Lativa Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

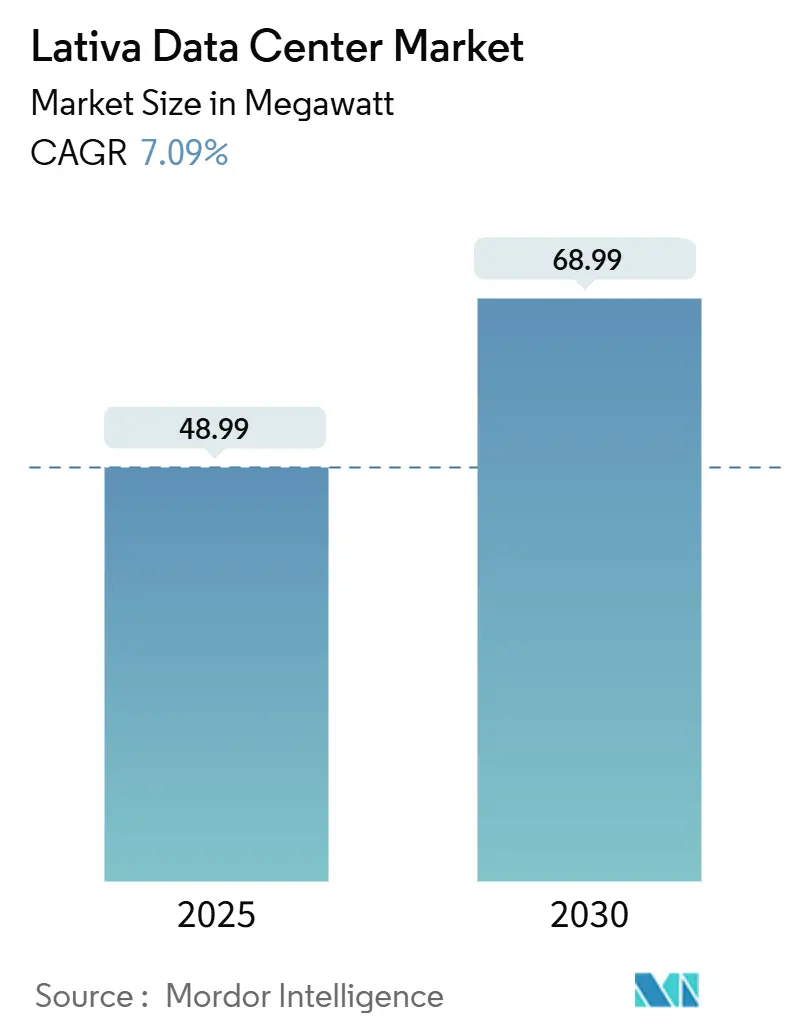

| Market Volume (2025) | 48.99 megawatt |

| Market Volume (2030) | 68.99 megawatt |

| Growth Rate (2025 - 2030) | 7.09% CAGR |

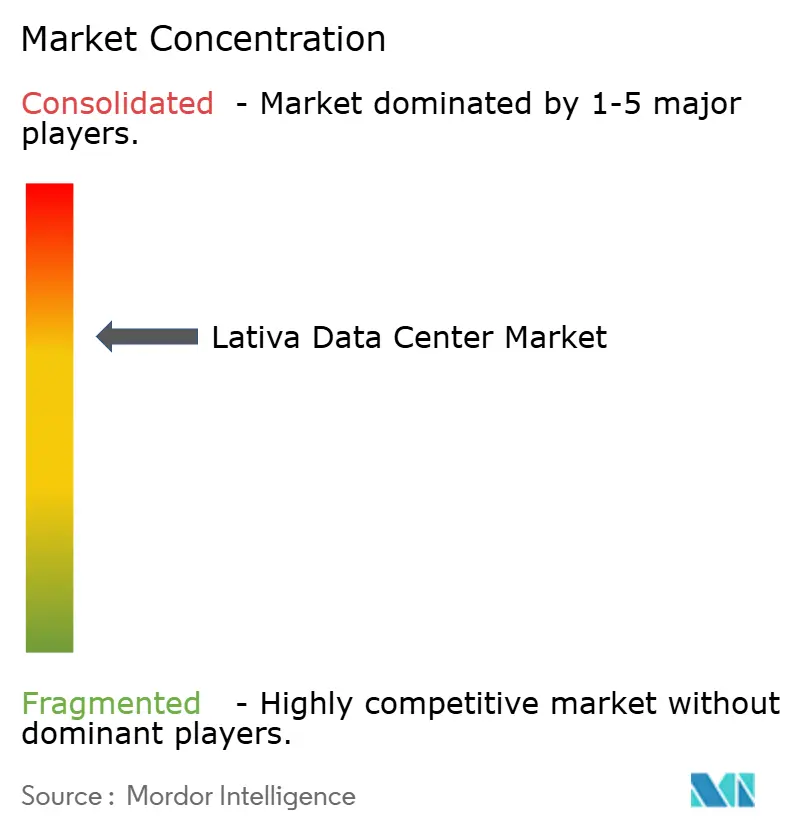

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lativa Data Center Market Analysis by Mordor Intelligence

The Latvia data center market size stood at 48.99 MW in 2025 and is forecast to reach 68.99 MW by 2030, translating into a 7.09% CAGR through the outlook period. Rapid cloud adoption, ever-stricter cybersecurity rules, and low-latency fiber corridors linking the Nordics with Central-Eastern Europe are the major demand catalysts. International investors are expanding facility footprints to capture regional overflow from congested Western hubs, while national grid modernization lowers power-supply risk. Submarine and terrestrial fiber builds have strengthened resiliency, positioning Riga as a preferred colocation gateway. Meanwhile, tax perks for data-center real-estate investment trusts (REITs) and a fast-growing renewable energy mix improve cost competitiveness and sustainability credentials.

Key Report Takeaways

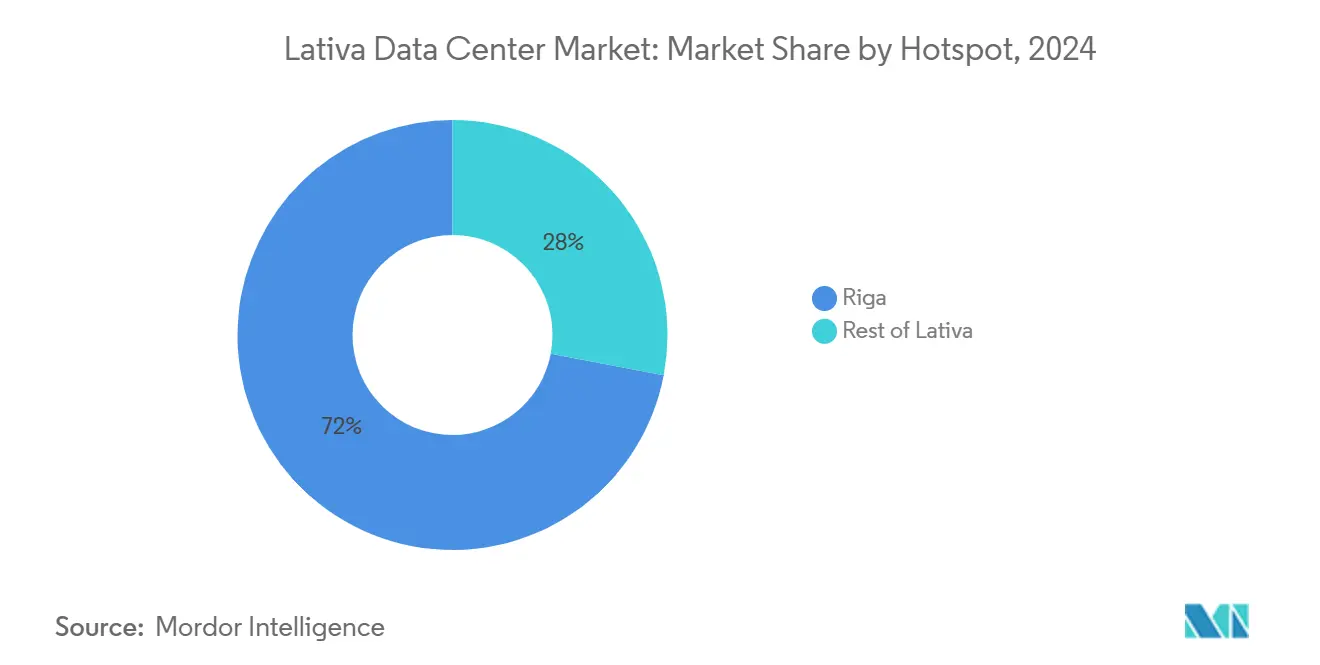

- By hotspot, Riga led with 72% of Latvia data center market share in 2024, whereas Other Urban Areas are projected to post the fastest 7.09% CAGR to 2030.

- By data-center size, medium facilities accounted for 40% of the Latvia data center market size in 2024, while mega facilities are expected to expand at an 8.38% CAGR through 2030.

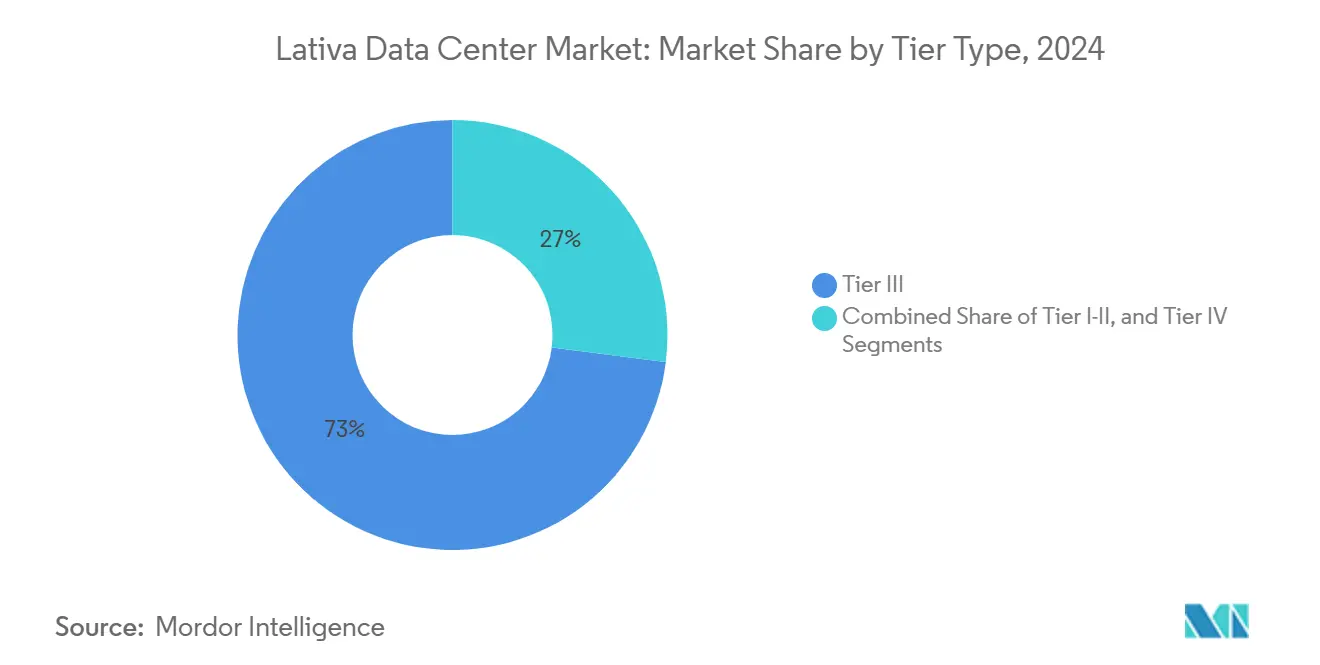

- By tier type, Tier III sites held 73% share of the Latvia data center market size in 2024 and Tier IV sites are on track for an 8.6% CAGR during 2025–2030.

- By absorption, utilized capacity reached 77% of the Latvia data center market size in 2024, with hyperscale colocation forecast to register an 8.5% CAGR by 2030.

Lativa Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cloud and edge-computing adoption surge | +1.1% | Riga and Other Urban Areas | Medium term (2-4 years) |

| Submarine cable expansions to Baltics | +0.8% | National; primary benefits to Riga connectivity hub | Long term (≥4 years) |

| Government digitalisation push | +1.2% | National; early adoption in public sector facilities | Short term (≤2 years) |

| Renewable-powered, low-cost energy mix | +0.9% | National; grid-modernization focus | Medium term (2-4 years) |

| Riga as low-latency Nordics–CEE bridge | +0.7% | Regional | Long term (≥4 years) |

| Tax incentives for data-center REITs (2025) | +0.6% | National; SEZ benefits | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Government Digitalization Push

Latvia’s Recovery and Resilience Plan earmarks EUR 1.97 billion (USD 2.29 billion), of which 23% of the funds will be allocated to digital transition projects that consolidate fragmented public IT estates into a central federal cloud.[1]Latvia’s Recovery and Resilience Plan earmarks EUR 1.97 billion, of which 23% funds digital transition project. Immediate colocation demand arises as ministries migrate workloads that must comply with the National Cybersecurity Law adopted in June 2024. The Ministry of Smart Administration is executing the EU AI Act domestically, mandating Tier III and Tier IV infrastructure for high-risk AI workloads.

Cloud and Edge-Computing Adoption Surge

Tet Cloud revenues advanced 35% year-on-year in 2025, reflecting enterprise preference for domestic data sovereignty and low-latency edge processing.[2]Tet Cloud revenues advanced 35% year-on-year in 2025 The Baltic Highway now delivers sub-35 ms round-trip latency between Tallinn and Frankfurt via Riga, a decisive factor for fintech and gaming workloads. Microsoft’s planned National AI Hub reinforces hyperscale interest, likely stimulating new build-to-suit capacity.

Submarine Cable Expansions to Baltics

Repeated cuts to the Latvia–Sweden subsea cable in 2025 highlighted single-route vulnerability, prompting state operator LVRTC to fast-track redundant landing projects.[3]Repeated cuts to the Latvia–Sweden subsea cable in 2025. GlobalConnect’s Sweden-Finland terrestrial super-route grants Latvia alternative 3 Pbit/s backbone access, boosting network diversity for regional colocation clients.

Renewable-Powered, Low-Cost Energy Mix

After disconnecting from the Russian grid in February 2025, Latvia invested EUR 1.6 billion (USD 1.86 billion) to join the EU synchronous system, thereby stabilizing the frequency and reducing geopolitical risk. Solar output tripled year-over-year in May 2024 to surpass 60 GWh, underscoring the value of green-power purchase agreements for data-center operators. TSO Augstsprieguma tīkls plans EUR 444.85 million (USD 516.14 million) in new transmission projects through 2034, enabling higher rack-power densities.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited domestic demand scale | −0.4% | National; smaller urban markets | Long term (≥4 years) |

| Engineering skills shortage | −0.3% | National; specialized data-center roles | Medium term (2-4 years) |

| Riga-East grid congestion | −0.5% | Eastern Riga industrial zones | Short term (≤2 years) |

| Cyber-insurance premium spikes | −0.2% | Global; intensified by regional geopolitics | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Engineering Skills Shortage

Latvia lists shortages in 367 of 436 tracked occupations, including electrical and HVAC technicians vital for data-center builds. From January 2025, stricter foreign-labor rules oblige firms to re-advertise vacancies locally, stretching project timelines.

Limited Domestic Demand Scale

With only 1.9 million residents, local workloads cannot alone support hyperscale economics; operators must instead court Nordic and CEE tenants, routing traffic through Latvia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hotspot: Riga anchors national capacity yet growth shifts beyond the capital

Riga accounted for 72% of Latvia data center market size in 2024 on the strength of its dense carrier hotels and the Port of Riga’s 5G-enabled logistics zones. Heavy public-cloud and government workloads sustain absorption rates close to 80%, encouraging brownfield expansions. Emerging fiber corridors and government regional development grants are steering new builds toward Valmiera and Liepāja, giving Other Urban Areas the fastest 7.09% CAGR outlook to 2030. The wider Latvia data center market benefits from this geographic spread, lowering single-city risk and shortening last-mile latency to end-users nationwide.

Riga’s innovation clusters, including a EUR 450,000 (USD 522,112.50) municipal start-up center and Roche’s 200-person shared-services campus, generate strong demand for enterprises and pilot AI workloads. Sub-40 ms round-trip times to Stockholm and Warsaw enable real-time analytics for maritime, gaming, and fintech actors. Municipal zoning reforms that pre-approve sites for mission-critical infrastructure further reduce lead times, preserving Riga’s dominance even as secondary cities gain traction.

By Data-Center Size: Mega facilities signal hyperscale arrival

Medium sites still hold 40% of Latvia data center market share thanks to legacy colocation footprints serving domestic SMEs and agencies. Yet mega facilities are expected to deliver an 8.38% CAGR, indicating Latvia’s graduation to hyperscale hosting. Delska’s 20 MW renewable-powered campus exemplifies low-PUE, high-density design that appeals to global cloud tenants. Foreign capital infusions, such as Quaero Capital’s acquisition of DEAC, shorten funding cycles, and REIT tax breaks lower the cost of equity. The Latvia data center industry is therefore pivoting toward large contiguous halls capable of phased 40 MW build-outs, aligning with multi-availability-zone cloud architectures.

Small edge sites remain relevant for latency-sensitive IoT and 5G workloads along transport corridors, while large enterprise-class facilities cater to single-tenant financial and healthcare applications. However, price-per-kW compression from mega-scale economics forces sub-10 MW sites to pursue specialization in high-margin managed services to defend yields.

By Tier Type: Reliability spending climbs

Tier III infrastructure represented 73% of Latvia data center market size in 2024, reflecting the preferred cost-resilience trade-off for cloud and SaaS customers. Growing AI and fintech activity raises the bar. Tier IV capacity is forecast to leap 8.6% annually as operators chase 99.995% availability SLAs. The National Cybersecurity Law compels approximately 2,000 vital-service providers to migrate to certified facilities, influencing procurement decisions toward Tier III+ and Tier IV designs.

Capital discipline is critical; the delta in build cost between Tier III and Tier IV exceeds 20%, making anchor-tenant commitments essential before groundbreaking. Nonetheless, strengthened grid stability and growing renewable capacity mitigate OPEX fears once associated with Tier IV power redundancy, enlarging its addressable market.

By Absorption: Utilization rates underscore disciplined capacity management

Utilized racks captured 77% of installed power in 2024, evidencing prudent build-to-demand strategies that safeguard returns even at modest domestic scale. Hyperscale colocation within this utilized portion will post an 8.5% CAGR as Western European clouds offload overflow to Riga. Non-utilized reserves grant operators agility to execute rapid containerized data-hall expansions when win-rates with multinational tenants spike.

Retail colocation retains sticky revenue through cross-connect and managed-service upselling, offsetting wholesale’s thinner margins. Cryptocurrency-hosting demand could lift overnight if Latvia’s crypto-tax reforms attract mining and exchange operators; however, power-price spikes would hinder this niche, explaining the sector’s modest share inside the Latvia data center market.

Geography Analysis

Latvia straddles critical North-South and East-West digital corridors. The Baltic Highway fibre link, inaugurated in January 2025, spans 3,000 km between Tallinn and Frankfurt, via Riga, offering a throughput of 9.6 Tb/s and a latency of 35 ms. This asset anchors the Latvia data center market as a redundancy node for Nordic hyperscalers weary of Amsterdam’s moratorium and Frankfurt’s saturated grid.

Energy security improved markedly once Latvia left the Russian synchronous zone in February 2025; EUR 1.6 billion (USD 1.86 billion) invested in frequency-control and reserve capacity upgrades now underpins grid reliability for high-density halls. Solar generation exceeded 60 GWh in May 2024, tripling year-over-year and enabling data center PPAs that satisfy ESG mandates. The average spot prices of EUR 117.16/MWh (USD 135.93) in January 2024 place Latvia below many of its Western peers, thereby sustaining its cost edge.

Nonetheless, submarine-cable vulnerabilities surfaced after repeat cuts to the Latvia–Gotland cable in early 2025, reinforcing the business case for multi-path routing inside every Latvia data center market SLA. The new Sweden–Finland land-route lifts effective redundancy, but operators must still diversify paths through Lithuania and Poland to achieve five-nines network uptime.

Competitive Landscape

Latvia’s colocation sector exhibits moderate concentration, with the top five operators jointly supplying around 60% of the installed MW in 2024. DEAC, now backed by Quaero Capital, and Tet, majority-owned by the state, dominate brownfield capacity, while LVRTC leverages sovereign rights-of-way to cross-subsidize new halls with tower income. Delska differentiates via 100% renewable sourcing and sub-1.3 PUE engineering, targeting sustainability-minded hyperscalers.

Strategic moves highlight three themes. First, cross-border connectivity, DEAC’s Delska campus interconnects directly with Tallinn and Vilnius internet exchanges to lure regional OTTs. Second, vertical specialization. Tet markets sovereign-cloud partitions featuring domestic jurisdiction, appealing to regulated BFSI players. Third, capital scale-up, Telia Company’s plan to exit its Latvian assets may trigger a bidding war that reconfigures fiber backhaul ownership and data-center peering economics.

Prospective entrants, such as Vantage Data Centers, armed with a EUR 1.4 billion (USD 1.62 billion) EMEA war chest, and Meta’s scouted AI excellence center, could compress rack-rate pricing while simultaneously accelerating ecosystem maturity. For incumbents, moving up the value stack into managed security and AI-ready GPU clusters mitigates commoditization risk in the Latvia data center market.

Lativa Data Center Industry Leaders

Delska (DEAC)

Telia Company (Tet SIA)

Tet

Latvia State Radio and Television Centre

SIA VERSIJA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Telia Company announced plans to dispose of Latvian operations, opening MandA opportunities in backhaul and edge facilities.

- February 2025: Vantage Data Centers committed EUR 1.4 billion (USD 1.62 billion) to its EMEA platform, signaling capital depth that could funnel toward Riga expansions.

- February 2025: Baltic states disconnected from the Russian grid and joined the EU synchronous system, improving power-supply resilience.

- January 2025: Baltic Highway 3,000 km fiber-optic route went live, cutting Estonia–Germany latency to 35 ms.

Lativa Data Center Market Report Scope

| Riga |

| Rest of Latvia |

| Small |

| Medium |

| Large |

| Mega |

| Tier I-II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| By Hotspot | Riga | ||

| Rest of Latvia | |||

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| By Tier Type | Tier I-II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

Key Questions Answered in the Report

How fast will power demand for Latvian facilities grow through 2030?

Installed IT load is forecast to rise from 48.99 MW in 2025 to 68.99 MW by 2030, a 7.09% CAGR.

Which city provides most rack capacity?

Riga hosts 72% of national installed power, benefiting from carrier density and government workloads.

What reliability tier is gaining momentum?

Tier IV sites show the highest growth at an 8.6% CAGR, spurred by fintech and AI compliance needs.

How competitive are electricity prices versus Western Europe?

January 2024 averages of EUR 117.16/MWh remain lower than many Western hubs, underpinning cost advantage.

Which foreign investors recently entered the ecosystem?

Quaero Capital acquired DEAC and Vantage Data Centers earmarked EUR 1.4 billion for EMEA expansion that could include Riga.

What role do tax incentives play?

Special Economic Zone reforms grant five-year property-tax holidays and accelerated depreciation for data-center REITs, improving project IRRs

Page last updated on: