Life Sciences Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

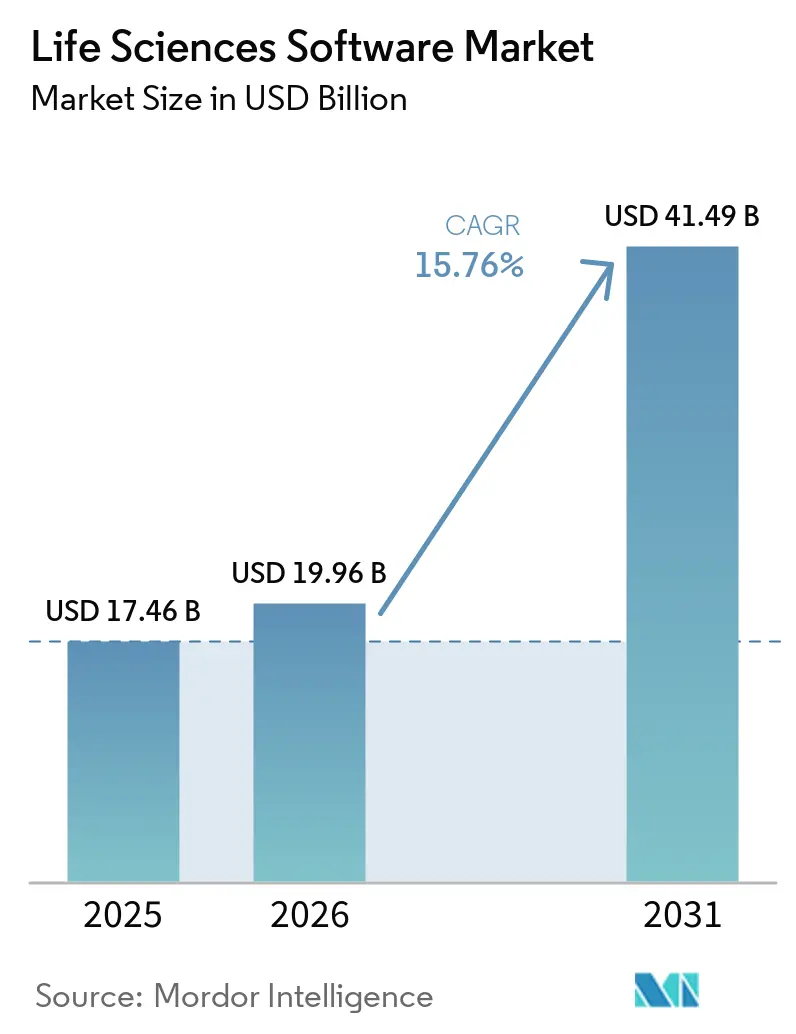

| Market Size (2026) | USD 19.96 Billion |

| Market Size (2031) | USD 41.49 Billion |

| Growth Rate (2026 - 2031) | 15.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Life Sciences Software Market Analysis by Mordor Intelligence

The Life Sciences Software Market size is expected to grow from USD 17.46 billion in 2025 to USD 19.96 billion in 2026 and is forecast to reach USD 41.49 billion by 2031 at 15.76% CAGR over 2026-2031.

The pace of the life sciences software market reflects steady demand for digital systems across discovery, clinical development, regulatory work, quality operations, and post-market safety management. Regulatory requirements for audit-ready electronic records continue to push companies away from paper files and disconnected legacy applications toward integrated platforms that can support validation, traceability, and standardized submissions. AI-enabled workflow tools are also changing buying behavior in the life sciences software market, because customers increasingly prefer platforms that combine analysis, automation, and compliance in one environment instead of maintaining several separate tools. Large pharmaceutical companies remain the main spending base, while emerging biotechs and service providers are expanding adoption as cloud delivery, shared data models, and API-based integration reduce deployment friction. The competitive pattern in the life sciences software market remains mixed, with a small group of broad platform vendors leading in regulated and commercial workflows, while many focused providers still compete in discovery informatics, bioinformatics, laboratory systems, and quality applications.

Key Report Takeaways

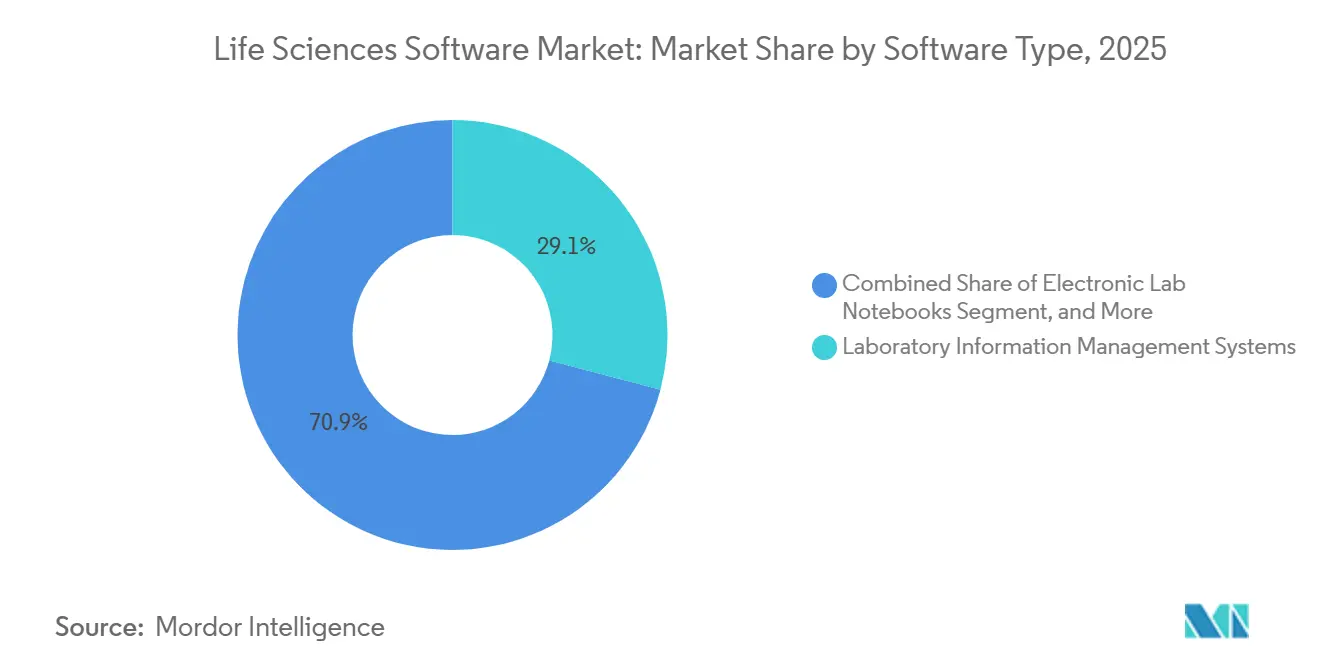

- By software type, laboratory information management systems held 29.13% of the life sciences software market share in 2025, while electronic lab notebooks are projected to grow at a 16.78% CAGR through 2031.

- By deployment, cloud-based deployment accounted for 71.83% share of the life sciences software market size in 2025 and is also projected to advance at a 15.85% CAGR through 2031.

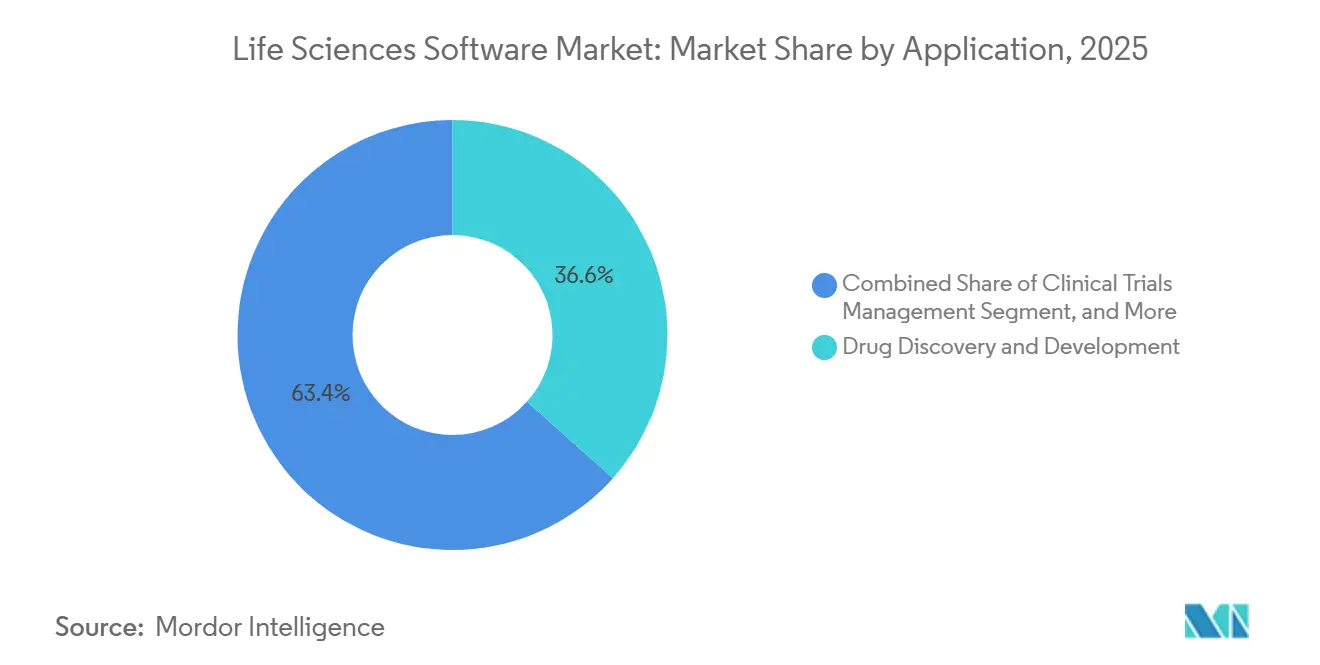

- By application, drug discovery and development accounted for 36.64% share of the life sciences software market size in 2025, while regulatory compliance and submissions are forecast to expand at an 18.05% CAGR through 2031.

- By end user, pharmaceutical companies held 54.23% share of the life sciences software market share in 2025, while biotechnology companies are projected to grow at a 16.17% CAGR through 2031.

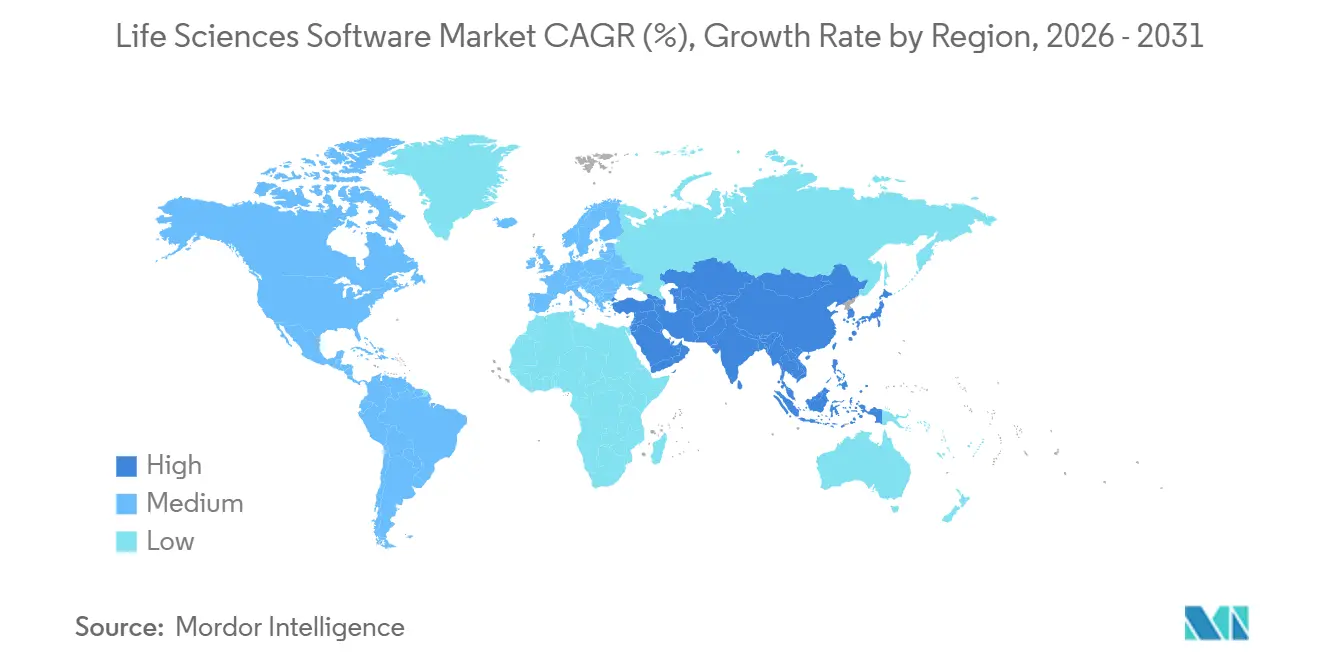

- By geography, North America held 41.23% of the life sciences software market in 2025, while Asia-Pacific is projected to record the fastest regional growth at a 17.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Life Sciences Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Regulated Digital Recordkeeping in Drug Development | +3.2% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Expansion of Multi-Modal Clinical and Real-World Data Workflows | +2.0% | Global, with deepening traction in North America and Asia-Pacific | Medium term (2-4 years) |

| Cloud Migration for Cross-Site Scientific Collaboration | +2.6% | Global, with fastest uptake in Asia-Pacific and broad adoption in North America and the EU | Short term (≤ 2 years) |

| AI-Enabled Trial Optimization and Bioinformatics Adoption | +2.4% | Global, led by North America with rapid acceleration in Asia-Pacific | Medium term (2-4 years) |

| Software Validation Complexity Favoring Integrated Suites Over Point Tools | +1.1% | Global, most acute in North America and the EU | Medium term (2-4 years) |

| Growth in Cell and Gene Therapy, and Multi-Omics Workloads | +1.6% | North America and Europe, with emerging demand in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Regulated Digital Recordkeeping in Drug Development

The move from paper records to validated digital systems has become a core operating requirement across the life sciences software market, especially in laboratories, safety teams, and regulatory functions. The FDA confirmed that all postmarketing Individual Case Safety Reports submitted through ESG NextGen must follow ICH E2B(R3) electronic standards from October 1, 2026, which is forcing upgrades in pharmacovigilance platforms that still rely on older workflows.[1]U.S. Food and Drug Administration, “Electronic Submission of Postmarketing Individual Case Safety Reports to the Food and Drug Administration,” Federal Register, federalregister.gov The same compliance push is visible in regulatory submissions, where the FDA accepted eCTD v4.0 from September 2024, and regulators in the United States and Europe have encouraged companies to pilot the standard early. The U.S. Pharmacopeia also launched MethodConnect in May 2026, creating a machine-readable library of more than 2,600 verified methods that can connect directly with LIMS, LES, and ELN platforms. These parallel deadlines are pushing buyers in the life sciences software market toward fewer, broader platforms, because validating one integrated stack is often simpler than revalidating several disconnected tools. That shift is supporting vendors that combine laboratory, quality, regulatory, and safety capabilities in one architecture, especially when those modules share a common data model and audit framework.

AI-Enabled Trial Optimization and Bioinformatics Adoption

AI tools are reshaping how research teams use the life sciences software market, because faster model-based decisions now matter in discovery, protocol design, and data review. Benchling launched Model Hub in May 2026 to embed scientific AI models directly inside R&D workflows, and the company linked that effort to partnerships that give customers access to models built on Eli Lilly research data. Schrödinger connected TuneLab to LiveDesign in January 2026, and later reported full-year 2025 software revenue of USD 199.5 million with 2026 Annual Contract Value guidance of USD 218 million to USD 228 million. These moves matter in the life sciences software market because smaller biotech companies can now use trained models inside commercial platforms without building large internal AI teams. That narrows part of the historical capability gap between large pharmaceutical groups and emerging biotech companies. It also helps explain why biotechnology companies are the fastest-growing end-user cohort through 2031, as AI access becomes easier to embed in everyday research workflows.

Cloud Migration for Cross-Site Scientific Collaboration

Cloud adoption has become a structural force in the life sciences software market, because modern development programs depend on shared data across sites, functions, and partners. GSK consolidated data from 1,500 active studies and more than 6 million records after moving to Veeva CTMS, while removing more than 100 legacy integrations in the process.[2]Veeva Systems, “An Inside Look at GSK’s Successful CTMS Modernization Journey,” Veeva Systems, veeva.com Recordati also reported a 25% cut in document lifecycle time and zero inspection findings after centralizing oversight on the Veeva Clinical Platform. The Association of Clinical Research Professionals stated in February 2026 that modern cloud migration supports the higher data volumes created by digital biomarkers and remote monitoring. Even so, the life sciences software market is not shifting to the cloud in a uniform way, because regulated environments still require validation of the application and the infrastructure that hosts it. That requirement continues to favor specialized SaaS vendors that can provide pre-validated environments, documented controls, and established compliance packages.

Growth in Cell and Gene Therapy, and Multi-Omics Workloads

Cell and gene therapy programs are adding new complexity to the life sciences software market because these programs need chain-of-identity tracking, controlled manufacturing records, and genomic data management in one operating flow. The FDA finalized guidance on CMC flexibilities for cell and gene therapies in May 2026 and issued new draft guidance in June 2026 on the use of platform knowledge in gene therapy submissions.[3]Regulatory Affairs Professionals Society, “FDA Finalizes Guidance on CMC Flexibilities for Cell and Gene Therapies,” RAPS, raps.org Those actions support a stronger demand for software that can manage structured development and submission records across highly controlled programs. In the research layer, OmnibusX was published in PLOS Computational Biology in 2026 as an end-to-end platform for multi-omics analysis that reduces the need for coding expertise. The broader message for the life sciences software market is that vendors need to support proteomics, transcriptomics, sequence analysis, and manufacturing traceability in more connected ways. As these workloads expand from academic settings into mainstream biopharma R&D, software providers with stronger data orchestration and workflow coverage are likely to gain a durable position.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Validation, Integration, and Change Management | -1.5% | Global, most severe in North America, the EU, and Japan where GxP validation requirements are strictest | Medium term (2-4 years) |

| Interoperability Gaps Across Legacy Lab, Clinical, and Commercial Systems | -1.1% | Global, most pronounced in large pharmaceutical organizations with multi-decade system estates | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Constraints in Cloud Deployment | -0.8% | Europe, China, India, Japan, with growing regulatory scope in North America | Long term (≥ 4 years) |

| Skills Shortage in Bioinformatics, Quality Systems, and Regulatory Informatics | -0.5% | Global, most acute in emerging markets and mid-size organizations without dedicated informatics teams | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Validation, Integration, and Change Management

The cost of deploying the life sciences software market goes well beyond license fees, because validated systems in regulated settings require testing, documentation, training, and change control before go-live. That burden is especially visible in quality and manufacturing settings, where installation qualification, operational qualification, and performance qualification can delay deployment for months. MasterControl reported in 2026 that 43% of surveyed pharmaceutical quality leaders ranked quality defect prediction and prevention among their top three AI priorities, yet employee engagement with quality systems remained a major barrier. The same company launched AI-powered SOP Analyzer in January 2026 and Event Summarizer in April 2026, showing that vendors are trying to reduce friction after deployment, not just sell new features. Buyers in the life sciences software market are therefore paying closer attention to training effort, validation reuse, and implementation services when comparing vendors. That favors integrated suites when they can reduce the number of systems that must be tested and maintained across the same regulated workflow.

Cybersecurity and Data Sovereignty Constraints in Cloud Deployment

Cybersecurity and data control issues continue to slow parts of the life sciences software market, even as cloud adoption remains the main direction of travel. Regulated buyers are under pressure to confirm where data is stored, how access is controlled, and how vendors manage incident response across internal and partner environments. This is one reason hybrid architectures remain relevant in the life sciences software market, especially where global research operations intersect with local compliance obligations. MasterControl achieved FedRAMP Moderate authorization for Quality Excellence Gov in May 2025, which showed that security accreditation can become a clear buying advantage in regulated procurement. Buyers are also looking for clearer security governance around AI functions, particularly when those functions touch quality, safety, or submission content. The result is a slower and more selective migration path, with customers favoring vendors that can document security controls, validated hosting, and country-specific deployment options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: LIMS Leads While AI-Native ELN Platforms Converge with Discovery Informatics

Laboratory Information Management Systems held 29.13% of the life sciences software market in 2025, which kept LIMS as the largest software type in regulated laboratory operations. Electronic Lab Notebooks are projected to grow at a 16.78% CAGR through 2031, making ELN the fastest-growing software type as organizations replace paper-based records with structured digital workflows. This pattern shows that the life sciences software market still relies on LIMS for control and traceability, while newer spending is leaning toward collaborative and AI-enabled research tools. Large pharmaceutical companies continue to use LIMS as the backbone for sample management, quality control, and manufacturing support in GxP settings. At the same time, mid-size biotechs and service organizations are increasing ELN adoption because implementation is now easier within cloud-ready research environments.

The software type mix across the life sciences software market is also becoming less siloed, because vendors increasingly combine laboratory control, documentation, and analytics in one suite. LabVantage released version 8.9 of its LIMS platform in March 2025 with AI-driven productivity features, stronger ELN functionality, and audit trail filtering. Sapio Sciences introduced what it described as the first 3rd-generation ELN in September 2025, with embedded AI support across cheminformatics, bioinformatics, and structure-based design. USP MethodConnect adds another layer to this shift, because machine-readable methods can reduce manual setup work inside connected LIMS and ELN environments. The result is that the life sciences software industry is moving toward broader laboratory informatics suites rather than keeping LIMS and ELN as isolated purchasing categories.

By Deployment: Cloud Dominance Masks a Persistent Hybrid Architecture Requirement

Cloud-based deployment accounted for 71.83% of the life sciences software market in 2025 and is projected to expand at a 15.85% CAGR through 2031, which means the largest deployment model is also the fastest-growing one. That combination shows the cloud shift is advanced, but not complete, across the life sciences software market. Enterprise customers are moving major clinical, quality, and commercial workloads to cloud environments because cross-site access and centralized upgrades are now core operating requirements. Oracle reported 24% growth in total cloud revenue in fiscal 2025 and expected more than 40% growth in fiscal 2026 across cloud applications and infrastructure. Veeva stated that more than 125 customers were live on Vault CRM in 2026 and that 14 of the top 20 biopharmas are expected to commit globally, which underscores the scale of cloud adoption in regulated commercial software.

Even with that momentum, on-premises and hybrid models still matter in the life sciences software market because validation risk, migration cost, and continuity needs remain high in manufacturing and quality systems. Many organizations continue to keep GxP-critical records in controlled local environments while adding cloud-based analytics and collaboration layers on top. This is less a sign of cloud resistance and more a sign of careful migration across validated environments. MasterControl’s FedRAMP authorization in 2025 showed that secure cloud pathways are expanding, but they still depend on strong documentation and approved controls. Over time, the life sciences software market is likely to keep favoring cloud delivery, yet hybrid architecture will remain important where sovereign hosting, audit readiness, and revalidation cost still shape deployment decisions.

By Application: Drug Discovery Anchors Demand While Regulatory Submissions Drive the Fastest Expansion

Drug Discovery and Development represented 36.64% of the life sciences software market in 2025, which made it the largest application area across research and early development workflows. Regulatory Compliance and Submissions is projected to grow at an 18.05% CAGR through 2031, the fastest application rate in the life sciences software market. This gap shows that discovery remains the main spending base, while regulatory systems are gaining importance because submissions, safety reporting, and structured data standards are becoming more demanding. Drug discovery platforms continue to benefit from the growth of computational chemistry, biological data analysis, and lab automation. Regulatory platforms, in contrast, are gaining share because poor submission readiness can now slow approvals, increase remediation work, and create direct business risk.

The vendor actions in this segment show how quickly application priorities are shifting inside the life sciences software market. ArisGlobal launched XDI in February 2026 and said the product can reduce pharmacovigilance compliance efforts by 70% to 80%, while a top-10 pharmaceutical company selected its advanced intake and literature intelligence capability for a safety volume of around 500,000 cases a year. ArisGlobal also launched NavaX Translation in February 2026 to cut manual translation time in global pharmacovigilance case processing. Veeva had its first AI agents live in CRM and commercial content from December 2025, which showed that AI deployment is expanding beyond research and into field-facing application areas. The FDA’s October 2026 ICH E2B(R3) requirement is also driving active replacement cycles in safety systems, which gives compliant vendors a clear near-term revenue opening.

By End User: Pharma as the Foundation, Biotechs and CDMOs as the Expansion Frontier

Pharmaceutical companies accounted for 54.23% of the life sciences software market in 2025, which keeps pharma as the main demand base across regulated and research-intensive workflows. Biotechnology companies are projected to grow at a 16.17% CAGR through 2031, the fastest end-user rate in the life sciences software market. Large pharmaceutical buyers still support the biggest budgets, especially in CTMS, regulatory systems, safety platforms, commercial applications, and quality management. Their spending mix is changing, though, because more of the budget now goes to the replacement of older platforms and the removal of integration debt from accumulated point solutions. That replacement cycle supports vendors that can show validated migration paths, broad workflow coverage, and lower long-term maintenance effort.

The faster growth among biotechs and service providers comes from simpler access to advanced tools, not from lower complexity in their science. Benchling partnered with Lilly TuneLab in January 2026 to make AI models available to more than 1,300 biotech customers, which lowers a major entry barrier for smaller organizations that lack large internal model development teams. CDMOs, CROs, medical device companies, academic institutes, and diagnostics labs each bring different requirements to the life sciences software market, especially around sponsor separation, quality events, and controlled documentation. MasterControl highlighted its Quality Excellence platform for CDMOs in December 2025 with a focus on QMSR and ISO 13485 compliance, which reflects the different quality framework in device-related operations. The life sciences software industry is therefore expanding beyond traditional pharma buyers, but growth remains strongest where new customer groups can access validated cloud systems without building large informatics teams from scratch.

Geography Analysis

North America held 41.23% of the life sciences software market in 2025, which made it the largest regional contributor. The United States remains the center of demand because it combines the highest concentration of pharmaceutical and biotech R&D spending with the most mature set of digital regulatory expectations. FDA support for eCTD v4.0 from September 2024 and the mandatory shift to ICH E2B(R3) postmarketing safety reporting from October 2026 create a concentrated compliance cycle that supports steady platform replacement and expansion. That environment favors vendors with stronger submission, safety, and audit-ready workflow capabilities across the life sciences software market. Canada and Mexico remain smaller contributors, but both continue to support demand in clinical, discovery, and laboratory informatics.

Europe remains a major region in the life sciences software market because regulatory modernization is pushing upgrades in clinical and regulatory systems. Regulators in both the United States and Europe encouraged companies to pilot eCTD v4.0, and the EMA accepted the standard from late December 2025. That has increased attention on submission platforms that can support parallel transition schedules across regions. The region also remains important for validated quality and manufacturing systems, where software changes tend to move more slowly because deployment carries a heavier documentation burden. As a result, the life sciences software market in Europe continues to reward vendors that can combine cloud flexibility with stronger compliance packaging and controlled implementation paths.

Asia-Pacific is projected to expand at a 17.13% CAGR through 2031, making it the fastest-growing region in the life sciences software market. Growth is being supported by rising biopharma investment, wider digital infrastructure, and faster development activity across the region’s largest markets. IQVIA highlighted in early 2026 that China introduced fast-track IND reviews that allow innovative drug applications to proceed within 30 working days, which helps compress trial initiation timelines and raises the need for stronger CTMS and regulatory systems. The Middle East and Africa and South America remain smaller contributors, but targeted demand continues to build around clinical operations, safety systems, and outsourced development services.

Competitive Landscape

The life sciences software market has a dual structure, with a concentrated top layer of broad platform vendors and a much wider field of specialized providers. Veeva Systems, Oracle, SAP, Dassault Systèmes including Medidata, and IQVIA compete for large enterprise programs that cut across clinical, quality, regulatory, and commercial functions. Specialized vendors remain active in laboratory informatics, discovery platforms, bioinformatics, pharmacovigilance, and quality workflows, where customers still buy best-fit tools for specific use cases. This mix means the life sciences software market is neither fully consolidated nor fully fragmented. It also means switching costs are high in some sub-segments and much lower in others, depending on validation depth and workflow scope.

Recent company moves show that scale and platform breadth are becoming more important in the life sciences software market. Siemens completed its USD 5.1 billion acquisition of Dotmatics in July 2025, bringing a scientific software platform used by more than 2 million scientists and 14,000 customers into Siemens Digital Industries Software. Veeva reported total fiscal year 2026 revenue of USD 3,195.3 million, up 16% year over year, and continued rolling out AI agents across core commercial workflows. MasterControl used compliance credibility as a competitive tool by securing FedRAMP Moderate authorization in 2025 and building AI capabilities on top of controlled governance. ArisGlobal expanded NavaX Agents Suite in March 2026 with additional agentic systems for publishing, signals, and dossier compliance review.

The strongest white-space opportunities in the life sciences software market remain in mid-size biotechs, CDMOs, and device-oriented quality environments. Those buyers often need strong compliance support, but they do not always want the cost and complexity of a very broad enterprise stack. Benchling, Sapio Sciences, Dotmatics, and other focused vendors are using AI-enabled workflow design and faster deployment to compete for these accounts. Even so, regulatory expectations across submission, safety, quality, and laboratory systems still favor vendors with stronger validation support and documented compliance controls. That limits how quickly new entrants can disrupt the most regulated parts of the market. It also keeps M&A, platform expansion, and module integration at the center of competition across the life sciences software market.

Life Sciences Software Industry Leaders

Agilent Technologies, Inc.

IQVIA Holdings Inc.

Microsoft Corporation

Oracle Corporation

Veeva Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Benchling launched Model Hub and Benchling Inference. Model Hub puts scientific AI models inside the R&D workflow for all Benchling customers, with proprietary access through partnerships with Lilly TuneLab and Boltz PBC. Benchling Inference, built on Baseten, provides scalable GPU capacity for in silico discovery without infrastructure management across 1,300+ biotech customers, accelerating AI-native drug discovery for companies of all sizes.

- May 2026: USP launched MethodConnect. The U.S. Pharmacopeia launched a machine-readable library of 2,600+ verified test methods for direct LIMS, LES, and ELN integration. Agilent Technologies is the first platform integrator via OpenLab Sync, connecting USP-NF content directly into digital, operational laboratory workflows.

- April 2026: MasterControl launched AI-powered Event Summarizer. A new AI capability within Quality Excellence that generates instant summaries of complex quality events, enabling quality leaders to rapidly assess status and take action, directly addressing the engagement barrier identified in the company’s 2026 pharmaceutical quality survey.

- April 2026: Benchling launched AI Connectors (MCP-based). Connecting Benchling’s structured R&D data repository to the growing ecosystem of external AI tools using Model Context Protocol, enabling AI systems to query, retrieve, and reason over experimental data in standardized workflows across biotech R&D.

Global Life Sciences Software Market Report Scope

Life Sciences Software comprises specialized IT platforms designed for the biotechnology, pharmaceutical, and medical device sectors. These solutions automate research, manage clinical trials, ensure regulatory compliance, and optimize supply chains.

The Life Sciences Software Market is segmented across several dimensions. By software type, it includes Laboratory Information Management Systems, Electronic Lab Notebooks, Clinical Trial Management Systems, Regulatory Information Management Systems, Quality Management Systems, Pharmacovigilance Software, Bioinformatics and Genomics Software, Drug Discovery Informatics, Scientific Data Management Systems, Manufacturing Execution Systems, and Sales, CRM, and Commercial Operations Software. By deployment, the market is segmented into Cloud-Based, On-Premises, and Hybrid solutions. By application, the market spans Drug Discovery and Development, Clinical Trials Management, Laboratory Operations and Sample Management, Regulatory Compliance and Submissions, Quality Assurance and Audit Management, Pharmacovigilance and Safety, Commercial Operations and Field Engagement, and Bioinformatics and Multi-Omics Analytics. By end user, the market is divided into Pharmaceutical Companies, Biotechnology Companies, Contract Research Organizations, Contract Development and Manufacturing Organizations, Medical Device Companies, Academic and Research Institutes, and Diagnostic Laboratories.

Geographically, the market is segmented into North America (United States, Canada, Mexico); Europe (Germany, United_Kingdom, France, Italy, Spain, and Rest of Europe); Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific); Middle East & Africa (GCC, South Africa, and Rest of Middle East & Africa); and South America (Brazil, Argentina, and Rest of South America).

| Laboratory Information Management Systems |

| Electronic Lab Notebooks |

| Clinical Trial Management Systems |

| Regulatory Information Management Systems |

| Quality Management Systems |

| Pharmacovigilance Software |

| Bioinformatics and Genomics Software |

| Drug Discovery Informatics |

| Scientific Data Management Systems |

| Manufacturing Execution Systems |

| Sales, CRM, and Commercial Operations Software |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Drug Discovery and Development |

| Clinical Trials Management |

| Laboratory Operations and Sample Management |

| Regulatory Compliance and Submissions |

| Quality Assurance and Audit Management |

| Pharmacovigilance and Safety |

| Commercial Operations and Field Engagement |

| Bioinformatics and Multi-Omics Analytics |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Contract Research Organizations |

| Contract Development and Manufacturing Organizations |

| Medical Device Companies |

| Academic and Research Institutes |

| Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Software Type | Laboratory Information Management Systems | |

| Electronic Lab Notebooks | ||

| Clinical Trial Management Systems | ||

| Regulatory Information Management Systems | ||

| Quality Management Systems | ||

| Pharmacovigilance Software | ||

| Bioinformatics and Genomics Software | ||

| Drug Discovery Informatics | ||

| Scientific Data Management Systems | ||

| Manufacturing Execution Systems | ||

| Sales, CRM, and Commercial Operations Software | ||

| By Deployment | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Drug Discovery and Development | |

| Clinical Trials Management | ||

| Laboratory Operations and Sample Management | ||

| Regulatory Compliance and Submissions | ||

| Quality Assurance and Audit Management | ||

| Pharmacovigilance and Safety | ||

| Commercial Operations and Field Engagement | ||

| Bioinformatics and Multi-Omics Analytics | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Contract Research Organizations | ||

| Contract Development and Manufacturing Organizations | ||

| Medical Device Companies | ||

| Academic and Research Institutes | ||

| Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of life sciences software in 2026?

The life sciences software market stands at USD 19.96 billion in 2026 and is forecast to reach USD 41.49 billion by 2031, growing at a 15.76% CAGR over 2026-2031.

Which software type leads demand across laboratories and regulated operations?

LIMS remained the largest software type in 2025 with a 29.13% share, supported by its role in sample tracking, data integrity, and GxP-ready laboratory workflows.

Why is regulatory software growing faster than other application areas?

Regulatory Compliance and Submissions is projected to grow at an 18.05% CAGR through 2031 because eCTD v4.0 and ICH E2B(R3) requirements are pushing faster upgrades in submission and safety systems.

Why does cloud remain the main deployment model in this space?

Cloud held 71.83% share in 2025 because companies need cross-site access, easier upgrades, and better collaboration across research, clinical, quality, and commercial teams.

Which end users are expanding fastest through 2031?

Biotechnology companies are projected to grow at a 16.17% CAGR as AI-ready and cloud-based platforms lower entry barriers for advanced research and data management tools.

Which region offers the strongest growth outlook?

Asia-Pacific is projected to record the fastest regional growth at a 17.13% CAGR through 2031, supported by stronger biopharma investment, regulatory activity, and digital development infrastructure.

Page last updated on: