Lung Cancer Screening Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.67 Billion |

| Market Size (2031) | USD 8.18 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

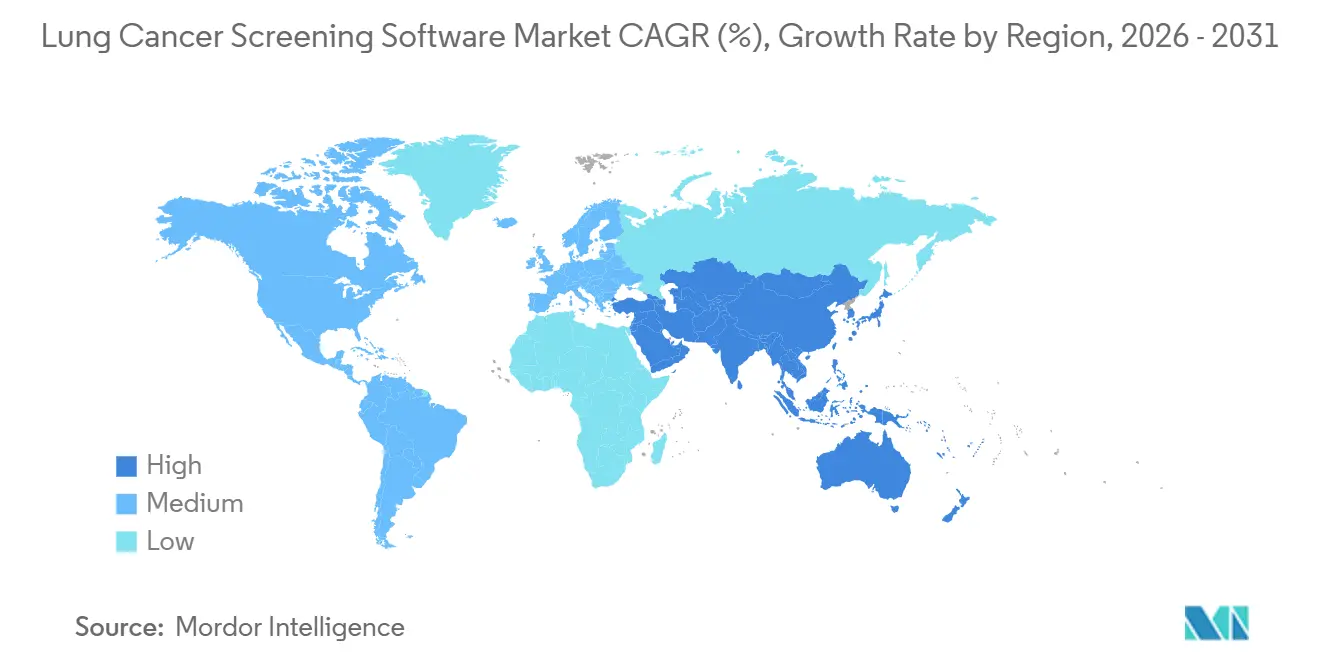

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lung Cancer Screening Software Market Analysis by Mordor Intelligence

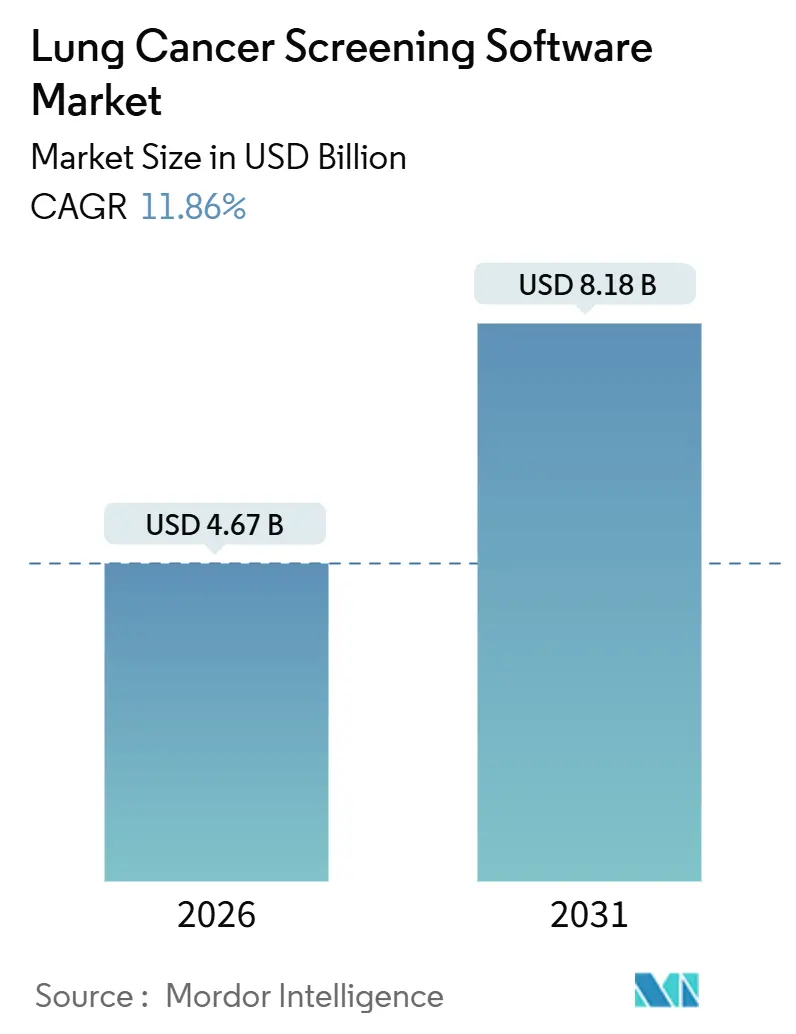

The Lung Cancer Screening Software Market size is estimated at USD 4.67 billion in 2026, and is expected to reach USD 8.18 billion by 2031, at a CAGR of 11.86% during the forecast period (2026-2031).

Widening low-dose computed-tomography (LDCT) mandates, U.S. and European regulatory clearances for deep-learning modules, and cloud-native deployment models are converging to accelerate adoption. U.S. Medicare’s 2022 rule that lowered the screening age to 50 immediately expanded the eligible population, stimulating sustained demand for automated nodule-workflow tools. Between 2024 and 2025, the U.S. FDA cleared several AI engines, including Qure.ai’s qXR-LN and V5med’s Lung AI, validating algorithmic performance that now rivals that of subspecialty radiologists in early-stage lesion detection. Cloud subscription pricing has removed the capital barrier for community hospitals, while payer mandates for registry reporting are driving the adoption of end-to-end patient navigation modules.

Key Report Takeaways

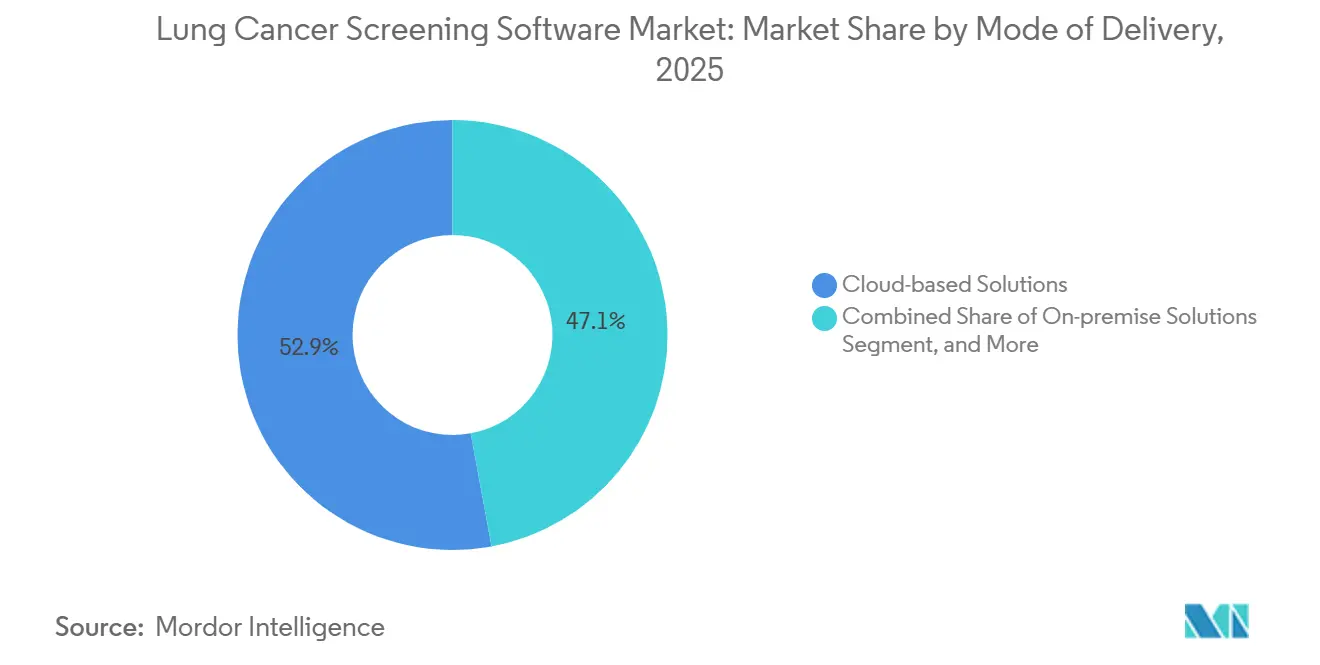

- By mode of delivery, cloud-based solutions held 52.91% of the lung cancer screening software market share in 2025; on-premise alternatives are forecast to trail as cloud expands at a 12.07% CAGR to 2031.

- By product, radiology and CADe software accounted for 36.73% of the lung cancer screening software market size in 2025, while patient-navigation modules are advancing at a 12.95% CAGR through 2031.

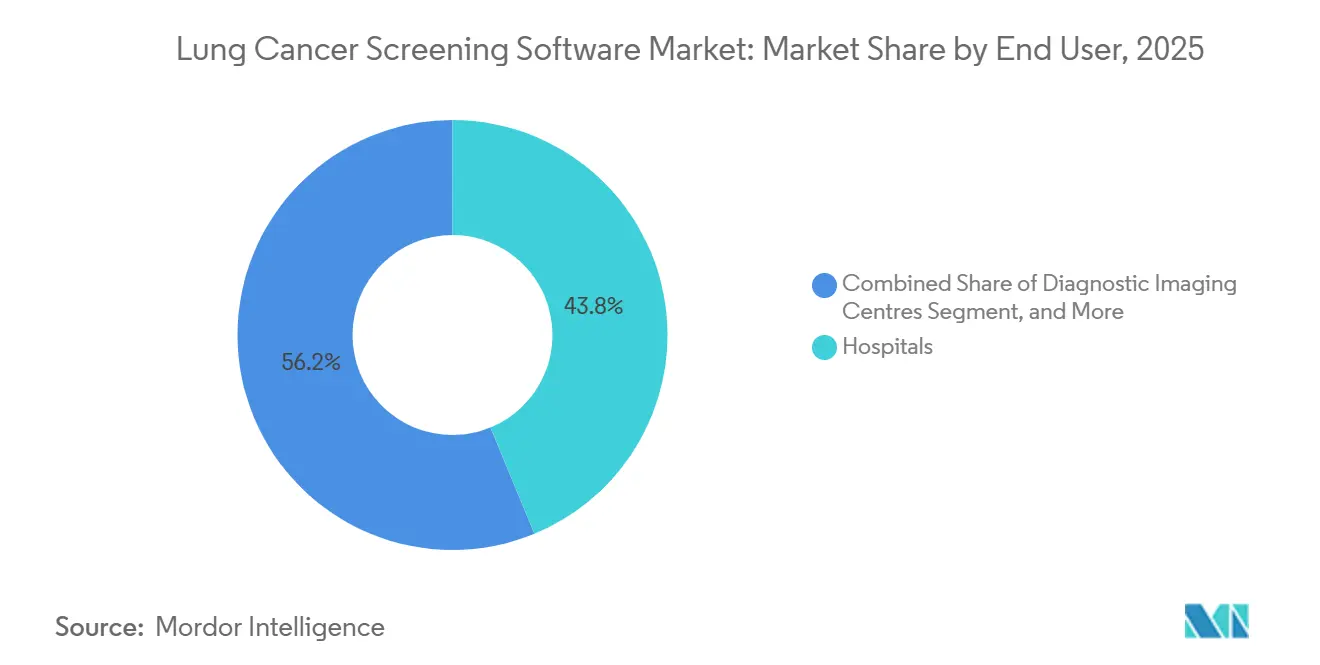

- By end user, hospitals led with 43.76% of revenue in 2025; diagnostic imaging centers are the fastest-growing channel at a 14.13% CAGR to 2031.

- By geography, North America accounted for 45.53% of revenue in 2025; Asia-Pacific is projected to expand at a 13.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lung Cancer Screening Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global lung-cancer incidence and LDCT expansion | +2.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| AI breakthroughs improving nodule detection | +2.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Government and payer reimbursement | +2.1% | North America and Germany, pilots in Japan and Australia | Medium term (2-4 years) |

| Cloud-SaaS delivery lowering CAPEX | +1.9% | Global, strongest in North America and Western Europe | Short term (≤ 2 years) |

| End-to-end registry & patient navigation | +1.4% | North America, selective in Europe | Medium term (2-4 years) |

| Federated-learning collaborations | +1.1% | Research hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Lung-Cancer Incidence & Expansion of LDCT Screening Programmes

Lung cancer remains the leading cause of cancer mortality worldwide, and aging populations, coupled with persistent smoking rates in emerging economies, keep incidence on an upward slope. U.S. Medicare’s 2022 eligibility expansion instantly brought an additional 6.4 million adults into the annual screening pool.[1]Centers for Medicare & Medicaid Services, “Lung Cancer Screening,” cms.gov Germany’s HANSE trial and the United Kingdom’s Targeted Lung Health Check program have demonstrated early-stage detection rates above 70%, galvanizing European payers to evaluate nationwide roll-outs. China’s tier-1 cities have launched AI-enabled pilots that offset local radiologist shortages and create large-scale demand for automated registry tools. As these initiatives mature, software that quantifies nodules, tracks interval growth, and generates structured Lung-RADS reports becomes indispensable to meeting quality metrics.

AI/Deep-Learning Breakthroughs Improving Nodule-Detection Accuracy & Workflow

Convolutional neural-network models trained on multinational datasets are now sensitive to nodules ≥3 mm with ≥90% accuracy, slashing historical false-negative rates. The FDA cleared Qure.ai’s qXR-LN in Jan 2024 and qCT LN Quant in Aug 2024, both of which were validated across ethnically diverse cohorts to mitigate bias.[2]U.S. Food and Drug Administration, “510(k) Premarket Notification,” fda.gov V5med’s Lung AI received clearance in Mar 2025, and AZmed’s AZnod followed in Dec 2025, signaling regulatory comfort with AI-assisted triage. Peer-reviewed studies show that AI can cut radiologist interpretation time by up to 40% while reducing false positives by 20-30%, allowing staff to focus on complex assessments.[3]Radiological Society of North America, “Radiology,” rsna.org European CE marking under the Medical Device Regulation framework further broadens marketable geographies.

Government & Payer Reimbursement for Lung-Cancer Screening

Coverage policies dictate adoption velocity. Medicare reimburses annual LDCT without patient cost-sharing when providers complete shared decision-making visits and push structured results to CMS-approved registries. Germany funds screening under insurer pilot contracts, and Japan’s private payers began covering scans for high-risk adults in 2024. Australia’s 2025 benefit-schedule addition opened public funding, though eligibility remains narrower than in the United States. Conversely, many emerging markets still lack billing codes, forcing vendors to rely on hospital capital budgets rather than fee-for-service payments.

Cloud-SaaS Delivery Lowering CAPEX for Small & Mid-Size Providers

Subscription-based deployment removes six-figure up-front hardware fees and lets facilities pay only for active users and storage. GE HealthCare’s cloud-native PACS scales elastically, Philips and Mass General Brigham proved multi-vendor interoperability across 12 hospitals in 2025, and Siemens Healthineers’ AI-Rad Companion now updates models overnight through secure web portals. NIST Special Publication 1800-24 provides an encryption and audit-logging playbook that de-risks cloud connectivity compliance. As 5G backbones and hospital edge appliances mature, even rural imaging centers can adopt sophisticated algorithms without local servers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation & PACS/RIS integration costs | -1.6% | Global, most acute in mid-size hospitals | Short term (≤ 2 years) |

| Data-privacy / cyber-security compliance | -1.2% | Strictest in EU and North America | Medium term (2-4 years) |

| Limited reimbursement outside U.S. and Germany | -1.0% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Scanner-protocol variability | -0.8% | Multi-vendor hospital networks worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation & PACS/RIS Integration Costs

Mid-size hospitals running legacy image archives frequently need middleware that translates DICOM tags, routes studies to cloud endpoints, and returns annotated images to radiologist worklists. Total integration outlays can exceed USD 500,000 once HL7 FHIR interfaces, firewall upgrades, and radiologist training are included. Vendors lacking ready connectors for dominant PACS brands must endure extended CIO vetting and custom builds that delay ROI. Temporary workflow slowdowns during go-live windows further discourage administrators who prioritize throughput over incremental improvements in accuracy.

Data-Privacy / Cyber-Security Compliance & Liability Exposure

Hospitals that send CT images to external AI servers must satisfy HIPAA’s encryption-in-transit rules and GDPR’s data-protection-impact-assessment mandates. In 2024, the U.S. HHS levied fines up to USD 1.5 million per violation category for gaps in business-associate agreements, while GDPR penalties can hit EUR 20 million or 4% of global turnover, whichever is higher. A spike in ransomware attacks on radiology networks prompted insurers to raise cyber-liability premiums and forced hospitals to conduct penetration testing before activating AI integrations. Vendors that store identifiers in low-sovereignty jurisdictions risk contract cancellations if breaches occur.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Delivery: Cloud Dominance Reshapes Capital Planning

Cloud-based deployments held 52.91% of the lung cancer screening software market share in 2025 and are on track for a 12.07% CAGR to 2031. The lung cancer screening software market for cloud solutions is projected to grow over the forecast horizon, supported by pay-as-you-go subscriptions that appeal to community hospitals. Hospitals avoid local server purchases, and IT departments benefit from overnight model updates pushed by vendors such as Siemens Healthineers and Philips that guarantee the latest weights without manual patching. 5G backbone roll-outs and edge caching now mitigate latency concerns even for rural imaging centers.

On-premise platforms remain necessary in jurisdictions with strict data localization rules or where chief information security officers prohibit external uploads. Web-based hybrids host inference engines on vendor servers but keep images on-site, offering a compliance middle ground. NIST’s SP 1800-24 blueprint helps institutions harden cloud endpoints and has shortened purchasing cycles by clarifying requirements for encryption, audit logging, and access controls. As CIOs refresh infrastructure over the next four years, hybrid cloud plus edge-appliance configurations are expected to dominate multi-site radiology groups.

By Product: Patient Navigation Modules Outpace Detection Software

Radiology and CADe engines commanded 36.73% of 2025 revenue, underscoring their role as the clinical backbone of the lung cancer screening software market. Yet registry-ready patient-navigation suites are growing 2.5 percentage points faster, reflecting CMS rules that tie payment to structured data submission.

ACR’s 2024 Lung-RADS update spurred software revisions that integrate volumetric thresholds and track nodule growth across serial scans. Optellum’s Virtual Lung Clinic already bundles risk stratification, MDT dashboards, and patient portals, while Aidence’s Veye Lung Nodules exports one-click structured reports directly into electronic medical records. Hospitals that miss registry deadlines risk CMS penalties, making integrated navigation a compliance imperative.

By End User: Imaging Centers Scale Faster Than Hospitals

Hospitals generated 43.76% of 2025 revenue, reflecting their dominant scan volumes and in-house radiology teams. However, diagnostic imaging centers, the next-largest cohort, are growing at a 14.13% CAGR. Cloud subscriptions eliminate high up-front costs, making sophisticated AI affordable to independent centers that compete on service differentiation. Qure.ai’s qXR-LN and qCT LN Quant, cleared in 2024, are specifically designed for imaging centers that lack thoracic subspecialists but wish to market LDCT screening services.

Oncology centers integrate screening pipelines with treatment-planning systems for seamless patient handoffs once biopsies confirm malignancy. Ambulatory surgical centers lag due to limited IT budgets and lower scan throughput. In China, Infervision’s InferRead CT Lung anchors rural county-hospital programs where subspecialty radiologists are scarce, offering a template for adoption in emerging markets. As value-based care contracts expand, all provider types must document detection rates and diagnostic timeliness, metrics that AI systems can automatically capture.

Geography Analysis

North America captured 45.53% of 2025 revenue, buoyed by Medicare coverage that removes patient co-pays and by a vibrant AI startup ecosystem clustered around Boston, Silicon Valley, and Madison. Canada’s Ontario and British Columbia pilots showed promising early detection outcomes, although national guidelines remain pending. U.S. vendors often bundle software with scanner upgrades, accelerating refresh cycles.

Europe ranked second in 2025, led by Germany’s insurer-funded pilots and the U.K.’s mobile CT fleets that visit underserved areas. CE-marked algorithms comply with the EU Medical Device Regulation, yet varying national reimbursement policies slow broad deployment, particularly in France and Spain.

Asia-Pacific is the fastest-growing territory at a 13.93% CAGR through 2031, underpinned by China’s city-level pilots, Japan’s guideline inclusion, and India’s private-hospital initiatives. InferRead CT Lung installations across Chinese county hospitals demonstrate viability in lower-resource settings, while Australia’s 2025 benefit-schedule item catalyzed uptake among radiology groups. South Korea’s national insurance program added LDCT for high-risk adults in 2024, providing vendors with an early revenue stream.

Middle East & Africa and South America remain nascent. Gulf states invest in high-end imaging for medical tourism but lack population screening mandates. Brazil and Argentina rolled out small pilots in 2025, yet face budget constraints that limit scale, suggesting a gradual revenue ramp into the next decade.

Competitive Landscape

The lung cancer screening software market is moderately fragmented. Imaging-equipment majors GE HealthCare, Siemens Healthineers, Philips, Canon Medical, and Fujifilm leverage installed CT bases to upsell bundled AI suites, securing multi-year service contracts. GE HealthCare’s 2024 launch of the Vscan Air CL handheld ultrasound and Siemens’ Naeotom Alpha photon-counting CT highlight a strategy to fuse hardware and software ecosystems.

Pure-play AI firms Aidence, Optellum, Qure.ai, and Infervision compete on algorithm precision and open APIs that integrate with leading PACS. Optellum won a 2024 U.S. patent for its risk-stratification engine that merges nodule morphology with demographics. Vendors lacking turnkey connectors for Fujifilm Synapse, GE Centricity, or Philips IntelliSpace endure longer procurement cycles as hospitals validate interoperability.

White-space opportunities abound in ambulatory surgical centers and in emerging regions where pay-per-scan licensing could offset absent reimbursement. Federated-learning initiatives, exemplified by the U.S. National Cancer Institute’s 10-site network, enable collaborative model training without central data pooling, reducing privacy concerns and enabling cross-border deployments.

Lung Cancer Screening Software Industry Leaders

Fujifilm Holdings Corporation

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Qure.ai

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: AZmed secured CE marking for AZnod, a subscription-priced nodule detector aimed at ambulatory surgical centers lacking thoracic subspecialists.

- November 2025: Qure.ai partnered with 20 U.S. community hospitals to deploy qXR-LN and qCT LN Quant across emergency departments, aiming to screen 500,000 patients annually under a shared-savings contract that ties vendor fees to early-stage detection rates.

- April 2025: V5med obtained FDA 510(k) clearance for Lung AI after an eight-center trial cut false-positive callbacks by 35% relative to unassisted reads.

- February 2025: Philips launched a multi-year collaboration with Mass General Brigham to deploy cloud-based AI across 12 hospitals and to co-develop federated-learning workflows.

Global Lung Cancer Screening Software Market Report Scope

| Cloud-based Solutions |

| On-premise Solutions |

| Web-based Solutions |

| Radiology/CADe Software |

| Nodule-Management Modules |

| Patient-Management & Navigation |

| Other Products (Screening PACS, Data Collection & Reporting, among others) |

| Hospitals |

| Diagnostic Imaging Centres |

| Oncology Centres |

| Ambulatory Surgical Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Mode of Delivery | Cloud-based Solutions | |

| On-premise Solutions | ||

| Web-based Solutions | ||

| By Product | Radiology/CADe Software | |

| Nodule-Management Modules | ||

| Patient-Management & Navigation | ||

| Other Products (Screening PACS, Data Collection & Reporting, among others) | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centres | ||

| Oncology Centres | ||

| Ambulatory Surgical Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the lung cancer screening software market expected to grow through 2031?

It is forecast to grow at a 11.86% CAGR, rising from USD 4.67 billion in 2026 to USD 8.18 billion by 2031.

Which delivery model is gaining the most traction for lung screening software?

Cloud-based deployments lead with 52.91% share in 2025 and are expanding at a 12.07% CAGR as hospitals shift away from on-premise servers.

Which segment is advancing the fastest within product categories?

Patient navigation modules are growing at 12.95% annually because payers require registry data and documented shared decision-making.

Which region is forecast to be the fastest-expanding market?

Asia-Pacific, driven by China’s urban pilots and Japan’s guideline inclusion, is expected to grow at 13.93% per year through 2031.

What is the main barrier to adoption outside North America and Germany?

Absence of dedicated reimbursement codes forces providers to rely on capital budgets, slowing uptake in many emerging markets.

Page last updated on: