Market Overview

| Study Period | 2020 - 2031 |

|---|---|

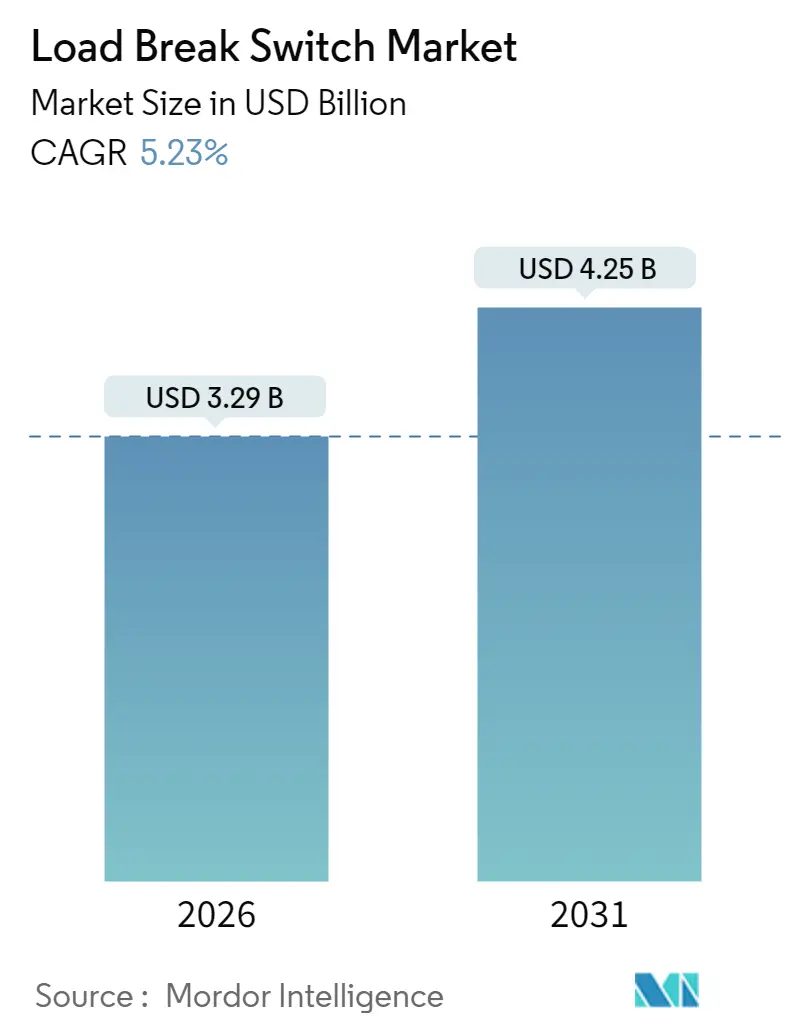

| Market Size (2026) | USD 3.29 Billion |

| Market Size (2031) | USD 4.25 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

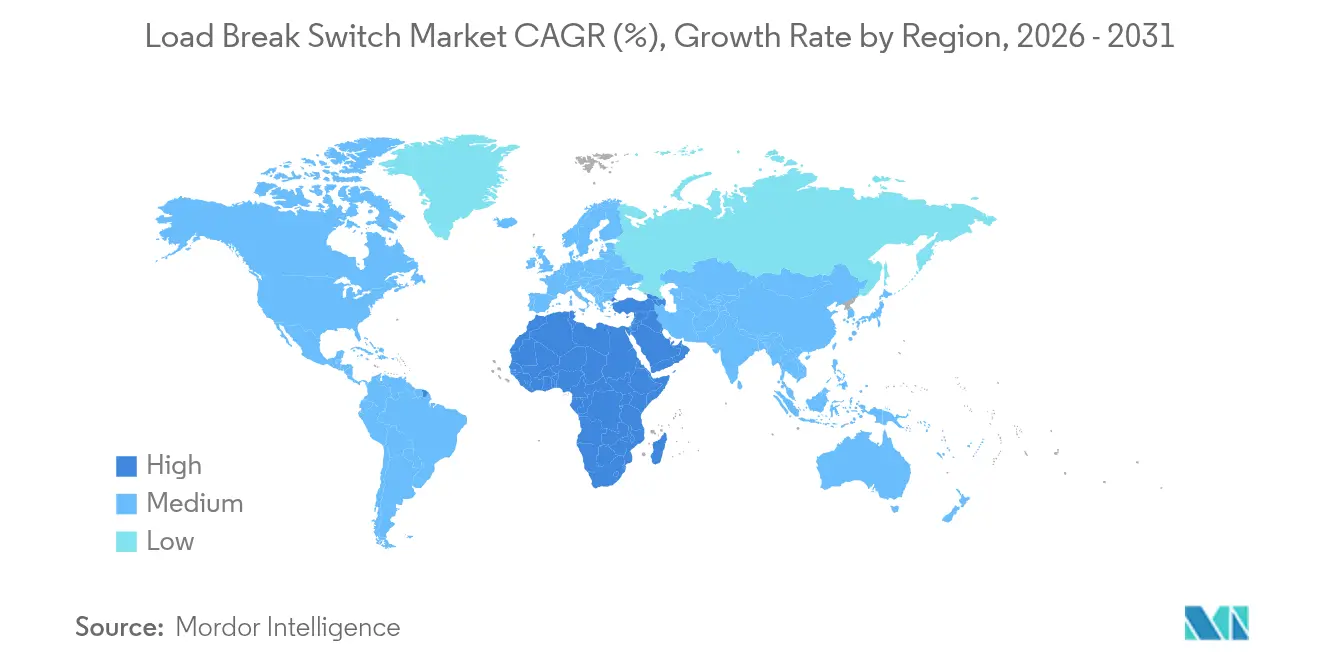

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

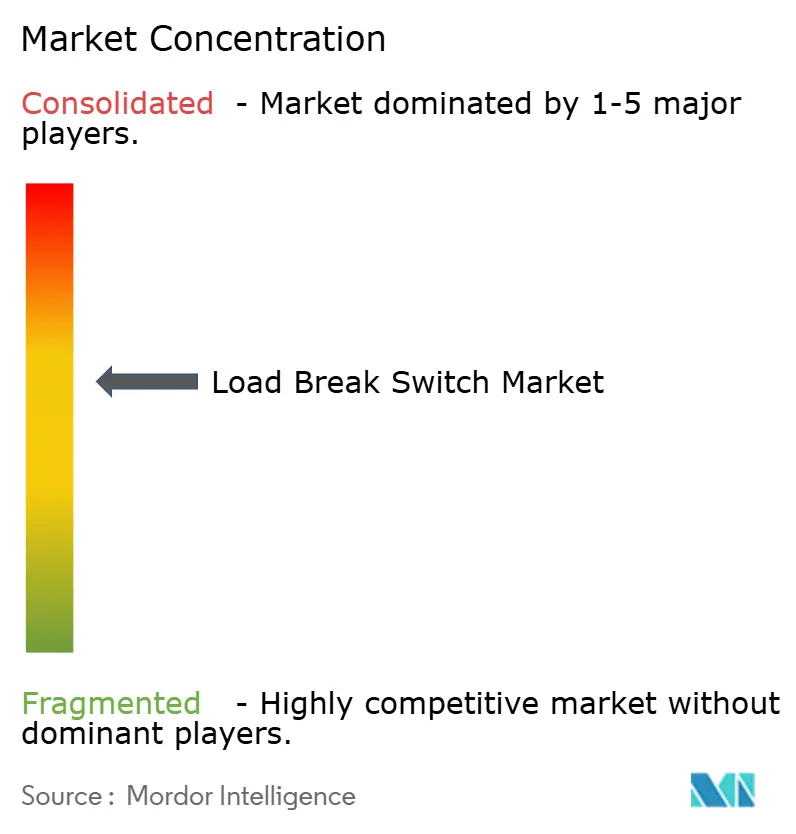

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Load Break Switch Market Analysis by Mordor Intelligence

Load Break Switch market size in 2026 is estimated at USD 3.29 billion, growing from 2025 value of USD 3.13 billion with 2031 projections showing USD 4.25 billion, growing at 5.23% CAGR over 2026-2031. Widespread grid-modernization programs in North America and Europe, coupled with electrification projects across Asia-Pacific, position the Load Break Switch market as a critical enabler of reliable, flexible medium-voltage distribution networks. Strong policy support for renewable integration, data-center expansion, and rail electrification is reshaping demand toward more automated, SF₆-free products. Meanwhile, cost volatility in copper and stainless steel, together with regulatory uncertainty around SF₆ phase-out, introduces margin pressure and planning complexity for manufacturers. Competitive differentiation is therefore shifting from price toward technology leadership in digital control, eco-efficient insulation, and application-specific designs that meet emerging standards for sustainability and resiliency.

Key Report Takeaways

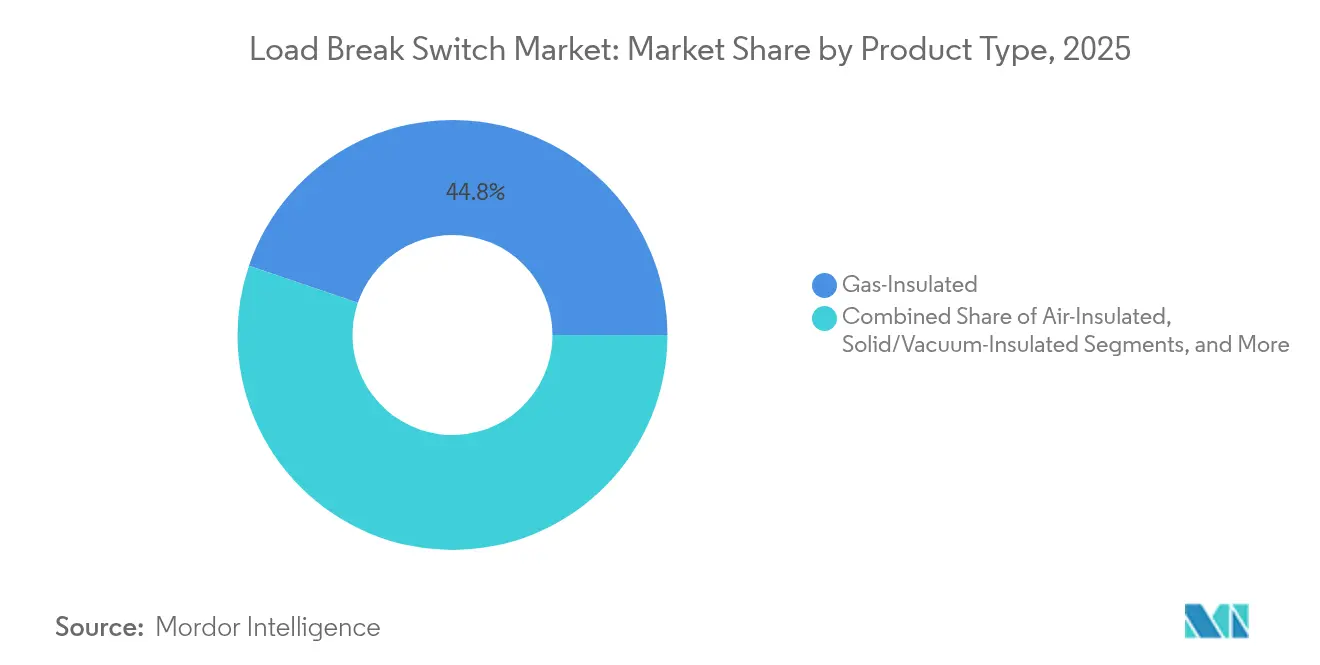

- By product type, gas-insulated units led with 44.78% Load Break Switch market share in 2025, whereas solid/vacuum-insulated switches are advancing at a 6.71% CAGR through 2031.

- By installation, outdoor pole-mounted equipment accounted for 52.58% of the Load Break Switch market in 2025, while indoor panel-mounted solutions are forecast to grow 7.18% annually to 2031.

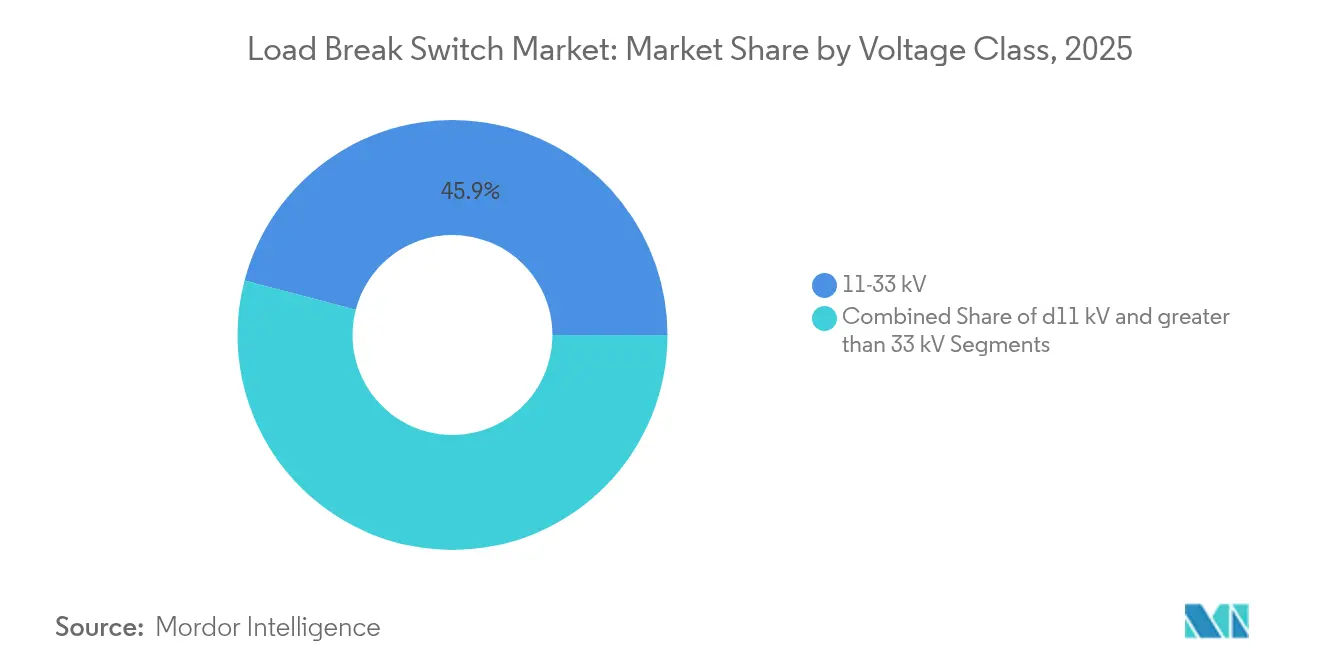

- By voltage class, the 11–33 kV segment held 45.92% of Load Break Switch market share in 2025; the >33 kV class is projected to expand at a 7.26% CAGR over the same horizon.

- By operating mechanism, manual devices dominated with a 62.53% share in 2025, yet motorized/automatic models are set to post a 7.54% CAGR through 2031.

- By end-user, utilities commanded 40.92% of the Load Break Switch market in 2025, whereas renewable IPPs and micro-grids recorded the quickest growth at 6.89% CAGR.

- By geography, Asia-Pacific contributed 38.45% of global revenue in 2025; the Middle East and Africa register the fastest regional CAGR at 7.05% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Load Break Switch Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid refurbishment programs in developed economies | +1.1% | North America and Europe | Medium term (2-4 years) |

| Renewable-energy driven medium-voltage switch demand | +1.2% | Global, with APAC leading | Long term (≥ 4 years) |

| Urban distribution automation roll-outs | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Electrification of rail and metro networks | +0.9% | Europe and APAC primarily | Long term (≥ 4 years) |

| MV switch as integral to data-center resiliency | +0.7% | North America and Europe | Short term (≤ 2 years) |

| ESG push for SF₆-free LBS designs | +0.6% | Europe leading, global adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Refurbishment Programs in Developed Economies

Utilities in North America and Europe are replacing legacy switchgear to handle bidirectional power flows required by distributed resources, triggering steady demand for advanced units that interface seamlessly with automated feeders. Asset-replacement cycles of 25–30 years coincide with new smart-grid mandates enforced under 55% carbon-reduction goals, elevating specifications for remote control and condition monitoring. Vendors that embed sensors and communication modules into the Load Break Switch market portfolio capture premium margins as operators prioritize uptime and workforce safety.

Renewable-Energy Driven Medium-Voltage Switch Demand

As ASEAN nations alone prepare to add 30 GW of solar and wind capacity, project developers specify switches engineered for fluctuating output and anti-islanding functions. Solutions must integrate vacuum or solid dielectric interruption with fast reclosing to meet grid-code requirements, growing the Load Break Switch market addressable value in utility-scale renewables.

Urban Distribution Automation Roll-outs

Major Asian cities deploy FLISR and Volt/VAr optimization schemes that depend on motorized switches to localize faults within seconds and balance voltage proactively. [1]Siemens, “Distribution Automation Box,” siemens.com Capital spending on automation software drives parallel hardware upgrades, reinforcing the Load Break Switch market as a gateway to smarter distribution grids.

Electrification of Rail and Metro Networks

Rising investment in traction-power networks—exemplified by the EUR 49.33 million Larissa-Volos line in Greece—requires vibration-resistant load interrupters that withstand inductive loads. Tailored designs enhance the Load Break Switch market penetration in rolling-stock depots and sub-stations for both AC and DC systems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile copper and stainless-steel prices | -0.4% | Global | Short term (≤ 2 years) |

| Regulatory uncertainty over SF₆ phase-out timelines | -0.3% | Europe and North America | Medium term (2-4 years) |

| Limited OEM localisation in Africa and S-America | -0.2% | Africa and South America | Long term (≥ 4 years) |

| Slow standardisation for solid-insulated LBS | -0.2% | Global, with Europe leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Stainless-Steel Prices

Copper climbed to USD 5.20 per pound in May 2024, prompting OEM list-price hikes of up to 45% and complicating budget cycles for price-sensitive utilities. [2]LAPP Tannehill, “The Copper Boom: Understanding Record-High Prices,” lapptannehill.com Smaller firms lacking hedging programs face working-capital strain, potentially slowing new orders in the Load Break Switch market until commodity costs normalize.

Regulatory Uncertainty Over SF₆ Phase-out Timelines

Divergent schedules between EU, California, and federal US rules force suppliers to maintain dual product lines, raising R&D and inventory overhead. Ambiguity over enforcement dates can delay customer purchasing decisions, dampening near-term growth prospects in the Load Break Switch market despite long-term decarbonization drivers.

Segment Analysis

By Product Type: SF₆-Free Innovation Accelerates

Gas-insulated models delivered 44.78% Load Break Switch market share in 2025 due to proven compactness and dielectric strength. Yet solid/vacuum designs are scaling fastest at 6.71% CAGR because regulators cap SF₆ usage, and cost differentials narrow as volumes rise. The Load Break Switch market size for vacuum units is projected to expand from USD 1.11 billion in 2026 to USD 1.58 billion by 2031 at plant-level pricing, underscoring the sustainability premium.

Technology migration favors OEMs that secure eco-gas patents or deploy vacuum interrupters across higher voltage classes. ABB’s puffer-type switch with alternative gases and Siemens Energy’s Blue platform cut lifecycle CO₂ equivalents by more than 80%. Utilities issuing net-zero tenders expedite the replacement of SF₆ baselines, further diversifying the Load Break Switch market.

Note: Segment shares of all individual segments available upon report purchase

By Installation: Indoor Applications Drive Growth

Outdoor pole-mounted units represented 52.58% revenue in 2025, due to overhead line prevalence in rural grids. However, the Load Break Switch market size for indoor panel-mounted configurations is forecast to grow 7.18% annually, reaching USD 1.44 billion by 2031, propelled by data-center and industrial retrofits that prize climate-controlled enclosures.

High-density facilities demand arc-flash mitigation and cyber-secure SCADA interfaces that indoor gear accommodates readily. Pad-mounted variants bridge the gap for suburban substations, preserving upgrade flexibility while keeping footprints compact. Investment in intelligent panels, therefore, redistributes revenue streams across the Load Break Switch market, even as outdoor hardware maintains baseline volumes.

By Voltage Class: Higher Voltages Gain Momentum

The 11–33 kV band captured 45.92% Load Break Switch market share in 2025, supporting mainstream distribution feeders worldwide. Utilities now migrate to 35 kV circuits to reduce thermal losses and connect utility-scale renewables more efficiently, fueling a 7.26% CAGR for >33 kV switches through 2031.

Sub-transmission expansion, especially in wind-rich zones, raises technical requirements for higher BIL ratings and extended mechanical endurance. Premium pricing in this class compensates for lower unit volumes, lifting overall Load Break Switch market revenue. Meanwhile, the ≤11 kV niche remains stable, anchored by rooftop solar farms and light industrial loads.

Note: Segment shares of all individual segments available upon report purchase

By Operating Mechanism: Automation Transforms Operations

Manual handles dominated 62.53% of shipments in 2025 due to straightforward design and low acquisition cost. Yet remote-ready motor drives register a 7.54% CAGR because FLISR programs demand split-second isolation without dispatching field crews.

The Load Break Switch industry is converging on plug-and-play motor kits that retrofit legacy units, accelerating automation without full replacement. Utilities justify the premium via avoided outage penalties and reduced truck rolls, injecting resilient growth into the segment. Integration of IEC 61850 digital relaying and cloud analytics redefines value propositions. The Load Break Switch market responds with firmware-upgradable controllers that allow predictive maintenance via temperature and pressure sensors. Cybersecurity certification further elevates market entry barriers, rewarding incumbents that embed secure boot and encryption protocols.

By End-user: Renewables Reshape Demand

Utilities procured 40.92% of units in 2025, but renewable IPPs and micro-grids will outpace at 6.89% CAGR to 2031. Hybrid micro-grids serving remote mines or islands specify switches capable of seamless grid-to-island transfer, differentiating the Load Break Switch market from conventional feeder applications.

Commercial campuses and industrial parks incorporate medium-voltage loops to accommodate on-site PV and battery assets, widening the customer base. OEM channel strategies now target EPCs and energy-as-a-service providers that bundle switchgear with storage and controls.

Geography Analysis

Asia-Pacific led with 38.45% of 2025 revenue, anchored by Chinese renewable build-outs and Indian rural electrification that necessitate robust feeder automation. Urban megaprojects in ASEAN capitals likewise boost demand for compact, arc-resistant assemblies that fit underground substations. Policymakers prioritize domestic manufacturing incentives, which encourage joint ventures and technology transfer within the Load Break Switch market.

Middle East and Africa log the highest regional CAGR at 7.05% as Egypt’s Megaproject added 14.4 GW of capacity and Gulf states diversify grids to host mega-solar complexes. Public-private partnerships accelerate procurement, while multilaterals finance upgrades in Sub-Saharan Africa, driving adoption of low-maintenance, weather-proof models.

North America and Europe sustain sizeable installed bases that require replacement of 1990s-era gear now reaching end-of-life. The US medium-voltage switchgear market, worth roughly USD 2 billion, is growing 10.5% annually on data-center builds and undergrounding programs that favor sealed interrupters. Europe pioneers SF₆-free standards, compelling accelerated upgrades, and spurring innovation clusters that enhance the global Load Break Switch market.

Competitive Landscape

The market is moderately fragmented. Global majors—Schneider Electric, ABB, Siemens, Eaton—share roughly 55% of global revenue, while dozens of regionals compete on niche customizations. Large players leverage integrated portfolios that span substation automation, breakers, and digital services, enabling turnkey bids that win utility tenders.

Technology differentiation is sharpening around eco-efficient gases and solid-state interruption. ABB’s SACE Infinitus solid-state breaker debuted in April 2025, breaking the 2,500 A ceiling and setting new response benchmarks. Siemens Energy’s Blue range eliminates greenhouse gases entirely, appealing to European DSOs with strict ESG mandates. Emerging disruptors such as Atom Power push silicon-based devices that integrate metering and analytics, challenging mechanical designs in premium applications.

Strategic moves include Eaton’s double-digit backlog growth in 2024 on data-center-focused lines and Schneider Electric’s 2025 acquisition of Motivair to broaden liquid-cooling capabilities for critical power sectors. Suppliers targeting SF₆-free patents or digital-native platforms gain pricing power, tilting competition toward innovation rather than scale alone within the Load Break Switch market.

Load Break Switch Industry Leaders

Schneider Electric SE

ABB Ltd.

Siemens AG

Eaton Corporation plc

Lucy Group Ltd. (Lucy Electric)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABB launched the SACE Infinitus, the first fully IEC 60947-2 certified solid-state breaker rated 2,500 A / 1,250 V DC, delivering 70% lower losses.

- October 2024: Eaton posted record Q3 2024 earnings, with Electrical Americas sales hitting USD 3.0 billion, up 26% in backlog.

- August 2024: Hitachi Energy unveiled the EconiQ 550 kV SF₆-free breaker, securing initial orders from TenneT and Hydro One.

- July 2024: Schneider Electric’s H1 2024 revenue reached EUR 18.2 billion, driven by Energy Management's 8.9% growth.

Global Load Break Switch Market Report Scope

The load break switch market report includes:

By Product Type

| Gas-Insulated |

| Air-Insulated |

| Solid/Vacuum-Insulated |

| Hybrid and SF?-Free Alternatives |

By Installation

| Outdoor – Pole-Mounted |

| Outdoor – Pad/Cubicle-Mounted |

| Indoor – Panel-Mounted |

By Voltage Class

| ≤11 kV |

| 11–33 kV |

| >33 kV |

By Operating Mechanism

| Manual |

| Motorised/Automatic |

By End-user

| Utilities |

| Industrial Facilities |

| Commercial and Institutional Buildings |

| Renewable IPPs and Micro-grids |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Gas-Insulated | ||

| Air-Insulated | |||

| Solid/Vacuum-Insulated | |||

| Hybrid and SF?-Free Alternatives | |||

| By Installation | Outdoor – Pole-Mounted | ||

| Outdoor – Pad/Cubicle-Mounted | |||

| Indoor – Panel-Mounted | |||

| By Voltage Class | ≤11 kV | ||

| 11–33 kV | |||

| >33 kV | |||

| By Operating Mechanism | Manual | ||

| Motorised/Automatic | |||

| By End-user | Utilities | ||

| Industrial Facilities | |||

| Commercial and Institutional Buildings | |||

| Renewable IPPs and Micro-grids | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Load Break Switch market?

The market stands at USD 3.29 billion in 2026 and is projected to reach USD 4.25 billion by 2031 at a 5.23% CAGR.

Which region leads the Load Break Switch market?

Asia-Pacific commands 38.45% of global revenue, driven by large-scale infrastructure and renewable investments.

Why are SF₆-free load break switches gaining traction?

Environmental regulations that phase out high-GWP gases are pushing utilities to adopt vacuum or eco-gas alternatives that cut lifecycle emissions by over 80%.

What segment is growing fastest by installation type?

Indoor panel-mounted switches show the highest growth at 7.18% CAGR because data centers and industrial plants prefer climate-controlled, secure environments.

How are commodity prices affecting manufacturers?

Record-high copper costs forced up to 45% price increases, squeezing margins for suppliers lacking hedging strategies.

Who are the major players in the Load Break Switch market?

Key companies include Schneider Electric, ABB, Siemens, Eaton and emerging entrants like Atom Power focusing on solid-state technology.

Page last updated on: