Leber Congenital Amaurosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

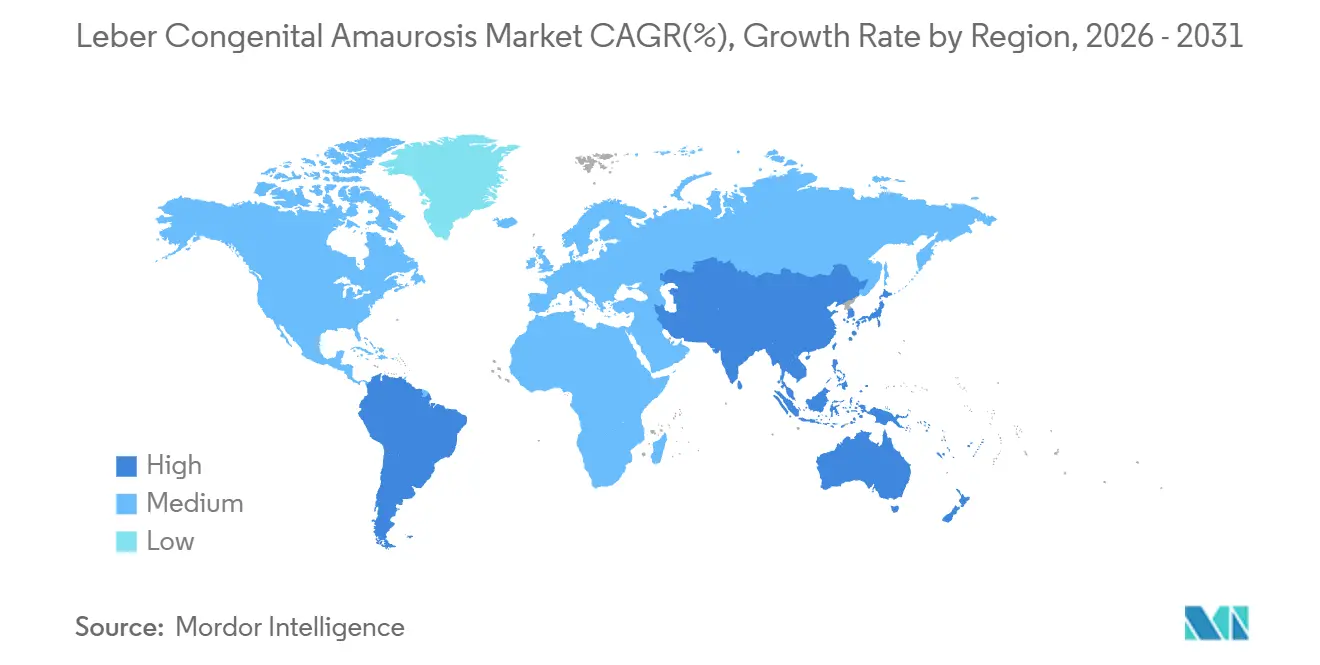

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leber Congenital Amaurosis Market Analysis by Mordor Intelligence

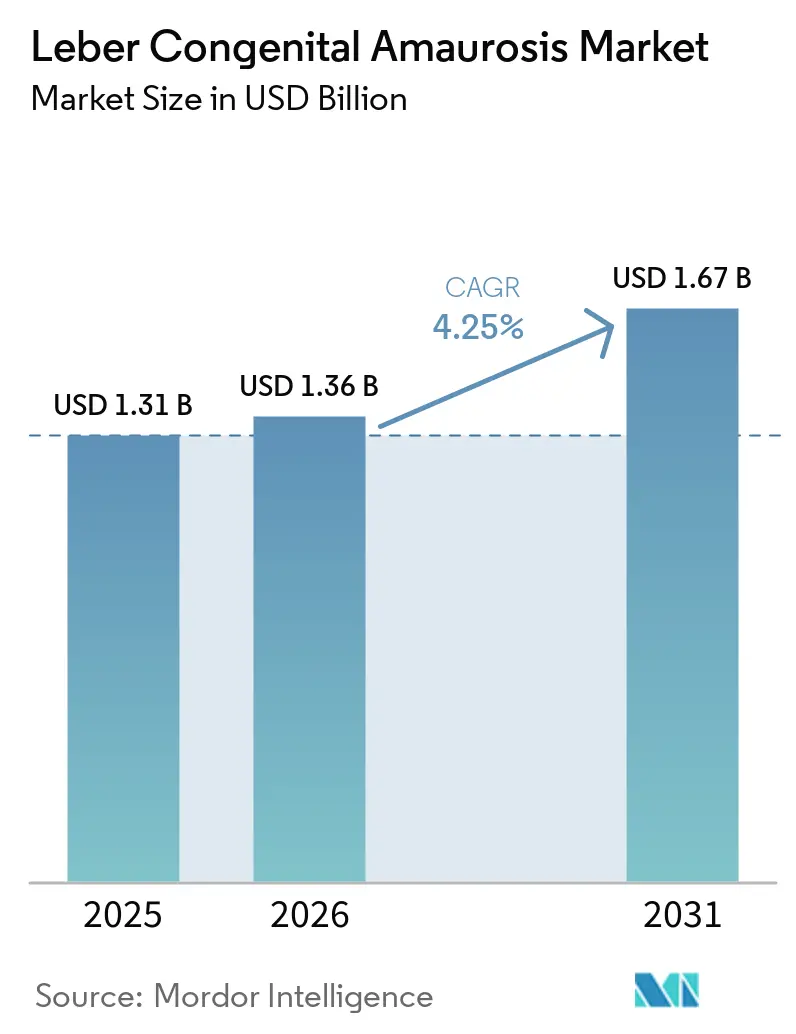

The Leber Congenital Amaurosis Market size was valued at USD 1.31 billion in 2025 and is estimated to grow from USD 1.36 billion in 2026 to reach USD 1.67 billion by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

The Leber congenital amaurosis market is expanding at a steady pace, reflecting the structural realities of ultra-orphan genetics and the small pool of confirmed, targetable mutations. Gene therapy remains the anchor of the Leber congenital amaurosis market, supported by advancing pipelines and a growing base of clinical programs that target single-gene defects with well-defined functional endpoints. Pricing dynamics influence access, since the USD 425,000 per eye list price for voretigene neparvovec creates friction between durability expectations and payer willingness for one-time therapies. In 2025, North America retained the largest regional position, while Asia-Pacific is set to be the fastest-growing geography through 2031 as manufacturing and clinical infrastructure scale. Government-backed facilities such as Australia’s viral vector manufacturing hub add capacity for sponsors that focus on inherited retinal diseases, supporting multi-center trials and later-stage supply.

Key Report Takeaways

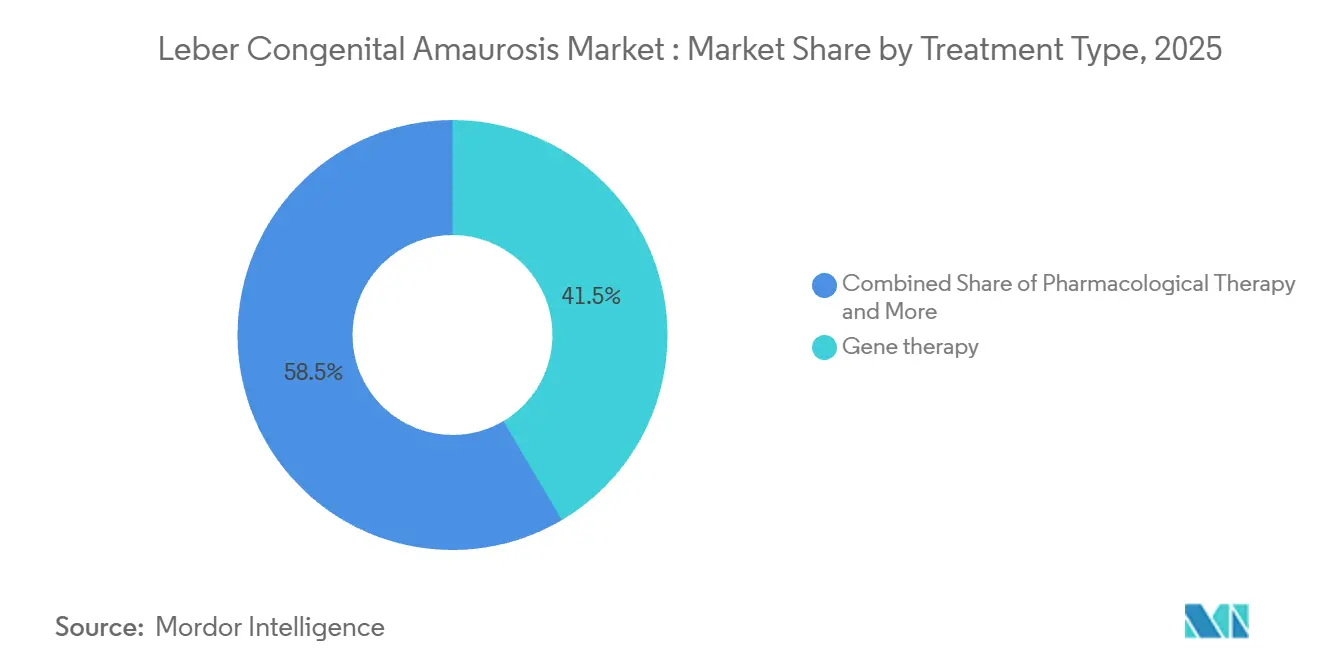

By treatment type, gene therapy led with 41.50% revenue share in 2025 and is projected to expand at 4.78% annually through 2031.

By target gene, CEP290 accounted for 25.81% share in 2025 and is expected to grow at a 4.66% rate through 2031.

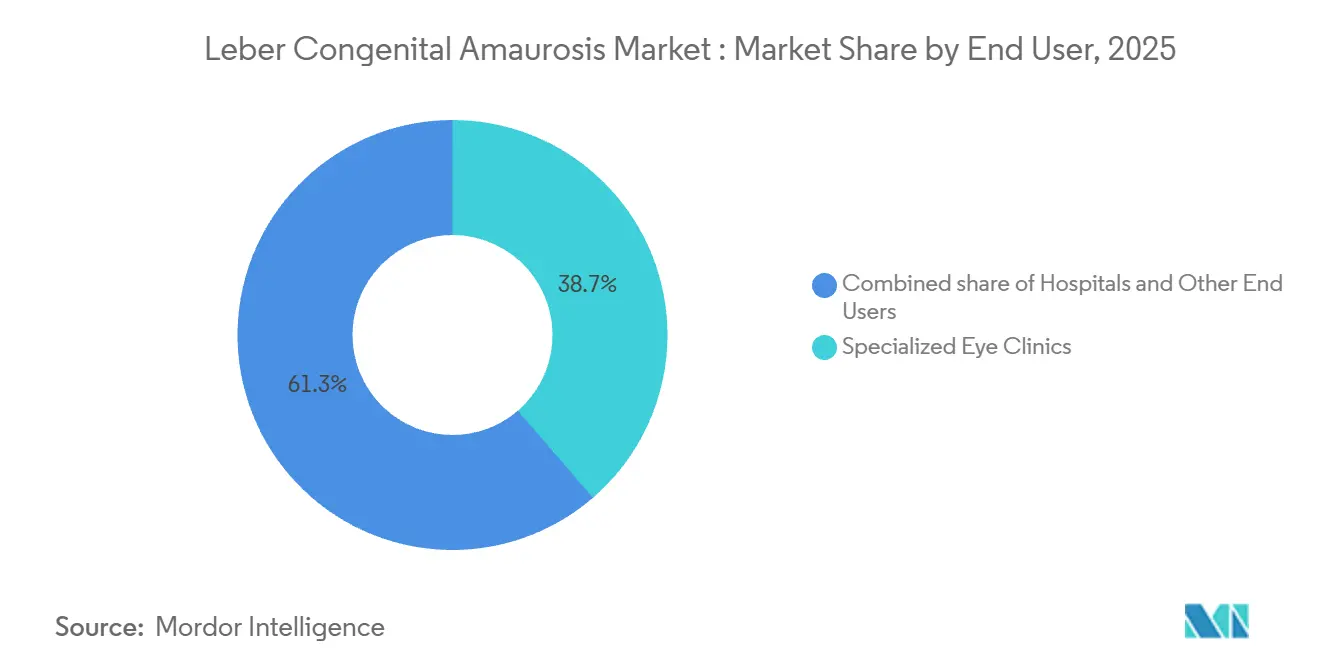

By end user, specialized eye clinics held 38.67% share in 2025, while ophthalmology research centers are set to record the fastest growth at 4.98% through 2031.

By geography, North America captured 45.18% share in 2025, while Asia-Pacific is expected to post the highest growth at 4.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Leber Congenital Amaurosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid commercial uptake of Luxturna and forthcoming gene-therapy approvals | +0.9% | North America and EU | Medium term (2-4 years) |

| Expansion of newborn, carrier, and population genetic-testing panels | +0.7% | Global, with early gains in US, Australia, UK | Long term (≥ 4 years) |

| Orphan-drug, Priority Review, and Rare Pediatric Disease incentives | +0.6% | US and EU | Short term (≤ 2 years) |

| Rising venture, pharma, and public funding for inherited retinal disease R&D | +1.0% | North America, EU core with spillover to Singapore and Australia | Medium term (2-4 years) |

| Asia-Pacific viral-vector manufacturing hubs delivering lower COGS | +0.5% | APAC core with supply chains to US and EU | Long term (≥ 4 years) |

| AI-guided adaptive-optics retinal imaging platforms | +0.4% | Advanced research centers globally with early adoption in US and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Commercial Uptake of Luxturna and Forthcoming Gene-Therapy Approvals

Voretigene neparvovec established proof-of-concept for AAV-mediated ocular gene augmentation and remains a clinical precedent that validates one-time treatment strategies in pediatric-onset blindness. Adoption is shaped by the high list price and the concentration of administration within a network of designated subretinal injection centers. The pipeline is diversifying across multiple LCA genotypes as next-generation constructs pursue pivotal paths backed by regulatory designations. Opus Genetics advanced OPGx-LCA5 with Regenerative Medicine Advanced Therapy status, setting up a pivotal design that aims to convert earlier functional gains into confirmatory outcomes. MeiraGTx reported clinically meaningful visual acuity gains with AAV-AIPL1 in children with LCA4, and the program is being positioned for regulatory review in the United Kingdom and dialogue with U.S. authorities [1]MeiraGTx Authors, “Gene therapy for AIPL1-associated Leber congenital amaurosis,” .

Expansion of Newborn, Carrier, and Population Genetic-Testing Panels

Genomic newborn screening programs and expanded carrier testing are broadening the diagnostic funnel for inherited retinal diseases that present in infancy or early childhood. A U.S. pilot, Early Check, showed a measurable yield of actionable findings through genome sequencing in a general newborn cohort, supporting earlier identification of ultra-rare conditions that can inform trial enrollment and clinical surveillance. Carrier screening guidance encourages universal, ethnicity-agnostic approaches for conditions with relevant carrier frequencies, which cover many LCA-associated genes. ACOG affirmed broad support for expanded carrier screening, which aligns obstetric practice with genetic approaches that can identify at-risk families before symptom onset in offspring. Earlier diagnosis and counseling increase the likelihood of timely referral to specialized centers and faster entry into gene-therapy pathways, adding momentum to the Leber congenital amaurosis market.

Orphan-Drug, Priority Review, and Rare Pediatric Disease Incentives

Incentive frameworks support late-stage development by aligning regulatory resources with ultra-orphan pediatric conditions. Programs such as RMAT help sponsors secure iterative guidance that can compress timelines once early efficacy is established on clinically meaningful endpoints. Opus Genetics received Rare Pediatric Disease Designation in 2024 for OPGx-LCA5 and subsequently secured RMAT in 2025, demonstrating how layered pathways can support a rapid transition to pivotal designs in a focused indication. Engagement with regulators under these frameworks can streamline endpoint selection, study design, and CMC expectations in pediatric trials. These mechanisms collectively create a predictable route for sponsors that operate in the Leber congenital amaurosis market with constrained prevalence and small trial cohorts.

Rising Venture, Pharma, and Public Funding for Inherited Retinal Disease R&D

Funding cycles have shifted back toward gene and genetic medicine platforms in ophthalmology, and sponsors have secured fresh capital to progress rare retinal programs to proof-of-concept and registration. Ray Therapeutics won a USD 8 million state-backed grant in 2025 to advance an optogenetic program, reinforcing public support for sight-restoring interventions. Opus Genetics raised USD 23 million in late 2025 to extend runway across priority programs, including LCA5. MeiraGTx signed a multi-asset ophthalmology collaboration with Eli Lilly that brought upfront and milestone components to help scale its manufacturing and development footprint. ProQR’s collaboration progress and milestones evidenced sustained industry interest in RNA-editing approaches that can complement or substitute for AAV in select genotypes within the Leber congenital amaurosis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| $400k-plus per-eye therapy costs restricting payer uptake | -0.8% | Global with acute constraints in U.S. commercial and Medicaid plans | Short term (≤ 2 years) |

| Scarcity of accredited sub-retinal surgery centers outside U.S. and EU | -0.5% | APAC, Latin America, and MEA with limited impact in North America and EU | Medium term (2-4 years) |

| Global viral-vector fill-finish capacity bottlenecks delaying launches | -0.6% | Global supply chains with acute constraints for select serotypes | Short term (≤ 2 years) |

| Highly fragmented mutation landscape diluting ROI for long-tail gene targets | -0.9% | Global, affecting all sponsors pursuing mutation-specific approaches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

400k-Plus Per-Eye Therapy Costs Restricting Payer Uptake

The high list price for the only approved ocular gene therapy creates a demanding evidence bar and protracted prior authorization workflows for pediatric patients. Large payers require genetic confirmation and documentation of viable retinal cells before authorizing treatment, and many plans limit retreatment for previously injected eyes. Sponsors have implemented co-pay assistance and referral pathways to charitable support for eligible patients, which helps but does not eliminate administrative friction. Outcomes-based contracts tied to functional vision endpoints have been advanced to reduce payer risk, which shifts focus toward real-world durability. A federal model that centralizes outcomes-based contracting for cell and gene therapies aims to reduce state-level negotiation burden in public coverage programs, creating a precedent that could extend to inherited retinal diseases.

Scarcity Of Accredited Sub-Retinal Surgery Centers Outside the U.S. and the EU

Subretinal gene-therapy delivery requires vitreoretinal expertise and cold-chain logistics that keep product shipments within strict temperature controls through preparation. In the United States, a limited number of designated treatment centers concentrate administration and follow-up care to ensure consistency in outcomes and safety.

The United Kingdom established NHS-funded delivery capacity and has supported clinical programs for multiple LCA genotypes through academic eye hospitals. Pediatric centers of excellence coordinate dosing and follow-up for complex cases, which reinforces the role of specialized networks as more programs move to pivotal phases. Outside North America and Europe, treatment infrastructure remains limited and is only beginning to scale, which continues to constrain near-term access in the Leber congenital amaurosis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Gene Therapy Leads Despite Luxturna’s Stumble

Gene therapy captured 41.50% of the Leber congenital amaurosis market share in 2025 and is on track to grow at 4.78% annually through 2031, maintaining leadership in a category shaped by single-dose treatments and rigorous functional endpoints. The premium price point weighs on near-term uptake, but concentrated surgical networks, payer pathways, and clear eligibility criteria create a framework that supports steady adoption in qualified candidates. Evidence continues to accumulate as next-generation constructs demonstrate improvements in pediatric cohorts, including notable gains in visual function for children with AIPL1-associated disease. OPGx-LCA5 progressed under RMAT, and pivotal planning reflects growing confidence in clinically meaningful endpoints for inherited retinal diseases. Pharmacologic options remain limited to supportive care and do not materially change disease trajectory, which reinforces gene therapy’s central role in the Leber congenital amaurosis market.

The Leber congenital amaurosis market size for gene therapy is set to expand at a 4.78% CAGR through 2031 as pivotal programs mature and payer pathways evolve. Programs that deploy CRISPR-Cas9 and other editing modalities showed proof-of-concept in defined CEP290 mutations, and sponsors are advancing trial designs that link structural biomarkers with functional gains in vision. Supportive devices and prosthetics have a minor revenue role as sponsors and clinicians focus on preserving or restoring endogenous photoreceptor function in amenable genotypes. Regulatory flexibility around pediatric endpoints and iterative guidance under RMAT support well-designed trials that can read out on meaningful outcomes, which benefits the Leber congenital amaurosis market.

By Target Gene: CEP290 Leads on Prevalence, While Niche Targets Advance Through Designations

CEP290 accounted for 25.81% of total revenues in 2025 and is forecast to grow at a 4.66% rate through 2031 as clinical programs translate early efficacy into larger studies. In the BRILLIANCE study [2]NEI Clinical Team, “BRILLIANCE Trial Update for CEP290 Editing,” National Eye Institute, nei.nih.gov, a majority of dosed participants with defined intronic CEP290 mutations experienced improvement in at least one efficacy endpoint, reinforcing the therapeutic rationale for gene editing. RPE65 remains a smaller prevalence genotype that anchors an approved augmentation precedent and informs center-level logistics for administration and follow-up. MeiraGTx reported significant visual acuity gains with AAV-AIPL1 in LCA4, positioning that program for U.K. regulatory consideration and setting a clinical benchmark for pediatric outcomes. The Leber congenital amaurosis market continues to be segmented by genotype as sponsors align modality choices with packaging limits, transduction profiles, and surgical delivery considerations.

The Leber congenital amaurosis market size for CEP290 is projected to expand at a 4.66% CAGR through 2031 as sponsors prioritize editing or augmentation strategies aligned to intronic variants. Programs that target GUCY2D and AIPL1 add breadth to the pipeline and support a diversified set of pivotal candidates that can sustain category growth even when individual cohorts are small. The evolving mix of augmentation and editing aligns with CMC and delivery trade-offs that are especially salient in pediatric eyes, where surgical precision and dose control are critical. As more programs approach registration milestones, sponsors will need to harmonize biomarker strategies and endpoint readouts that resonate with regulators, clinicians, and payers operating in the Leber congenital amaurosis market.

By End User: Research Centers Accelerate as Trials Pivot to Efficacy

Specialized eye clinics held 38.67% in 2025 due to their role as designated treatment hubs that coordinate subretinal injections, perioperative management, and follow-up testing. Pediatric and academic centers such as those in the U.S. serve as both treatment sites and trial hubs that conduct mobility testing, stimulus thresholds, and ocular imaging for longitudinal assessment. The vertical integration of clinical care and research enables efficient identification of eligible patients, streamlined consent, and higher data quality across endpoints that regulators weigh in pediatric blindness. Designated centers reduce geographic variability in care standards, which protects trial integrity and operational consistency in the Leber congenital amaurosis market.

Ophthalmology research centers are set to record the fastest growth at 4.98% through 2031 as multi-center pivotal trials recruit across pediatric cohorts and integrate advanced imaging along with functional measures. Academic partnerships in the U.K. and U.S. illustrate how child-focused hospitals coordinate complex gene-therapy administration with post-dose testing and safety surveillance. This operational model supports faster transition from early safety to pivotal efficacy, creating a favorable backdrop for sponsors active in the Leber congenital amaurosis industry. Hospitals outside these networks focus more on supportive care and referral pathways, which anchors their smaller revenue role next to clinics and research institutes in the Leber congenital amaurosis market.

Geography Analysis

North America retained 45.18% in 2025 on the strength of designated treatment networks, high genetic testing penetration, and mature clinical infrastructure for pediatric gene therapy. The limited set of U.S. centers streamlines administration and consolidates experience in dosing and follow-up, which contributes to safety and data consistency. Prior authorization requirements commonly request genetic confirmation and evidence of viable retinal cells, which adds time and administrative steps before dosing. A federal model for outcomes-based contracting seeks to reduce the burden on state programs, which could provide a template for broader access over time. Sponsors engaged in regulatory dialogue for pivotal progression during 2025, signaling continued momentum toward larger confirmatory studies in the Leber congenital amaurosis market.

Europe is the second pillar with established centers that deliver both commercial and investigational therapies for inherited retinal diseases. U.K. pediatric eye hospitals have treated children with AAV-based constructs and continue to collaborate across clinical and academic partners to advance programs toward review. A peer-reviewed report[3]GOSH Clinical Team, “Pediatric Gene Therapy Program Updates,” Great Ormond Street Hospital documented significant visual function gains in LCA4 children who received an AAV-mediated AIPL1 construct, highlighting the potential for meaningful pediatric benefit. A large German cohort showed that the diagnostic yield reached 54.3% in the most recent decade, which underscores the synergy between broader panels and improved phenotyping. European reference networks and professional societies coordinate shared care pathways and virtual clinics that support consistent standards across member countries in the Leber congenital amaurosis market.

Asia-Pacific is expected to grow at 4.67% through 2031 with government-backed manufacturing capacity and expanding newborn screening programs that raise early identification. The Leber congenital amaurosis market size in Asia-Pacific is forecast to expand at a 4.67% CAGR as facilities in Australia provide GMP-grade vector production that supports clinical and commercial supply for regional and international sponsors. Australia funded national newborn screening enhancements that broaden the scope of early detection and lay the groundwork for timely referral in inherited disorders. As designated treatment infrastructure outside Western hubs continues to scale, APAC’s influence on clinical development and supply logistics is poised to rise within the Leber congenital amaurosis market.

Competitive Landscape

The Leber congenital amaurosis market features moderate to high competition intensity with multiple sponsors pursuing overlapping targets through augmentation, editing, and RNA-modulation strategies. The absence of a single dominant therapy keeps pipeline programs in focus and elevates the importance of trial design, surgical standardization, and functional endpoints that translate into payer-relevant evidence. Pediatric outcomes showing clinically meaningful gains in small cohorts strengthen the case for next-generation constructs and continue to attract partnerships and investments. Regulatory progress under RMAT and other designations sustains sponsor momentum and reinforces the case for continued capital deployment into the Leber congenital amaurosis market.

Strategic partnerships are a central feature of sponsor strategies as platforms expand and sponsors seek to diversify modality options. A major ophthalmology genetic medicines collaboration between MeiraGTx and Eli Lilly combined rights to an LCA4 program with access to intravitreal capsids and bespoke promoters to accelerate development and manufacturing scale-up. Editas Medicine pivoted its resource allocation toward in vivo cardiometabolic and hematology programs while CEP290 editing remains a touchstone for feasibility in ocular gene editing. ProQR’s RNA-editing platform advanced through early clinical milestones and remains a credible non-viral alternative for genotypes that present vector packaging or durability challenges in the Leber congenital amaurosis market.

Technology differentiation centers on modality selection, serotype and capsid engineering, and regulatory strategy that prioritizes pediatric endpoints and durability evidence. Sponsors with vertical integration across vector manufacturing and plasmid supply can compress timelines and reduce third-party risk, which is relevant as more programs enter pivotal phases. CRISPR-based editing and optogenetic concepts provide complementary avenues to gene augmentation, and near-term readouts will shape investment priorities across genotypes in the Leber congenital amaurosis industry.

Leber Congenital Amaurosis Industry Leaders

Spark Therapeutics

GenSight Biologics

MeiraGTx

Atsena Therapeutics

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Eli Lilly and MeiraGTx entered a strategic collaboration and license agreement for ophthalmology genetic medicines, including exclusive rights to AAV-AIPL1 for LCA4 and access to intravitreal capsids and bespoke promoters.

- November 2025: Opus Genetics announced a successful Type B RMAT meeting with the FDA for OPGx-LCA5 and enrolled the first participant in the run-in period for a planned adaptive Phase 3 trial.

- October 2025: Australia’s Viral Vector Manufacturing Facility officially opened in Sydney’s Westmead Health and Innovation District with NSW Government investment supporting clinical and commercial GMP production.

- September 2025: Editas Medicine nominated EDIT-401 as its lead in vivo candidate for hyperlipidemia with an IND planned by mid-2026.

Global Leber Congenital Amaurosis Market Report Scope

| Gene Therapy |

| Pharmacological Therapy |

| Retinal Prosthesis |

| Assistive Devices |

| Other Supportive Treatments |

| RPE65 |

| CEP290 |

| GUCY2D |

| AIPL1 |

| CRB1 |

| RPGRIP1 |

| Others |

| Hospitals |

| Specialized Eye Clinics |

| Ophthalmology Research Centers |

| Home Care Settings |

| Others |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Gene Therapy | |

| Pharmacological Therapy | ||

| Retinal Prosthesis | ||

| Assistive Devices | ||

| Other Supportive Treatments | ||

| By Target Gene | RPE65 | |

| CEP290 | ||

| GUCY2D | ||

| AIPL1 | ||

| CRB1 | ||

| RPGRIP1 | ||

| Others | ||

| By End User | Hospitals | |

| Specialized Eye Clinics | ||

| Ophthalmology Research Centers | ||

| Home Care Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Leber congenital amaurosis market and how fast is it growing?

The Leber congenital amaurosis market size stands at USD 1.31 billion in 2026 and is forecast to reach USD 1.67 billion by 2031 at a 4.25% CAGR.

Which treatment type leads today and what is the growth outlook to 2031?

Gene therapy leads with 41.50% share in 2025 and is projected to grow at 4.78% annually through 2031 as pivotal programs mature and payer pathways evolve.

Which target gene segment is largest within the Leber congenital amaurosis market?

CEP290 is the largest target gene segment with 25.81% share in 2025 and a 4.66% growth rate through 2031 supported by clinical progress in editing programs.

Which region is largest and which is growing fastest in this space?

North America is largest with 45.18% share in 2025 while Asia-Pacific is the fastest growing at 4.67% through 2031 supported by manufacturing scale-up and screening expansion.

What are the main barriers to faster adoption in this market?

High per-eye prices, prior authorization requirements, limited designated surgical centers outside Western hubs, and manufacturing capacity constraints at fill-finish remain the main barriers.

How do regulatory designations affect timelines for programs in this field?

RMAT and related designations provide iterative guidance and enable streamlined pivotal designs once early efficacy is evident, which can reduce development timelines for well-designed pediatric programs.

Page last updated on: