Lithium Compound for Battery Application Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

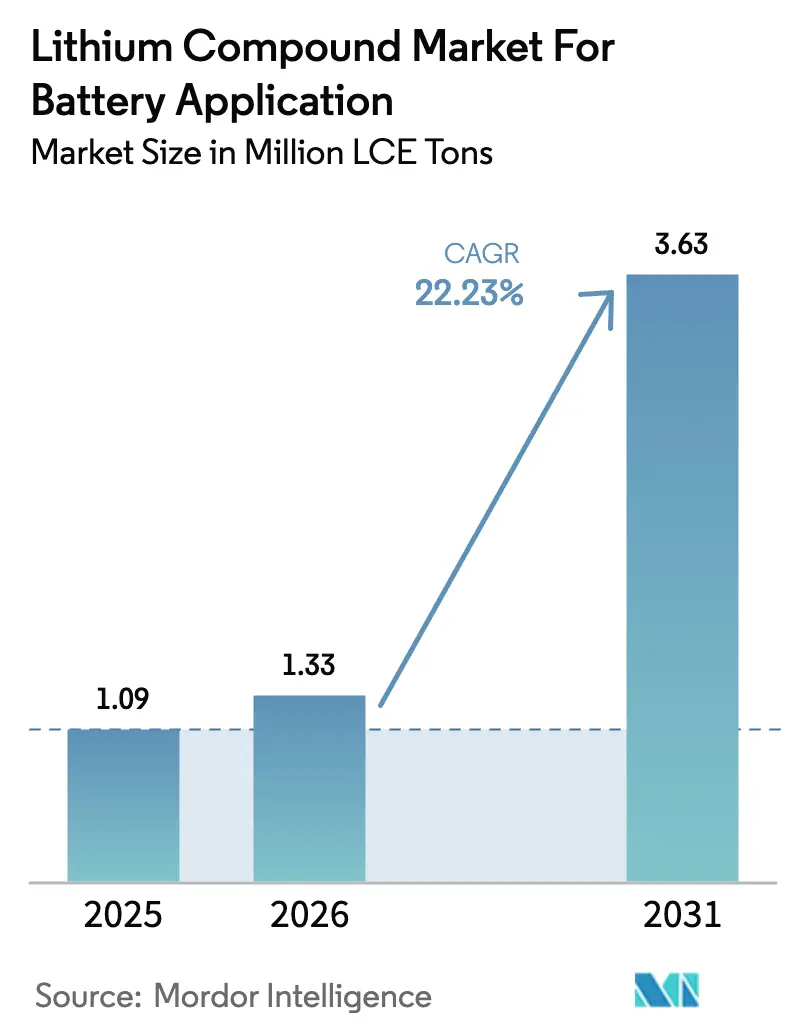

| Market Volume (2026) | 1.33 Million LCE tons |

| Market Volume (2031) | 3.63 Million LCE tons |

| Growth Rate (2026 - 2031) | 22.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithium Compound for Battery Application Market Analysis by Mordor Intelligence

The Lithium Compound for Battery Application Market Industry size was valued at 1.09 LCE million tons in 2025 and is estimated to grow from 1.33 LCE million tons in 2026 to reach 3.63 LCE million tons by 2031, at a CAGR of 22.23% during the forecast period (2026-2031). Electric-vehicle mandates, grid-scale storage procurement, and a shift to high-nickel cathodes—consuming more lithium per kilowatt-hour than previous chemistries—drive the sharp expansion. While automotive demand, particularly from China, the European Union, and North America, anchors volume, emerging utility storage projects broaden the addressable base. Although lithium carbonate maintains its cost leadership for LFP cells, lithium hydroxide is gaining traction as automakers ramp up their nickel-rich NCM and NCA programs. Integrated Asian refineries bolster regional dominance but simultaneously highlight supply security vulnerabilities for the U.S. and Europe. Leading producers, through midstream-to-upstream integration, not only safeguard their margins but also adeptly pivot between carbonate and hydroxide in response to shifting price signals.

Key Report Takeaways

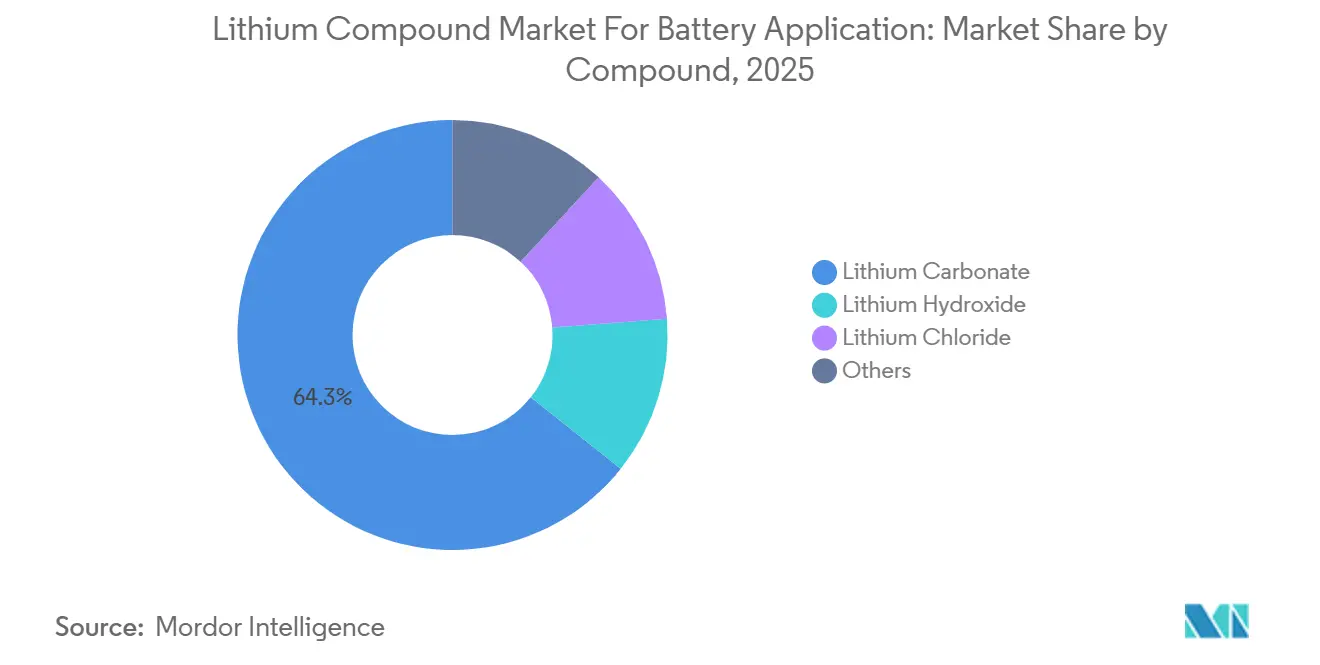

- By compound, lithium carbonate led with 64.31% of the lithium compound market share in 2025, and is forecast to advance at a 22.79% CAGR through 2031.

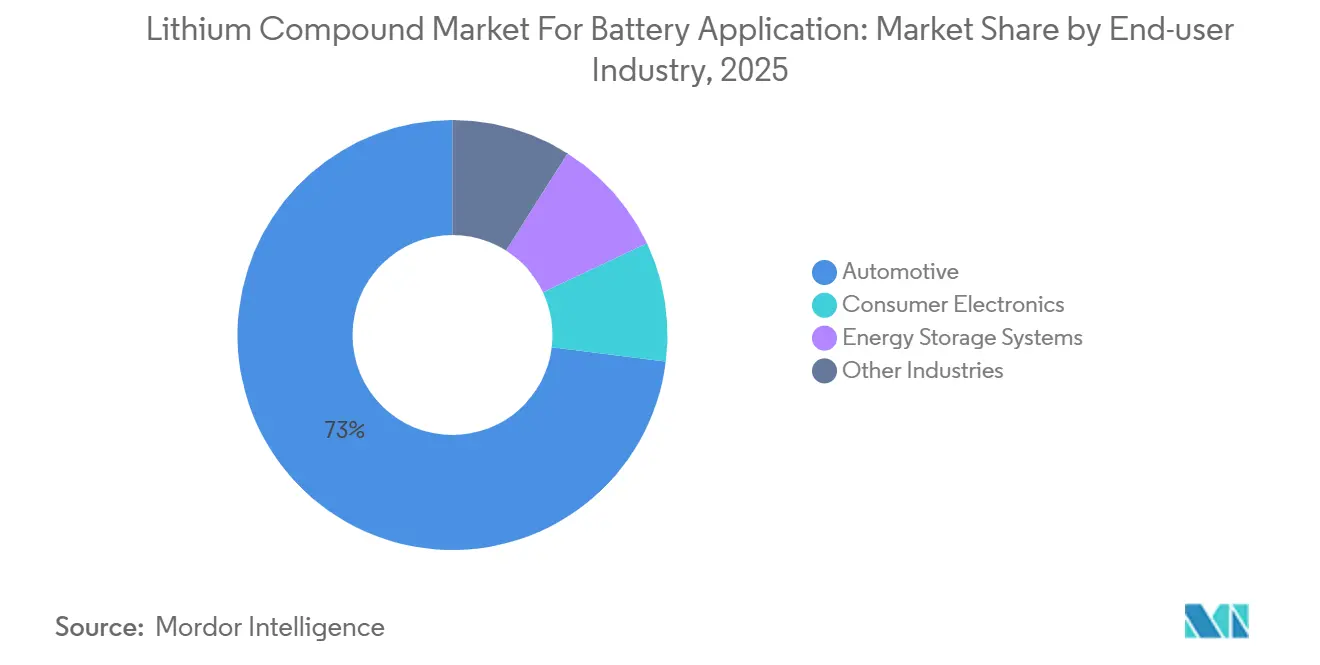

- By end-user industry, automotive applications captured 73.02% of volume in 2025 and are slated to expand at a 23.01% CAGR to 2031.

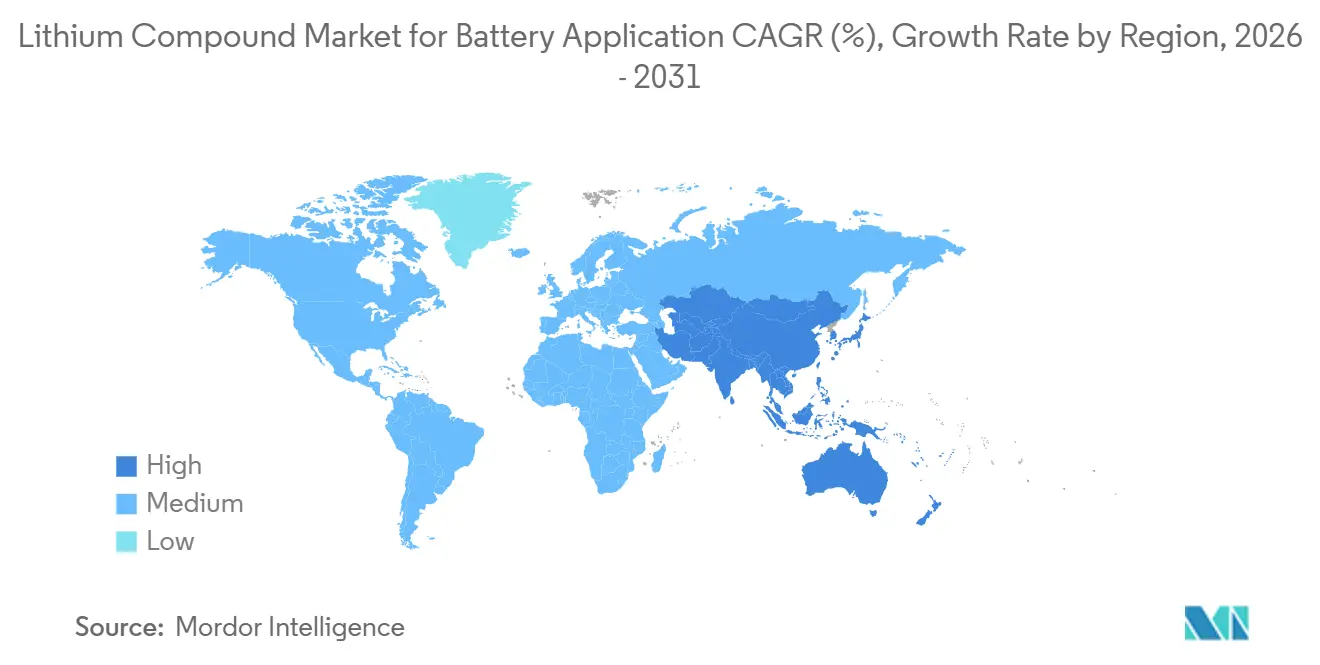

- By geography, Asia-Pacific commanded 64.86% of the lithium compound market size in 2025 and is projected to maintain the fastest regional CAGR of 23.85% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lithium Compound for Battery Application Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in electric-vehicle adoption | +6.2% | Global, with concentration in China, EU, North America | Medium term (2-4 years) |

| Growth in renewable-energy storage deployments | +4.8% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Expansion of consumer electronics and power tools | +2.1% | Global, led by APAC manufacturing hubs | Short term (≤ 2 years) |

| Localization of battery supply chains in emerging economies | +3.9% | India, Indonesia, Mexico, Morocco | Long term (≥ 4 years) |

| Higher Li-intensity from high-nickel and solid-state chemistries | +4.3% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Electric-Vehicle Adoption

In 2025, global sales of passenger and commercial electric vehicles (EVs) surpassed significant milestones, solidifying a robust demand for battery-grade lithium compounds. Fleets in Europe and North America, emphasizing higher mileage, are gravitating towards nickel-rich cells. These cells are driving a surge in hydroxide adoption. Meanwhile, China plays a crucial role: domestic OEMs dispatched a substantial number of EVs, capitalizing on cost-effective lithium iron phosphate (LFP) packs derived from carbonate feedstock. Thanks to incentives from the Inflation Reduction Act, North America saw a flurry of commitments for cell plants[1]U.S. Department of Energy, “IRA Battery Manufacturing Grants 2025,” energy.gov. Each plant is poised to draw in an annual supply of lithium carbonate equivalent (LCE). As the divide between high-nickel and LFP strategies widens, both carbonate and hydroxide markets are set for simultaneous growth. Furthermore, the electrification of commercial vehicles, spanning from city buses to medium-duty trucks, introduces a consistent demand throughout the year.

Growth in Renewable-Energy Storage Deployments

Utility-scale battery installations are expected to continue climbing as solar and wind build-outs require firming capacity. California's Self-Generation Incentive Program has authorized significant funding for residential systems, predominantly utilizing LFP cells that depend on lithium carbonate. China's newly introduced storage-mandate policy for wind and solar plants is spurring demand for LFP modules. In India, a tender for storage underscores the nation's escalating grid-balancing demands, even as financing models lean towards shorter-duration assets with reduced lithium reliance. While long-duration chemistries like iron-air are poised to carve out niches in the latter part of the decade, they remain in their commercial infancy, ensuring lithium's dominance at least until 2031.

Localization of Battery Supply Chains in Emerging Economies

In a bid to diversify supply and bolster local value addition, India, Indonesia, Mexico, and Morocco have collectively pledged significant investments in 2024-2025 towards domestic cell and precursor plants[2]Ministry of Heavy Industries India, “PLI Scheme for ACC Battery Storage,” heavyindustries.gov.in. India's Production Linked Incentive program is backing five gigafactories, eyeing a combined target of substantial capacity. Indonesia's nickel export regulations, tied to local smelting, have inadvertently boosted imports of hydroxide for co-precipitation with nickel sulfate. Mexico, capitalizing on USMCA's origin rules, has secured U.S. tax credits, drawing a wave of investors from upstream to packaging into Nuevo León. In Morocco, a collaboration with Gotion High-Tech is weaving local phosphate resources into LFP cathodes, ensuring a steady stream of lithium carbonate. These initiatives challenge China's historical grip on global cell production. However, hurdles like permitting delays and a shortage of skilled labor have already pushed many commissioning timelines to 2028.

Higher Li-Intensity from High-Nickel and Solid-State Chemistries

Cathode recipes now boast high nickel content, boosting lithium demand per kilowatt-hour compared to traditional NCM 6-2-2 blends. General Motors’ Ultium platform mandates NCM 90-5-5 cells, consuming LiOH per kWh. Meanwhile, BMW’s Neue Klasse cylinders opt for NCA cathodes, achieving high energy density, also dependent on hydroxide routes. Solid-state prototypes from QuantumScape and Toyota, featuring lithium-metal anodes and sulfide electrolytes, incorporate additional lithium salts per kWh to stabilize interfaces. As pilot lines advance, hydroxide and specialty salts, like lithium sulfide, are poised to outpace carbonate in premium models.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain bottlenecks and spodumene shortages | -2.7% | Australia, China refining hubs | Short term (≤ 2 years) |

| Stringent water-use and environmental regulations | -1.9% | Chile, Argentina, Nevada | Medium term (2-4 years) |

| Lithium-price volatility driven by speculation | -1.5% | Global, concentrated in China spot markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Bottlenecks and Spodumene Shortages

In 2025, Australian miners curtailed spodumene concentrate production as prices fell. This move reduced feedstock for Chinese converters and brought refinery inventories down to minimal levels. Typically, new hard-rock capacities take several months from the final investment decision to produce their first product. Thus, today's cancellations hint at potential shortages for the growing electric vehicle (EV) market in the late decade. Liontown's delay of the Kathleen Valley project means a loss of additional supply from the chain. With EV sales set to grow annually, demand for spodumene could surpass economically viable supply in the coming years. While brines offer some respite, they come with environmental challenges, and direct lithium extraction technologies are still in the pilot phase. Without a consistent price rebound to bolster mine cash flows, the lithium compound market may face periodic squeezes, jeopardizing stable planning downstream.

Stringent Water-Use and Environmental Regulations

Updated Atacama permits in Chile now cap brine extraction, curbing SQM and Albemarle's ability to expand carbonate capacity without investing in desalination. In Argentina, provincial governments are tightening water-balance audits at the Salar del Hombre Muerto, leading to longer permitting cycles for brownfield expansions. Meanwhile, Nevada’s Division of Water Resources has introduced groundwater modeling requirements, potentially adding two to three years to project development timelines. Environmental pressures are also focusing on carbon footprints: the European Union's proposed Battery Passport mandates life-cycle disclosures. This move not only incentivizes low-emission DLE routes but also complicates capitalization for smaller players. If mitigation measures don't keep pace with regulatory timelines, compliance costs and permitting delays could reduce the forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compound: Carbonate Retains Scale While Hydroxide Accelerates Premium Growth

Lithium carbonate held 64.31% of the 2025 volume, primarily due to its pivotal role in LFP cathodes. These cathodes are the backbone of China's burgeoning mass-market electric vehicle (EV) and stationary energy segments. LFP battery packs achieved a notable milestone, reaching total system costs that underscored their competitiveness and highlighted a significant advantage over nickel-based chemistries, further bolstering the demand for lithium carbonate. The lithium compound market size for carbonate applications is projected to advance at a 22.79% CAGR, driven by the swift electrification of two-wheelers and a growing emphasis on energy storage. Meanwhile, lithium hydroxide, while accounting for a significant portion of the 2025 output, commanded a premium, contributing a disproportionately higher share of revenue. This was largely due to battery-grade premiums. The dynamics between the two products reveal a strategic balance: while lithium carbonate ensures volume stability, lithium hydroxide offers enhanced profit margins and greater bargaining power.

While second-tier compounds like lithium chloride, fluoride, oxide, and sulfide constituted about 6% of the 2025 volume, their significance looms large in niche applications. For instance, developers of solid-state electrolytes turn to high-purity lithium chloride, essential for crafting sulfide-based films. These films boast ionic conductivities exceeding 10 mS/cm, a benchmark that mainstream carbonate routes struggle to achieve. Lithium fluoride, on the other hand, plays a crucial role as a high-voltage electrolyte additive, preventing transition-metal dissolution in 4.5-V NM cathodes. Notably, prices for these specialty salts can outstrip carbonate benchmarks. Furthermore, demand for these compounds closely follows research and development milestones set by major OEMs. As pilot production lines transition from gram-scale experiments to ton-scale operations, specialty producers stand poised to carve out lucrative micro-markets. These markets, rich in intellectual property, may not boast high tonnage but promise significant value.

By End-User Industry: Automotive Dominates While Energy Storage Systems Rise Fast

Automotive applications absorbed 73.02% of 2025 volume and will expand at 23.01% CAGR through 2031. While mass-market sedans utilize cost-effective LFP packs, premium crossovers and trucks are turning to nickel-rich cells, boosting the flow of hydroxide. Tesla’s Semi heavy-duty truck, with its 900 kWh pack, underscores the intensity of commercial vehicle demand. While policy clarity surrounding the EU's 2035 phase-out of combustion engines bolsters demand, it's worth noting that subsidy reductions in certain member states highlight the critical need for cost efficiencies. By 2031, the lithium compound market size dedicated to automotive supply is projected to surpass significant levels, underscoring its strategic significance.

Energy storage systems (ESS) held a notable share of the volume in 2025. However, as grids increasingly adopt four-hour batteries for renewable energy smoothing, the market share for lithium compounds in ESS is set to surge. Initiatives like California’s Manatee project and mandates from various provinces in China are already propelling ESS consumption to substantial levels annually. Meanwhile, consumer electronics, holding a considerable market share, are witnessing modest growth as the market for smartphones and laptops nears saturation. The "other industries" segment—encompassing medical, aerospace, and power tools—constitutes a small portion of the overall demand. However, this segment commands premium margins, thanks to its rigorous traceability and performance standards.

Geography Analysis

Asia-Pacific controlled 64.86% of the 2025 volume and 23.85% CAGR through 2031, reinforcing the region’s stewardship of the lithium compound market. China, a significant player, refined a substantial amount of LCE, primarily servicing cell plants in its Guangdong, Jiangsu, and Sichuan provinces. Ganfeng's Xinyu refinery, with an annual capacity, adeptly shifts between producing carbonate and hydroxide, responding to fluctuations in nickel prices. While India imported a substantial percentage of its LCE requirement in 2025, the nation is accelerating domestic exploration efforts in Jammu and Kashmir, with hopes of curbing its import reliance by the decade's end. Both Japan and South Korea, despite being net importers, leverage their processing expertise through giants like Panasonic and LG Energy Solution, collectively utilizing LCE for their cylindrical and pouch-cell productions.

North America accounted for a notable share of the 2025 demand. At Albemarle's Silver Peak brine site, carbonate was produced, and the company is pushing forward with plans for an annual capacity hydroxide facility at Kings Mountain, aiming for a 2027 launch. Lithium Americas' Thacker Pass project, having navigated federal approvals, is set to commence in 2027 with an output of carbonate. In Quebec, Canada’s Nemaska is reviving operations to add hydroxide, utilizing hydropower for a greener processing approach. Meanwhile, Mexico's growing electric vehicle hub in Nuevo León anticipates a demand of LCE annually by 2028, with supplies expected from both South American brines and potential resources in Sonora.

Europe secured a portion of the global lithium volume in 2025, hampered by a scarcity of local ore. Germany's Vulcan Energy is pioneering geothermal-brine extraction, targeting an output of hydroxide in 2026, with ambitions to scale up by 2028. In France, Imerys is evaluating the feasibility of extracting hydroxide from its Beauvoir site starting in 2028. The UK, while benefiting from grants under the Automotive Transformation Fund for cell assembly, still faces refining shortfalls, leading to a reliance on hydroxide imports from Asia. In South America, both Chile and Argentina were responsible for a significant share of the primary lithium output in 2025. Meanwhile, in the Middle East, Saudi Arabia is investing in direct lithium extraction (DLE) pilots on Red Sea brines, hinting at the emergence of new low-carbon supply sources.

Competitive Landscape

The lithium compound market for battery applications is moderately consolidated. Albemarle leverages joint ownership of Wodgina to secure spodumene feedstock for its Kemerton hydroxide plant. Ganfeng operates hard-rock mines in Australia and brine assets in Argentina, allowing feedstock arbitrage and rapid response to price signals. ISO 9001 and ISO 17034 certifications have turned into gating factors for OEM qualification, raising hurdles for new converters. Integrated incumbents thus wield scale and balance-sheet strength to weather volatility and shape contract terms.

Lithium Compound for Battery Application Industry Leaders

Jiangxi Ganfeng Lithium Group Co., Ltd.

Albemarle Corporation

SQM S.A.

Tianqi Lithium Co., Ltd.

Arcadium Lithium

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Royal Court of Jersey cleared Rio Tinto’s USD 6.7 billion acquisition of Arcadium Lithium; the renamed Rio Tinto Lithium now adds the Rincon brine project to its suite.

- March 2024: Mineral Resources announced plans to establish a lithium processing hub in the southern Goldfields region. This followed a Binding Heads of Agreement with Poseidon Nickel to acquire the Lake Johnston nickel concentrator plant and associated tenure, supporting the development of its battery-grade lithium production capabilities.

Global Lithium Compound for Battery Application Market Report Scope

The lithium compound market for battery applications is defined as the market encompassing high-purity chemical compounds, primarily lithium carbonate and lithium hydroxide, along with lithium chloride and other essential compounds. These compounds are integral to the production of cathodes and electrolytes in rechargeable lithium-ion batteries.

The lithium market is segmented by compound, end-user industry, and geography. By compound, the market is segmented into lithium carbonate, lithium hydroxide, lithium chloride, and others (including lithium oxide, lithium fluoride, lithium sulfide, and lithium sulfate). By end-user industry, the market is segmented into automotive (electric vehicles), consumer electronics, energy storage systems, and other industries (such as power tools, aerospace, etc.). The report also covers the market size and forecasts in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (LCE Tons).

| Lithium Carbonate |

| Lithium Hydroxide |

| Lithium Chloride |

| Others (Lithium Oxide, Lithium Fluoride, Lithium Sulfide, and Lithium Sulfate) |

| Automotive (Electric Vehicles) |

| Consumer Electronics |

| Energy Storage Systems |

| Other Industries (Power tools, Aerospace, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Compound | Lithium Carbonate | |

| Lithium Hydroxide | ||

| Lithium Chloride | ||

| Others (Lithium Oxide, Lithium Fluoride, Lithium Sulfide, and Lithium Sulfate) | ||

| By End-user Industry | Automotive (Electric Vehicles) | |

| Consumer Electronics | ||

| Energy Storage Systems | ||

| Other Industries (Power tools, Aerospace, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for battery-grade lithium compounds be by 2031?

Forecasts indicate the lithium compound market will reach 3.63 LCE million tons by 2031, expanding at a 22.23% CAGR from 1.33LCE million tons in 2026.

Which product type is growing fastest within battery-grade lithium supply?

Lithium hydroxide posts the highest growth as nickel-rich NCM and NCA chemistries for long-range vehicles rely on hydroxide precursors.

Why does Asia-Pacific dominate the lithium supply chain?

The region refines the majority of global feedstock, and the Asia-Pacific region controlled 64.86% of the 2025 volume.

What risks could slow lithium supply expansion?

Spodumene price collapses, stringent water-use rules in brine basins, and multi-year permitting timelines for new mines pose the largest near-term risks.

How are automakers securing lithium availability?

Strategies include direct investment in mining projects, long-term offtake contracts, and partnerships with emerging DLE providers to diversify sources.

Will solid-state batteries reduce lithium demand?

Solid-state designs use lithium-metal anodes and, in many cases, lithium-sulfide electrolytes, increasing lithium intensity per kilowatt-hour in the medium term.

Page last updated on: