Liquid Crystal Polymer (LCP) Fibers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

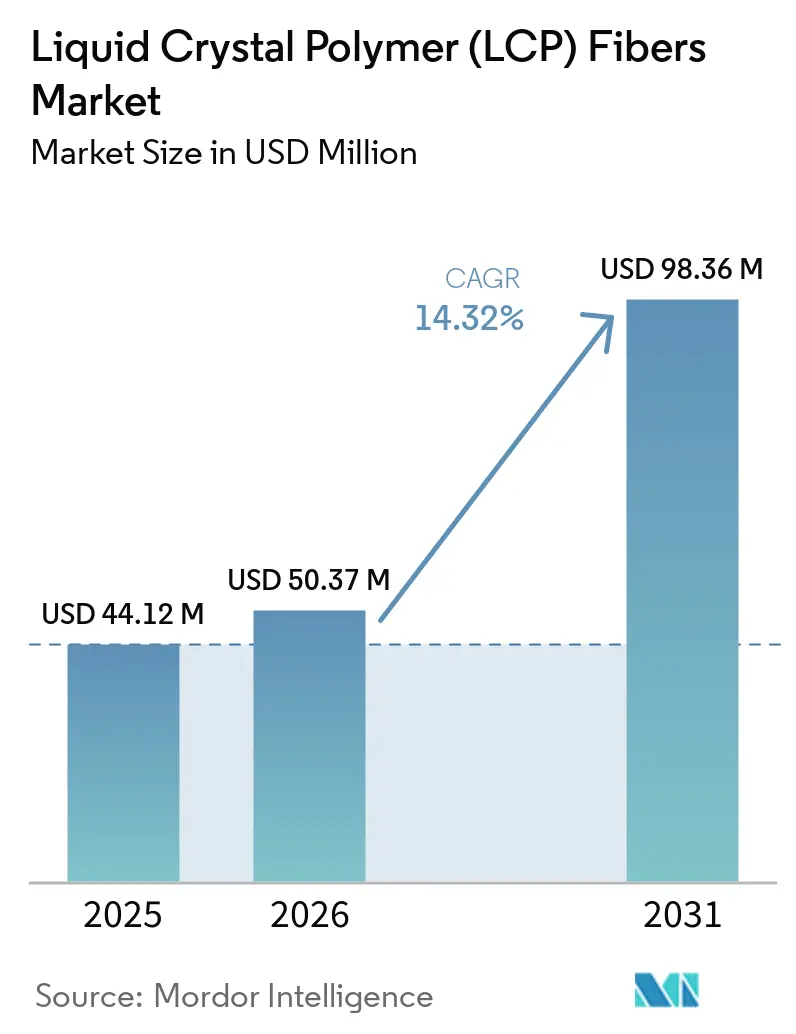

| Market Size (2026) | USD 50.37 Million |

| Market Size (2031) | USD 98.36 Million |

| Growth Rate (2026 - 2031) | 14.32% CAGR |

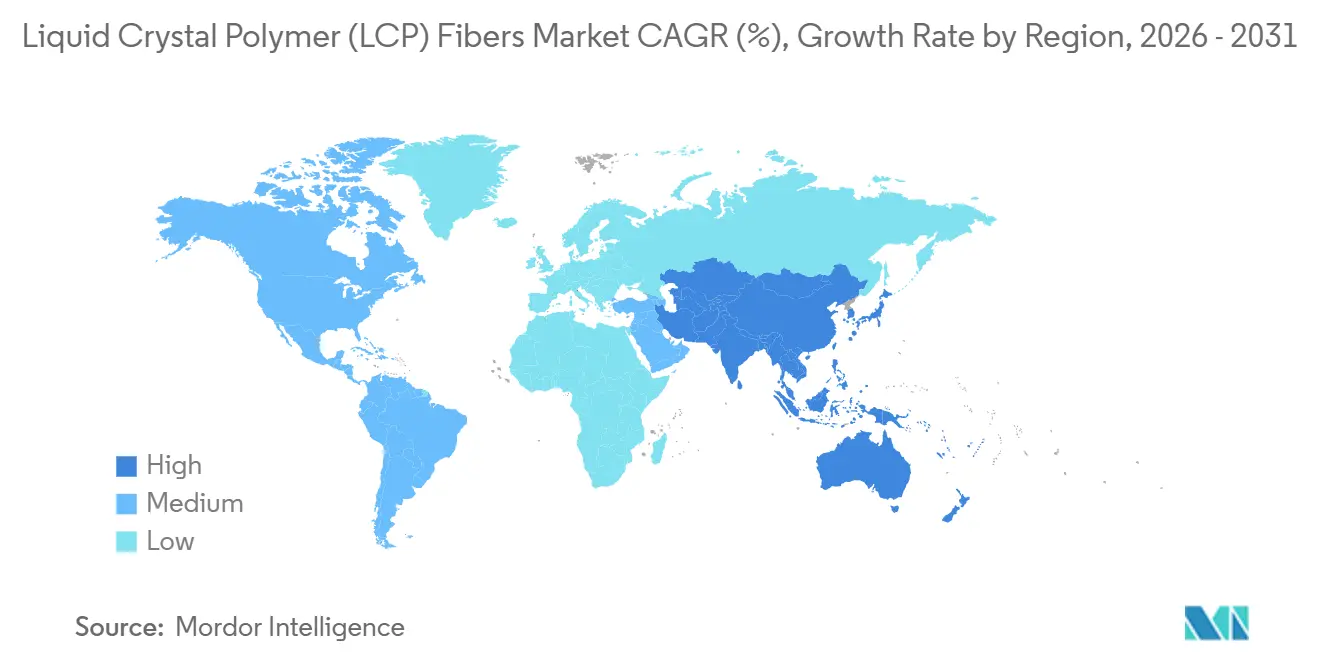

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

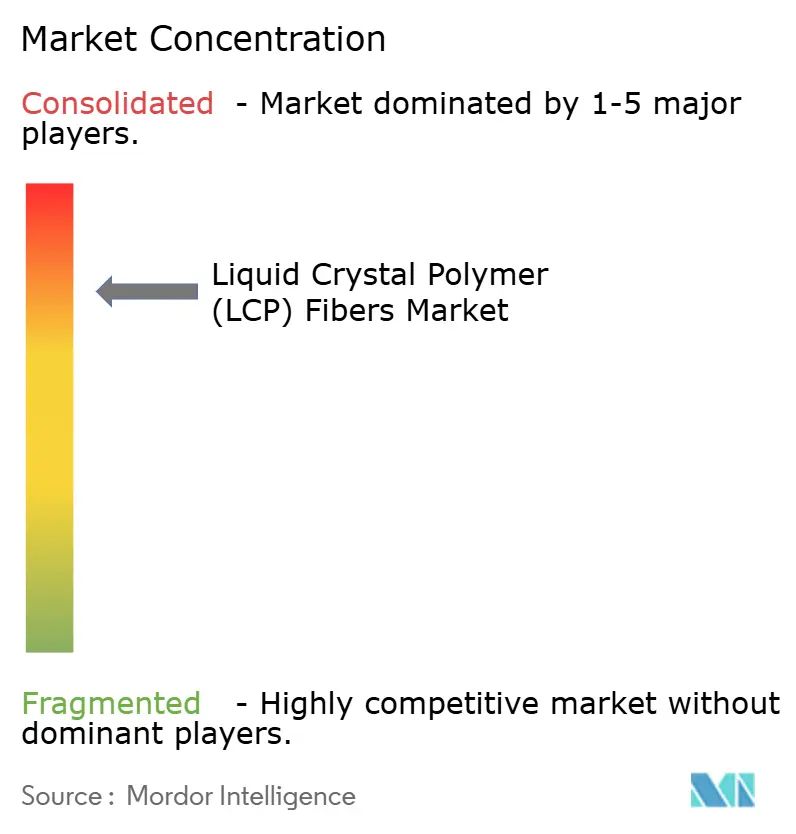

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Crystal Polymer (LCP) Fibers Market Analysis by Mordor Intelligence

The Liquid Crystal Polymer (LCP) Fibers Market size is expected to increase from USD 44.12 million in 2025 to USD 50.37 million in 2026 and reach USD 98.36 million by 2031, growing at a CAGR of 14.32% over 2026-2031. Demand is accelerating because 5G antenna engineers specify ultra-low-loss substrates, medical-device designers replace metal braids with MRI-compatible monofilaments, and aerospace primes mandate zero-creep tethers for satellite deployment. Filament yarn remains the anchor product, yet woven fabric is scaling fastest as converters master sizing chemistry that cushions the polymer’s low elongation. Asia-Pacific leads revenue thanks to China’s flexible-printed-circuit dominance and Japan’s fiber-spinning hub, while North America secures high-value aerospace and healthcare contracts. Capital spending by Polyplastics, Celanese, and Sumitomo Chemical is widening raw-material access and easing historical dependence on a single spinner.

Key Report Takeaways

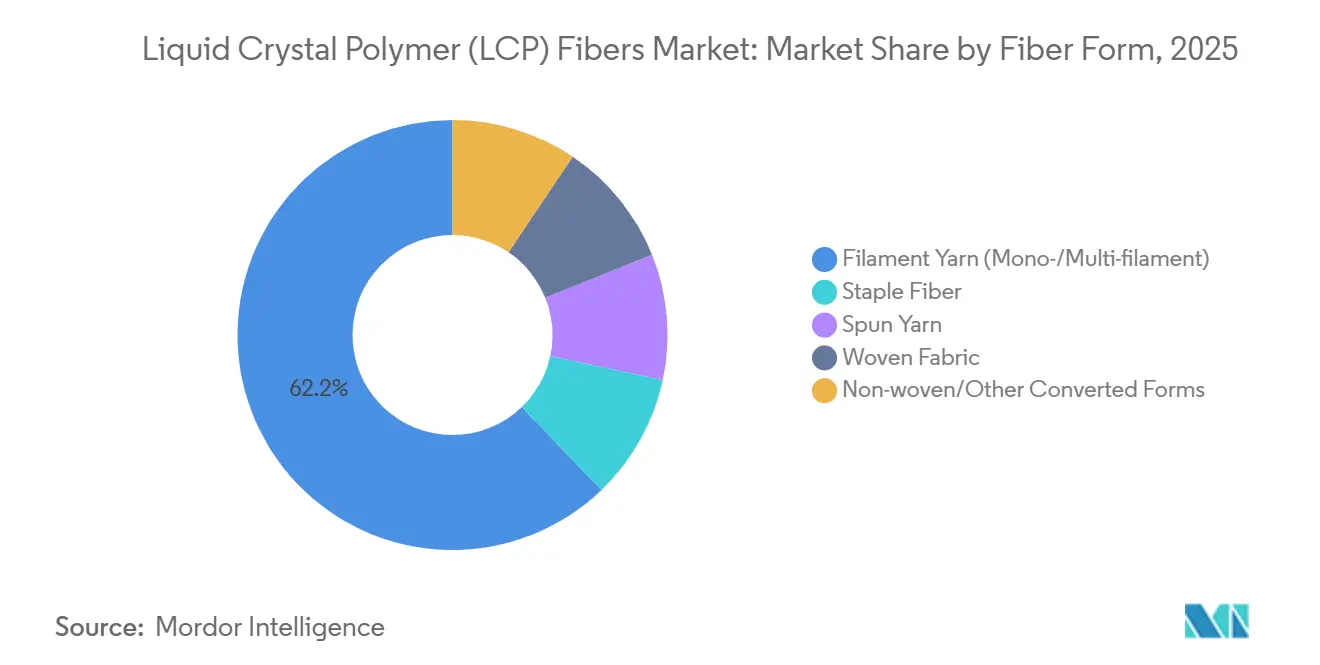

- By fiber form, filament yarn commanded the largest share of 62.18% of the 2025 revenue of the Liquid Crystal Polymer (LCP) Fibers market. Moreover, the share of woven fabrics is expected to grow at the fastest CAGR of 21.51% during the forecast period (2026-2031).

- By product grade, high-tenacity grade had the largest market share of 44.32% in 2025, and the share of surface-treated/coated grade is expected to increase with the fastest CAGR of 23.20% during the forecast period (2026-2031).

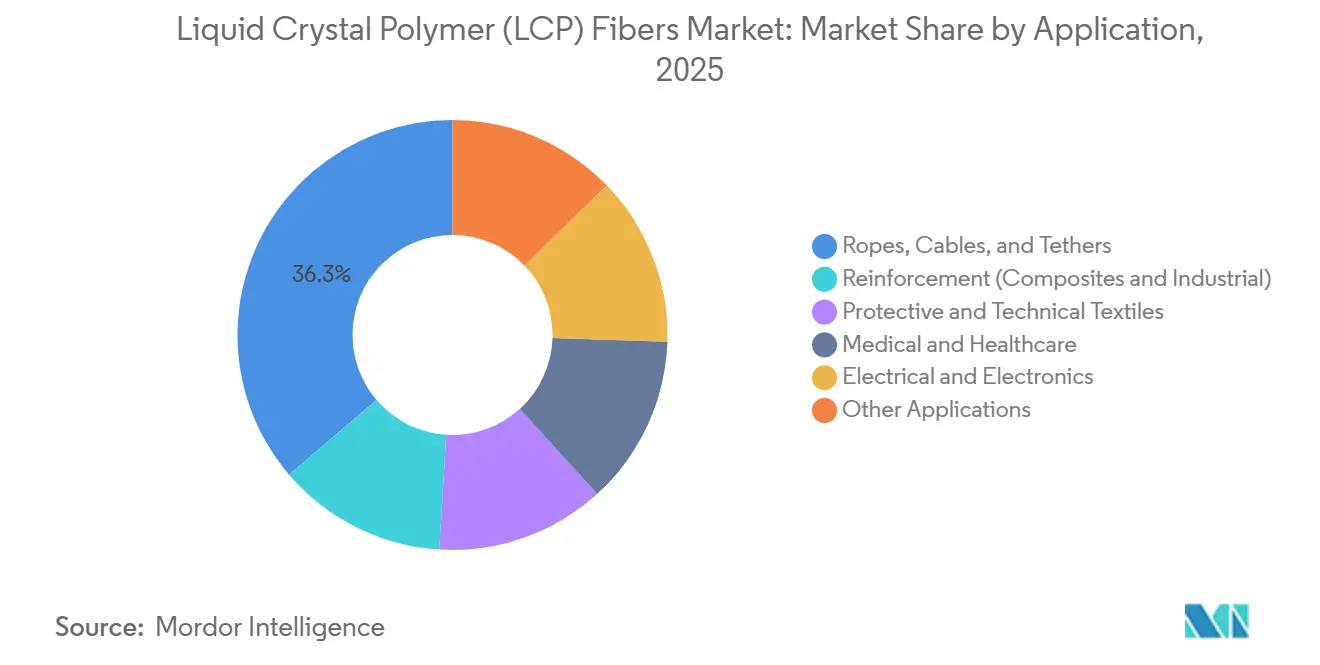

- By application, ropes, cables, and tethers had a share of 36.27% of the market in 2025, and the medical and healthcare sector's share is expected to grow with the fastest CAGR of 24.07% during the forecast period (2026-2031).

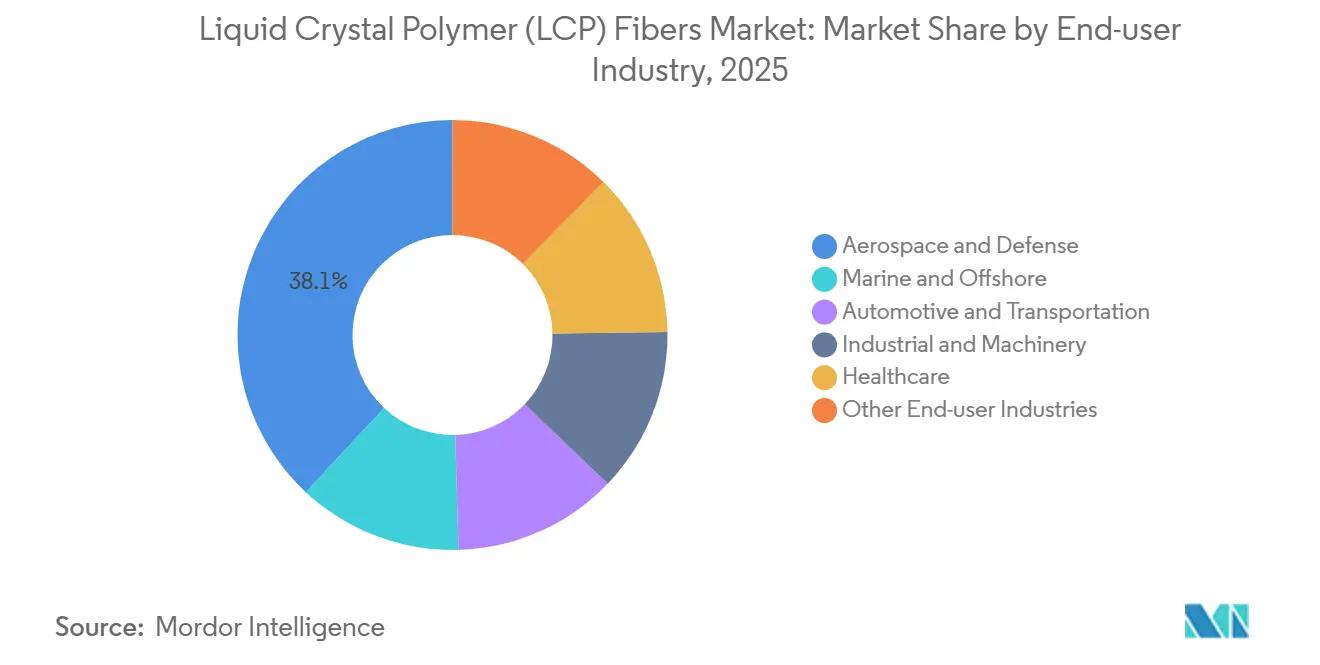

- By end-user industry, the aerospace and defence industry had a market share of 38.05% in 2025. However, the healthcare industry's market share is expected to grow at the fastest CAGR of 22.91% during the forecast period (2026-2031).

- By geography, Asia Pacific held a share of 46.44% of the market in 2025 and this share is expected to grow with a CAGR of 18.67% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Crystal Polymer (LCP) Fibers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G/6G high-frequency connector demand | +4.2% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Electric-vehicle lightweight wiring harness adoption | +3.1% | Global, with early concentration in China, Germany, United States | Medium term (2-4 years) |

| Rising penetration of mini-LED/µLED backlights | +2.4% | APAC (China, South Korea, Taiwan display fabs) | Long term (≥ 4 years) |

| Increasing aerospace demand for ultra-high-tenacity tethers | +2.8% | North America & EU (satellite primes), spill-over to APAC launch services | Long term (≥ 4 years) |

| Growing robotic-surgery consumables needing sterilizable sutures | +1.9% | North America & EU (medical-device hubs), expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in 5G/6G High-Frequency Connector Demand

Connector makers are swapping modified polyimide for LCP because dielectric constants of 2.9-3.0 and dissipation factors below 0.002 keep millimeter-wave losses low. Panasonic’s 0.35-mm-pitch RF4 connectors illustrate how the resin fills 0.3-mm walls without warpage across -196°C to +240°C. Polyplastics’ LH and TF grades, launched in 2025, target the same sub-0.4-mm pitches for base-station modules. Moisture absorption under 0.04% prevents dielectric drift in humid sites, a priority for Asian tower installations. Celanese’s 20-kt plant in China underwrites local supply for Huawei and Xiaomi back-end molders[1]Celanese Corporation, “Celanese Commissions 20 kt LCP Facility in China,” celanese.com.

Electric-Vehicle Lightweight Wiring-Harness Adoption

Tier-ones report 15-20% mass cuts when copper cables adopt LCP jackets and braids. The polymer meets ISO 6722 without halogenated additives because its limiting-oxygen index exceeds 28%. Sumitomo Chemical’s biomass-based grade couples the same 400°C decomposition ceiling with a smaller carbon footprint, aligning with EU circularity rules. Toray’s USD 366 million Korean fiber project intensifies price competition, yet LCP still wins on 5-15-second molding cycles. Automakers view every gram saved as either extra range or fewer battery cells, reinforcing harness conversions[2]Sumitomo Chemical Co. Ltd., “Biomass-Derived LCP Development,” sumitomochem.co.jp.

Rising Penetration of Mini-LED/µLED Backlights

Premium TVs and car dashboards now exceed 10,000 dimming zones, compressing bend radii and trace spacing. LCP films handle 25-µm lines and spaces while preserving impedance at 1 MHz driver frequencies. Kuraray is reviewing new VECSTAR film capacity to meet notebook and radar demand. A thermal-expansion match with ITO glass cuts delamination risk from -40°C to +105°C. Flexible-circuit shops across China, South Korea, and Taiwan have booked LCP for 2026 rollouts, positioning the liquid crystal polymer fibers market for structural electronics growth.

Increasing Aerospace Demand for Ultra-High-Tenacity Tethers

Low-earth-orbit satellites need cords that neither creep nor outgas. VECTRAN fiber posts 3.0 GPa strength and negligible creep at 50% load, confirmed by NASA and adopted in tether systems. Linden Photonics’ ROV cables marry LCP jackets with near-neutral buoyancy for 3,000-m dives. Cortland’s 4.9-Mlb ropes serve offshore wind turbines, cutting winch loads 65% versus steel. These credentials cement LCP as the preferred material for deep-space and deep-sea lines, a high-margin niche within the liquid crystal polymer fibers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High polymerization cost of hydroxy-benzoic acid feedstock | -2.7% | Global, acute in regions lacking integrated HBA production | Medium term (2-4 years) |

| Supply-chain concentration around single fiber spinner | -1.8% | Global, most visible in aerospace/marine sectors reliant on VECTRAN | Short term (≤ 2 years) |

| Processing brittleness limiting textile weaving speeds | -1.3% | Global, particularly APAC textile converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Polymerization Cost of Hydroxy-Benzoic Acid Feedstock

Only five producers supply 4-HBA, yet polymerization capacity expanded 30% between 2024 and 2026. The acetylation sequence runs above 325°C and consumes 40% more energy than conventional polyester lines, lifting resin costs USD 2-3 kg for non-integrated compounders. Celanese’s China complex co-locates with phenol upstream units to temper volatility, while Sumitomo Chemical trials lignin-derived phenol to loosen the feedstock squeeze. Until new entrants scale, pricing headwinds will clip margins across the liquid crystal polymer fibers market.

Supply-Chain Concentration Around Single Fiber Spinner

Kuraray’s Saijo plant remains the lone source of melt-spun aromatic-polyester yarn, around 1,000 tons per year. A single outage would stall satellite-tether and LNG-rope programs. Rope makers hedge by blending VECTRAN cores with aramid jackets, but requalification under API RP 2SM drags 18-24 months. Resin suppliers are promoting alternative spunbond or extruded monofilaments; yet tensile strengths trail VECTRAN HT by 20-30%, limiting substitution. Diversification remains an urgent agenda item for the liquid crystal polymer fibers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Form: Filament Yarn Retains Volume Leadership

Filament yarn held 62.18% of the 2025 Liquid Crystal Polymer (LCP) Fibers market revenue, underscoring economies of melt spinning that deliver 23-30 grams per denier (g/d) strengths without post-draw. This slice of the market share benefits from denier versatility, covering 200- to 2,250-denier cables. Woven fabrics, though smaller, are propelling growth with a 21.51% CAGR during the forecast period (2026-2031) as hybrid warp-weft designs lessen breakage, enlarging the liquid crystal polymer fibers market.

The progress of staple fiber and spun yarn is capped by brittleness in carding. Non-wovens and film grades secured the balance; PCB laminators value VECSTAR film for 5G modules. As more polymer becomes available for casting and spunbond lines, converter integration will diversify revenue streams across the liquid crystal polymer fibers market.

By Product Grade: Surface-Treated Grades Gain Momentum

High-tenacity yarns delivered 44.32% of 2025 turnover, essential for aerospace tethers and LNG moorings. Surface-treated/coated grades, however, are rising at a 23.20% CAGR during the forecast period (2026-2031) to address peel-strength targets above 1.5 N/mm in copper-foil laminates, widening the liquid crystal polymer fibers market size for electronics. Standard grades serve protective textiles where the inherent LOI of 28-30% negates halogen additives. High thermal/chemical-resistance grades find demand in under-hood sensors and chemical pumps; Sumitomo’s biomass variant aims to cut carbon footprints yet keep 400°C stability, reflecting sustainability priorities inside the Liquid Crystal Polymer Fibers market.

By Application: Healthcare Racing Ahead

Ropes, cables, and tethers delivered 36.27% of 2025 revenue, a legacy beachhead won on zero creep and abrasion endurance. Medical and healthcare devices, though smaller, are climbing 24.07% CAGR during the forecast period (2026-2031) as catheter braids and micro-needles exploit autoclave resilience. Electrical and electronics uses top 22% of revenue, fueled by 5G antenna rollouts that rely on dielectric constancy, extending the liquid crystal polymer fibers market reach into RF modules. Reinforcement composites and technical textiles round out demand with sound-damping and cut-proof roles.

By End-User Industry: Aerospace Still Dominant, Healthcare Fastest

Aerospace and defense consumed 38.05% in 2025, where deployment cords survive -150°C cycling and atomic-oxygen erosion. Healthcare is scaling at 22.91% CAGR during the forecast period (2026-2031) on sterilizable sutures and wearable devices, reshaping the liquid crystal polymer fibers market profile. Marine, automotive, and industrial users each contribute mid-teen shares; EV wiring harnesses and offshore wind moorings anchor future upside. Consumer electronics and sporting goods supply the remainder, leveraging vibration damping and stable dielectric properties.

Geography Analysis

Asia-Pacific generated 46.44% of 2025 revenue and is forecast to grow 18.67% CAGR to 2031. China’s FPCB (flexible printed circuit board) assemblers, Japan’s Saijo fiber hub, and Taiwan’s 5,000-ton polymer expansion keep the liquid crystal polymer fibers market centered in the region. South Korea’s fiber investments stiffen rivalry, though LCP’s fast molding cycles preserve cost edges in connectors. India and ASEAN lag because import tariffs inflate resin costs by up to 25%.

North America's revenue, led by the United States aerospace primes and FDA-regulated device firms that prize VECTRAN’s Master File standing. Mexico’s harness assemblers test LCP jackets to meet ISO 6722 without brominated retardants, nudging the liquid crystal polymer fibers market toward automotive scale-up.

Europe's 2025 market share significantly depended upon German automakers evaluating 15-20 % mass savings from LCP harnesses and European Union (EU) recycling rules curbing halogens. Italy’s tether makers and UK offshore-wind contractors specify VECTRAN for long-life ropes. South America, the Middle East and Africa together accounted for a small market share, with Brazil's offshore oil-and-gas sector representing the largest single application (floating-production-storage-offloading mooring ropes) and Saudi Arabia's petrochemical complexes evaluating LCP for chemical-processing equipment (pump diaphragms, valve seats) exposed to concentrated acids and bases.

Competitive Landscape

The Liquid Crystal Polymer (LCP) Fibers market is highly consolidated. Kuraray monopolizes melt-spun yarn under the VECTRAN brand, while Polyplastics, Celanese, and Sumitomo Chemical scale resin plants that empower converters to extrude films and monofilaments. Regulatory files (ISO 13485 and FDA Master Access) and application engineering expertise remain durable barriers to new entrants.

Liquid Crystal Polymer (LCP) Fibers Industry Leaders

Kuraray Co., Ltd.

Celanese Corporation

Sumitomo Chemical Co., Ltd.

TORAY INDUSTRIES, INC.

Polyplastics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Z-Polymers Inc. announced a strategic investment from the wholly owned U.S. subsidiary of Tokyo-based Kureha Corp., along with a joint development agreement aimed at accelerating the commercialization of Z-Polymers’ proprietary Tullomer liquid crystal polymer (LCP) platform. These high-performance fibers are reported to exceed the mechanical and thermal performance of conventional melt-processable liquid crystal polymers.

- December 2025: Polyplastics Co., Ltd. expanded its LAPEROS liquid crystal polymer (LCP) product line with the launch of the new LH and TF series materials, which meet the electronics market’s growing demand for higher performance and miniaturization. This innovation can bolster the global LCP fibers market.

Global Liquid Crystal Polymer (LCP) Fibers Market Report Scope

Liquid Crystal Polymer (LCP) fibers are high-performance, melt-spun thermoplastic filaments known for exceptional strength, high modulus, and superior creep resistance. They are five times stronger than steel and possess high chemical/thermal resistance, making them ideal for specialized industrial, electronics, and aerospace applications.

The Liquid Crystal Polymer (LCP) Fibers market report is segmented by fiber form (filament yarn (mono-/multi-filament), staple fiber, spun yarn, woven fabric, and non-woven/other converted forms), product grade (standard grade, high-tenacity grade, high thermal/chemical-resistance grade, and surface-treated/coated grade), application (ropes, cables, and tethers, reinforcement (composites and industrial), protective and technical textiles, medical and healthcare, electrical and electronics, and other applications), end-user industry (aerospace and defense, marine and offshore, automotive and transportation, industrial and machinery, healthcare, and other end-user industries). The report also covers the market size and forecasts for liquid crystal polymer (LCP) fibers in 15 countries across major regions. The market forecasts are provided in terms of value (USD).

| Filament Yarn (Mono-/Multi-filament) |

| Staple Fiber |

| Spun Yarn |

| Woven Fabric |

| Non-woven/Other Converted Forms |

| Standard Grade |

| High-Tenacity Grade |

| High Thermal/Chemical-Resistance Grade |

| Surface-Treated/Coated Grade |

| Ropes, Cables and Tethers |

| Reinforcement (Composites and Industrial) |

| Protective and Technical Textiles |

| Medical and Healthcare |

| Electrical and Electronics |

| Other Applications |

| Aerospace and Defense |

| Marine and Offshore |

| Automotive and Transportation |

| Industrial and Machinery |

| Healthcare |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Fiber Form | Filament Yarn (Mono-/Multi-filament) | |

| Staple Fiber | ||

| Spun Yarn | ||

| Woven Fabric | ||

| Non-woven/Other Converted Forms | ||

| By Product Grade | Standard Grade | |

| High-Tenacity Grade | ||

| High Thermal/Chemical-Resistance Grade | ||

| Surface-Treated/Coated Grade | ||

| By Application | Ropes, Cables and Tethers | |

| Reinforcement (Composites and Industrial) | ||

| Protective and Technical Textiles | ||

| Medical and Healthcare | ||

| Electrical and Electronics | ||

| Other Applications | ||

| By End-user Industry | Aerospace and Defense | |

| Marine and Offshore | ||

| Automotive and Transportation | ||

| Industrial and Machinery | ||

| Healthcare | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the liquid crystal polymer (LCP) fibers market?

The liquid crystal polymer (LCP) fibers market stands at USD 50.37 million in 2026 and is projected to reach USD 98.36 million by 2031.

Why do 5G connectors prefer LCP over traditional polymers?

LCP offers dielectric constants around 2.9 and dissipation factors below 0.002 up to 38 GHz, minimizing signal loss in millimeter-wave antennas.

What keeps Kuraray dominant in high-tenacity LCP yarn?

Proprietary melt-spinning assets, 830 g/d modulus grades, and established aerospace qualifications deter new fiber entrants.

Which application is the fastest-growing for LCP fibers?

Medical and healthcare devices are rising at a 24.07% CAGR during the forecast period (2026-2031)owing to sterilizable catheter braids and micro-molded drug-delivery parts.

Page last updated on: