Long-Haul and Metro Fiber Backbone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.32 Billion |

| Market Size (2031) | USD 50.12 Billion |

| Growth Rate (2026 - 2031) | 13.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long-Haul and Metro Fiber Backbone Market Analysis by Mordor Intelligence

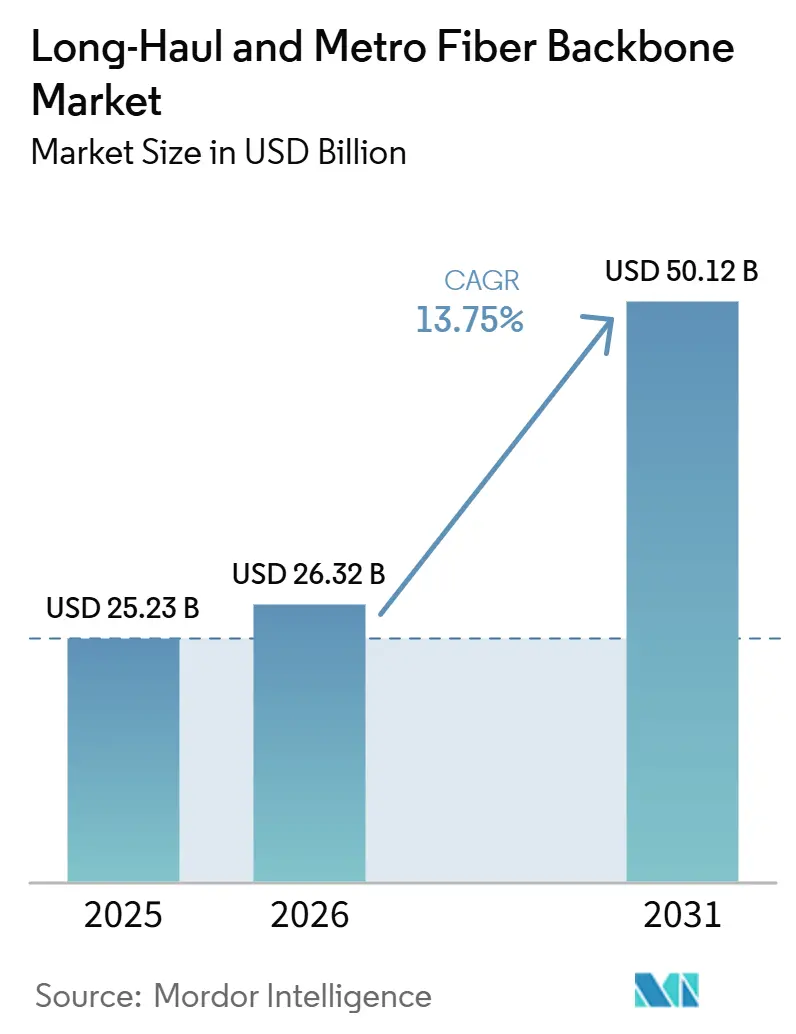

The long-haul and metro fiber backbone market size is expected to increase from USD 25.23 billion in 2025 to USD 26.32 billion in 2026 and reach USD 50.12 billion by 2031, growing at a CAGR of 13.75% over 2026-2031. The long-haul and metro fiber backbone market is moving up on several demand tracks at the same time, with AI computing, 5G transport, and national connectivity programs all calling for more backbone depth and more resilient route design. The long-haul and metro fiber backbone market is also shifting toward denser, lower-loss architectures, because metro rings and intercity routes now need to support 400G and 800G coherent optics over broader traffic loads. Revenue in the long-haul and metro fiber backbone market still leans toward metro deployments, because urban interconnection around hyperscale campuses, colocation sites, and enterprise nodes remains the most immediate source of utilization. At the same time, the strongest new-build opportunity in the long-haul and metro fiber backbone market is moving toward long-haul corridors connecting distributed AI campuses in power-available locations with established exchange and peering hubs. Competition remains active across optical transport vendors, cable manufacturers, and network operators, and project timing is increasingly shaped by civil works discipline, route access, and the availability of advanced optical components.

Key Report Takeaways

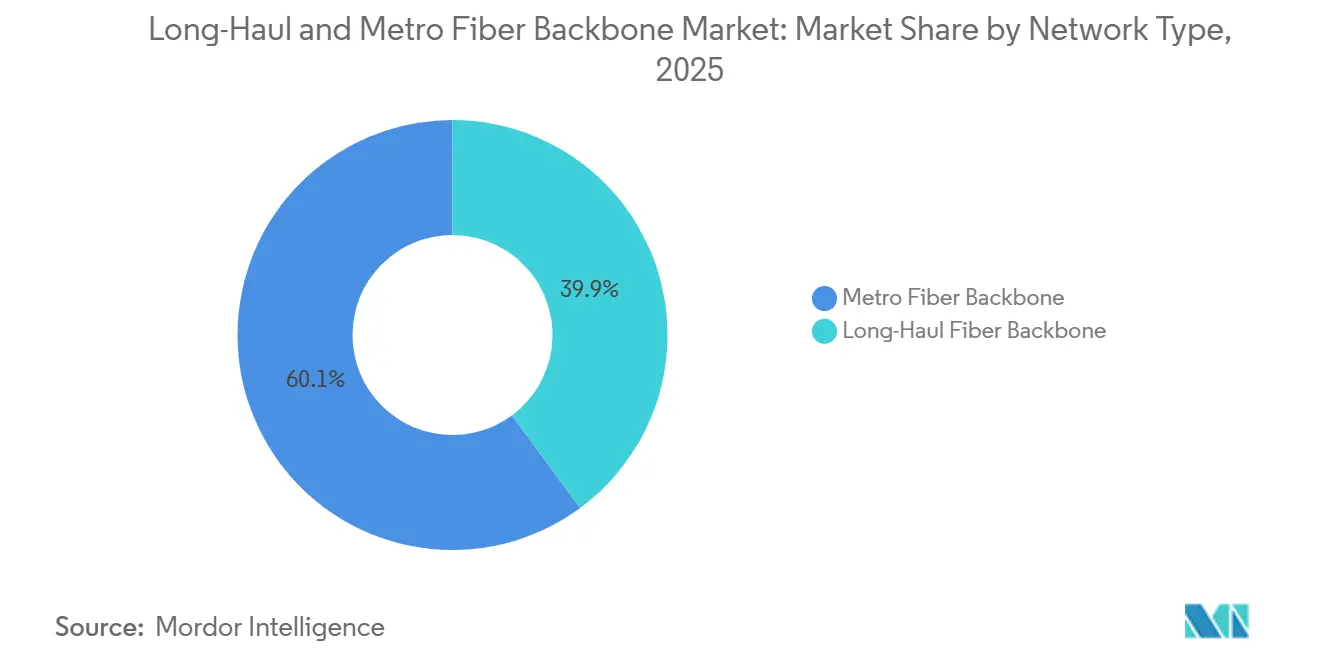

- By network type, Metro Fiber Backbone held 60.12% share in 2025, while Long-Haul Fiber Backbone is projected to expand at 13.80% CAGR through 2031.

- By fiber type, Single-Mode Fiber held an 87.55% share in 2025, while Multi-Mode Fiber played a smaller role, with no faster CAGR disclosed in the input.

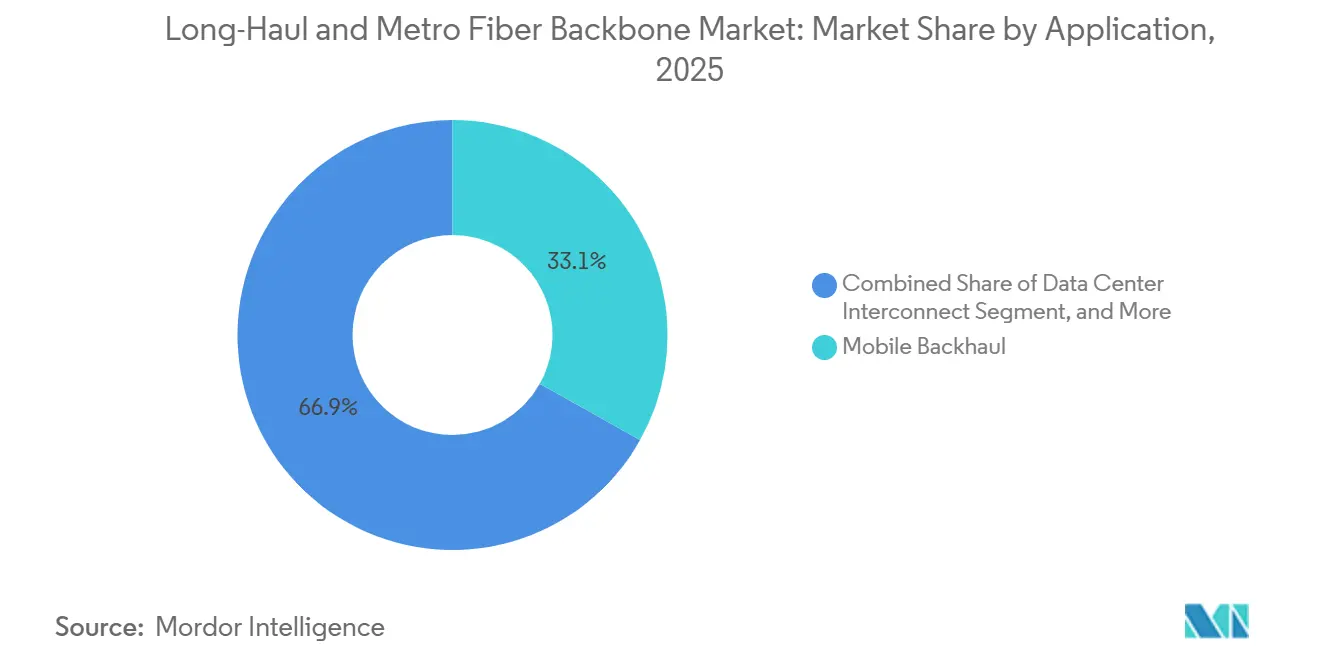

- By application, Mobile Backhaul accounted for 33.12% share in 2025, while Data Center Interconnect is projected to expand at 13.55% CAGR through 2031.

- By end user, Telecom Operators held 48.11% share in 2025, while Hyperscale Cloud Providers are projected to expand at 14.40% CAGR through 2031.

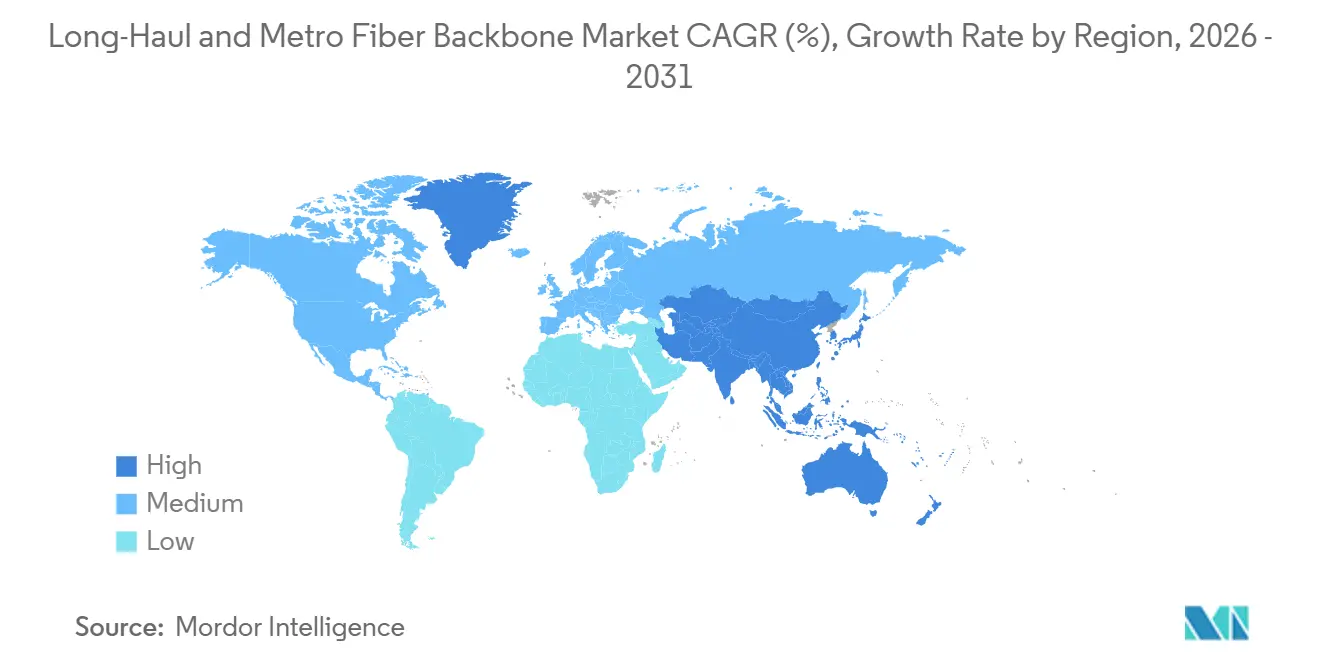

- By geography, North America held 33.89% of the long-haul and metro fiber backbone market share in 2025, while the Asia Pacific is projected to expand at 14.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Long-Haul and Metro Fiber Backbone Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hyperscale Data Center Interconnect Demand | +3.8% | Global, concentrated in North America and the Asia Pacific | Short term (≤ 2 years) |

| AI Workload-Driven Long-Haul Capacity Expansion | +2.9% | Global, with early gains in North America and spillover into Europe and the Asia Pacific | Short term (≤ 2 years) |

| 5G Transport and Mobile Backhaul Densification | +2.4% | Asia Pacific core, with North America and Europe secondary | Medium term (2-4 years) |

| National Broadband and Digital Infrastructure Buildouts | +1.8% | North America, Europe, South America, and select Asia Pacific markets | Medium term (2-4 years) |

| Open-Access Fiber and Wholesale Network Monetization | +1.1% | Europe and North America, with early-stage activity in the Middle East and Africa | Long term (≥ 4 years) |

| Conduit Permitting Relief and Micro-Trenching Economics | +0.7% | National, with early gains in high-density urban corridors in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Data Center Interconnect Demand

Data center interconnect has moved from a supporting workload to a core build trigger in the long-haul and metro fiber backbone market, because AI clusters now need persistent, low-latency links between campuses, exchanges, and compute zones. Meta stated that its 10x backbone program was built to scale AI inference and to strengthen the connection between the IP and optical layers, showing how backbone planning is now tied directly to AI service architecture rather than to general internet traffic growth alone.[1]Meta Engineering, “10x Backbone, How Meta Is Scaling Backbone Connectivity for AI,” Meta Engineering Blog, engineering.fb.com Google has also described its global data center and network estate as infrastructure built for the AI era, reinforcing the same pattern across large cloud operators that are shaping route demand with internal network design choices.[2]Google Cloud, “Data Center and Global Networks Built for AI Era,” Google Cloud Blog, cloud.google.com Corning and NVIDIA announced in May 2026 that they would expand U.S.-based optical connectivity manufacturing capacity tenfold and raise fiber production capacity by more than 50%, indicating that suppliers are already committing capital in anticipation of sustained DCI-driven demand.[3]Corning Incorporated, “NVIDIA and Corning Announce Long-Term Partnership to Strengthen U.S. Manufacturing for AI Infrastructure,” Corning Incorporated, corning.com As a result, the long-haul and metro fiber backbone market is seeing more demand in corridors that were not central in earlier cloud cycles, especially where hyperscalers need to connect secondary compute sites back to established interconnection hubs.

AI Workload-Driven Long-Haul Capacity Expansion

Generative AI training has made long-distance capacity a design issue for the long-haul and metro fiber backbone market, because distributed compute clusters require large, stable data exchange across regions rather than within a single campus. The Fiber Broadband Association projected that long-haul fiber route miles would need to rise from 95,000 to 187,000 by 2029, while fiber miles would expand to 373 million, indicating a major increase in route depth and strand count over a short planning window.[4]Fiber Broadband Association, “AI Data Center White Paper, Long-Haul Fiber Route Miles,” Fiber Broadband Association, fiberbroadband.org Lumen said in September 2025 that it had deployed more than 2.2 million new intercity fiber miles in 2025 and planned to reach 47 million intercity fiber miles by the end of 2028, which shows how AI demand is already reshaping private backbone investment plans.[5]Lumen Technologies, “Lumen Accelerates Multi-Billion-Dollar Network Expansion to Meet Soaring AI Demand,” Lumen Technologies, ir.lumen.com NTT demonstrated 160 Tbps transmission over more than 1,000 km in August 2025 using a new X-band wavelength regime, supporting the view that higher capacity per route will continue to strengthen the economic case for advanced long-haul builds. This is pushing the long-haul and metro fiber backbone market toward routes that can win early anchor tenants from hyperscalers and then attract wider enterprise and carrier demand after the initial build is complete.

5G Transport and Mobile Backhaul Densification

Mobile backhaul remains a core workload in the long-haul and metro fiber backbone market, because 5G densification continues to push more traffic from radio sites into metro aggregation layers and national backbone routes. Prysmian launched Sirocco Ultra in March 2026 for high-density broadband, 5G, and data center deployments, demonstrating that vendors are designing cable systems specifically for the constrained duct environments common in dense metro transport networks. KDDI, Nokia, and APRESIA demonstrated point-to-multipoint all-photonics transmission in a commercial environment in May 2026, suggesting that operators are also seeking more efficient ways to extend optical reach to a larger number of endpoints across metro domains. SoftBank, JR West Optical Network, and JR Kyushu Electric System also announced an Ethernet leased-line collaboration using railway-corridor optical cable in February 2026, which shows how route diversity is being used to support transport expansion beyond traditional urban conduit paths. Taken together, these moves show that the long-haul and metro fiber backbone market is not only adding capacity for AI, but also reinforcing the fiber foundations that support persistent 5G transport growth.

National Broadband and Digital Infrastructure Buildouts

Public and quasi-public digital infrastructure programs are expanding the addressable base of the long-haul and metro fiber backbone market, as every new access network requires aggregation and backhaul into metro rings and intercity corridors. The Fiber Broadband Association and Cartesian reported that deployment activity remained elevated in 2025, even as project costs rose, suggesting that fiber build programs are being treated as strategic infrastructure rather than discretionary network upgrades. NEC and Nokia said in February 2026 that they would expand Eletronet’s optical fiber network in Brazil by 8,000 km, increasing coverage across all 23 Brazilian states, illustrating how national-scale plans are extending backbone routes beyond a few high-volume metro areas. SoftBank’s February 2026 railway-corridor optical service initiative also shows that alternative national rights-of-way are being used to create new backbone paths where standard deployment routes are crowded or slow to secure. This means the long-haul and metro fiber backbone market is drawing support from both commercial AI demand and broader infrastructure agendas that keep route construction active across multiple geographies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Civil Works Cost and Right-of-Way Delays | -2.0% | Global, most acute in North America and Europe urban corridors | Short term (≤ 2 years) |

| Stringent Pole Attachment and Permitting Complexity | -1.2% | North America, with growing relevance in Europe and South America | Medium term (2-4 years) |

| Long Lead Times for Optical Transport Electronics | -0.9% | Global, concentrated in markets sourcing Western vendor equipment | Short term (≤ 2 years) |

| Route-Level Overbuild Risk in Dense Corridors | -0.7% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Civil Works Cost and Right-Of-Way Delays

Civil works remain the largest practical barrier in the long-haul and metro fiber backbone market, because route economics are heavily exposed to trenching costs, engineering work, and local access delays. The Fiber Broadband Association and Cartesian found that median underground deployment cost reached USD 18 per foot in 2025, compared with USD 8 per foot for aerial deployment, and 92% of builders reported rising costs during the year. That cost structure tends to favor routes with committed anchor tenants, because speculative corridors become harder to finance as both labor and access costs rise. For the long-haul and metro fiber backbone market, this keeps investment concentrated in the strongest demand corridors even when adjacent geographies also need more capacity.

Stringent Pole Attachment and Permitting Complexity

Permitting complexity continues to slow the long-haul and metro fiber backbone market, especially in corridors where demand is strongest but route approvals are fragmented across many local authorities and infrastructure owners. USTelecom said railroad crossing permits in the United States often take 12 to 15 months for a response and can cost from USD 5,000 to more than USD 110,000 per crossing, while pole attachment make-ready cycles add a further 180-day minimum through standard review and move sequences. USTelecom also noted that extreme municipal fee structures can force providers to abandon projects even when there is clear service demand, which shows how local process variation can undermine otherwise viable route plans. This matters most in dense metro corridors, where enterprise traffic, hyperscale interconnect, and 5G transport overlap, and where delayed execution incurs the highest commercial cost. As a result, the long-haul and metro fiber backbone market remains highly sensitive to approval reform, even as optical technology and end demand are advancing rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Network Type: Metro Networks Anchor Revenue While Long-Haul Scales For AI

Metro Fiber Backbone accounted for 60.12% of revenue in 2025, keeping this segment at the center of the long-haul and metro fiber backbone market, as dense urban rings still carry the highest concentration of immediate enterprise, carrier, and cloud traffic. That position reflects the fact that metro routes can connect hyperscale campuses, colocation buildings, enterprise clusters, and mobile aggregation points within a relatively compact footprint. The revenue case is stronger in metro settings because a single route can serve many customers simultaneously and support both lit services and dark fiber leasing. This is why operators with strong urban footprints continue to treat metro assets as the most dependable near-term revenue base in the long-haul and metro fiber backbone market. Metro route density also gives operators more room to monetize wavelength services, campus diversity, and cross-connect traffic without waiting for a long build cycle or anchor-tenant threshold.

Long-Haul Fiber Backbone is projected to expand at a 13.80% CAGR through 2031, making it the fastest-growing network type as AI clusters spread across regions with more available land and power. The long-haul and metro fiber backbone industry is therefore seeing more value in networks that can link distributed compute campuses back to peering points and metro exchange hubs through a single operating fabric. Zayo completed the acquisition of Crown Castle’s Fiber Solutions business in May 2026, adding 90,000 metro-dense route miles and bringing its North American footprint to 224,000 route miles, which shows how scale across both network tiers is becoming a competitive advantage. Lumen also expanded its intercity program to meet AI traffic needs, reinforcing the same view that long-haul routes are no longer a secondary layer but a direct demand target. In practice, the operators best placed in the long-haul and metro fiber backbone market are those that can move traffic cleanly from metro aggregation into long-distance transport without handing the customer to another provider.

By Fiber Type: Single-Mode Fiber Dominates Across All Distance Tiers

Single-Mode Fiber accounted for 87.55% of revenue in 2025 and held the largest share of the long-haul and metro fiber backbone market, reflecting its broad suitability across aggregation, metro, and intercity transport. Its lead is not just about installed base, because current network upgrades also favor single-mode designs that can support longer spans, higher coherent rates, and tighter operating margins on future traffic growth. The long-haul and metro fiber backbone market is also moving toward single-mode designs, from standard designs toward lower-loss, bend-tolerant variants better suited to high-capacity backbone workloads. Prysmian’s March 2026 launch of Sirocco Ultra, with 288 fibers in a 6.1 mm diameter using 160-micron single-mode fiber, shows how vendors are pushing fiber density and duct efficiency simultaneously. In dense metro routing, these design shifts matter because operators often need to add capacity inside legacy ducts where space and bend tolerance are real operating constraints.

The performance ceiling for single-mode deployments is also rising quickly, which supports its continued dominance in the long-haul and metro fiber backbone market even as traffic loads become more demanding. NTT’s August 2025 demonstration of 160 Tbps transmission over more than 1,000 km showed that advanced optical systems can continue to extract far more capacity from backbone fiber as plant quality improves. Multi-Mode Fiber, by contrast, remains much more limited in this space because its role is largely tied to short-reach links inside data center environments rather than to metro or intercity transport. The long-haul and metro fiber backbone industry, therefore, continues to favor single-mode upgrades when operators decide where to allocate new capital for scalable backbone services. That pattern also means cable suppliers with strong single-mode portfolios remain more closely aligned with the highest-growth segments of the long-haul and metro fiber backbone market.

By Application: Mobile Backhaul Leads While Data Center Interconnect Draws the Fastest Capital

Mobile Backhaul remained the largest application with 33.12% share in 2025, while Data Center Interconnect is projected to grow at 13.55% CAGR through 2031 and is becoming the main source of incremental capital redirection. The largest revenue block still sits in mobile transport because national operators continue to feed dense radio layers into metro and backbone fiber, especially in urban corridors where wireless alternatives lose cost or latency advantage at scale. Even so, the fastest change in the long-haul and metro fiber backbone market is driven by AI-driven DCI, as cloud operators increase the number, size, and geographic spread of compute clusters that must remain tightly linked. Meta’s 10x backbone program made clear that AI inference support now depends on deeper integration between the optical and IP layers, which aligns with the way DCI traffic is moving from periodic expansion to continuous architectural scaling. This is why the long-haul and metro fiber backbone market is seeing more route selection based on campus-to-campus latency and diversity rather than only on traditional metro demand density.

Cloud and content distribution workloads are also broadening the application map, as inference serving pushes more traffic to regional nodes that require strong fiber links back to the origin infrastructure and exchange points. Google described its networks as built for the AI era, which supports the view that cloud backbone planning now extends across data center fabrics, terrestrial transport, and global interconnection layers. Enterprise WAN demand remains strong as large users adopt higher-capacity wavelength and dark fiber services to support cloud-intensive operations and resilience across multiple sites. Subsea landing to terrestrial backhaul is still smaller in direct revenue terms, but it carries strategic weight because each new landing point creates an additional inland transport node that must be connected to metro and national backbone grids. For that reason, the long-haul and metro fiber backbone market is being reshaped not only by one fast-growing application, but by several traffic classes that now rely on the same optical transport foundation.

By End User: Telecom Operators Retain Scale While Hyperscalers Raise Their Direct Ownership

Telecom Operators held a 48.11% share in 2025, making them the largest end-user group in the long-haul and metro fiber backbone market, as they still operate the broadest mix of national transport, wholesale, enterprise, and mobile workloads. Their position remains strong because they control legacy rights-of-way, service operations, and large customer bases that continue to consume backbone capacity across several product lines. At the same time, the input shows that Hyperscale Cloud Providers are projected to grow at a 14.40% CAGR through 2031, making them the fastest-growing buyer group in the long-haul and metro fiber backbone market. This shift is changing commercial terms, because large cloud operators are more willing to self-build dark fiber, secure long-term supply, and shape route design around internal AI plans rather than around standard carrier offerings. As a result, telecom operators are still central, but they are no longer the only group defining how backbone routes are financed and deployed.

Meta’s public explanation of its 10x backbone program shows how hyperscalers are taking a more direct role in optical architecture, network simplification, and backbone scaling to support AI. Google has made a similar case for global networks built for the AI era, which indicates that the leading cloud platforms are treating backbone ownership and control as strategic assets rather than as outsourced transport functions. Internet Service Providers also remain important in the long-haul and metro fiber backbone market as residential broadband upgrades raise aggregation traffic into metro rings and intercity routes. Colocation operators, public safety networks, and enterprises form smaller end-user groups, yet they still provide stable demand where campus interconnect, route diversity, and secure wavelength services matter more than pure scale. That mix keeps the long-haul and metro fiber backbone market broad enough to sustain multiple commercial models even as hyperscalers become the fastest-growing class of direct backbone spenders.

Geography Analysis

North America accounted for 33.89% of revenue in 2025 and represented the largest regional share of the long-haul and metro fiber backbone market, supported by hyperscaler concentration, strong enterprise interconnection demand, and ongoing transport investment along 5G and cloud corridors. The region also faces some of the hardest build conditions, because underground deployment costs reached a median USD 18 per foot in 2025 compared with USD 8 per foot for aerial deployment, which directly affects route pacing in dense markets. Lumen’s intercity expansion program and its focus on AI traffic show that new North American route construction is being tied closely to future data movement needs rather than to legacy carrier demand patterns alone. Zayo’s May 2026 acquisition of Crown Castle’s Fiber Solutions business follows the same regional logic, as operators use acquisitions to deepen both metro density and long-distance reach under a single footprint. This leaves North America with the largest present revenue base in the long-haul and metro fiber backbone market, even though cost pressure and permitting remain real constraints on how fast additional corridors can be activated.

Asia Pacific is projected to expand at 14.32% CAGR through 2031, making it the fastest-growing geography in the long-haul and metro fiber backbone market as carriers, cloud operators, and infrastructure vendors expand optical depth across both metro and intercity networks. KDDI, Nokia, and APRESIA demonstrated point-to-multipoint all-photonics transmission in a commercial environment in May 2026, which supports the view that the region is not only adding routes but also testing more efficient optical architectures for future scale. SoftBank’s railway-corridor optical initiative adds another sign that Asia Pacific operators are using alternative physical paths to extend network reach and route diversity where conventional corridors are crowded. In South America, NEC and Nokia’s 8,000 km Eletronet expansion in Brazil shows that the region is also strengthening national backbone depth and moving toward broader multi-state optical coverage.

Europe held a significant share of 2025 revenue in the long-haul and metro fiber backbone market, supported by ongoing gigabit connectivity targets and the need for denser metro backbones in large national economies. The Middle East and Africa remained the smallest regional segment, yet activity is rising as new terrestrial routes and subsea-linked corridors create more inland backhaul demand from landing points and urban hubs. East African backbone additions, including the new Nairobi-Kampala route cited in the input, demonstrate how regional transport grids are becoming increasingly connected to carrier-grade optical infrastructure rather than relying solely on isolated national links. Across Europe, the Middle East and Africa, and South America, the long-haul and metro fiber backbone market is following a similar pattern, where more access networks, more data center activity, and more route diversity plans all increase the need for backbone depth over time.

Competitive Landscape

The long-haul and metro fiber backbone market competes across 2 linked layers: the physical infrastructure layer of fiber cable and duct assets, and the optical systems layer of transport equipment that determines the capacity of those routes. The supply side of physical cable remains more concentrated because preform production is capital-intensive and time-consuming to expand, giving established manufacturers a clear advantage when demand rises quickly. Corning’s Optical Communications business expanded strongly into 2026, and its multi-year partnership with NVIDIA will raise U.S. optical connectivity manufacturing capacity tenfold while increasing fiber production capacity by more than 50%. Prysmian’s March 2026 Sirocco Ultra launch shows that cable suppliers are also competing on density, duct efficiency, and deployment practicality, rather than only on volume. This means the long-haul and metro fiber backbone market is not driven solely by route demand, because supplier readiness and product design now shape how quickly operators can turn planned builds into live capacity.

On the operator side, competition is becoming more active around route control, metro depth, and the ability to provide one network fabric across local aggregation and intercity transport. Zayo’s Crown Castle Fiber Solutions acquisition is a clear example, because it added metro-dense assets and on-net enterprise reach while also strengthening scale in North America’s broader backbone footprint. Lumen’s intercity expansion is another example, with route additions tied directly to AI data movement rather than to a broad, undifferentiated capacity strategy. Smaller builders are also entering the long-haul and metro fiber backbone market with purpose-built AI routes, intensifying competition in selected corridors even as national coverage remains concentrated among larger incumbents.

In the optical systems layer, vendors are competing on capacity per wavelength, reach, power use, and the ability to simplify deployment in demanding backbone environments. BB Backbone and Ciena’s February 2026 demonstration of 1.6 Tbps long-distance transmission in a commercial network shows how live-network performance is becoming a practical differentiator for backbone contracts. KDDI’s commercial all-photonics demonstration with Nokia and APRESIA shows a similar focus on scaling optical efficiency across metro transport environments. At the same time, hyperscalers such as Meta and Google are increasing their direct influence on design choices and procurement priorities, which means the long-haul and metro fiber backbone market is being shaped as much by buyer architecture decisions as by seller product portfolios.

Long-Haul and Metro Fiber Backbone Industry Leaders

Corning Incorporated

Prysmian S.p.A.

Zayo Group Holdings, Inc.

Lumen Technologies, Inc.

Nexans

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Aureon, Nokia, t3 Broadband, and Midco delivered a new 100 Tbps long-haul transport route from Ellendale, North Dakota, to Chicago using Nokia's 1830 Global Express platform and 1.2T ICE7 coherent optics, with design scalability to 400 Tbps to support future AI-driven demand growth.

- May 2026: Lightpath announced a new 392-mile, multi-conduit long-haul route connecting Columbus and Chicago to support hyperscale, carrier, and enterprise customers with scalable, AI-grade connectivity. The route extends Lightpath's dense all-fiber network into a critical Midwest corridor.

- May 2026: DCN, Range, and WIN Technology launched the Heartland Fiber Project, a USD 700 million joint investment to build 2,000 miles of high-capacity long-haul fiber across Colorado, Wyoming, Montana, North Dakota, Minnesota, Wisconsin, and Illinois, targeting hyperscaler AI data center demand in the Upper Midwest. Construction is set to begin in summer 2026 with activation over the following 12 to 24 months.

- May 2026: Zayo completed the acquisition of Crown Castle's Fiber Solutions business on May 1, 2026, adding 90,000 metro-dense route miles and 40,000 on-net enterprise locations. The combined transaction value of the Fiber Solutions and Small Cells assets was USD 8.5 billion, and the deal represents Zayo's 50th and largest acquisition, bringing its total network footprint to 224,000 North American route miles.

Global Long-Haul and Metro Fiber Backbone Market Report Scope

The Long-Haul and Metro Fiber Backbone Market is Segmented by Network Type (Long-Haul and Metro), Fiber Type (Single-Mode and Multi-Mode), Application (DCI, Mobile Backhaul, CDN, Enterprise WAN, and Subsea Backhaul), End User (Telecom Operators, ISPs, Hyperscalers, Colo Operators, Government, and Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Long-Haul Fiber Backbone |

| Metro Fiber Backbone |

| Single-Mode Fiber |

| Multi-Mode Fiber |

| Data Center Interconnect |

| Mobile Backhaul |

| Cloud and Content Delivery Networks |

| Enterprise WAN Connectivity |

| Subsea Landing to Terrestrial Backhaul |

| Telecom Operators |

| Internet Service Providers |

| Hyperscale Cloud Providers |

| Colocation and Data Center Operators |

| Government and Public Safety Networks |

| Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Network Type | Long-Haul Fiber Backbone | ||

| Metro Fiber Backbone | |||

| By Fiber Type | Single-Mode Fiber | ||

| Multi-Mode Fiber | |||

| By Application | Data Center Interconnect | ||

| Mobile Backhaul | |||

| Cloud and Content Delivery Networks | |||

| Enterprise WAN Connectivity | |||

| Subsea Landing to Terrestrial Backhaul | |||

| By End User | Telecom Operators | ||

| Internet Service Providers | |||

| Hyperscale Cloud Providers | |||

| Colocation and Data Center Operators | |||

| Government and Public Safety Networks | |||

| Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the long-haul and metro fiber backbone market?

The long-haul and metro fiber backbone market size stands at USD 25.23 billion in 2025, reaches USD 26.32 billion in 2026, and is forecast to hit USD 50.12 billion by 2031 at a 13.75% CAGR.

Which network type leads revenue in backbone fiber deployments?

Metro Fiber Backbone led revenue with a 60.12% share in 2025 because dense urban interconnection around enterprises, carriers, and hyperscale campuses continues to drive the highest near-term utilization.

What is driving the fastest growth in backbone fiber demand?

AI-led data center interconnect and distributed compute buildouts are driving the fastest growth, which is why Long-Haul Fiber Backbone and Data Center Interconnect are projected to grow at 13.80% and 13.55% CAGRs, respectively, through 2031.

Why does single-mode fiber dominate backbone networks?

Single-Mode Fiber held an 87.55% share in 2025 because it better fits metro and intercity transport than alternatives and supports higher-capacity coherent optical systems over longer distances.

Which end users are increasing direct backbone spending the fastest?

Telecom Operators remained the largest end-user group with a 48.11% share in 2025, but Hyperscale Cloud Providers are expanding the fastest at a 14.40% CAGR as they take on a more direct role in route ownership and optical design.

Which region is growing the fastest for backbone fiber expansion?

North America remained the largest region with 33.89% share in 2025, while the Asia Pacific is forecast to grow the fastest at 14.32% CAGR as operators and infrastructure vendors expand optical capacity across metro and national routes.

Page last updated on: