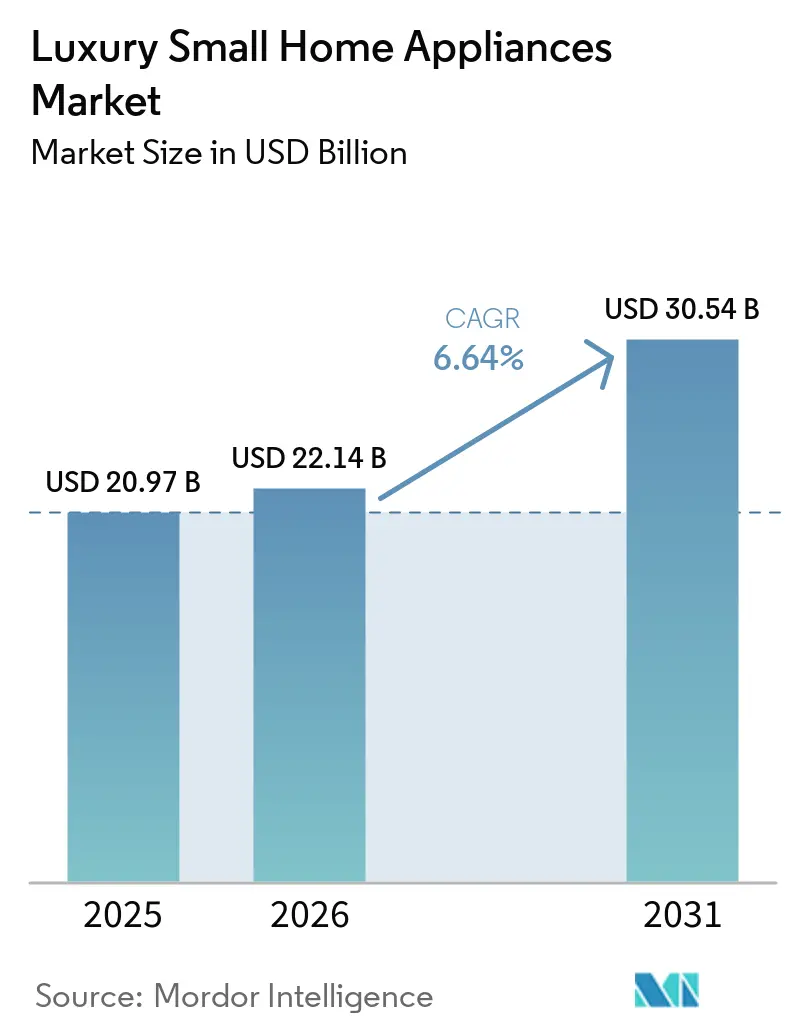

| Market Size (2026) | USD 22.14 Billion |

| Market Size (2031) | USD 30.54 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

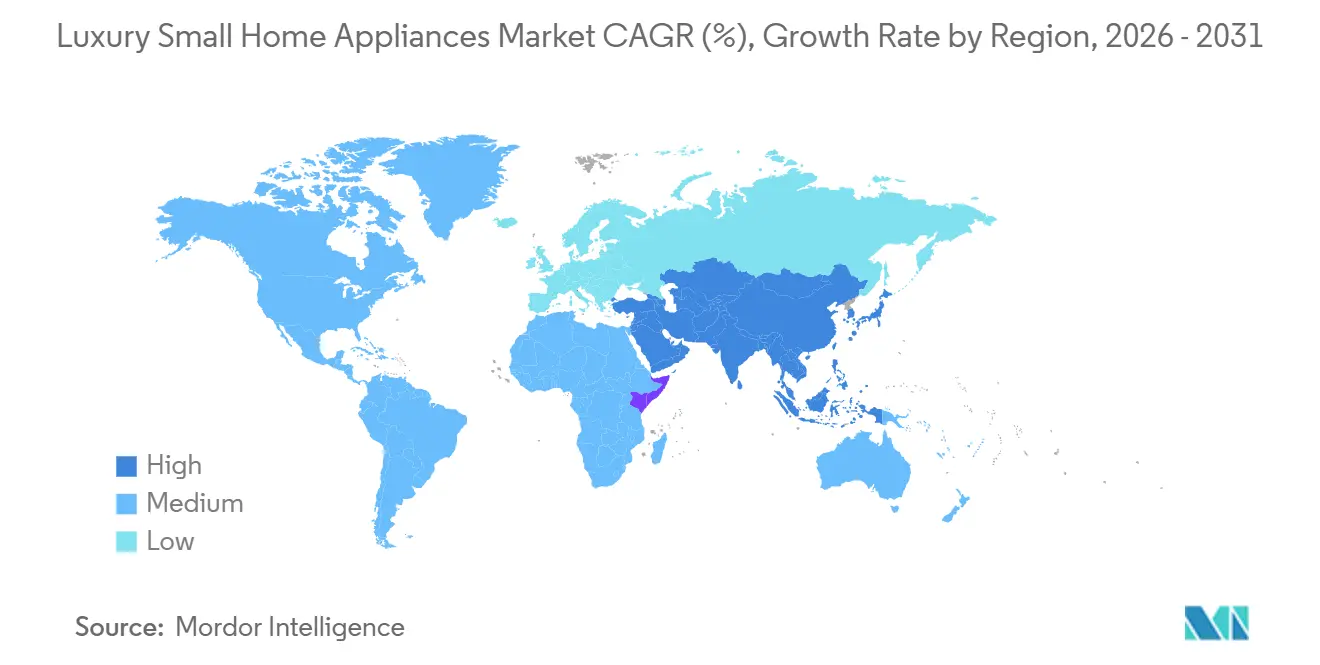

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

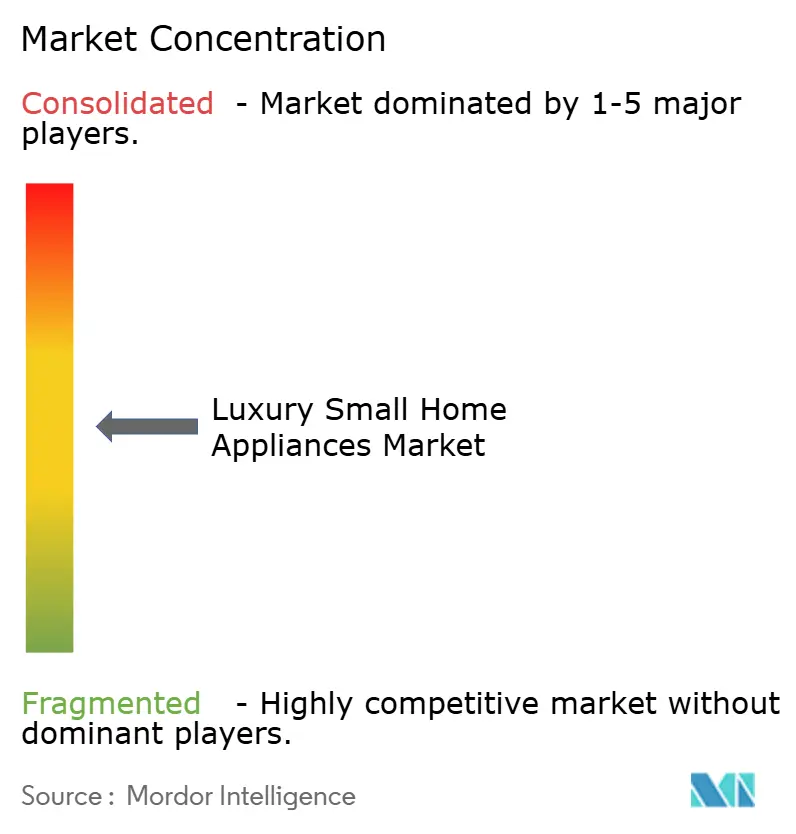

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Small Home Appliances Market Analysis by Mordor Intelligence

The luxury small home appliances market size is expected to increase from USD 20.97 billion in 2025 to USD 22.14 billion in 2026 and reach USD 30.54 billion by 2031, growing at a CAGR of 6.64% over 2026-2031. The luxury small home appliances market is being supported by premiumization, as affluent households place greater weight on design, product finish, ease of use, and connected features when upgrading their personal and kitchen spaces. Demand also remains tied to home-based cooking, coffee preparation, and self-care routines that persisted after the pandemic and now support replacement and trade-up purchases across premium categories. The luxury small home appliances market is also shaped by regional contrast, with Europe holding the largest position. At the same time, Asia-Pacific remains the main growth engine as wealth creation expands the base of first-time luxury buyers. Competition in the luxury small home appliances market remains active, as established European and Japanese brands defend their heritage and engineering strength. At the same time, faster-moving challengers use shorter launch cycles and digital features to narrow the gap. Near-term pressure on the luxury small home appliances market continues to come from supply disruptions, tariff exposure, counterfeit goods on online platforms, and mature urban demand pockets in Western Europe, where growth increasingly depends on upgrades rather than first purchases.

Key Report Takeaways

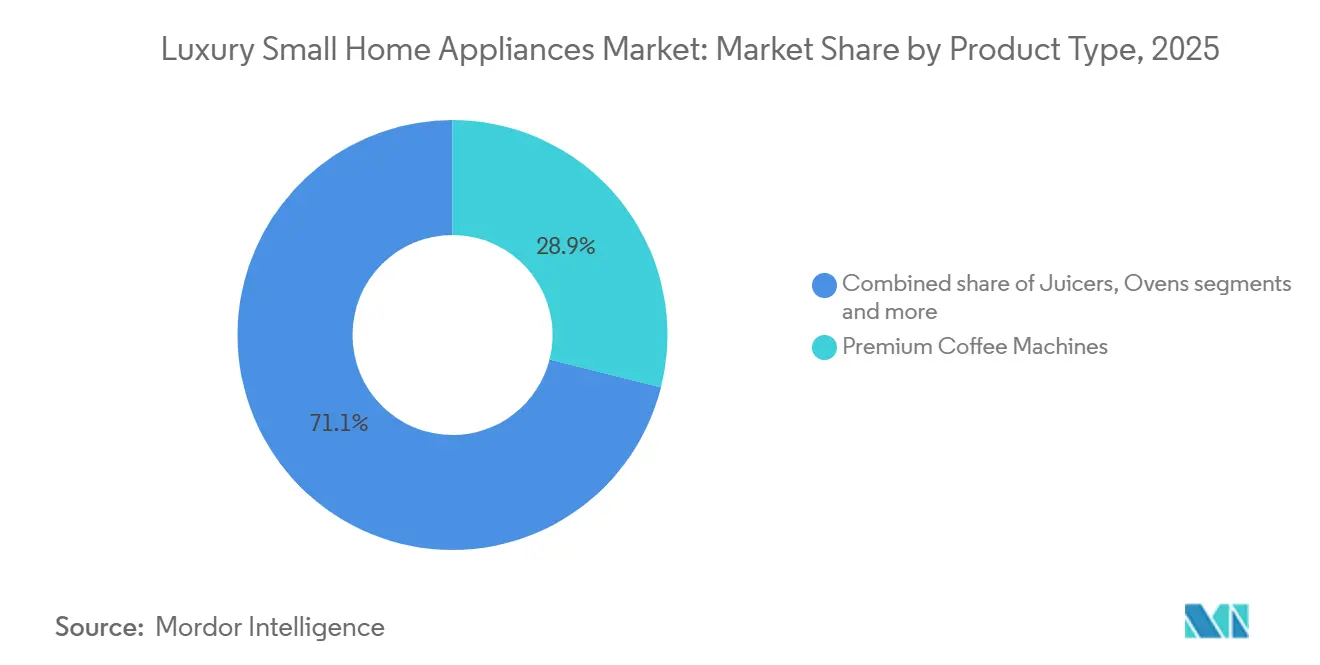

- By product type, premium coffee machines accounted for 28.92% of the luxury small home appliances market share in 2025, while robotic and cordless vacuum cleaners recorded the highest projected CAGR of 5.83% through 2031.

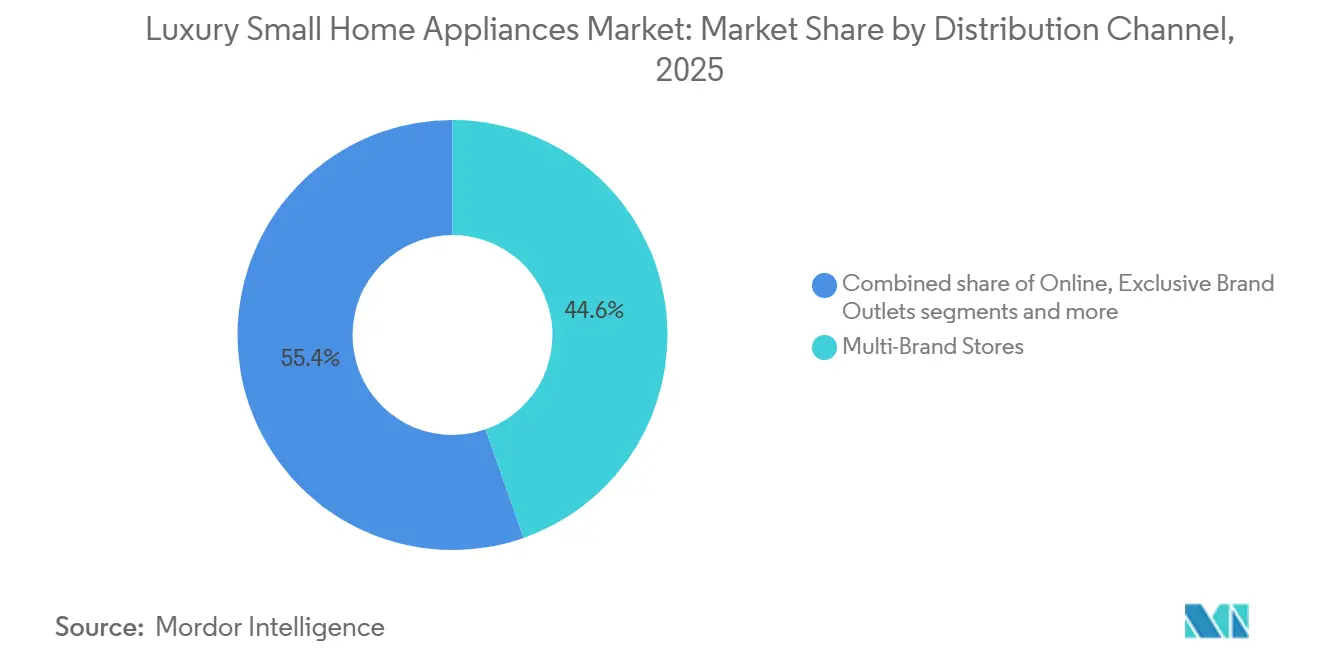

- By distribution channel, multi-brand stores accounted for 44.63% of the luxury small home appliances market in 2025, while online is projected to expand at a 6.83% CAGR through 2031.

- By geography, Europe captured a 35.41% share of the luxury small home appliances market size in 2025, while Asia-Pacific is forecast to grow at a 5.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Luxury Small Home Appliances Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise Of Affluent Millennial Homeowners In Asia-Pacific | +1.8% | Asia-Pacific core, spill-over to the Middle East | Medium term (2-4 years) |

| Smart-Kitchen Integration Boosting Appliance Upgrades | +1.5% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Premium Coffee Culture Expansion In North America And Europe | +1.2% | North America and Europe | Short term (≤ 2 years) |

| ESG-Driven Demand For Energy-Efficient Luxury Appliances | +0.9% | Europe and select Asia-Pacific markets | Long term (≥ 4 years) |

| Celebrity Chef And Influencer Endorsements Driving Aspirational Purchases | +0.6% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Growing HNW Refurbishment Of Secondary Residences Post-Pandemic | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise Of Affluent Millennial Homeowners In Asia-Pacific

Affluent millennial homeowners in Asia-Pacific are giving more attention to premium appliances as they furnish modern kitchens and living spaces in dense urban markets. The luxury small home appliances market benefits from this shift because younger high-income buyers are less focused on entry price and more focused on ease of use, product finish, and visible design value. India showed how quickly policy and income support can lift premium demand, as BSH reported that GST cuts introduced between September 2025 and January 2026 drove a major rise in dishwasher sales. That response matters because it shows that categories once treated as niche luxury purchases can move into broader premium adoption when income pressure eases. The same pattern supports the luxury small home appliances market across coffee, food preparation, and cleaning products, where first-time premium buyers often move from a single appliance purchase into a wider brand ecosystem over time.

Smart-Kitchen Integration Boosting High-Margin Appliance Upgrades

Connected features are no longer an optional extra at the upper end of the luxury small home appliances market, because buyers now expect premium devices to work with apps, save settings, and support automated routines. De'Longhi's April 2026 launch of the PrimaDonna Aromatic showed how brands are using Wi-Fi connectivity, bean-specific personalization, and recipe depth to justify a USD 2,499.95 price point[1]De'Longhi, “De'Longhi Unveils Its Most Advanced Espresso Machine Ever, Meet the PrimaDonna Aromatic,” PR Newswire, prnewswire.com. BSH also showed the scale of commitment needed in this area by investing USD 996.33 million (EUR 847 million) in R&D in 2025, equal to 5.6% of turnover, with continued work across connected and digital appliance capabilities[2]BSH Home Appliances Group, “Demonstrating Resilience, Investing in the Future, BSH Asserts Itself With a Turnover of 15 Euro Billion in 2025 in a Challenging Environment,” BSH Press Release, press.bsh-group.com. This matters for the luxury small home appliances market because connectivity is increasingly tied to after-sales engagement, software-based personalization, and stronger brand loyalty. It also creates a clearer gap between premium brands that can fund ecosystem development and smaller brands that still rely on standalone hardware appeal.

Premium Coffee Culture Expansion In North America And Europe

Premium home coffee preparation remains a significant factor influencing the demand within the luxury small home appliances market. The National Coffee Association reported in fall 2025 that a substantial portion of United States adults had consumed specialty coffee the previous day. That change supports a larger installed base for premium espresso machines, bean-to-cup systems, and related accessories because consumers now expect café-style output at home. Breville's August 2025 launch of the Oracle Dual Boiler at USD 2,999.95 showed that brands still see room for high-ticket, high-specification coffee equipment with advanced calibration, touchscreens, and connected features. For the luxury small home appliances market, the coffee category remains especially valuable because it combines repeat daily use, visible design value, and strong consumer willingness to trade up.

ESG-Driven Demand For Energy-Efficient Luxury Appliances

Energy efficiency is becoming a more visible part of premium appliance buying, especially among buyers who want performance, design quality, and lower long-term resource use from the same product. The luxury small home appliances market is affected by this trend because premium customers are more willing to pay for products that combine cleaner operation, better controls, and stronger build quality. Regulatory alignment also matters, since performance and safety standards continue to shape the way premium brands design new connected appliances for residential buyers and specifiers[3]International Electrotechnical Commission, “Household and Similar Electrical Appliances, Performance Standards,” International Electrotechnical Commission, iec.ch. In practice, this favors brands with the engineering depth to redesign platforms rather than make minor cosmetic updates. It also supports the luxury small home appliances market over the long term because compliance, energy signaling, and premium design increasingly move together rather than acting as separate purchase factors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Constraints In Precision Components | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| High Import Tariffs On Finished Appliances In Emerging Economies | -0.6% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Threat Of Counterfeit Premium Brands Online | -0.5% | Global, acute in Asia-Pacific online channels | Medium term (2-4 years) |

| Saturation Of Urban Markets In Western Europe | -0.4% | Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Constraints In Precision Components

The luxury small home appliances market relies on specialized parts, such as advanced motors, sensors, digital control modules, and precision grinding components, which are not easy to replace quickly. When those inputs tighten, premium brands face longer lead times, narrower model choice, and a harder balance between pricing and margin protection. The April 2026 Electrolux and Midea partnership in North America showed how important manufacturing scale, sourcing depth, and R&D support have become in a market that now places more value on supply resilience. Smaller premium labels are more exposed because they often lack the volume needed to secure priority access to constrained components or diversify production quickly. This can reduce assortment breadth in the luxury small home appliances market, particularly in slower-moving niche models where the cost of disruption is harder to absorb.

Threat Of Counterfeit Premium Brands Online

Counterfeit premium products remain a direct drag on the luxury small home appliances market, undermining trust, eroding perceived exclusivity, and complicating online conversion for high-value items. The OECD and EUIPO identified online platforms and small-parcel logistics as the main routes for counterfeit goods in global trade, which is especially important because online is also one of the fastest-growing routes for premium appliance sales. The same source base also linked large-scale counterfeit complaints during major shopping events to home appliances and consumer electronics, showing that the issue is not limited to fashion or accessories[4]OECD and EUIPO, “Mapping Global Trade in Fakes 2025,” OECD Publications, oecd.org. In the luxury small home appliances market, the real damage goes beyond lost unit sales because counterfeit exposure can undermine the price logic of products that depend on craftsmanship, reliability, and branded ownership experience. That makes authentication tools, direct channels, and controlled post-purchase service more important in preserving premium positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Coffee Machines Lead; Robotic Cleaners Extend the Growth Story

Premium coffee machines accounted for 28.92% of the luxury small home appliances market share in 2025, making them the largest product category by value. Their lead reflects how strongly home coffee rituals now connect with status, convenience, and design-led kitchen upgrades. The National Coffee Association reported in Fall 2025 that 48% of American adults had consumed specialty coffee in the past day, supporting steady demand for better home-brewing equipment. Breville's Oracle Dual Boiler and De'Longhi's PrimaDonna Aromatic show that the upper tier still supports price points well above USD 2,000 when brands combine automation, personalization, and premium build quality. Food processors, luxury blenders, and ovens constitute the next layer of demand, as affluent households increasingly treat the kitchen as both a performance and a design space.

Juicers, high-end toasters, and electric grills and roasters remain useful entry points into the luxury small home appliances industry, as they allow brands to reach premium buyers at lower ticket prices. Air fryers also have a growing premium niche as design-led brands bring better materials and stronger visual appeal into a category once dominated by function-first products. Within product categories, the luxury small home appliances market size for robotic and cordless vacuum cleaners is projected to expand at a 5.83% CAGR through 2031, the fastest rate in the portfolio. Dyson's March 2026 Spot+Scrub AI launch and its June 2026 V16 Piston Animal launch show how the cleaning category is moving toward stronger automation, smarter sensing, and faster feature refresh cycles. Luxury irons, garment steamers, and kettles continue to round out the mix as design-consistent extension products that help premium brands deepen household presence without relying on a single flagship appliance.

By Distribution Channel: Multi-Brand Stores Hold Scale; Online Builds Faster Premium Reach

Multi-brand stores held a 44.63% share of the luxury small home appliances market in 2025, maintaining their lead among channels. This position reflects the continued value of physical comparison, in-person demonstration, and guided selling for products that often cost more than USD 1,000. Buyers in the luxury small home appliances market still want to feel the finish quality, assess design fit, and compare feature sets before committing to a premium purchase. That is especially true for coffee machines, food preparation appliances, and robotic cleaning systems, where hands-on explanations can reduce hesitation and improve conversion rates. Exclusive brand outlets remain important in parallel because they enable premium labels to protect pricing, control service quality, and deliver a fully branded ownership experience from first visit to after-sales support.

Other routes, such as specification through luxury residential projects and interior design channels, also matter because appliance choices are increasingly made early in the home planning process. Online is projected to grow at a 6.83% CAGR through 2031, making it the fastest-growing channel in the luxury small home appliances market. That growth is supported by affluent digital buyers who are more comfortable completing high-value purchases through brand websites when images, product videos, reviews, and service terms are clear. In the luxury small home appliances industry, direct online storefronts are becoming increasingly valuable because they allow brands to bundle accessories, consumables, subscription support, and product education without relying on third-party marketplace control.

Geography Analysis

Europe accounted for 35.41% of the luxury small home appliances market size in 2025, making it the largest regional contributor. The region benefits from strong coffee culture, established specialty retail networks, and a long history of consumer comfort with premium kitchen and cleaning brands. Germany, the United Kingdom, France, Italy, and Spain remain the main demand centers because they combine higher spending power with mature premium retail distribution. BSH reported that built-in appliances in Europe rose 4% in 2025 despite a difficult operating backdrop, which supports the view that premium household demand remained resilient. Even so, parts of Western Europe, especially the BENELUX and the Nordics, now look more upgrade-driven than expansion-led because premium penetration is already high in urban households.

Asia-Pacific is forecast to expand at a 5.71% CAGR through 2031, making it the fastest-growing regional market for luxury small home appliances. The region is being lifted by rising wealth, the formation of urban premium households, and a broader willingness to spend on visible lifestyle products. India stands out because BSH reported 7% growth in 2025, with built-in steam oven demand rising 30%, suggesting a broadening premium buyer base. China remains central because urban affluent consumers treat premium appliances as a clear marker of lifestyle quality. At the same time, Japan and South Korea continue to contribute high value per unit through engineering-led preferences. Southeast Asia is also becoming more important as premium smart-home and robotic cleaning adoption spreads from advanced city markets into adjacent countries.

North America remained the second-largest market, with premium demand tied closely to high-income home construction, remodeling, and kitchen upgrade activity. BSH North America reported revenue growth of more than 5% in USD in 2025, with Gaggenau and Thermador driving the performance. South America still contributes on a smaller scale, with Brazil and Chile acting as the main premium appliance hubs despite tariff and currency friction. The Middle East and Africa remain earlier-stage premium markets, led by the UAE and Saudi Arabia, where luxury residential development and higher household spending continue to support future specification potential.

Competitive Landscape

The luxury small home appliances market remains moderately concentrated at the top, with a group of heritage brands and engineering-led specialists holding the strongest brand recognition and pricing power. The leading names compete on product quality, design identity, service credibility, and the ability to extend premium branding across multiple appliance categories. De'Longhi used product design and connectivity to reinforce that position when it launched the PrimaDonna Aromatic in April 2026, highlighting both Red Dot and iF design recognition ahead of the launch. BSH reinforced its premium defense with USD 996.33 million (EUR 847 million) in R&D spending in 2025, showing that scale, digital capability, and ongoing product refinement remain central to long-term brand strength. In the luxury small home appliances market, that investment gap matters because buyers increasingly expect strong software, refined automation, and consistent ecosystem support rather than only attractive hardware.

SharkNinja showed how a faster-moving challenger can still gain ground, with full-year 2025 net sales of USD 6,399.2 million, up 15.7% year on year, and Beauty and Home Environment Appliances growing more than 45%. That performance suggests that the luxury small home appliances market still rewards rapid launch cadence and international expansion when brand awareness and product function improve together. Electrolux and Midea also responded to margin and supply pressure through a strategic partnership in North America in April 2026, combining Electrolux's channel reach with Midea's manufacturing and R&D scale. Dyson's 2026 launches in robotic and cordless cleaning show another route to advantage, where repeated upgrades help premium brands keep pace with shifting consumer expectations. This keeps competitive pressure high even when the top tier is relatively stable.

A major structural shift in the luxury small home appliances market is the rise of premium Asian challengers, especially in robotic cleaning, where product intelligence and feature speed can quickly narrow legacy brand advantages. That change does not remove the value of heritage positioning, but it does force established brands to defend quality claims with real product performance and faster innovation cycles. Compliance and product standards also matter more in premium channels because residential specifiers and hospitality buyers increasingly assess safety, efficiency, and system compatibility together. IEC. The result is a market where a smaller group of well-funded brands controls much of the premium narrative. However, a wider set of challengers can still win share when they combine credible design, strong technology, and disciplined channel execution.

Luxury Small Home Appliances Industry Leaders

De’Longhi Group

Breville Group Limited

Dyson Ltd

SEB Groupe (Krups, Tefal)

Miele & Cie. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dyson launched the V16 Piston Animal cordless vacuum at USD 979 (USD 1,099 for the Submarine™ variant). The machine's All Floor Cones™ Sense cleaner head ejects hair directly into the bin and adapts suction intelligently—reinforcing Dyson's leadership in premium cordless cleaning and directly challenging Dreame's rising market share.

- May 2026: Dyson announced the V10 Konical and Auto-empty Dok™, the company's first self-emptying cordless vacuum system. The dock automatically transfers debris into a sealed bin liner holding up to 60 days of dirt. It integrates HEPA filtration during emptying, targeting the ultra-convenience tier of luxury home cleaning.

- April 2026: De'Longhi unveiled the PrimaDonna Aromatic at USD 2,499.95. Featuring Bean Adapt Technology, Cold Extraction Technology for cold brew in under 3 minutes, and Wi-Fi connectivity via the My Coffee Lounge app—and holding both the 2025 Red Dot Design Award and the iF Design Award—this is De'Longhi's most advanced super-automatic espresso machine to date.

- April 2026: Electrolux Group and Midea Group announced a strategic partnership in North America, combining Electrolux's distribution infrastructure and consumer insights with Midea's manufacturing scale and R&D, building on a 20-year sourcing relationship to accelerate growth and supply-chain resilience.

Global Luxury Small Home Appliances Market Report Scope

Luxury small home appliances are premium consumer electronics engineered to deliver superior performance, advanced technological integration, aesthetic elegance, and enhanced durability. Unlike mass-market alternatives, which prioritize basic functionality and cost efficiency, luxury appliances feature high-end materials, sophisticated design elements, advanced automation, and artisanal craftsmanship. The luxury small home appliances market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into premium coffee machines, high-end food processors, luxury blenders, juicers, high-end toasters, ovens, electric grills and roasters, air fryers, robotic & cordless vacuum cleaners, luxury irons & garment steamers, electric kettles, and others (waffle makers, ice-cream makers, stand mixers, etc.). By distribution channel, the market is segmented into multi-brand stores, exclusive brand outlets, online, and other distribution channels. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. The report provides the market size in USD for all the above-mentioned segments.

| Premium Coffee Machines |

| High-end Food Processors |

| Luxury Blenders |

| Juicers |

| High-End Toasters |

| Ovens |

| Electric Grills and Roasters |

| Air Fryers |

| Robotic & Cordless Vacuum Cleaners |

| Luxury Irons & Garment Steamers |

| Electric Kettles |

| Others (waffle makers, ice-cream makers, stand mixers, etc.) |

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Premium Coffee Machines | |

| High-end Food Processors | ||

| Luxury Blenders | ||

| Juicers | ||

| High-End Toasters | ||

| Ovens | ||

| Electric Grills and Roasters | ||

| Air Fryers | ||

| Robotic & Cordless Vacuum Cleaners | ||

| Luxury Irons & Garment Steamers | ||

| Electric Kettles | ||

| Others (waffle makers, ice-cream makers, stand mixers, etc.) | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for luxury small home appliances?

The category is forecast to reach USD 30.54 billion by 2031, up from USD 22.14 billion in 2026, with a 6.64% CAGR over 2026-2031.

Which product group leads premium demand?

Premium coffee machines led with 28.92% value share in 2025, supported by strong home coffee habits and continued high-end product launches.

Which category is growing fastest through 2031?

Robotic and cordless vacuum cleaners are projected to post the fastest growth at a 5.83% CAGR, helped by rapid advances in automation and sensing.

Why does Europe remain the largest regional contributor?

Europe held a 35.41% share in 2025, driven by a strong coffee culture, mature premium retail networks, and steady demand for design-led home upgrades.

Why is Asia-Pacific the main growth engine?

Asia-Pacific is forecast to grow at 5.71% CAGR through 2031 as wealth creation expands the base of first-time premium buyers across major urban markets.

What are the biggest risks facing premium appliance brands?

Supply constraints in precision components, counterfeit sales on online platforms, and saturation in mature Western European urban markets remain the most visible pressures.

Page last updated on: