Long QT Syndrome Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

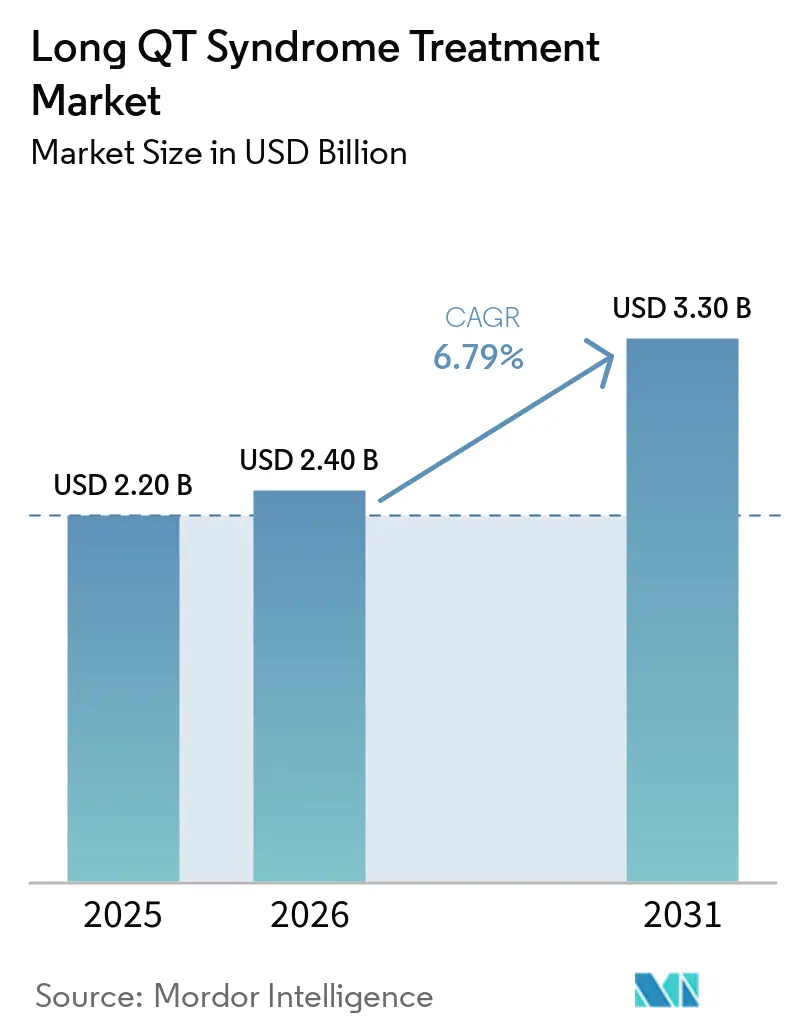

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 3.30 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

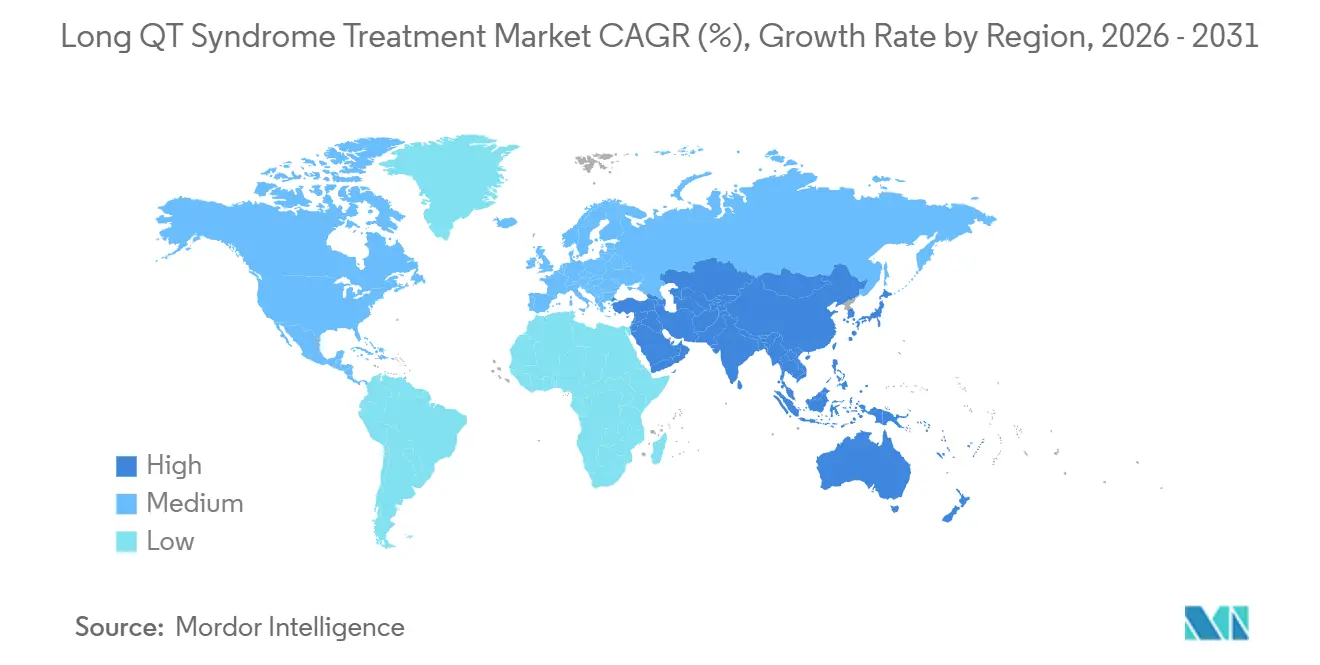

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long QT Syndrome Treatment Market Analysis by Mordor Intelligence

The Long QT Syndrome Treatment Market size is expected to grow from USD 2.20 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 3.30 billion by 2031 at 6.79% CAGR over 2026-2031.

Adoption of genotype-guided pharmacotherapy, expansion of video-assisted thoracoscopic left cardiac sympathetic denervation, and wider cascade family screening are jointly enlarging the treated population while reducing dependence on transvenous implantable cardioverter-defibrillators. Device makers are pivoting toward extravascular and subcutaneous ICD platforms that address pediatric anatomical constraints and bradycardia pacing needs. Generic competition in beta-blockers and mexiletine is compressing unit prices, yet precision therapies such as SGK1 inhibitors are attracting investment because they command premium pricing. North America remains the revenue anchor, but Asia-Pacific is growing the fastest as Japan and China build national genetic registries and subsidize screening programs. Remote monitoring ecosystems that pair Bluetooth-enabled devices with artificial-intelligence triage are improving adherence and curbing inappropriate shocks, which supports sustained device utilization [1]U.S. Food and Drug Administration, “QTc Information in Human Prescription Drug and Biological Product Labeling,” fda.gov.

Key Report Takeaways

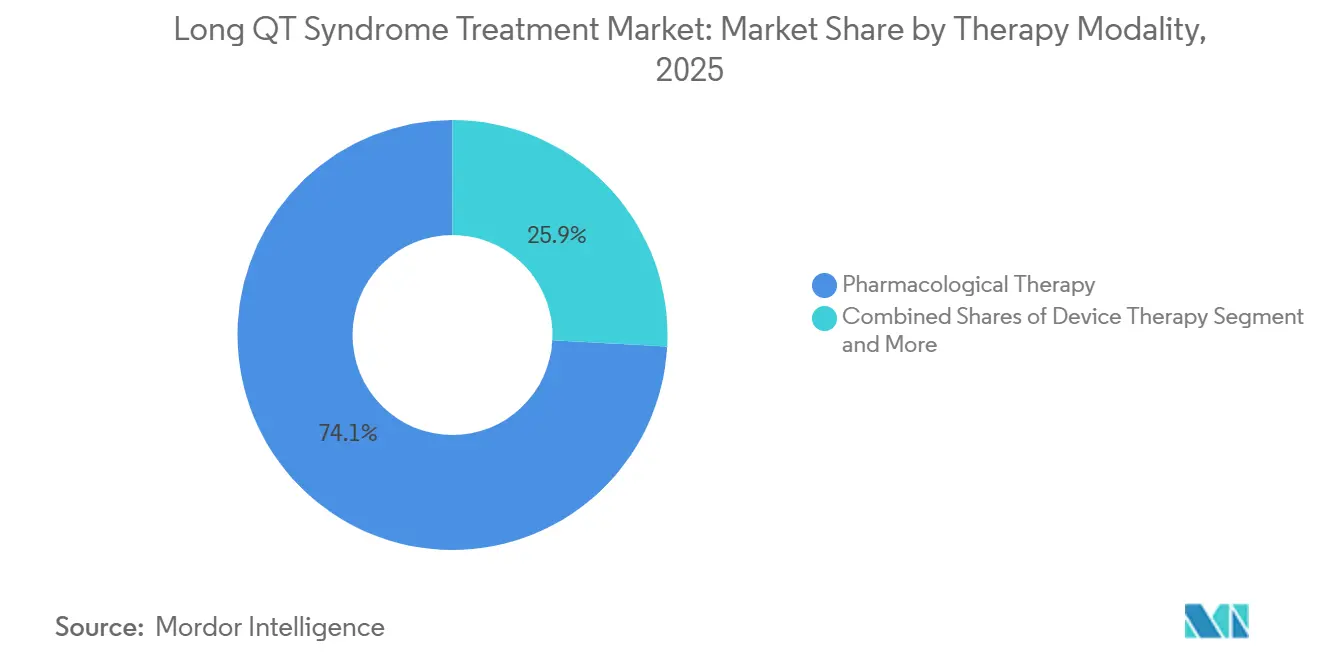

- By therapy modality, pharmacological treatment held 74.15% of the Long QT Syndrome Treatment market share in 2025, while surgical interventions are advancing at an 8.15% CAGR through 2031.

- By patient age group, adults contributed 68.38% revenue share in 2025, whereas pediatrics is projected to expand at a 7.93% CAGR to 2031.

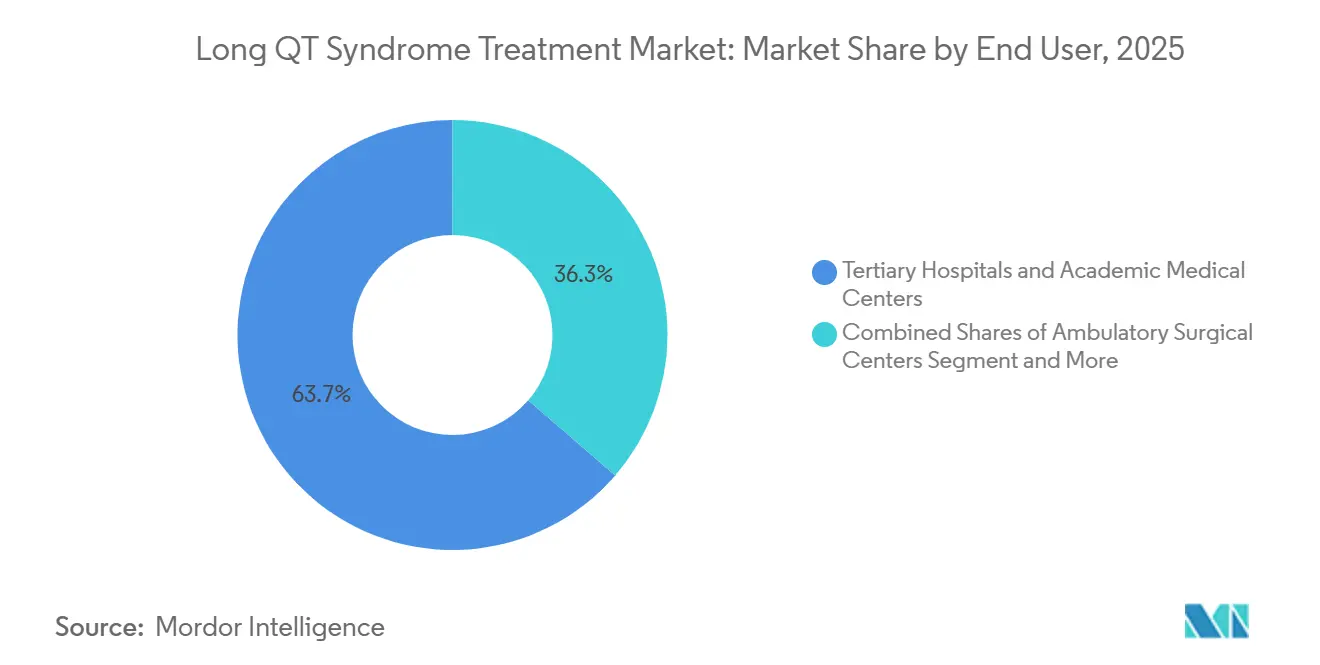

- By end user, tertiary hospitals and academic medical centers accounted for 63.66% of the Long QT Syndrome Treatment market size in 2025, and specialty arrhythmia centers are growing at an 8.39% CAGR through 2031.

- By geography, North America led with 43.17% revenue share in 2025, while Asia-Pacific is forecast to record an 8.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Long QT Syndrome Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Guideline-backed beta-blocker therapy | +1.2% | Global, highest adherence in North America and Europe | Long term (≥ 4 years) |

| Genotype-guided therapy adoption | +0.9% | North America, Europe, Japan, urban China and India | Medium term (2-4 years) |

| Expanding ICD use with subcutaneous systems | +1.1% | North America and Europe core, Asia-Pacific accelerating | Medium term (2-4 years) |

| Cascade genetic testing and earlier diagnosis | +0.8% | Japan, China, South Korea, North America, Europe | Long term (≥ 4 years) |

| Remote monitoring and digital follow-up | +0.6% | North America, Western Europe, pilot city programs in Asia-Pacific | Short term (≤ 2 years) |

| Emerging pipeline of ion-channel modulators | +0.7% | Global trials centered in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Guideline-Backed Beta-Blocker Therapy as Foundation of Care

Nonselective beta-blockers remain the cornerstone of congenital LQTS management across international cardiology guidelines. A 2025 network meta-analysis of 5,692 patients showed that nadolol reduced arrhythmic events more effectively than propranolol in LQT1 and delivered dose-dependent protection in LQT2 and LQT3, which is driving payer acceptance of higher-cost nadolol when measured against avoided cardiac arrests [2]Youxu Jiang et al., “Different Beta-Blockers for Preventing Arrhythmic Events,” Frontiers in Medicine, frontiersin.org. FDA labeling guidance mandating QTc data for non-antiarrhythmic drugs indirectly reinforces beta-blocker primacy by highlighting the risk of untreated QTc prolongation. Reliable global supply from Alembic, Kaken, and Daewoong ensures access, although quality audits of certain Chinese API facilities persist. Collectively, these factors underpin the sustained dominance of pharmacologic first-line care within the Long QT Syndrome Treatment market.

Genotype-Guided Therapy Adoption

Mexiletine has proven QT-shortening benefits in LQT3 patients with SCN5A variants and, according to a 2024 Circulation study, benefits selected LQT2 mutations as well, expanding its clinical utility. High-throughput patch-clamp and iPSC cardiomyocyte platforms allow laboratories to predict patient drug response, supporting precision prescribing. Generic competition from Teva, ANI, and Sun Pharma has driven unit cost below USD 1.50, removing price as an adoption barrier and making mexiletine a cost-effective adjunct to beta-blockers. Integration of genetic results into electronic health records in the United States and Japan automates therapy suggestions, though limited testing infrastructure slows uptake in lower-income regions. As variant-specific evidence enlarges, the Long QT Syndrome Treatment market sees genotype-guided therapy permeate beyond academic centers.

Expanding ICD Use with Shift Toward Subcutaneous ICDs in Channelopathies

The FDA approval of Medtronic’s Aurora extravascular ICD in 2023 introduced a lead pathway beneath the sternum that allows antibradycardia and antitachycardia pacing at lower shock energies, addressing historical limitations of subcutaneous systems[3]Yael L. Maxwell, “FDA Approves First Extravascular ICD,” TCTMD, tctmd.com. Clinical registries report fewer vascular complications compared with transvenous leads, an important consideration in pediatric and young adult cohorts. Boston Scientific’s Emblem S-ICD still commands a substantial installed base, but Aurora’s pacing capability is shifting physician preference in patients with pause-dependent torsades. Device demand is further supported by Medtronic's revenue growth of 7% in fiscal 2025, which underscores commercial traction for innovative rhythm-management hardware. Together, these dynamics sustain device momentum inside the Long QT Syndrome Treatment market despite debate over primary-prevention indications.

Cascade Genetic Testing and Earlier Diagnosis Expanding Treated Population

Japan’s nationwide registry achieved 98% genetic testing among 3,851 enrolled patients by 2025, doubling diagnosed prevalence and transforming silent gene carriers into therapy candidates. China and India report high rates of compound heterozygosity that portend severe phenotypes, underscoring the benefit of systematic screening. While test costs of USD 500-2,000 remain barriers in many countries, pilot programs in urban centers demonstrate feasibility and are attracting public-health funding. Broader identification of at-risk relatives enlarges the Long QT Syndrome Treatment market by lifting the ceiling on patient counts and fostering earlier intervention, which improves long-term outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small eligible patient pool | -0.8% | Global | Long term (≥ 4 years) |

| Genericization and price erosion in pharmacotherapy | -0.6% | North America, Europe, mature Asia-Pacific | Medium term (2-4 years) |

| Device cost and infrastructure gaps in low-income countries | -0.5% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Procedure and device complications | -0.4% | Global, intensified in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Small Eligible Patient Pool Limits Absolute Revenues

Clinical prevalence of 1 in 2,000 translates to 3-4 million potential patients worldwide, yet underdiagnosis keeps the actively treated population far smaller, which caps absolute revenue for device and drug suppliers. Payers scrutinize ICD spending in asymptomatic carriers when specialty-center data show mortality as low as 0.03% with optimized medical therapy and LCSD. Limited patient numbers also hamper randomized trial feasibility, forcing reliance on registries that regulators view as less robust. Consequently, revenue forecasts within the Long QT Syndrome Treatment market remain sensitive to small variations in diagnosis rates.

Genericization and Price Erosion in Pharmacotherapy

Loss of exclusivity for beta-blockers and mexiletine has driven prices to commodity levels, cutting per-patient revenue by more than 70% in some regions. Branded manufacturers have exited, leaving generic giants to compete on supply-chain efficiency. The resulting margin squeeze reduces industry willingness to fund large clinical trials, which slows the generation of new evidence that might otherwise expand indications or improve dosing algorithms. This price compression weighs on the pharmacologic portion of the Long QT Syndrome Treatment market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Modality: Pharmacological Dominates While Surgery Gains Momentum

Pharmacological therapy accounted for 74.15% of the Long QT Syndrome Treatment market in 2025, reflecting beta-blocker guideline dominance and expanding mexiletine use in mutation-specific cohorts. Surgical options, principally left cardiac sympathetic denervation, are growing at an 8.15% CAGR as specialty centers adopt video-assisted thoracoscopic techniques that avoid ICD complications. Device therapy remains essential for secondary prevention but faces re-evaluation of primary-prevention indications. Adjunctive acute management, such as wearable cardioverter-defibrillators, provides temporary protection yet contributes a minor revenue slice.

Clinical data from Mayo Clinic and Milan documented an 86% reduction in cardiac events post-LCSD, with sustained QTc improvement predicting long-term success. This outcome parity with ICDs, coupled with lower complication risk, is propelling surgical adoption among young high-risk patients. Pharmacotherapy continues to confront price erosion, yet its foundational role sustains share. Together, these shifts redefine therapeutic balance inside the Long QT Syndrome Treatment market size forecast.

By Patient Age Group: Adults Lead, Pediatrics Accelerate

Adults held 68.38% revenue share in 2025, driven by cumulative prevalence and higher device utilization, but pediatric cases are rising at a 7.93% CAGR through 2031 as cascade screening uncovers early-onset genotypes. Device miniaturization and extravascular lead pathways now permit implantation in smaller physiques, widening treatment eligibility among children.

Pediatric management emphasizes combination pharmacotherapy and LCSD to sidestep transvenous lead complications, yet adoption of Micra leadless pacemakers and Aurora ICDs is increasing in adolescents. Adult cohorts benefit from mature evidence bases but carry comorbidities that complicate therapy selection and device programming. Growing pediatric detection expands the Long QT Syndrome Treatment market by introducing lifelong therapy journeys that begin earlier.

By End User: Tertiary Hospitals Anchor, Specialty Centers Surge

Tertiary hospitals and academic centers captured 63.66% of 2025 revenue because they integrate genetic testing, electrophysiology, surgery, and psychological support under one roof. Specialty arrhythmia centers are expanding at an 8.39% CAGR as payers funnel complex device cases to high-volume teams that demonstrate fewer complications.

Ambulatory surgical centers are beginning to implant insertable monitors and perform LCSD on an outpatient basis, driven by reimbursement shifts away from inpatient care. Remote monitoring lets high-volume centers manage patients at a distance, extending reach without physical expansion. These models continue to grow the Long QT Syndrome Treatment market share of specialized facilities.

Geography Analysis

North America generated 43.17% of 2025 revenue, underpinned by broad ICD reimbursement, robust genetic testing networks, and established remote monitoring codes. Specialty centers in the United States pair device implantation with AI-driven follow-up, which lifts adherence and reduces inappropriate shocks. Canada leverages provincial rare-disease frameworks to fund cascade screening, though provincial variability affects uniformity of access.

Asia-Pacific is the fastest-growing region at an 8.41% CAGR as Japan’s national registry and China’s expanding tertiary network bring previously undiagnosed families into care. Japanese payers reimburse LCSD and subcutaneous ICDs, accelerating adoption, while China is localizing device manufacturing through partnerships with MicroPort. South Korea’s universal health system funds genetic testing panels, sustaining early diagnosis.

Europe benefits from centralized genomic programs and pan-EU registries that facilitate data sharing, but reimbursement heterogeneity delays therapy rollout in Southern and Eastern states. The Middle East and Africa and South America lag because of device cost and specialist shortages, limiting the Long QT Syndrome Treatment market size expansion despite growing awareness. MicroPort’s merger with CardioFlow is expected to introduce lower-cost ICDs that could improve penetration in these under-served regions.

Competitive Landscape

The long QT syndrome treatment market is moderately concentrated. Medtronic, Boston Scientific, and Abbott dominate devices, leveraging differentiated ICD platforms and proprietary remote-monitoring clouds. Medtronic’s Aurora EV-ICD edges ahead because it adds pacing functions without transvenous leads, while Boston Scientific maintains loyalty through the established Emblem S-ICD user base. Abbott competes with dual-chamber CRT-D systems that manage concomitant heart-failure patients.

Generic manufacturers such as Teva, Sun Pharma, and ANI own the pharmacologic space, competing mainly on price and distribution. This fragmentation suppresses margins but guarantees the supply of beta-blockers and mexiletine. Thryv Therapeutics introduces innovation with its SGK1 inhibitor, supported by the FDA Fast Track, and could change the therapy mix if late-stage trials succeed.

Emerging players aim for white spaces. MicroPort is integrating structural heart and rhythm portfolios to undercut Western pricing in Asia. ZOLL’s LifeVest addresses interim protection needs, and Biotronik is extending its European ICD footprint into emerging markets. Genetic testing firms Invitae and GeneDx partner with device companies to boost cascade screening uptake. This ecosystem continues to evolve, yet device majors retain scale advantages in manufacturing and regulatory compliance.

Long QT Syndrome Treatment Industry Leaders

Medtronic Plc

Boston Scientific Corporation

Abbott Laboratories

Teva Pharmaceutical Industries Ltd.

Sun Pharmaceutical Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Thryv Therapeutics received FDA Fast Track designation for THRV-1268 and opened a Phase 2/3 trial targeting QTc shortening across genotypes.

- December 2025: MicroPort CardioFlow completed its merger with MicroPort CRM to build an integrated cardiac solution platform aimed at emerging markets.

- December 2025: Thryv launched the myQTwave remote study using wearable ECG patches to monitor patients during THRV-1268 titration.

Global Long QT Syndrome Treatment Market Report Scope

As per the scope of the report, treatment for Long QT Syndrome (LQTS) focuses on managing the heart's electrical system to prevent life-threatening arrhythmias like Torsades de Pointes and reduce the risk of sudden cardiac death. For those with acquired LQTS, which is often triggered by external factors, the primary approach is to identify and address the underlying cause, such as stopping medications that prolong the QT interval or correcting electrolyte imbalances like low potassium or magnesium.

The long QT syndrome treatment market is segmented by therapy modality, patient age group, end-user, and geography. Based on therapy modality, the market is segmented into pharmacological therapy, device therapy, surgical therapy, and adjunctive/acute management. By patient age, the market is segmented into pediatric (≤17 years) and adult (≥18 years). By end users, the market is segmented into tertiary hospitals & academic medical centers, specialty arrhythmia centers/electrophysiology labs, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Pharmacological Therapy |

| Device Therapy |

| Surgical Therapy |

| Adjunctive/Acute Management |

| Pediatric (≤17 years) |

| Adult (≥18 years) |

| Tertiary Hospitals & Academic Medical Centers |

| Specialty Arrhythmia Centers / Electrophysiology Labs |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Modality | Pharmacological Therapy | |

| Device Therapy | ||

| Surgical Therapy | ||

| Adjunctive/Acute Management | ||

| By Patient Age Group | Pediatric (≤17 years) | |

| Adult (≥18 years) | ||

| By End User | Tertiary Hospitals & Academic Medical Centers | |

| Specialty Arrhythmia Centers / Electrophysiology Labs | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Long QT Syndrome Treatment market today, and where is it headed?

Long QT Syndrome Treatment market at USD 2.4 billion in 2026 and expects it to reach USD 3.3 billion by 2031, reflecting a 6.79% CAGR through 2031.

Which type of therapy still leads the field?

Medicines remain the mainstay, holding 74.15% of 2025 revenue. Guideline-preferred beta-blockers and mutation-guided mexiletine drive most prescriptions, even as left cardiac sympathetic denervation is the fastest-rising option.

Why is Asia–Pacific growing faster than other regions?

National cascade-testing programs, Japan’s registry alone has screened almost 4,000 families, are uncovering previously silent cases. Combined with rising healthcare budgets in China and South Korea, this pushes Asia–Pacific toward the highest regional CAGR at 8.41% through 2031.

Who are the big names to watch?

Medtronic, Boston Scientific, and Abbott dominate devices, while Teva, ANI Pharmaceuticals, and Sun Pharma supply most generic drugs. Pipeline activity centers on Thryv Therapeutics, whose SGK1 inhibitor (THRV-1268) secured FDA Fast Track status in 2026.

Page last updated on: