Liquid Filled Hard Capsules Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.85 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

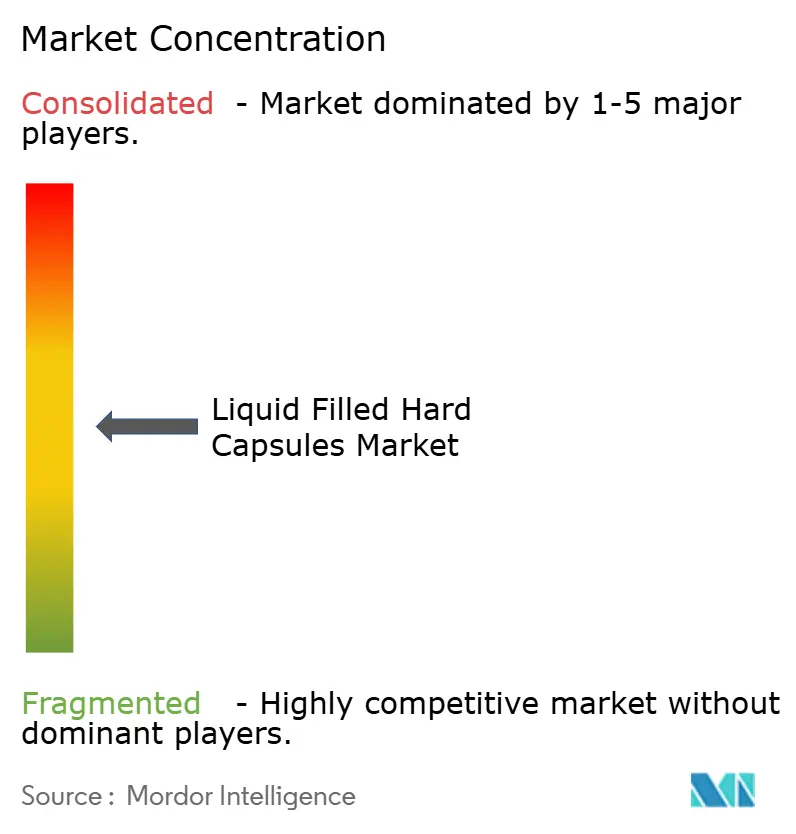

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Filled Hard Capsules Market Analysis by Mordor Intelligence

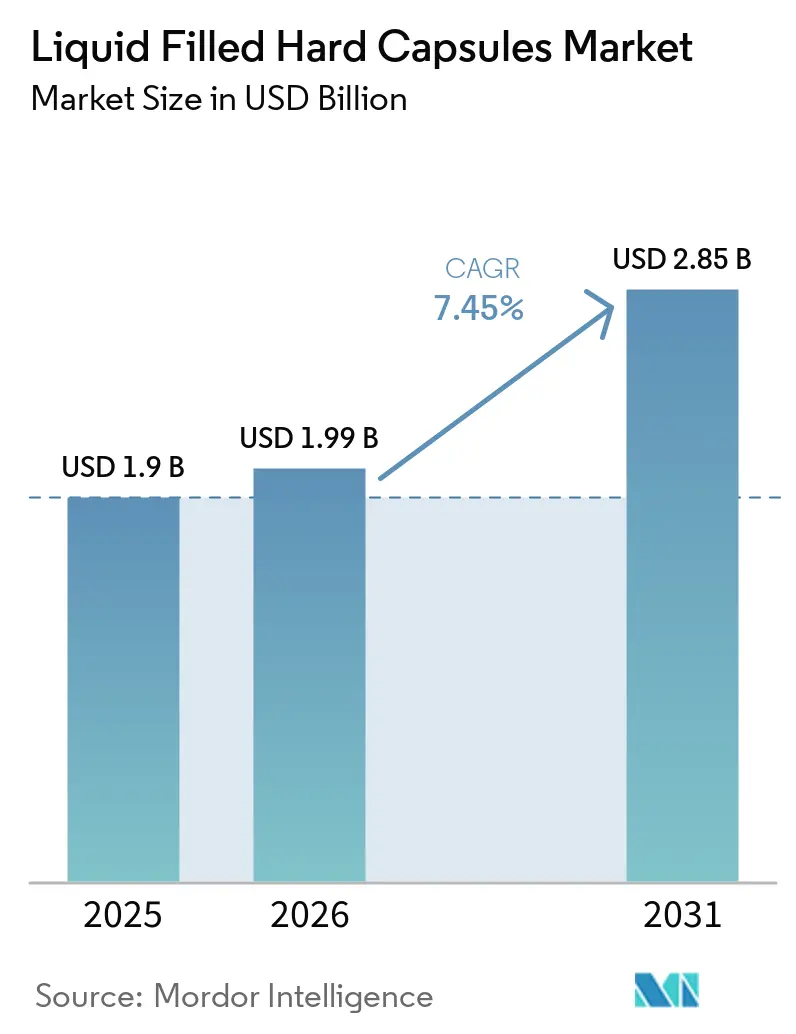

The Liquid Filled Hard Capsules Market size is projected to be USD 1.9 billion in 2025, USD 1.99 billion in 2026, and reach USD 2.85 billion by 2031, growing at a CAGR of 7.45% from 2026 to 2031.

Strong demand is anchored in the industry shift toward bioavailability-first oral delivery for poorly soluble APIs, where lipid-based fills like SEDDS and SMEDDS are advancing absorption and dose predictability. The liquid filled hard capsules market reflects manufacturers’ preference for moisture-stable HPMC shells in use cases where gelatin cross-linking risks would degrade dissolution behavior[1]ACG, “ACGcaps H+ Clean Label Vegetarian Capsules,” ACG, acg-world.com. Equipment innovation is also setting a faster operating baseline, with modern high-throughput filling systems scaling to 210,000 capsules per hour while maintaining in-line controls for quality and integrity. In parallel, fusion sealing platforms designed for hermetic closure and oxygen control are expanding premium applications in both pharmaceuticals and nutraceuticals.

Key Report Takeaways

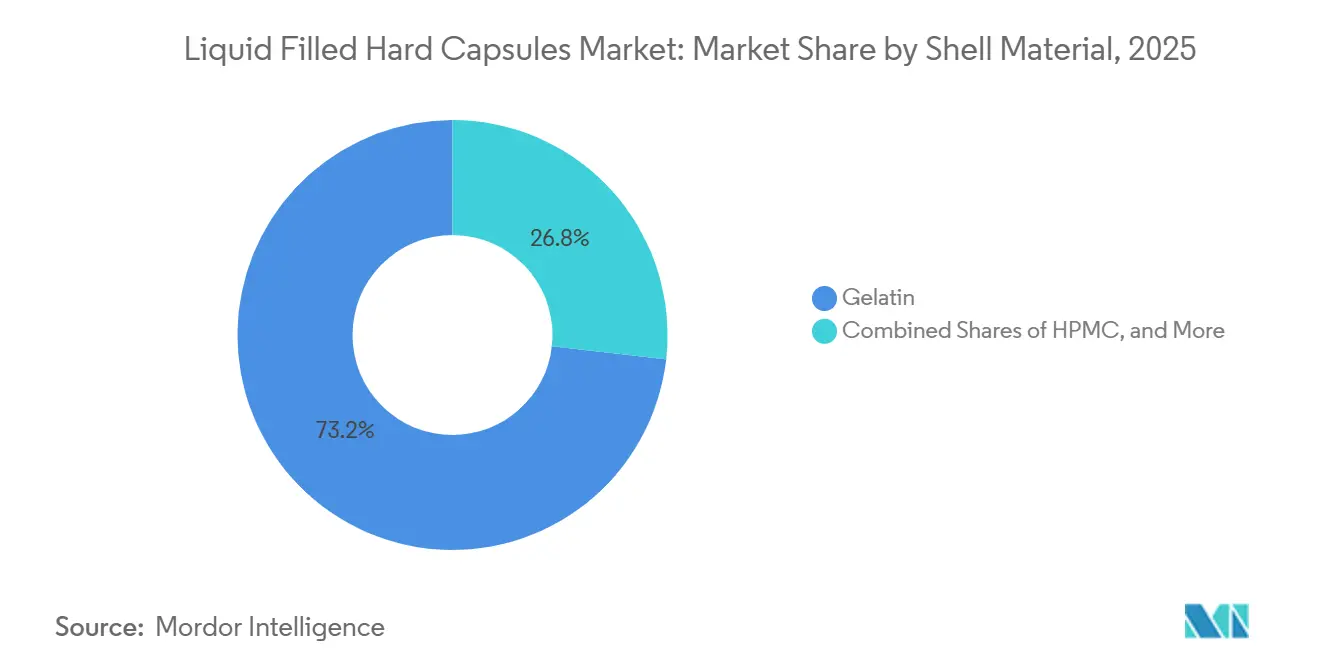

- By shell material, gelatin held 73.24% of the liquid filled hard capsules market share in 2025, while HPMC is projected to expand at an 8.51% CAGR through 2031.

- By filling state, oil-based liquids accounted for 45.32% share of the liquid filled hard capsules market size in 2025, and self-emulsifying systems (SEDDS/SMEDDS) are projected at a 9.85% CAGR to 2031.

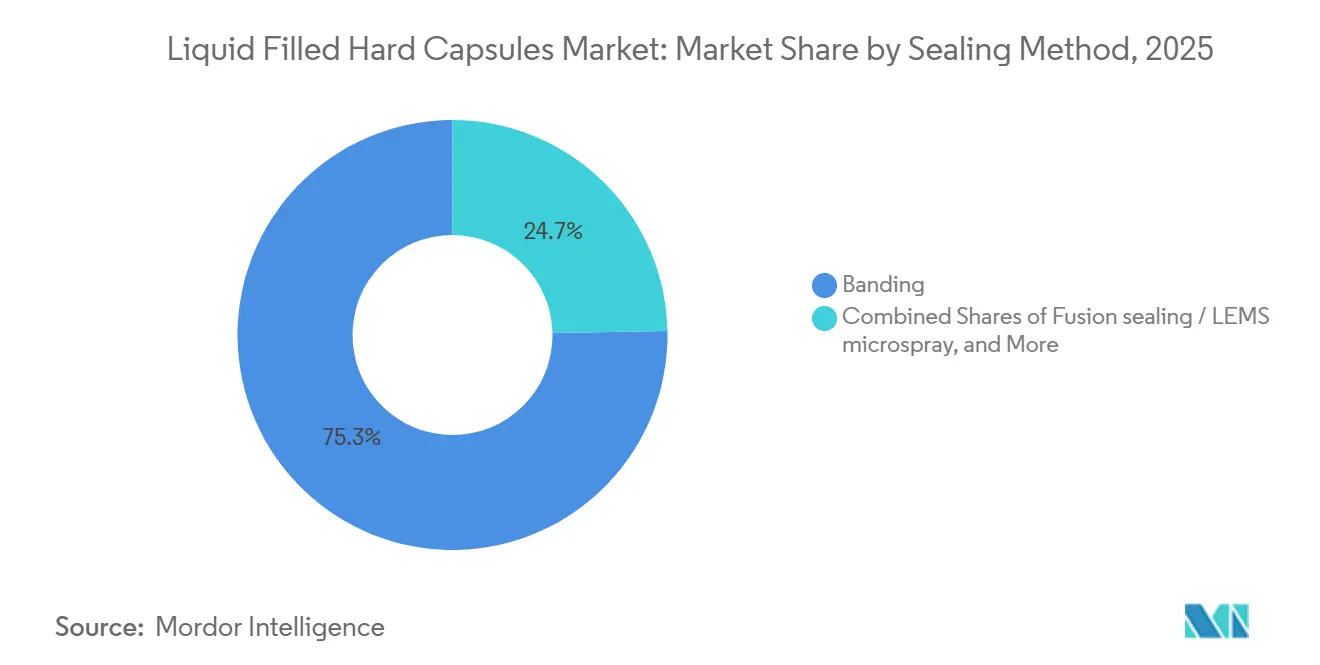

- By sealing method, banding led with 75.32% share of the liquid filled hard capsules market size in 2025, while fusion sealing is forecast to grow at 9.23% CAGR through 2031.

- By end use, Rx pharmaceuticals commanded 61.91% share in 2025, and nutraceuticals are projected to post an 8.84% CAGR through 2031.

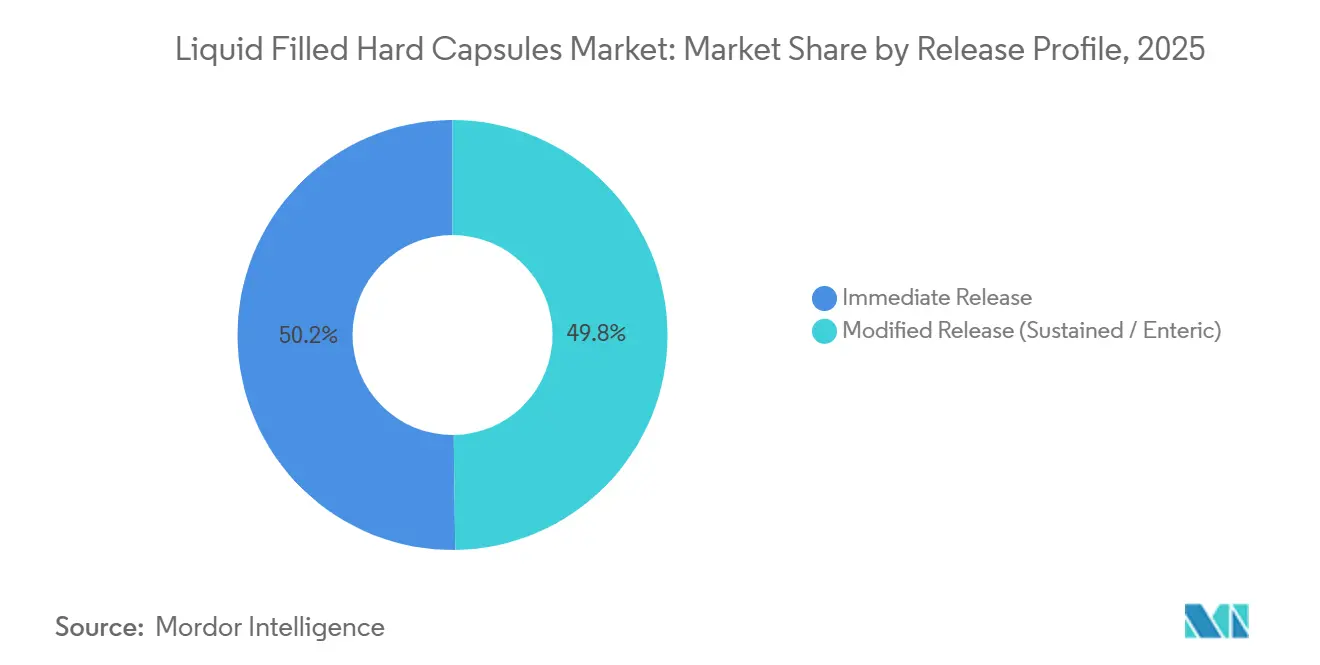

- By release profile, immediate-release captured 50.22% of the liquid filled hard capsules market share in 2025, and modified-release is projected at a 7.55% CAGR through 2031.

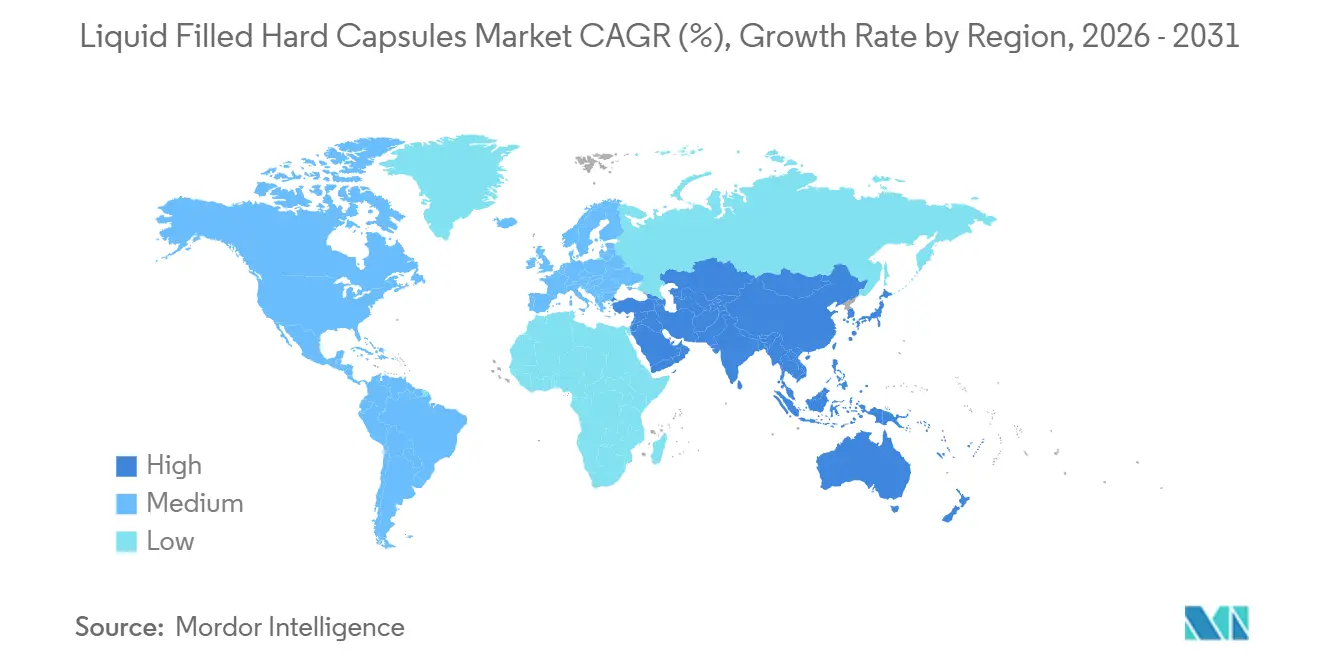

- By geography, North America held 34.56% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 9.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Filled Hard Capsules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bioavailability Push For Poorly Soluble APIs (Lipid-Based Fills, SEDDS/SMEDDS) | +2.1% | Global, with concentrated R&D activity in North America, Western Europe, Japan | Medium term (2-4 years) |

| Nutraceutical Growth And Capsule Preference | +1.8% | North America, Europe, Asia-Pacific (India, China driving volume) | Short term (≤ 2 years) |

| Advances In Liquid Dosing And Sealing Accuracy | +1.3% | Global manufacturing hubs; early gains in Germany, US, Japan | Medium term (2-4 years) |

| HPMC Adoption For Moisture-Sensitive And Vegetarian Formulations | +1.4% | Europe (35%+ vegetarian capsule share), North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| High-Throughput Capsule Machinery Enabling LFHC Scale-Up | +0.6% | Global; advanced automation in Europe, North America; capacity additions in China, India | Medium term (2-4 years) |

| Banding/Fusion Sealing Enabling Tamper-Evidence And Premiumization | +0.8% | North America, Europe; adoption expanding in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bioavailability Push For Poorly Soluble APIs Drives Liquid-Fill Adoption

A large share of new small-molecule candidates presents low aqueous solubility, which steers development teams toward lipid-based liquid-fill strategies such as SEDDS and SMEDDS to increase dissolution and absorption in the gastrointestinal tract[2]Mihir Rathod, Bhoomika Malete, and Priyanka Patil, “Self Micro Emulsifying Drug Delivery Systems (SMEDDS): A Comprehensive Review of Formulation, Mechanisms, and Applications,” International Journal of Pharmaceutical Sciences, ijpsjournal.com. These systems combine oils with surfactants and co-surfactants to spontaneously form fine emulsions on contact with intestinal fluids, which increases interfacial area and supports more predictable uptake. In the liquid filled hard capsules market, this approach aligns with the objective of reducing variability in drug exposure for BCS Class II and IV compounds, which can otherwise show erratic plasma profiles when delivered as conventional tablets.

Manufacturers pair these fills with shell selections that avoid cross-linking and moisture-driven degradation so that dissolution kinetics remain consistent during shelf life. Regulatory frameworks and compendial standards reinforce quality-by-design practices for liquid oral dosage forms, improving the predictability of development and scale-up paths for these capsule formats. As a result, the liquid filled hard capsules market is positioned to capture a larger share of pipeline reformulations that target solubility-limited exposure.

Nutraceutical Growth Propels Capsule Demand Across Consumer Segments

Consumers continue to prefer single-dose formats that are easy to swallow with perceived faster uptake, which has lifted capsule-based delivery for oils, vitamins, enzymes, and probiotics in retail channels. In the liquid filled hard capsules market, brands are leveraging fusion sealing and enhanced oxygen barriers to protect oxidation-sensitive actives like omega-3, CoQ10, and certain botanicals while also enhancing tamper-evidence. Probiotic and enzyme formulations are adopting HPMC shells with delayed-release designs so that sensitive ingredients survive gastric conditions before releasing in the intestine, which strengthens efficacy positioning without adding a coating operation.

As manufacturers expand dose ranges for categories like collagen or multi-ingredient blends, portion sizes and ease of regimen adherence remain central to packaging and format decisions in retail lines[3]TOSLA Nutricosmetics Team, “Consumer Study: Collagen Format Preferences and the Rise of Liquids,” TOSLA Nutricosmetics, toslanutricosmetics.com. These user-centric attributes are helping the liquid filled hard capsules market capture growth opportunities where taste masking, stability, and clean-label shell certifications are key differentiators. As nutraceutical portfolios diversify, suppliers with integrated shell, sealing, and fill expertise are positioned to translate new concepts into shelf-stable SKUs at speed.

Advances In Liquid Dosing And Sealing Accuracy

Upgrades in filling platforms are enabling liquid and semi-solid formulations to scale while meeting strict content uniformity objectives for low-dose and potent actives. In the liquid filled hard capsules market, modern lines incorporate servo controls, in-line weight checks, and automated rejection to keep within validated limits while running challenging excipient systems. High-throughput systems now exceed 150,000 capsules per hour in commercial settings, with fully automatic solutions reaching 210,000 capsules per hour for large-volume programs. Equipment innovations extend beyond speed to include flexible changeovers, hot-melt capability, and PAT-style sensors that help operators maintain control of critical parameters during long campaigns. These capabilities support scale-up for complex lipid fills and suspensions while reducing the manual interventions that can elevate contamination risks[4]Capsugel Equipment, “CFS 1200 Capsule Liquid Filling & Sealing Machine,” Capsugel, capsugel.com. As outsourcing demand increases, contract partners with advanced, configurable lines are well placed to win projects that require tight process windows at commercial speeds.

HPMC Adoption For Moisture-Sensitive And Vegetarian Formulations

HPMC shells are gaining ground where moisture-sensitive actives, solvent-containing fills, or cultural requirements make gelatin less suitable, which supports broader adoption in the liquid filled hard capsules market. The lower inherent moisture content of HPMC relative to gelatin helps protect hygroscopic APIs and can mitigate precipitation risks that arise when fills and shells interact. In parallel, vegetarian and halal certifications allow brands and sponsors to address consumer and patient preferences in markets where animal-origin inputs face restrictions.

Because HPMC resists aldehyde-driven cross-linking that can impede dissolution in gelatin, formulators gain an extra margin of safety on long-term stability for specific actives and excipient systems. These functional and labeling benefits are expanding the role of HPMC in both pharmaceutical and nutraceutical programs, especially where premium sealing approaches or delayed-release formats are part of the target product profile. With supply scale and certifications now well established among leading producers, the liquid filled hard capsules market is set to see continued HPMC share gains as pipelines evolve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialized Sealing Adds Cost And Process Complexity | -0.9% | Global; more pronounced in cost-sensitive markets (India, Southeast Asia, Latin America) | Medium term (2-4 years) |

| Excipient–Shell Compatibility And Regulatory Validation Burdens | -0.7% | Global pharmaceutical markets; stricter in EU, US, Japan | Long term (≥ 4 years) |

| Gelatin Supply And Cultural Constraints Create Volatility | -0.5% | Middle East, South Asia (halal requirements); Europe (vegetarian preferences) | Short term (≤ 2 years) |

| Oxygen/Moisture Ingress Risk Without Advanced Sealing/Packaging | -0.4% | Tropical markets (Southeast Asia, Sub-Saharan Africa); hot-humid climates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Specialized Sealing Adds Cost And Process Complexity

Liquid-filled formats often require banding or fusion sealing as part of container-closure integrity, which adds steps that can raise capital and operating burdens compared to conventional hard capsules. In the liquid filled hard capsules market, fusion systems that create hermetic, continuous seams deliver premium protection, yet they call for dedicated equipment, validation, and operator skill that not all sites maintain. As lines become more advanced, firms must validate in-line controls and inspection steps that ensure weight, seal integrity, and appearance meet specifications in real time. This escalates the quality management footprint, which can lengthen tech transfers for smaller batches or frequent SKU changeovers. Sponsors that need premium tamper-evidence and oxidative protection gain shelf-life and quality benefits, but the added complexity may weigh on programs where price competition is tight. The trade-off shapes facility strategies and outsourcing choices across the liquid filled hard capsules market.

Excipient–Shell Interactions Demand Extensive Validation Protocols

Liquid fills that include surfactants, co-solvents, or reactive excipients require careful compatibility assessments with shell polymers to ensure that dissolution, integrity, and release profiles remain consistent across shelf life. In the liquid filled hard capsules market, sponsors and CDMOs screen shell materials like gelatin and HPMC against representative fills under accelerated and long-term conditions to de-risk late-stage surprises. Compendial updates on oral dosage forms have reinforced expectations around extractables and leachables, which add method development and toxicological review steps when shell polymers contact surfactant-rich systems. These requirements drive more robust design-of-experiments at feasibility and scale-up, yet they can extend timelines for complex actives that need unconventional excipients. The net effect is a higher upfront workload to secure reliable performance, which is essential for maintaining regulatory confidence and patient safety. As pipelines diversify, this validation burden remains a gating factor for some liquid-fill launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Shell Material: Plant-Based Alternatives Reshape Supply Economics

Gelatin capsules held 73.24% of the liquid filled hard capsules market share in 2025, supported by mature processing infrastructure and well-understood dissolution behavior across common oil and suspension fills. This installed base keeps gelatin central to high-volume programs where formulations avoid excipient chemistries that could drive cross-linking. Sponsors value streamlined qualification when working with established gelatin supply networks and site-level experience in banding workflows. HPMC continues to expand faster because of inherent resistance to aldehyde-driven cross-linking, lower shell moisture, and its suitability for delayed or modified-release designs, all of which increase formulation headroom. Certification footprints that include non-GMO, halal, and vegan claims also help HPMC unlock labeled product opportunities that are central to many consumer portfolios. Within the liquid filled hard capsules market, the dynamic between gelatin’s scale economics and HPMC’s functional and labeling advantages will continue to shape shell selection decisions through 2031.

HPMC is projected to post an 8.51% CAGR through 2031 as more moisture-sensitive APIs, probiotics, enzymes, and solvent-containing fills shift away from gelatin to maintain stability and predictable release. Suppliers have invested in thermogelation processes and polymer-engineering advances that deliver pH-independent dissolution and consistent performance across liquid-fill modalities. In the liquid filled hard capsules industry, this capability lets formulators design products that combine delayed-release features with lipid vehicles while maintaining label claims that matter in consumer-facing channels. Gelatin remains a strong fit for stable, neutral-pH oils and simpler suspensions, so portfolio-specific criteria continue to drive hybrid procurement strategies at large buyers. Over time, rising comfort with HPMC in regulated products and the expansion of certified supply may gradually rebalance shares in favor of plant-based shells.

By Filling State: Self-Emulsifying Systems Lead Innovation Trajectory

Oil-based liquid fills accounted for 45.32% of the liquid filled hard capsules market size in 2025, reflecting their central role in vitamins, oils, and hormone products where solubilization is straightforward. Operators continue to favor oil vehicles for their process simplicity, stable handling windows, and broad compatibility with both gelatin and HPMC shells. Where APIs demand stronger solubilization, programs migrate toward engineered emulsifying systems that deliver higher exposure with tighter inter-patient variability. This is where the liquid filled hard capsules market is seeing the greatest formulation innovation, because shell, seal, and fill must be tuned together to preserve performance across shelf life. In parallel, equipment providers have improved throughput, in-line control, and temperature management for hot fills and viscous systems that need tight processing windows.

Self-emulsifying SEDDS/SMEDDS are projected to grow at a 9.85% CAGR through 2031, reinforced by peer-reviewed evidence that lipid microemulsions improve solubilization and exposure for difficult APIs. The ability to target droplet sizes in the nano to submicron range increases interfacial area, which helps drive consistent absorption even under variable fed-state conditions. Suspension and hot-melt applications maintain clear roles where actives have low oil solubility or benefit from semi-solid matrices, yet they rely more heavily on robust process controls to manage sedimentation and thermal profiles. As pipelines evolve toward complex delivery goals, the liquid filled hard capsules market will keep allocating greater share to emulsifying systems that can integrate release control with solubilization strategies.

By Sealing Method: Fusion Technologies Capture Premium Segments

Banding captured 75.32% of the liquid filled hard capsules market size in 2025, supported by broad equipment availability and familiarity across pharmaceutical and nutraceutical lines. Many contract partners rely on high-speed banding to deliver consistent closure and visual tamper-evidence for large retail volumes. The approach offers pragmatic changeovers and keeps format flexibility high across shell materials and sizes. For oxidatively sensitive or high-value fills, more programs are shifting to fusion sealing due to its larger effective seal zone and hermetic closure properties. That shift is most pronounced in capsules built for long ambient storage or for excipient systems that benefit from reduced ingress risks.

Fusion sealing is projected to grow at a 9.23% CAGR through 2031 as sponsors standardize on platforms that combine micro-spray seam activation with controlled thermal fusion to create a continuous shell body. The liquid filled hard capsules market increasingly values this seal integrity for oxidation-prone nutraceuticals and dose-critical drug products where leakage tolerance is near zero. While lock-only configurations remain niche due to lower resistance to pressure changes, banding maintains an important role wherever speed and cost-effectiveness rank highest. Across categories, container-closure integrity expectations continue to tighten, and fusion platforms are well aligned with modern test methods and production controls. This balance between operational pragmatism and premium sealing explains the bifurcation in adoption patterns over the forecast period.

By End Use: Nutraceutical Demand Outpaces Pharmaceutical Growth

Rx pharmaceuticals accounted for 61.91% of 2025 revenues, underpinning the liquid filled hard capsules market with use cases that emphasize dose predictability, stability, and bioavailability gains. Sponsors select shell materials based on chemical compatibility and release goals, with fusion sealing used in programs where oxidative control or tamper-evidence is integral to risk management. In parallel, HPMC-based delayed-release designs allow sensitive actives to bypass gastric conditions without adding a coating step, which can streamline development. These attributes sustain capsule selection for targeted patient subgroups or actives where tablets would require complex processing to achieve similar exposure. As a result, the liquid filled hard capsules market remains a key route for lifecycle management that seeks to improve consistency of therapeutic effect.

Nutraceuticals are projected to post an 8.84% CAGR, advancing on consumer preference for convenient, perceived high-bioavailability formats that deliver oils, enzymes, and probiotics in a single dose. Fusion sealing and HPMC shells enable cleaner labels, stronger oxygen control, and delayed release where needed, which support premium positioning in retail channels. Probiotic and enzyme products, in particular, benefit when delayed-release capsules help protect actives through stomach transit before disintegration in the intestine. As nutraceuticals continue to differentiate on ingredients and claims, liquid-fill know-how around sealing and packaging will be pivotal to deliver stability and shelf life at scale. This reinforces the growth profile for consumer health programs within the liquid filled hard capsules market.

By Release Profile: Modified Release Gains Traction For Targeted Delivery

Immediate-release formats held 50.22% share of the liquid filled hard capsules market in 2025, consistent with use cases where fast onset and simple oil vehicles match the therapeutic or consumer objective. Operators align dissolution performance to compendial expectations for oral dosage forms, with in-process checks and post-process testing supporting batch release. apsules that present pre-dissolved actives or microemulsions typically pass immediate-release tests with margin, which keeps this format a versatile choice across categories. Where delayed action or gastric protection is required, formulators adjust shell choice, sealing approach, and fill composition to reach the desired profile. These options help the liquid-filled hard capsules market cover both rapid-onset needs and targeted delivery goals with the same platform family.

Modified-release is projected at a 7.55% CAGR, propelled by delayed-release HPMC designs that can hold intact in gastric media and then disintegrate in the intestine without a separate coating step. That capability is gaining traction in probiotics, enzymes, and certain small molecules that benefit from enteric protection. Suppliers also support hybrid dose strategies where immediate and delayed effects are combined across SKUs or through nested formats, which broadens the design space without tablet compression. Advances in sealing and shell polymers create more room to fine-tune dissolution and to maintain stability under real-world distribution conditions. These design choices underpin the adoption trajectory for modified-release capsules across regulated and consumer health programs alike.

Geography Analysis

North America held 34.56% of the liquid filled hard capsules market in 2025, supported by a strong base of pharmaceutical sponsors, established capsule manufacturing, and mature regulatory systems for oral dosage forms. U.S. cGMP requirements and container-closure integrity expectations have helped standardize quality and documentation practices for liquid-fill programs. Capsules with fusion sealing and HPMC shells are increasing in projects where oxidative stability and label claims support premium therapies and consumer products. The region’s installed base of high-throughput lines supports large-volume runs across both Rx and OTC, which anchors capacity for launches and reformulations. This ecosystem positions North America to remain an influential buyer and producer through the forecast window.

Asia-Pacific is projected to be the fastest-growing region at a 9.32% CAGR through 2031, reflecting strong manufacturing capability and increasing adoption of premium sealing and shell options in both pharmaceutical and nutraceutical pipelines. Regional suppliers and global multinationals are expanding capacity and technology stacks to serve local and export demand with higher integrity formats. As sponsors localize production and upgrade equipment, high-speed lines with in-line controls are becoming more common in leading hubs. HPMC adoption is rising alongside demand for vegetarian and halal certification, which supports retail and Rx use cases across major markets. This combination of quality, speed, and certification breadth supports the region’s outperformance in the liquid filled hard capsules market.

Europe shows steady growth under rigorous quality standards that favor producers with validated processes for liquid fills, fusion sealing, and advanced release designs. Activity includes capacity additions in packaging and integrated services that support both pharma and consumer health customers. HPMC uptake is strong in use cases that require moisture management or expand labeled claims for vegetarian and halal preferences. With a high bar for documentation, extractables and leachables testing, and in-process controls, European manufacturers have built operating models that align with complex liquid-fill demands. This keeps the region well positioned in regulated markets while also serving global supply needs in the liquid filled hard capsules market.

Competitive Landscape

The liquid filled hard capsules market features a moderately fragmented market with a mix of global capsule producers, equipment specialists, and CDMOs that provide formulation through commercial-scale filling and sealing. Providers differentiate through shell portfolios, sealing technologies, certifications, and the ability to integrate process controls across long campaigns. Lonza’s fusion sealing and licaps platform has anchored premium applications that need tight oxygen control, robust tamper-evidence, and strong stability under varied climates. ACG has advanced HPMC shell offerings that target moisture-sensitive and vegetarian needs, pairing materials science with application support for regulated and consumer programs. Equipment innovators such as Syntegon and MG2 have expanded their performance series to integrate weight checks, PAT-style sensors, and rapid changeovers that help manufacturers meet quality expectations at throughput.

Strategic investment continues around capacity localization, high-potent handling, and integrated packaging. Aenova reported record investments in 2024 to scale oral solid and capsule capabilities across its network, with a focus on high-potent handling and expanded volume for solid dose. In Europe, Sirio opened a USD 18.78 million full-service packaging facility in Germany in 2024 to support blister and bottle formats under unified GMP standards, which extends downstream support for capsule-based portfolios. atalent’s established footprint in Asia includes its Kakegawa site in Japan, which complements multi-region clinical and commercial supply options for sponsors planning capsule-based pathways. These moves indicate how leaders are reinforcing end-to-end offerings to secure new molecule launches and lifecycle programs in the liquid filled hard capsules market.

Liquid Filled Hard Capsules Industry Leaders

Lonza

ACG

Qualicaps

Suheung (EMBO CAPS)

CapsCanada

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lone Star acquired Capsugel from Lonza Group AG, with Lonza reinvesting about 40% of the equity while Lone Star takes the majority stake. The transaction underlines Capsugel’s strong position as a global player in hard empty and liquid-filled hard capsules.

- September 2025: Bora Pharmaceuticals Co., Ltd. introduced liquid‑filled hard capsule (LFC) manufacturing at its Zhunan, Taiwan site, marking a key expansion of its production capabilities.

Global Liquid Filled Hard Capsules Market Report Scope

The liquid filled hard capsules market comprises two‑piece hard capsules filled with liquid, semi‑solid, or lipid‑based formulations that are designed to enhance bioavailability, stability, and patient compliance in oral drug delivery. These capsules are widely used across pharmaceutical and nutraceutical applications, particularly for poorly soluble or sensitive active ingredients.

The market is segmented by shell material, including gelatin, HPMC, and pullulan or other cellulose; by filling state, including oil‑based liquids, suspensions, semi‑solid or hot‑melt fills, and self‑emulsifying SEDDS or SMEDDS; by sealing method, including banding, fusion sealing or LEMS microspray, and lock‑only; by end use, including Rx pharmaceuticals, OTC products, and nutraceuticals or dietary supplements; by release profile, including immediate release and modified release. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Gelatin |

| HPMC |

| Pullulan / Other Cellulose |

| Oil-based liquids |

| Suspensions |

| Semi-solid / Hot-melt fills |

| Self-emulsifying (SEDDS/SMEDDS) |

| Banding |

| Fusion sealing / LEMS microspray |

| Lock-only |

| Rx Pharmaceuticals |

| OTC |

| Nutraceuticals / Dietary Supplements |

| Immediate Release |

| Modified Release (Sustained / Enteric) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Shell Material | Gelatin | |

| HPMC | ||

| Pullulan / Other Cellulose | ||

| By Filling State | Oil-based liquids | |

| Suspensions | ||

| Semi-solid / Hot-melt fills | ||

| Self-emulsifying (SEDDS/SMEDDS) | ||

| By Sealing Method | Banding | |

| Fusion sealing / LEMS microspray | ||

| Lock-only | ||

| By End Use | Rx Pharmaceuticals | |

| OTC | ||

| Nutraceuticals / Dietary Supplements | ||

| By Release Profile | Immediate Release | |

| Modified Release (Sustained / Enteric) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the liquid filled hard capsules market size and growth outlook through 2031

It reached USD 1.90 billion in 2025 and is projected to reach USD 2.85 billion by 2031 at a 7.45% CAGR over 2026-2031.

Which end-use segments are leading in the liquid filled hard capsules market

Rx pharmaceuticals led with 61.91% share in 2025, while nutraceuticals are projected to grow fastest at 8.84% CAGR through 2031.

Which filling-state formats show the strongest momentum

Oil-based formats led with 45.32% share in 2025, while self-emulsifying SEDDS/SMEDDS are projected to grow at 9.85% CAGR to 2031.

How are sealing technologies evolving within this market

Banding held 75.32% share in 2025, while fusion sealing is the fastest-growing method at a 9.23% CAGR through 2031 due to hermetic closure and integrity benefits.

What role do HPMC shells play in the liquid filled hard capsules market

HPMC supports moisture-sensitive and vegetarian requirements and is projected to expand at an 8.51% CAGR through 2031 as adoption increases.

Which regions are set to drive incremental growth

North America led with 34.56% share in 2025, and Asia-Pacific is projected to be the fastest-growing region at a 9.32% CAGR through 2031.

Page last updated on: