Live Sports Streaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

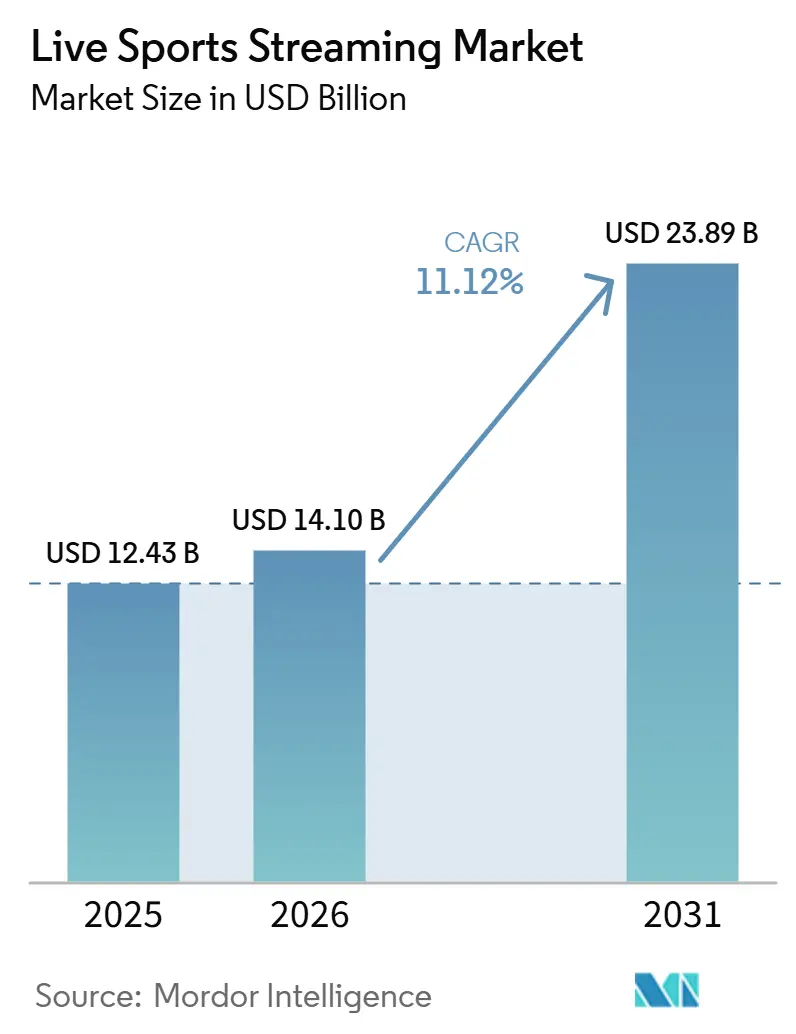

| Market Size (2026) | USD 14.10 Billion |

| Market Size (2031) | USD 23.89 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Live Sports Streaming Market Analysis by Mordor Intelligence

The live sports streaming market size is expected to increase from USD 12.43 billion in 2025 to USD 14.1 billion in 2026 and reach USD 23.89 billion by 2031, growing at a CAGR of 11.12% over 2026-2031. The live sports streaming market is moving deeper into direct distribution as leagues, broadcasters, and digital platforms place live rights at the center of subscriber growth and retention. The strongest momentum is coming from the continued move away from traditional television bundles, the wider use of connected devices, and steady investment in premium sports rights that can attract large audiences at once. This shift is also changing competition because diversified technology platforms can support sports spending with revenue from advertising, commerce, devices, and cloud services, while specialist streamers depend far more on the economics of sports alone. Growth opportunities in the live sports streaming market remain strongest where mobile access is broad, connected television usage is rising, and platforms can combine live coverage with advertising, interactivity, and localized viewing experiences. Margin pressure from rights inflation and the recurring threat of piracy still limit upside, but they also push the live sports streaming market toward larger platforms with the balance sheets and distribution reach to sustain premium rights over multiple cycles.

Key Report Takeaways

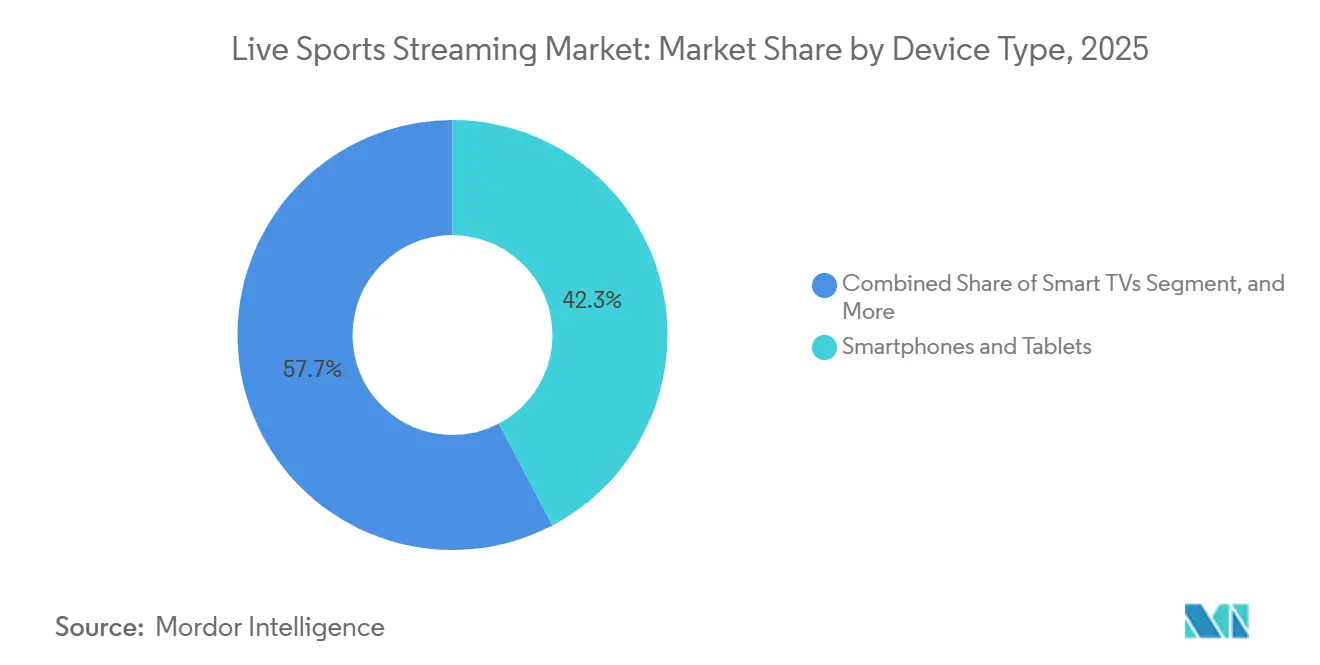

- By device type, smartphones and tablets held 42.31% share of the live sports streaming market in 2025, while smart TVs are projected to expand at 11.34% CAGR through 2031.

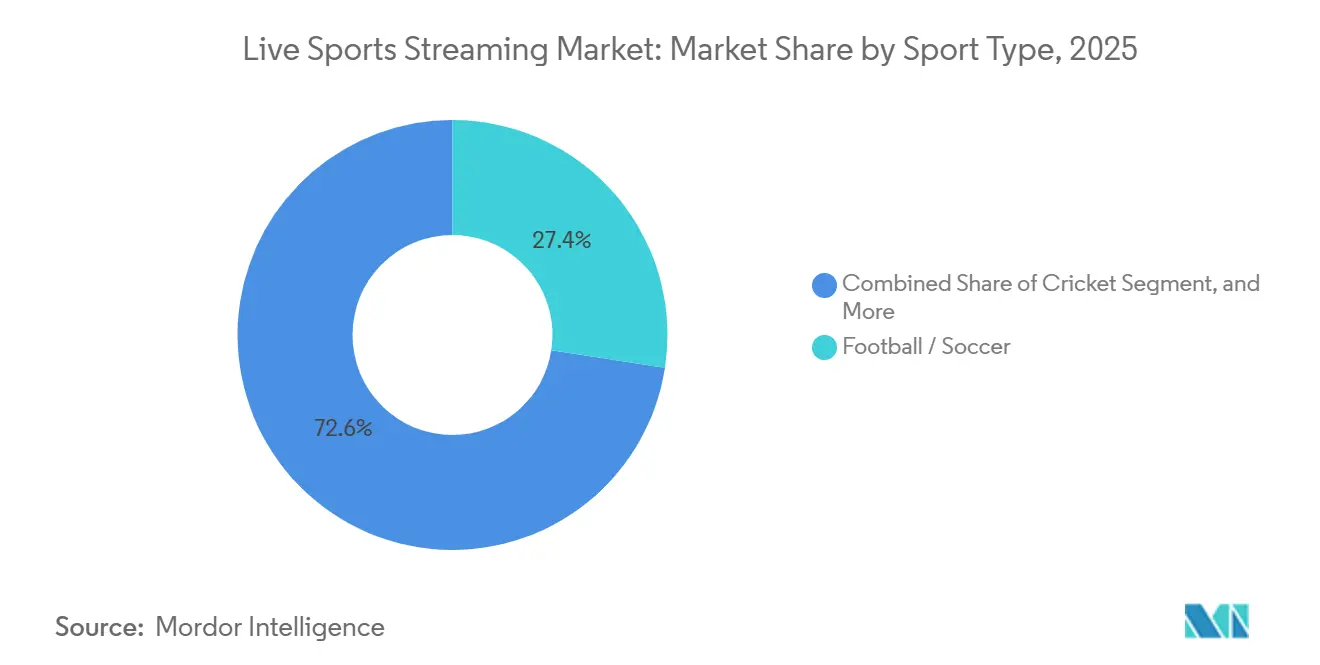

- By sport type, football/soccer accounted for 27.44% of the live sports streaming market share in 2025, while cricket is projected to advance at 11.43% CAGR through 2031.

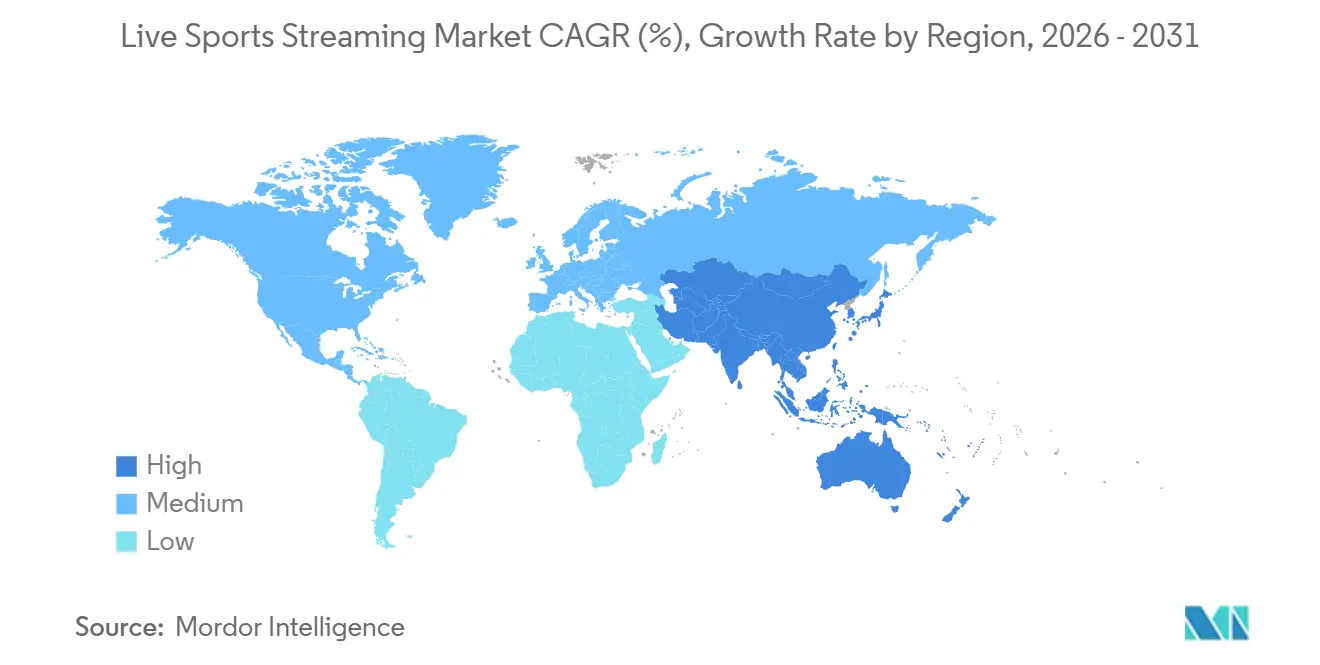

- By geography, North America held 32.53% share in 2025, while Asia-Pacific is expected to grow at 11.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Live Sports Streaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cord-Cutting and Shift From Pay TV to Direct-To-Consumer Sports | +3.5% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Expansion of Low-Latency 5G and Fiber Connectivity | +2.8% | Global, with Asia-Pacific and Middle East as accelerating markets | Medium term (2-4 years) |

| Escalating Value of Exclusive Sports Rights | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growth of Mobile-First Sports Consumption | +1.5% | Asia-Pacific, Africa, South America | Short term (≤ 2 years) |

| Ad-Supported Streaming Monetization for Live Sports | +1.2% | North America, Europe | Medium term (2-4 years) |

| Interactive Viewing, Betting, and Fan Engagement Features | +0.8% | North America, Europe, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cord-Cutting And Shift From Pay TV To Direct-To-Consumer Sports

The live sports streaming market is being pushed forward by the steady movement of sports rights from traditional television structures into direct digital distribution. Large rights packages now sit at the center of platform strategy because live events keep viewers engaged and reduce the risk of subscriber churn when major games are on the schedule. The pattern is visible across the live sports streaming market in the way conferences, leagues, and media groups are launching or expanding direct access products instead of depending only on older broadcast models. The Mountain West Conference launched MW+ in July 2026 as a direct-to-consumer platform, which showed that even collegiate properties are building their own digital route to fans and new revenue streams. The CW Network and ESPN also widened digital availability for college sports through their April 2026 agreement to place more than 800 hours of live CW Sports events on the ESPN App. As more rights holders see the value of direct fan relationships, the live sports streaming market gains a stronger base for subscriptions, advertising, and audience data that was harder to capture in legacy television arrangements.

Expansion Of Low-Latency 5G And Fiber Connectivity

The live sports streaming market is also benefiting from network improvements that make live delivery more reliable and more interactive. Better 5G and fiber access do more than reduce buffering because they support real-time overlays, camera switching, and synchronized viewing experiences that are harder to deliver on weaker networks. T-Mobile used its 5G Advanced Network at the 2025 PGA Championship to support a real-time augmented reality visualization layer that overlaid player shot data during the broadcast.[1]T-Mobile, “T-Mobile 5G Powers One of the Most Connected Majors Ever at 2025 PGA Championship,” Nasdaq, nasdaq.com That kind of deployment matters to the live sports streaming market because it turns network quality into a visible part of the product instead of a hidden technical feature. It also supports future growth in ad-supported viewing, in-play betting, and richer statistics displays that depend on low delay and stable transmission. As these capabilities become more common, platforms with stronger delivery architecture are likely to hold audiences for longer periods and compete more effectively for premium rights.

Escalating Value Of Exclusive Sports Rights

Exclusive rights remain one of the clearest growth drivers in the live sports streaming market because they shape where audiences go and how long they stay. The NBA announced an 11-year media rights agreement worth approximately USD 76 billion in July 2024, and the new structure took effect from the 2025-26 season across Disney, NBCUniversal, and Amazon Prime Video.[2]National Basketball Association, “NBA Announces New 11-Year Media Agreements,” NBA.com, nba.com Amazon also confirmed that Prime Video secured an 11-year streaming deal for NBA and WNBA rights, including regular-season games and knockout rounds of the Emirates NBA Cup. Netflix extended its NFL deal through the 2029-30 season in May 2026 and added more game windows and the NFL Honors awards show, which showed that league relationships are widening beyond a narrow set of marquee dates. This creates a reinforcing cycle inside the live sports streaming market because platforms with exclusive packages gain stronger subscriber demand, while leagues and federations gain more leverage in future negotiations. Over time, this pushes live sports rights higher on the strategic priority list for both global technology platforms and established media groups.

Growth Of Mobile-First Sports Consumption

Mobile usage remains one of the clearest demand anchors for the live sports streaming market, especially in regions where smartphones are the main screen for daily media use. Smartphones and tablets delivered 42.31% of global consumption in 2025, which reflected how large audiences still enter the category through mobile data rather than fixed television setups. JioStar reported that the TATA IPL 2026 season reached a cumulative audience of over 1.2 billion, with digital video views reaching 25 billion and regional-language watch time on digital rising 33%.[3]JioStar, “JioStar Takes TATA IPL 2026 Reach to an All-Time High of Over 1.2 Billion,” JioStar, jiostar.com JioStar also stated that JioHotstar reached 550 million monthly active users by March 2026, which underscored how sports streaming can operate at a very large scale on mobile-led platforms. This matters to the live sports streaming market because localized language support, efficient data usage, and simple payment paths can directly widen the paying and ad-supported audience. Platforms that treat mobile as a lasting consumption model instead of a temporary step are likely to stay closer to the fastest-growing user pools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sports Rights Inflation and Margin Pressure | -2.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Piracy and Unauthorized Restreaming of Live Events | -1.6% | Global, most severe in Southern Europe, India, and Middle East | Medium term (2-4 years) |

| Latency, Peak Load, and Network Quality Challenges | -0.9% | Emerging markets in Asia-Pacific and Africa | Medium term (2-4 years) |

| Fragmented Rights Holders and Windowing Complexity | -0.7% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Sports Rights Inflation And Margin Pressure

Rights inflation remains a major constraint on the live sports streaming market because premium properties are getting more expensive while subscriber and advertising returns do not rise at the same pace for every platform. The NBA's approximately USD 76 billion agreement raised the financial bar for top-tier sports packages and reinforced the view that future renewals will be negotiated from a higher base. This pressure is easier for large technology and media ecosystems to absorb because sports can support broader goals in retail, advertising, hardware, or cloud services. In contrast, pure-play sports services in the live sports streaming market depend more directly on whether each rights cycle can be monetized through subscriptions, sponsorships, and advertising around the events themselves. As a result, the live sports streaming market is becoming harder for narrowly focused operators to navigate at the premium end. That imbalance is likely to shape future bidding behavior and could further concentrate the most valuable rights among companies with deeper financial support.

Piracy And Unauthorized Restreaming Of Live Events

Piracy continues to take revenue and viewing time away from the live sports streaming market, especially during premium live events that attract large audiences at once. The September 2025 takedown of Streameast covered 80 associated domains that averaged 136 million monthly visits and 1.6 billion annual visits, which showed how large illicit sports streaming networks had become before enforcement action was taken. LALIGA reported that piracy detection in sports and other live events reached record levels in 2025 and stated that piracy still costs Spain's professional clubs and wider sports ecosystem EUR 600-700 million, or USD 651-759 million, each year. The same issue also adds friction to subscriber growth because fragmented legal access pushes some viewers toward unauthorized streams rather than paid services. For the live sports streaming market, the damage is not limited to lost subscriptions because it also weakens advertising value, distorts audience measurement, and reduces the return on expensive rights packages. Until enforcement tools become faster and more consistent across jurisdictions, piracy will remain a persistent drag on revenue quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Mobile Scale Leads While Smart TV Growth Gains Ground

Smartphones and tablets held 42.31% of the live sports streaming market share in 2025, which kept mobile at the center of audience reach across Asia-Pacific, Africa, and South America. In the live sports streaming market, that lead came from practical access patterns because many viewers entered live viewing through affordable mobile data plans and handheld screens rather than through dedicated home entertainment systems. The live sports streaming market also continues to benefit from mobile's ability to support regional languages, flexible viewing windows, and simpler access for fans who watch while commuting or multitasking. JioStar's IPL 2026 results showed how powerful that model remains because digital video views reached 25 billion and regional-language watch time on digital increased 33% during the season. The same release made clear that digital reach in live sports is not limited to major cities, which supports the mobile foundation of the live sports streaming market in high-volume regions.

Smart TVs, however, are expected to grow at 11.34% CAGR through 2031, which shows that living-room viewing is becoming more important as the live sports streaming market matures. JioStar stated in May 2026 that connected TV reach during TATA IPL 2026 grew 26% year over year, and that connected TV consumption rose 20%, with the season matching the previous season's full connected TV reach by game 45. That shift matters because larger screens support more premium ad placements, better picture quality, and a viewing habit that looks closer to traditional appointment television. Fox Corporation's announced USD 22 billion acquisition of Roku in June 2026 showed that device software and distribution control now matter almost as much as rights ownership in the live sports streaming industry. Laptops, desktops, gaming consoles, and portable streaming devices still serve important use cases, but the live sports streaming industry is increasingly defined by the balance between mobile scale and connected television monetization.

By Sport Type: Football Leads While Cricket Sets The Growth Pace

Football/soccer accounted for 27.44% share of the live sports streaming market size in 2025, which reflected the sport's unmatched international audience and the commercial pull of league and tournament rights. The live sports streaming market continues to rely on football as a durable traffic driver because domestic leagues, UEFA competitions, and major international tournaments create steady viewing demand across regions and seasons. Basketball also remains a major engine for the live sports streaming market, especially after the NBA's new media agreement moved national coverage more firmly into streaming distribution from the 2025-26 season. Baseball, motorsports, and tennis each support important clusters of loyal viewers, which helps platforms balance global tentpole events with sport-specific subscriber communities. That mix gives the live sports streaming market a wider demand base and reduces dependence on a single annual tournament cycle.

Cricket is projected to expand at 11.43% CAGR through 2031, which makes it the fastest-growing sport type in the live sports streaming market. JioStar reported that the TATA IPL 2026 season reached over 1.2 billion viewers, total watch time hit 870 billion minutes, and 125 new advertisers joined the platform, which showed how concentrated cricket audiences can translate into very strong commercial value. JioHotstar also set a global concurrent streaming record of 72.5 million viewers during the ICC Men's T20 World Cup 2026 final in India, which underlined cricket's ability to test and prove platform scale during short, intense demand windows. Zee Entertainment's move to secure FIFA rights in India through 2034 showed that major media groups are broadening their sports portfolios beyond cricket, which could gradually spread viewer attention and advertising budgets across more properties over time. Even so, cricket remains one of the clearest growth engines inside the live sports streaming market because of its scale in South Asia and its strong pull among diaspora audiences.

Geography Analysis

North America held 32.53% of the live sports streaming market share in 2025, which kept it in the leading regional position because revenue per user is high and premium rights are deeply embedded in viewer habits. The live sports streaming market in North America is also shaped by a dense pipeline of high-value rights, with the NFL, NBA, college sports, and other major properties spread across several large digital platforms. Amazon strengthened that position through its NBA and WNBA streaming agreement, which added a major year-round property to a sports portfolio that already included the NFL and important European football rights. Netflix widened its NFL relationship in May 2026 by extending the deal through the 2029-30 season and adding more game windows and the NFL Honors awards show. The CW Network and ESPN added another layer of digital reach in April 2026 by making the ESPN App the exclusive streaming home for all CW Sports live events, which expanded access to more than 800 hours of live coverage each year.

Asia-Pacific is expected to grow at 11.46% CAGR through 2031, which makes it the fastest-growing regional engine in the live sports streaming market. The region's strength comes from a combination of mass cricket audiences, mobile-first access, and the ability of large platforms to reach viewers in multiple languages and price points. JioHotstar's 72.5 million peak concurrent viewers during the ICC Men's T20 World Cup 2026 final set a global benchmark and showed how large the live sports streaming market can become when infrastructure and audience concentration align. In South America, CazéTV secured an exclusive six-season LaLiga agreement in Brazil for all 380 matches from 2026-27 through 2031-32 and will distribute them live and free through YouTube and partner streaming services, which supports ad-led access models in price-sensitive markets.

Europe remains important to the live sports streaming market, but its rights structure is more fragmented and often requires fans to move across several services to follow all major competitions. That fragmentation can support competition, but it can also increase churn and make illegal alternatives more attractive when access becomes too complex or too expensive. LALIGA stated in November 2025 that it pressed for binding anti-piracy legislation after the European Union Intellectual Property Office found that voluntary measures had lost effectiveness against increasingly sophisticated pirate networks. In the Middle East, beIN Media Group remains a key rights holder across Gulf and North Africa markets, while Africa's live sports streaming market is still in an early growth phase led by urban demand in countries such as South Africa, Egypt, and Nigeria. Across those markets, payment systems and content delivery build-out still matter as much as audience appetite, which means regional expansion depends on both demand and execution.

Competitive Landscape

The live sports streaming market is moderately consolidated at the top, but it remains diverse below that level because global platforms, league-owned services, and regional specialists all play different roles. Amazon, Alphabet, and Apple have treated live sports as part of a broader ecosystem strategy, which gives them more room to invest than platforms whose business depends mainly on sports subscriptions. This difference affects the live sports streaming market because premium rights are expensive, renewal cycles are frequent, and the ability to support sports spending with revenue from other activities creates a lasting advantage. Amazon's NBA and WNBA agreement, added to its NFL and European football portfolio, is one of the clearest examples of a scaled platform building a year-round sports presence across several major properties. Netflix's expanded NFL arrangement showed a similar pattern because it moved from a narrow event package toward a broader annual relationship with the league. These moves raise the competitive bar for the rest of the live sports streaming market because they combine rights access, platform scale, and strong consumer visibility.

Specialist platforms are responding by going deeper into selected sports or communities rather than matching the broad rights portfolios of larger technology groups. DAZN's 2025 agreement with Premier Boxing Champions reflected that approach because it strengthened DAZN's position in a sport where dedicated fans value depth, regular scheduling, and consistent international availability. League-owned offers such as NFL+, MLB.TV, and F1 TV also remain relevant in the live sports streaming market because they provide fans with direct access and a degree of sport-specific coverage that broader aggregators do not always replicate. Regional services such as Viaplay, CANAL+, ViX, SonyLIV, and JioHotstar remain important because local language, culture, and rights structures still shape how fans choose platforms. This keeps the live sports streaming market from becoming a simple winner-take-all contest even as top rights continue to cluster among the largest players.

A second layer of competition is forming around interactivity, advertising quality, and control of the connected television environment. Fox Corporation's announced USD 22 billion acquisition of Roku showed that ownership of the operating system and ad technology stack is becoming strategically important for companies that want stronger control over sports discovery and monetization. FanDuel Sports Network reported a 25% year-over-year increase in total ad impressions through Magnite's SpringServe platform in 2025, which highlighted the value of improving ad execution around live sports inventory. Monumental Sports Network launched integrated betting and gamification features for Capitals and Wizards streams in February 2025 and later extended similar features to Mystics games in June 2025, which showed that interactivity is spreading beyond a single sport or audience segment. TAPPP and BetPlay also launched an end-to-end betting experience on live television football in Colombia in May 2025, which showed that the live sports streaming market is testing new monetization models well beyond North America.

Live Sports Streaming Industry Leaders

Amazon.com, Inc.

The Walt Disney Company

DAZN Group Limited

Warner Bros. Discovery, Inc.

Paramount Skydance Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: The Mountain West Conference launched MW+, a new subscription video-on-demand streaming platform powered by Kiswe, providing fans direct-to-consumer access to college sports events. The platform introduces a new revenue-sharing model for college athletics, decoupling sports streaming rights from traditional broadcast network arrangements and positioning the conference for DTC monetization.

- July 2026: Australia's National Rugby League announced a new broadcast rights deal valued at approximately AUD 5.3 billion (approximately USD 3.4 billion) over 7 years commencing after the 2027 season, with Channel Nine retaining free-to-air rights and Foxtel Group continuing as pay-TV partner. The deal is explicitly structured to "future-proof" the league through an expanded digital streaming strategy that shifts draw control from broadcasters to the league itself.

- June 2026: Fox Corporation announced an agreement to acquire Roku for USD 22 billion, combining Fox's sports and news content with Roku's connected TV operating system and 90+ million active accounts. The acquisition signals a major strategic expansion by a traditional broadcaster into the connected TV distribution and programmatic advertising technology stack.

- April 2026: The CW Network and ESPN announced a partnership making the ESPN App the exclusive streaming home for all CW Sports live events, covering 800+ hours annually including ACC, Pac-12, and Mountain West college sports, NASCAR O'Reilly Auto Parts Series, and WWE NXT, expected to launch in summer 2026.

Global Live Sports Streaming Market Report Scope

Live Sports Streaming Market refers to the ecosystem of platforms, technologies, and services that deliver sports events in real time over the internet. It includes OTT apps, broadcaster-owned digital platforms, and third-party streaming services that let viewers watch matches on mobile, web, and connected TV devices.

The Live Sports Streaming Market Report is Segmented by Device Type (Smartphones and Tablets, Smart TVs, and Laptops and Desktops), Sport Type (Football/Soccer, Baseball, Basketball, Cricket, Motorsports, and Tennis), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Type |

| Football Soccer |

| Baseball |

| Basketball |

| Cricket |

| Motorsports |

| Tennis |

| Other Sport Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Type | ||

| By Sport Type | Football Soccer | |

| Baseball | ||

| Basketball | ||

| Cricket | ||

| Motorsports | ||

| Tennis | ||

| Other Sport Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the live sports streaming market?

The live sports streaming market stood at USD 12.43 billion in 2025, is valued at USD 14.1 billion in 2026, and is forecast to reach USD 23.89 billion by 2031 at an 11.12% CAGR over 2026-2031.

Which device category leads live sports streaming demand?

Smartphones and tablets led with 42.31% share in 2025, mainly because mobile access remains the most common viewing route in many high-growth markets.

Which device category is growing the fastest through 2031?

Smart TVs are the fastest-growing device type with an 11.34% CAGR through 2031, supported by rising connected television use and stronger large-screen viewing habits.

Which sport generates the largest share of streaming demand?

Football/soccer held the largest sport-type share at 27.44% in 2025 because of its broad international fan base and steady flow of premium league and tournament rights.

Why is cricket growing faster than other sports on streaming platforms?

Cricket is forecast to grow at 11.43% CAGR through 2031 because major tournaments in South Asia attract very large digital audiences and create strong advertising and engagement opportunities in short event windows.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is projected to grow at 11.46% CAGR through 2031, supported by mobile-first access, large cricket audiences, and platform models built around language localization and broad digital reach.

Page last updated on: